Ecratic Company: Improving Cost Management with Activity Based Costing

VerifiedAdded on 2023/03/23

|9

|2593

|88

Case Study

AI Summary

This case study examines Ecratic Company's costing system, highlighting the deficiencies in its conventional costing method and advocating for the implementation of Activity Based Costing (ABC). The analysis reveals that the company's traditional job costing system, which allocates overheads based on a single plant-wide rate, leads to inaccurate product costs and misinformed pricing decisions, particularly for its diverse ice cream product lines. By transitioning to ABC, the company can identify and allocate costs more accurately based on the actual consumption of resources by each product. The study demonstrates how ABC provides a more reliable measurement of product costs, improves pricing strategies, and ultimately enhances profitability, as evidenced by the significant changes in per-unit costs for Classic Vanilla and Butter Pecan under both costing systems. Desklib provides students access to this document and many more solved assignments and past papers.

Student No. 297012, Name: Mr. Hussein Rkein 2019

Introduction:

Ecratic Company is a manufacturer of wide range of Ice-creams in the country. The company

is in the business for last 20 years producing ice creams ranging from traditional Classic

Vanilla, Classic Chocolate, and Classic Rainbow to new flavours like Gourmet Vanilla Bean,

Butter Pecan and Coconut Vanilla Gelato.

The company was using conventional costing system wherein all the overheads of the

company was distributed to the product lines based on the total number of units

manufactured. Off late the company is struggling with keeping the same level of profits and

thus the senior management is concerned about the productivity of the employees.

We have critically analysed the company’s costs and there are deficiencies in the company’s

conventional costing system that the company currently adheres to.

Assignment of costs to activity centres:

Resource Driver Cost allocation

Cost

Category Wages

Building

Cost

Depreciat

ion

Consu

mables Energy Others

Total Cost

Activity

Centres (employees) (m2)

(Machine

Hours)

(Order

s)

(Kilow

att

Hours)

(employ

ees)

Product

Development

$1,71,586.1

345

$81,268.6

567 $0.0000

$1,120.

3704

$2,842.

2819

$1,525.2

101

$2,58,342.6

535

Sales and

Distribution

$6,86,344.5

378

$1,89,626

.8657 $0.0000

$1,120.

3704

$3,410.

7383

$6,100.8

403

$8,86,603.3

524

Inspecting

$1,14,390.7

563

$1,89,626

.8657 $0.0000

$1,120.

3704

$3,410.

7383

$1,016.8

067

$3,09,565.5

373

Pasteurizing

$17,15,861.

3445

$3,52,164

.1791

$4,84,000.

0000

$20,16

6.6667

$68,21

4.7651

$15,252.

1008

$26,55,659.

0562

Mixing

$17,15,861.

3445

$3,52,164

.1791

$6,05,000.

0000

$13,44

4.4444

$1,02,3

22.147

7

$15,252.

1008

$28,04,044.

2166

Freezing

$13,72,689.

0756

$3,52,164

.1791

$1,21,000.

0000

$20,16

6.6667

$68,21

4.7651

$12,201.

6807

$19,46,436.

3672

Administrati

on

$6,86,344.5

378

$1,89,626

.8657 $0.0000

$2,240.

7407

$2,842.

2819

$6,100.8

403

$8,87,155.2

664

Corporate

Management

$3,43,172.2

689

$1,08,358

.2090 $0.0000

$1,120.

3704

$2,842.

2819

$3,050.4

202

$4,58,543.5

503

1 | P a g e

Introduction:

Ecratic Company is a manufacturer of wide range of Ice-creams in the country. The company

is in the business for last 20 years producing ice creams ranging from traditional Classic

Vanilla, Classic Chocolate, and Classic Rainbow to new flavours like Gourmet Vanilla Bean,

Butter Pecan and Coconut Vanilla Gelato.

The company was using conventional costing system wherein all the overheads of the

company was distributed to the product lines based on the total number of units

manufactured. Off late the company is struggling with keeping the same level of profits and

thus the senior management is concerned about the productivity of the employees.

We have critically analysed the company’s costs and there are deficiencies in the company’s

conventional costing system that the company currently adheres to.

Assignment of costs to activity centres:

Resource Driver Cost allocation

Cost

Category Wages

Building

Cost

Depreciat

ion

Consu

mables Energy Others

Total Cost

Activity

Centres (employees) (m2)

(Machine

Hours)

(Order

s)

(Kilow

att

Hours)

(employ

ees)

Product

Development

$1,71,586.1

345

$81,268.6

567 $0.0000

$1,120.

3704

$2,842.

2819

$1,525.2

101

$2,58,342.6

535

Sales and

Distribution

$6,86,344.5

378

$1,89,626

.8657 $0.0000

$1,120.

3704

$3,410.

7383

$6,100.8

403

$8,86,603.3

524

Inspecting

$1,14,390.7

563

$1,89,626

.8657 $0.0000

$1,120.

3704

$3,410.

7383

$1,016.8

067

$3,09,565.5

373

Pasteurizing

$17,15,861.

3445

$3,52,164

.1791

$4,84,000.

0000

$20,16

6.6667

$68,21

4.7651

$15,252.

1008

$26,55,659.

0562

Mixing

$17,15,861.

3445

$3,52,164

.1791

$6,05,000.

0000

$13,44

4.4444

$1,02,3

22.147

7

$15,252.

1008

$28,04,044.

2166

Freezing

$13,72,689.

0756

$3,52,164

.1791

$1,21,000.

0000

$20,16

6.6667

$68,21

4.7651

$12,201.

6807

$19,46,436.

3672

Administrati

on

$6,86,344.5

378

$1,89,626

.8657 $0.0000

$2,240.

7407

$2,842.

2819

$6,100.8

403

$8,87,155.2

664

Corporate

Management

$3,43,172.2

689

$1,08,358

.2090 $0.0000

$1,120.

3704

$2,842.

2819

$3,050.4

202

$4,58,543.5

503

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Student No. 297012, Name: Mr. Hussein Rkein 2019

Assignment of costs to each activity under Pasteurizing Activity Centre:

Cost of Each Activity within the Activity Centre - Pasteurizing

Activity Wages

Buildin

g Cost

Depreci

ation

Consum

ables Energy Others

Total

Cost

Set up

Pasteurizer

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Weigh and

Sort

Ingredients

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Load

pasteurizer

$6,86,34

4.5378

$2,46,5

14.925

4

$20,166.

6667

$6,100.8

403

$9,59,12

6.9702

Operate

pasteurizer

$3,43,17

2.2689

$17,60

8.2090

$4,84,00

0.0000

$68,214.7

651

$3,050.4

202

$9,16,04

5.6631

Unload and

Clean

pasteurizer

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Move to

mixing room

$1,71,58

6.1345

$35,21

6.4179

$1,525.2

101

$2,08,32

7.7624

2 | P a g e

Assignment of costs to each activity under Pasteurizing Activity Centre:

Cost of Each Activity within the Activity Centre - Pasteurizing

Activity Wages

Buildin

g Cost

Depreci

ation

Consum

ables Energy Others

Total

Cost

Set up

Pasteurizer

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Weigh and

Sort

Ingredients

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Load

pasteurizer

$6,86,34

4.5378

$2,46,5

14.925

4

$20,166.

6667

$6,100.8

403

$9,59,12

6.9702

Operate

pasteurizer

$3,43,17

2.2689

$17,60

8.2090

$4,84,00

0.0000

$68,214.7

651

$3,050.4

202

$9,16,04

5.6631

Unload and

Clean

pasteurizer

$1,71,58

6.1345

$17,60

8.2090

$1,525.2

101

$1,90,71

9.5535

Move to

mixing room

$1,71,58

6.1345

$35,21

6.4179

$1,525.2

101

$2,08,32

7.7624

2 | P a g e

Student No. 297012, Name: Mr. Hussein Rkein 2019

Computation of per unit Cost using Bill of Activities: Classic Vanilla

Bill of activities - Cost for Classic Vanilla

Activities Consumed Annual Qty of

activity driver Activity driver Activity

Driver Rate Cost allocated

Corporate management NA NA NA $91,898.0000

Process receivables 600 invoices $58.1741 $34,904.4590

Process payables 200 purchase orders $111.8717 $22,374.3333

Production planning 170

production

schedules $162.5438 $27,632.4463

Reports to Health Dept 170 reports $25.2091 $4,285.5455

Process sales order 610 sales orders $117.3225 $71,566.7376

Dispatch sales order 500 dispatches $105.1173 $52,558.6667

Product Development NA NA NA $0.0000

Inspect cream 170 Batches $106.9719 $18,185.2231

Disposal of substandard

cream 170 Batches $25.2091 $4,285.5455

Move to pasteurizing room 170 Batches $25.2091 $4,285.5455

Set up pasteurizer 170 Batches $157.6195 $26,795.3092

Weigh and sort ingredients 170 Batches $157.6195 $26,795.3092

Load pasteurizer 48,500 litres $3.9633 $1,92,221.7275

Operate pasteurizer 170 Batches $757.0625 $1,28,700.6304

Unload and Clean pasteurizer 170 Batches $157.6195 $26,795.3092

Move to mixing room 170 Batches $172.1717 $29,269.1898

Set up scales 170 Batches $86.0860 $14,634.6116

Weigh ingredients 170 Batches $157.6198 $26,795.3719

Load mixers 170 Batches $315.2388 $53,590.6033

Operate mixers 48,500 litres $7.4282 $3,60,267.2190

Clean mixers 170 Batches $172.1719 $29,269.2231

Move mixture to freezer 48,500 litres $0.5032 $24,404.7190

Load hopper 1,93,600 Products $0.4486 $86,852.8000

Set up packaging and fill 1,940 trays $8.0629 $15,641.9514

Move to freezer 1,940 trays $4.4862 $8,703.2448

Freeze products 1,940 trays $55.6771 $1,08,013.6085

Unload freezer 1,940 trays $4.4862 $8,703.2448

Inspect finished products 0 trays $2.7678 $0.0000

Disposal of substandard

product 0 trays $1.5756 $0.0000

Move to truck 1,940 trays $5.3957 $10,467.6829

Total Allocated Cost $15,09,898.2579

Add: Direct Materials 48,500 litres $2.0000 $97,000.0000

Total Cost $16,06,898.2579

Annual Volume 1,94,000

Per Unit Cost of Classic Vanilla (Total Cost/Annual Volume) $8.2830

3 | P a g e

Computation of per unit Cost using Bill of Activities: Classic Vanilla

Bill of activities - Cost for Classic Vanilla

Activities Consumed Annual Qty of

activity driver Activity driver Activity

Driver Rate Cost allocated

Corporate management NA NA NA $91,898.0000

Process receivables 600 invoices $58.1741 $34,904.4590

Process payables 200 purchase orders $111.8717 $22,374.3333

Production planning 170

production

schedules $162.5438 $27,632.4463

Reports to Health Dept 170 reports $25.2091 $4,285.5455

Process sales order 610 sales orders $117.3225 $71,566.7376

Dispatch sales order 500 dispatches $105.1173 $52,558.6667

Product Development NA NA NA $0.0000

Inspect cream 170 Batches $106.9719 $18,185.2231

Disposal of substandard

cream 170 Batches $25.2091 $4,285.5455

Move to pasteurizing room 170 Batches $25.2091 $4,285.5455

Set up pasteurizer 170 Batches $157.6195 $26,795.3092

Weigh and sort ingredients 170 Batches $157.6195 $26,795.3092

Load pasteurizer 48,500 litres $3.9633 $1,92,221.7275

Operate pasteurizer 170 Batches $757.0625 $1,28,700.6304

Unload and Clean pasteurizer 170 Batches $157.6195 $26,795.3092

Move to mixing room 170 Batches $172.1717 $29,269.1898

Set up scales 170 Batches $86.0860 $14,634.6116

Weigh ingredients 170 Batches $157.6198 $26,795.3719

Load mixers 170 Batches $315.2388 $53,590.6033

Operate mixers 48,500 litres $7.4282 $3,60,267.2190

Clean mixers 170 Batches $172.1719 $29,269.2231

Move mixture to freezer 48,500 litres $0.5032 $24,404.7190

Load hopper 1,93,600 Products $0.4486 $86,852.8000

Set up packaging and fill 1,940 trays $8.0629 $15,641.9514

Move to freezer 1,940 trays $4.4862 $8,703.2448

Freeze products 1,940 trays $55.6771 $1,08,013.6085

Unload freezer 1,940 trays $4.4862 $8,703.2448

Inspect finished products 0 trays $2.7678 $0.0000

Disposal of substandard

product 0 trays $1.5756 $0.0000

Move to truck 1,940 trays $5.3957 $10,467.6829

Total Allocated Cost $15,09,898.2579

Add: Direct Materials 48,500 litres $2.0000 $97,000.0000

Total Cost $16,06,898.2579

Annual Volume 1,94,000

Per Unit Cost of Classic Vanilla (Total Cost/Annual Volume) $8.2830

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Student No. 297012, Name: Mr. Hussein Rkein 2019

Computation of per unit Cost using Bill of Activities: Butter Peccan

Bill of activities - Cost for Butter Peccan

Activities Consumed Annual Qty of

activity driver Activity driver Activity

Driver Rate Cost allocated

Corporate management NA NA NA $11,132.0000

Process receivables 200 invoices $58.1741 $11,634.8197

Process payables 100 purchase orders $111.8717 $11,187.1667

Production planning 60

production

schedules $162.5438 $9,752.6281

Reports to Health Dept 60 reports $25.2091 $1,512.5455

Process sales order 180 sales orders $117.3225 $21,118.0537

Dispatch sales order 100 dispatches $105.1173 $10,511.7333

Product Development NA NA NA $85,253.0000

Inspect cream 50 Batches $106.9719 $5,348.5950

Disposal of substandard cream 50 Batches $25.2091 $1,260.4545

Move to pasteurizing room 50 Batches $25.2091 $1,260.4545

Set up pasteurizer 50 Batches $157.6195 $7,880.9733

Weigh and sort ingredients 50 Batches $157.6195 $7,880.9733

Load pasteurizer 11,750 litres $3.9633 $46,569.1814

Operate pasteurizer 50 Batches $757.0625 $37,853.1266

Unload and Clean pasteurizer 50 Batches $157.6195 $7,880.9733

Move to mixing room 50 Batches $172.1717 $8,608.5852

Set up scales 50 Batches $86.0860 $4,304.2975

Weigh ingredients 50 Batches $157.6198 $7,880.9917

Load mixers 50 Batches $315.2388 $15,761.9421

Operate mixers 11,750 litres $7.4282 $87,281.2335

Clean mixers 50 Batches $172.1719 $8,608.5950

Move mixture to freezer 11,750 litres $0.5032 $5,912.4835

Load hopper 24,200 Products $0.4486 $10,856.6000

Set up packaging and fill 490 trays $8.0629 $3,950.8022

Move to freezer 490 trays $4.4862 $2,198.2423

Freeze products 490 trays $55.6771 $27,281.7877

Unload freezer 490 trays $4.4862 $2,198.2423

Inspect finished products 490 trays $2.7678 $1,356.2319

Disposal of substandard

product 490 trays $1.5756 $772.0284

Move to truck 470 trays $5.3957 $2,535.9850

Total Allocated Cost $4,67,544.7273

Add: Direct Materials 11,750 litres $4.0000 $47,000.0000

Total Cost $5,14,544.7273

Annual Volume 23,500

Per Unit Cost of Butter Peccan (Total Cost/Annual Volume) $21.8955

Use of Conventional Costing System:

4 | P a g e

Computation of per unit Cost using Bill of Activities: Butter Peccan

Bill of activities - Cost for Butter Peccan

Activities Consumed Annual Qty of

activity driver Activity driver Activity

Driver Rate Cost allocated

Corporate management NA NA NA $11,132.0000

Process receivables 200 invoices $58.1741 $11,634.8197

Process payables 100 purchase orders $111.8717 $11,187.1667

Production planning 60

production

schedules $162.5438 $9,752.6281

Reports to Health Dept 60 reports $25.2091 $1,512.5455

Process sales order 180 sales orders $117.3225 $21,118.0537

Dispatch sales order 100 dispatches $105.1173 $10,511.7333

Product Development NA NA NA $85,253.0000

Inspect cream 50 Batches $106.9719 $5,348.5950

Disposal of substandard cream 50 Batches $25.2091 $1,260.4545

Move to pasteurizing room 50 Batches $25.2091 $1,260.4545

Set up pasteurizer 50 Batches $157.6195 $7,880.9733

Weigh and sort ingredients 50 Batches $157.6195 $7,880.9733

Load pasteurizer 11,750 litres $3.9633 $46,569.1814

Operate pasteurizer 50 Batches $757.0625 $37,853.1266

Unload and Clean pasteurizer 50 Batches $157.6195 $7,880.9733

Move to mixing room 50 Batches $172.1717 $8,608.5852

Set up scales 50 Batches $86.0860 $4,304.2975

Weigh ingredients 50 Batches $157.6198 $7,880.9917

Load mixers 50 Batches $315.2388 $15,761.9421

Operate mixers 11,750 litres $7.4282 $87,281.2335

Clean mixers 50 Batches $172.1719 $8,608.5950

Move mixture to freezer 11,750 litres $0.5032 $5,912.4835

Load hopper 24,200 Products $0.4486 $10,856.6000

Set up packaging and fill 490 trays $8.0629 $3,950.8022

Move to freezer 490 trays $4.4862 $2,198.2423

Freeze products 490 trays $55.6771 $27,281.7877

Unload freezer 490 trays $4.4862 $2,198.2423

Inspect finished products 490 trays $2.7678 $1,356.2319

Disposal of substandard

product 490 trays $1.5756 $772.0284

Move to truck 470 trays $5.3957 $2,535.9850

Total Allocated Cost $4,67,544.7273

Add: Direct Materials 11,750 litres $4.0000 $47,000.0000

Total Cost $5,14,544.7273

Annual Volume 23,500

Per Unit Cost of Butter Peccan (Total Cost/Annual Volume) $21.8955

Use of Conventional Costing System:

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Student No. 297012, Name: Mr. Hussein Rkein 2019

The current costing system been followed in the company is Job costing method. This is one

of the simplest methods of costing approaches wherein the total costs incurred by the

company (Direct Material, Direct Labour and Manufacturing overheads) are applied to the

production on one uniform basis. Thus uniform basis can be labour hours, no. of products,

machine hours or any one single base for allocation of all the costs to the products

manufactured by the company. (Bragg, 2019)

With the use of the current system the cost of the product works out to be as below:

Computation of Per unit Cost

Particulars For Classic

Vanilla

For Butter

Peccan

Estimated Annual units produced 23,500 1,94,000

Direct Material $97,000 $47,000

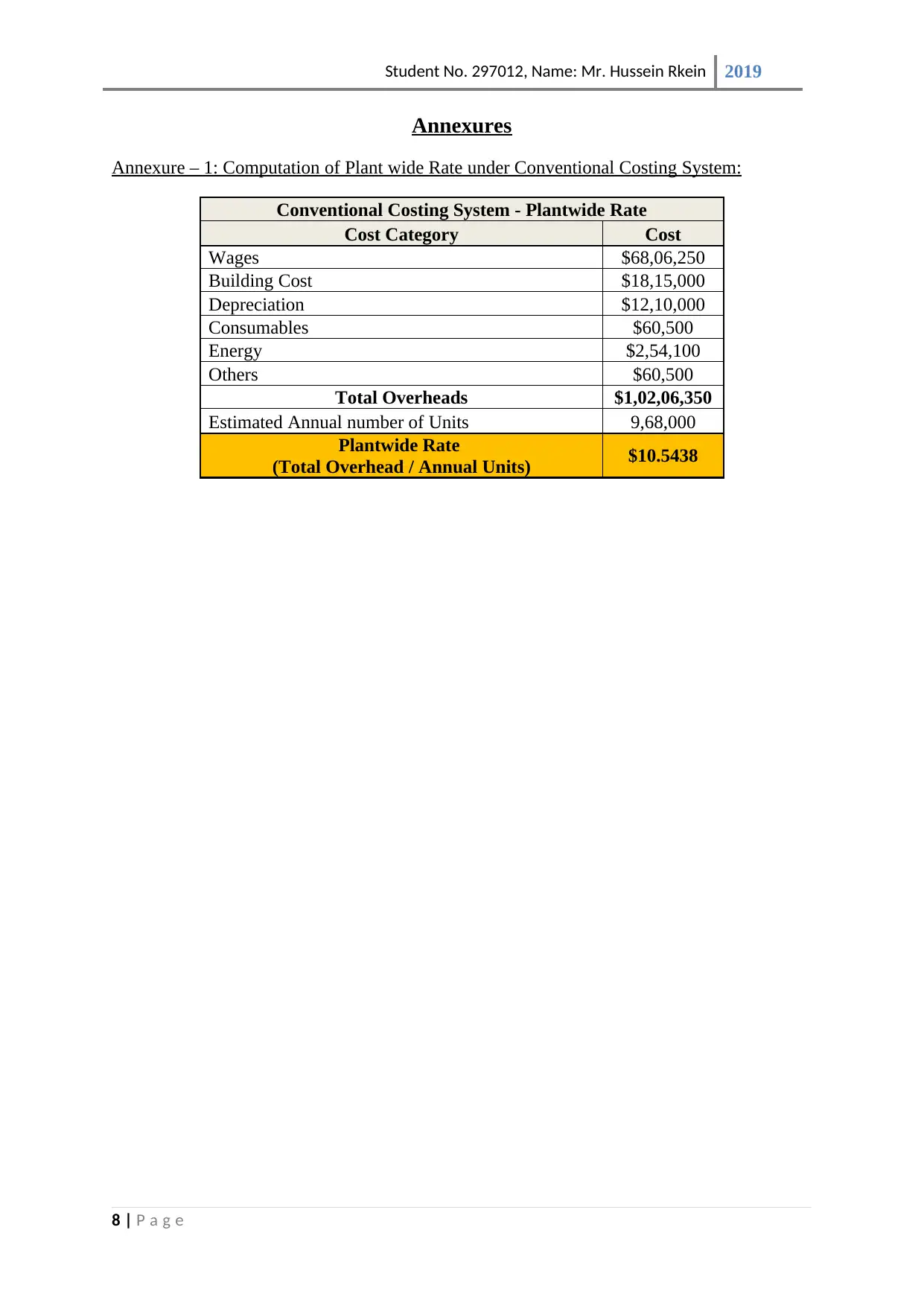

Overhead Allocated (No. of Units * Plant wide rate) $2,47,778 $20,45,488

Total Cost $3,44,778 $20,92,488

Per unit Cost (Total Cost/Units) $14.6714 $10.7860

(For computation of Plant wide Rate refer annexure 1)

Deficiency in the current Conventional Costing System:

The per unit cost of the products are comparable whereas the efforts required in both the

variety are not. This is the most critical deficiency in the current system which reveals

misguiding per unit cost and thus results into inaccurate pricing of the product leading to loss

of sale ultimately.

Use of Activity Based Costing System:

This deficiency in the system can be improved or overcome by use of Activity based costing.

Activity Based Costing is a more logical and robust method of allocating costs to the

products. The ABC method begins with identification of activities that are culminating into

costs for the company. The identified costs are then apportioned between each product based

on the usage or actual consumption of the resource by the products (AccountingCoach.com,

2019)

The benefits of using ABC in a manufacturing concern are:

a. ABC method provides reliable and accurate measurement of product costs by

focusing on actual consumption of resources by the product (Agarwal, 2019).

5 | P a g e

The current costing system been followed in the company is Job costing method. This is one

of the simplest methods of costing approaches wherein the total costs incurred by the

company (Direct Material, Direct Labour and Manufacturing overheads) are applied to the

production on one uniform basis. Thus uniform basis can be labour hours, no. of products,

machine hours or any one single base for allocation of all the costs to the products

manufactured by the company. (Bragg, 2019)

With the use of the current system the cost of the product works out to be as below:

Computation of Per unit Cost

Particulars For Classic

Vanilla

For Butter

Peccan

Estimated Annual units produced 23,500 1,94,000

Direct Material $97,000 $47,000

Overhead Allocated (No. of Units * Plant wide rate) $2,47,778 $20,45,488

Total Cost $3,44,778 $20,92,488

Per unit Cost (Total Cost/Units) $14.6714 $10.7860

(For computation of Plant wide Rate refer annexure 1)

Deficiency in the current Conventional Costing System:

The per unit cost of the products are comparable whereas the efforts required in both the

variety are not. This is the most critical deficiency in the current system which reveals

misguiding per unit cost and thus results into inaccurate pricing of the product leading to loss

of sale ultimately.

Use of Activity Based Costing System:

This deficiency in the system can be improved or overcome by use of Activity based costing.

Activity Based Costing is a more logical and robust method of allocating costs to the

products. The ABC method begins with identification of activities that are culminating into

costs for the company. The identified costs are then apportioned between each product based

on the usage or actual consumption of the resource by the products (AccountingCoach.com,

2019)

The benefits of using ABC in a manufacturing concern are:

a. ABC method provides reliable and accurate measurement of product costs by

focusing on actual consumption of resources by the product (Agarwal, 2019).

5 | P a g e

Student No. 297012, Name: Mr. Hussein Rkein 2019

b. It uses multiple activity drivers and then allocates the cost basis the usage of the

resource drivers and not merely on volume of production. (Agarwal, 2019).

c. ABC is simple and easy to understand. The companies using ABC have more accurate

and relevant cost of the product thus giving them an edge on pricing the product

accurately (Ayres, 2019)

ABC is more accurate in allocating the cost to various products being manufacture by the

company. It identifies the activities of cost for the company and then computes the total cost

for each such activity. ABC in contrast to conventional costing system do not use a single

plant wide rate for allocation of the total overhead of the company. ABC identifies each and

every activity and then their cost and then allocates them to product basis the usage of the

activity by the product. This leads to no duplication or omissions. Thus, ABC is a more

accurate and robust approach of assigning cost of the resources to the products.

The ABC is difficult and expensive to implement but once implemented its benefits surpasses

the cost incurred and gives the company a competitive edge. For Ecratic Company, we saw a

similar computation.

Conventional Costing System vs Activity Based Costing:

Under ABC costing the per unit cost of the products haven been worked as below:

The Classic vanilla is computed as $8.2380 whereas under conventional costing

system it was $14.6714.

The Butter pecan is computed as $21.8955 whereas under conventional costing

system it was $10.7860.

We clearly see that for butter peccan the per unit cost has increased by 103% from $10.7860

per unit to $21.8955 per unit. Further, for classic Vanilla it has decreased by 43% from

$14.6714 to $8.2380. This has happened because when we shift from convention costing

method to ABC the costs of the company are allocated on the basis of usage of the activity

and not simply on number of units produced.

The application of ABC for the company revealed that Butter pecan actually uses more

resources of the company and has a product cost of $21.8955 whereas it is sold for only $13

per unit. The sale price of $13 was fixed based on the cost of $10.7860 under conventional

6 | P a g e

b. It uses multiple activity drivers and then allocates the cost basis the usage of the

resource drivers and not merely on volume of production. (Agarwal, 2019).

c. ABC is simple and easy to understand. The companies using ABC have more accurate

and relevant cost of the product thus giving them an edge on pricing the product

accurately (Ayres, 2019)

ABC is more accurate in allocating the cost to various products being manufacture by the

company. It identifies the activities of cost for the company and then computes the total cost

for each such activity. ABC in contrast to conventional costing system do not use a single

plant wide rate for allocation of the total overhead of the company. ABC identifies each and

every activity and then their cost and then allocates them to product basis the usage of the

activity by the product. This leads to no duplication or omissions. Thus, ABC is a more

accurate and robust approach of assigning cost of the resources to the products.

The ABC is difficult and expensive to implement but once implemented its benefits surpasses

the cost incurred and gives the company a competitive edge. For Ecratic Company, we saw a

similar computation.

Conventional Costing System vs Activity Based Costing:

Under ABC costing the per unit cost of the products haven been worked as below:

The Classic vanilla is computed as $8.2380 whereas under conventional costing

system it was $14.6714.

The Butter pecan is computed as $21.8955 whereas under conventional costing

system it was $10.7860.

We clearly see that for butter peccan the per unit cost has increased by 103% from $10.7860

per unit to $21.8955 per unit. Further, for classic Vanilla it has decreased by 43% from

$14.6714 to $8.2380. This has happened because when we shift from convention costing

method to ABC the costs of the company are allocated on the basis of usage of the activity

and not simply on number of units produced.

The application of ABC for the company revealed that Butter pecan actually uses more

resources of the company and has a product cost of $21.8955 whereas it is sold for only $13

per unit. The sale price of $13 was fixed based on the cost of $10.7860 under conventional

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Student No. 297012, Name: Mr. Hussein Rkein 2019

costing system. But this is inaccurate as butter pecan is using more resources and is

expensive. ABC helped the company identifying the true reason of declining profitability

Similar, for classic vanilla the cost is much less as it is less recourses.

The cost allocation for overheads differs significantly under both the products namely classic

vanilla and Butter Peccan because of the difference in allocation of overheads under both the

methods.

Changes in the cost structure of the company:

The company cost structure has changed significantly in the last 15 years owing to

introduction of various product lines, changing technology, introduction of fresh talent,

increasing competition in the market, changing consumer needs and wants. The most

important change in the company’s cost structure was undoubtedly introduction of ABC for

allocation of overheads. This is because the declining profits forced the company to believe

that there are problems in pricing of the product and to streamline the prices, the accurate

costs were needed which was possible by ABC.

7 | P a g e

costing system. But this is inaccurate as butter pecan is using more resources and is

expensive. ABC helped the company identifying the true reason of declining profitability

Similar, for classic vanilla the cost is much less as it is less recourses.

The cost allocation for overheads differs significantly under both the products namely classic

vanilla and Butter Peccan because of the difference in allocation of overheads under both the

methods.

Changes in the cost structure of the company:

The company cost structure has changed significantly in the last 15 years owing to

introduction of various product lines, changing technology, introduction of fresh talent,

increasing competition in the market, changing consumer needs and wants. The most

important change in the company’s cost structure was undoubtedly introduction of ABC for

allocation of overheads. This is because the declining profits forced the company to believe

that there are problems in pricing of the product and to streamline the prices, the accurate

costs were needed which was possible by ABC.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Student No. 297012, Name: Mr. Hussein Rkein 2019

Annexures

Annexure – 1: Computation of Plant wide Rate under Conventional Costing System:

Conventional Costing System - Plantwide Rate

Cost Category Cost

Wages $68,06,250

Building Cost $18,15,000

Depreciation $12,10,000

Consumables $60,500

Energy $2,54,100

Others $60,500

Total Overheads $1,02,06,350

Estimated Annual number of Units 9,68,000

Plantwide Rate

(Total Overhead / Annual Units) $10.5438

8 | P a g e

Annexures

Annexure – 1: Computation of Plant wide Rate under Conventional Costing System:

Conventional Costing System - Plantwide Rate

Cost Category Cost

Wages $68,06,250

Building Cost $18,15,000

Depreciation $12,10,000

Consumables $60,500

Energy $2,54,100

Others $60,500

Total Overheads $1,02,06,350

Estimated Annual number of Units 9,68,000

Plantwide Rate

(Total Overhead / Annual Units) $10.5438

8 | P a g e

Student No. 297012, Name: Mr. Hussein Rkein 2019

References

Agarwal, R. (2019). Advantages and Demerits of Activity Based Costing (ABC). Your Article

Library. Retrieved from

http://www.yourarticlelibrary.com/accounting/costing/advantages-and-demerits-of-

activity-based-costing-abc/52617 on 17th May 2019.

Ayres, C. (2019). 8 Pros and Cons of Activity Based Costing. [Blog] Green Garage.

Retrieved from https://greengarageblog.org/8-pros-and-cons-of-activity-based-costing on

17th May 2019

AccountingCoach.com. (2019). Activity Based Costing | Explanation | AccountingCoach.

Retrieved from https://www.accountingcoach.com/activity-based-costing/explanation on

17th May 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 17th May 2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

dummies. (2019). Cost Accounting: The Weighted Average Costing Method - dummies.

Retrieved from https://www.dummies.com/business/accounting/cost-accounting-the-

weighted-average-costing-method/ on14 Apr. 2019].

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost accounting.

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

Turney, P. (1997). Activity based costing. London: Kogan Page.

9 | P a g e

References

Agarwal, R. (2019). Advantages and Demerits of Activity Based Costing (ABC). Your Article

Library. Retrieved from

http://www.yourarticlelibrary.com/accounting/costing/advantages-and-demerits-of-

activity-based-costing-abc/52617 on 17th May 2019.

Ayres, C. (2019). 8 Pros and Cons of Activity Based Costing. [Blog] Green Garage.

Retrieved from https://greengarageblog.org/8-pros-and-cons-of-activity-based-costing on

17th May 2019

AccountingCoach.com. (2019). Activity Based Costing | Explanation | AccountingCoach.

Retrieved from https://www.accountingcoach.com/activity-based-costing/explanation on

17th May 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 17th May 2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

dummies. (2019). Cost Accounting: The Weighted Average Costing Method - dummies.

Retrieved from https://www.dummies.com/business/accounting/cost-accounting-the-

weighted-average-costing-method/ on14 Apr. 2019].

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost accounting.

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

Turney, P. (1997). Activity based costing. London: Kogan Page.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.