MOD3327 Economics for Business: Production Decisions and Competition

VerifiedAdded on 2023/06/17

|10

|2506

|441

Report

AI Summary

This report explores the influence of inputs, costs, and market competition on production decisions and the supply of goods and services, focusing on the UK economy. It details how factors like raw materials, labor charges, capital, and entrepreneurship affect production decisions. The report further analyzes the impact of highly competitive markets, particularly perfect competition, on supply, considering short-run and long-run cost curves and their implications for manufacturing industries in the UK. It concludes that supply and production decisions are significantly shaped by input costs and the competitive landscape, impacting profitability and market dynamics.

Economics for

Business

Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

How does inputs and costs impact the production decisions in an industry. How are these

related to supply of goods and services.......................................................................................3

TASK 2............................................................................................................................................6

How does highly competitive markets or perfect competition impacts the supply of goods and

services........................................................................................................................................6

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

How does inputs and costs impact the production decisions in an industry. How are these

related to supply of goods and services.......................................................................................3

TASK 2............................................................................................................................................6

How does highly competitive markets or perfect competition impacts the supply of goods and

services........................................................................................................................................6

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Economics is the branch of social science which deals with the study of resources and the uses

these resources can be put to, keeping in mind that these resources are limited while the uses of

these resources are unending. It is a study of scarcity and its implications in an economy.

Economics for business is one of the important tool that helps the business, mainly the

manufacturing business to better understand the resources the need and how to mange them.

According to Alfred Marshall, Economics is “A study of mankind in the ordinary business of

life; it examines that part of individual and social action which is most closely connected with

the attainment and with the use of the material requisites of well-being” it basically studies the

human behaviour in relation to scare resources which can be put to alternative uses. This report

highlights how inputs and costs affects the production decision in regards to UK and how the

competition among the industry impacts the supply of goods.

TASK 1

How does inputs and costs impact the production decisions in an industry. How are these related

to supply of goods and services.

Supply: In the theory of economics, supply refers to the willingness of the producers of different

goods and services to supply these commodities in the market. It refers to the amount of goods

that are available to the customers to purchase. Supply and demand are inter related due to price.

Price of the product is determined by both demand and supply of a commodity. Price and supply

has a positive relation (Krugman and Wells. 2020). This means that if the supply of the product

increases its supply tends to increase. This happens because the suppliers want to earn more and

more at this increased price. But the price is also related to the costs that the suppliers tend to

face while production. These costs are generally related to the factors of production. These will

be discussed further.

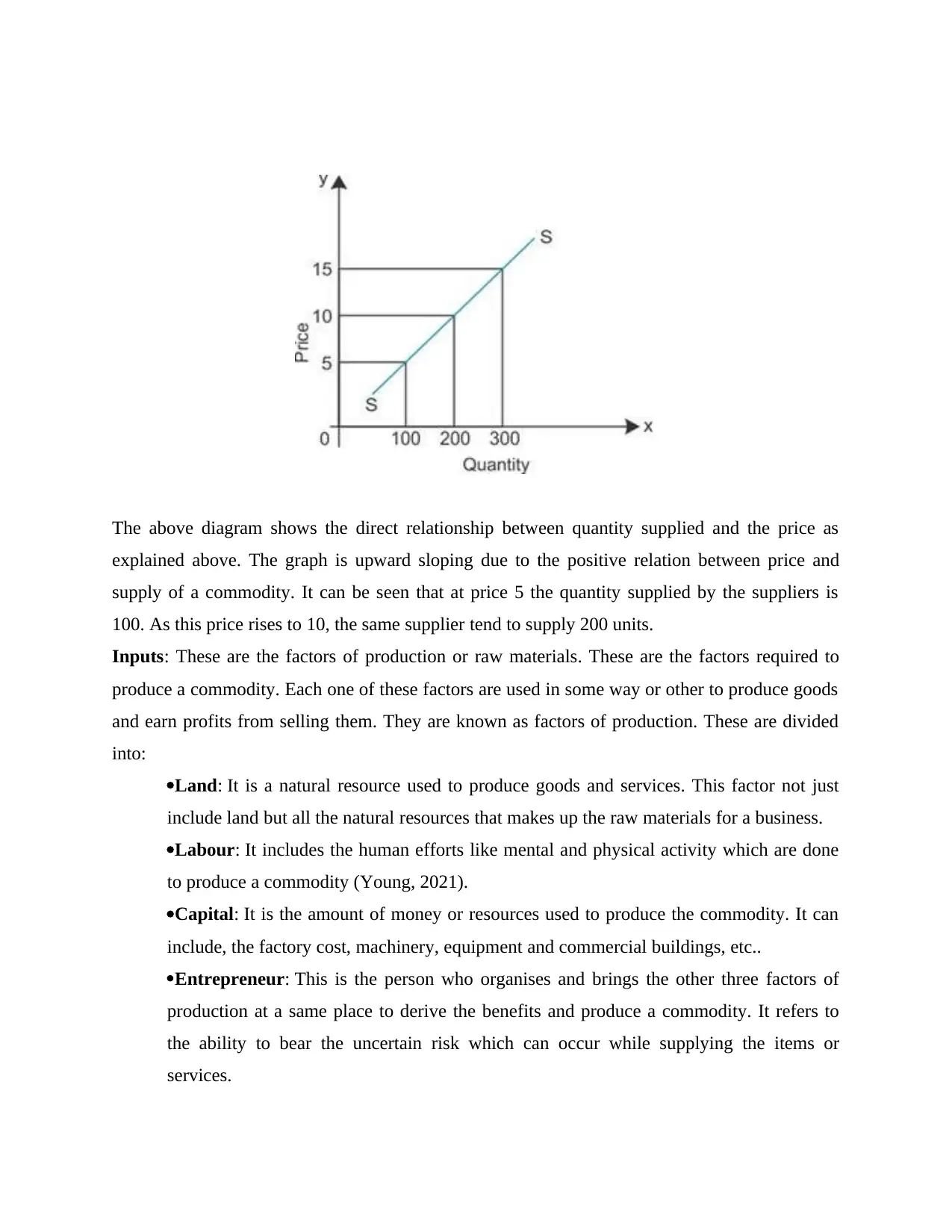

Law of supply is one of the microeconomic law which states that there is a positive relation

between the supply and price of the commodity, when other factors are being constant. It means

that greater the price is, more quantity of goods will be supplied by the supplier to earn more

revenue. The law of supply can be diagrammatically represented as follows:

Economics is the branch of social science which deals with the study of resources and the uses

these resources can be put to, keeping in mind that these resources are limited while the uses of

these resources are unending. It is a study of scarcity and its implications in an economy.

Economics for business is one of the important tool that helps the business, mainly the

manufacturing business to better understand the resources the need and how to mange them.

According to Alfred Marshall, Economics is “A study of mankind in the ordinary business of

life; it examines that part of individual and social action which is most closely connected with

the attainment and with the use of the material requisites of well-being” it basically studies the

human behaviour in relation to scare resources which can be put to alternative uses. This report

highlights how inputs and costs affects the production decision in regards to UK and how the

competition among the industry impacts the supply of goods.

TASK 1

How does inputs and costs impact the production decisions in an industry. How are these related

to supply of goods and services.

Supply: In the theory of economics, supply refers to the willingness of the producers of different

goods and services to supply these commodities in the market. It refers to the amount of goods

that are available to the customers to purchase. Supply and demand are inter related due to price.

Price of the product is determined by both demand and supply of a commodity. Price and supply

has a positive relation (Krugman and Wells. 2020). This means that if the supply of the product

increases its supply tends to increase. This happens because the suppliers want to earn more and

more at this increased price. But the price is also related to the costs that the suppliers tend to

face while production. These costs are generally related to the factors of production. These will

be discussed further.

Law of supply is one of the microeconomic law which states that there is a positive relation

between the supply and price of the commodity, when other factors are being constant. It means

that greater the price is, more quantity of goods will be supplied by the supplier to earn more

revenue. The law of supply can be diagrammatically represented as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above diagram shows the direct relationship between quantity supplied and the price as

explained above. The graph is upward sloping due to the positive relation between price and

supply of a commodity. It can be seen that at price 5 the quantity supplied by the suppliers is

100. As this price rises to 10, the same supplier tend to supply 200 units.

Inputs: These are the factors of production or raw materials. These are the factors required to

produce a commodity. Each one of these factors are used in some way or other to produce goods

and earn profits from selling them. They are known as factors of production. These are divided

into:

Land: It is a natural resource used to produce goods and services. This factor not just

include land but all the natural resources that makes up the raw materials for a business.

Labour: It includes the human efforts like mental and physical activity which are done

to produce a commodity (Young, 2021).

Capital: It is the amount of money or resources used to produce the commodity. It can

include, the factory cost, machinery, equipment and commercial buildings, etc..

Entrepreneur: This is the person who organises and brings the other three factors of

production at a same place to derive the benefits and produce a commodity. It refers to

the ability to bear the uncertain risk which can occur while supplying the items or

services.

explained above. The graph is upward sloping due to the positive relation between price and

supply of a commodity. It can be seen that at price 5 the quantity supplied by the suppliers is

100. As this price rises to 10, the same supplier tend to supply 200 units.

Inputs: These are the factors of production or raw materials. These are the factors required to

produce a commodity. Each one of these factors are used in some way or other to produce goods

and earn profits from selling them. They are known as factors of production. These are divided

into:

Land: It is a natural resource used to produce goods and services. This factor not just

include land but all the natural resources that makes up the raw materials for a business.

Labour: It includes the human efforts like mental and physical activity which are done

to produce a commodity (Young, 2021).

Capital: It is the amount of money or resources used to produce the commodity. It can

include, the factory cost, machinery, equipment and commercial buildings, etc..

Entrepreneur: This is the person who organises and brings the other three factors of

production at a same place to derive the benefits and produce a commodity. It refers to

the ability to bear the uncertain risk which can occur while supplying the items or

services.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Costs: These refers to the expenditure which is faced by the entrepreneur to produce and sell in

the market. It generally includes the costs of production like labour charges, manufacturing

overheads, etc.

Production decision: These refers to the decisions that are taken up by the entrepreneur of the

business to generate the goods and services that the business works in. In this the owner goes for

a search of the raw material and different resources that are needed for production and the

techniques with which they will produce commodities.

Different factors influence the production decisions of a business enterprise. Following is the

discussion on how inputs and costs have an impact on these decisions.

Entrepreneurship: This factor refers to the opportunities and willingness of the

entrepreneur and managers to run an organisation. This affects the business in an

economy directly. In regards to UK, the country faced shift in the government which led

to a sort of distortion in the country which in turn reduced the economic condition of the

country. This reduced the willingness of the entrepreneurs to further invest in the

business.

Raw Materials: This factor of production is essential for production. These have to be

acquired on time and put to different uses with no delay. In the case of UK, the country

suffered the worst depression in the economy for a certain long time. It made the country

face lack of raw materials, and in return they had to reduce their exports to fulfil the

demand in the local market.

Labour Charges: As discussed above, labour refers to the human efforts that helps the

business change raw materials into finished goods. The company requires to pay some

charges to them. These charges also determine the production decisions. If these charges

increase, this would increase the standards of living in the country. In the year 2010,

these charges fell in the UK due to recession which also created shortage of products.

Capital: This factor is supposed to be invested over a period of time for further

advancements of the enterprise. In a country, government invests in the infrastructure of

the country (Young, 2021). The authorities issues budget and provide with the resources

needed. Any mismanagement of any kind by these authorities will lead to delayed

resources and have negative influence on the UK economy.

the market. It generally includes the costs of production like labour charges, manufacturing

overheads, etc.

Production decision: These refers to the decisions that are taken up by the entrepreneur of the

business to generate the goods and services that the business works in. In this the owner goes for

a search of the raw material and different resources that are needed for production and the

techniques with which they will produce commodities.

Different factors influence the production decisions of a business enterprise. Following is the

discussion on how inputs and costs have an impact on these decisions.

Entrepreneurship: This factor refers to the opportunities and willingness of the

entrepreneur and managers to run an organisation. This affects the business in an

economy directly. In regards to UK, the country faced shift in the government which led

to a sort of distortion in the country which in turn reduced the economic condition of the

country. This reduced the willingness of the entrepreneurs to further invest in the

business.

Raw Materials: This factor of production is essential for production. These have to be

acquired on time and put to different uses with no delay. In the case of UK, the country

suffered the worst depression in the economy for a certain long time. It made the country

face lack of raw materials, and in return they had to reduce their exports to fulfil the

demand in the local market.

Labour Charges: As discussed above, labour refers to the human efforts that helps the

business change raw materials into finished goods. The company requires to pay some

charges to them. These charges also determine the production decisions. If these charges

increase, this would increase the standards of living in the country. In the year 2010,

these charges fell in the UK due to recession which also created shortage of products.

Capital: This factor is supposed to be invested over a period of time for further

advancements of the enterprise. In a country, government invests in the infrastructure of

the country (Young, 2021). The authorities issues budget and provide with the resources

needed. Any mismanagement of any kind by these authorities will lead to delayed

resources and have negative influence on the UK economy.

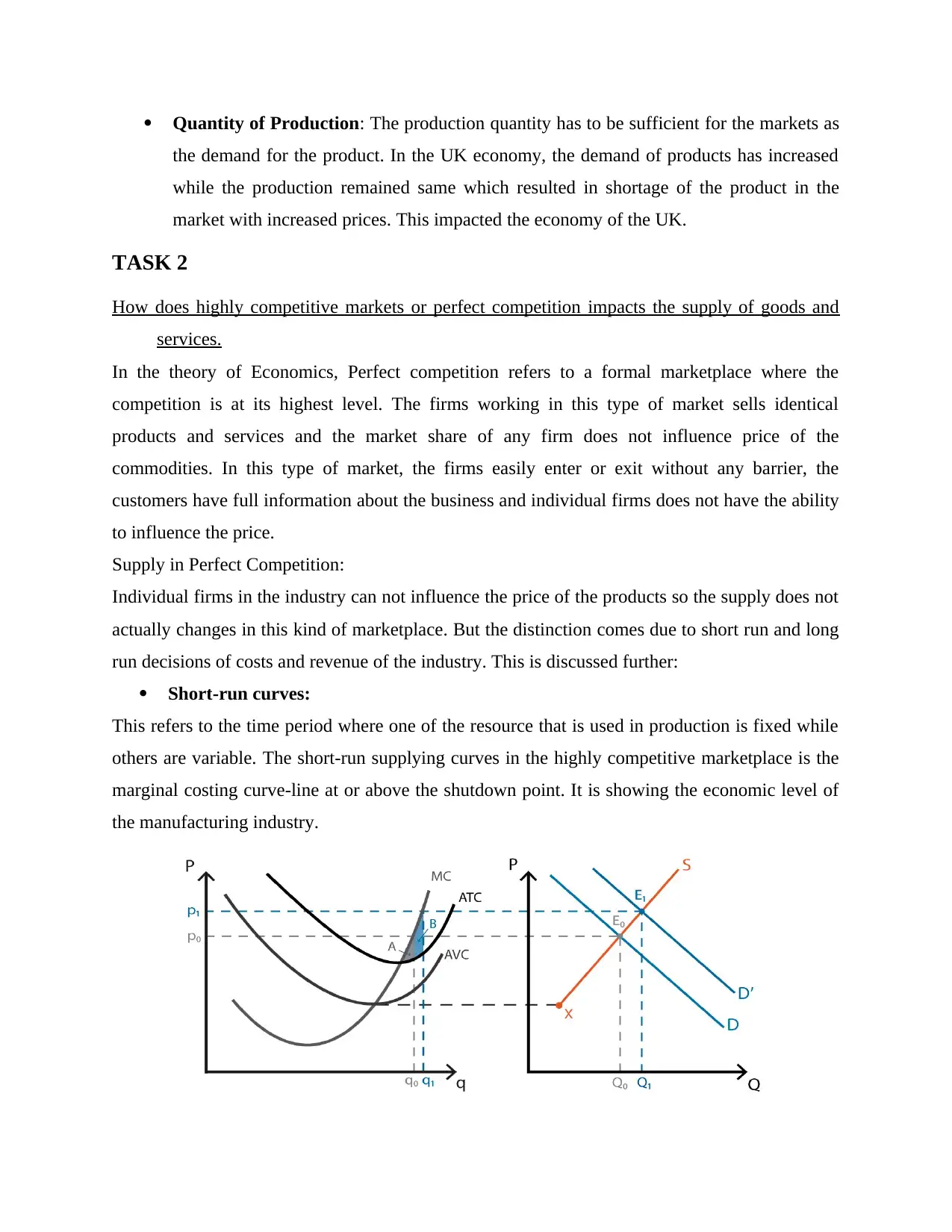

Quantity of Production: The production quantity has to be sufficient for the markets as

the demand for the product. In the UK economy, the demand of products has increased

while the production remained same which resulted in shortage of the product in the

market with increased prices. This impacted the economy of the UK.

TASK 2

How does highly competitive markets or perfect competition impacts the supply of goods and

services.

In the theory of Economics, Perfect competition refers to a formal marketplace where the

competition is at its highest level. The firms working in this type of market sells identical

products and services and the market share of any firm does not influence price of the

commodities. In this type of market, the firms easily enter or exit without any barrier, the

customers have full information about the business and individual firms does not have the ability

to influence the price.

Supply in Perfect Competition:

Individual firms in the industry can not influence the price of the products so the supply does not

actually changes in this kind of marketplace. But the distinction comes due to short run and long

run decisions of costs and revenue of the industry. This is discussed further:

Short-run curves:

This refers to the time period where one of the resource that is used in production is fixed while

others are variable. The short-run supplying curves in the highly competitive marketplace is the

marginal costing curve-line at or above the shutdown point. It is showing the economic level of

the manufacturing industry.

the demand for the product. In the UK economy, the demand of products has increased

while the production remained same which resulted in shortage of the product in the

market with increased prices. This impacted the economy of the UK.

TASK 2

How does highly competitive markets or perfect competition impacts the supply of goods and

services.

In the theory of Economics, Perfect competition refers to a formal marketplace where the

competition is at its highest level. The firms working in this type of market sells identical

products and services and the market share of any firm does not influence price of the

commodities. In this type of market, the firms easily enter or exit without any barrier, the

customers have full information about the business and individual firms does not have the ability

to influence the price.

Supply in Perfect Competition:

Individual firms in the industry can not influence the price of the products so the supply does not

actually changes in this kind of marketplace. But the distinction comes due to short run and long

run decisions of costs and revenue of the industry. This is discussed further:

Short-run curves:

This refers to the time period where one of the resource that is used in production is fixed while

others are variable. The short-run supplying curves in the highly competitive marketplace is the

marginal costing curve-line at or above the shutdown point. It is showing the economic level of

the manufacturing industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above graph shows the mechanism of cost and revenue and how these makes the firm decide

its supply in the market. The Industry's supply and demand curve shows inverse relation but the

individual firm's demand curve/ Average revenue and Marginal revenue is a straight line parallel

to x-axis.

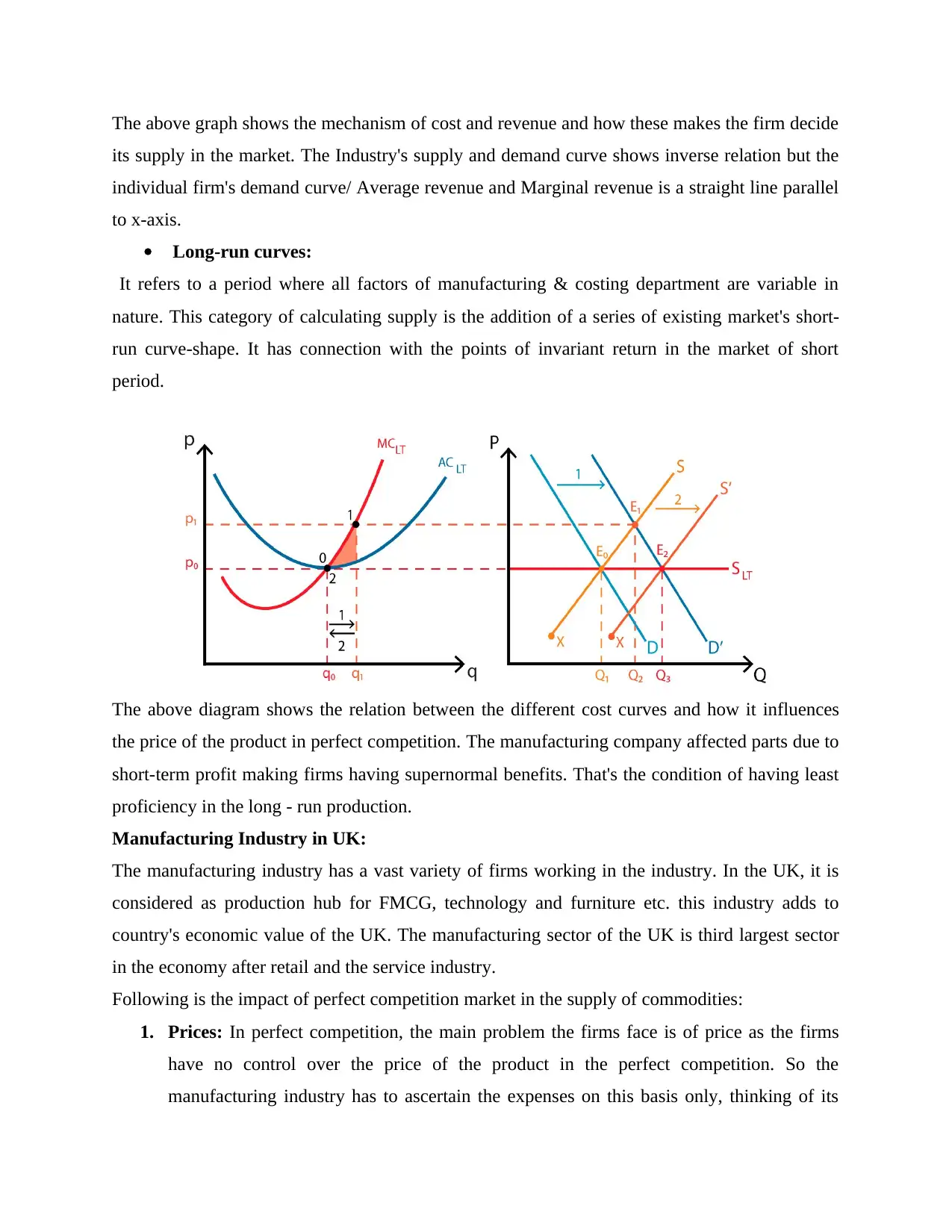

Long-run curves:

It refers to a period where all factors of manufacturing & costing department are variable in

nature. This category of calculating supply is the addition of a series of existing market's short-

run curve-shape. It has connection with the points of invariant return in the market of short

period.

The above diagram shows the relation between the different cost curves and how it influences

the price of the product in perfect competition. The manufacturing company affected parts due to

short-term profit making firms having supernormal benefits. That's the condition of having least

proficiency in the long - run production.

Manufacturing Industry in UK:

The manufacturing industry has a vast variety of firms working in the industry. In the UK, it is

considered as production hub for FMCG, technology and furniture etc. this industry adds to

country's economic value of the UK. The manufacturing sector of the UK is third largest sector

in the economy after retail and the service industry.

Following is the impact of perfect competition market in the supply of commodities:

1. Prices: In perfect competition, the main problem the firms face is of price as the firms

have no control over the price of the product in the perfect competition. So the

manufacturing industry has to ascertain the expenses on this basis only, thinking of its

its supply in the market. The Industry's supply and demand curve shows inverse relation but the

individual firm's demand curve/ Average revenue and Marginal revenue is a straight line parallel

to x-axis.

Long-run curves:

It refers to a period where all factors of manufacturing & costing department are variable in

nature. This category of calculating supply is the addition of a series of existing market's short-

run curve-shape. It has connection with the points of invariant return in the market of short

period.

The above diagram shows the relation between the different cost curves and how it influences

the price of the product in perfect competition. The manufacturing company affected parts due to

short-term profit making firms having supernormal benefits. That's the condition of having least

proficiency in the long - run production.

Manufacturing Industry in UK:

The manufacturing industry has a vast variety of firms working in the industry. In the UK, it is

considered as production hub for FMCG, technology and furniture etc. this industry adds to

country's economic value of the UK. The manufacturing sector of the UK is third largest sector

in the economy after retail and the service industry.

Following is the impact of perfect competition market in the supply of commodities:

1. Prices: In perfect competition, the main problem the firms face is of price as the firms

have no control over the price of the product in the perfect competition. So the

manufacturing industry has to ascertain the expenses on this basis only, thinking of its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit as well as the revenues. For example, a firm working in the perfect competition

will try to reduce its supply if the profits he will receive are less than what they wishes

for. Another example is of Unilever, which manufactures a variety of products. So this

will result the supplier of the product who will sell it until the price of the goods increases

or the cost exceeds the price of the item. In this, the buyers will also keep on purchasing

the products as long as the satisfaction level of consumers reaches at the top. Until the

supplier has come to the point of market clearing price, which means, when the demand

for the items is equal to the number of products produced at the same price.

2. Competition: The amount of manufacturers in the marketplace is very large that the

rivalry within the country has increased. The level of the competition is influenced by the

amount of the buyers and the sellers. The prices of the products supplied to the retailers

by the producing business will be low in cost and high in the quality, this will effect the

supply of the goods and service in the market. The other competitor will also happen to

decrease the cost of their items with a better customer experience. This will influence the

economic condition of the UK because, the number of purchaser and the sellers are in the

long – run market.

3. Maximize profit: The main objective of the competitive markets is to maximise their

profitability by supplying the goods in the marketplace by valuing its resources at the

lowest cost and by considering the supply curves of the manufacturing industry.

4. Number of sellers: There are different type of commodity which are sold in the market,

which means that the same item are being manufactured. It states that there are infinite

number of manufacturers and in the perfect competition market there is no barrier of

entry and exit which make in difficult to determine for the producer to idealise the

quantity which has to supplied in the market. In UK, it is a constraint which will effect

the economy of the country.

CONCLUSION

From the above report it can be concluded that the supply of goods and services and production

decision have a greater influence from the costs and input prices of a commodity. Businesses

have to work in such a way that the resources are put to the best possible use that they derive the

max profits. The factors which influence the economy of the UK is the labour, entrepreneurship,

will try to reduce its supply if the profits he will receive are less than what they wishes

for. Another example is of Unilever, which manufactures a variety of products. So this

will result the supplier of the product who will sell it until the price of the goods increases

or the cost exceeds the price of the item. In this, the buyers will also keep on purchasing

the products as long as the satisfaction level of consumers reaches at the top. Until the

supplier has come to the point of market clearing price, which means, when the demand

for the items is equal to the number of products produced at the same price.

2. Competition: The amount of manufacturers in the marketplace is very large that the

rivalry within the country has increased. The level of the competition is influenced by the

amount of the buyers and the sellers. The prices of the products supplied to the retailers

by the producing business will be low in cost and high in the quality, this will effect the

supply of the goods and service in the market. The other competitor will also happen to

decrease the cost of their items with a better customer experience. This will influence the

economic condition of the UK because, the number of purchaser and the sellers are in the

long – run market.

3. Maximize profit: The main objective of the competitive markets is to maximise their

profitability by supplying the goods in the marketplace by valuing its resources at the

lowest cost and by considering the supply curves of the manufacturing industry.

4. Number of sellers: There are different type of commodity which are sold in the market,

which means that the same item are being manufactured. It states that there are infinite

number of manufacturers and in the perfect competition market there is no barrier of

entry and exit which make in difficult to determine for the producer to idealise the

quantity which has to supplied in the market. In UK, it is a constraint which will effect

the economy of the country.

CONCLUSION

From the above report it can be concluded that the supply of goods and services and production

decision have a greater influence from the costs and input prices of a commodity. Businesses

have to work in such a way that the resources are put to the best possible use that they derive the

max profits. The factors which influence the economy of the UK is the labour, entrepreneurship,

capital and land. These inputs are the essence of any economy because without these factors, the

industries will not be able to produce commodities. If the goods and services are not supplied at

the right time, the economy will face consequences of the same. Hence, the production decision

is one of the major decision that has to be taken up by the economy and the decision related to

allocation of its resources. The perfect competition market which is mainly used to set a

benchmark for the existing market structure like monopoly. This existing rivalry differentiates

the firm and their products in the manufacturing industry which happens to increase in the prices

to market more profit compared to the rival firm. In this market, the businesses has the

capabilities of controlling the pricing structure in the industry.

industries will not be able to produce commodities. If the goods and services are not supplied at

the right time, the economy will face consequences of the same. Hence, the production decision

is one of the major decision that has to be taken up by the economy and the decision related to

allocation of its resources. The perfect competition market which is mainly used to set a

benchmark for the existing market structure like monopoly. This existing rivalry differentiates

the firm and their products in the manufacturing industry which happens to increase in the prices

to market more profit compared to the rival firm. In this market, the businesses has the

capabilities of controlling the pricing structure in the industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Krugman and Wells. 2020. Essentials of Economics. New York: Worth Publishers. Pages 355-

451.

Young, M. 2021 Lecture 6: Supply curve, inputs, and costs. MOD3327 Economics for Business.

Anglia Ruskin University of London.

Young, M. 2021 Lecture 7: Perfect competition and market efficiency. MOD3327 Economics

for Business. Anglia Ruskin University of London.

UK news sources: BBC News, Financial Times newspaper, London Evening Standard, The

Economist, The Guardian newspaper, The Independent, The Telegraph

UK Government information sources: UK Office of National Statistics (ONS) UK Government

websites ending in “gov.uk” or “parliament.uk”

Books and Journals

Krugman and Wells. 2020. Essentials of Economics. New York: Worth Publishers. Pages 355-

451.

Young, M. 2021 Lecture 6: Supply curve, inputs, and costs. MOD3327 Economics for Business.

Anglia Ruskin University of London.

Young, M. 2021 Lecture 7: Perfect competition and market efficiency. MOD3327 Economics

for Business. Anglia Ruskin University of London.

UK news sources: BBC News, Financial Times newspaper, London Evening Standard, The

Economist, The Guardian newspaper, The Independent, The Telegraph

UK Government information sources: UK Office of National Statistics (ONS) UK Government

websites ending in “gov.uk” or “parliament.uk”

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.