Contemporary Business Economics Report: Theories and Models Analysis

VerifiedAdded on 2022/08/25

|14

|3272

|26

Report

AI Summary

This report delves into essential microeconomic concepts crucial for business operations, focusing on the laws of demand and supply. It analyzes the factors influencing the movement of demand and supply curves, providing examples to illustrate these principles. The report then contrasts classical economic theories prevalent in the 20th century with the Keynesian economic theory, which is more relevant in the 21st century. The comparison includes an examination of how these theories impact business practices and economic management. The report includes an introduction to the concepts, a detailed discussion of the laws of demand and supply, and a comparison between the economic theories of the 20th and 21st centuries. The report concludes with a summary of the key findings and their implications for contemporary business economics.

Running Head: Economics

0

Contemporary Business Economics

1/16/2020

0

Contemporary Business Economics

1/16/2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics

1

Contents

Introduction........................................................................................................................2

Task 1................................................................................................................................2

Law of demand...............................................................................................................2

Movement in the demand curve.....................................................................................3

Factors which led to the change in the demand curve..................................................3

Law of supply..................................................................................................................5

Movement in the supply curve.......................................................................................6

Factors which led to the supply in the supply curve.......................................................7

Task 2................................................................................................................................9

Comparing the emerging theories and models of the 21 century with the 20 century. .9

Conclusion.......................................................................................................................11

References.......................................................................................................................12

1

Contents

Introduction........................................................................................................................2

Task 1................................................................................................................................2

Law of demand...............................................................................................................2

Movement in the demand curve.....................................................................................3

Factors which led to the change in the demand curve..................................................3

Law of supply..................................................................................................................5

Movement in the supply curve.......................................................................................6

Factors which led to the supply in the supply curve.......................................................7

Task 2................................................................................................................................9

Comparing the emerging theories and models of the 21 century with the 20 century. .9

Conclusion.......................................................................................................................11

References.......................................................................................................................12

Economics

2

Introduction

In microeconomics, it is necessary to consider the concepts and principles which are

essential for the retail business. This report includes an analysis of the law of demand

and the law of supply. The evaluation of alternative theories of economics is discussed

which are essential for the business (Vigersky, et al., 2014). The movement of the

supply and demand curve will be discussed which are affected because of the various

factors. Emerging philosophies and models of the 20th and 21st century will be discussed

which are related to the practices of modern business.

Task 1

Law of demand

It can be stated as the inverse connection among the price value and the amount

demanded the goods and services. As per this law, if the price of any product enhanced

in the market then quantity demanded that particular product will fall but the other

factors being the constant.

Example: The items of the grocery are purchased by the consumer more when there

are prices are lower. Similarly, when the prices of the grocery increase, the demand for

food decreases (Thimmapuram and Kim, 2013).

2

Introduction

In microeconomics, it is necessary to consider the concepts and principles which are

essential for the retail business. This report includes an analysis of the law of demand

and the law of supply. The evaluation of alternative theories of economics is discussed

which are essential for the business (Vigersky, et al., 2014). The movement of the

supply and demand curve will be discussed which are affected because of the various

factors. Emerging philosophies and models of the 20th and 21st century will be discussed

which are related to the practices of modern business.

Task 1

Law of demand

It can be stated as the inverse connection among the price value and the amount

demanded the goods and services. As per this law, if the price of any product enhanced

in the market then quantity demanded that particular product will fall but the other

factors being the constant.

Example: The items of the grocery are purchased by the consumer more when there

are prices are lower. Similarly, when the prices of the grocery increase, the demand for

food decreases (Thimmapuram and Kim, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics

3

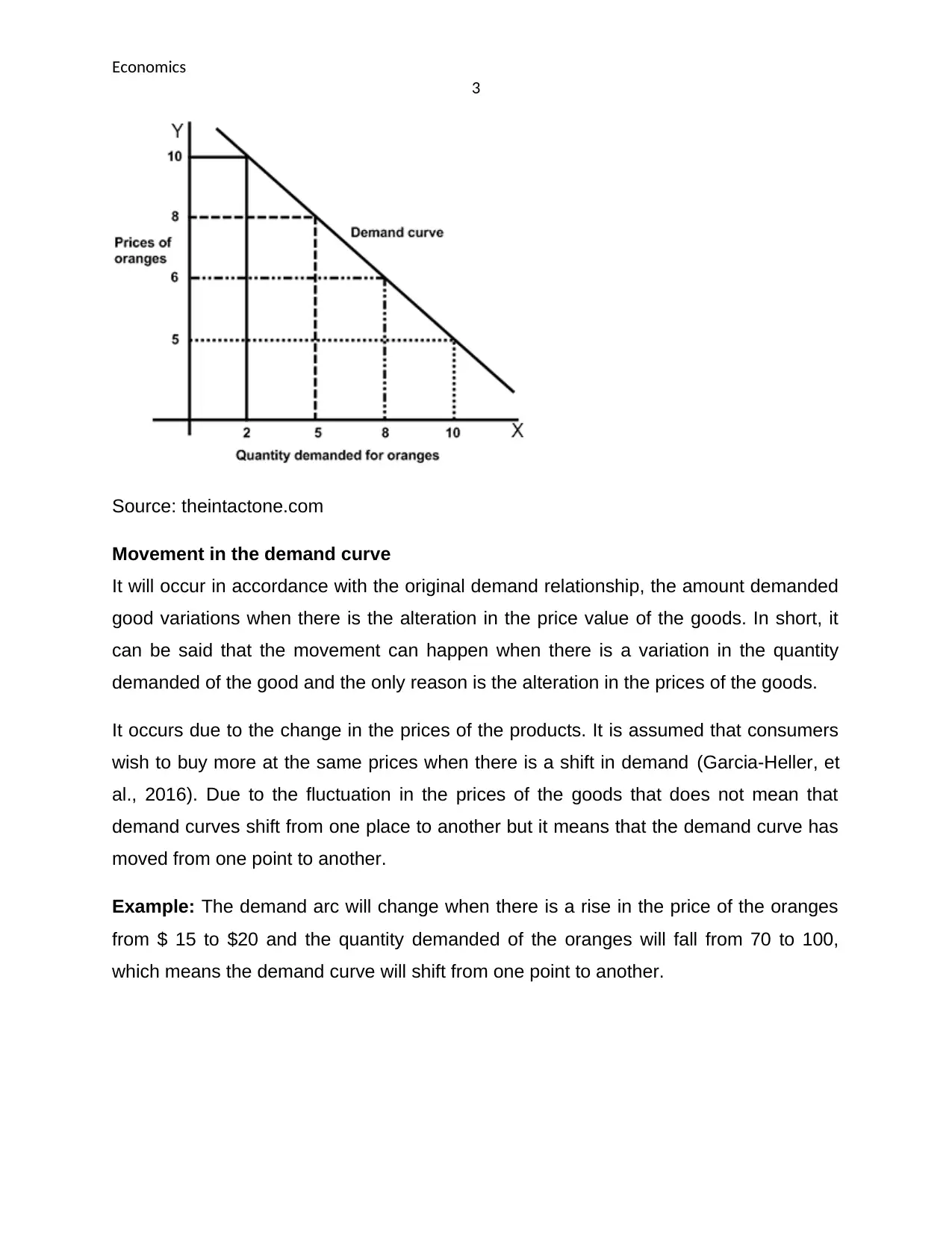

Source: theintactone.com

Movement in the demand curve

It will occur in accordance with the original demand relationship, the amount demanded

good variations when there is the alteration in the price value of the goods. In short, it

can be said that the movement can happen when there is a variation in the quantity

demanded of the good and the only reason is the alteration in the prices of the goods.

It occurs due to the change in the prices of the products. It is assumed that consumers

wish to buy more at the same prices when there is a shift in demand (Garcia-Heller, et

al., 2016). Due to the fluctuation in the prices of the goods that does not mean that

demand curves shift from one place to another but it means that the demand curve has

moved from one point to another.

Example: The demand arc will change when there is a rise in the price of the oranges

from $ 15 to $20 and the quantity demanded of the oranges will fall from 70 to 100,

which means the demand curve will shift from one point to another.

3

Source: theintactone.com

Movement in the demand curve

It will occur in accordance with the original demand relationship, the amount demanded

good variations when there is the alteration in the price value of the goods. In short, it

can be said that the movement can happen when there is a variation in the quantity

demanded of the good and the only reason is the alteration in the prices of the goods.

It occurs due to the change in the prices of the products. It is assumed that consumers

wish to buy more at the same prices when there is a shift in demand (Garcia-Heller, et

al., 2016). Due to the fluctuation in the prices of the goods that does not mean that

demand curves shift from one place to another but it means that the demand curve has

moved from one point to another.

Example: The demand arc will change when there is a rise in the price of the oranges

from $ 15 to $20 and the quantity demanded of the oranges will fall from 70 to 100,

which means the demand curve will shift from one point to another.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics

4

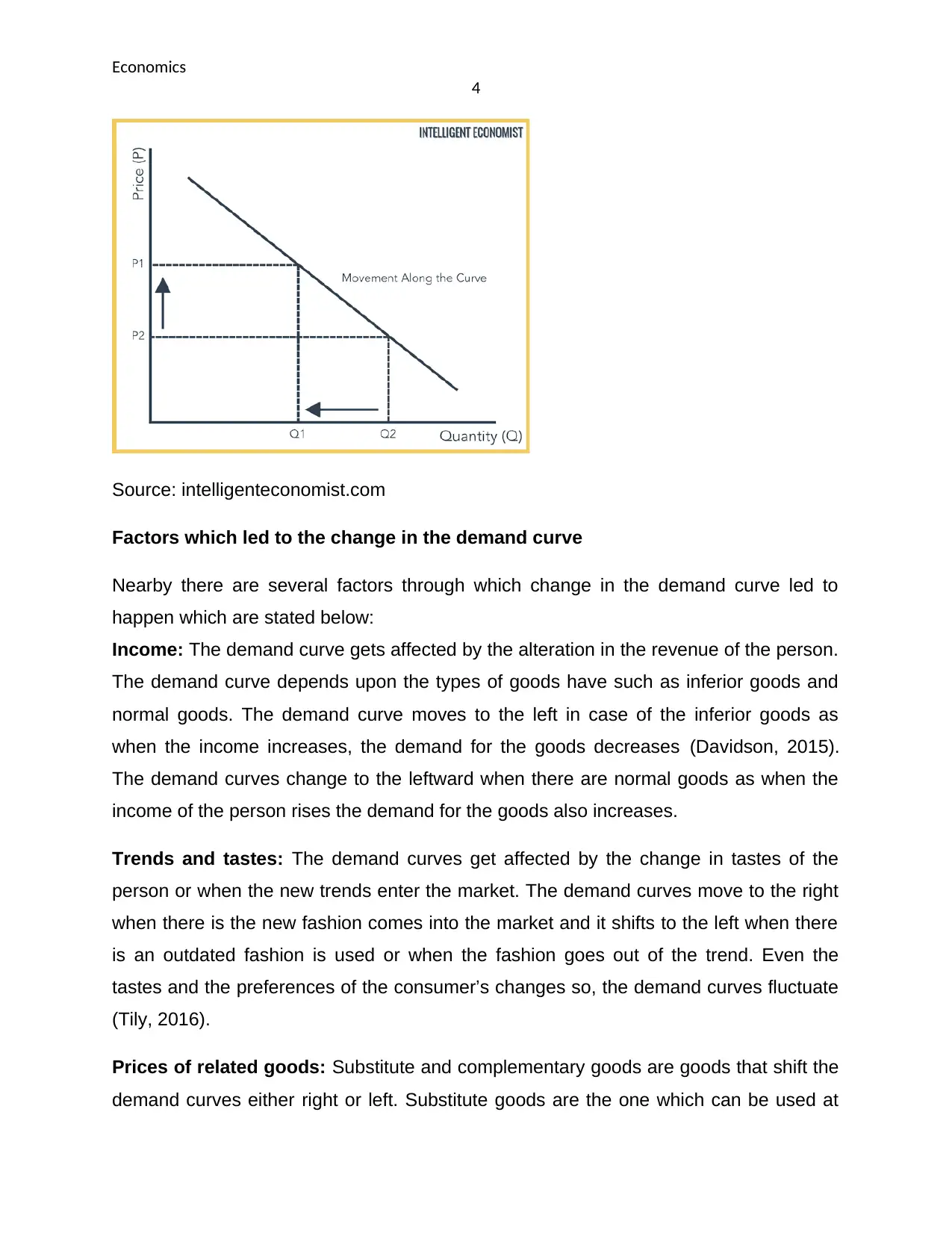

Source: intelligenteconomist.com

Factors which led to the change in the demand curve

Nearby there are several factors through which change in the demand curve led to

happen which are stated below:

Income: The demand curve gets affected by the alteration in the revenue of the person.

The demand curve depends upon the types of goods have such as inferior goods and

normal goods. The demand curve moves to the left in case of the inferior goods as

when the income increases, the demand for the goods decreases (Davidson, 2015).

The demand curves change to the leftward when there are normal goods as when the

income of the person rises the demand for the goods also increases.

Trends and tastes: The demand curves get affected by the change in tastes of the

person or when the new trends enter the market. The demand curves move to the right

when there is the new fashion comes into the market and it shifts to the left when there

is an outdated fashion is used or when the fashion goes out of the trend. Even the

tastes and the preferences of the consumer’s changes so, the demand curves fluctuate

(Tily, 2016).

Prices of related goods: Substitute and complementary goods are goods that shift the

demand curves either right or left. Substitute goods are the one which can be used at

4

Source: intelligenteconomist.com

Factors which led to the change in the demand curve

Nearby there are several factors through which change in the demand curve led to

happen which are stated below:

Income: The demand curve gets affected by the alteration in the revenue of the person.

The demand curve depends upon the types of goods have such as inferior goods and

normal goods. The demand curve moves to the left in case of the inferior goods as

when the income increases, the demand for the goods decreases (Davidson, 2015).

The demand curves change to the leftward when there are normal goods as when the

income of the person rises the demand for the goods also increases.

Trends and tastes: The demand curves get affected by the change in tastes of the

person or when the new trends enter the market. The demand curves move to the right

when there is the new fashion comes into the market and it shifts to the left when there

is an outdated fashion is used or when the fashion goes out of the trend. Even the

tastes and the preferences of the consumer’s changes so, the demand curves fluctuate

(Tily, 2016).

Prices of related goods: Substitute and complementary goods are goods that shift the

demand curves either right or left. Substitute goods are the one which can be used at

Economics

5

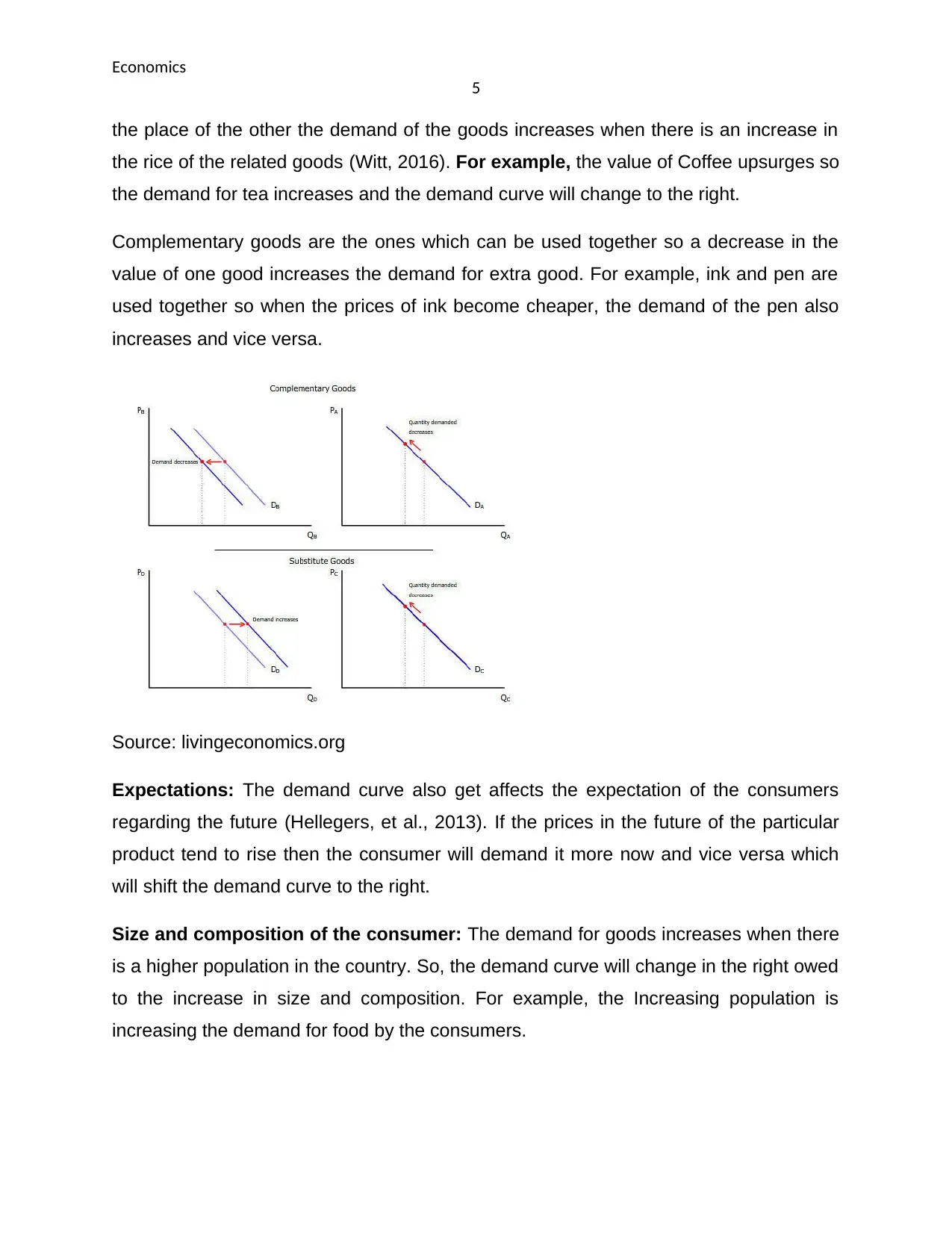

the place of the other the demand of the goods increases when there is an increase in

the rice of the related goods (Witt, 2016). For example, the value of Coffee upsurges so

the demand for tea increases and the demand curve will change to the right.

Complementary goods are the ones which can be used together so a decrease in the

value of one good increases the demand for extra good. For example, ink and pen are

used together so when the prices of ink become cheaper, the demand of the pen also

increases and vice versa.

Source: livingeconomics.org

Expectations: The demand curve also get affects the expectation of the consumers

regarding the future (Hellegers, et al., 2013). If the prices in the future of the particular

product tend to rise then the consumer will demand it more now and vice versa which

will shift the demand curve to the right.

Size and composition of the consumer: The demand for goods increases when there

is a higher population in the country. So, the demand curve will change in the right owed

to the increase in size and composition. For example, the Increasing population is

increasing the demand for food by the consumers.

5

the place of the other the demand of the goods increases when there is an increase in

the rice of the related goods (Witt, 2016). For example, the value of Coffee upsurges so

the demand for tea increases and the demand curve will change to the right.

Complementary goods are the ones which can be used together so a decrease in the

value of one good increases the demand for extra good. For example, ink and pen are

used together so when the prices of ink become cheaper, the demand of the pen also

increases and vice versa.

Source: livingeconomics.org

Expectations: The demand curve also get affects the expectation of the consumers

regarding the future (Hellegers, et al., 2013). If the prices in the future of the particular

product tend to rise then the consumer will demand it more now and vice versa which

will shift the demand curve to the right.

Size and composition of the consumer: The demand for goods increases when there

is a higher population in the country. So, the demand curve will change in the right owed

to the increase in size and composition. For example, the Increasing population is

increasing the demand for food by the consumers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics

6

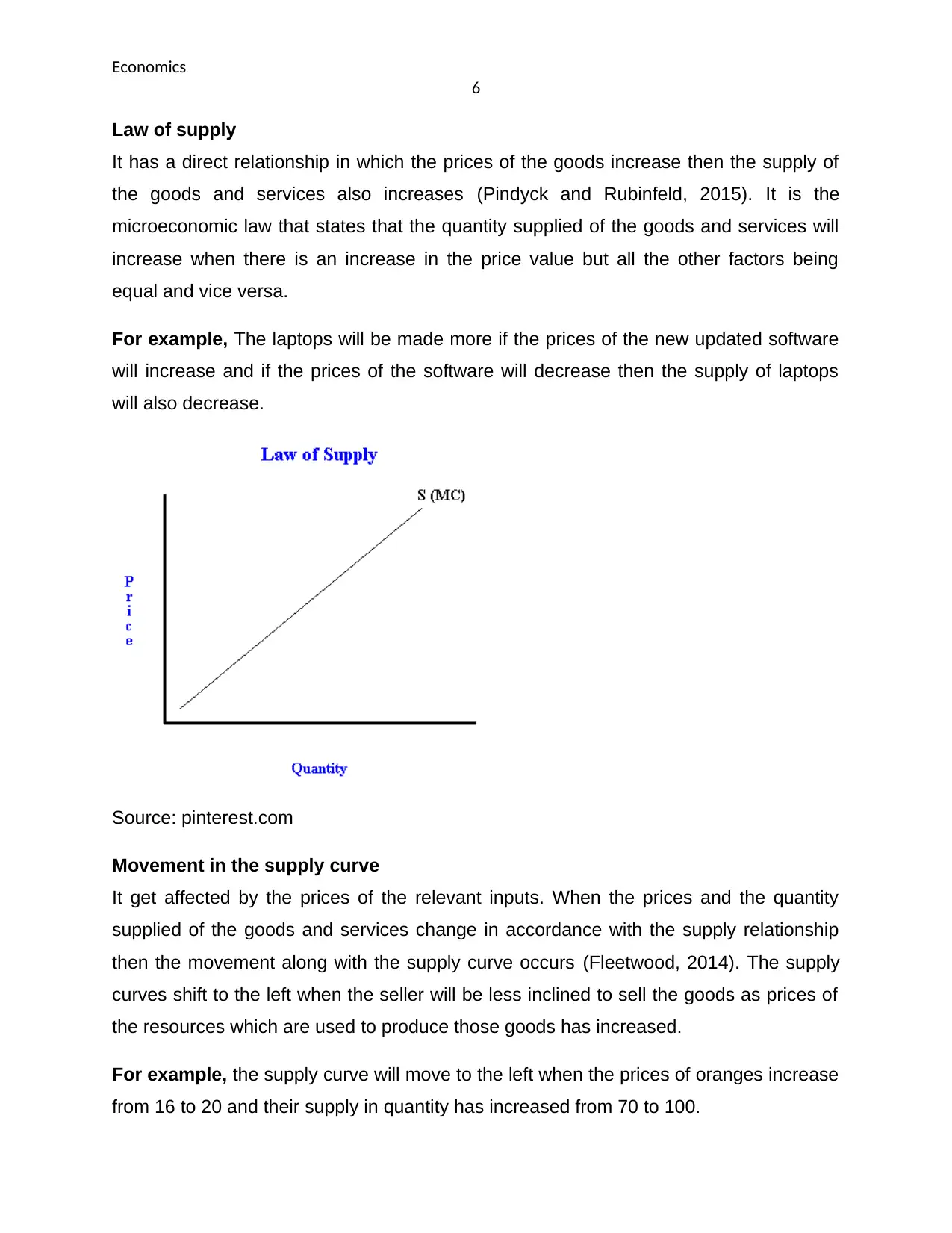

Law of supply

It has a direct relationship in which the prices of the goods increase then the supply of

the goods and services also increases (Pindyck and Rubinfeld, 2015). It is the

microeconomic law that states that the quantity supplied of the goods and services will

increase when there is an increase in the price value but all the other factors being

equal and vice versa.

For example, The laptops will be made more if the prices of the new updated software

will increase and if the prices of the software will decrease then the supply of laptops

will also decrease.

Source: pinterest.com

Movement in the supply curve

It get affected by the prices of the relevant inputs. When the prices and the quantity

supplied of the goods and services change in accordance with the supply relationship

then the movement along with the supply curve occurs (Fleetwood, 2014). The supply

curves shift to the left when the seller will be less inclined to sell the goods as prices of

the resources which are used to produce those goods has increased.

For example, the supply curve will move to the left when the prices of oranges increase

from 16 to 20 and their supply in quantity has increased from 70 to 100.

6

Law of supply

It has a direct relationship in which the prices of the goods increase then the supply of

the goods and services also increases (Pindyck and Rubinfeld, 2015). It is the

microeconomic law that states that the quantity supplied of the goods and services will

increase when there is an increase in the price value but all the other factors being

equal and vice versa.

For example, The laptops will be made more if the prices of the new updated software

will increase and if the prices of the software will decrease then the supply of laptops

will also decrease.

Source: pinterest.com

Movement in the supply curve

It get affected by the prices of the relevant inputs. When the prices and the quantity

supplied of the goods and services change in accordance with the supply relationship

then the movement along with the supply curve occurs (Fleetwood, 2014). The supply

curves shift to the left when the seller will be less inclined to sell the goods as prices of

the resources which are used to produce those goods has increased.

For example, the supply curve will move to the left when the prices of oranges increase

from 16 to 20 and their supply in quantity has increased from 70 to 100.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics

7

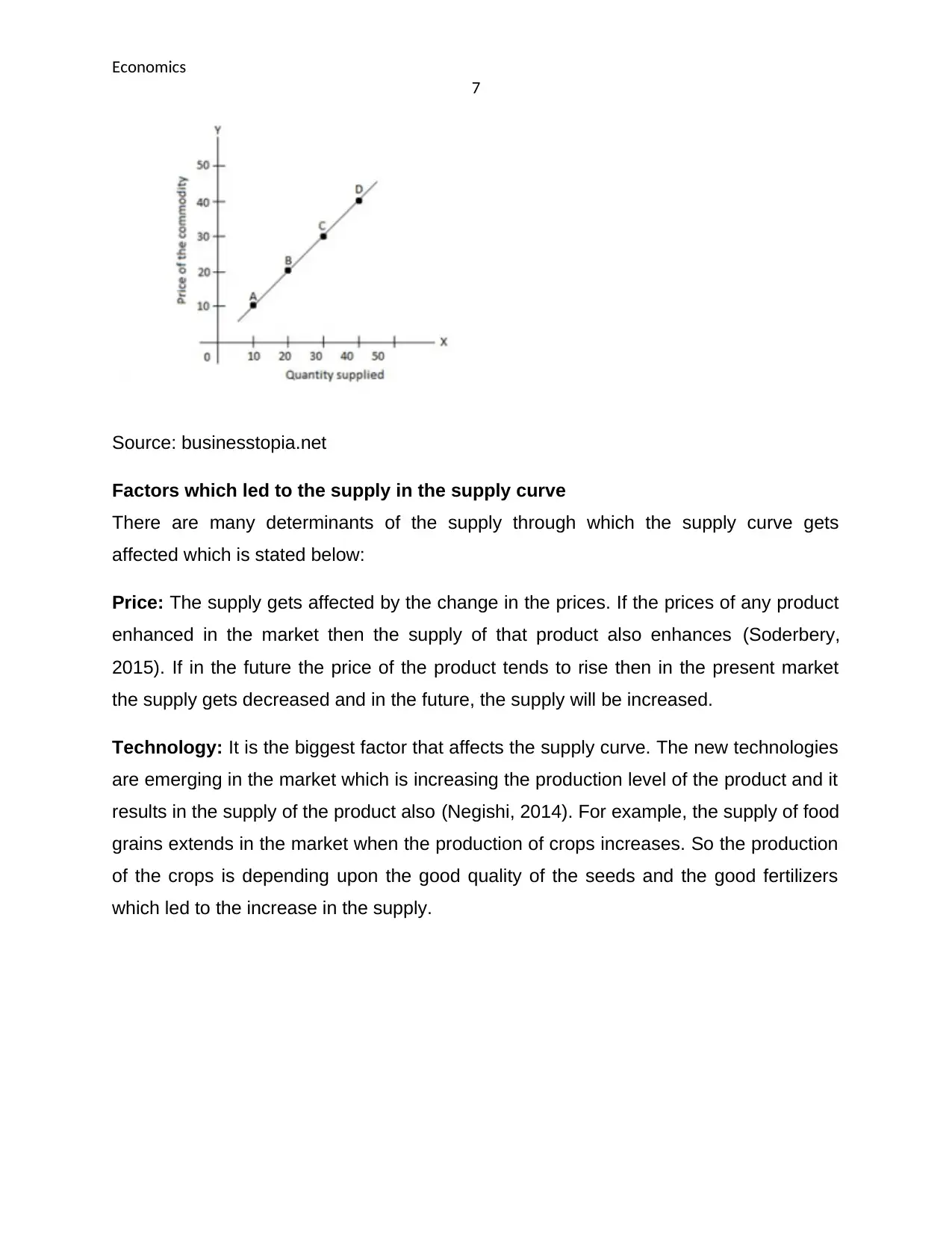

Source: businesstopia.net

Factors which led to the supply in the supply curve

There are many determinants of the supply through which the supply curve gets

affected which is stated below:

Price: The supply gets affected by the change in the prices. If the prices of any product

enhanced in the market then the supply of that product also enhances (Soderbery,

2015). If in the future the price of the product tends to rise then in the present market

the supply gets decreased and in the future, the supply will be increased.

Technology: It is the biggest factor that affects the supply curve. The new technologies

are emerging in the market which is increasing the production level of the product and it

results in the supply of the product also (Negishi, 2014). For example, the supply of food

grains extends in the market when the production of crops increases. So the production

of the crops is depending upon the good quality of the seeds and the good fertilizers

which led to the increase in the supply.

7

Source: businesstopia.net

Factors which led to the supply in the supply curve

There are many determinants of the supply through which the supply curve gets

affected which is stated below:

Price: The supply gets affected by the change in the prices. If the prices of any product

enhanced in the market then the supply of that product also enhances (Soderbery,

2015). If in the future the price of the product tends to rise then in the present market

the supply gets decreased and in the future, the supply will be increased.

Technology: It is the biggest factor that affects the supply curve. The new technologies

are emerging in the market which is increasing the production level of the product and it

results in the supply of the product also (Negishi, 2014). For example, the supply of food

grains extends in the market when the production of crops increases. So the production

of the crops is depending upon the good quality of the seeds and the good fertilizers

which led to the increase in the supply.

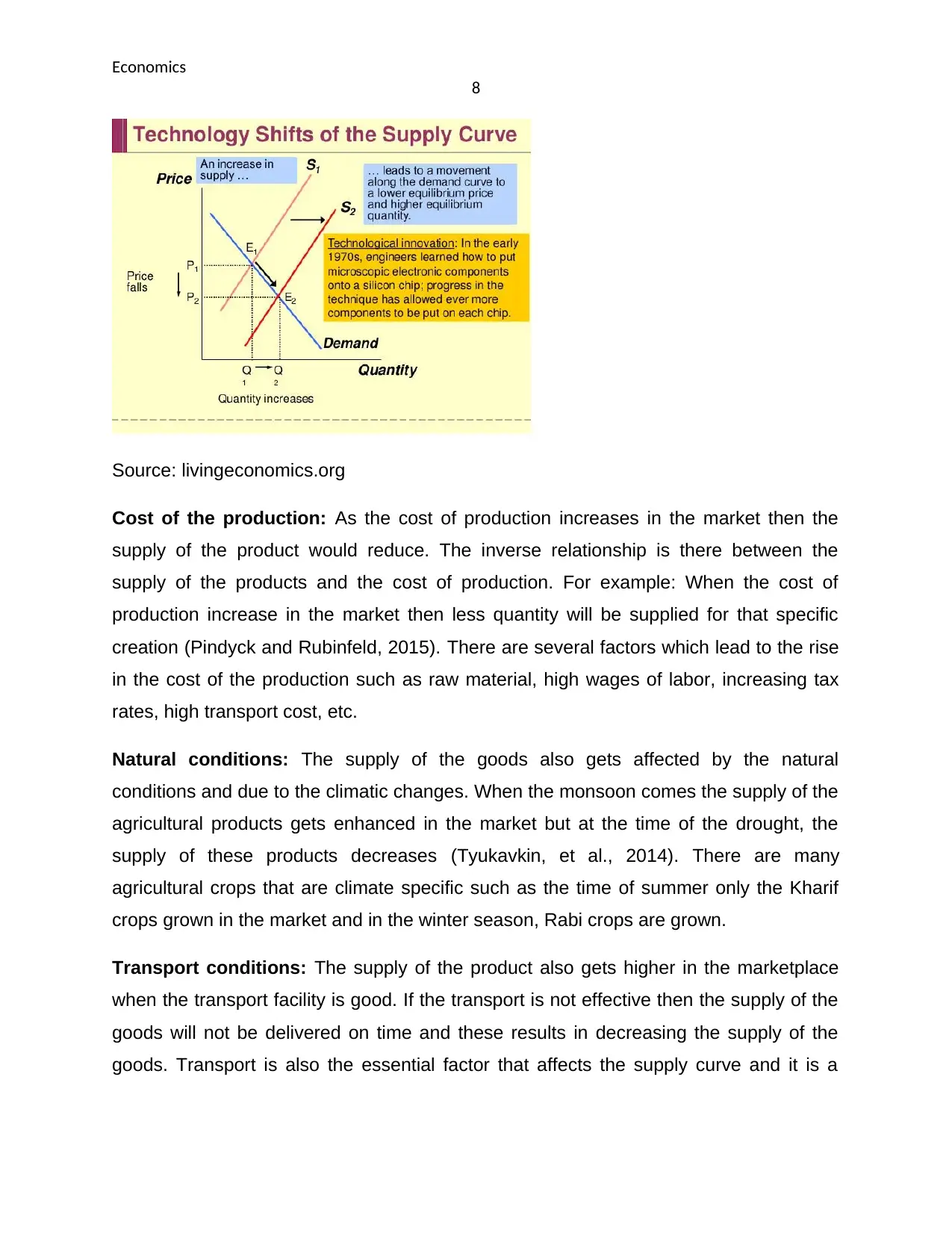

Economics

8

Source: livingeconomics.org

Cost of the production: As the cost of production increases in the market then the

supply of the product would reduce. The inverse relationship is there between the

supply of the products and the cost of production. For example: When the cost of

production increase in the market then less quantity will be supplied for that specific

creation (Pindyck and Rubinfeld, 2015). There are several factors which lead to the rise

in the cost of the production such as raw material, high wages of labor, increasing tax

rates, high transport cost, etc.

Natural conditions: The supply of the goods also gets affected by the natural

conditions and due to the climatic changes. When the monsoon comes the supply of the

agricultural products gets enhanced in the market but at the time of the drought, the

supply of these products decreases (Tyukavkin, et al., 2014). There are many

agricultural crops that are climate specific such as the time of summer only the Kharif

crops grown in the market and in the winter season, Rabi crops are grown.

Transport conditions: The supply of the product also gets higher in the marketplace

when the transport facility is good. If the transport is not effective then the supply of the

goods will not be delivered on time and these results in decreasing the supply of the

goods. Transport is also the essential factor that affects the supply curve and it is a

8

Source: livingeconomics.org

Cost of the production: As the cost of production increases in the market then the

supply of the product would reduce. The inverse relationship is there between the

supply of the products and the cost of production. For example: When the cost of

production increase in the market then less quantity will be supplied for that specific

creation (Pindyck and Rubinfeld, 2015). There are several factors which lead to the rise

in the cost of the production such as raw material, high wages of labor, increasing tax

rates, high transport cost, etc.

Natural conditions: The supply of the goods also gets affected by the natural

conditions and due to the climatic changes. When the monsoon comes the supply of the

agricultural products gets enhanced in the market but at the time of the drought, the

supply of these products decreases (Tyukavkin, et al., 2014). There are many

agricultural crops that are climate specific such as the time of summer only the Kharif

crops grown in the market and in the winter season, Rabi crops are grown.

Transport conditions: The supply of the product also gets higher in the marketplace

when the transport facility is good. If the transport is not effective then the supply of the

goods will not be delivered on time and these results in decreasing the supply of the

goods. Transport is also the essential factor that affects the supply curve and it is a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics

9

constraint factor to the supply of the product which would not increase with the increase

in the price (Parker, et al., 2010).

Availability of the raw materials: The important factor of the supply is the availability

of the things as the production of the goods increase when there are certain inputs

available to make those goods such as equipment, machines, raw materials, etc. The

supply of the product will increase when there is a sufficient quantity of the inputs is

available at the lower prices.

Task 2

Comparing the emerging theories and models of the 21 century with the 20

century

The Classical economic theory used in the 20th century

This theory is used in the 20th century as it cannot include all the aspects of economics

and it is used in the process of traditional business. This theory manages all the

traditional aspects and it promotes the laissez-faire policy. The business-cycle easily

manage the process of the management and all the economic process of the business

can be easily maintained by using this theory. It enables the private entities to affect the

production factors as they are more important in the overall process. The limited

government includes in the aspects of this theory and it also uses a balanced budget

and little debt (Lillo, et al., 2013).

Classical theory was used to direct towards macroeconomics which was based on

unrestricted the markets and pursuit of an individual’s self-interest. The key

assumptions were included in the classical theory which was flexible prices; say’s the

law and saving-investment equality. In contemporary economics, the classical theory

was applied in which the employee’s economic and physical needs were considered.

Social needs and job satisfaction were not considered. For economic development in

business, the classical theory was implemented during the 20th century (Morais, et al.,

2014). It was expected to increase the profits by increasing the investment which helps

in adding the existing stock capital and improving the techniques. In modern business

9

constraint factor to the supply of the product which would not increase with the increase

in the price (Parker, et al., 2010).

Availability of the raw materials: The important factor of the supply is the availability

of the things as the production of the goods increase when there are certain inputs

available to make those goods such as equipment, machines, raw materials, etc. The

supply of the product will increase when there is a sufficient quantity of the inputs is

available at the lower prices.

Task 2

Comparing the emerging theories and models of the 21 century with the 20

century

The Classical economic theory used in the 20th century

This theory is used in the 20th century as it cannot include all the aspects of economics

and it is used in the process of traditional business. This theory manages all the

traditional aspects and it promotes the laissez-faire policy. The business-cycle easily

manage the process of the management and all the economic process of the business

can be easily maintained by using this theory. It enables the private entities to affect the

production factors as they are more important in the overall process. The limited

government includes in the aspects of this theory and it also uses a balanced budget

and little debt (Lillo, et al., 2013).

Classical theory was used to direct towards macroeconomics which was based on

unrestricted the markets and pursuit of an individual’s self-interest. The key

assumptions were included in the classical theory which was flexible prices; say’s the

law and saving-investment equality. In contemporary economics, the classical theory

was applied in which the employee’s economic and physical needs were considered.

Social needs and job satisfaction were not considered. For economic development in

business, the classical theory was implemented during the 20th century (Morais, et al.,

2014). It was expected to increase the profits by increasing the investment which helps

in adding the existing stock capital and improving the techniques. In modern business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics

10

practices, the adoption of the classical theory is required for managing the activities and

profits of the business.

The Keynesian Economic Theory used by 21st century

Keynesian theory is a famous theory used in economics in the era of the 21 st century.

This theory is widely used by the business to manage the economics in the business

(Soderbery, 2015). It is an economic theory that includes total expenditure in the

economy and its impacts on the output results and price increases. This theory is

adopted for increasing the expenditures of the government and lowers the taxes to

manage the demand and also maintain the global economy out of the depression. This

theory is adopted by several business organizations to manage their demand process

as it gives a large impact on the inflation rate of the business.

This theory is totally different from the theories used in the 20th century as the theories

used in the 20th century are different in nature and the demand is not related in the

theory of the 20th century. This theory is based on two main ideas. The second idea

relates to wages and price which can be sticky and increases unemployment in the

country. This theory is mainly related to the tax simulation and this theory is used in a

proper form to stimulate the tax of the organization (Kurz and Salvadori, 2014).

In the 21st century, the entire business functions become advance so they need an

advanced theory for their management of economics. Keynesian theory helps in solving

all the problems related to economics mainly it relates to the demand and the tax of the

company (Green, 2016). The model of Keynesian theory is a simple Keynesian model

(SKM) which shows that national output reaches its equilibrium value to manage the

process of the demand. The expenditure of the company and government is shown in

the overall process of the economic output. The theory supports the expansionary policy

to manage all the expenditures of the organization.

This theory improves all the economics process of 21st century and business achieves

several objectives by using this theory in their management. But this policy affects

inflation. This theory argues that the spending of government is important for managing

full employment (Joung and Kim, 2013). In this century, this theory also creates several

10

practices, the adoption of the classical theory is required for managing the activities and

profits of the business.

The Keynesian Economic Theory used by 21st century

Keynesian theory is a famous theory used in economics in the era of the 21 st century.

This theory is widely used by the business to manage the economics in the business

(Soderbery, 2015). It is an economic theory that includes total expenditure in the

economy and its impacts on the output results and price increases. This theory is

adopted for increasing the expenditures of the government and lowers the taxes to

manage the demand and also maintain the global economy out of the depression. This

theory is adopted by several business organizations to manage their demand process

as it gives a large impact on the inflation rate of the business.

This theory is totally different from the theories used in the 20th century as the theories

used in the 20th century are different in nature and the demand is not related in the

theory of the 20th century. This theory is based on two main ideas. The second idea

relates to wages and price which can be sticky and increases unemployment in the

country. This theory is mainly related to the tax simulation and this theory is used in a

proper form to stimulate the tax of the organization (Kurz and Salvadori, 2014).

In the 21st century, the entire business functions become advance so they need an

advanced theory for their management of economics. Keynesian theory helps in solving

all the problems related to economics mainly it relates to the demand and the tax of the

company (Green, 2016). The model of Keynesian theory is a simple Keynesian model

(SKM) which shows that national output reaches its equilibrium value to manage the

process of the demand. The expenditure of the company and government is shown in

the overall process of the economic output. The theory supports the expansionary policy

to manage all the expenditures of the organization.

This theory improves all the economics process of 21st century and business achieves

several objectives by using this theory in their management. But this policy affects

inflation. This theory argues that the spending of government is important for managing

full employment (Joung and Kim, 2013). In this century, this theory also creates several

Economics

11

problems in the management of fiscal policy and the management of tax. The economic

growth cannot increase by this process but it maintains the money supply. It affects the

overall cost of the tax and increases the poverty rate. Sometimes, this process affects

the demands of consumers and creates many problems for the business.

Conclusion

In order to conclude the report, it is analyzed that the various factors affect the

movement of demand and supply curve. The law of demand and law of supply are

required to be included in the retailing business. The economic theory of the 20th

century which was used in contemporary economics includes the classical theory which

is discussed in the report and in modern business practices; the adoption of Keynesian

theory is required in the 21st century for achieving the goals and objectives of the

management.

11

problems in the management of fiscal policy and the management of tax. The economic

growth cannot increase by this process but it maintains the money supply. It affects the

overall cost of the tax and increases the poverty rate. Sometimes, this process affects

the demands of consumers and creates many problems for the business.

Conclusion

In order to conclude the report, it is analyzed that the various factors affect the

movement of demand and supply curve. The law of demand and law of supply are

required to be included in the retailing business. The economic theory of the 20th

century which was used in contemporary economics includes the classical theory which

is discussed in the report and in modern business practices; the adoption of Keynesian

theory is required in the 21st century for achieving the goals and objectives of the

management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.