MN5904 - Ecovista PLC Chairman's Statement Analysis and Findings

VerifiedAdded on 2023/04/23

|17

|3404

|397

Report

AI Summary

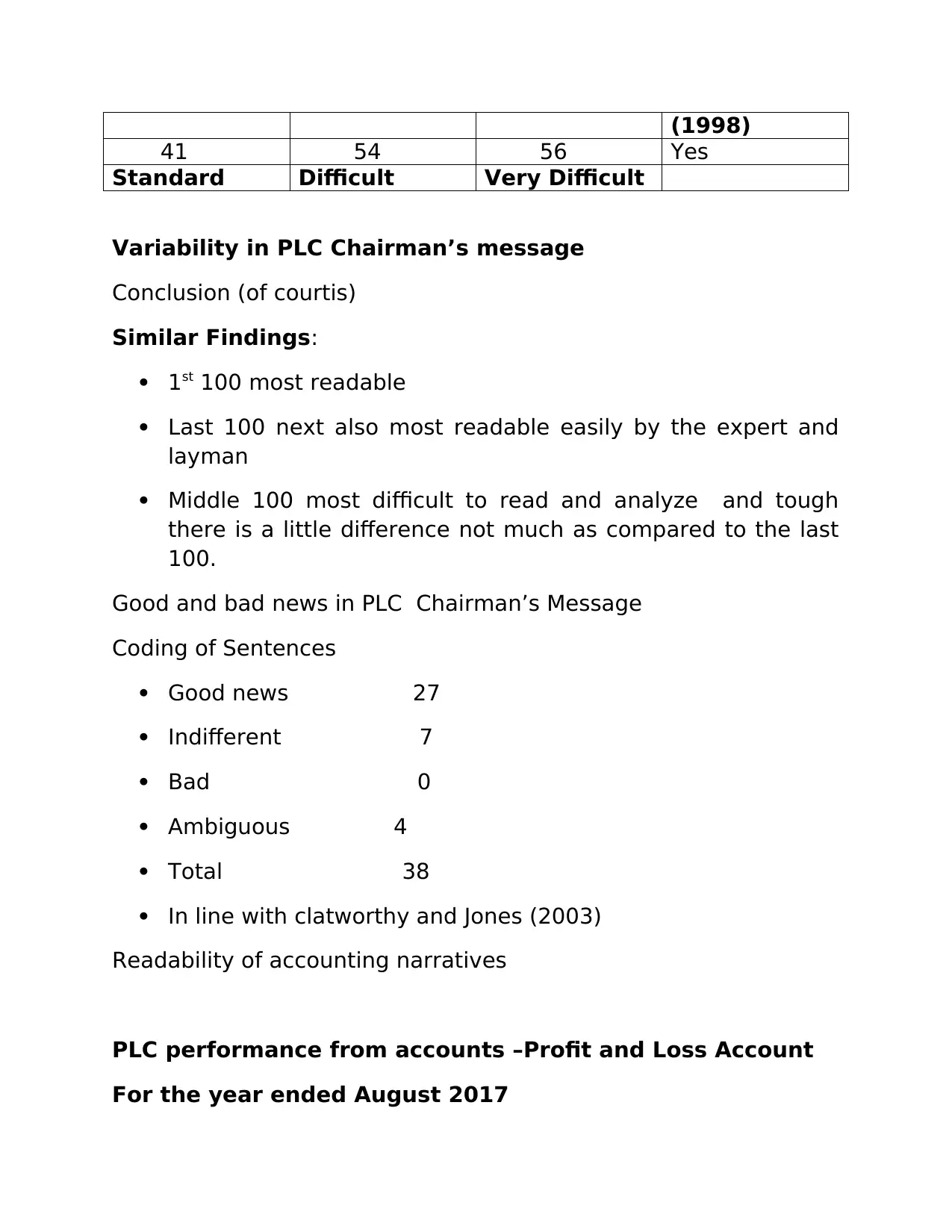

This report provides an in-depth analysis of Ecovista PLC's Chairman's Statement, focusing on financial reporting and potential impression management techniques. The analysis begins with an introduction to Ecovista PLC, followed by an overview of the relevant regulations and background information. The core of the report examines the narratives within the Chairman's Statement, including readability assessments using the Flesch and LIX indices. The findings are then compared with the company's financial statements, specifically the Profit and Loss Account and Balance Sheet, to assess the presence of impression management. The report also compares the findings with previous research on the topic. Furthermore, the report investigates the tone of the Chairman's message, identifying the use of active and passive voice, personal references, and the portrayal of good and bad news. The analysis reveals the variability in readability across different sections of the statement, aligning with prior research. The report concludes with a summary of the findings and their implications for understanding Ecovista PLC's financial communications.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.