Business Economics Assignment: Analyzing Market Efficiency and Costs

VerifiedAdded on 2023/03/17

|13

|1904

|20

Homework Assignment

AI Summary

This business economics assignment delves into various aspects of market structures, including allocative efficiency under perfect and monopolistic competition, and the concepts of marginal cost and marginal product in production. It analyzes long-run average cost curves and explores constant and increasing cost industries, examining their supply curves. Furthermore, the assignment addresses market-based solutions to pollution externalities, such as taxation and tradeable pollution permits, providing a comprehensive understanding of these economic principles. Finally, the assignment includes practical applications of cost and profit analysis, offering a detailed breakdown of a firm's output, costs, and profit under different pricing scenarios.

Running head: BUSINESS ECONOMICS

Business Economics

Name of the Student

Name of the University

Student ID

Business Economics

Name of the Student

Name of the University

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS ECONOMICS

Table of Contents

Answer 2....................................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................3

Answer 3....................................................................................................................................4

Answer a.................................................................................................................................4

Answer b................................................................................................................................5

Answer c.................................................................................................................................6

Answer 5....................................................................................................................................6

Answer 6....................................................................................................................................8

Answer 8..................................................................................................................................10

Answer a...............................................................................................................................10

Answer b..............................................................................................................................10

Answer c...............................................................................................................................10

Answer d..............................................................................................................................10

Answer e...............................................................................................................................10

Answer f...............................................................................................................................11

Answer g..............................................................................................................................11

Answer h..............................................................................................................................11

Answer i...............................................................................................................................11

References................................................................................................................................12

Table of Contents

Answer 2....................................................................................................................................2

Answer a.................................................................................................................................2

Answer b................................................................................................................................3

Answer 3....................................................................................................................................4

Answer a.................................................................................................................................4

Answer b................................................................................................................................5

Answer c.................................................................................................................................6

Answer 5....................................................................................................................................6

Answer 6....................................................................................................................................8

Answer 8..................................................................................................................................10

Answer a...............................................................................................................................10

Answer b..............................................................................................................................10

Answer c...............................................................................................................................10

Answer d..............................................................................................................................10

Answer e...............................................................................................................................10

Answer f...............................................................................................................................11

Answer g..............................................................................................................................11

Answer h..............................................................................................................................11

Answer i...............................................................................................................................11

References................................................................................................................................12

2BUSINESS ECONOMICS

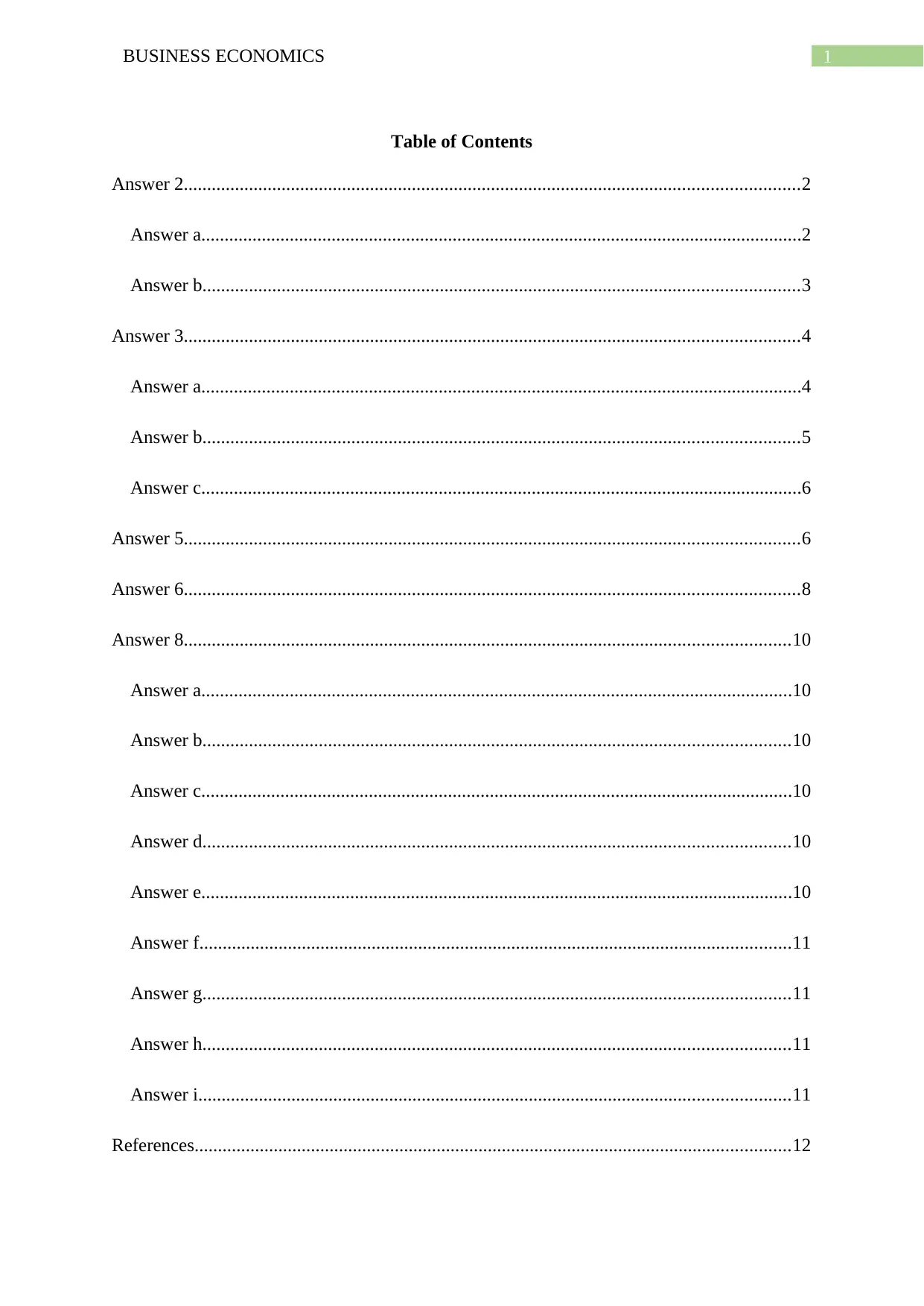

Answer 2

Answer a

Allocative efficiency refers to the state of the economy where production takes place

according to preference of consumers. In economic terms allocative efficiency is achieved

when each good or service is produced till the point where marginal benefit to consumers

from last unit of the good is equal to the marginal cost of producing the last unit. Allocative

efficiency is achieved only under perfect competition. Because of zero market power of firms

in the perfectly competitive market, firms are able to charge price that equal marginal cost of

production. Because of large number of identical firms in the market selling a homogenous

good, firms cannot charge price that exceeds marginal cost (Waldman and Jensen 2016). As

price is used as a measure of marginal benefit, under perfect competition marginal benefit to

society always equals marginal cost achieving allocative efficiency. Perfectly competitive

market is therefore considered as a benchmark of allocative efficiency.

Figure 1: Long run equilibrium and allocative efficiency under perfect competition

Answer 2

Answer a

Allocative efficiency refers to the state of the economy where production takes place

according to preference of consumers. In economic terms allocative efficiency is achieved

when each good or service is produced till the point where marginal benefit to consumers

from last unit of the good is equal to the marginal cost of producing the last unit. Allocative

efficiency is achieved only under perfect competition. Because of zero market power of firms

in the perfectly competitive market, firms are able to charge price that equal marginal cost of

production. Because of large number of identical firms in the market selling a homogenous

good, firms cannot charge price that exceeds marginal cost (Waldman and Jensen 2016). As

price is used as a measure of marginal benefit, under perfect competition marginal benefit to

society always equals marginal cost achieving allocative efficiency. Perfectly competitive

market is therefore considered as a benchmark of allocative efficiency.

Figure 1: Long run equilibrium and allocative efficiency under perfect competition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS ECONOMICS

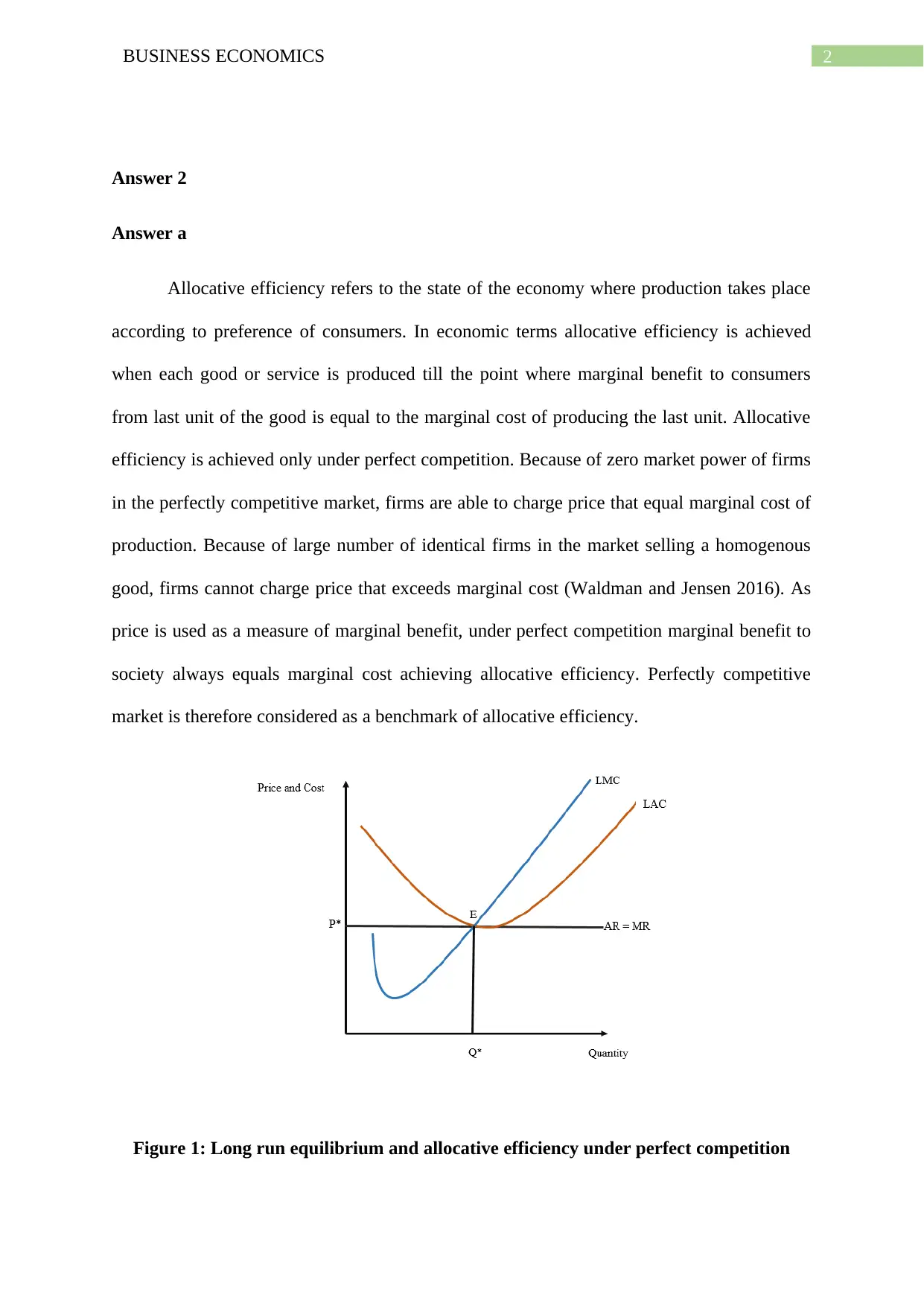

Answer b

Monopolistically competitive firms though have some similarities with perfect

competition, the market fails to achieve allocative efficiency. Unlike perfect competition

monopolistically competitive firms do not sell identical products rather they differentiate

their product. This allows monopolistically competitive firms some degree of market power.

Firms here maximize profit by equating marginal revenue and marginal cost. The demand

curve for a monopolistically competitive market slopes downward (Belleflamme and Peitz

2015). Market price thus is greater than marginal cost as shown in the figure below.

Corresponding to long run equilibrium point, society suffers a net welfare loss (loss in

consumer and producer surplus) making the production allocative inefficient.

Figure 2: Long run equilibrium and allocative inefficiency under monopolistic

competition

Answer b

Monopolistically competitive firms though have some similarities with perfect

competition, the market fails to achieve allocative efficiency. Unlike perfect competition

monopolistically competitive firms do not sell identical products rather they differentiate

their product. This allows monopolistically competitive firms some degree of market power.

Firms here maximize profit by equating marginal revenue and marginal cost. The demand

curve for a monopolistically competitive market slopes downward (Belleflamme and Peitz

2015). Market price thus is greater than marginal cost as shown in the figure below.

Corresponding to long run equilibrium point, society suffers a net welfare loss (loss in

consumer and producer surplus) making the production allocative inefficient.

Figure 2: Long run equilibrium and allocative inefficiency under monopolistic

competition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS ECONOMICS

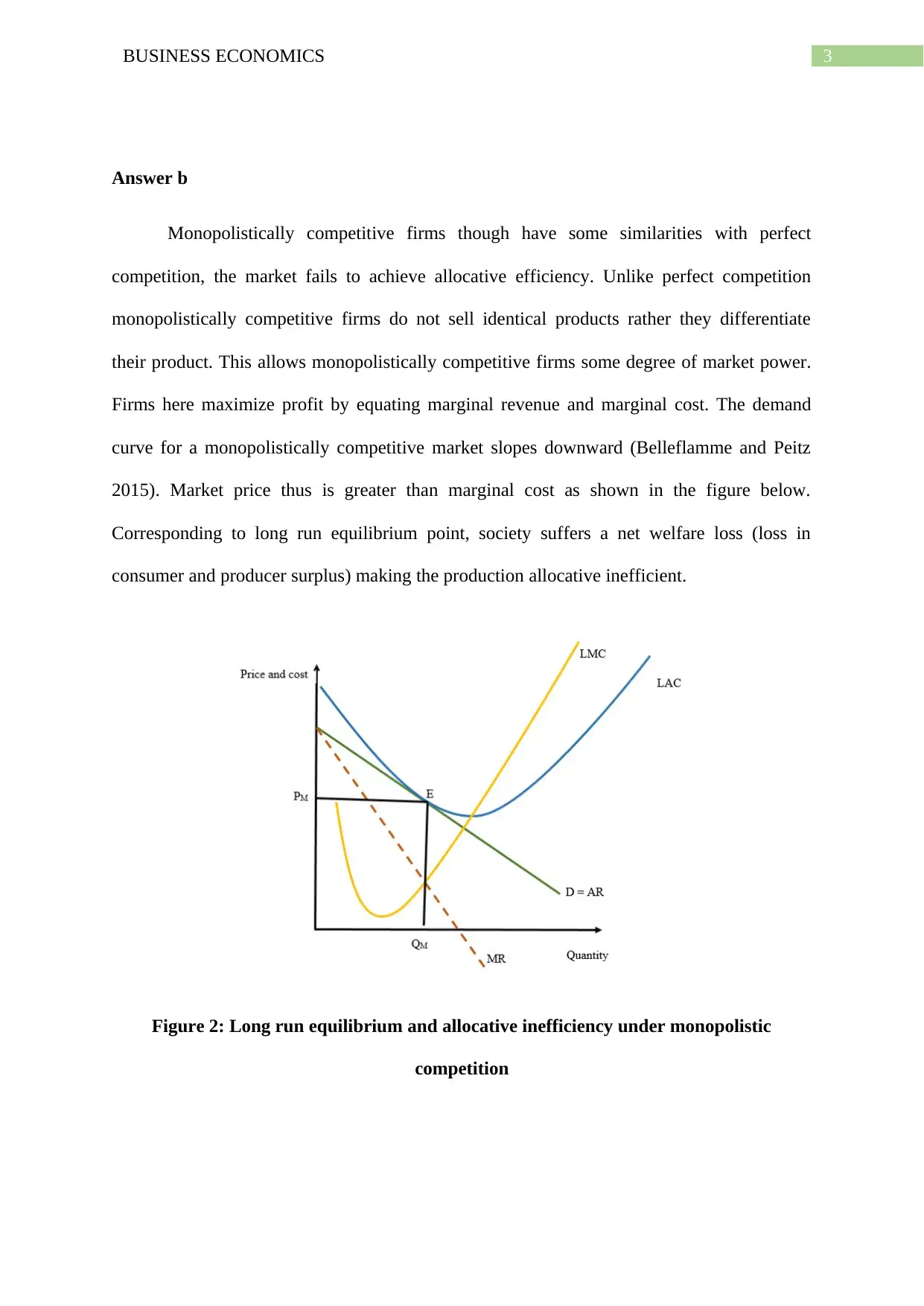

Answer 3

Answer a

In the production process, marginal cost indicates the additional cost to produce one

additional unit of a good or service. Marginal product is the additional production resulted

from adding one extra unit of variable factor. The shape of marginal product and marginal

cost curves are mirror image to each other showing close association between the two.

Quantity of output corresponding to which marginal cost in minimum is the same point where

the output produced by the variable input is associated with the maximum point of marginal

product of the inputs (Shepherd 2015). The range of production over which marginal product

increase, the variable input constitutes an increasing marginal return indicating a falling

marginal cost. For the range of production for which marginal product increases, the variable

input constitutes a decreasing marginal returns indicating rising marginal cost. Varying return

to scale associated with various level of production.

Answer 3

Answer a

In the production process, marginal cost indicates the additional cost to produce one

additional unit of a good or service. Marginal product is the additional production resulted

from adding one extra unit of variable factor. The shape of marginal product and marginal

cost curves are mirror image to each other showing close association between the two.

Quantity of output corresponding to which marginal cost in minimum is the same point where

the output produced by the variable input is associated with the maximum point of marginal

product of the inputs (Shepherd 2015). The range of production over which marginal product

increase, the variable input constitutes an increasing marginal return indicating a falling

marginal cost. For the range of production for which marginal product increases, the variable

input constitutes a decreasing marginal returns indicating rising marginal cost. Varying return

to scale associated with various level of production.

5BUSINESS ECONOMICS

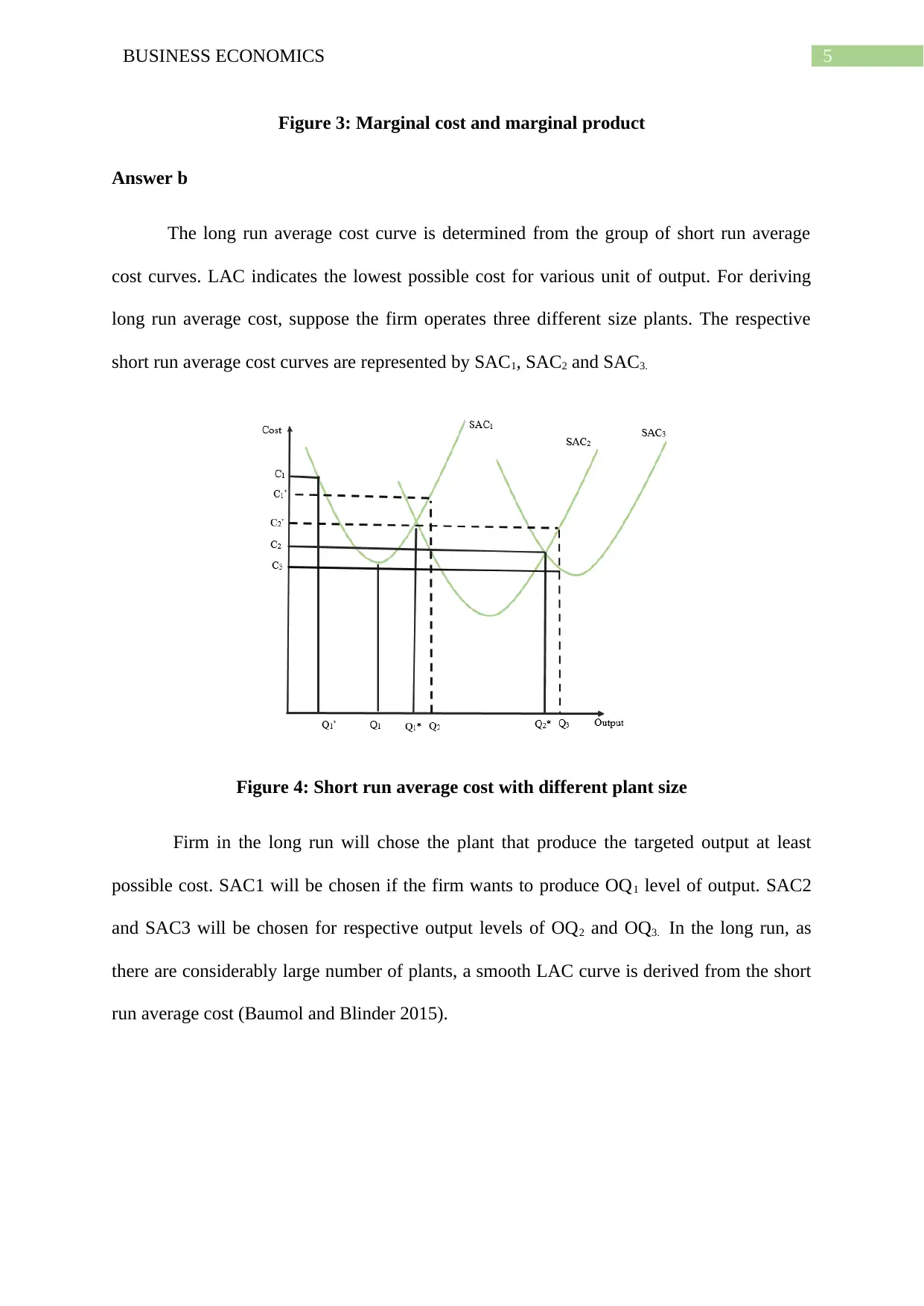

Figure 3: Marginal cost and marginal product

Answer b

The long run average cost curve is determined from the group of short run average

cost curves. LAC indicates the lowest possible cost for various unit of output. For deriving

long run average cost, suppose the firm operates three different size plants. The respective

short run average cost curves are represented by SAC1, SAC2 and SAC3.

Figure 4: Short run average cost with different plant size

Firm in the long run will chose the plant that produce the targeted output at least

possible cost. SAC1 will be chosen if the firm wants to produce OQ1 level of output. SAC2

and SAC3 will be chosen for respective output levels of OQ2 and OQ3. In the long run, as

there are considerably large number of plants, a smooth LAC curve is derived from the short

run average cost (Baumol and Blinder 2015).

Figure 3: Marginal cost and marginal product

Answer b

The long run average cost curve is determined from the group of short run average

cost curves. LAC indicates the lowest possible cost for various unit of output. For deriving

long run average cost, suppose the firm operates three different size plants. The respective

short run average cost curves are represented by SAC1, SAC2 and SAC3.

Figure 4: Short run average cost with different plant size

Firm in the long run will chose the plant that produce the targeted output at least

possible cost. SAC1 will be chosen if the firm wants to produce OQ1 level of output. SAC2

and SAC3 will be chosen for respective output levels of OQ2 and OQ3. In the long run, as

there are considerably large number of plants, a smooth LAC curve is derived from the short

run average cost (Baumol and Blinder 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS ECONOMICS

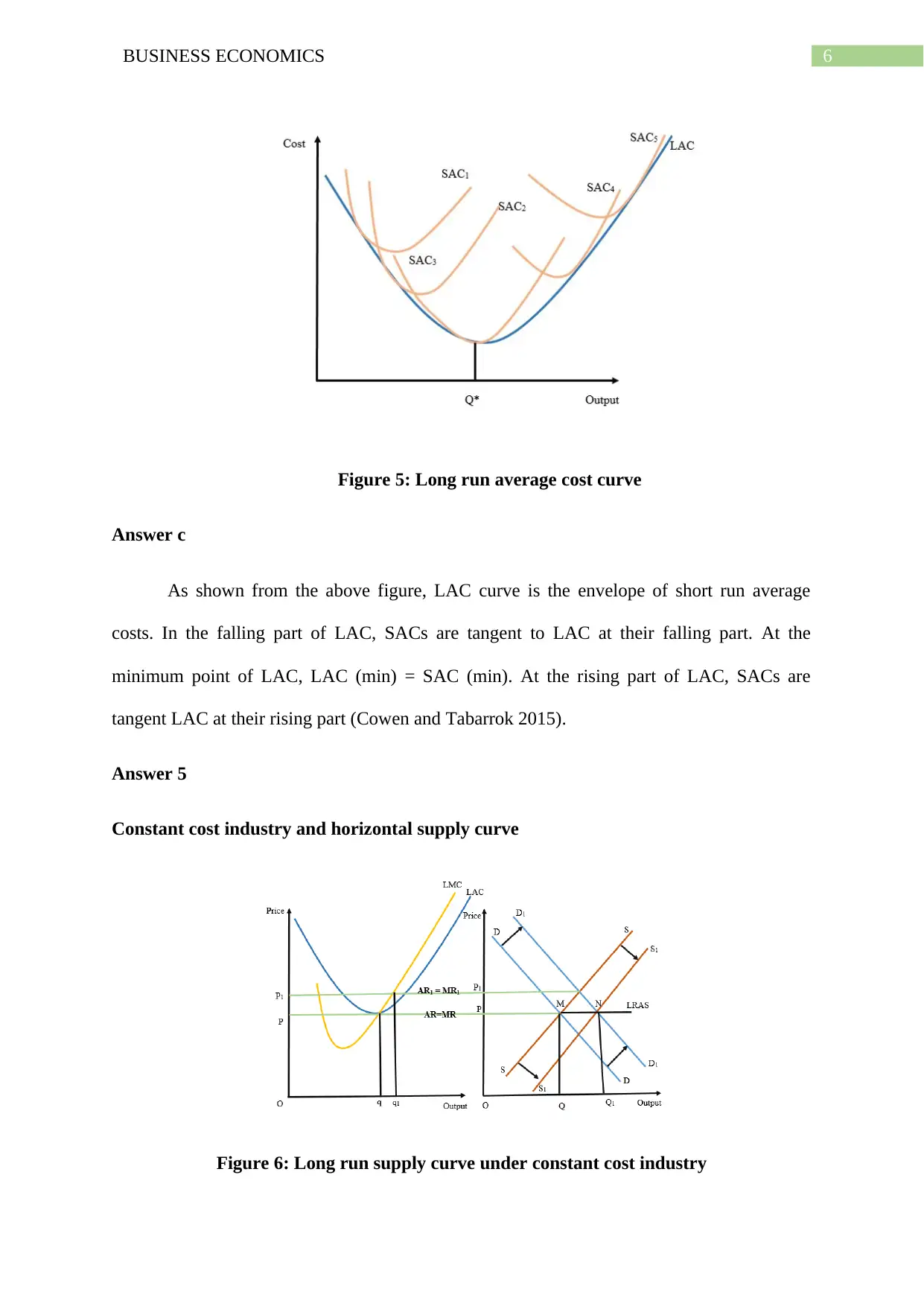

Figure 5: Long run average cost curve

Answer c

As shown from the above figure, LAC curve is the envelope of short run average

costs. In the falling part of LAC, SACs are tangent to LAC at their falling part. At the

minimum point of LAC, LAC (min) = SAC (min). At the rising part of LAC, SACs are

tangent LAC at their rising part (Cowen and Tabarrok 2015).

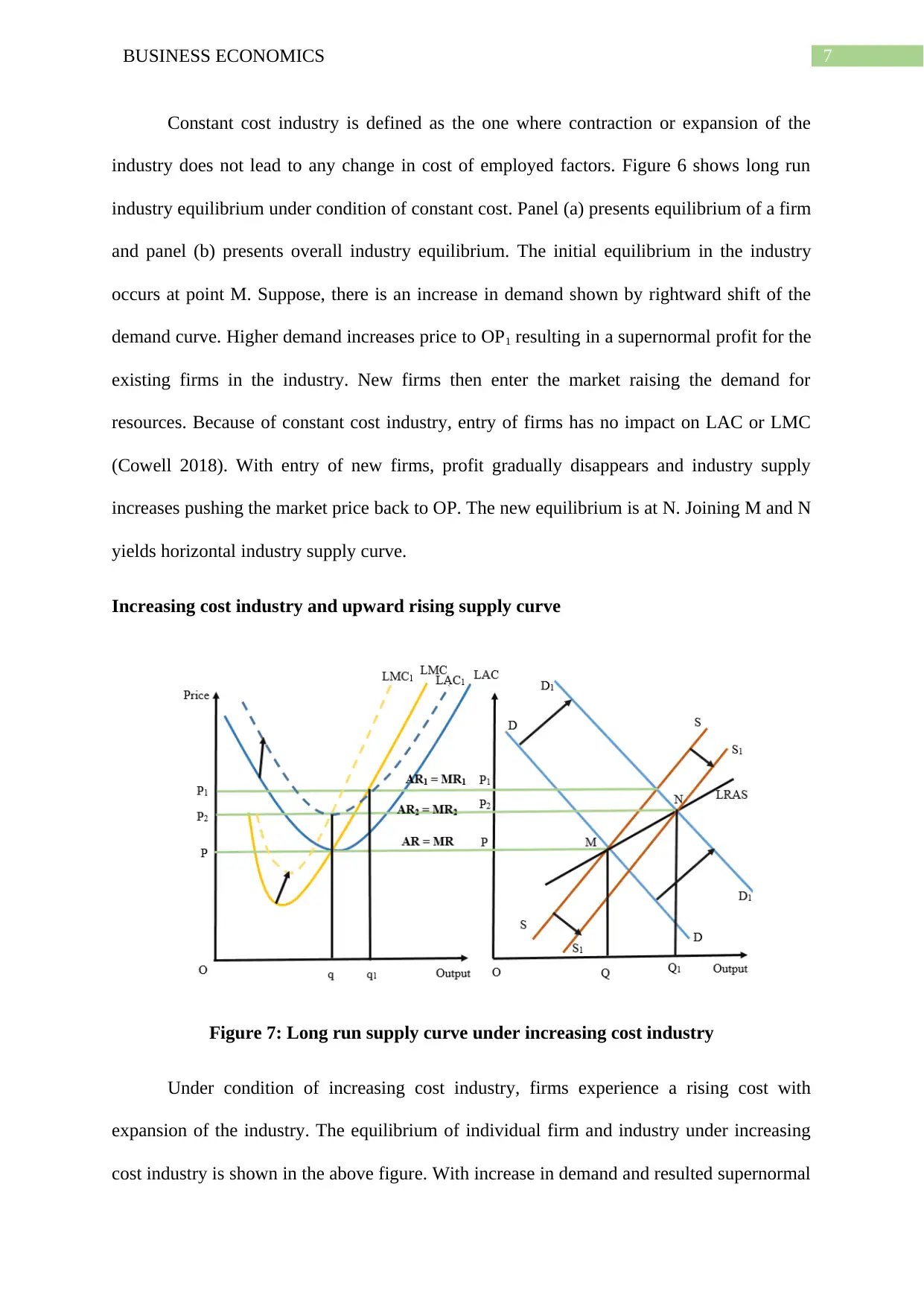

Answer 5

Constant cost industry and horizontal supply curve

Figure 6: Long run supply curve under constant cost industry

Figure 5: Long run average cost curve

Answer c

As shown from the above figure, LAC curve is the envelope of short run average

costs. In the falling part of LAC, SACs are tangent to LAC at their falling part. At the

minimum point of LAC, LAC (min) = SAC (min). At the rising part of LAC, SACs are

tangent LAC at their rising part (Cowen and Tabarrok 2015).

Answer 5

Constant cost industry and horizontal supply curve

Figure 6: Long run supply curve under constant cost industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ECONOMICS

Constant cost industry is defined as the one where contraction or expansion of the

industry does not lead to any change in cost of employed factors. Figure 6 shows long run

industry equilibrium under condition of constant cost. Panel (a) presents equilibrium of a firm

and panel (b) presents overall industry equilibrium. The initial equilibrium in the industry

occurs at point M. Suppose, there is an increase in demand shown by rightward shift of the

demand curve. Higher demand increases price to OP1 resulting in a supernormal profit for the

existing firms in the industry. New firms then enter the market raising the demand for

resources. Because of constant cost industry, entry of firms has no impact on LAC or LMC

(Cowell 2018). With entry of new firms, profit gradually disappears and industry supply

increases pushing the market price back to OP. The new equilibrium is at N. Joining M and N

yields horizontal industry supply curve.

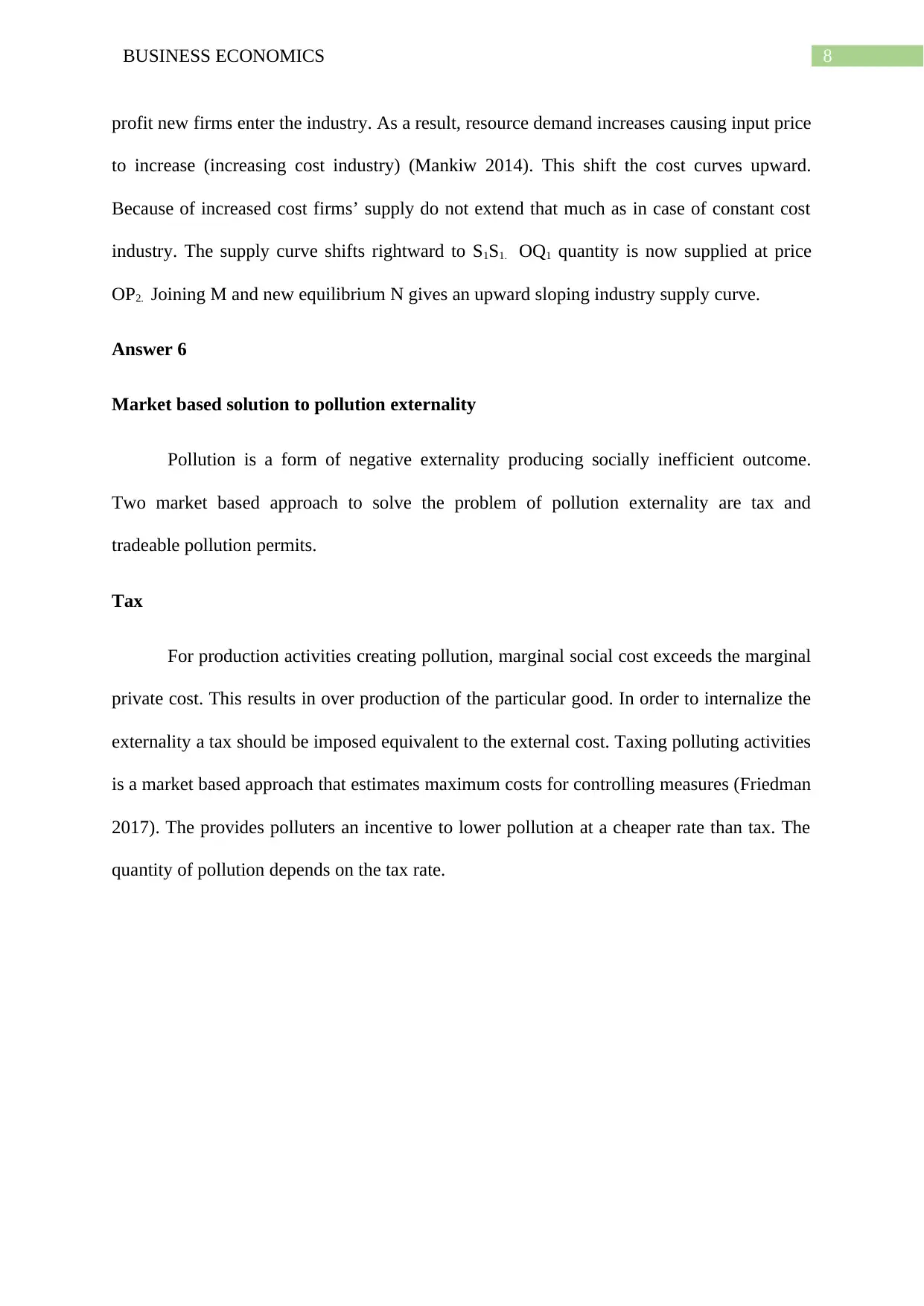

Increasing cost industry and upward rising supply curve

Figure 7: Long run supply curve under increasing cost industry

Under condition of increasing cost industry, firms experience a rising cost with

expansion of the industry. The equilibrium of individual firm and industry under increasing

cost industry is shown in the above figure. With increase in demand and resulted supernormal

Constant cost industry is defined as the one where contraction or expansion of the

industry does not lead to any change in cost of employed factors. Figure 6 shows long run

industry equilibrium under condition of constant cost. Panel (a) presents equilibrium of a firm

and panel (b) presents overall industry equilibrium. The initial equilibrium in the industry

occurs at point M. Suppose, there is an increase in demand shown by rightward shift of the

demand curve. Higher demand increases price to OP1 resulting in a supernormal profit for the

existing firms in the industry. New firms then enter the market raising the demand for

resources. Because of constant cost industry, entry of firms has no impact on LAC or LMC

(Cowell 2018). With entry of new firms, profit gradually disappears and industry supply

increases pushing the market price back to OP. The new equilibrium is at N. Joining M and N

yields horizontal industry supply curve.

Increasing cost industry and upward rising supply curve

Figure 7: Long run supply curve under increasing cost industry

Under condition of increasing cost industry, firms experience a rising cost with

expansion of the industry. The equilibrium of individual firm and industry under increasing

cost industry is shown in the above figure. With increase in demand and resulted supernormal

8BUSINESS ECONOMICS

profit new firms enter the industry. As a result, resource demand increases causing input price

to increase (increasing cost industry) (Mankiw 2014). This shift the cost curves upward.

Because of increased cost firms’ supply do not extend that much as in case of constant cost

industry. The supply curve shifts rightward to S1S1. OQ1 quantity is now supplied at price

OP2. Joining M and new equilibrium N gives an upward sloping industry supply curve.

Answer 6

Market based solution to pollution externality

Pollution is a form of negative externality producing socially inefficient outcome.

Two market based approach to solve the problem of pollution externality are tax and

tradeable pollution permits.

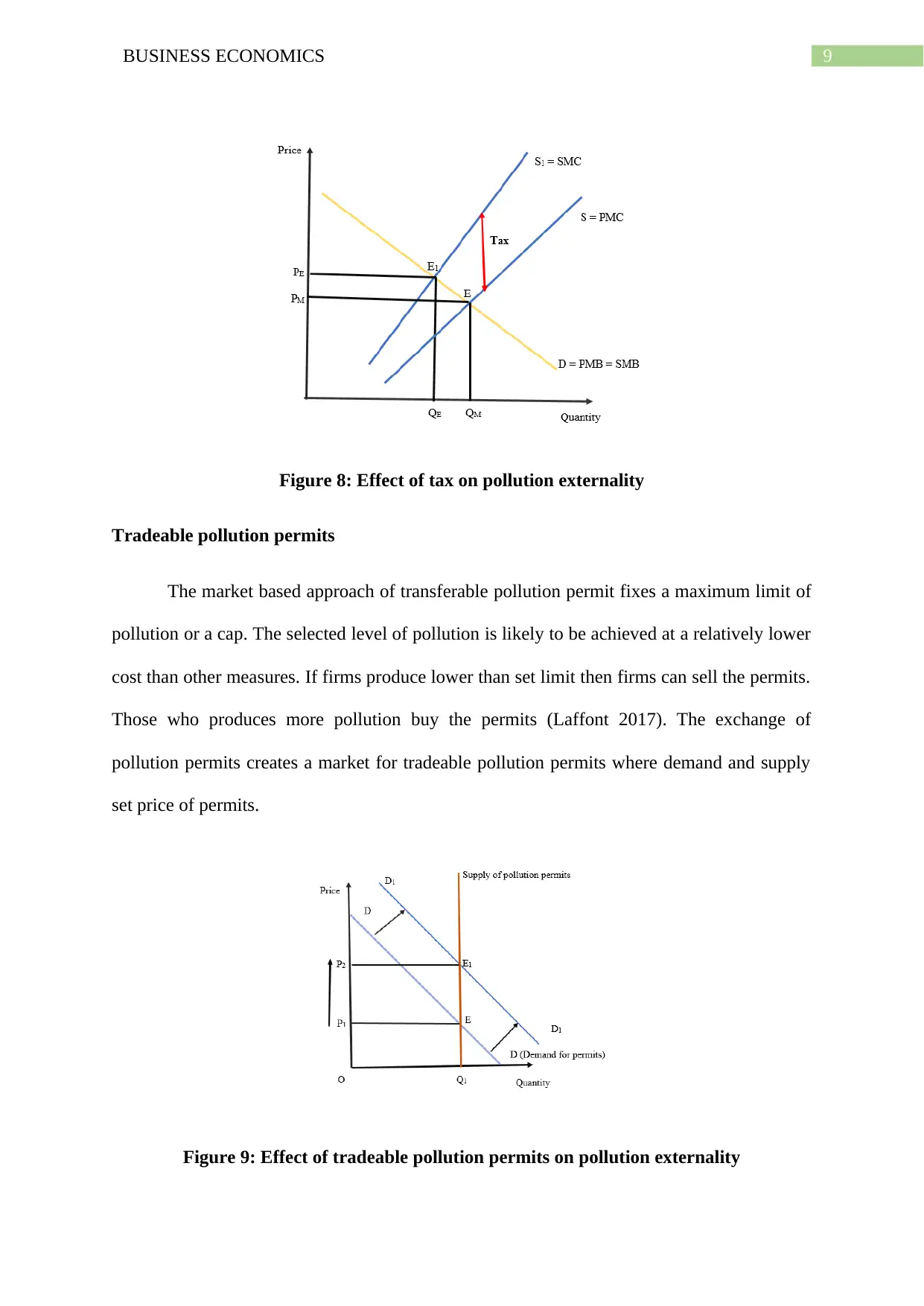

Tax

For production activities creating pollution, marginal social cost exceeds the marginal

private cost. This results in over production of the particular good. In order to internalize the

externality a tax should be imposed equivalent to the external cost. Taxing polluting activities

is a market based approach that estimates maximum costs for controlling measures (Friedman

2017). The provides polluters an incentive to lower pollution at a cheaper rate than tax. The

quantity of pollution depends on the tax rate.

profit new firms enter the industry. As a result, resource demand increases causing input price

to increase (increasing cost industry) (Mankiw 2014). This shift the cost curves upward.

Because of increased cost firms’ supply do not extend that much as in case of constant cost

industry. The supply curve shifts rightward to S1S1. OQ1 quantity is now supplied at price

OP2. Joining M and new equilibrium N gives an upward sloping industry supply curve.

Answer 6

Market based solution to pollution externality

Pollution is a form of negative externality producing socially inefficient outcome.

Two market based approach to solve the problem of pollution externality are tax and

tradeable pollution permits.

Tax

For production activities creating pollution, marginal social cost exceeds the marginal

private cost. This results in over production of the particular good. In order to internalize the

externality a tax should be imposed equivalent to the external cost. Taxing polluting activities

is a market based approach that estimates maximum costs for controlling measures (Friedman

2017). The provides polluters an incentive to lower pollution at a cheaper rate than tax. The

quantity of pollution depends on the tax rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS ECONOMICS

Figure 8: Effect of tax on pollution externality

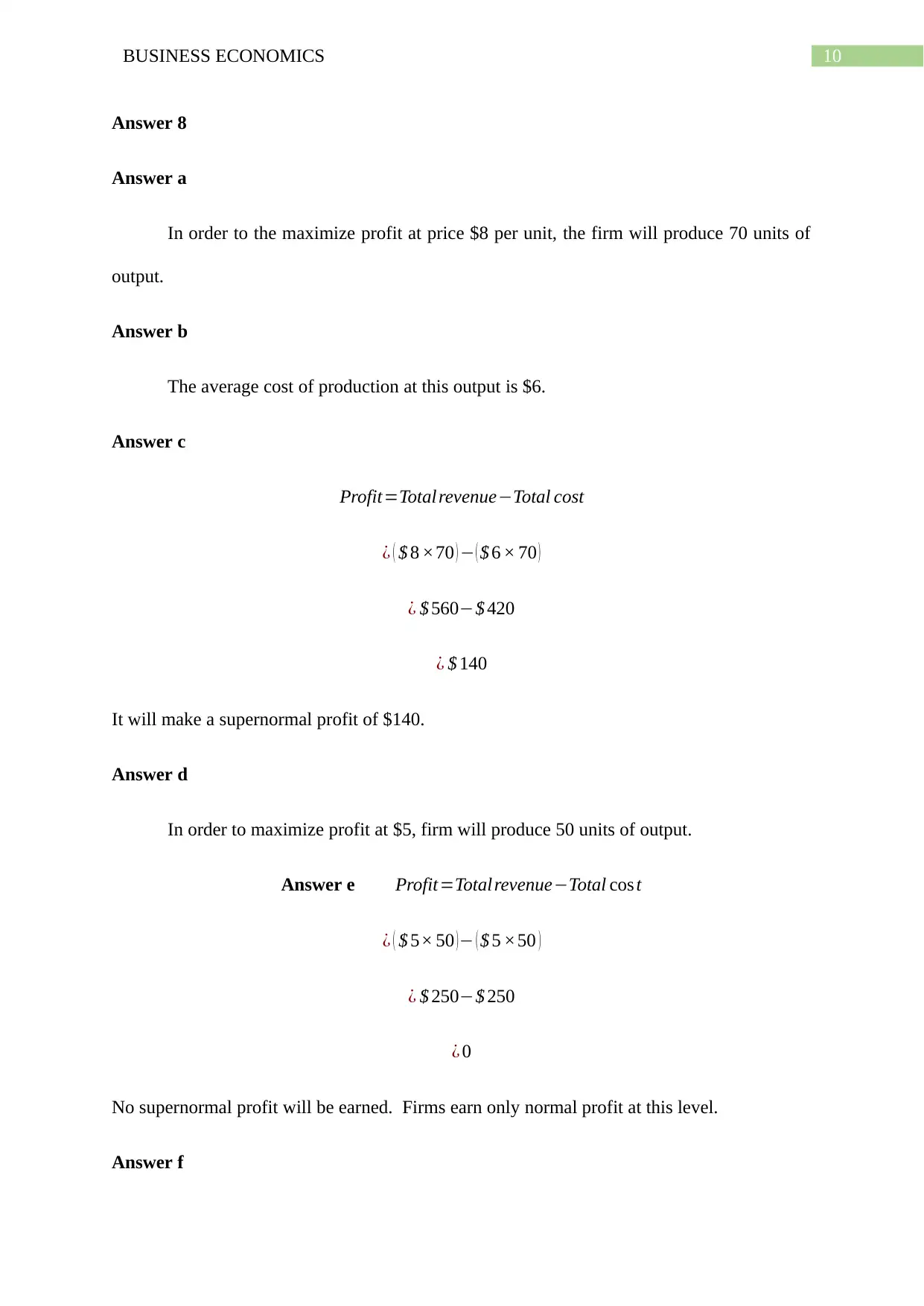

Tradeable pollution permits

The market based approach of transferable pollution permit fixes a maximum limit of

pollution or a cap. The selected level of pollution is likely to be achieved at a relatively lower

cost than other measures. If firms produce lower than set limit then firms can sell the permits.

Those who produces more pollution buy the permits (Laffont 2017). The exchange of

pollution permits creates a market for tradeable pollution permits where demand and supply

set price of permits.

Figure 9: Effect of tradeable pollution permits on pollution externality

Figure 8: Effect of tax on pollution externality

Tradeable pollution permits

The market based approach of transferable pollution permit fixes a maximum limit of

pollution or a cap. The selected level of pollution is likely to be achieved at a relatively lower

cost than other measures. If firms produce lower than set limit then firms can sell the permits.

Those who produces more pollution buy the permits (Laffont 2017). The exchange of

pollution permits creates a market for tradeable pollution permits where demand and supply

set price of permits.

Figure 9: Effect of tradeable pollution permits on pollution externality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS ECONOMICS

Answer 8

Answer a

In order to the maximize profit at price $8 per unit, the firm will produce 70 units of

output.

Answer b

The average cost of production at this output is $6.

Answer c

Profit=Total revenue−Total cost

¿ ( $ 8 ×70 ) − ( $ 6 × 70 )

¿ $ 560−$ 420

¿ $ 140

It will make a supernormal profit of $140.

Answer d

In order to maximize profit at $5, firm will produce 50 units of output.

Answer e Profit=Total revenue−Total cos t

¿ ( $ 5× 50 )− ( $ 5 ×50 )

¿ $ 250−$ 250

¿ 0

No supernormal profit will be earned. Firms earn only normal profit at this level.

Answer f

Answer 8

Answer a

In order to the maximize profit at price $8 per unit, the firm will produce 70 units of

output.

Answer b

The average cost of production at this output is $6.

Answer c

Profit=Total revenue−Total cost

¿ ( $ 8 ×70 ) − ( $ 6 × 70 )

¿ $ 560−$ 420

¿ $ 140

It will make a supernormal profit of $140.

Answer d

In order to maximize profit at $5, firm will produce 50 units of output.

Answer e Profit=Total revenue−Total cos t

¿ ( $ 5× 50 )− ( $ 5 ×50 )

¿ $ 250−$ 250

¿ 0

No supernormal profit will be earned. Firms earn only normal profit at this level.

Answer f

11BUSINESS ECONOMICS

In order to maximize profit at $4, firm will produce 40 units of output.

Answer g

Profit=Total revenue−Total cost

¿ ( $ 4 × 40 )− ( $ 5.5× 40 )

¿ $ 160−$ 220

¿−$ 60

As price is below the average cost firm earns no profit. Rather it suffers a loss of $60.

Answer h

Shut down point in the short run is at minimum of average variable cost. In the short run, firm

should shut down at price below $3.5.

Answer i

Shut down point in the long run is at minimum of average cost (Cowell 2018). In the

long run, firm should shut down at price below $5.

In order to maximize profit at $4, firm will produce 40 units of output.

Answer g

Profit=Total revenue−Total cost

¿ ( $ 4 × 40 )− ( $ 5.5× 40 )

¿ $ 160−$ 220

¿−$ 60

As price is below the average cost firm earns no profit. Rather it suffers a loss of $60.

Answer h

Shut down point in the short run is at minimum of average variable cost. In the short run, firm

should shut down at price below $3.5.

Answer i

Shut down point in the long run is at minimum of average cost (Cowell 2018). In the

long run, firm should shut down at price below $5.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.