Economics Assignment: Market Structures, Elasticity, and Policy

VerifiedAdded on 2020/03/16

|28

|4338

|142

Homework Assignment

AI Summary

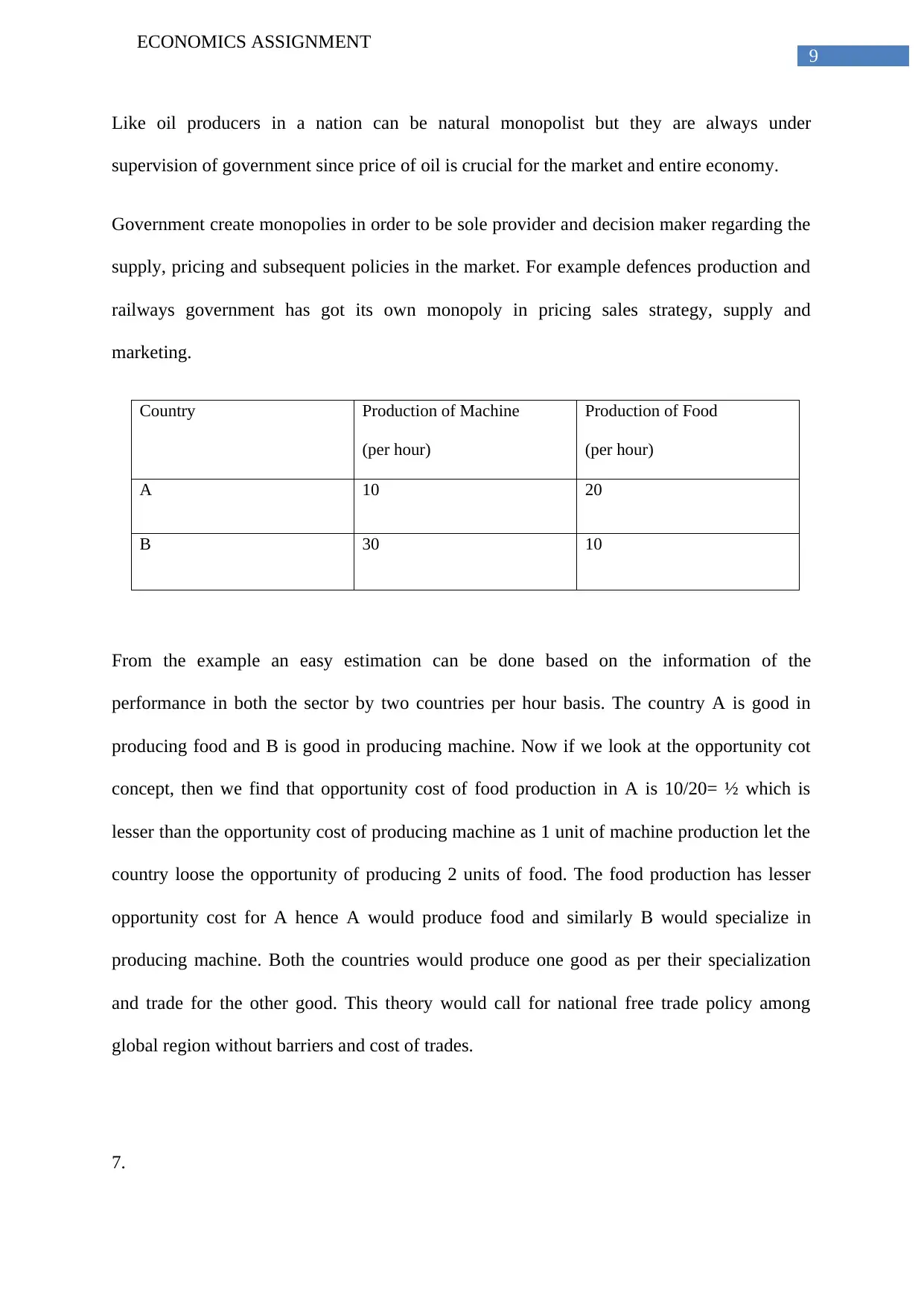

This economics assignment provides a detailed analysis of various economic concepts. It begins with calculations related to perfect competition, including total revenue, marginal cost, and profit maximization. The assignment then delves into market equilibrium, elasticity of demand, and the effects of taxation on consumer and producer surplus, including deadweight loss. Further, it explores the characteristics of different market structures, such as perfect competition and monopolies, along with government interventions. The assignment also covers comparative advantage and international trade, the impact of government monetary policy through open market operations, and the effects of deflation and inflation. Finally, it includes an analysis of game theory, specifically the Nash equilibrium, in the context of a prisoner's dilemma.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.