Economics 3307: Money and Banking Assignment, Summer 2018

VerifiedAdded on 2023/06/09

|9

|1959

|235

Homework Assignment

AI Summary

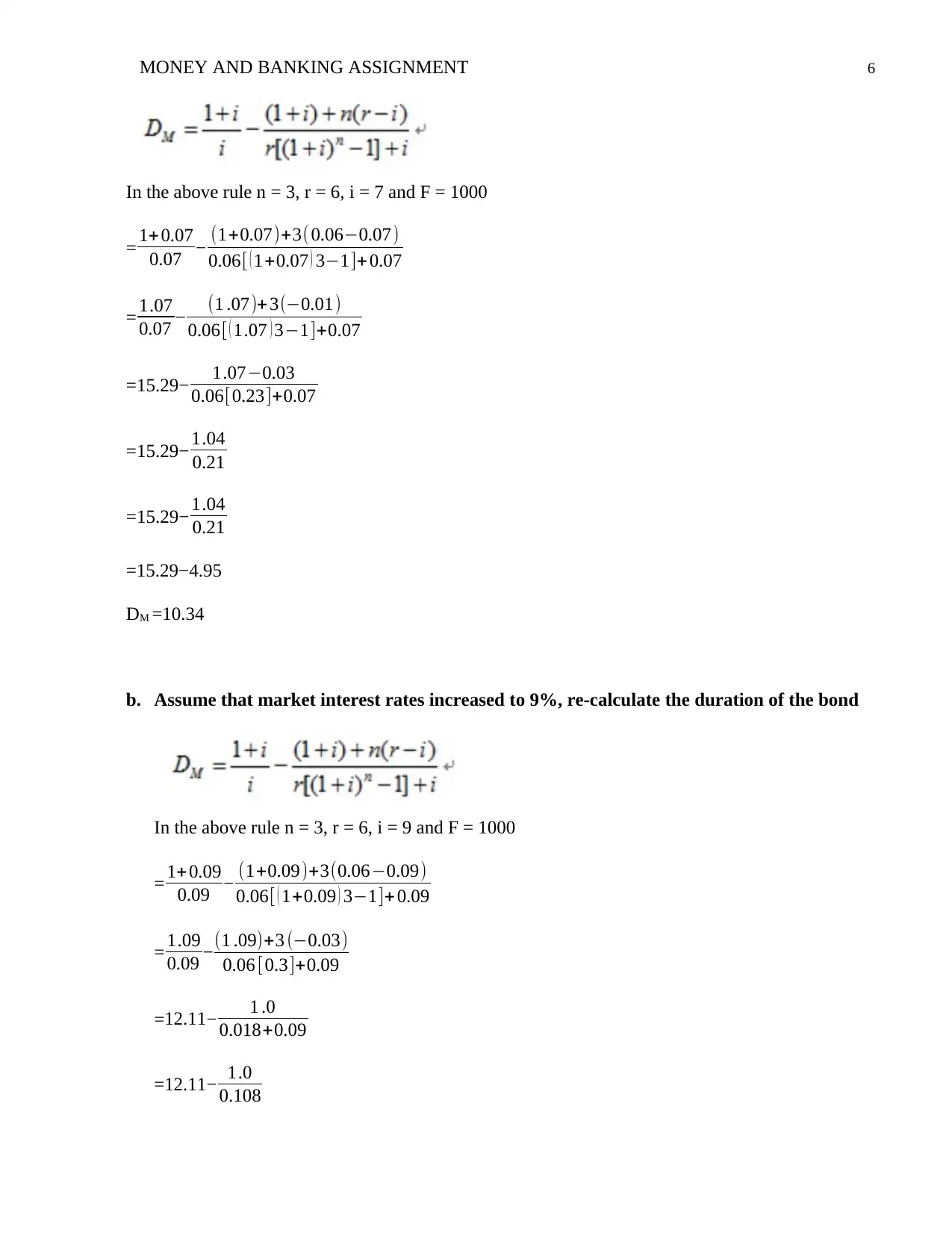

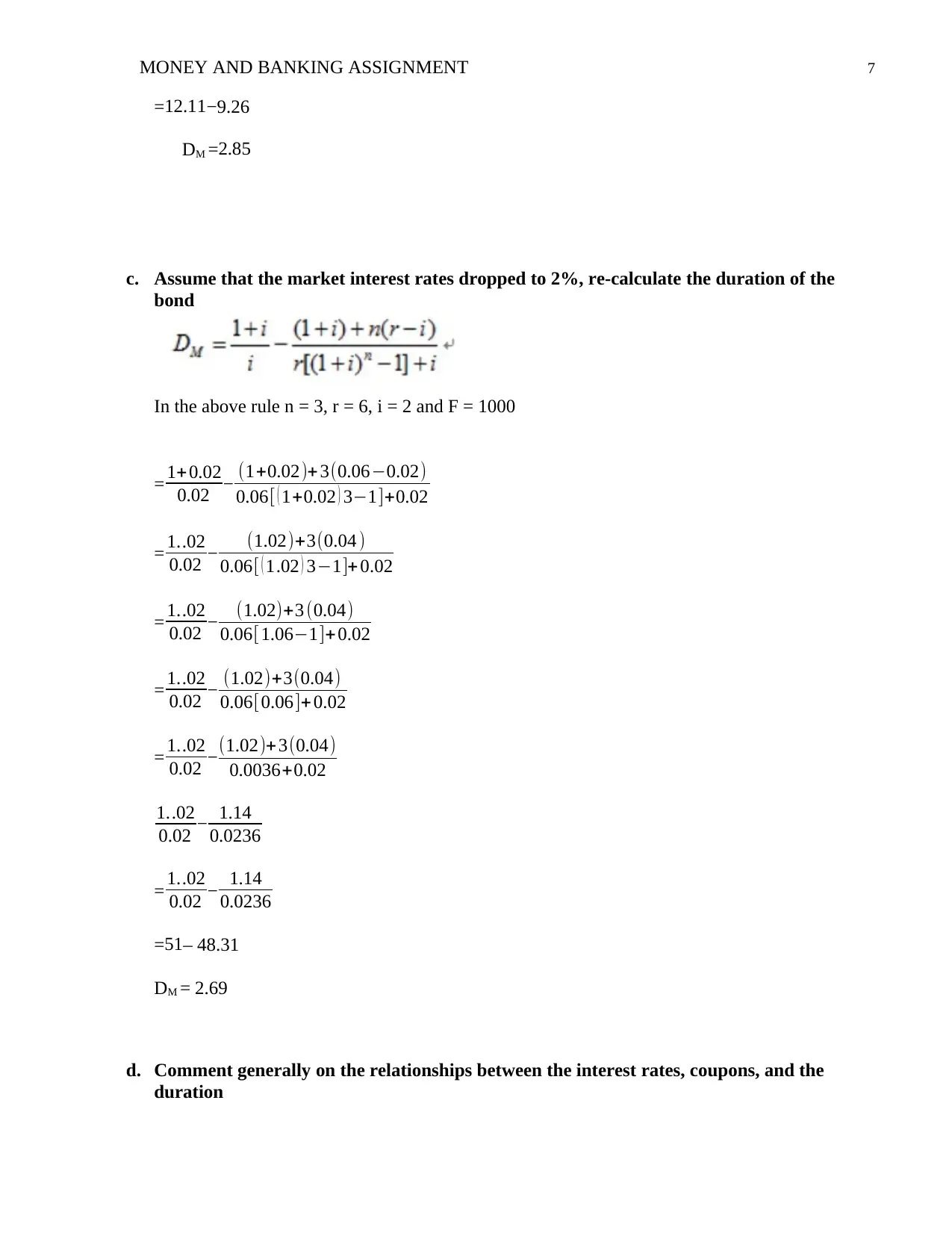

This document presents a comprehensive solution to a Money and Banking assignment, covering key concepts in finance. The assignment begins with an analysis of coupon bonds, requiring the calculation of current yields for various Canadian bonds and a comparison with yield to maturity. The next section delves into the term structure of interest rates, utilizing the yieldcurve.com website to examine upward and inverted yield curves, and discusses the implications of the term structure theories. The assignment also explores bond duration, calculating it under different market interest rate scenarios and analyzing the relationships between interest rates, coupons, and duration. Finally, it includes a critical evaluation of a financial advisor's advice on long-term bond investments. The student provides calculations, graphs, and explanations to support their answers, demonstrating an understanding of bond valuation, interest rate dynamics, and financial market analysis. This assignment is a valuable resource for students studying finance and economics.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.