ECON1000 Introductory Economics Report: Oil Price Analysis

VerifiedAdded on 2022/09/21

|11

|2342

|22

Report

AI Summary

This report, prepared for an introductory economics course, analyzes the dynamics of oil prices using microeconomic principles. It begins with an overview of key concepts such as demand, supply, and price elasticity of demand, explaining their relevance to market analysis. The report then applies these concepts to the context of fluctuating oil prices, discussing how factors like OPEC production, global demand, and the US-China trade war influence the market. It examines the interplay of supply and demand forces, highlighting the impact of inelastic demand for gasoline and diesel on crude oil market dynamics. The report also includes technical details, such as graphical representations of demand and supply curves, and concludes with a discussion of the uncertainties in the oil market and recommendations for market stabilization. The analysis emphasizes the influence of supply-side uncertainties and weak global demand on oil price movements, considering the implications for various economic actors.

Running head: INTRODUCTORY ECONOMICS

Introductory Economics

Name of the Student

Name of the University

Course ID

Introductory Economics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTORY ECONOMICS

Table of Contents

Introduction................................................................................................................................2

Analysis......................................................................................................................................2

Brief explanation of theory related to demand, supply and elasticity....................................2

Application of theory to the article........................................................................................4

Technical details.....................................................................................................................5

Conclusion..................................................................................................................................7

References..................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Analysis......................................................................................................................................2

Brief explanation of theory related to demand, supply and elasticity....................................2

Application of theory to the article........................................................................................4

Technical details.....................................................................................................................5

Conclusion..................................................................................................................................7

References..................................................................................................................................9

2INTRODUCTORY ECONOMICS

Introduction

Microeconomics refers to the branch of economics that studies behavior of individual,

firm or household in the decision making related to resource allocation. The relevant concepts

of microeconomics are applicable to the market for goods and services and address issues

related to individual and single market (Parkin and Bade 2013). The paper analyzes an article

that deals with specific microeconomics concepts of demand, supply and price elasticity of

demand. Demand, supply and associated elasticities are important in explaining workings of

free market. The article deals with a recent hike in oil prices. Globally, fluctuation in oil

prices is one of the most debated topics due to its link with global commodity market. The

weak demand condition has been offset by supply side uncertainties related to oil production

in OPEC and Middle East. The risk of weak global demand and associated elasticity of

gasoline will adversely affect the crude oil market. The movement of oil prices are discussed

using relevant microeconomics concepts.

Analysis

Brief explanation of theory related to demand, supply and elasticity

The concepts of microeconomics that are relevant for the articles are demand, supply

and price elasticity of demand. Each of these concepts has its own importance in the field of

microeconomics. The basic concepts of demand, supply and elasticity are briefly discussed

below.

Demand:

In economic terms, demand simply refers to the quantity of a particular product or

service that people are willing to buy given the ability to purchase given price of the product

in a given period of time. The theory of demand is one of the primary theories of

microeconomics (Baumol and Blinder 2015). It intends to answer some basic question related

Introduction

Microeconomics refers to the branch of economics that studies behavior of individual,

firm or household in the decision making related to resource allocation. The relevant concepts

of microeconomics are applicable to the market for goods and services and address issues

related to individual and single market (Parkin and Bade 2013). The paper analyzes an article

that deals with specific microeconomics concepts of demand, supply and price elasticity of

demand. Demand, supply and associated elasticities are important in explaining workings of

free market. The article deals with a recent hike in oil prices. Globally, fluctuation in oil

prices is one of the most debated topics due to its link with global commodity market. The

weak demand condition has been offset by supply side uncertainties related to oil production

in OPEC and Middle East. The risk of weak global demand and associated elasticity of

gasoline will adversely affect the crude oil market. The movement of oil prices are discussed

using relevant microeconomics concepts.

Analysis

Brief explanation of theory related to demand, supply and elasticity

The concepts of microeconomics that are relevant for the articles are demand, supply

and price elasticity of demand. Each of these concepts has its own importance in the field of

microeconomics. The basic concepts of demand, supply and elasticity are briefly discussed

below.

Demand:

In economic terms, demand simply refers to the quantity of a particular product or

service that people are willing to buy given the ability to purchase given price of the product

in a given period of time. The theory of demand is one of the primary theories of

microeconomics (Baumol and Blinder 2015). It intends to answer some basic question related

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTORY ECONOMICS

to desire of people to buy something and associated change in demand because of the change

in income levels and level of satisfaction. The relation between quantities demanded and own

price of a good is explained in the law of demand. The law portraits an inverse relation

between own price and demand. That means, given all the factors affecting demand, demand

of a good moves in the opposite direction of price. Apart from own price, other factors

affecting demand include income, tastes and preferences, price of related goods and others.

Supply:

Associated with demand, another important force determining market equilibrium is

supply. Supply refers to the quantity of a particular product or service that producers are

willing and at the same time able to supply at a specific price. The law of supply captures the

relation between price of a good and its supply. Given all other factors determining supply,

there exists a direct relation between price and quantity supplied of a good that is quantity

supplied increases with increase in price and vice versa (Cowen and Tabarrok 2015). Factors

other than price affecting supply of a product are production cost, natural condition, transport

condition, technology, input prices and availability of inputs, price of substitutes and

complements, policies of government and others.

Price elasticity of demand:

Price elasticity of demand relates relative responsiveness of quantity demanded with

respect to certain percentage change in own price of the product. Elasticity of demand with

respect to own price plays an important role in determining price because of its impact on

revenue of a firm. When change in demand is proportionately greater than the change in price

then demand is considered as relatively elastic. Under such condition a decline in price

increases revenue by increasing demand by a large amount (Nicholson and Snyder 2014). If

change in demand is proportionately less than price change then demand is considered as

to desire of people to buy something and associated change in demand because of the change

in income levels and level of satisfaction. The relation between quantities demanded and own

price of a good is explained in the law of demand. The law portraits an inverse relation

between own price and demand. That means, given all the factors affecting demand, demand

of a good moves in the opposite direction of price. Apart from own price, other factors

affecting demand include income, tastes and preferences, price of related goods and others.

Supply:

Associated with demand, another important force determining market equilibrium is

supply. Supply refers to the quantity of a particular product or service that producers are

willing and at the same time able to supply at a specific price. The law of supply captures the

relation between price of a good and its supply. Given all other factors determining supply,

there exists a direct relation between price and quantity supplied of a good that is quantity

supplied increases with increase in price and vice versa (Cowen and Tabarrok 2015). Factors

other than price affecting supply of a product are production cost, natural condition, transport

condition, technology, input prices and availability of inputs, price of substitutes and

complements, policies of government and others.

Price elasticity of demand:

Price elasticity of demand relates relative responsiveness of quantity demanded with

respect to certain percentage change in own price of the product. Elasticity of demand with

respect to own price plays an important role in determining price because of its impact on

revenue of a firm. When change in demand is proportionately greater than the change in price

then demand is considered as relatively elastic. Under such condition a decline in price

increases revenue by increasing demand by a large amount (Nicholson and Snyder 2014). If

change in demand is proportionately less than price change then demand is considered as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTORY ECONOMICS

relatively inelastic. Increasing price in this case is beneficial for firm as decline in volume of

sales is more than offset by a larger increase in price.

Application of theory to the article

The article named “Oil price settle higher for the day and the week” describes the

recent increase in oil price. Price of a commodity is generally determined by the combined

forces of demand and supply. In case of oil, demand for oil constitutes a weak trend. Decline

in demand for oil tends to decline price of oil. However, as suggested by the analysts weak

demand is more than offset by the uncertainties related to supply. The interruption in supply

of oil has been resulted from production glut in OPEC and oil producers in Middle East

nations (Saefong and Watts 2019). The supply side interruption results in a shortage of oil in

the market. The resulting shortage of oil offsets downward pressure on price and increases

price accordingly. With a continuous decline in oil demand, there still remains a threat of

decline in long term prices of oil.

At present, there is a recorded increase in price of oil in US because of dominance of

supply side forces. In West Texas, price of intermediate crude oil rose by 0.11 percent to

become 40 cents or increased by 0.7 percent for settling at $54.87 barrel which traded as high

as at a price of $55.67(Saefong and Watts 2019). The price of Brent crude oil prices recorded

another 0.7 percent increase in price and became $58.64 per barrel. The increasing trend in

crude oil price shows the dominance of supply side uncertainties over the weak demand

condition.

The demand and supply dynamics of oil can be described as follows. Regarding the

demand oil, the Organization of Petroleum Exporting Countries forecast a decline in global

demand of oil by nearly 40,000 barrel per day reaching the demand to 1.1 million barrels a

day (Saefong and Watts 2019). The forecasted oil demand in 2020 remained unchanged at

relatively inelastic. Increasing price in this case is beneficial for firm as decline in volume of

sales is more than offset by a larger increase in price.

Application of theory to the article

The article named “Oil price settle higher for the day and the week” describes the

recent increase in oil price. Price of a commodity is generally determined by the combined

forces of demand and supply. In case of oil, demand for oil constitutes a weak trend. Decline

in demand for oil tends to decline price of oil. However, as suggested by the analysts weak

demand is more than offset by the uncertainties related to supply. The interruption in supply

of oil has been resulted from production glut in OPEC and oil producers in Middle East

nations (Saefong and Watts 2019). The supply side interruption results in a shortage of oil in

the market. The resulting shortage of oil offsets downward pressure on price and increases

price accordingly. With a continuous decline in oil demand, there still remains a threat of

decline in long term prices of oil.

At present, there is a recorded increase in price of oil in US because of dominance of

supply side forces. In West Texas, price of intermediate crude oil rose by 0.11 percent to

become 40 cents or increased by 0.7 percent for settling at $54.87 barrel which traded as high

as at a price of $55.67(Saefong and Watts 2019). The price of Brent crude oil prices recorded

another 0.7 percent increase in price and became $58.64 per barrel. The increasing trend in

crude oil price shows the dominance of supply side uncertainties over the weak demand

condition.

The demand and supply dynamics of oil can be described as follows. Regarding the

demand oil, the Organization of Petroleum Exporting Countries forecast a decline in global

demand of oil by nearly 40,000 barrel per day reaching the demand to 1.1 million barrels a

day (Saefong and Watts 2019). The forecasted oil demand in 2020 remained unchanged at

5INTRODUCTORY ECONOMICS

1.14 million barrel per day. So far as supply is concerned OPEC currently cut its outlook for

growth in oil supply from non-OPEC countries. The demand and supply forces thus likely to

move future oil prices in opposite direction. A decline in global demand means a decline in

oil price (Kang, de Gracia and Ratti 2019). A fall in growth in oil supply in contrast means an

increase in price due to shortage of supply in order to meet existing demand.

The broad picture of the global economy indicates that the economy will continue to

struggle in 2020 with a weak confidence among many global players. The weak condition of

global economy is further attributed from the on-going trade escalation between China and

US (Liu and Woo 2018). In response to imposed tariff on China’s import by President

Trump, China has taken retaliatory measures in the form of imposing equivalent amount of

tariff on import from US. This has deepen the trade disputes between two nations adversely

affecting the global economy (Tankersley and Bradsher 2018).

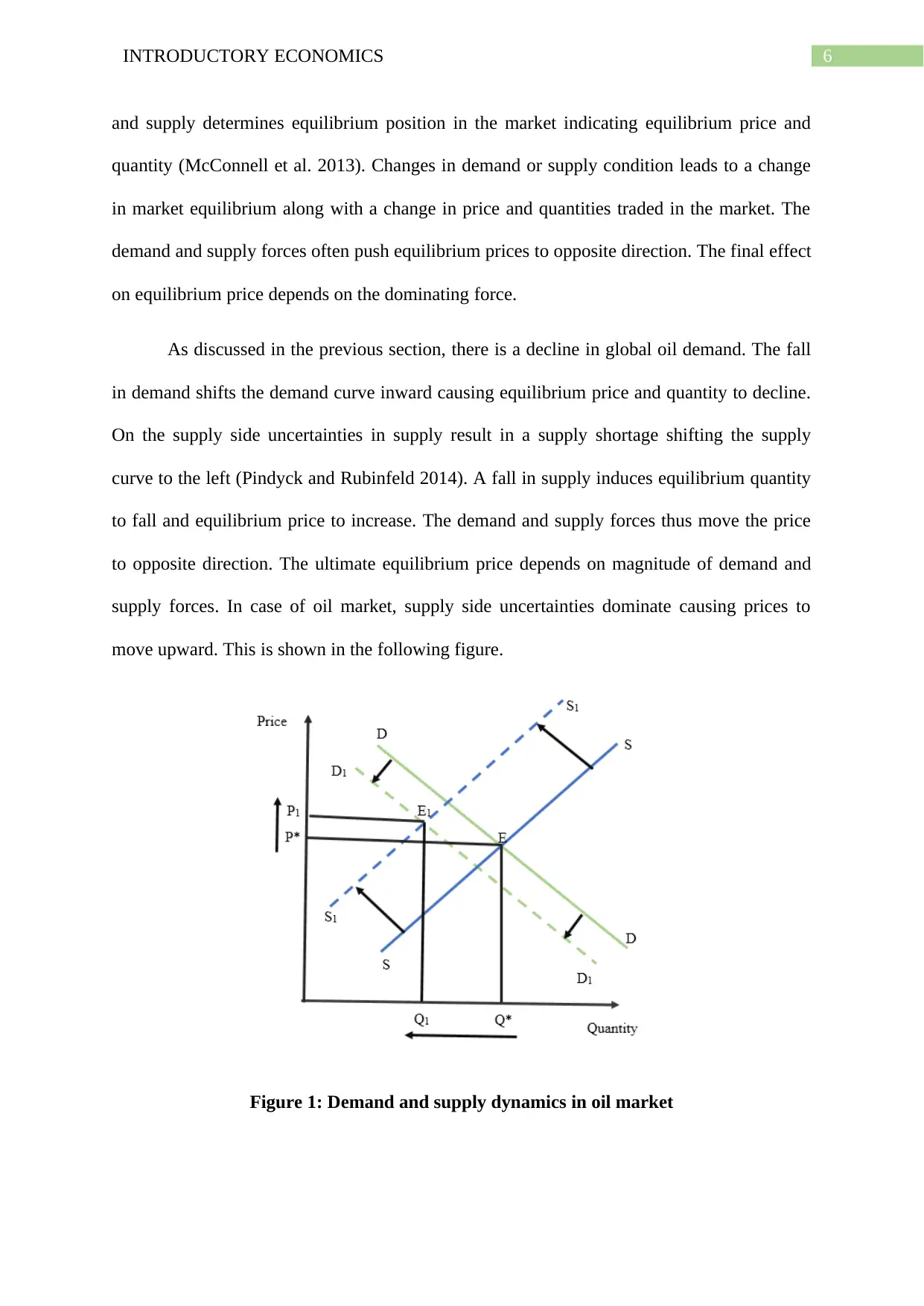

Another concern related to market of crude oil market is related to elasticity of

products such as gasoline and diesel. These products have relatively lower elasticity of

demand (Clemente 2019). Therefore, a decline in price would not increase demand much

resulting in a decline in revenue of sellers. The market of crude oil as a complementary

products of gasoline and diesel will face an adverse consequence of weak demand condition.

Most of the emerging markets again heavily rely on crude oil for their future growth. Supply

side glut of crude oil again hamper economic growth of these nations (Thorbecke 2019). Data

suggests that price of oil increased by more than 4 percent while supply rose lesser than that

expected indicating a relatively inelastic supply.

Technical details

The demand and supply side factors as discussed in the articles can be explained with

the aid of appropriate microeconomic theory. In a free market independent forces of demand

1.14 million barrel per day. So far as supply is concerned OPEC currently cut its outlook for

growth in oil supply from non-OPEC countries. The demand and supply forces thus likely to

move future oil prices in opposite direction. A decline in global demand means a decline in

oil price (Kang, de Gracia and Ratti 2019). A fall in growth in oil supply in contrast means an

increase in price due to shortage of supply in order to meet existing demand.

The broad picture of the global economy indicates that the economy will continue to

struggle in 2020 with a weak confidence among many global players. The weak condition of

global economy is further attributed from the on-going trade escalation between China and

US (Liu and Woo 2018). In response to imposed tariff on China’s import by President

Trump, China has taken retaliatory measures in the form of imposing equivalent amount of

tariff on import from US. This has deepen the trade disputes between two nations adversely

affecting the global economy (Tankersley and Bradsher 2018).

Another concern related to market of crude oil market is related to elasticity of

products such as gasoline and diesel. These products have relatively lower elasticity of

demand (Clemente 2019). Therefore, a decline in price would not increase demand much

resulting in a decline in revenue of sellers. The market of crude oil as a complementary

products of gasoline and diesel will face an adverse consequence of weak demand condition.

Most of the emerging markets again heavily rely on crude oil for their future growth. Supply

side glut of crude oil again hamper economic growth of these nations (Thorbecke 2019). Data

suggests that price of oil increased by more than 4 percent while supply rose lesser than that

expected indicating a relatively inelastic supply.

Technical details

The demand and supply side factors as discussed in the articles can be explained with

the aid of appropriate microeconomic theory. In a free market independent forces of demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTORY ECONOMICS

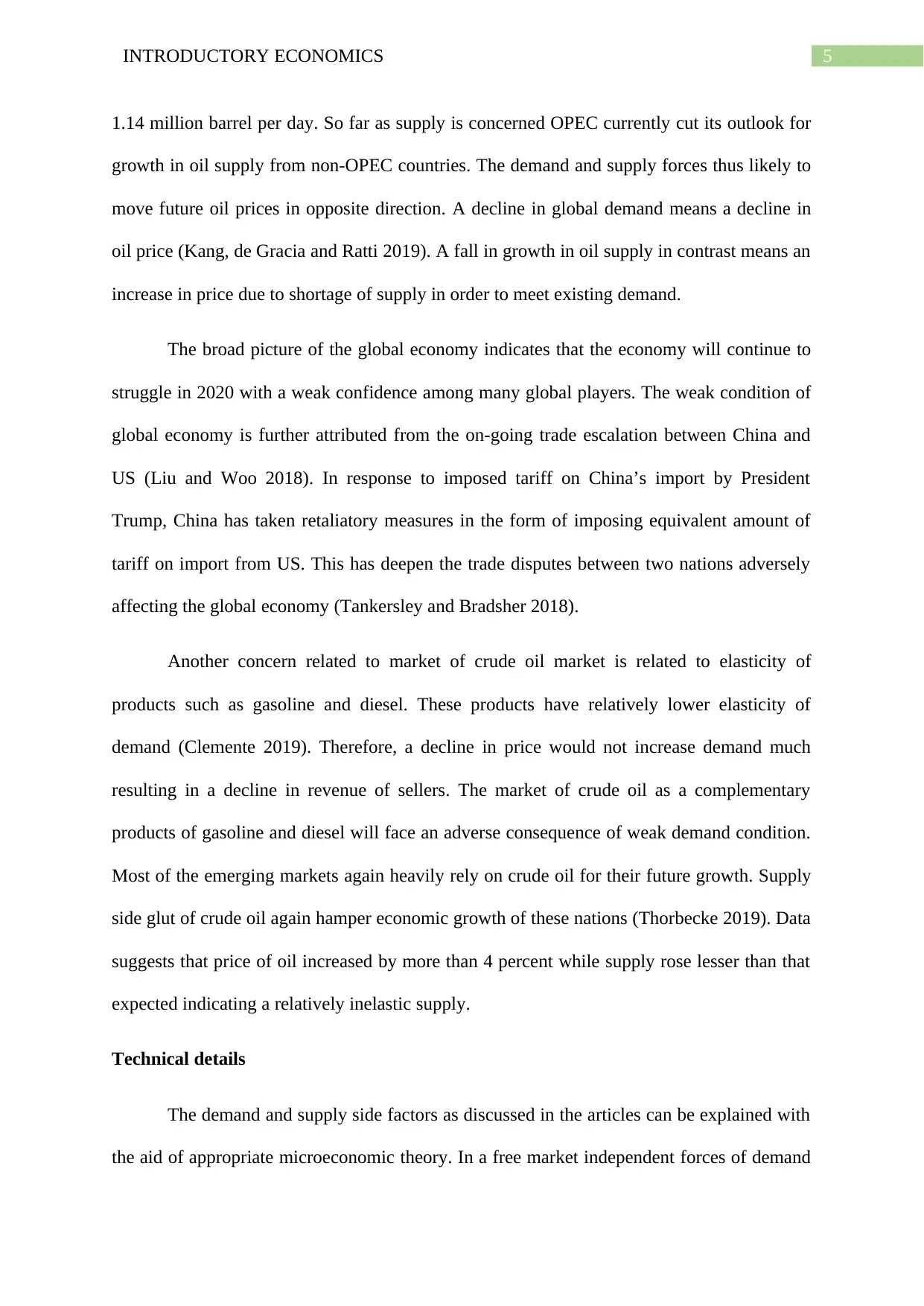

and supply determines equilibrium position in the market indicating equilibrium price and

quantity (McConnell et al. 2013). Changes in demand or supply condition leads to a change

in market equilibrium along with a change in price and quantities traded in the market. The

demand and supply forces often push equilibrium prices to opposite direction. The final effect

on equilibrium price depends on the dominating force.

As discussed in the previous section, there is a decline in global oil demand. The fall

in demand shifts the demand curve inward causing equilibrium price and quantity to decline.

On the supply side uncertainties in supply result in a supply shortage shifting the supply

curve to the left (Pindyck and Rubinfeld 2014). A fall in supply induces equilibrium quantity

to fall and equilibrium price to increase. The demand and supply forces thus move the price

to opposite direction. The ultimate equilibrium price depends on magnitude of demand and

supply forces. In case of oil market, supply side uncertainties dominate causing prices to

move upward. This is shown in the following figure.

Figure 1: Demand and supply dynamics in oil market

and supply determines equilibrium position in the market indicating equilibrium price and

quantity (McConnell et al. 2013). Changes in demand or supply condition leads to a change

in market equilibrium along with a change in price and quantities traded in the market. The

demand and supply forces often push equilibrium prices to opposite direction. The final effect

on equilibrium price depends on the dominating force.

As discussed in the previous section, there is a decline in global oil demand. The fall

in demand shifts the demand curve inward causing equilibrium price and quantity to decline.

On the supply side uncertainties in supply result in a supply shortage shifting the supply

curve to the left (Pindyck and Rubinfeld 2014). A fall in supply induces equilibrium quantity

to fall and equilibrium price to increase. The demand and supply forces thus move the price

to opposite direction. The ultimate equilibrium price depends on magnitude of demand and

supply forces. In case of oil market, supply side uncertainties dominate causing prices to

move upward. This is shown in the following figure.

Figure 1: Demand and supply dynamics in oil market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTORY ECONOMICS

The figure above shows demand and supply dynamics related to oil market. As

demand contracts, the demand curve shifts inward to D1D1. The supply side interruption due

to difficulties arising from OPEC and other countries in Middle East, supply contracts

shifting the supply curve inward to S1S1. As the magnitude of contraction in supply is greater

than the magnitude of demand contraction price ultimately increases to P1 (Mahanty 2014).

Another technical term important for analyzing the future of crude oil market is the

associated elasticity of demand (Nechyba 2016). The low elasticity of demand for gasoline

and diesel further deepens the risk for crude oil market.

Figure 2: Inelastic demand curve for gasoline and diesel

Conclusion

The paper summarizes demand and supply side issues related to fluctuation of oil

prices. On the demand side, a weak demand has been recorded due to slowdown of global

economy. On the supply side supply has been interrupted due to uncertainties related to

OPEC and non-OPEC countries. The dominance of supply side uncertainties explain the

current increase in crude oil prices. Weak global demand however threatened the oil market

The figure above shows demand and supply dynamics related to oil market. As

demand contracts, the demand curve shifts inward to D1D1. The supply side interruption due

to difficulties arising from OPEC and other countries in Middle East, supply contracts

shifting the supply curve inward to S1S1. As the magnitude of contraction in supply is greater

than the magnitude of demand contraction price ultimately increases to P1 (Mahanty 2014).

Another technical term important for analyzing the future of crude oil market is the

associated elasticity of demand (Nechyba 2016). The low elasticity of demand for gasoline

and diesel further deepens the risk for crude oil market.

Figure 2: Inelastic demand curve for gasoline and diesel

Conclusion

The paper summarizes demand and supply side issues related to fluctuation of oil

prices. On the demand side, a weak demand has been recorded due to slowdown of global

economy. On the supply side supply has been interrupted due to uncertainties related to

OPEC and non-OPEC countries. The dominance of supply side uncertainties explain the

current increase in crude oil prices. Weak global demand however threatened the oil market

8INTRODUCTORY ECONOMICS

in future. US-China trade war is one factor that leads to a decline in oil demand by increasing

uncertainties in both the economy. The downside risk in the global market adversely affects

crude oil market because of low elasticity of demand of gasoline and diesels and huge

dependency of emerging markets.

Considering the uncertainties on the demand and supply side and resulting instability

in oil price measures should be taken to stabilize the market. The suppliers should adapt

measures to ensure a smooth supply of oil. OPEC members in particular need to take curbing

policies to balance supply and demand of oil. In order to overcome uncertainties resulted

from US-China trade war both the nation should negotiate on a mutually beneficial trade

agreement. This will help to combat some of the weak demand in coming years.

in future. US-China trade war is one factor that leads to a decline in oil demand by increasing

uncertainties in both the economy. The downside risk in the global market adversely affects

crude oil market because of low elasticity of demand of gasoline and diesels and huge

dependency of emerging markets.

Considering the uncertainties on the demand and supply side and resulting instability

in oil price measures should be taken to stabilize the market. The suppliers should adapt

measures to ensure a smooth supply of oil. OPEC members in particular need to take curbing

policies to balance supply and demand of oil. In order to overcome uncertainties resulted

from US-China trade war both the nation should negotiate on a mutually beneficial trade

agreement. This will help to combat some of the weak demand in coming years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTORY ECONOMICS

References

Baumol, William J., and Alan S. Blinder. Microeconomics: Principles and policy. Nelson

Education, 2015.

Clemente, Jude 2019 "The Link Between Crude Oil And Gasoline Prices".

2019. Forbes.Com. Accessed August 19 2019.

https://www.forbes.com/sites/judeclemente/2018/06/27/the-link-between-crude-oil-and-

gasoline-prices/#70d523cf37db.

Cowen, Tyler, and Alex Tabarrok. Modern principles of microeconomics. Macmillan

International Higher Education, 2015.

Kang, Wensheng, Fernando Perez de Gracia, and Ronald A. Ratti. "The asymmetric response

of gasoline prices to oil price shocks and policy uncertainty." Energy Economics 77 (2019):

66-79.

Liu, Tao, and Wing Thye Woo. "Understanding the US-China trade war." China Economic

Journal 11, no. 3 (2018): 319-340.

Mahanty, Aroop K. Intermediate microeconomics with applications. Academic Press, 2014.

McConnell, Campbell R., Stanley L. Brue, Sean Masaki Flynn, and Randy R.

Grant. Microeconomics: Brief Edition. McGraw-Hill/Irwin, 2013.

Nechyba, Thomas. Microeconomics: an intuitive approach with calculus. Nelson Education,

2016.

Nicholson, Walter, and Christopher M. Snyder. Intermediate microeconomics and its

application. Nelson Education, 2014.

Parkin, Michael, and Robin Bade. Foundations of microeconomics. Pearson, 2013.

References

Baumol, William J., and Alan S. Blinder. Microeconomics: Principles and policy. Nelson

Education, 2015.

Clemente, Jude 2019 "The Link Between Crude Oil And Gasoline Prices".

2019. Forbes.Com. Accessed August 19 2019.

https://www.forbes.com/sites/judeclemente/2018/06/27/the-link-between-crude-oil-and-

gasoline-prices/#70d523cf37db.

Cowen, Tyler, and Alex Tabarrok. Modern principles of microeconomics. Macmillan

International Higher Education, 2015.

Kang, Wensheng, Fernando Perez de Gracia, and Ronald A. Ratti. "The asymmetric response

of gasoline prices to oil price shocks and policy uncertainty." Energy Economics 77 (2019):

66-79.

Liu, Tao, and Wing Thye Woo. "Understanding the US-China trade war." China Economic

Journal 11, no. 3 (2018): 319-340.

Mahanty, Aroop K. Intermediate microeconomics with applications. Academic Press, 2014.

McConnell, Campbell R., Stanley L. Brue, Sean Masaki Flynn, and Randy R.

Grant. Microeconomics: Brief Edition. McGraw-Hill/Irwin, 2013.

Nechyba, Thomas. Microeconomics: an intuitive approach with calculus. Nelson Education,

2016.

Nicholson, Walter, and Christopher M. Snyder. Intermediate microeconomics and its

application. Nelson Education, 2014.

Parkin, Michael, and Robin Bade. Foundations of microeconomics. Pearson, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTRODUCTORY ECONOMICS

Pindyck, Robert, and Daniel Rubinfeld. Microeconomics GE. Pearson Australia Pty Limited,

2014.

Saefong, Myra, and William Watts. 2019. "Oil Prices Settle Higher For The Day And The

Week". Marketwatch. Accessed August 19 2019. https://www.marketwatch.com/story/oil-on-

track-for-weekly-gain-but-trims-rise-after-downbeat-opec-outlook-2019-08-16.

Tankersley, Jim, and Keith Bradsher. "Trump hits China with tariffs on $200 billion in goods,

escalating trade war." New York Times (2018).

Thorbecke, Willem. "Oil Prices and the US Economy: Evidence from the stock

market." Journal of Macroeconomics (2019): 103137.

Pindyck, Robert, and Daniel Rubinfeld. Microeconomics GE. Pearson Australia Pty Limited,

2014.

Saefong, Myra, and William Watts. 2019. "Oil Prices Settle Higher For The Day And The

Week". Marketwatch. Accessed August 19 2019. https://www.marketwatch.com/story/oil-on-

track-for-weekly-gain-but-trims-rise-after-downbeat-opec-outlook-2019-08-16.

Tankersley, Jim, and Keith Bradsher. "Trump hits China with tariffs on $200 billion in goods,

escalating trade war." New York Times (2018).

Thorbecke, Willem. "Oil Prices and the US Economy: Evidence from the stock

market." Journal of Macroeconomics (2019): 103137.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.