Analysis of Market Structures: Economics for Managers Report

VerifiedAdded on 2020/03/04

|15

|3702

|45

Report

AI Summary

This report provides an analysis of various market structures, including monopoly, oligopoly, monopolistic competition, and perfect competition, outlining their key characteristics and differences. It explores the concepts of short-run and long-run profits and losses within each market structure, explaining the factors that influence profitability. The report further examines resource allocation in these markets, comparing the efficiency and fairness of each structure. Additionally, it discusses negative externalities, their impact on society, and includes a case study on the transport sector in America, highlighting environmental concerns and potential solutions. The report also includes diagrams illustrating key concepts and market dynamics, offering a comprehensive overview of market structures and their implications.

ECONOMICS FOR MANAGERS 1

Economics for managers

Name of institution

Name of student

Name of instructor

Date

Economics for managers

Name of institution

Name of student

Name of instructor

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS FOR MANAGERS 2

Features of market structures

There are different markets within an economy. The markets exist due to the types of

competition in that market. Each market has different characteristics making it unique

compared to others. Economic planners have a duty of creating policies that control the

existence of the markets without exploiting consumers. (Arnold, 2015)

Monopoly market

This is a structure made up of one supplier of a commodity and a large number of

customers in the market (Behravesh, 2014). The size of a monopoly does not matter in the

definition because small suppliers can also be monopolies. This indicates that a monopoly is

the only supplier of a certain commodity in the market. Most monopolies charge high prices

for their products due to lack of competition. Monopolies result from private access of raw

materials. This ownership enables firms to become the sole producer of a product. The entry

conditions into a monopoly include such as the ownership of private raw material access

which other firms do not have.additionally,the ability to pay the high market entrance costs

enable suppliers to enter a monopoly market (Burda, July 25, 2017).

Oligopoly

This is a market system, which only a few number of firms control the market (Flynn,

2011). There is similarity to a monopoly only that in oligopoly, it is more than one supplier in

the market. There is no set limit to the maximum number of supplier in an oligopoly.

However, the number is low to ensure that the actions of one firm influence the actions of the

other firms. Oligopolies ability to set prices for their products enables them to set the prices

they want other than take prices from consumers. The products in this market are such as oil,

which has privacy of ownership and high market entry fees. For a supplier to enter this

Features of market structures

There are different markets within an economy. The markets exist due to the types of

competition in that market. Each market has different characteristics making it unique

compared to others. Economic planners have a duty of creating policies that control the

existence of the markets without exploiting consumers. (Arnold, 2015)

Monopoly market

This is a structure made up of one supplier of a commodity and a large number of

customers in the market (Behravesh, 2014). The size of a monopoly does not matter in the

definition because small suppliers can also be monopolies. This indicates that a monopoly is

the only supplier of a certain commodity in the market. Most monopolies charge high prices

for their products due to lack of competition. Monopolies result from private access of raw

materials. This ownership enables firms to become the sole producer of a product. The entry

conditions into a monopoly include such as the ownership of private raw material access

which other firms do not have.additionally,the ability to pay the high market entrance costs

enable suppliers to enter a monopoly market (Burda, July 25, 2017).

Oligopoly

This is a market system, which only a few number of firms control the market (Flynn,

2011). There is similarity to a monopoly only that in oligopoly, it is more than one supplier in

the market. There is no set limit to the maximum number of supplier in an oligopoly.

However, the number is low to ensure that the actions of one firm influence the actions of the

other firms. Oligopolies ability to set prices for their products enables them to set the prices

they want other than take prices from consumers. The products in this market are such as oil,

which has privacy of ownership and high market entry fees. For a supplier to enter this

ECONOMICS FOR MANAGERS 3

market, they require to have the finances to pay the high market entry fees or privately own

the products dealt with by the oligopoly.

Perfect competition

Perfect competitions exist where consumers set prices, firms sell identical products,

sellers have a small market share, buyers have all the information about the market and the

market has freedom of entry and exit (James Michael Stewart, 2015). This market is usually

theoretical and it is what other markets could wish to become. The consumers in this market

have alternatives to buy from other suppliers when one supplier charges high fees. The

companies are characterised by earning just enough profits to enable them survive in the

market. Entry to the market is easy as there are no barriers to enter the market. Suppliers try

to gain market by differentiating their products and advertising them. They try to cut prices to

gain more customers and charge high prices sometimes to increase their profit margins.

Monopolistic competition

This market sell similar products but are not perfect substitutes (Jones, 2017). There

are low barriers to entry in the market and the actions of one firm do not affect the actions of

other firms in the market. The market suppliers set prices for their products and the customers

buy at those prices. The market players have little market power and thus are not able to

influence each other’s actions. The entry to the market is easy as there are few barrier of entry

thus new suppliers cans enter and leave the market at will.

Short run and long run profits and losses

Short run period refers to a period when a firm incurs both fixed and variable costs

during a production period (Jones, 2017). This period prevents the outcome, salaries and

prices of a firm from attaining equilibrium. On the other hand, long run is the period in which

all production costs are variable and firms are able to adjust to costs. Long run enables firms

market, they require to have the finances to pay the high market entry fees or privately own

the products dealt with by the oligopoly.

Perfect competition

Perfect competitions exist where consumers set prices, firms sell identical products,

sellers have a small market share, buyers have all the information about the market and the

market has freedom of entry and exit (James Michael Stewart, 2015). This market is usually

theoretical and it is what other markets could wish to become. The consumers in this market

have alternatives to buy from other suppliers when one supplier charges high fees. The

companies are characterised by earning just enough profits to enable them survive in the

market. Entry to the market is easy as there are no barriers to enter the market. Suppliers try

to gain market by differentiating their products and advertising them. They try to cut prices to

gain more customers and charge high prices sometimes to increase their profit margins.

Monopolistic competition

This market sell similar products but are not perfect substitutes (Jones, 2017). There

are low barriers to entry in the market and the actions of one firm do not affect the actions of

other firms in the market. The market suppliers set prices for their products and the customers

buy at those prices. The market players have little market power and thus are not able to

influence each other’s actions. The entry to the market is easy as there are few barrier of entry

thus new suppliers cans enter and leave the market at will.

Short run and long run profits and losses

Short run period refers to a period when a firm incurs both fixed and variable costs

during a production period (Jones, 2017). This period prevents the outcome, salaries and

prices of a firm from attaining equilibrium. On the other hand, long run is the period in which

all production costs are variable and firms are able to adjust to costs. Long run enables firms

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS FOR MANAGERS 4

to control their cost while in short run; firms are only able to control prices through adjusting

their production levels.

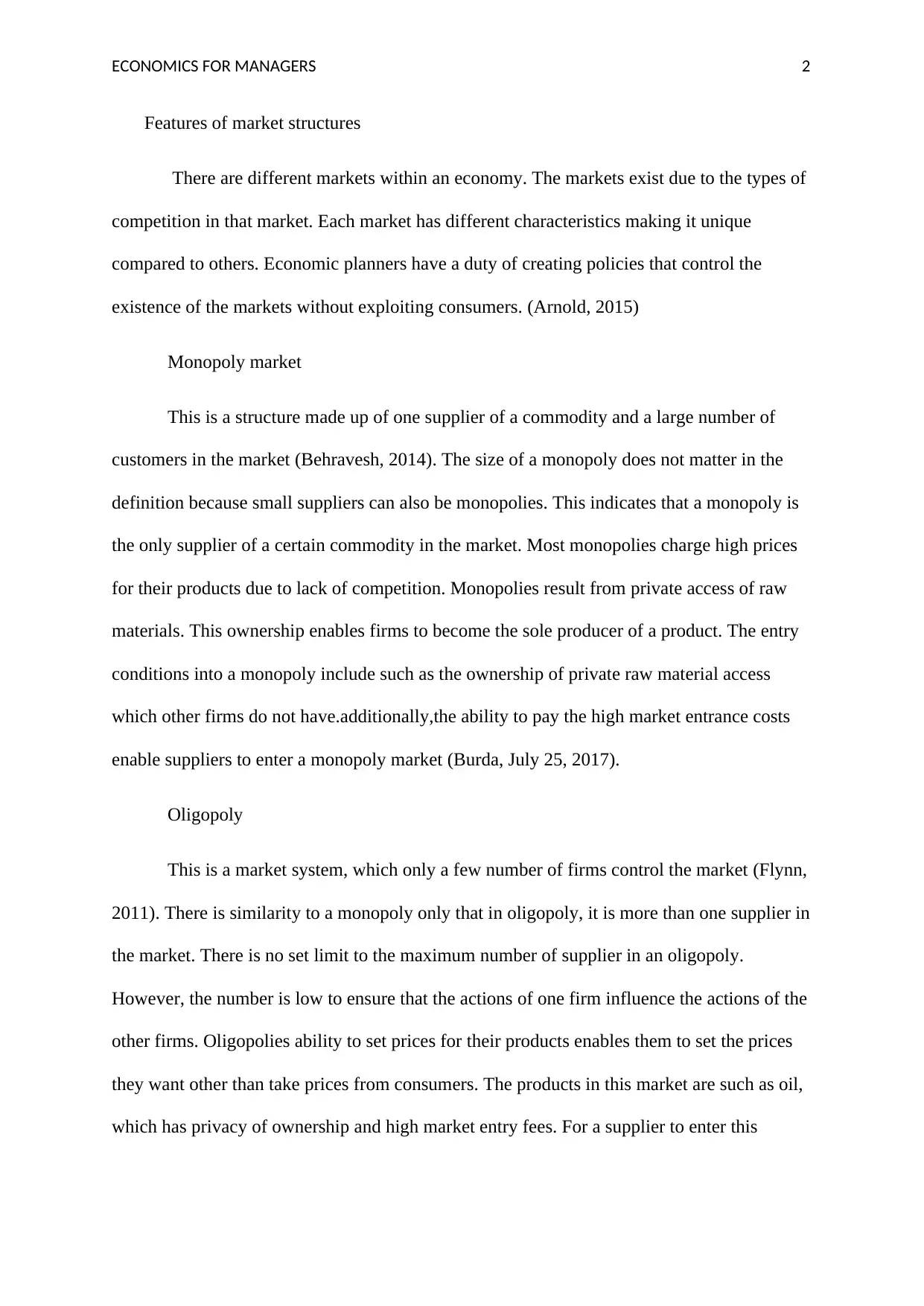

Perfect competition market

Short run profits are realised when the price of commodities is more than the average

total cost (Lee Coppock, 2017). The firm’s production is usually at a point where marginal

revenue equals marginal cost. This indicates that the firm is realising profits within the short

run period of production.

Perfect competition markets incur short run losses when the prices are less than

average total cost for the firm. The production level is usually at a point where marginal

revenue is equal to marginal cost. This way the firm tries to reduce short run losses.

Long run profits refers to when the market is making economic gains from market

activities (MIller, 2017). The reason for increased gains is due to increase in the supply

activities such as gaining new customers. The aim of firms is to ensure that they live this

period for long avoiding losses. Long run losses refers to when the firm commodity prices are

less than the variable costs incurred in production. The firm at this period may consider

leaving the industry if they are unable to reduce the variable costs.

to control their cost while in short run; firms are only able to control prices through adjusting

their production levels.

Perfect competition market

Short run profits are realised when the price of commodities is more than the average

total cost (Lee Coppock, 2017). The firm’s production is usually at a point where marginal

revenue equals marginal cost. This indicates that the firm is realising profits within the short

run period of production.

Perfect competition markets incur short run losses when the prices are less than

average total cost for the firm. The production level is usually at a point where marginal

revenue is equal to marginal cost. This way the firm tries to reduce short run losses.

Long run profits refers to when the market is making economic gains from market

activities (MIller, 2017). The reason for increased gains is due to increase in the supply

activities such as gaining new customers. The aim of firms is to ensure that they live this

period for long avoiding losses. Long run losses refers to when the firm commodity prices are

less than the variable costs incurred in production. The firm at this period may consider

leaving the industry if they are unable to reduce the variable costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS FOR MANAGERS 5

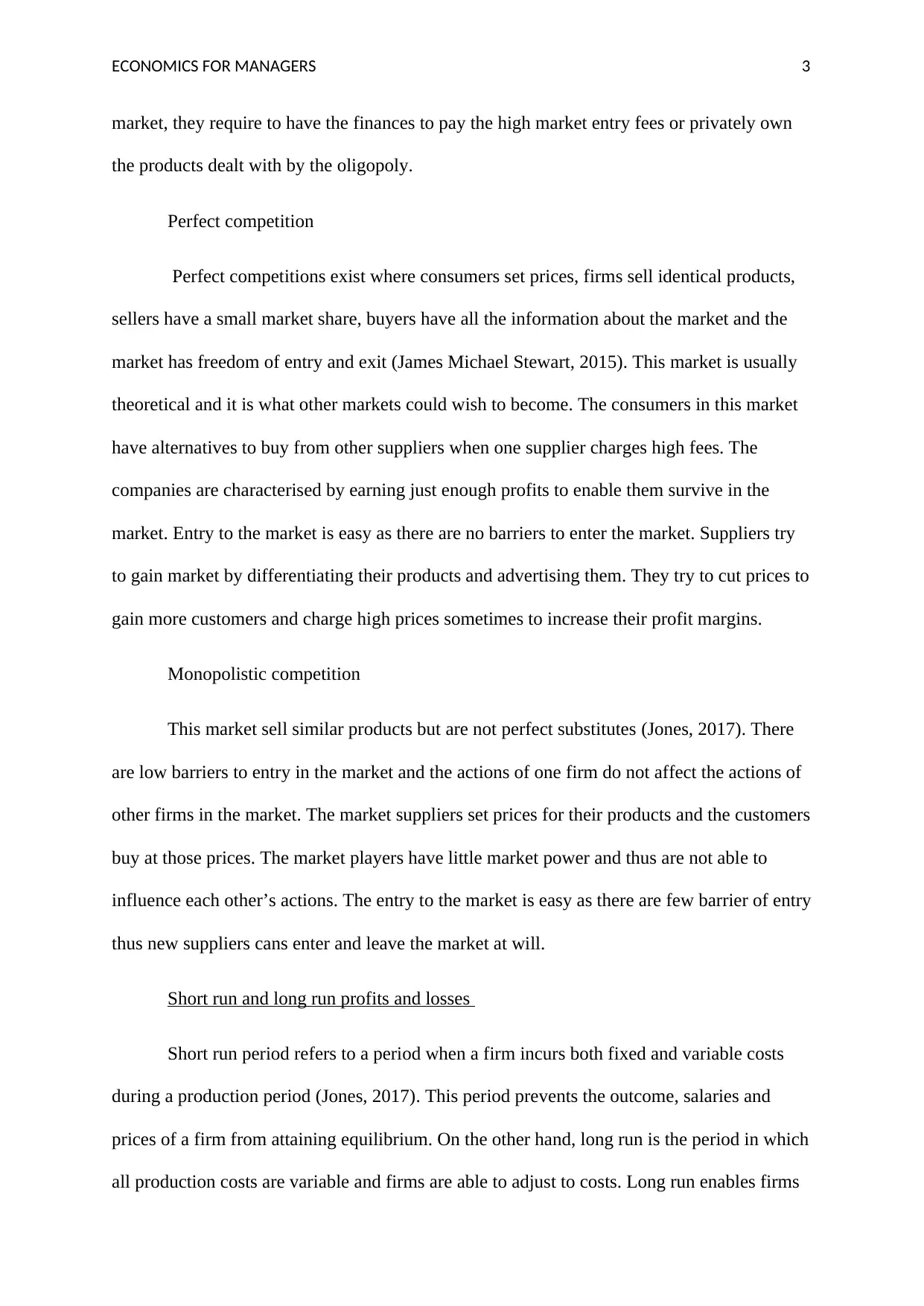

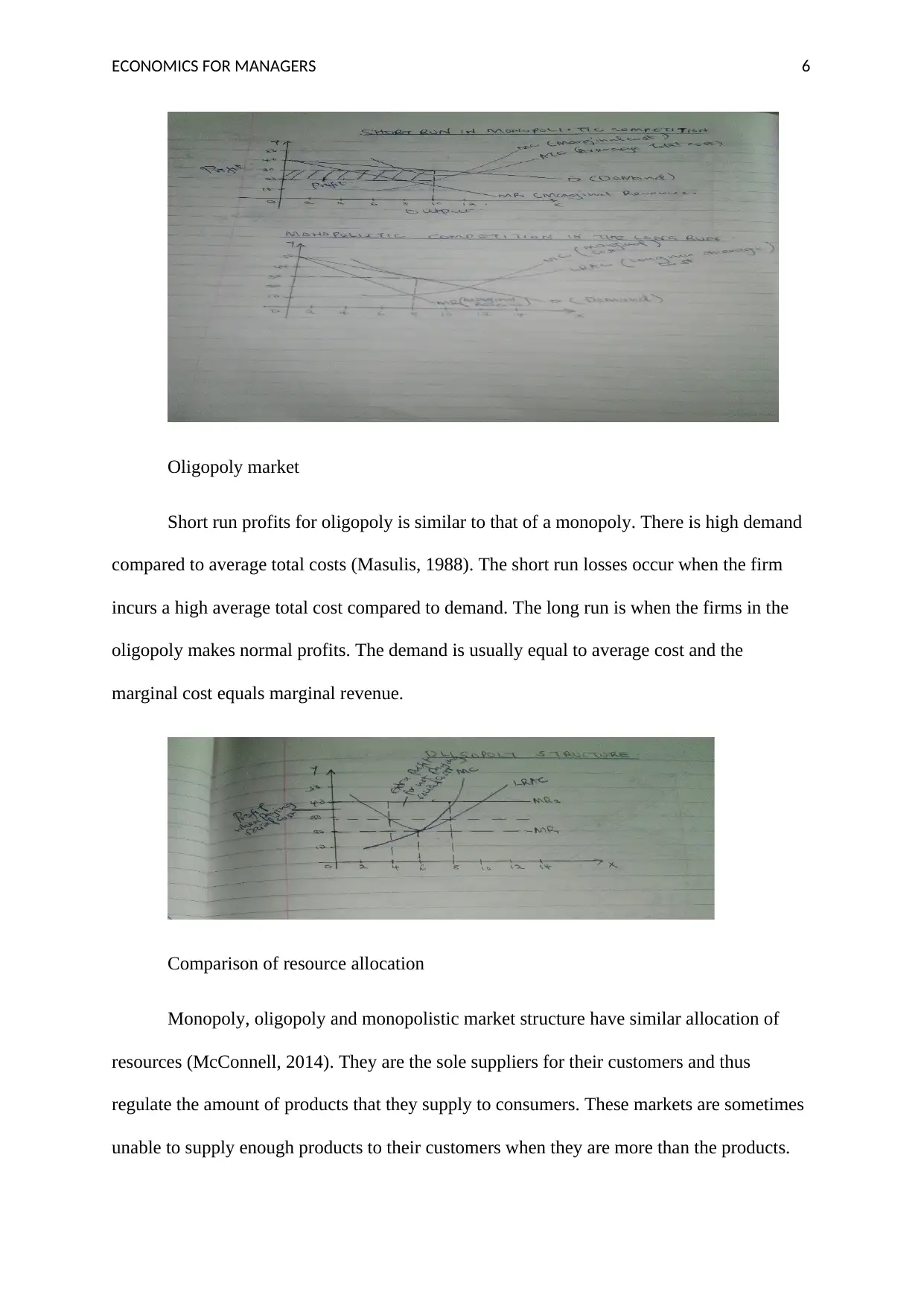

Monopoly

Short run profits refers to the period when a monopoly demand curve is greater than

the average total curve (MIller, 2017). This is usually at a certain quantity where the

monopoly earns short run profits. Short run losses refers to the point where the demand curve

is less than the average total curve.

A monopoly earns long run profits when the monopoly revenues are more than the

costs incurred (Mankiw, 2017). When all production factors remain constant then the

monopoly continues making profits in the long run. The monopoly tends to prevent other

firms from entering the market so that they continue making profit. The long run losses are

when the variable costs for production are more than the revenues earned by the firm. The

company tries to reduce the losses by increasing the prices for their products.

Diagram

Monopolistic competition

Firms earn short run profits when the demand for products is less than average total

cost. Short run losses occur when the average total costs exceeds the demand for product

(Margaret Ray, 2015). In the long run unlike in the short run, the firms make normal profits.

The demand is equal to long run average cost at a quantity point where marginal revenue

equals marginal cost.

Diagram

Monopoly

Short run profits refers to the period when a monopoly demand curve is greater than

the average total curve (MIller, 2017). This is usually at a certain quantity where the

monopoly earns short run profits. Short run losses refers to the point where the demand curve

is less than the average total curve.

A monopoly earns long run profits when the monopoly revenues are more than the

costs incurred (Mankiw, 2017). When all production factors remain constant then the

monopoly continues making profits in the long run. The monopoly tends to prevent other

firms from entering the market so that they continue making profit. The long run losses are

when the variable costs for production are more than the revenues earned by the firm. The

company tries to reduce the losses by increasing the prices for their products.

Diagram

Monopolistic competition

Firms earn short run profits when the demand for products is less than average total

cost. Short run losses occur when the average total costs exceeds the demand for product

(Margaret Ray, 2015). In the long run unlike in the short run, the firms make normal profits.

The demand is equal to long run average cost at a quantity point where marginal revenue

equals marginal cost.

Diagram

ECONOMICS FOR MANAGERS 6

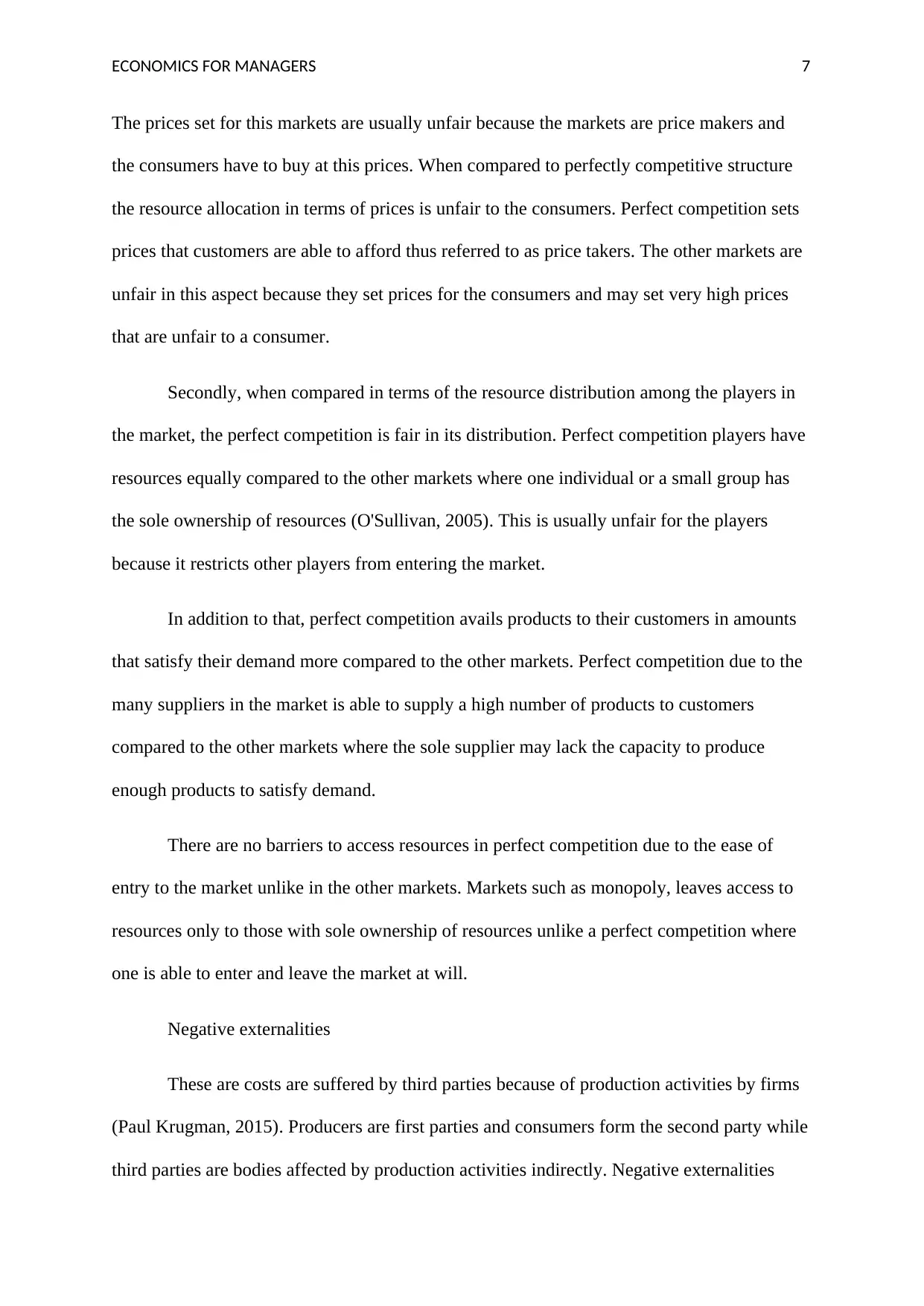

Oligopoly market

Short run profits for oligopoly is similar to that of a monopoly. There is high demand

compared to average total costs (Masulis, 1988). The short run losses occur when the firm

incurs a high average total cost compared to demand. The long run is when the firms in the

oligopoly makes normal profits. The demand is usually equal to average cost and the

marginal cost equals marginal revenue.

Comparison of resource allocation

Monopoly, oligopoly and monopolistic market structure have similar allocation of

resources (McConnell, 2014). They are the sole suppliers for their customers and thus

regulate the amount of products that they supply to consumers. These markets are sometimes

unable to supply enough products to their customers when they are more than the products.

Oligopoly market

Short run profits for oligopoly is similar to that of a monopoly. There is high demand

compared to average total costs (Masulis, 1988). The short run losses occur when the firm

incurs a high average total cost compared to demand. The long run is when the firms in the

oligopoly makes normal profits. The demand is usually equal to average cost and the

marginal cost equals marginal revenue.

Comparison of resource allocation

Monopoly, oligopoly and monopolistic market structure have similar allocation of

resources (McConnell, 2014). They are the sole suppliers for their customers and thus

regulate the amount of products that they supply to consumers. These markets are sometimes

unable to supply enough products to their customers when they are more than the products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS FOR MANAGERS 7

The prices set for this markets are usually unfair because the markets are price makers and

the consumers have to buy at this prices. When compared to perfectly competitive structure

the resource allocation in terms of prices is unfair to the consumers. Perfect competition sets

prices that customers are able to afford thus referred to as price takers. The other markets are

unfair in this aspect because they set prices for the consumers and may set very high prices

that are unfair to a consumer.

Secondly, when compared in terms of the resource distribution among the players in

the market, the perfect competition is fair in its distribution. Perfect competition players have

resources equally compared to the other markets where one individual or a small group has

the sole ownership of resources (O'Sullivan, 2005). This is usually unfair for the players

because it restricts other players from entering the market.

In addition to that, perfect competition avails products to their customers in amounts

that satisfy their demand more compared to the other markets. Perfect competition due to the

many suppliers in the market is able to supply a high number of products to customers

compared to the other markets where the sole supplier may lack the capacity to produce

enough products to satisfy demand.

There are no barriers to access resources in perfect competition due to the ease of

entry to the market unlike in the other markets. Markets such as monopoly, leaves access to

resources only to those with sole ownership of resources unlike a perfect competition where

one is able to enter and leave the market at will.

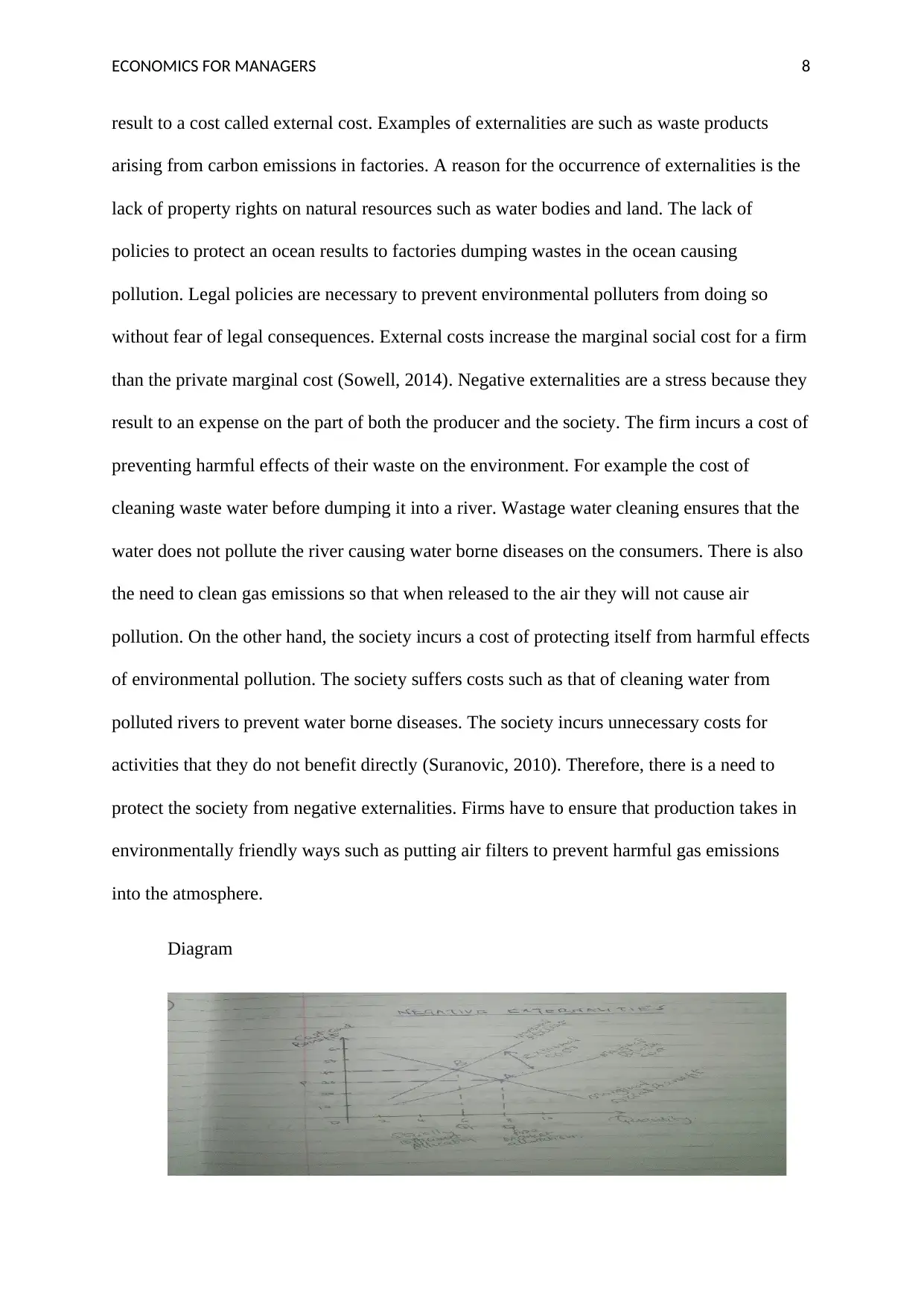

Negative externalities

These are costs are suffered by third parties because of production activities by firms

(Paul Krugman, 2015). Producers are first parties and consumers form the second party while

third parties are bodies affected by production activities indirectly. Negative externalities

The prices set for this markets are usually unfair because the markets are price makers and

the consumers have to buy at this prices. When compared to perfectly competitive structure

the resource allocation in terms of prices is unfair to the consumers. Perfect competition sets

prices that customers are able to afford thus referred to as price takers. The other markets are

unfair in this aspect because they set prices for the consumers and may set very high prices

that are unfair to a consumer.

Secondly, when compared in terms of the resource distribution among the players in

the market, the perfect competition is fair in its distribution. Perfect competition players have

resources equally compared to the other markets where one individual or a small group has

the sole ownership of resources (O'Sullivan, 2005). This is usually unfair for the players

because it restricts other players from entering the market.

In addition to that, perfect competition avails products to their customers in amounts

that satisfy their demand more compared to the other markets. Perfect competition due to the

many suppliers in the market is able to supply a high number of products to customers

compared to the other markets where the sole supplier may lack the capacity to produce

enough products to satisfy demand.

There are no barriers to access resources in perfect competition due to the ease of

entry to the market unlike in the other markets. Markets such as monopoly, leaves access to

resources only to those with sole ownership of resources unlike a perfect competition where

one is able to enter and leave the market at will.

Negative externalities

These are costs are suffered by third parties because of production activities by firms

(Paul Krugman, 2015). Producers are first parties and consumers form the second party while

third parties are bodies affected by production activities indirectly. Negative externalities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS FOR MANAGERS 8

result to a cost called external cost. Examples of externalities are such as waste products

arising from carbon emissions in factories. A reason for the occurrence of externalities is the

lack of property rights on natural resources such as water bodies and land. The lack of

policies to protect an ocean results to factories dumping wastes in the ocean causing

pollution. Legal policies are necessary to prevent environmental polluters from doing so

without fear of legal consequences. External costs increase the marginal social cost for a firm

than the private marginal cost (Sowell, 2014). Negative externalities are a stress because they

result to an expense on the part of both the producer and the society. The firm incurs a cost of

preventing harmful effects of their waste on the environment. For example the cost of

cleaning waste water before dumping it into a river. Wastage water cleaning ensures that the

water does not pollute the river causing water borne diseases on the consumers. There is also

the need to clean gas emissions so that when released to the air they will not cause air

pollution. On the other hand, the society incurs a cost of protecting itself from harmful effects

of environmental pollution. The society suffers costs such as that of cleaning water from

polluted rivers to prevent water borne diseases. The society incurs unnecessary costs for

activities that they do not benefit directly (Suranovic, 2010). Therefore, there is a need to

protect the society from negative externalities. Firms have to ensure that production takes in

environmentally friendly ways such as putting air filters to prevent harmful gas emissions

into the atmosphere.

Diagram

result to a cost called external cost. Examples of externalities are such as waste products

arising from carbon emissions in factories. A reason for the occurrence of externalities is the

lack of property rights on natural resources such as water bodies and land. The lack of

policies to protect an ocean results to factories dumping wastes in the ocean causing

pollution. Legal policies are necessary to prevent environmental polluters from doing so

without fear of legal consequences. External costs increase the marginal social cost for a firm

than the private marginal cost (Sowell, 2014). Negative externalities are a stress because they

result to an expense on the part of both the producer and the society. The firm incurs a cost of

preventing harmful effects of their waste on the environment. For example the cost of

cleaning waste water before dumping it into a river. Wastage water cleaning ensures that the

water does not pollute the river causing water borne diseases on the consumers. There is also

the need to clean gas emissions so that when released to the air they will not cause air

pollution. On the other hand, the society incurs a cost of protecting itself from harmful effects

of environmental pollution. The society suffers costs such as that of cleaning water from

polluted rivers to prevent water borne diseases. The society incurs unnecessary costs for

activities that they do not benefit directly (Suranovic, 2010). Therefore, there is a need to

protect the society from negative externalities. Firms have to ensure that production takes in

environmentally friendly ways such as putting air filters to prevent harmful gas emissions

into the atmosphere.

Diagram

ECONOMICS FOR MANAGERS 9

Negative externality case study

In America, the transport sector causes many negative externalities such as the

emission of carbon fumes from the burning of fuel. These gases are dangerous to the society

because of the resulting damage to the environment. Polluted air causes airborne diseases

such as asthma causing the government to incur financial expenses in buying medicines for

the affected. The government also incurs a cost of trying to clean the air from these

pollutants. The government also incurs costs in research and development of drugs to cure

new illnesses that emerge from the harmful effects of the emissions.

Fuel fumes from automobiles cause damage if the ozone layer of the atmosphere

resulting to climate changes in America. Temperatures in America increase each year. This

trend is worrying because of the resulting reduction in water levels in oceans and other water

bodies. There is also reduction in the yearly amounts of rainfall causing problems to the

agriculture sector. The fumes from vehicles cause all this damage.

Vehicles have also caused congestion in roads and cities. Vehicle ownership in

America has increased in the past years at a very high rate. This has caused lots of congestion

in the towns, as many citizens prefer using their vehicles than public means of transport. The

congestion results from such as traffic jams, which traps vehicles in roads. Lot of time

wastage happens in traffic jams reducing time for important economic activities. Congestion

results from parking lots, which take up large spaces. Without the many vehicles, the parking

lots would be clear making town centres more spacious.

The American government incurs huge expenses trying to reduce the effects of

externalities. Governments try to reduce the effects because in most cases they cause the

society added unnecessary costs. The society pays external costs trying to protect themselves

from the harmful effects of the externalities.

Negative externality case study

In America, the transport sector causes many negative externalities such as the

emission of carbon fumes from the burning of fuel. These gases are dangerous to the society

because of the resulting damage to the environment. Polluted air causes airborne diseases

such as asthma causing the government to incur financial expenses in buying medicines for

the affected. The government also incurs a cost of trying to clean the air from these

pollutants. The government also incurs costs in research and development of drugs to cure

new illnesses that emerge from the harmful effects of the emissions.

Fuel fumes from automobiles cause damage if the ozone layer of the atmosphere

resulting to climate changes in America. Temperatures in America increase each year. This

trend is worrying because of the resulting reduction in water levels in oceans and other water

bodies. There is also reduction in the yearly amounts of rainfall causing problems to the

agriculture sector. The fumes from vehicles cause all this damage.

Vehicles have also caused congestion in roads and cities. Vehicle ownership in

America has increased in the past years at a very high rate. This has caused lots of congestion

in the towns, as many citizens prefer using their vehicles than public means of transport. The

congestion results from such as traffic jams, which traps vehicles in roads. Lot of time

wastage happens in traffic jams reducing time for important economic activities. Congestion

results from parking lots, which take up large spaces. Without the many vehicles, the parking

lots would be clear making town centres more spacious.

The American government incurs huge expenses trying to reduce the effects of

externalities. Governments try to reduce the effects because in most cases they cause the

society added unnecessary costs. The society pays external costs trying to protect themselves

from the harmful effects of the externalities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS FOR MANAGERS

10

Solutions to externalities

The government, society and producers have come up with solutions to solve the

problem of negative externalities. All players in the market put efforts in reducing negative

externalities for the good of their market. For example when a producer fails to prevent air

pollution, then it damages its image in the society. The consumers also protect themselves

from negative externalities through such as treating home water. The consumers are very

important also in ensuring that they push producers to come up with solutions to externalities.

In USA, various solutions solve the problem of negative externalities caused by

automobiles. For example the government through the technology sector has come tried the

possibility of using electric vehicles. These vehicles do not use petrol and diesel, which emit

carbon fumes into the air. Electric vehicles are the future of cars that do not cause pollution.

Electric vehicles are powered using solar energy or electricity, which are very friendly to the

environment. Solar energy is considered environmental friendly and thus when used in cars,

then the problem of carbon fumes is eliminated. Use of electric powered vehicles saves the

government finances because of the reduction of air pollution, which is usually a cost to the

government. There is also a reduction in the amounts used for importing petroleum.

The problem of global warming caused by carbon fumes solved through various

methods. The American government and NGOs sponsor tree planting campaigns. Tree

plantation helps largely in controlling the increase of carbon in the air. This prevents damage

to the ozone layer thus reduce the global warming effects. This solution is important to the

country as it reduces expenses incurred by the society trying to curb the effects of global

warming. The agricultural sector too improves due to the availability of water, as the water

bodies do not experience reduction in water levels. Rainfall amounts also increase and this

boosts the environmental sector largely.

10

Solutions to externalities

The government, society and producers have come up with solutions to solve the

problem of negative externalities. All players in the market put efforts in reducing negative

externalities for the good of their market. For example when a producer fails to prevent air

pollution, then it damages its image in the society. The consumers also protect themselves

from negative externalities through such as treating home water. The consumers are very

important also in ensuring that they push producers to come up with solutions to externalities.

In USA, various solutions solve the problem of negative externalities caused by

automobiles. For example the government through the technology sector has come tried the

possibility of using electric vehicles. These vehicles do not use petrol and diesel, which emit

carbon fumes into the air. Electric vehicles are the future of cars that do not cause pollution.

Electric vehicles are powered using solar energy or electricity, which are very friendly to the

environment. Solar energy is considered environmental friendly and thus when used in cars,

then the problem of carbon fumes is eliminated. Use of electric powered vehicles saves the

government finances because of the reduction of air pollution, which is usually a cost to the

government. There is also a reduction in the amounts used for importing petroleum.

The problem of global warming caused by carbon fumes solved through various

methods. The American government and NGOs sponsor tree planting campaigns. Tree

plantation helps largely in controlling the increase of carbon in the air. This prevents damage

to the ozone layer thus reduce the global warming effects. This solution is important to the

country as it reduces expenses incurred by the society trying to curb the effects of global

warming. The agricultural sector too improves due to the availability of water, as the water

bodies do not experience reduction in water levels. Rainfall amounts also increase and this

boosts the environmental sector largely.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS FOR MANAGERS

11

The government has also come up with solutions to curb congestion caused by

vehicles. Government policies such as preventing the citizens from driving their vehicles to

the city centres. This has resulted to fewer vehicles in the city centres thus vehicle congestion

reduction. Traffic jams reduction have also been experienced in the towns because of the few

vehicles brought to town,additionaly the roads have been tailored to correct the problem, of

traffic jam.dual carriages and underground roads have increased the capacity of roads thus

reducing time wastage on roads through traffic jams

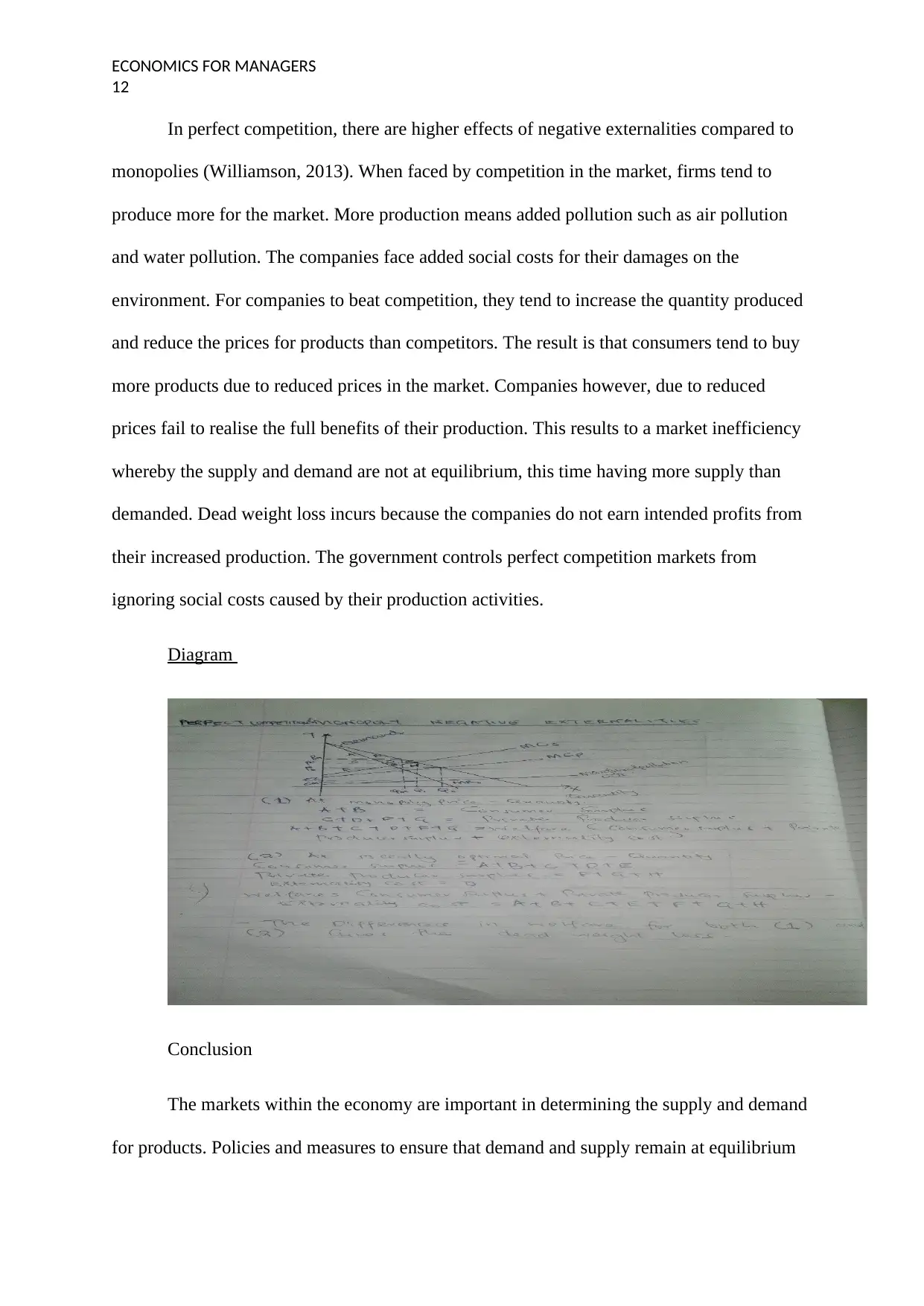

Effects of externalities on monopoly and perfect competition

Monopolies have lesser negative externalities compared to other markets (Tucker,

2016). Monopolies operate in markets without competition unlike other markets. Monopolies

do not need to increase their production levels to compete with the market. Increase in

production results to more pollution due to extra waste. This problem does not usually apply

to monopoly markets. However, when a monopoly produces a negative externality such as

pollution, the monopoly produces less than the social optimal output. The monopolies due to

lack of competition try to cover their costs through reducing production and increasing the

prices of their products. This causes a problem to the market due to the low supply and high

prices. The market also fails to operate at equilibrium due to low supply and high demand

(Tyler Cowen, 2014). Monopolies do this due to lack of competition in the market. The

reduction of supply of products to the market below the demand of the product results to

market inefficiencies. Consumers buy less of the products and on the other hand, the

producers fail to recover full benefits from sales. This results to dead weight loss in the

market as well market inefficiency. Monopolies require constant control by the government

to ensure that they do not ignore paying social costs for damages caused by their production

activities.

11

The government has also come up with solutions to curb congestion caused by

vehicles. Government policies such as preventing the citizens from driving their vehicles to

the city centres. This has resulted to fewer vehicles in the city centres thus vehicle congestion

reduction. Traffic jams reduction have also been experienced in the towns because of the few

vehicles brought to town,additionaly the roads have been tailored to correct the problem, of

traffic jam.dual carriages and underground roads have increased the capacity of roads thus

reducing time wastage on roads through traffic jams

Effects of externalities on monopoly and perfect competition

Monopolies have lesser negative externalities compared to other markets (Tucker,

2016). Monopolies operate in markets without competition unlike other markets. Monopolies

do not need to increase their production levels to compete with the market. Increase in

production results to more pollution due to extra waste. This problem does not usually apply

to monopoly markets. However, when a monopoly produces a negative externality such as

pollution, the monopoly produces less than the social optimal output. The monopolies due to

lack of competition try to cover their costs through reducing production and increasing the

prices of their products. This causes a problem to the market due to the low supply and high

prices. The market also fails to operate at equilibrium due to low supply and high demand

(Tyler Cowen, 2014). Monopolies do this due to lack of competition in the market. The

reduction of supply of products to the market below the demand of the product results to

market inefficiencies. Consumers buy less of the products and on the other hand, the

producers fail to recover full benefits from sales. This results to dead weight loss in the

market as well market inefficiency. Monopolies require constant control by the government

to ensure that they do not ignore paying social costs for damages caused by their production

activities.

ECONOMICS FOR MANAGERS

12

In perfect competition, there are higher effects of negative externalities compared to

monopolies (Williamson, 2013). When faced by competition in the market, firms tend to

produce more for the market. More production means added pollution such as air pollution

and water pollution. The companies face added social costs for their damages on the

environment. For companies to beat competition, they tend to increase the quantity produced

and reduce the prices for products than competitors. The result is that consumers tend to buy

more products due to reduced prices in the market. Companies however, due to reduced

prices fail to realise the full benefits of their production. This results to a market inefficiency

whereby the supply and demand are not at equilibrium, this time having more supply than

demanded. Dead weight loss incurs because the companies do not earn intended profits from

their increased production. The government controls perfect competition markets from

ignoring social costs caused by their production activities.

Diagram

Conclusion

The markets within the economy are important in determining the supply and demand

for products. Policies and measures to ensure that demand and supply remain at equilibrium

12

In perfect competition, there are higher effects of negative externalities compared to

monopolies (Williamson, 2013). When faced by competition in the market, firms tend to

produce more for the market. More production means added pollution such as air pollution

and water pollution. The companies face added social costs for their damages on the

environment. For companies to beat competition, they tend to increase the quantity produced

and reduce the prices for products than competitors. The result is that consumers tend to buy

more products due to reduced prices in the market. Companies however, due to reduced

prices fail to realise the full benefits of their production. This results to a market inefficiency

whereby the supply and demand are not at equilibrium, this time having more supply than

demanded. Dead weight loss incurs because the companies do not earn intended profits from

their increased production. The government controls perfect competition markets from

ignoring social costs caused by their production activities.

Diagram

Conclusion

The markets within the economy are important in determining the supply and demand

for products. Policies and measures to ensure that demand and supply remain at equilibrium

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.