Economics for Business (BECO001) Case Study: Sugary Drink Taxation

VerifiedAdded on 2022/11/26

|14

|3294

|63

Report

AI Summary

This report examines the potential implementation of a sugary drinks tax in Australia, addressing the country's obesity problem. It investigates the issue by analyzing the reluctance of the Australian government to impose the tax despite its prevalence in other countries, such as the United States and the United Kingdom. The report explores the causes behind this reluctance, including concerns about regressivity and existing regulations. It identifies key stakeholders like consumers, firm owners, and the government, discussing their respective stakes in the market. Furthermore, it applies economic concepts such as demand and supply, price elasticity of demand, and market distortion to understand the effects of a sugar tax. The report also proposes alternate solutions such as awareness programs, product innovation, and promoting healthy drink consumption. The conclusion emphasizes the need for measures to reduce sugary drink consumption, offering recommendations for policy changes to improve public health and address the obesity problem.

Running head: ECONOMICS FOR BUSINESS

Economics for Business

Name of the Student

Name of the University

Author Note

Economics for Business

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS FOR BUSINESS

Executive Summary

This report aims to discuss the policy of tax imposition is Australia. Many countries

implemented the policy of tax imposition, but Australia did not, due to various reasons

discussed in the report. The issue of taxing sugary drinks has been discussed, and the causes

that are prohibiting Australia from taking measures to impose tax are mentioned. The

stakeholders of the sugary drink market have been identified, and their stakes were discussed.

The economics of the market and policy have been discussed in the report. Also, alternate

solutions to the problem were given in the report. The report concluded that sugary drink

consumption should be reduced in Australia to deal with the obesity problem of the country.

Thus, to address the problem, recommendations have been made in the report.

Executive Summary

This report aims to discuss the policy of tax imposition is Australia. Many countries

implemented the policy of tax imposition, but Australia did not, due to various reasons

discussed in the report. The issue of taxing sugary drinks has been discussed, and the causes

that are prohibiting Australia from taking measures to impose tax are mentioned. The

stakeholders of the sugary drink market have been identified, and their stakes were discussed.

The economics of the market and policy have been discussed in the report. Also, alternate

solutions to the problem were given in the report. The report concluded that sugary drink

consumption should be reduced in Australia to deal with the obesity problem of the country.

Thus, to address the problem, recommendations have been made in the report.

2ECONOMICS FOR BUSINESS

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Main Issue............................................................................................................................3

2.1 Causes..............................................................................................................................4

3.0 Stakeholders.........................................................................................................................4

3.1 Stakeholder 1: Consumers................................................................................................5

3.2 Stakeholder 2: Firm Owners............................................................................................5

3.5 Stakeholder 3: Government..............................................................................................5

4.0 Economic Concepts..............................................................................................................6

4.1 Demand and Supply.........................................................................................................6

4.2 Price Elasticity of Demand...............................................................................................6

4.3 Tax and market distortion................................................................................................7

5.0 Alternate Solutions...............................................................................................................8

5.1 Awareness Programmes...................................................................................................9

5.2 Innovation in Sugary Drinks............................................................................................9

5.3 Consumption of Healthy Drinks......................................................................................9

6.0 Conclusion and Recommendations......................................................................................9

7.0 Reference List....................................................................................................................11

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Main Issue............................................................................................................................3

2.1 Causes..............................................................................................................................4

3.0 Stakeholders.........................................................................................................................4

3.1 Stakeholder 1: Consumers................................................................................................5

3.2 Stakeholder 2: Firm Owners............................................................................................5

3.5 Stakeholder 3: Government..............................................................................................5

4.0 Economic Concepts..............................................................................................................6

4.1 Demand and Supply.........................................................................................................6

4.2 Price Elasticity of Demand...............................................................................................6

4.3 Tax and market distortion................................................................................................7

5.0 Alternate Solutions...............................................................................................................8

5.1 Awareness Programmes...................................................................................................9

5.2 Innovation in Sugary Drinks............................................................................................9

5.3 Consumption of Healthy Drinks......................................................................................9

6.0 Conclusion and Recommendations......................................................................................9

7.0 Reference List....................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS FOR BUSINESS

1.0 Introduction

The world is growing fast economically, and the disposable income is simultaneously

growing and leading to more consumption in every respect. Consequently, the consumption

of sugary drinks has increased by many folds. Whenever people feel tired of thirsty, they tend

to consume sugary drinks to refuel or to quench thirst. It is scientifically proven that

consuming sugary drinks aggravates the chances of becoming obese. Both evidence and

research have shown that the top obese countries in the world consume more sugars (Basu et

al., 2013). Obesity gives rise to various chronic diseases. Hence, considering the health

issues, many countries have already imposed a tax on sugary drinks to discourage

consumption. This report discusses the effect of sugar tax from the stakeholders’ viewpoint

based on a selected case in Australia The discussion mainly focuses on why or why not

Australia is imposing a tax on sugary drinks and the possible outcomes of the available

decisions. The economic concepts of taxation on sugary drinks are discussed, along with

possible and more feasible solutions. The report recommends policy solutions, that could help

all the stakeholders and guide them to avoid welfare loss in case of any of the stakeholders of

the industry. Thus, studying the case of Australia regarding tax imposition on sugary drinks

leads to the big picture of Australian sugary drinks industry and the necessity of sugary

drinks tax.

2.0 Main Issue

The concerned case of a tax on sugary drinks discusses the importance of tax on sugary

drinks to discourage consumption and avoid the increasing harmful health trend of obesity

(Han & Powell 2013). Perceiving the health threat, countries like the United States, Ireland,

Saudi Arabia, South Africa and other twenty-six countries have already imposed a tax on

sugary drinks. Thus, the positive relation between sugary drinks and obesity is attracting the

1.0 Introduction

The world is growing fast economically, and the disposable income is simultaneously

growing and leading to more consumption in every respect. Consequently, the consumption

of sugary drinks has increased by many folds. Whenever people feel tired of thirsty, they tend

to consume sugary drinks to refuel or to quench thirst. It is scientifically proven that

consuming sugary drinks aggravates the chances of becoming obese. Both evidence and

research have shown that the top obese countries in the world consume more sugars (Basu et

al., 2013). Obesity gives rise to various chronic diseases. Hence, considering the health

issues, many countries have already imposed a tax on sugary drinks to discourage

consumption. This report discusses the effect of sugar tax from the stakeholders’ viewpoint

based on a selected case in Australia The discussion mainly focuses on why or why not

Australia is imposing a tax on sugary drinks and the possible outcomes of the available

decisions. The economic concepts of taxation on sugary drinks are discussed, along with

possible and more feasible solutions. The report recommends policy solutions, that could help

all the stakeholders and guide them to avoid welfare loss in case of any of the stakeholders of

the industry. Thus, studying the case of Australia regarding tax imposition on sugary drinks

leads to the big picture of Australian sugary drinks industry and the necessity of sugary

drinks tax.

2.0 Main Issue

The concerned case of a tax on sugary drinks discusses the importance of tax on sugary

drinks to discourage consumption and avoid the increasing harmful health trend of obesity

(Han & Powell 2013). Perceiving the health threat, countries like the United States, Ireland,

Saudi Arabia, South Africa and other twenty-six countries have already imposed a tax on

sugary drinks. Thus, the positive relation between sugary drinks and obesity is attracting the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS FOR BUSINESS

attention of many governments in the world. From the article concerned, it is evident that

Australia, however, is not considering the policy of taxing sugary drinks. It is quite

astonishing, that being the country of one of the largest population of fattest people in the

world (Hambleton, 2014), the government of Australia is reluctant to impose a tax on sugary

drinks.

2.1 Causes

Many argues, taking the reference of Mexico and suggest not to tax sugary drinks as it may

turn out to be regressive and poor people might get exploited (Long et al. 2015). However,

many are of an opinion and provided evidence that taxation on sugary drinks proved to be

beneficial for Mexico (Colchero, Molina, & Guerrero-López 2017). On the other hand, the

government of Australia believes that tax on sugary drinks is not required because food

labelling laws and advertisement restricting laws are sufficient (The Guardian 2018). As there

is no pressure from the opposition regarding sugary drink tax, probably government is not

emphasizing on the matter. Economically the price of any product is growing every year due

to inflation (Backholer & Baker 2018). Alternatively, tax imposition could make the situation

worse by aggravating the effect of inflation.

3.0 Stakeholders

In sugary drink manufacturing industry, there are many stakeholders such as

employees, consumers, raw material suppliers, dealers, retailers, firm owners, the government

and machinery suppliers. The stakeholders can further be categorized into primary and

secondary stakeholders. The primary stakeholders of the sugary drink manufacturing are raw

material suppliers, firm owners, employees, dealers, retailers and consumers and the

government is the secondary stakeholders (Fernandez-Feijoo, Romero & Ruiz 2014). In this

attention of many governments in the world. From the article concerned, it is evident that

Australia, however, is not considering the policy of taxing sugary drinks. It is quite

astonishing, that being the country of one of the largest population of fattest people in the

world (Hambleton, 2014), the government of Australia is reluctant to impose a tax on sugary

drinks.

2.1 Causes

Many argues, taking the reference of Mexico and suggest not to tax sugary drinks as it may

turn out to be regressive and poor people might get exploited (Long et al. 2015). However,

many are of an opinion and provided evidence that taxation on sugary drinks proved to be

beneficial for Mexico (Colchero, Molina, & Guerrero-López 2017). On the other hand, the

government of Australia believes that tax on sugary drinks is not required because food

labelling laws and advertisement restricting laws are sufficient (The Guardian 2018). As there

is no pressure from the opposition regarding sugary drink tax, probably government is not

emphasizing on the matter. Economically the price of any product is growing every year due

to inflation (Backholer & Baker 2018). Alternatively, tax imposition could make the situation

worse by aggravating the effect of inflation.

3.0 Stakeholders

In sugary drink manufacturing industry, there are many stakeholders such as

employees, consumers, raw material suppliers, dealers, retailers, firm owners, the government

and machinery suppliers. The stakeholders can further be categorized into primary and

secondary stakeholders. The primary stakeholders of the sugary drink manufacturing are raw

material suppliers, firm owners, employees, dealers, retailers and consumers and the

government is the secondary stakeholders (Fernandez-Feijoo, Romero & Ruiz 2014). In this

5ECONOMICS FOR BUSINESS

case, five stakeholders have been considered that are directly influenced by the tax imposition

on sugary drinks.

3.1 Stakeholder 1: Consumers

It is already evident from the above discussion that consuming sugary drink does

contribute to making a person fat and excessive consumption of sugary drinks aggravate the

obese condition (Sahoo et al. 2015). Like many other countries, Australians consume a large

number of sugary drinks. Consumption of sugary drink is much popular among the youth

(18-24 years) in comparison to aged person. As age grows, a tendency of sugary drink

consumption decreases. During youth, 61.3 per cent of Australians used to consume sugary

drinks at least once a week. Thus, the increase in the obese population of Australia is justified

with the given data (Tesafa 2014). Hence, policies should be designed to reduce consumption

of sugary drinks. Imposition of tax is considered as one suggestive policy to control

consumption of sugary beverages. However, it has already been argued that imposition of tax

on sugary drinks might increase the burden of poor people as it did in Mexico.

3.2 Stakeholder 2: Firm Owners

The imposition of tax on sugary drinks directly affects the firm owners first as the

sales are supposed to decrease (Powell et al. 2013). The profitability of a firm will reduce, but

health is also an important factor. Hence, policies are required that will bring a balance

between firms’ profitability and health. This could be done by reducing the number of sugars

avoid listing of their product into the taxed group of drinks.

3.5 Stakeholder 3: The Government

The government is a secondary stakeholder of the sugary drinks market as far as the

health issue is concerned. Thus, the government should take care of the health of its subjects

prior to any product market (Lawman et al. 2013). In this case, the gamble is quite high, and

case, five stakeholders have been considered that are directly influenced by the tax imposition

on sugary drinks.

3.1 Stakeholder 1: Consumers

It is already evident from the above discussion that consuming sugary drink does

contribute to making a person fat and excessive consumption of sugary drinks aggravate the

obese condition (Sahoo et al. 2015). Like many other countries, Australians consume a large

number of sugary drinks. Consumption of sugary drink is much popular among the youth

(18-24 years) in comparison to aged person. As age grows, a tendency of sugary drink

consumption decreases. During youth, 61.3 per cent of Australians used to consume sugary

drinks at least once a week. Thus, the increase in the obese population of Australia is justified

with the given data (Tesafa 2014). Hence, policies should be designed to reduce consumption

of sugary drinks. Imposition of tax is considered as one suggestive policy to control

consumption of sugary beverages. However, it has already been argued that imposition of tax

on sugary drinks might increase the burden of poor people as it did in Mexico.

3.2 Stakeholder 2: Firm Owners

The imposition of tax on sugary drinks directly affects the firm owners first as the

sales are supposed to decrease (Powell et al. 2013). The profitability of a firm will reduce, but

health is also an important factor. Hence, policies are required that will bring a balance

between firms’ profitability and health. This could be done by reducing the number of sugars

avoid listing of their product into the taxed group of drinks.

3.5 Stakeholder 3: The Government

The government is a secondary stakeholder of the sugary drinks market as far as the

health issue is concerned. Thus, the government should take care of the health of its subjects

prior to any product market (Lawman et al. 2013). In this case, the gamble is quite high, and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS FOR BUSINESS

thus, the government should intervene actively to reduce sugary drink consumption without

affecting the manufacturers of sugary drinks.

4.0 Economic Concepts

Tax imposition on sugary drinks to reduce consumption of sugar is based on demand-

supply economics. However, the outcomes may have some other macroeconomic

implications other than the demand and supply. Those are market economics and

macroeconomic factors.

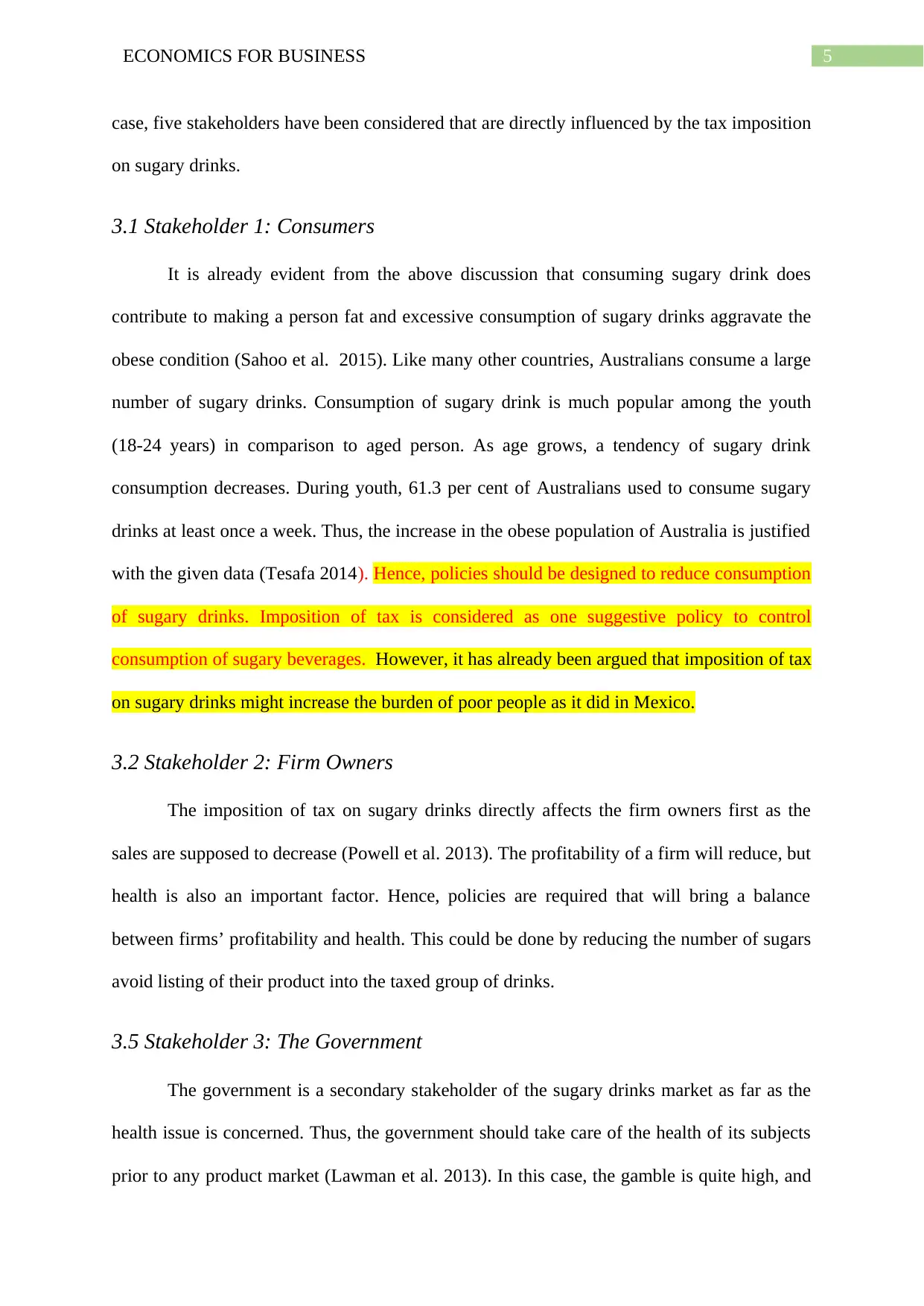

4.1 Demand and Supply

Figure 1: Price-Demand Relation

The tax imposition on sugary drinks has been conceptualised based on the theory of

demand and supply. Demand and supply theory suggests that an increase in the price of a

product decreases its demand. Hence, price increase discourages consumption of products

(Friedman 2017). The relation between price and quantity is shown in Figure 1. Therefore,

tax imposition on sugary drinks will increase the price and results in decreased consumption

of the drinks through increased price. The fall in demand will influence the supply and firms

will manufacture fewer drinks and cut the supply to avoid the cost.

Q2

D

P1

P2

Q1

Price

QuantityO

thus, the government should intervene actively to reduce sugary drink consumption without

affecting the manufacturers of sugary drinks.

4.0 Economic Concepts

Tax imposition on sugary drinks to reduce consumption of sugar is based on demand-

supply economics. However, the outcomes may have some other macroeconomic

implications other than the demand and supply. Those are market economics and

macroeconomic factors.

4.1 Demand and Supply

Figure 1: Price-Demand Relation

The tax imposition on sugary drinks has been conceptualised based on the theory of

demand and supply. Demand and supply theory suggests that an increase in the price of a

product decreases its demand. Hence, price increase discourages consumption of products

(Friedman 2017). The relation between price and quantity is shown in Figure 1. Therefore,

tax imposition on sugary drinks will increase the price and results in decreased consumption

of the drinks through increased price. The fall in demand will influence the supply and firms

will manufacture fewer drinks and cut the supply to avoid the cost.

Q2

D

P1

P2

Q1

Price

QuantityO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS FOR BUSINESS

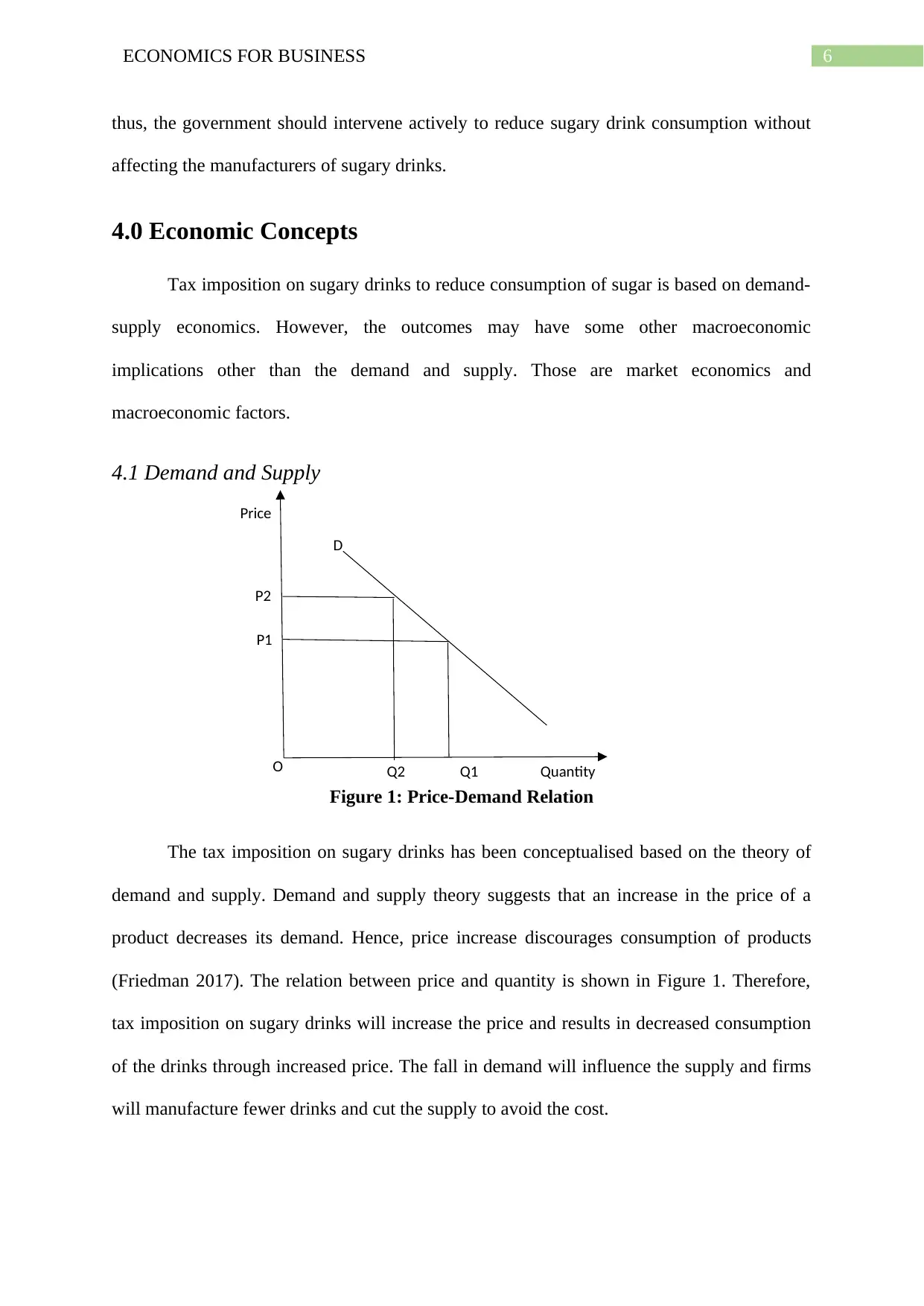

4.2 Price Elasticity of Demand

Theory of price elasticity of demand measures the magnitude of change in demand for

a product due to change in its price and is given by

Price elasticity of demand= Percentage change ∈demand of good

Percentage change∈the price of a good

According to Annualreviews.org 2019 review mentioned how sugary drinks elasticity

is -0.8 to -1.2 which below 1. Because of number of available substitute of sugary drinks,

own price elasticity of demand is relatively Inelastic. The concerned topic, the concept of

cross price elasticity for substitutes is visible, that means, increase in price of sugary drinks

increase the consumption of its substitute drink example milk (Guerrero-López, Unar-

Munguía & Colchero 2017).

Figure 2: Effect of a sugar tax on the market of milk

Hence, after imposition of tax on sugary drinks in Mexico the sales of non-taxed substitute

drinks like milk increased. This evidence further showed at Annualreviews.org how the tax

has reduced the SSB purchases in Mexico, while the water bottle purchases increase.

4.2 Price Elasticity of Demand

Theory of price elasticity of demand measures the magnitude of change in demand for

a product due to change in its price and is given by

Price elasticity of demand= Percentage change ∈demand of good

Percentage change∈the price of a good

According to Annualreviews.org 2019 review mentioned how sugary drinks elasticity

is -0.8 to -1.2 which below 1. Because of number of available substitute of sugary drinks,

own price elasticity of demand is relatively Inelastic. The concerned topic, the concept of

cross price elasticity for substitutes is visible, that means, increase in price of sugary drinks

increase the consumption of its substitute drink example milk (Guerrero-López, Unar-

Munguía & Colchero 2017).

Figure 2: Effect of a sugar tax on the market of milk

Hence, after imposition of tax on sugary drinks in Mexico the sales of non-taxed substitute

drinks like milk increased. This evidence further showed at Annualreviews.org how the tax

has reduced the SSB purchases in Mexico, while the water bottle purchases increase.

8ECONOMICS FOR BUSINESS

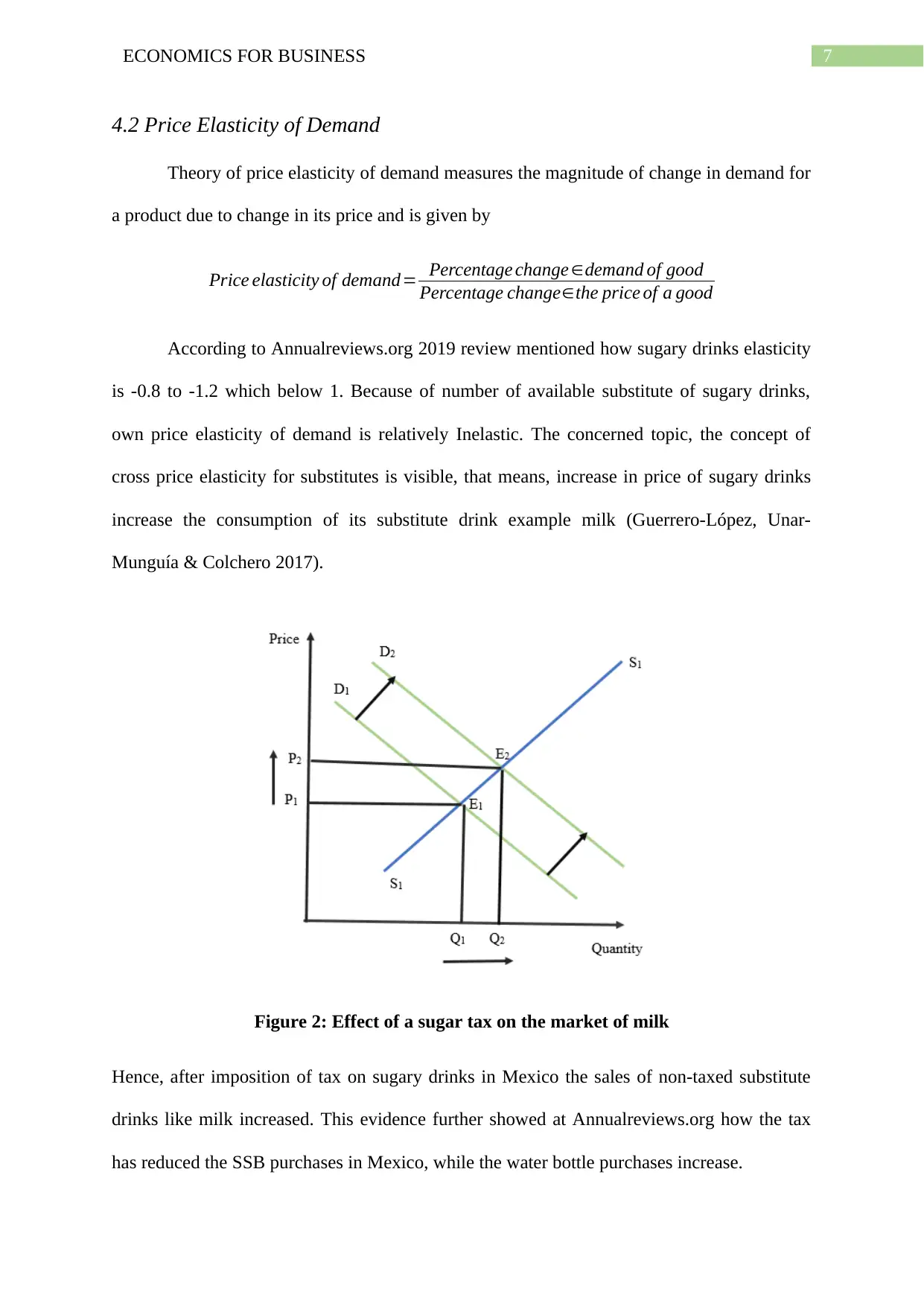

4.3 Tax and market distortion

The imposition of tax distorts free market activity by interrupting demand or supply

side. The forceful intervention in the market through tax results in inefficient allocation of

resources known as a deadweight loss. This is shown in the figure below. The imposition of

tax discourages production and shifts the supply curve to the left to S1S1. After the tax, the

price that buyers pay increases to P2 and price that sellers receive reduces to P1. The

government earns a tax revenue shown by the area P2E1FP1. Equilibrium quantity in the

market reduces to Q1. The proposed policy, however, leads to a welfare loss called

deadweight loss shown by the triangle EE1F in figure 3.

Figure 3: Tax and market distortion

5.0 Alternate Solutions

The policy of tax imposition on sugary drinks is not welcome in Australia, which is

clear from the stand of the government. Thus, new policies are required in the case of

Australia to reduce the consumption of sugary drinks and thereby control the obesity problem

of the country.

4.3 Tax and market distortion

The imposition of tax distorts free market activity by interrupting demand or supply

side. The forceful intervention in the market through tax results in inefficient allocation of

resources known as a deadweight loss. This is shown in the figure below. The imposition of

tax discourages production and shifts the supply curve to the left to S1S1. After the tax, the

price that buyers pay increases to P2 and price that sellers receive reduces to P1. The

government earns a tax revenue shown by the area P2E1FP1. Equilibrium quantity in the

market reduces to Q1. The proposed policy, however, leads to a welfare loss called

deadweight loss shown by the triangle EE1F in figure 3.

Figure 3: Tax and market distortion

5.0 Alternate Solutions

The policy of tax imposition on sugary drinks is not welcome in Australia, which is

clear from the stand of the government. Thus, new policies are required in the case of

Australia to reduce the consumption of sugary drinks and thereby control the obesity problem

of the country.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS FOR BUSINESS

5.1 Awareness Programmes

The government should make people aware of the effect of sugar on increasing

obesity. Awareness programme will only make the consumers aware of the obesity factors

and harmful health conditions that may arise due to obesity (Cummins, Flint & Matthews

2014). These programmes also not directly affect the market, and there will be no burden of

tax on the poor section of the country.

5.2 Innovation in Sugary Drinks

Sugary drink manufacturers should invest in innovation and reduction of sugar in the

drinks to allowed level as fixed by the government. This is one of the best possible solutions

for the sugary drink consumption control because this neither decreases the sales of the drinks

nor aggravates the issue of obesity (Harris et al. 2013).

5.3 Consumption of Healthy Drinks

People should be encouraged to consume healthy drinks like milk (Park et al. 2013).

Hospitals and other healthcare facilities, including medicine stores may also participate in

healthy drinks movement by limiting amount of sugary drinks in the building and providing

free waters. These facilities may also promote the healthier choices and alternatives for the

community and the people. Consuming and purchasing unhealthy drinks in the facilities may

be charged excess tax to increase awareness of the community.

6.0 Conclusion and Recommendations

From the above discussion, it can be concluded that obesity is a real problem in the

world in recent times, and it must be controlled immediately. However, many countries have

implemented tax policies to control sugary drinks consumption but most of the countries are

left to take effective steps and Australia is among one of them. The government of Australia

5.1 Awareness Programmes

The government should make people aware of the effect of sugar on increasing

obesity. Awareness programme will only make the consumers aware of the obesity factors

and harmful health conditions that may arise due to obesity (Cummins, Flint & Matthews

2014). These programmes also not directly affect the market, and there will be no burden of

tax on the poor section of the country.

5.2 Innovation in Sugary Drinks

Sugary drink manufacturers should invest in innovation and reduction of sugar in the

drinks to allowed level as fixed by the government. This is one of the best possible solutions

for the sugary drink consumption control because this neither decreases the sales of the drinks

nor aggravates the issue of obesity (Harris et al. 2013).

5.3 Consumption of Healthy Drinks

People should be encouraged to consume healthy drinks like milk (Park et al. 2013).

Hospitals and other healthcare facilities, including medicine stores may also participate in

healthy drinks movement by limiting amount of sugary drinks in the building and providing

free waters. These facilities may also promote the healthier choices and alternatives for the

community and the people. Consuming and purchasing unhealthy drinks in the facilities may

be charged excess tax to increase awareness of the community.

6.0 Conclusion and Recommendations

From the above discussion, it can be concluded that obesity is a real problem in the

world in recent times, and it must be controlled immediately. However, many countries have

implemented tax policies to control sugary drinks consumption but most of the countries are

left to take effective steps and Australia is among one of them. The government of Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS FOR BUSINESS

should take effective measures to control the consumption of sugars and thus controlling the

consumption of sugary drinks could be the first step as it has a significant amount of share in

total sugar consumption. The government is, however, not intended to do so as it has the

opinion that imposition of the tax is not a proper policy to control it. There are several

reasons that influenced the government from not imposing the tax like a protest from

Australian Beverage Council, different and feasible solutions from oppositions, negative

impacts on Mexico due to sugary drink tax and the probability of tax burden on poor. The

economic factors that explain this case are demand, supply, price elasticity, employment and

government policy implications.

Alternatively, there are solutions that are capable of mitigating the problem of over-

consumption of sugar and obesity problem in Australia with effective recommendations.

Firstly, the government of Australia should fix a slot in television to aware the people to

reduce consumption of sugary drinks and take care of health such that Australia can be freed

from the obesity problem. Secondly, the government can give a tax credit to the firm for

investing and developing drinks with less amount of sugar (fixed amount allowed as per

government norms) (Kansagra et al. 2014). Thirdly, people should be incentivised if they

purchase healthy drinks like milk for consumption by providing discounts on purchase (CNN,

2018). Fourthly, the sugar drink advertisements that influence children should be restricted,

and if any manufacturer does advertise its product targeting the children, then it should be

penalized.

should take effective measures to control the consumption of sugars and thus controlling the

consumption of sugary drinks could be the first step as it has a significant amount of share in

total sugar consumption. The government is, however, not intended to do so as it has the

opinion that imposition of the tax is not a proper policy to control it. There are several

reasons that influenced the government from not imposing the tax like a protest from

Australian Beverage Council, different and feasible solutions from oppositions, negative

impacts on Mexico due to sugary drink tax and the probability of tax burden on poor. The

economic factors that explain this case are demand, supply, price elasticity, employment and

government policy implications.

Alternatively, there are solutions that are capable of mitigating the problem of over-

consumption of sugar and obesity problem in Australia with effective recommendations.

Firstly, the government of Australia should fix a slot in television to aware the people to

reduce consumption of sugary drinks and take care of health such that Australia can be freed

from the obesity problem. Secondly, the government can give a tax credit to the firm for

investing and developing drinks with less amount of sugar (fixed amount allowed as per

government norms) (Kansagra et al. 2014). Thirdly, people should be incentivised if they

purchase healthy drinks like milk for consumption by providing discounts on purchase (CNN,

2018). Fourthly, the sugar drink advertisements that influence children should be restricted,

and if any manufacturer does advertise its product targeting the children, then it should be

penalized.

11ECONOMICS FOR BUSINESS

7.0 Reference List

Backholer, K., & Baker, P. 2018. Sugar-Sweetened Beverage Taxes: the Potential for

Cardiovascular Health. Current Cardiovascular Risk Reports, 12(12), 28.

Basu, S., McKee, M., Galea, G., & Stuckler, D. (2013). Relationship of soft drink

consumption to global overweight, obesity, and diabetes: a cross-national analysis of

75 countries. American journal of public health, 103(11), 2071-2077.

Chaloupka, F.J., Powell, L.M., Warner, K.E, 2019, Annual Review of Public Health. The Use

of Excise Taxes to Reduce Tobacco, Alcohol and Sugary Beverage Consumption, Vol

40, pp 187 – 201.

CNN 2018, Physician groups call for taxes and regulations on kids' access to sugary drinks,

CNN. viewed 18 May 2019, <https://edition.cnn.com/2019/03/25/health/sodas-

sugary-drinks-policy-statement-study/index.html>.

Colchero, M.A., Molina, M. & Guerrero-López, C.M. 2017. After Mexico implemented a

tax, purchases of sugar-sweetened beverages decreased and water increased:

difference by place of residence, household composition, and income level. The

Journal of nutrition, 147(8), pp.1552-1557.

Cummins, S., Flint, E. & Matthews, S.A. 2014. New neighborhood grocery store increased

awareness of food access but did not alter dietary habits or obesity. Health

affairs, 33(2), pp.283-291.

Fernandez-Feijoo, B., Romero, S. & Ruiz, S. 2014. Effect of stakeholders’ pressure on

transparency of sustainability reports within the GRI framework. Journal of business

ethics, 122(1), pp.53-63.

7.0 Reference List

Backholer, K., & Baker, P. 2018. Sugar-Sweetened Beverage Taxes: the Potential for

Cardiovascular Health. Current Cardiovascular Risk Reports, 12(12), 28.

Basu, S., McKee, M., Galea, G., & Stuckler, D. (2013). Relationship of soft drink

consumption to global overweight, obesity, and diabetes: a cross-national analysis of

75 countries. American journal of public health, 103(11), 2071-2077.

Chaloupka, F.J., Powell, L.M., Warner, K.E, 2019, Annual Review of Public Health. The Use

of Excise Taxes to Reduce Tobacco, Alcohol and Sugary Beverage Consumption, Vol

40, pp 187 – 201.

CNN 2018, Physician groups call for taxes and regulations on kids' access to sugary drinks,

CNN. viewed 18 May 2019, <https://edition.cnn.com/2019/03/25/health/sodas-

sugary-drinks-policy-statement-study/index.html>.

Colchero, M.A., Molina, M. & Guerrero-López, C.M. 2017. After Mexico implemented a

tax, purchases of sugar-sweetened beverages decreased and water increased:

difference by place of residence, household composition, and income level. The

Journal of nutrition, 147(8), pp.1552-1557.

Cummins, S., Flint, E. & Matthews, S.A. 2014. New neighborhood grocery store increased

awareness of food access but did not alter dietary habits or obesity. Health

affairs, 33(2), pp.283-291.

Fernandez-Feijoo, B., Romero, S. & Ruiz, S. 2014. Effect of stakeholders’ pressure on

transparency of sustainability reports within the GRI framework. Journal of business

ethics, 122(1), pp.53-63.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.