Economics of the UK Housing Market: Analysis of Trends and Factors

VerifiedAdded on 2021/04/24

|17

|3292

|226

Report

AI Summary

This report provides a comprehensive analysis of the UK housing market, examining trends in house prices from 2006 to 2016, with a particular focus on the factors influencing these prices. It delves into both demand-side factors, such as economic growth, affordability, interest rates, population, and mortgage availability, and supply-side factors, including construction rates and planning restrictions. The report also investigates the implications of housing shortages and evaluates the impact of various government schemes, including Help to Buy and Shared Ownership, on the housing market and affordability. The analysis highlights the interplay of economic conditions, government interventions, and market dynamics, providing a detailed understanding of the UK housing sector.

Running Head: ECONOMICS FOR BUSINESS

Economics for Business

Name of the Student

Name of the University

Author note

Economics for Business

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS FOR BUSINESS

Table of Contents

Introduction................................................................................................................................2

Trend in UK house prices..........................................................................................................2

Factors affecting housing price..................................................................................................4

Demand side factors of UK housing market..........................................................................4

Supply side factor of UK housing market..............................................................................8

Implication of Housing shortage..........................................................................................10

Different government schemes in the housing market.............................................................11

Help to Buy..........................................................................................................................11

Shared Ownership................................................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................15

Table of Contents

Introduction................................................................................................................................2

Trend in UK house prices..........................................................................................................2

Factors affecting housing price..................................................................................................4

Demand side factors of UK housing market..........................................................................4

Supply side factor of UK housing market..............................................................................8

Implication of Housing shortage..........................................................................................10

Different government schemes in the housing market.............................................................11

Help to Buy..........................................................................................................................11

Shared Ownership................................................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................15

2ECONOMICS FOR BUSINESS

Introduction

The analysis of housing market of UK is an interesting aspect for several reasons.

Housing market in UK holds a pivotal position in the economy. As compared to other

European nations UK has a much higher owner occupation rate. In 2011, UK’s owner

occupation rate was 70% as compared to a rate of 45% in Germany and 56% in France. The

housing price in UK has constituted a steady upward trend in the last few years. The housing

market experienced two biggest bubble during world crisis of 1980 and 2008 (Wilcox and

Perry 2014). The price showed an upward trend from 1995 to late 2000 and suddenly

declined in the phase of crisis. The bubbles are mainly caused by ease of bank regulation and

restricted supply resulted from restriction imposed on land. Different demand and supply side

factors together determine housing price in UK. These factors include cost of construction,

affordability, supply of credit, disposable income and others. The affordability of people and

hence housing prices are also influenced by different government schemes such as Help to

buy scheme, Shared Ownership, Starter Homes Scheme, right to buy and others (Kuttner

2014). The report evaluates factors affecting UK housing price from 2006 to 2016.

Additionally attention has been also given on impact of different government schemes on

housing price.

Trend in UK house prices

Introduction

The analysis of housing market of UK is an interesting aspect for several reasons.

Housing market in UK holds a pivotal position in the economy. As compared to other

European nations UK has a much higher owner occupation rate. In 2011, UK’s owner

occupation rate was 70% as compared to a rate of 45% in Germany and 56% in France. The

housing price in UK has constituted a steady upward trend in the last few years. The housing

market experienced two biggest bubble during world crisis of 1980 and 2008 (Wilcox and

Perry 2014). The price showed an upward trend from 1995 to late 2000 and suddenly

declined in the phase of crisis. The bubbles are mainly caused by ease of bank regulation and

restricted supply resulted from restriction imposed on land. Different demand and supply side

factors together determine housing price in UK. These factors include cost of construction,

affordability, supply of credit, disposable income and others. The affordability of people and

hence housing prices are also influenced by different government schemes such as Help to

buy scheme, Shared Ownership, Starter Homes Scheme, right to buy and others (Kuttner

2014). The report evaluates factors affecting UK housing price from 2006 to 2016.

Additionally attention has been also given on impact of different government schemes on

housing price.

Trend in UK house prices

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS FOR BUSINESS

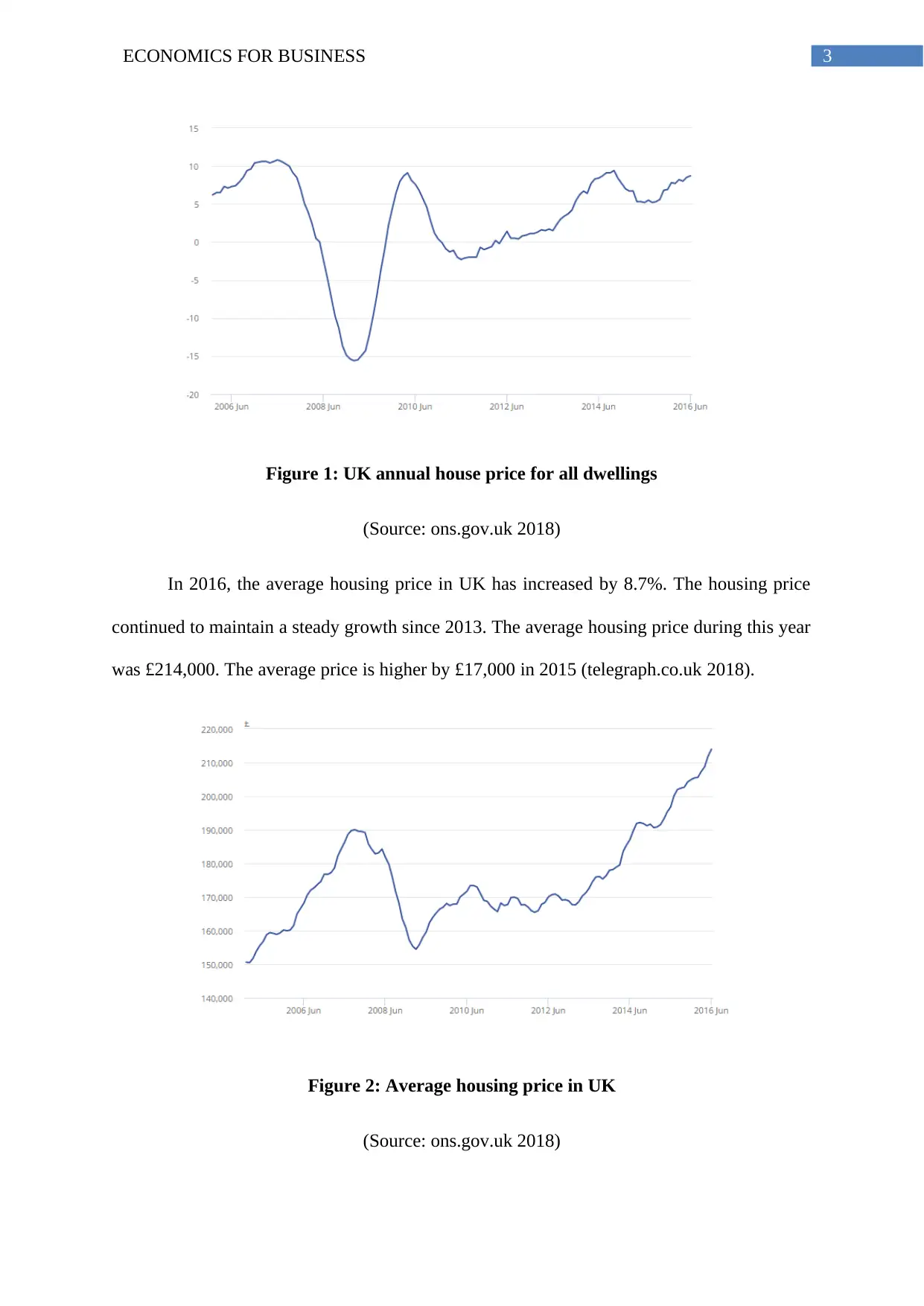

Figure 1: UK annual house price for all dwellings

(Source: ons.gov.uk 2018)

In 2016, the average housing price in UK has increased by 8.7%. The housing price

continued to maintain a steady growth since 2013. The average housing price during this year

was £214,000. The average price is higher by £17,000 in 2015 (telegraph.co.uk 2018).

Figure 2: Average housing price in UK

(Source: ons.gov.uk 2018)

Figure 1: UK annual house price for all dwellings

(Source: ons.gov.uk 2018)

In 2016, the average housing price in UK has increased by 8.7%. The housing price

continued to maintain a steady growth since 2013. The average housing price during this year

was £214,000. The average price is higher by £17,000 in 2015 (telegraph.co.uk 2018).

Figure 2: Average housing price in UK

(Source: ons.gov.uk 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS FOR BUSINESS

The average housing price in UK has constituted a steady upward trend from 2006 to

2016. England is the main contributor of growing housing price trend in UK. Housing price

in England grew by 9.3% in the year 2016. The average house price in England now is

£229,000. In Wales, housing price grew by 4.9% for the past few years. The housing price is

recorded as £145,000 (ons.gov.uk 2018). The average house price in Scotland is £143,000

recording a growth rate of 4.6%. In Northern Ireland, housing price stands at £123,000.

The regional housing price trend shows London continues to be region having highest

average house price of £472,000. The region was followed by South East and East England

region where housing price stands at £309,000 and £270,000 respectively. The North East

region recorded the lowest average price of £124,000 (Kuttner 2014). The local authority of

UK has shown largest annual growth.

Factors affecting housing price

Different factors influencing housing price are economic state, interest rate, size of

population and real income. Besides these demand side factors, the available supply of

housing affect housing prices.

Demand side factors of UK housing market

Economic growth: Income is an important determinant of housing demand. In the phase of

economic growth, people experiences an increase in their income. The increased income

raises ability of people to afford higher mortgage encouraging housing demand (Wilcox and

Perry 2014). In times of economic boom, housing demand grows at a fast pace.

Affordability: Housing affordability depends on the income of people. Increasing income

implies people can afford more houses. Demand of houses tend be highly income elastic.

The average housing price in UK has constituted a steady upward trend from 2006 to

2016. England is the main contributor of growing housing price trend in UK. Housing price

in England grew by 9.3% in the year 2016. The average house price in England now is

£229,000. In Wales, housing price grew by 4.9% for the past few years. The housing price is

recorded as £145,000 (ons.gov.uk 2018). The average house price in Scotland is £143,000

recording a growth rate of 4.6%. In Northern Ireland, housing price stands at £123,000.

The regional housing price trend shows London continues to be region having highest

average house price of £472,000. The region was followed by South East and East England

region where housing price stands at £309,000 and £270,000 respectively. The North East

region recorded the lowest average price of £124,000 (Kuttner 2014). The local authority of

UK has shown largest annual growth.

Factors affecting housing price

Different factors influencing housing price are economic state, interest rate, size of

population and real income. Besides these demand side factors, the available supply of

housing affect housing prices.

Demand side factors of UK housing market

Economic growth: Income is an important determinant of housing demand. In the phase of

economic growth, people experiences an increase in their income. The increased income

raises ability of people to afford higher mortgage encouraging housing demand (Wilcox and

Perry 2014). In times of economic boom, housing demand grows at a fast pace.

Affordability: Housing affordability depends on the income of people. Increasing income

implies people can afford more houses. Demand of houses tend be highly income elastic.

5ECONOMICS FOR BUSINESS

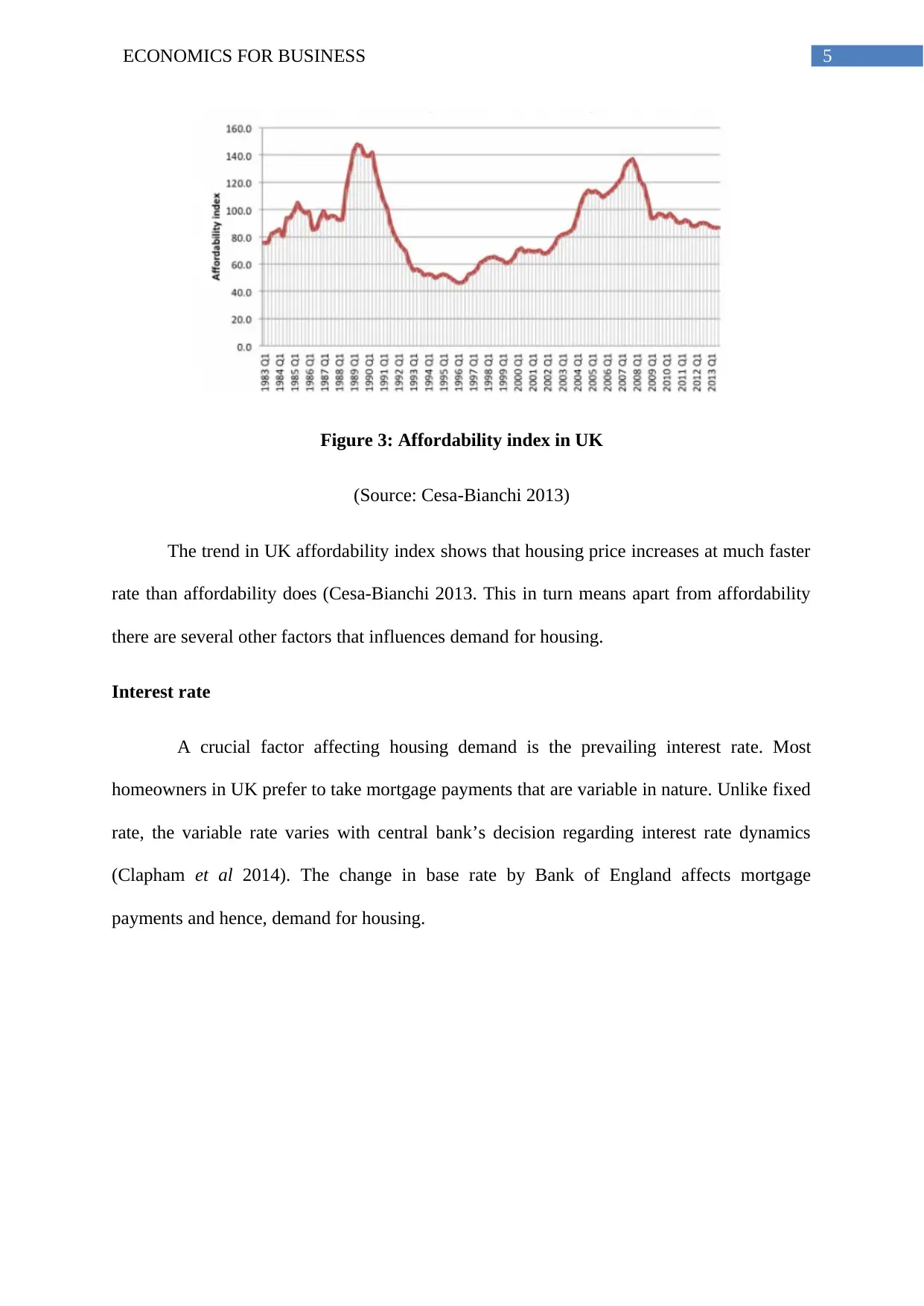

Figure 3: Affordability index in UK

(Source: Cesa-Bianchi 2013)

The trend in UK affordability index shows that housing price increases at much faster

rate than affordability does (Cesa-Bianchi 2013. This in turn means apart from affordability

there are several other factors that influences demand for housing.

Interest rate

A crucial factor affecting housing demand is the prevailing interest rate. Most

homeowners in UK prefer to take mortgage payments that are variable in nature. Unlike fixed

rate, the variable rate varies with central bank’s decision regarding interest rate dynamics

(Clapham et al 2014). The change in base rate by Bank of England affects mortgage

payments and hence, demand for housing.

Figure 3: Affordability index in UK

(Source: Cesa-Bianchi 2013)

The trend in UK affordability index shows that housing price increases at much faster

rate than affordability does (Cesa-Bianchi 2013. This in turn means apart from affordability

there are several other factors that influences demand for housing.

Interest rate

A crucial factor affecting housing demand is the prevailing interest rate. Most

homeowners in UK prefer to take mortgage payments that are variable in nature. Unlike fixed

rate, the variable rate varies with central bank’s decision regarding interest rate dynamics

(Clapham et al 2014). The change in base rate by Bank of England affects mortgage

payments and hence, demand for housing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS FOR BUSINESS

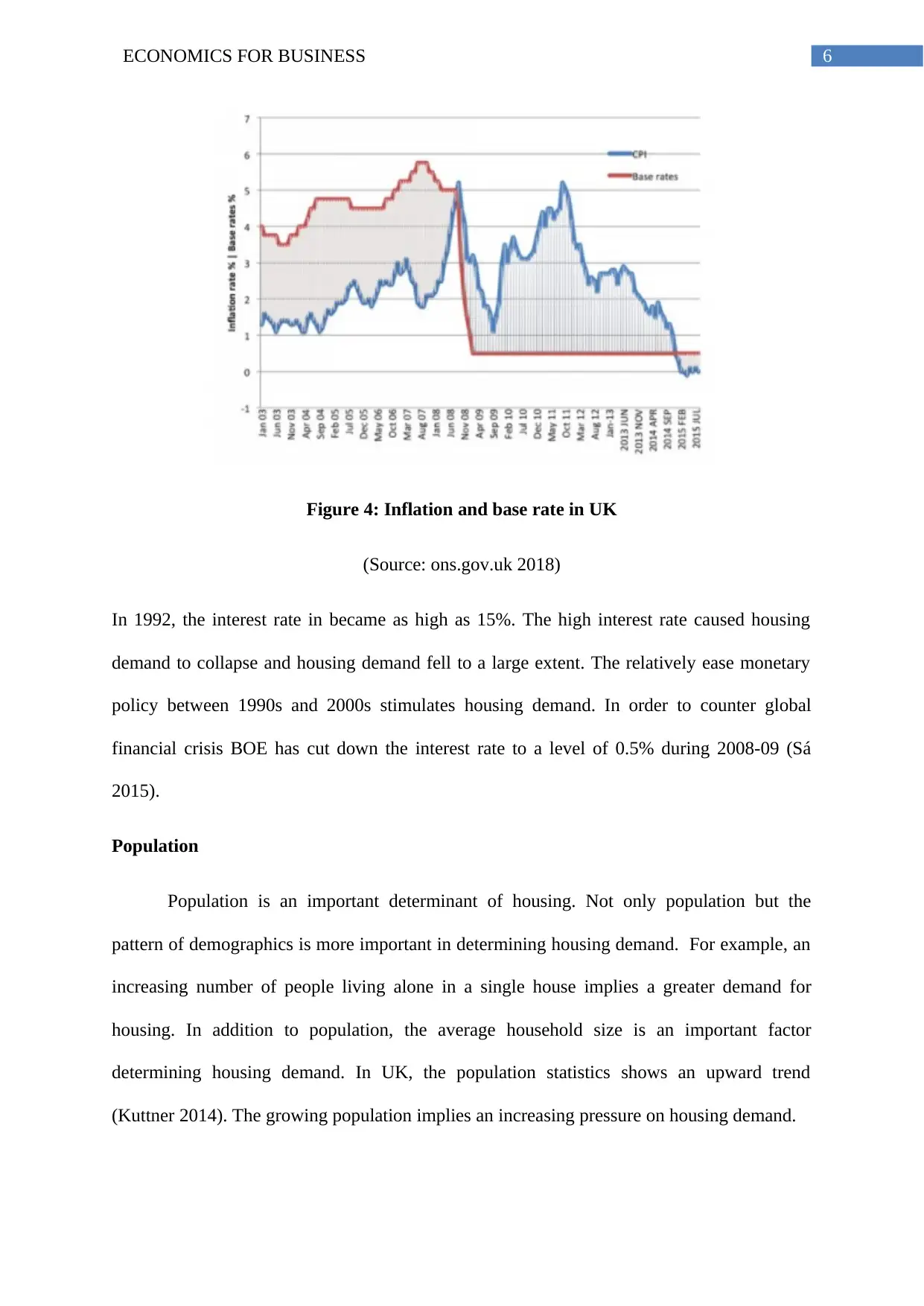

Figure 4: Inflation and base rate in UK

(Source: ons.gov.uk 2018)

In 1992, the interest rate in became as high as 15%. The high interest rate caused housing

demand to collapse and housing demand fell to a large extent. The relatively ease monetary

policy between 1990s and 2000s stimulates housing demand. In order to counter global

financial crisis BOE has cut down the interest rate to a level of 0.5% during 2008-09 (Sá

2015).

Population

Population is an important determinant of housing. Not only population but the

pattern of demographics is more important in determining housing demand. For example, an

increasing number of people living alone in a single house implies a greater demand for

housing. In addition to population, the average household size is an important factor

determining housing demand. In UK, the population statistics shows an upward trend

(Kuttner 2014). The growing population implies an increasing pressure on housing demand.

Figure 4: Inflation and base rate in UK

(Source: ons.gov.uk 2018)

In 1992, the interest rate in became as high as 15%. The high interest rate caused housing

demand to collapse and housing demand fell to a large extent. The relatively ease monetary

policy between 1990s and 2000s stimulates housing demand. In order to counter global

financial crisis BOE has cut down the interest rate to a level of 0.5% during 2008-09 (Sá

2015).

Population

Population is an important determinant of housing. Not only population but the

pattern of demographics is more important in determining housing demand. For example, an

increasing number of people living alone in a single house implies a greater demand for

housing. In addition to population, the average household size is an important factor

determining housing demand. In UK, the population statistics shows an upward trend

(Kuttner 2014). The growing population implies an increasing pressure on housing demand.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS FOR BUSINESS

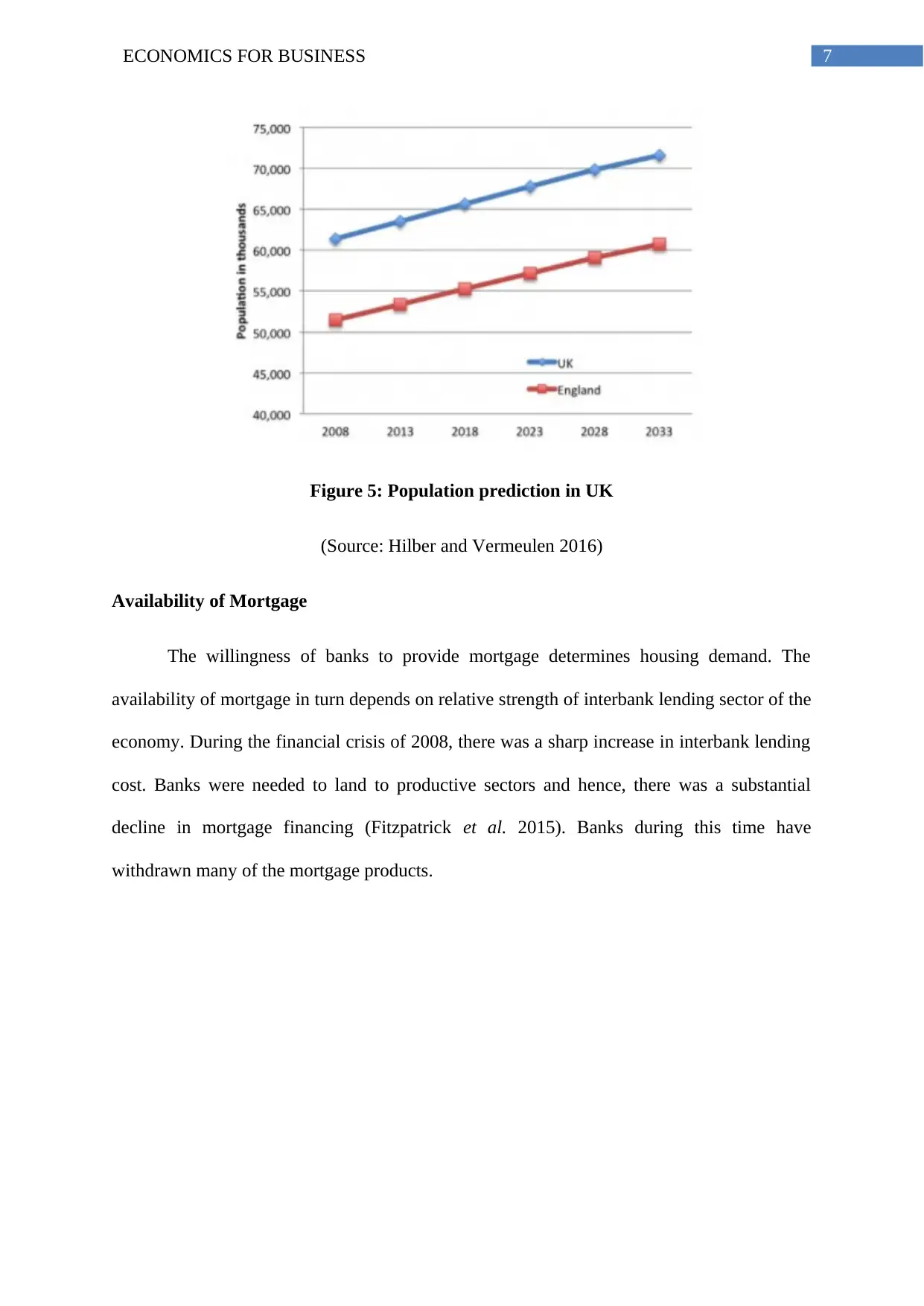

Figure 5: Population prediction in UK

(Source: Hilber and Vermeulen 2016)

Availability of Mortgage

The willingness of banks to provide mortgage determines housing demand. The

availability of mortgage in turn depends on relative strength of interbank lending sector of the

economy. During the financial crisis of 2008, there was a sharp increase in interbank lending

cost. Banks were needed to land to productive sectors and hence, there was a substantial

decline in mortgage financing (Fitzpatrick et al. 2015). Banks during this time have

withdrawn many of the mortgage products.

Figure 5: Population prediction in UK

(Source: Hilber and Vermeulen 2016)

Availability of Mortgage

The willingness of banks to provide mortgage determines housing demand. The

availability of mortgage in turn depends on relative strength of interbank lending sector of the

economy. During the financial crisis of 2008, there was a sharp increase in interbank lending

cost. Banks were needed to land to productive sectors and hence, there was a substantial

decline in mortgage financing (Fitzpatrick et al. 2015). Banks during this time have

withdrawn many of the mortgage products.

8ECONOMICS FOR BUSINESS

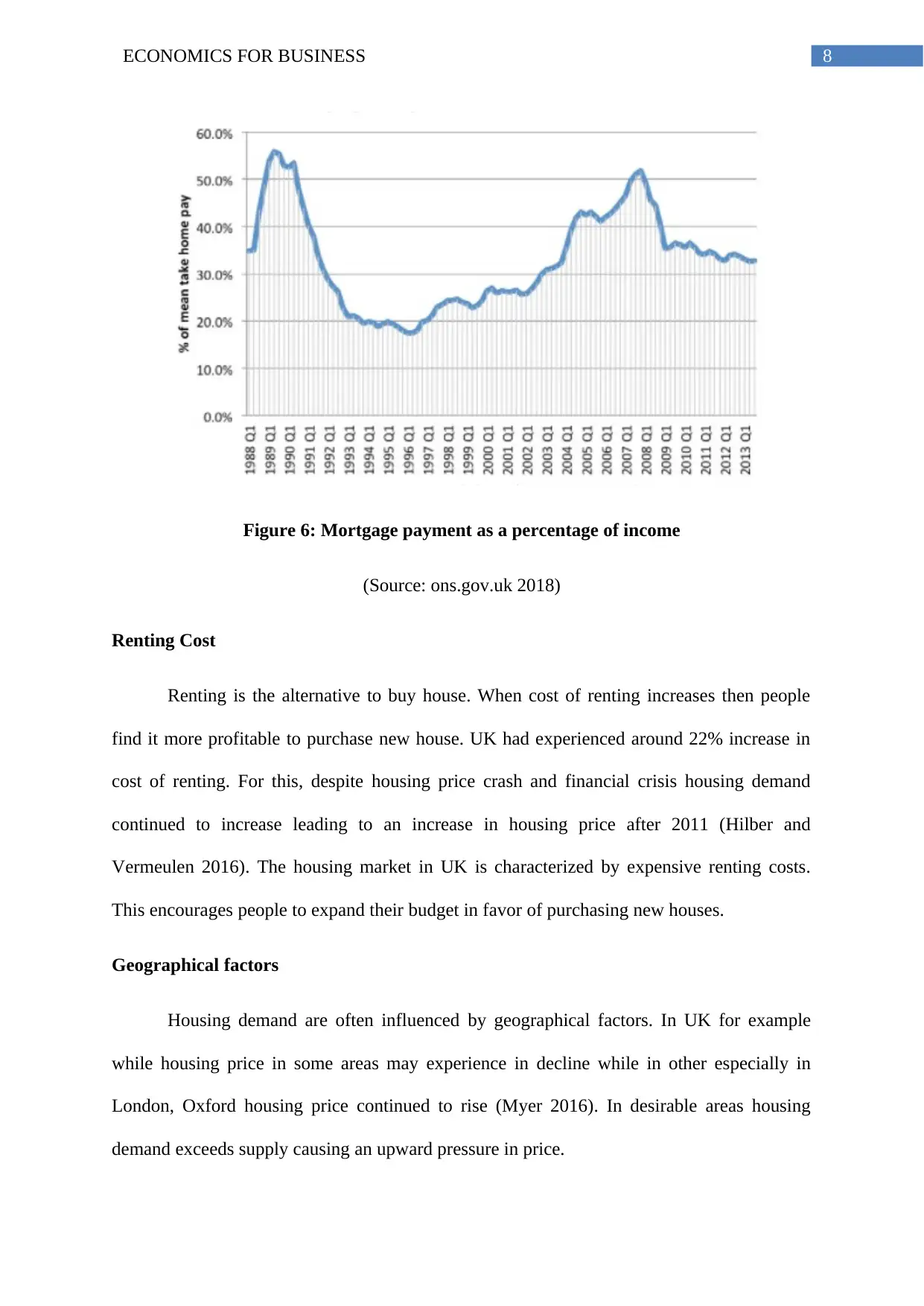

Figure 6: Mortgage payment as a percentage of income

(Source: ons.gov.uk 2018)

Renting Cost

Renting is the alternative to buy house. When cost of renting increases then people

find it more profitable to purchase new house. UK had experienced around 22% increase in

cost of renting. For this, despite housing price crash and financial crisis housing demand

continued to increase leading to an increase in housing price after 2011 (Hilber and

Vermeulen 2016). The housing market in UK is characterized by expensive renting costs.

This encourages people to expand their budget in favor of purchasing new houses.

Geographical factors

Housing demand are often influenced by geographical factors. In UK for example

while housing price in some areas may experience in decline while in other especially in

London, Oxford housing price continued to rise (Myer 2016). In desirable areas housing

demand exceeds supply causing an upward pressure in price.

Figure 6: Mortgage payment as a percentage of income

(Source: ons.gov.uk 2018)

Renting Cost

Renting is the alternative to buy house. When cost of renting increases then people

find it more profitable to purchase new house. UK had experienced around 22% increase in

cost of renting. For this, despite housing price crash and financial crisis housing demand

continued to increase leading to an increase in housing price after 2011 (Hilber and

Vermeulen 2016). The housing market in UK is characterized by expensive renting costs.

This encourages people to expand their budget in favor of purchasing new houses.

Geographical factors

Housing demand are often influenced by geographical factors. In UK for example

while housing price in some areas may experience in decline while in other especially in

London, Oxford housing price continued to rise (Myer 2016). In desirable areas housing

demand exceeds supply causing an upward pressure in price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS FOR BUSINESS

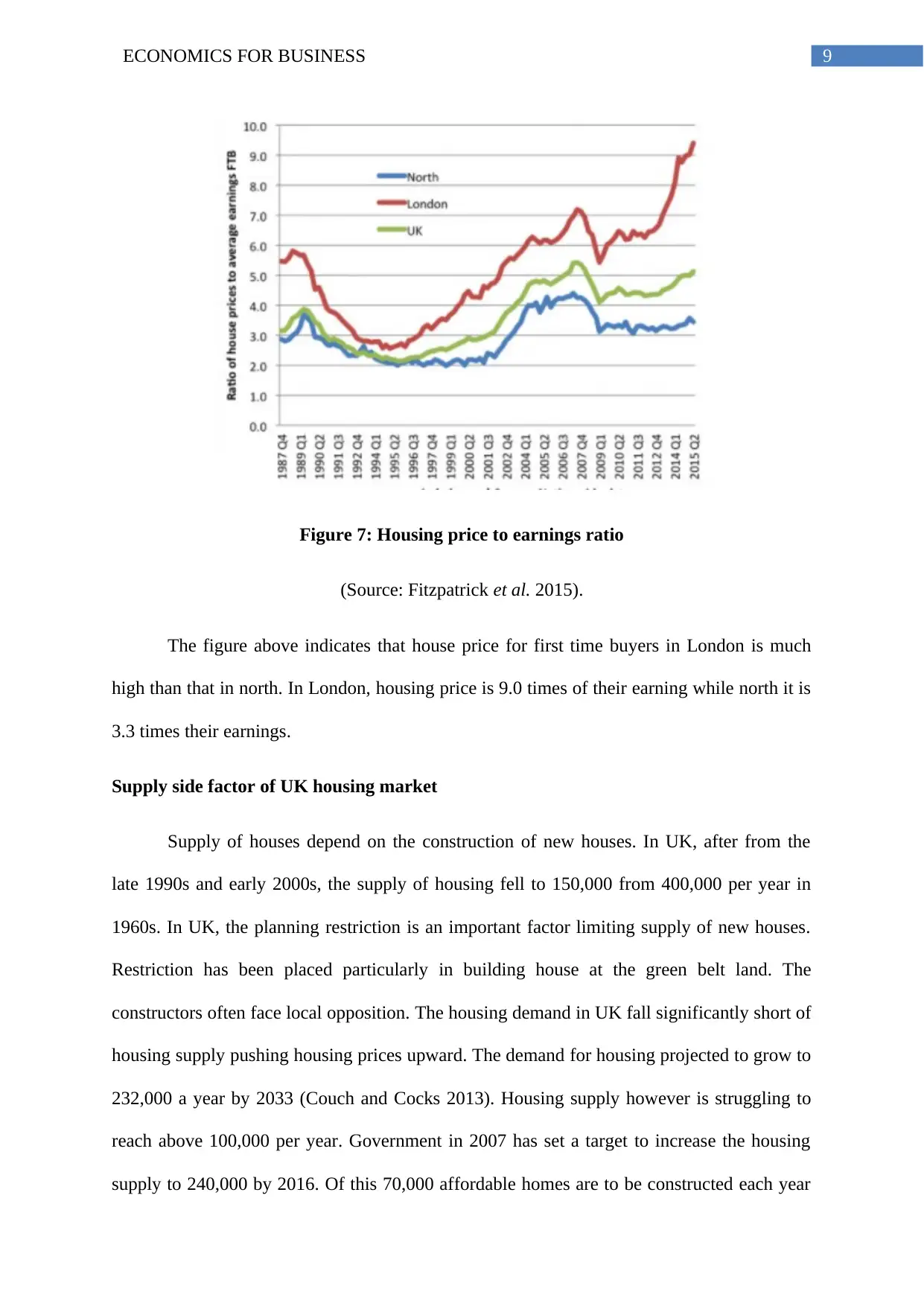

Figure 7: Housing price to earnings ratio

(Source: Fitzpatrick et al. 2015).

The figure above indicates that house price for first time buyers in London is much

high than that in north. In London, housing price is 9.0 times of their earning while north it is

3.3 times their earnings.

Supply side factor of UK housing market

Supply of houses depend on the construction of new houses. In UK, after from the

late 1990s and early 2000s, the supply of housing fell to 150,000 from 400,000 per year in

1960s. In UK, the planning restriction is an important factor limiting supply of new houses.

Restriction has been placed particularly in building house at the green belt land. The

constructors often face local opposition. The housing demand in UK fall significantly short of

housing supply pushing housing prices upward. The demand for housing projected to grow to

232,000 a year by 2033 (Couch and Cocks 2013). Housing supply however is struggling to

reach above 100,000 per year. Government in 2007 has set a target to increase the housing

supply to 240,000 by 2016. Of this 70,000 affordable homes are to be constructed each year

Figure 7: Housing price to earnings ratio

(Source: Fitzpatrick et al. 2015).

The figure above indicates that house price for first time buyers in London is much

high than that in north. In London, housing price is 9.0 times of their earning while north it is

3.3 times their earnings.

Supply side factor of UK housing market

Supply of houses depend on the construction of new houses. In UK, after from the

late 1990s and early 2000s, the supply of housing fell to 150,000 from 400,000 per year in

1960s. In UK, the planning restriction is an important factor limiting supply of new houses.

Restriction has been placed particularly in building house at the green belt land. The

constructors often face local opposition. The housing demand in UK fall significantly short of

housing supply pushing housing prices upward. The demand for housing projected to grow to

232,000 a year by 2033 (Couch and Cocks 2013). Housing supply however is struggling to

reach above 100,000 per year. Government in 2007 has set a target to increase the housing

supply to 240,000 by 2016. Of this 70,000 affordable homes are to be constructed each year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS FOR BUSINESS

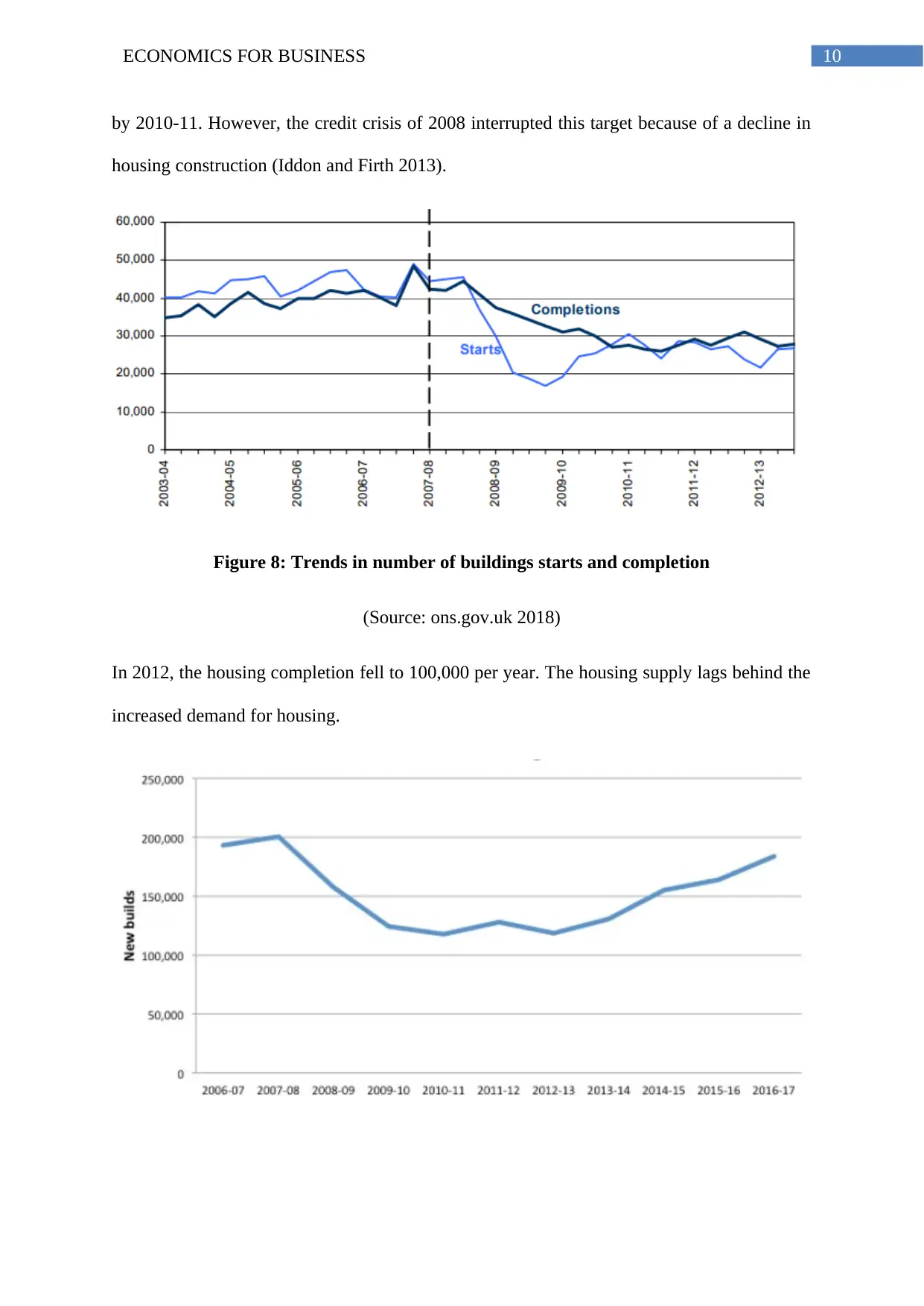

by 2010-11. However, the credit crisis of 2008 interrupted this target because of a decline in

housing construction (Iddon and Firth 2013).

Figure 8: Trends in number of buildings starts and completion

(Source: ons.gov.uk 2018)

In 2012, the housing completion fell to 100,000 per year. The housing supply lags behind the

increased demand for housing.

by 2010-11. However, the credit crisis of 2008 interrupted this target because of a decline in

housing construction (Iddon and Firth 2013).

Figure 8: Trends in number of buildings starts and completion

(Source: ons.gov.uk 2018)

In 2012, the housing completion fell to 100,000 per year. The housing supply lags behind the

increased demand for housing.

11ECONOMICS FOR BUSINESS

Figure 9: New house building in UK

(Source: Myers 2016)

With different schemes of the government there is hope that the mortgage availability will

increases construction of private dwellings. However, increasing mortgage availability will

not solve other supply side constraint like regulation in planning and local opposition on large

scale house building (Jones and Richardson 2014). The housing demand is growing at a must

faster rate than addition to the stock of new houses, thriving pressure on prices.

Implication of Housing shortage

House price continues to increase

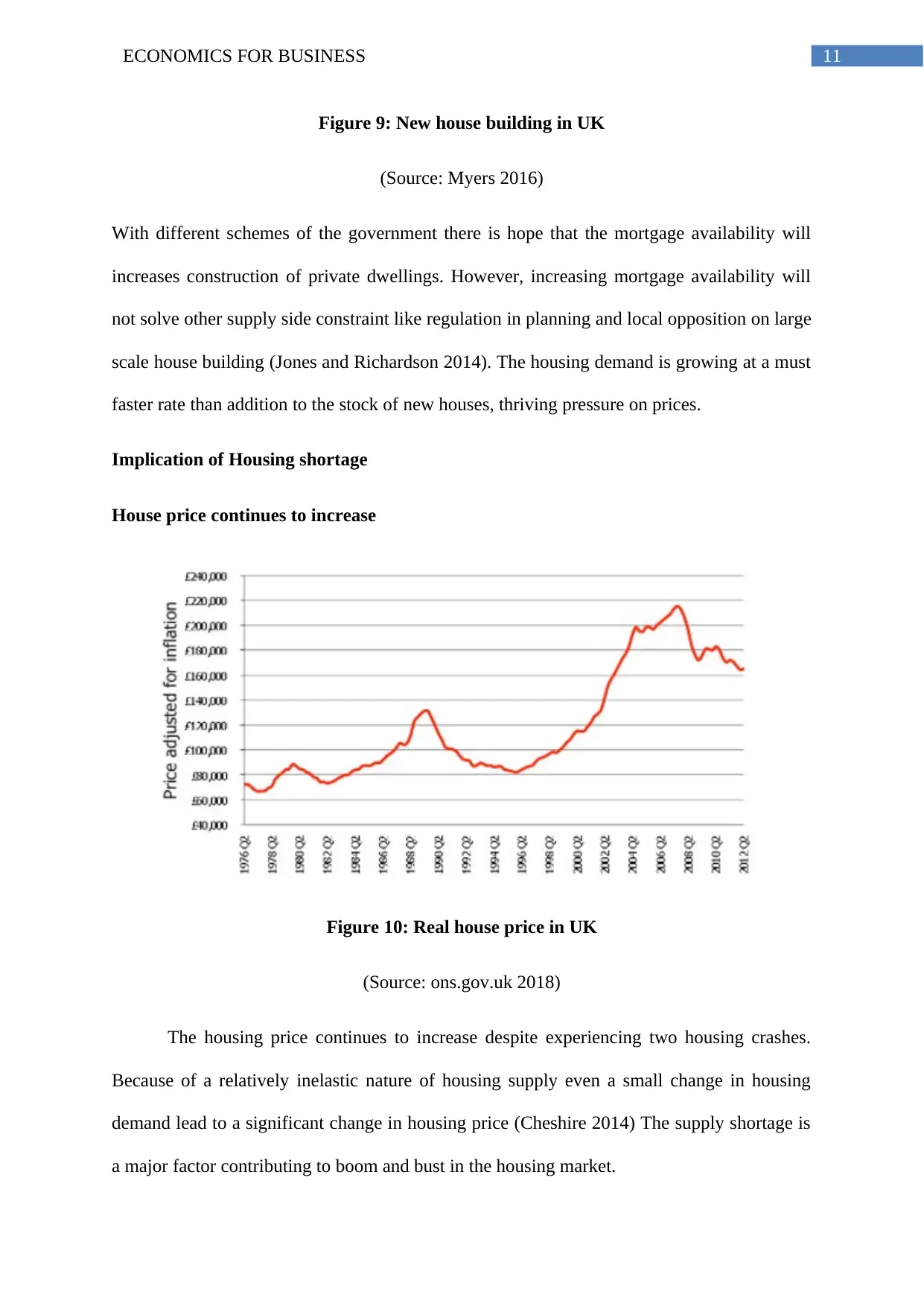

Figure 10: Real house price in UK

(Source: ons.gov.uk 2018)

The housing price continues to increase despite experiencing two housing crashes.

Because of a relatively inelastic nature of housing supply even a small change in housing

demand lead to a significant change in housing price (Cheshire 2014) The supply shortage is

a major factor contributing to boom and bust in the housing market.

Figure 9: New house building in UK

(Source: Myers 2016)

With different schemes of the government there is hope that the mortgage availability will

increases construction of private dwellings. However, increasing mortgage availability will

not solve other supply side constraint like regulation in planning and local opposition on large

scale house building (Jones and Richardson 2014). The housing demand is growing at a must

faster rate than addition to the stock of new houses, thriving pressure on prices.

Implication of Housing shortage

House price continues to increase

Figure 10: Real house price in UK

(Source: ons.gov.uk 2018)

The housing price continues to increase despite experiencing two housing crashes.

Because of a relatively inelastic nature of housing supply even a small change in housing

demand lead to a significant change in housing price (Cheshire 2014) The supply shortage is

a major factor contributing to boom and bust in the housing market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.