Economics Assignment: Analyzing Output, Costs, and Market Dynamics

VerifiedAdded on 2021/12/28

|13

|1561

|43

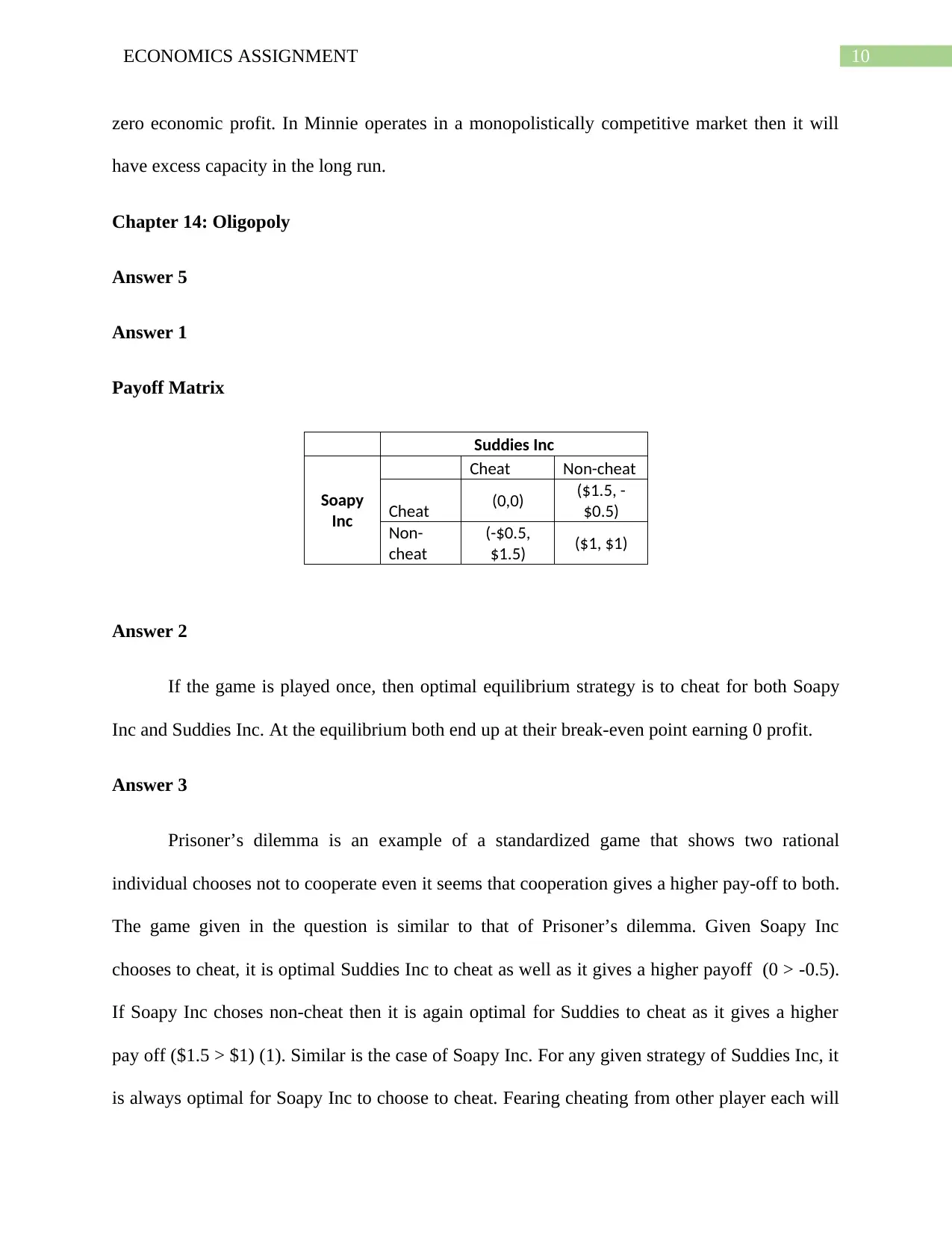

Homework Assignment

AI Summary

This economics assignment delves into microeconomic principles, focusing on output and costs, perfect competition, monopoly, monopolistic competition, and oligopoly. It begins with an analysis of output and costs, including calculations of total variable cost, total fixed cost, and marginal cost. The assignment then explores perfect competition, determining profit-maximizing output levels based on marginal cost and price, and analyzing the shut-down price. Furthermore, it examines monopoly and monopolistic competition, calculating marginal revenue and economic profit, and contrasting the market dynamics of each. Finally, the assignment concludes with a discussion of oligopoly, including the application of payoff matrices and the prisoner's dilemma to analyze strategic interactions between firms, along with references to relevant economic literature.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.