Economics Assignment: Cost Analysis and Market Equilibrium Concepts

VerifiedAdded on 2022/10/01

|13

|1762

|306

Homework Assignment

AI Summary

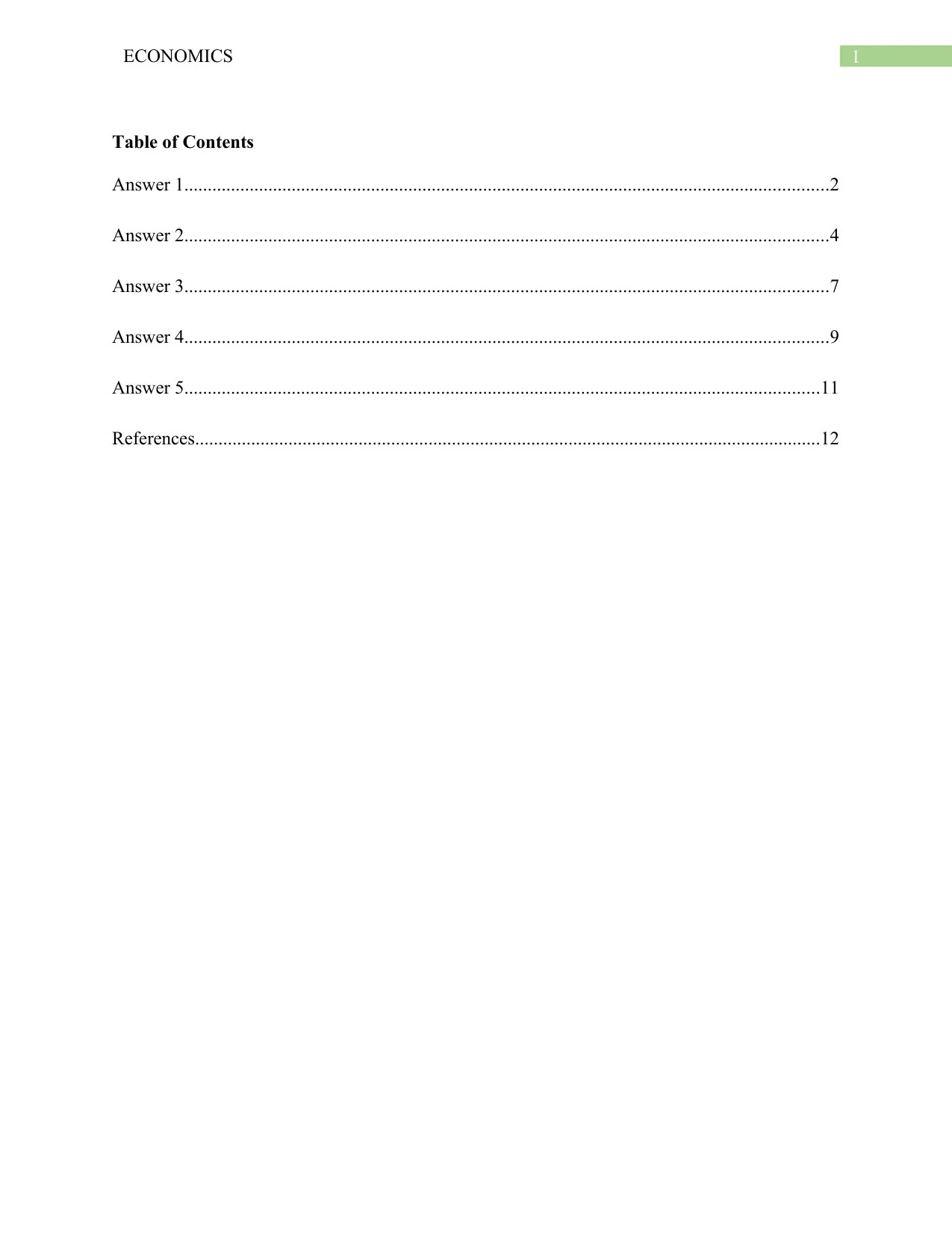

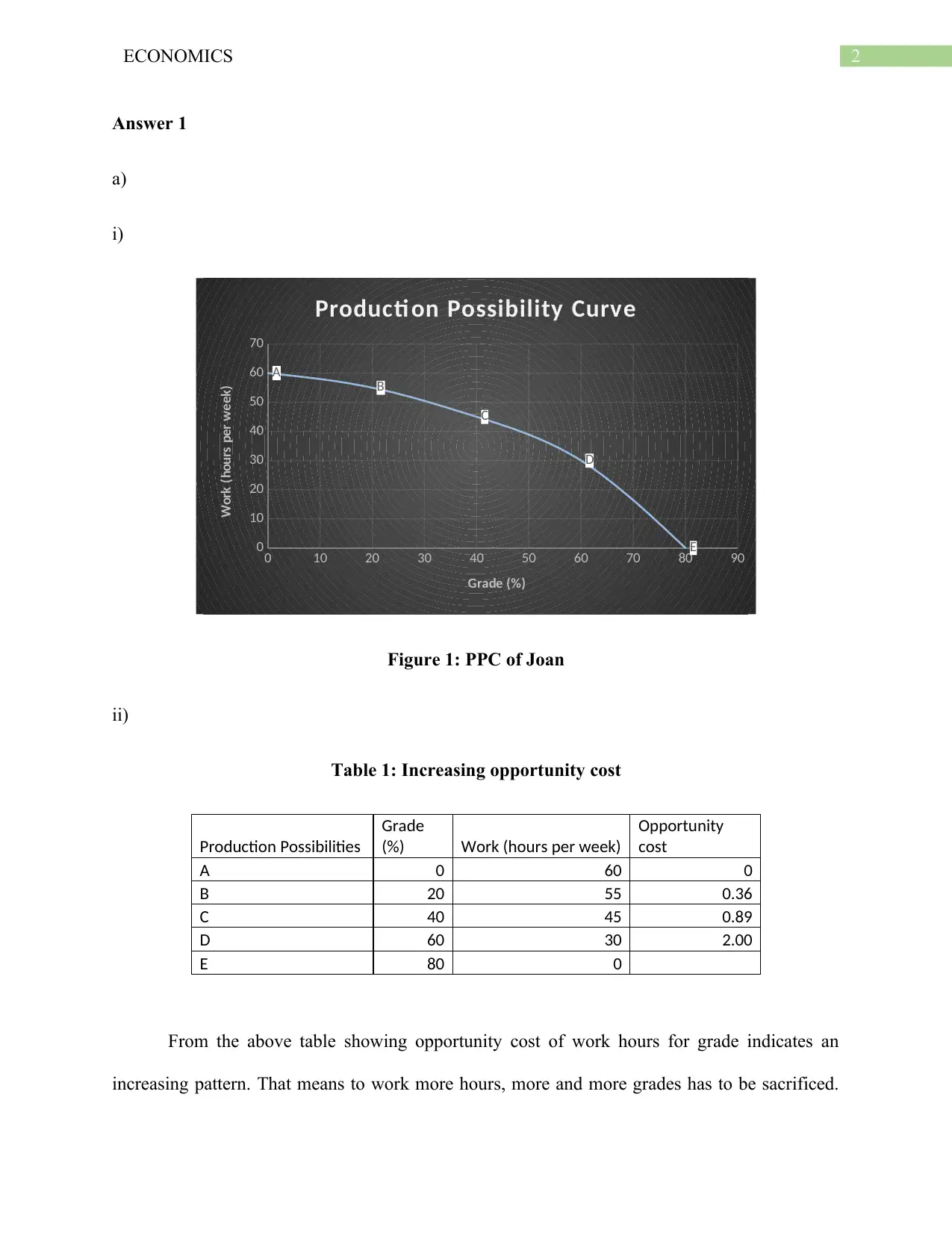

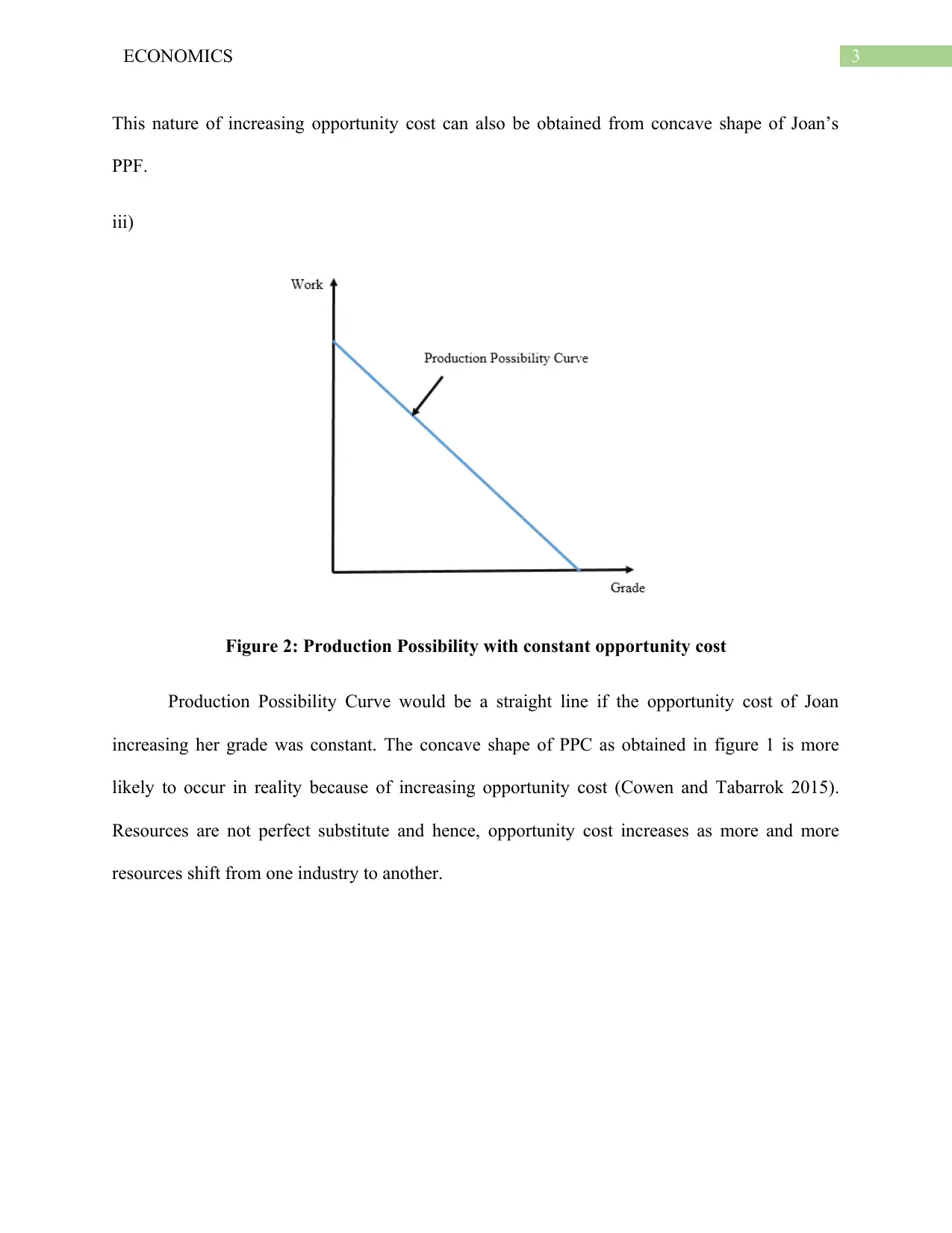

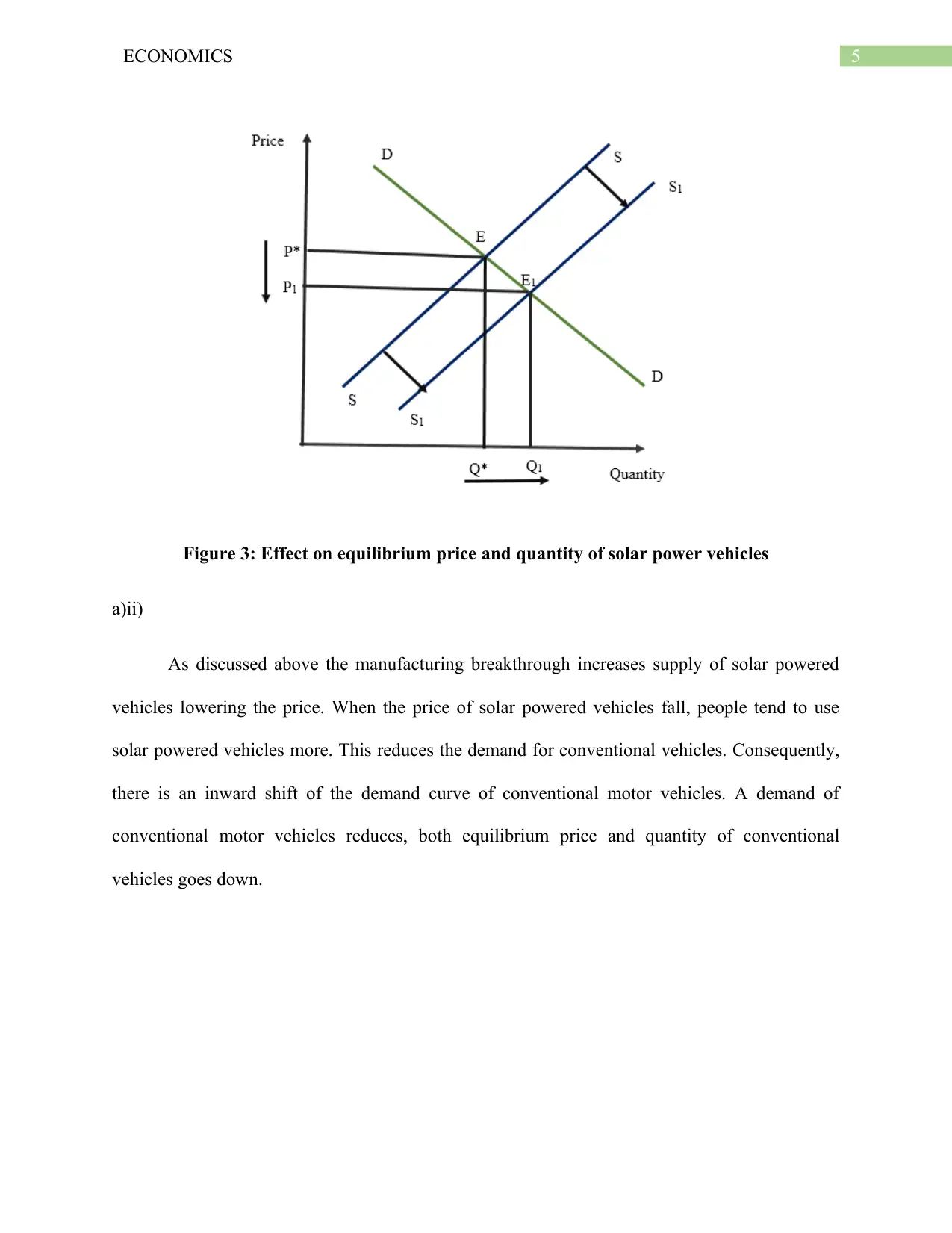

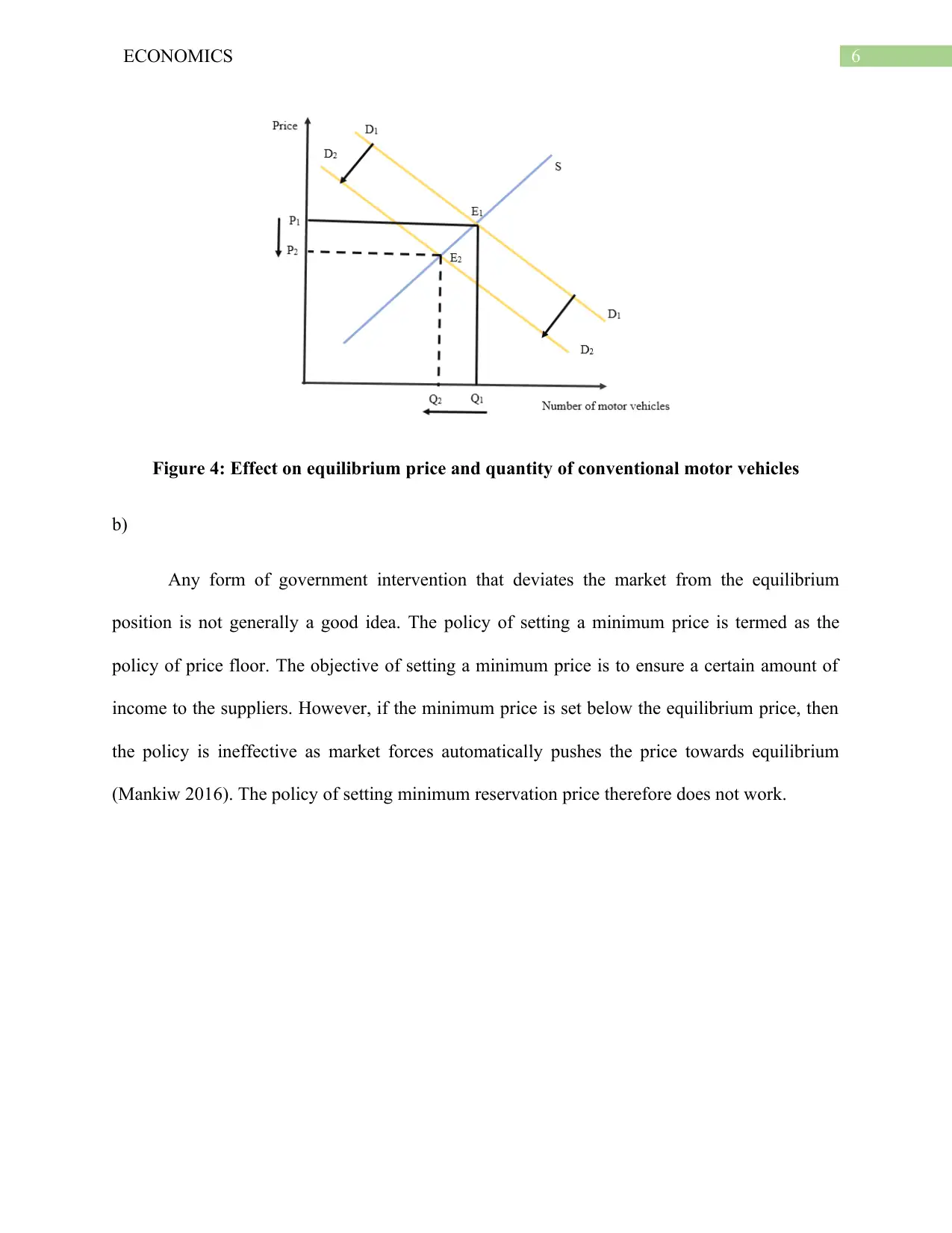

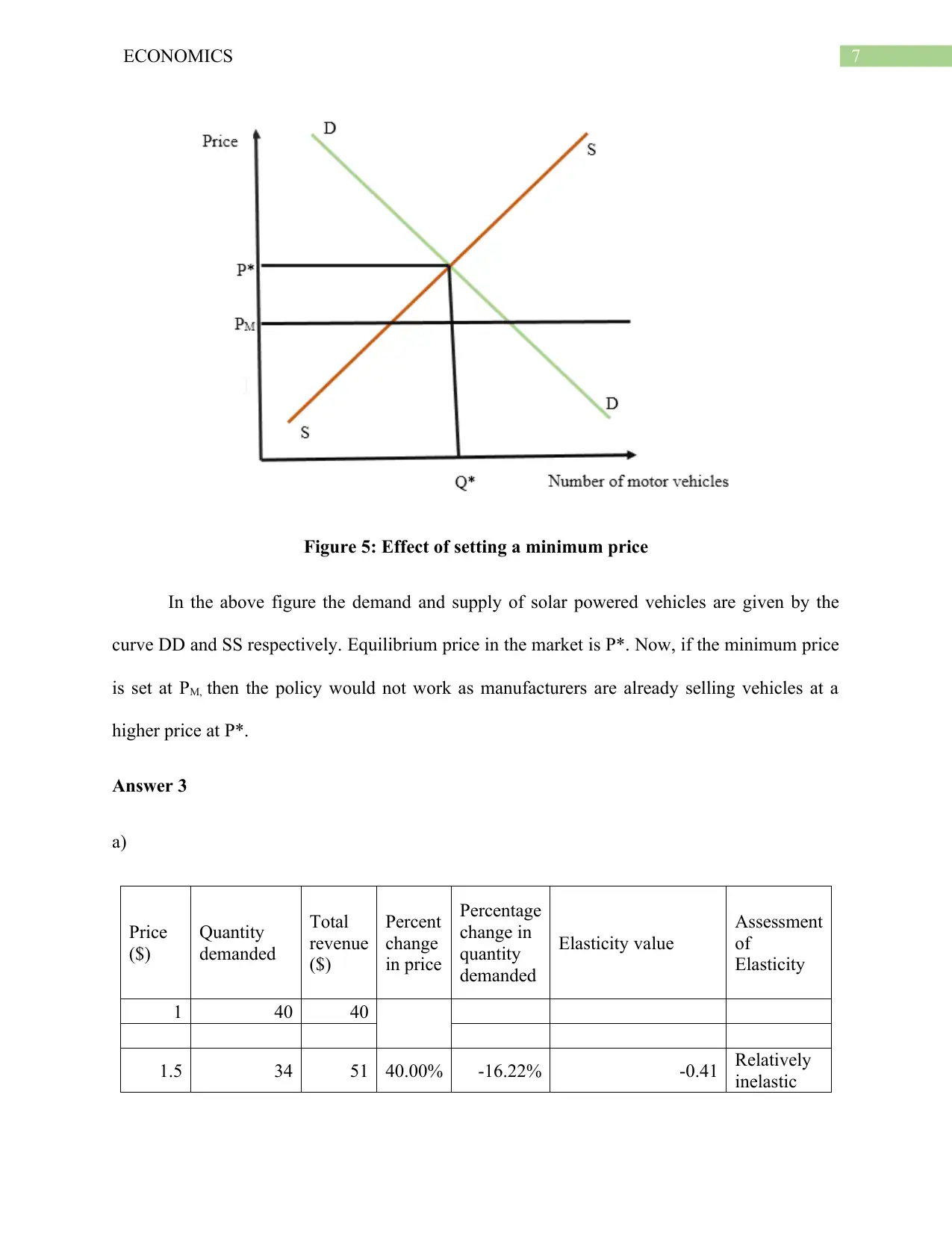

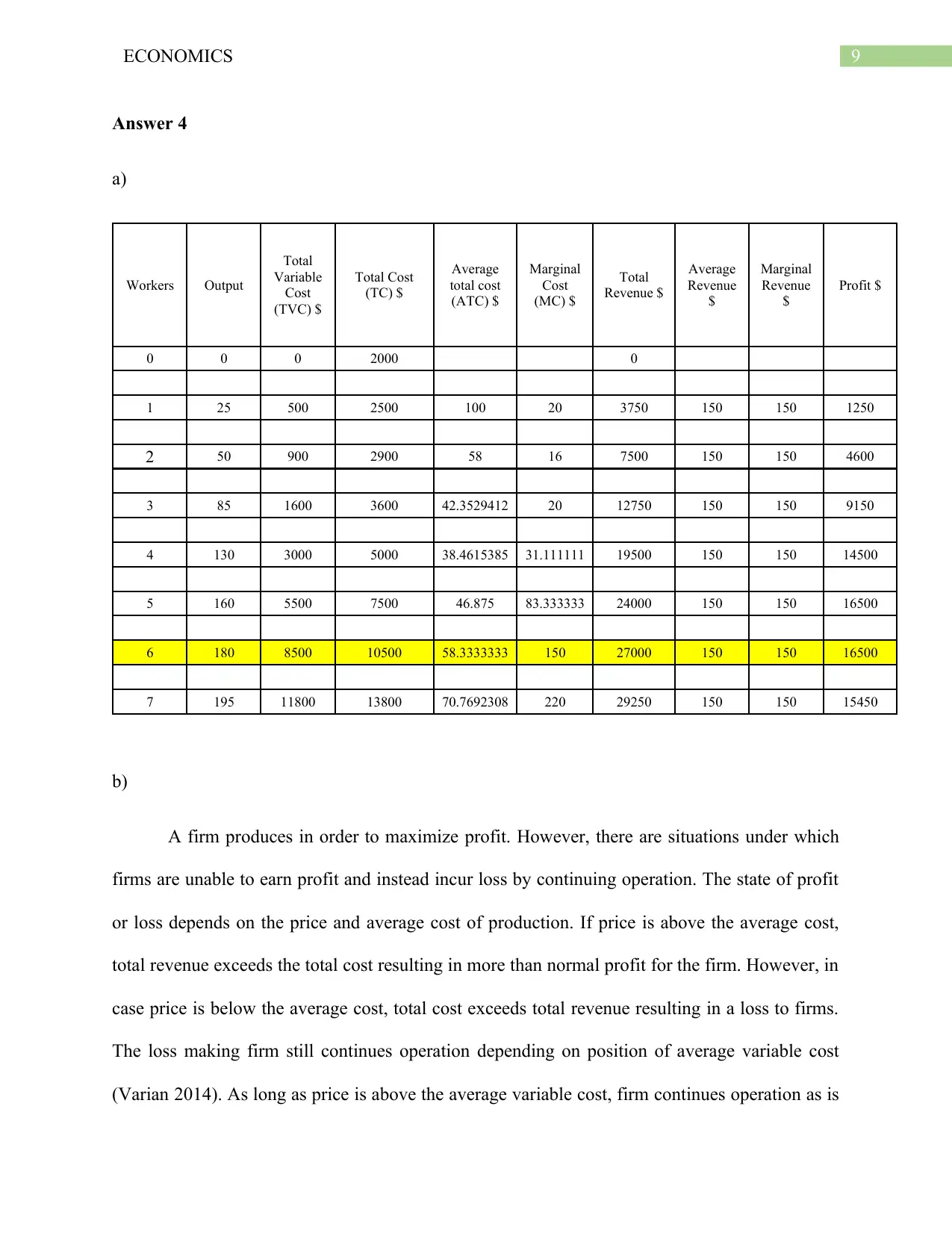

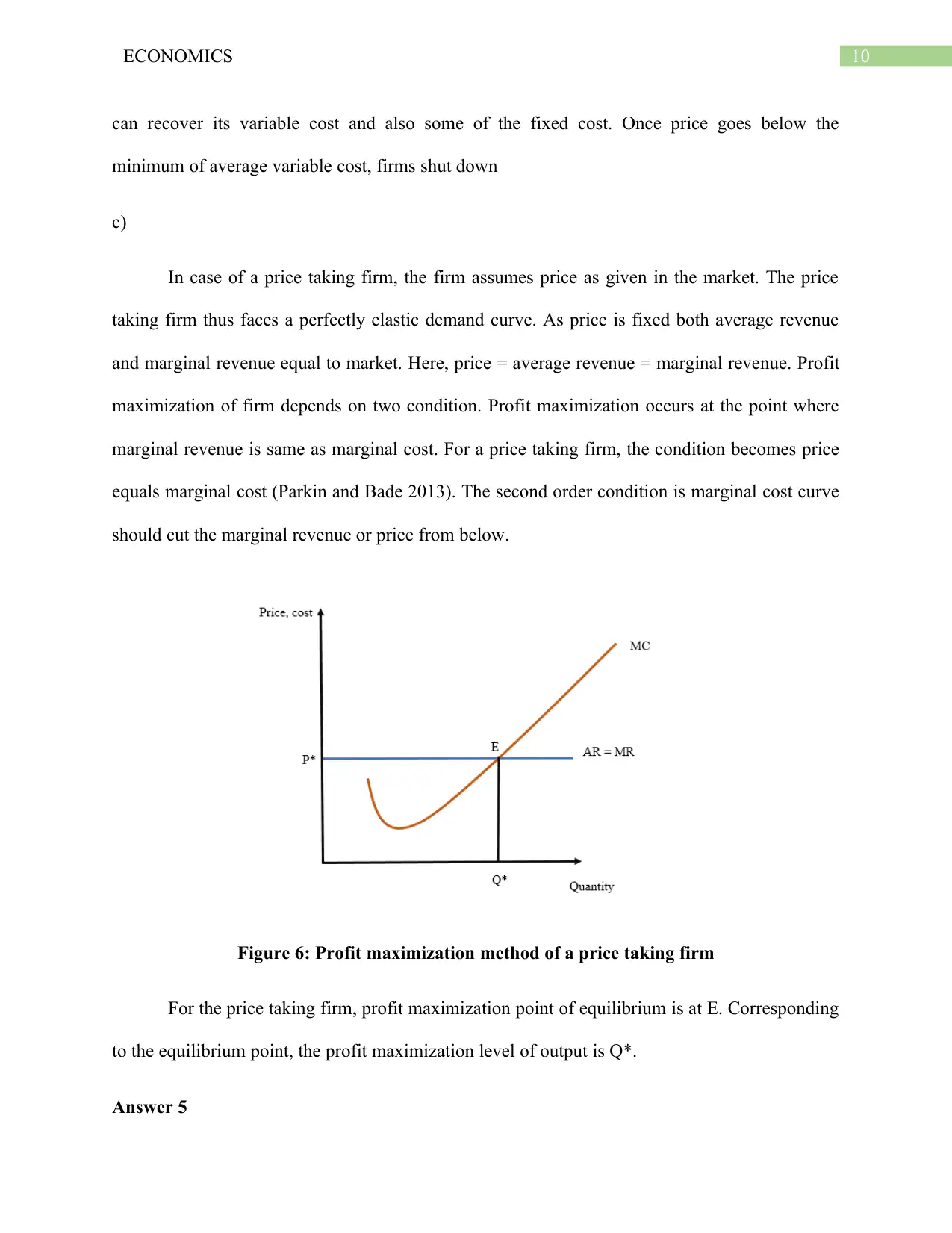

This economics assignment solution covers fundamental concepts including production possibilities, opportunity cost, market equilibrium, and cost analysis. It addresses the concept of increasing opportunity cost using production possibility curves and tables, illustrating resource allocation and efficiency. The solution also explores the impact of technological breakthroughs on market equilibrium, analyzing shifts in supply and demand curves for solar-powered and conventional vehicles. Furthermore, it discusses the ineffectiveness of minimum price policies when set below the equilibrium price. The assignment delves into price elasticity of demand, explaining its variation across seasons and for habit-forming goods. Cost analysis is performed by calculating total variable cost, total cost, average total cost, and marginal cost to determine profit-maximizing output levels for firms. Finally, the solution examines market structures, using the Australian banking industry as an example of a concentrated market dominated by a few major players, which can lead to disadvantages for consumers. Desklib provides access to similar solved assignments and resources for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.