Economics Assignment: Market Structures, Profit, and Revenue Analysis

VerifiedAdded on 2022/11/25

|12

|2541

|297

Homework Assignment

AI Summary

This economics assignment delves into the analysis of market structures, focusing on both perfect and monopolistic competition. The student completes tables to calculate total revenue, marginal cost, and marginal revenue, subsequently determining equilibrium points and profit or loss for firms. The assignment further explores the short-run versus long-run perspectives of firms, as well as the characteristics of monopolistic firms. The analysis extends to the difference between marginal and average revenue for a monopolistic firm, supported by relevant diagrams and economic principles. The student provides detailed explanations and calculations to demonstrate a comprehensive understanding of microeconomic concepts.

Running head: ECONOMICS 1

ECONOMICS

Student Name

Institution Affiliation

Course

Facilitator

Date

ECONOMICS

Student Name

Institution Affiliation

Course

Facilitator

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 2

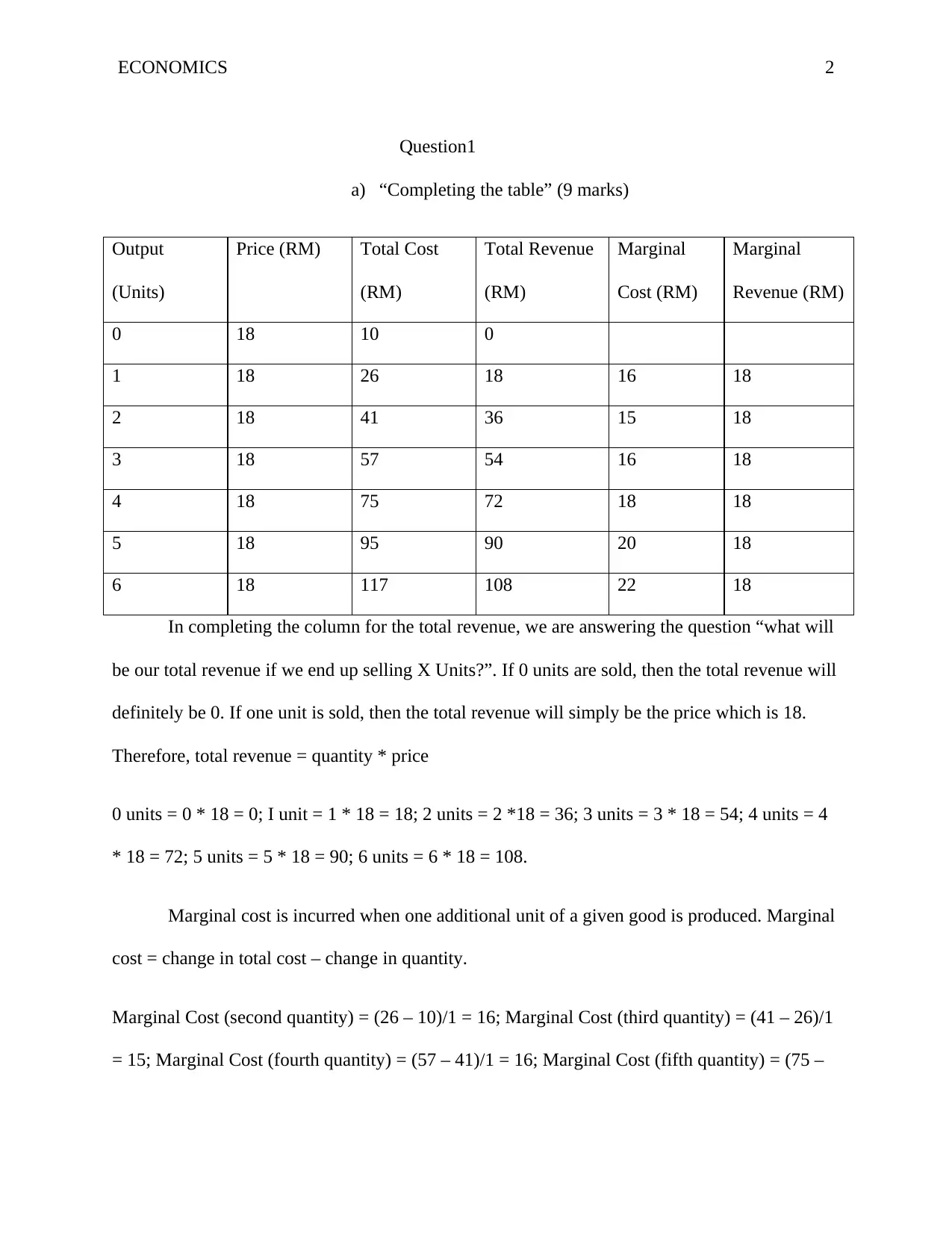

Question1

a) “Completing the table” (9 marks)

Output

(Units)

Price (RM) Total Cost

(RM)

Total Revenue

(RM)

Marginal

Cost (RM)

Marginal

Revenue (RM)

0 18 10 0

1 18 26 18 16 18

2 18 41 36 15 18

3 18 57 54 16 18

4 18 75 72 18 18

5 18 95 90 20 18

6 18 117 108 22 18

In completing the column for the total revenue, we are answering the question “what will

be our total revenue if we end up selling X Units?”. If 0 units are sold, then the total revenue will

definitely be 0. If one unit is sold, then the total revenue will simply be the price which is 18.

Therefore, total revenue = quantity * price

0 units = 0 * 18 = 0; I unit = 1 * 18 = 18; 2 units = 2 *18 = 36; 3 units = 3 * 18 = 54; 4 units = 4

* 18 = 72; 5 units = 5 * 18 = 90; 6 units = 6 * 18 = 108.

Marginal cost is incurred when one additional unit of a given good is produced. Marginal

cost = change in total cost – change in quantity.

Marginal Cost (second quantity) = (26 – 10)/1 = 16; Marginal Cost (third quantity) = (41 – 26)/1

= 15; Marginal Cost (fourth quantity) = (57 – 41)/1 = 16; Marginal Cost (fifth quantity) = (75 –

Question1

a) “Completing the table” (9 marks)

Output

(Units)

Price (RM) Total Cost

(RM)

Total Revenue

(RM)

Marginal

Cost (RM)

Marginal

Revenue (RM)

0 18 10 0

1 18 26 18 16 18

2 18 41 36 15 18

3 18 57 54 16 18

4 18 75 72 18 18

5 18 95 90 20 18

6 18 117 108 22 18

In completing the column for the total revenue, we are answering the question “what will

be our total revenue if we end up selling X Units?”. If 0 units are sold, then the total revenue will

definitely be 0. If one unit is sold, then the total revenue will simply be the price which is 18.

Therefore, total revenue = quantity * price

0 units = 0 * 18 = 0; I unit = 1 * 18 = 18; 2 units = 2 *18 = 36; 3 units = 3 * 18 = 54; 4 units = 4

* 18 = 72; 5 units = 5 * 18 = 90; 6 units = 6 * 18 = 108.

Marginal cost is incurred when one additional unit of a given good is produced. Marginal

cost = change in total cost – change in quantity.

Marginal Cost (second quantity) = (26 – 10)/1 = 16; Marginal Cost (third quantity) = (41 – 26)/1

= 15; Marginal Cost (fourth quantity) = (57 – 41)/1 = 16; Marginal Cost (fifth quantity) = (75 –

ECONOMICS 3

57)/1 = 18; Marginal Cost (sixth quantity) = (95 – 75)/1 = 20; Marginal Cost (seventh quantity) =

(117 – 95)/1 = 22.

Marginal revenue is earned when one additional unit of a good is produced (Board &

Skrzypacz, 2016). Marginal revenue = change in total revenue/change in quantity.

Marginal Revenue (second quantity) = (18 – 0)/1 = 18; Marginal Revenue (third quantity) = (36

– 18)/1 = 18; Marginal Revenue (fourth quantity) = (54 – 36)/1 = 18; Marginal Revenue (fifth

quantity) = (72 – 54)/1 = 18; Marginal Revenue (sixth quantity) = (90 – 72)/1 = 18; Marginal

Revenue (seventh quantity) = (108 – 90)/1 = 18.

b) “The price and output determination at equilibrium” (6 marks)

At the equilibrium point, the marginal cost of a firm is equal to its marginal revenue and

the curve for the marginal cost cuts the curve for the marginal revenue from below (Von

Stackelberg, 2010). From the completed table above, the equilibrium point where the marginal

cost of the firm and its marginal revenue are equal is 18 (the equilibrium point is the point where

marginal cost = marginal revenue = 18). At the equilibrium point, the price for the firm is 18 and

the output is 4 units.

c) “Profit or loss calculation at equilibrium” (4 marks)

Profit or loss for a firm is obtained by subtracting the total costs from the total revenue

for the firm. Therefore, profit or loss = Total Revenue – Total Costs.

57)/1 = 18; Marginal Cost (sixth quantity) = (95 – 75)/1 = 20; Marginal Cost (seventh quantity) =

(117 – 95)/1 = 22.

Marginal revenue is earned when one additional unit of a good is produced (Board &

Skrzypacz, 2016). Marginal revenue = change in total revenue/change in quantity.

Marginal Revenue (second quantity) = (18 – 0)/1 = 18; Marginal Revenue (third quantity) = (36

– 18)/1 = 18; Marginal Revenue (fourth quantity) = (54 – 36)/1 = 18; Marginal Revenue (fifth

quantity) = (72 – 54)/1 = 18; Marginal Revenue (sixth quantity) = (90 – 72)/1 = 18; Marginal

Revenue (seventh quantity) = (108 – 90)/1 = 18.

b) “The price and output determination at equilibrium” (6 marks)

At the equilibrium point, the marginal cost of a firm is equal to its marginal revenue and

the curve for the marginal cost cuts the curve for the marginal revenue from below (Von

Stackelberg, 2010). From the completed table above, the equilibrium point where the marginal

cost of the firm and its marginal revenue are equal is 18 (the equilibrium point is the point where

marginal cost = marginal revenue = 18). At the equilibrium point, the price for the firm is 18 and

the output is 4 units.

c) “Profit or loss calculation at equilibrium” (4 marks)

Profit or loss for a firm is obtained by subtracting the total costs from the total revenue

for the firm. Therefore, profit or loss = Total Revenue – Total Costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 4

At the equilibrium point, profit or loss for 4 units = total revenue for 4 units – total costs

for 4 units = 72 – 75 = RM -3. This means that, at the equilibrium point, the firm makes a loss of

RM 3.

d) “Determining whether the firm is in the short-run or long-run” (5 marks)

The firm is in the short-run period. This is because despite the fact that the firm is making

losses (losses are made since the average costs are above the average revenue) it still continues to

operate. This is because the firm can recover its average variable costs since it must pay the fixed

costs whether it produces or not. Therefore, since the firm’s average costs are below its average

revenue, it continues to operate in the short-run since it can still recover its average variable

costs.

e) “Determining the market structure of the firm” (6 marks)

The firm belongs to a perfect competition market structure. This is due to the following

reasons. Firstly, from the table, each unit is being sold at the same price. This means that

marginal revenue which is the revenue earned when one more unit is sold would remain the

same. Therefore, the marginal revenue curve will be horizontal completely. This scenario

happens for perfectly competitive firms. Secondly, the average revenue which is obtained when

the total revenue is divided by the output remains the same since all the units are sold at the same

price. From the table, price, average revenue and marginal revenue for all the units are equal.

This fulfills the condition for a perfectly competitive market structure where price = average

revenue = marginal revenue and hence the firm is said to belong to a perfect competition market

structure.

At the equilibrium point, profit or loss for 4 units = total revenue for 4 units – total costs

for 4 units = 72 – 75 = RM -3. This means that, at the equilibrium point, the firm makes a loss of

RM 3.

d) “Determining whether the firm is in the short-run or long-run” (5 marks)

The firm is in the short-run period. This is because despite the fact that the firm is making

losses (losses are made since the average costs are above the average revenue) it still continues to

operate. This is because the firm can recover its average variable costs since it must pay the fixed

costs whether it produces or not. Therefore, since the firm’s average costs are below its average

revenue, it continues to operate in the short-run since it can still recover its average variable

costs.

e) “Determining the market structure of the firm” (6 marks)

The firm belongs to a perfect competition market structure. This is due to the following

reasons. Firstly, from the table, each unit is being sold at the same price. This means that

marginal revenue which is the revenue earned when one more unit is sold would remain the

same. Therefore, the marginal revenue curve will be horizontal completely. This scenario

happens for perfectly competitive firms. Secondly, the average revenue which is obtained when

the total revenue is divided by the output remains the same since all the units are sold at the same

price. From the table, price, average revenue and marginal revenue for all the units are equal.

This fulfills the condition for a perfectly competitive market structure where price = average

revenue = marginal revenue and hence the firm is said to belong to a perfect competition market

structure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 5

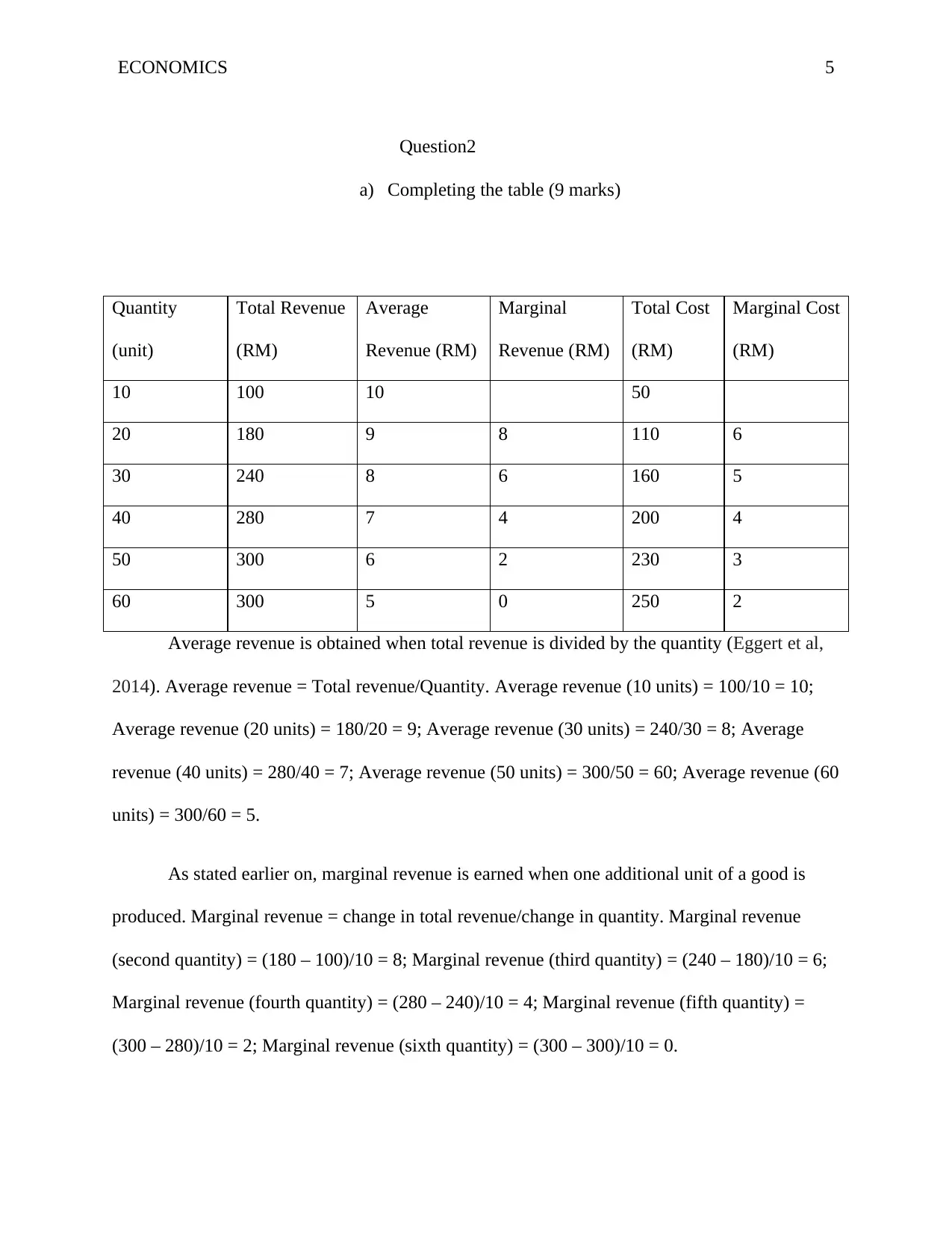

Question2

a) Completing the table (9 marks)

Quantity

(unit)

Total Revenue

(RM)

Average

Revenue (RM)

Marginal

Revenue (RM)

Total Cost

(RM)

Marginal Cost

(RM)

10 100 10 50

20 180 9 8 110 6

30 240 8 6 160 5

40 280 7 4 200 4

50 300 6 2 230 3

60 300 5 0 250 2

Average revenue is obtained when total revenue is divided by the quantity (Eggert et al,

2014). Average revenue = Total revenue/Quantity. Average revenue (10 units) = 100/10 = 10;

Average revenue (20 units) = 180/20 = 9; Average revenue (30 units) = 240/30 = 8; Average

revenue (40 units) = 280/40 = 7; Average revenue (50 units) = 300/50 = 60; Average revenue (60

units) = 300/60 = 5.

As stated earlier on, marginal revenue is earned when one additional unit of a good is

produced. Marginal revenue = change in total revenue/change in quantity. Marginal revenue

(second quantity) = (180 – 100)/10 = 8; Marginal revenue (third quantity) = (240 – 180)/10 = 6;

Marginal revenue (fourth quantity) = (280 – 240)/10 = 4; Marginal revenue (fifth quantity) =

(300 – 280)/10 = 2; Marginal revenue (sixth quantity) = (300 – 300)/10 = 0.

Question2

a) Completing the table (9 marks)

Quantity

(unit)

Total Revenue

(RM)

Average

Revenue (RM)

Marginal

Revenue (RM)

Total Cost

(RM)

Marginal Cost

(RM)

10 100 10 50

20 180 9 8 110 6

30 240 8 6 160 5

40 280 7 4 200 4

50 300 6 2 230 3

60 300 5 0 250 2

Average revenue is obtained when total revenue is divided by the quantity (Eggert et al,

2014). Average revenue = Total revenue/Quantity. Average revenue (10 units) = 100/10 = 10;

Average revenue (20 units) = 180/20 = 9; Average revenue (30 units) = 240/30 = 8; Average

revenue (40 units) = 280/40 = 7; Average revenue (50 units) = 300/50 = 60; Average revenue (60

units) = 300/60 = 5.

As stated earlier on, marginal revenue is earned when one additional unit of a good is

produced. Marginal revenue = change in total revenue/change in quantity. Marginal revenue

(second quantity) = (180 – 100)/10 = 8; Marginal revenue (third quantity) = (240 – 180)/10 = 6;

Marginal revenue (fourth quantity) = (280 – 240)/10 = 4; Marginal revenue (fifth quantity) =

(300 – 280)/10 = 2; Marginal revenue (sixth quantity) = (300 – 300)/10 = 0.

ECONOMICS 6

As stated earlier on, marginal cost is incurred when one additional unit of a given good is

produced. Marginal cost = change in total cost – change in quantity. Marginal Cost (second

quantity) = (110 – 50) = 6; Marginal Cost (third quantity) = (160 – 110)/10 = 5; Marginal Cost

(fourth quantity) = (200 – 160)/10 = 4; Marginal Cost (fifth quantity) = (230 – 200)/10 = 3;

Marginal Cost (sixth quantity) = (250 – 230)/10 = 2.

b) Determining the market structure of the firm

The firm belongs to a monopolistic market structure. This is due to the following reasons.

The firm initially makes supernormal profits by producing less and charging higher prices and

this is termed as productive and allocative inefficiencies. The firm continues to produce as long

as the marginal cost is higher than the marginal cost until the profit-maximizing point is reached.

Just like the monopolistic competitive firms, when the firm attempts to produce a quantity above

the equilibrium quantity, the marginal cost becomes greater than the marginal revenue as

indicated in the table since total costs continue to increase.

c) Determining the equilibrium output and price (4 marks)

The firm is said to be at the equilibrium point when the marginal cost equals the marginal

revenue the curve for the marginal cost cuts the curve for the marginal revenue from below.

From the table the equilibrium point where marginal cost = marginal revenue = 4. The

equilibrium output is 40. The equilibrium price = total revenue at equilibrium/quantity at

equilibrium = 280/40 = RM 7.

d) Profit or loss calculation at equilibrium (4 marks)

As stated earlier on, marginal cost is incurred when one additional unit of a given good is

produced. Marginal cost = change in total cost – change in quantity. Marginal Cost (second

quantity) = (110 – 50) = 6; Marginal Cost (third quantity) = (160 – 110)/10 = 5; Marginal Cost

(fourth quantity) = (200 – 160)/10 = 4; Marginal Cost (fifth quantity) = (230 – 200)/10 = 3;

Marginal Cost (sixth quantity) = (250 – 230)/10 = 2.

b) Determining the market structure of the firm

The firm belongs to a monopolistic market structure. This is due to the following reasons.

The firm initially makes supernormal profits by producing less and charging higher prices and

this is termed as productive and allocative inefficiencies. The firm continues to produce as long

as the marginal cost is higher than the marginal cost until the profit-maximizing point is reached.

Just like the monopolistic competitive firms, when the firm attempts to produce a quantity above

the equilibrium quantity, the marginal cost becomes greater than the marginal revenue as

indicated in the table since total costs continue to increase.

c) Determining the equilibrium output and price (4 marks)

The firm is said to be at the equilibrium point when the marginal cost equals the marginal

revenue the curve for the marginal cost cuts the curve for the marginal revenue from below.

From the table the equilibrium point where marginal cost = marginal revenue = 4. The

equilibrium output is 40. The equilibrium price = total revenue at equilibrium/quantity at

equilibrium = 280/40 = RM 7.

d) Profit or loss calculation at equilibrium (4 marks)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 7

Profit or loss at equilibrium = Total Revenue at equilibrium – Total Costs at equilibrium

= 280 – 200 = RM 80. At equilibrium, the firm makes a profit of RM 80.

Question3 “Explaining why perfectly competitive firms only receive normal profit in the long-run”

(20 marks)

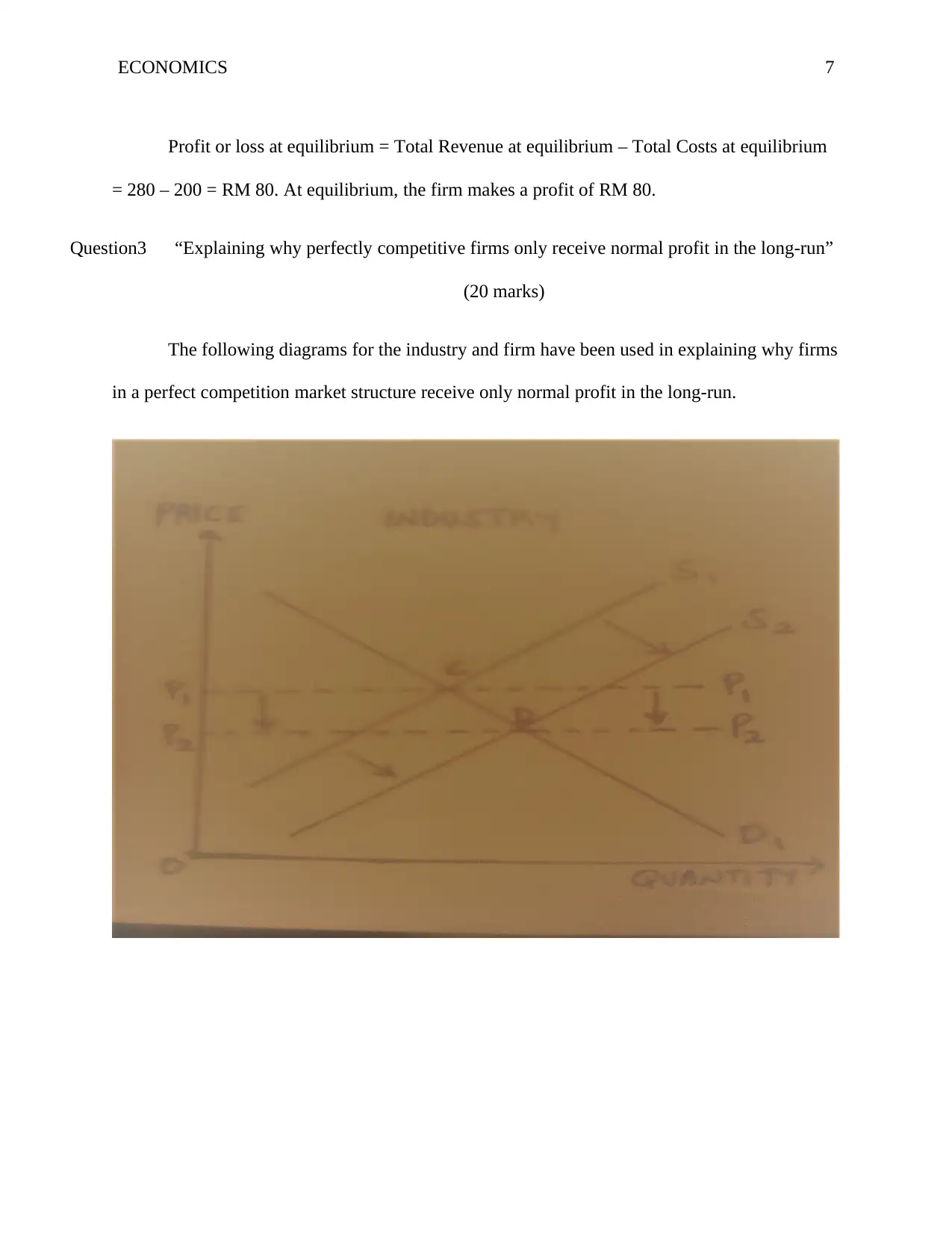

The following diagrams for the industry and firm have been used in explaining why firms

in a perfect competition market structure receive only normal profit in the long-run.

Profit or loss at equilibrium = Total Revenue at equilibrium – Total Costs at equilibrium

= 280 – 200 = RM 80. At equilibrium, the firm makes a profit of RM 80.

Question3 “Explaining why perfectly competitive firms only receive normal profit in the long-run”

(20 marks)

The following diagrams for the industry and firm have been used in explaining why firms

in a perfect competition market structure receive only normal profit in the long-run.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 8

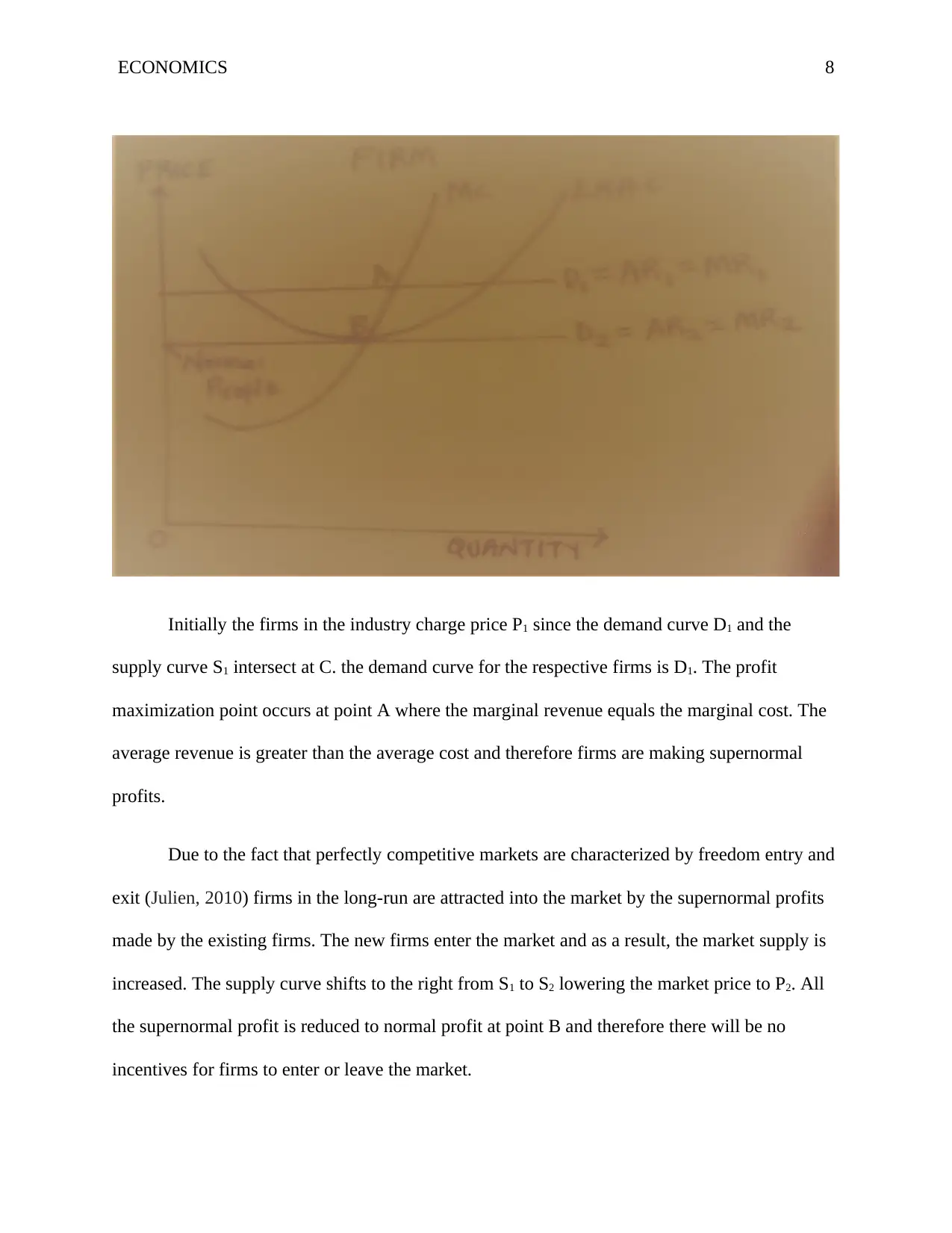

Initially the firms in the industry charge price P1 since the demand curve D1 and the

supply curve S1 intersect at C. the demand curve for the respective firms is D1. The profit

maximization point occurs at point A where the marginal revenue equals the marginal cost. The

average revenue is greater than the average cost and therefore firms are making supernormal

profits.

Due to the fact that perfectly competitive markets are characterized by freedom entry and

exit (Julien, 2010) firms in the long-run are attracted into the market by the supernormal profits

made by the existing firms. The new firms enter the market and as a result, the market supply is

increased. The supply curve shifts to the right from S1 to S2 lowering the market price to P2. All

the supernormal profit is reduced to normal profit at point B and therefore there will be no

incentives for firms to enter or leave the market.

Initially the firms in the industry charge price P1 since the demand curve D1 and the

supply curve S1 intersect at C. the demand curve for the respective firms is D1. The profit

maximization point occurs at point A where the marginal revenue equals the marginal cost. The

average revenue is greater than the average cost and therefore firms are making supernormal

profits.

Due to the fact that perfectly competitive markets are characterized by freedom entry and

exit (Julien, 2010) firms in the long-run are attracted into the market by the supernormal profits

made by the existing firms. The new firms enter the market and as a result, the market supply is

increased. The supply curve shifts to the right from S1 to S2 lowering the market price to P2. All

the supernormal profit is reduced to normal profit at point B and therefore there will be no

incentives for firms to enter or leave the market.

ECONOMICS 9

Also, if more firms continue to enter the market, the firms in the market will end up

making losses as market supply increases further. As a result, some firms will exit the market.

This will reduce the market supply and shift the supply curve back to S2 whereby each firm earns

only a normal profit. This is, therefore, the long-run equilibrium for perfectly competitive firms

and only normal profit can be earned as explained.

Question4 “Four characteristics of a monopolistic firm” (16 marks)

i. “Product Differentiation”

Monopolistic firms differentiate their products through various ways such as branding,

design, service and quality among others. The firms’ products are close but not perfect

substitutes. Product differentiation gives monopolistic firms some monopoly power to control the

price for their products.

ii. “Freedom of entry and exit”

Monopolistic firms have the freedom to either enter or leave the market (Geroski &

Jacquemin, 2013). New firms enter the market when existing firms are making supernormal

profits. The entry of new firms into the market reduces supernormal profits to normal profits

since the market supply is increased and prices are reduced. If existing firms make unsustainable

losses, they leave the industry and the profit moves back to normal in the long-run period.

iii. “Imperfect knowledge”

Monopolistic firms and buyers have imperfect knowledge about the market. Buyers do

not know which seller has cheap or the best quality products. Similarly, sellers (monopolistic

firms) do not know exactly what buyers prefer.

Also, if more firms continue to enter the market, the firms in the market will end up

making losses as market supply increases further. As a result, some firms will exit the market.

This will reduce the market supply and shift the supply curve back to S2 whereby each firm earns

only a normal profit. This is, therefore, the long-run equilibrium for perfectly competitive firms

and only normal profit can be earned as explained.

Question4 “Four characteristics of a monopolistic firm” (16 marks)

i. “Product Differentiation”

Monopolistic firms differentiate their products through various ways such as branding,

design, service and quality among others. The firms’ products are close but not perfect

substitutes. Product differentiation gives monopolistic firms some monopoly power to control the

price for their products.

ii. “Freedom of entry and exit”

Monopolistic firms have the freedom to either enter or leave the market (Geroski &

Jacquemin, 2013). New firms enter the market when existing firms are making supernormal

profits. The entry of new firms into the market reduces supernormal profits to normal profits

since the market supply is increased and prices are reduced. If existing firms make unsustainable

losses, they leave the industry and the profit moves back to normal in the long-run period.

iii. “Imperfect knowledge”

Monopolistic firms and buyers have imperfect knowledge about the market. Buyers do

not know which seller has cheap or the best quality products. Similarly, sellers (monopolistic

firms) do not know exactly what buyers prefer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 10

iv. “Independence and limited market share”

Monopolistic firms are independent and have a limited market share. This is because they

are vast in number and any decision by one firm will be spread over many firms such that the

overall impact is minute and other firms have no reason to react. This gives individual firms

some control over their market price.

Question5 “The difference between marginal and average revenue for a monopolistic firm” (14

marks)

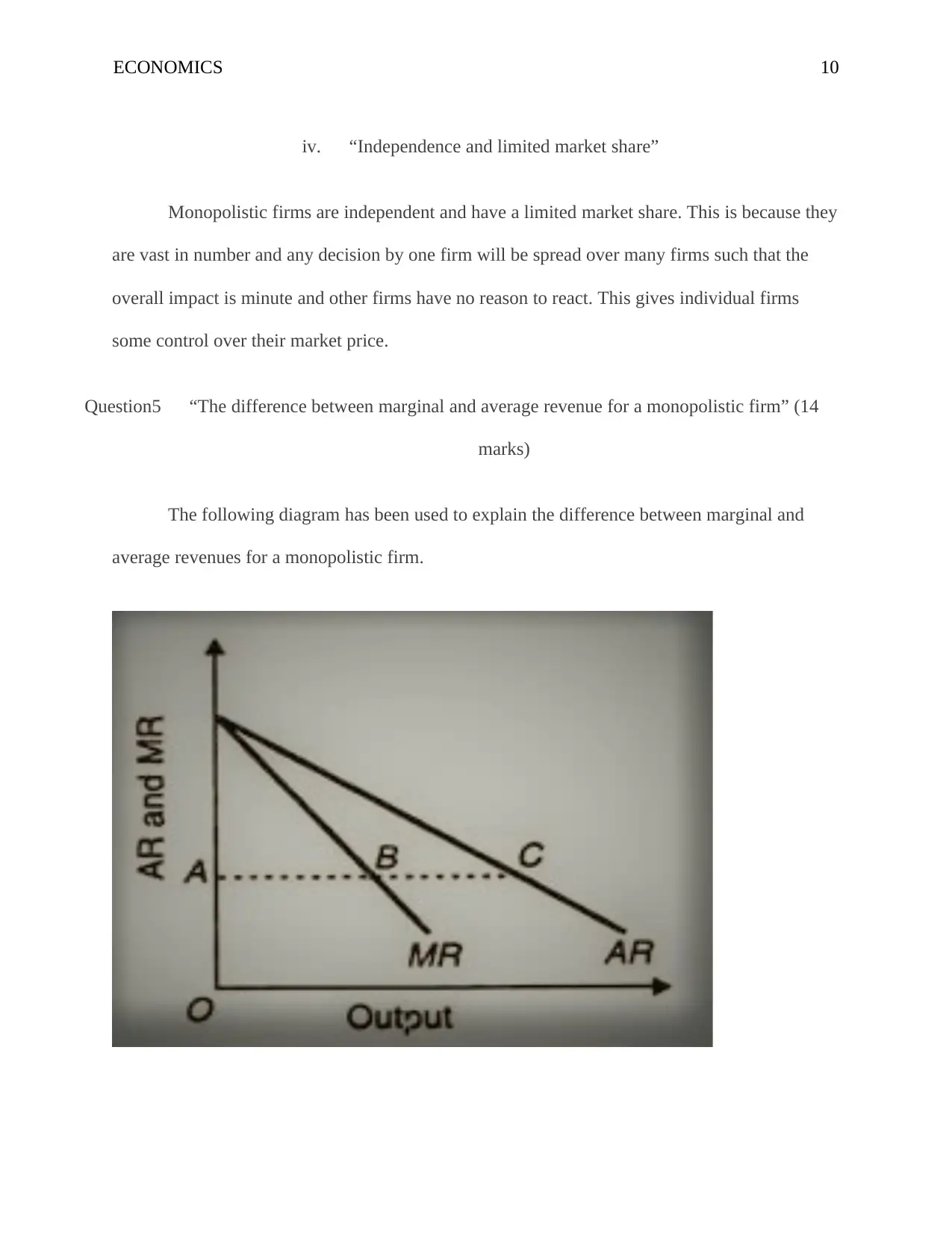

The following diagram has been used to explain the difference between marginal and

average revenues for a monopolistic firm.

iv. “Independence and limited market share”

Monopolistic firms are independent and have a limited market share. This is because they

are vast in number and any decision by one firm will be spread over many firms such that the

overall impact is minute and other firms have no reason to react. This gives individual firms

some control over their market price.

Question5 “The difference between marginal and average revenue for a monopolistic firm” (14

marks)

The following diagram has been used to explain the difference between marginal and

average revenues for a monopolistic firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 11

Average revenue is obtained when total revenue is divided by the quantity. Marginal

revenue is earned when one additional unit of a good is produced. Marginal revenue = change in

total revenue/change in quantity. The average revenue represents industry demand. For a

monopolistic firm, the marginal revenue is always less than the corresponding average revenue.

This means that the marginal revenue curve lies below the average revenue curve as shown in the

diagram above.

The average revenue curve for a monopolistic firm is more elastic as compared to its

marginal revenue and hence the marginal revenue curve is steeper than the average revenue

curve (Bertoletti & Etro, 2016) as shown in the diagram above. This is because monopolistic

firms sell products which are close but not perfect substitutes.

The rate of decrease of the marginal and average revenues is also different considering a

case whereby a monopolistic firm lowers its price to increase sales. The marginal revenue falls at

a greater rate than the average revenue for this case.

Average revenue is obtained when total revenue is divided by the quantity. Marginal

revenue is earned when one additional unit of a good is produced. Marginal revenue = change in

total revenue/change in quantity. The average revenue represents industry demand. For a

monopolistic firm, the marginal revenue is always less than the corresponding average revenue.

This means that the marginal revenue curve lies below the average revenue curve as shown in the

diagram above.

The average revenue curve for a monopolistic firm is more elastic as compared to its

marginal revenue and hence the marginal revenue curve is steeper than the average revenue

curve (Bertoletti & Etro, 2016) as shown in the diagram above. This is because monopolistic

firms sell products which are close but not perfect substitutes.

The rate of decrease of the marginal and average revenues is also different considering a

case whereby a monopolistic firm lowers its price to increase sales. The marginal revenue falls at

a greater rate than the average revenue for this case.

ECONOMICS 12

References

Bertoletti, P., & Etro, F. (2016). Monopolistic competition when income matters. The Economic

Journal, 127(603), 1217-1243.

Board, S., & Skrzypacz, A. (2016). Revenue management with forward-looking buyers. Journal

of Political Economy, 124(4), 1046-1087.

Eggert, A., Hogreve, J., Ulaga, W., & Muenkhoff, E. (2014). Revenue and profit implications of

industrial service strategies. Journal of Service Research, 17(1), 23-39.

Geroski, P. G., & Jacquemin, A. (2013). Barriers to entry and strategic competition. Routledge.

Julien, L. A. (2010). From imperfect to perfect competition: a parametric approach through

conjectural variations. The Manchester School, 78(6), 660-677.

Von Stackelberg, H. (2010). Market structure and equilibrium. Springer Science & Business

Media.

References

Bertoletti, P., & Etro, F. (2016). Monopolistic competition when income matters. The Economic

Journal, 127(603), 1217-1243.

Board, S., & Skrzypacz, A. (2016). Revenue management with forward-looking buyers. Journal

of Political Economy, 124(4), 1046-1087.

Eggert, A., Hogreve, J., Ulaga, W., & Muenkhoff, E. (2014). Revenue and profit implications of

industrial service strategies. Journal of Service Research, 17(1), 23-39.

Geroski, P. G., & Jacquemin, A. (2013). Barriers to entry and strategic competition. Routledge.

Julien, L. A. (2010). From imperfect to perfect competition: a parametric approach through

conjectural variations. The Manchester School, 78(6), 660-677.

Von Stackelberg, H. (2010). Market structure and equilibrium. Springer Science & Business

Media.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.