Management Accounting Report: Edwards Company Financial Analysis

VerifiedAdded on 2021/02/20

|23

|6007

|32

Report

AI Summary

This report provides a detailed analysis of management accounting, focusing on its role in strategic decision-making and financial control within organizations. It begins with an explanation of management accounting and its various systems, including cost accounting, price optimization, and inventory management. The report then explores different methods of management accounting reporting, such as budget reports, inventory reports, performance reports, and cost management reports. It examines the benefits of management accounting systems, highlighting their application in organizational contexts. Furthermore, the report delves into costing techniques, specifically marginal and absorption costing, and provides examples of income statements under each method. It also discusses the advantages and disadvantages of planning tools used for budgetary control and analyzes how organizations use management accounting systems to respond to financial problems, concluding with an evaluation of planning tools for solving financial issues.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Explain management accounting and the important requirement of different types of

management accounting systems.................................................................................................2

P2. Explain different methods used for management accounting reporting................................4

M1 Examine the benefits of management accounting systems with their applications in

organisational context..................................................................................................................5

D1 Critically evaluate management accounting system and management accounting reporting

integrated with organisational process.........................................................................................5

TASK 2............................................................................................................................................5

P3. Computation of costs as per Marginal and Absorption Costing techniques..........................5

M2. Application of Management Accounting Techniques and production of appropriate

financial reporting documents....................................................................................................11

D2. Production of Financial reports which accurately apply and interpret data for a range of

business activities:.....................................................................................................................12

TASK 3..........................................................................................................................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3 Analyse the use of different planning tools and their application for forecasting budget...16

TASK 4..........................................................................................................................................16

P5. Comparison of manner by which organisations are using management accounting systems

to respond financial problems:...................................................................................................16

M4 Analyse how, in responding to financial problems, management accounting proved helpful

to get sustainable success...........................................................................................................18

D3 Evaluate planning tools for accounting respond appropriately for solving financial

problems.....................................................................................................................................19

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Explain management accounting and the important requirement of different types of

management accounting systems.................................................................................................2

P2. Explain different methods used for management accounting reporting................................4

M1 Examine the benefits of management accounting systems with their applications in

organisational context..................................................................................................................5

D1 Critically evaluate management accounting system and management accounting reporting

integrated with organisational process.........................................................................................5

TASK 2............................................................................................................................................5

P3. Computation of costs as per Marginal and Absorption Costing techniques..........................5

M2. Application of Management Accounting Techniques and production of appropriate

financial reporting documents....................................................................................................11

D2. Production of Financial reports which accurately apply and interpret data for a range of

business activities:.....................................................................................................................12

TASK 3..........................................................................................................................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3 Analyse the use of different planning tools and their application for forecasting budget...16

TASK 4..........................................................................................................................................16

P5. Comparison of manner by which organisations are using management accounting systems

to respond financial problems:...................................................................................................16

M4 Analyse how, in responding to financial problems, management accounting proved helpful

to get sustainable success...........................................................................................................18

D3 Evaluate planning tools for accounting respond appropriately for solving financial

problems.....................................................................................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

.......................................................................................................................................................21

INTRODUCTION

Management accounting that also known as managerial accounting that defined as a

process to accumulating financial information and resources for the managers in taking important

decisions for future growth and enhancement. It is only used for internal team of the

organisation and that attribute makes in different from financial accounting. This report is based

on Edwards which is an vacuum engineering company headquarter is in London, United

Kingdom. This report is based on management accounting and its essential requirement of

various kinds of management accounting systems with various methods of it. It also includes

various costs and income statement by evaluating its attributes. In it advantages and disadvantage

of various kinds of planning tools and techniques for budgetary control, It focus on comparison

of management accounting systems to respond financial problems. It also evaluate various

practices by comparing and contrasting with management reporting in better way.

TASK 1

P1. Explain management accounting and the important requirement of different types of

management accounting systems.

Management accounting is a tool used by the company and managers regarding the formation of

strategies which require necessary information so this information can be assessed by them

which increases the efficiency of decision making. (Apak and et.al ., 2012.). This refers to a

process which is involved in planning and increase value of the performance managing systems

which increases the expertise level of financial reporting. Therefore, it control the management

strategy.

Management accounting system includes preparation of financial and statistical

information for business manger so they can form decisions regarding day to day operations and

short term managerial decisions.

The management accounting system has its scope in strategic management, performance

management and risk management ( Christ and Burritt, 2017 ). The accountant applies this

system to look forward and take decision regarding the future of the company. This helps

REFERENCES..............................................................................................................................20

.......................................................................................................................................................21

INTRODUCTION

Management accounting that also known as managerial accounting that defined as a

process to accumulating financial information and resources for the managers in taking important

decisions for future growth and enhancement. It is only used for internal team of the

organisation and that attribute makes in different from financial accounting. This report is based

on Edwards which is an vacuum engineering company headquarter is in London, United

Kingdom. This report is based on management accounting and its essential requirement of

various kinds of management accounting systems with various methods of it. It also includes

various costs and income statement by evaluating its attributes. In it advantages and disadvantage

of various kinds of planning tools and techniques for budgetary control, It focus on comparison

of management accounting systems to respond financial problems. It also evaluate various

practices by comparing and contrasting with management reporting in better way.

TASK 1

P1. Explain management accounting and the important requirement of different types of

management accounting systems.

Management accounting is a tool used by the company and managers regarding the formation of

strategies which require necessary information so this information can be assessed by them

which increases the efficiency of decision making. (Apak and et.al ., 2012.). This refers to a

process which is involved in planning and increase value of the performance managing systems

which increases the expertise level of financial reporting. Therefore, it control the management

strategy.

Management accounting system includes preparation of financial and statistical

information for business manger so they can form decisions regarding day to day operations and

short term managerial decisions.

The management accounting system has its scope in strategic management, performance

management and risk management ( Christ and Burritt, 2017 ). The accountant applies this

system to look forward and take decision regarding the future of the company. This helps

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company in building the organisation financial strength through proper use of financial

resources.

There are different types of management accounting system are as-

Cost accounting system- The cost accounting system is also known as costing system

which is used to determine the cost allocation of different activity operated in business.

This accounting system helps Edwards to manage and control the cost of activities and

this tool is used by company to calculate the total cost of the company which incur in

performing different activities and it evaluates the cost and the reasons to incur. The

calculation of total cost incurred will help the company to calculate their profitability In

this type of accounting system the cost is allocated through various approaches such as

job-order costing, process costing etc. and these have their own. different structure and

benefits. The estimation of cost is necessary for Edward as the fixation of price is totally

based on it.

Price optimisation system- This is the system which is considered as mathematical

programs which calculate the demand which varies according to the different price level.

The data is combined with the calculated cost and their inventory levels at recommended

prices which will increase the profitability (Edwards, 2013.). The Edwards uses this

programme to control the level of price by proper calculation of cost and it helps in

determination of price of the goods or products of the company. This provides benefits to

both company and customers as the cost calculation will lead to company in fixing lower

price and it allow customer to buy the product at reasonable price.

Inventory management system- This is a system which helps the management of

company in managing and controlling the inventory level of the company (Farouk,

Cherian and Jacob, 2012.). The inventory word includes raw material, work-in-progress

and closing stock of the company. The Edwards use this system to control the raw

materials of the company which helps in reducing wastage as according to the demand

production is required to be take place. The system can be used by the company to

control the quantity of raw material by using LIFO and FIFO. These are the techniques

which are used by the company to maintain the quality of raw material. The last in first

out refers to the system where last produced quantity will be sold first and in FIFO the

resources.

There are different types of management accounting system are as-

Cost accounting system- The cost accounting system is also known as costing system

which is used to determine the cost allocation of different activity operated in business.

This accounting system helps Edwards to manage and control the cost of activities and

this tool is used by company to calculate the total cost of the company which incur in

performing different activities and it evaluates the cost and the reasons to incur. The

calculation of total cost incurred will help the company to calculate their profitability In

this type of accounting system the cost is allocated through various approaches such as

job-order costing, process costing etc. and these have their own. different structure and

benefits. The estimation of cost is necessary for Edward as the fixation of price is totally

based on it.

Price optimisation system- This is the system which is considered as mathematical

programs which calculate the demand which varies according to the different price level.

The data is combined with the calculated cost and their inventory levels at recommended

prices which will increase the profitability (Edwards, 2013.). The Edwards uses this

programme to control the level of price by proper calculation of cost and it helps in

determination of price of the goods or products of the company. This provides benefits to

both company and customers as the cost calculation will lead to company in fixing lower

price and it allow customer to buy the product at reasonable price.

Inventory management system- This is a system which helps the management of

company in managing and controlling the inventory level of the company (Farouk,

Cherian and Jacob, 2012.). The inventory word includes raw material, work-in-progress

and closing stock of the company. The Edwards use this system to control the raw

materials of the company which helps in reducing wastage as according to the demand

production is required to be take place. The system can be used by the company to

control the quantity of raw material by using LIFO and FIFO. These are the techniques

which are used by the company to maintain the quality of raw material. The last in first

out refers to the system where last produced quantity will be sold first and in FIFO the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quantity which is produced firstly has to be sold firstly. This system is used by desktop,

barcode scanners and other devices to determine the accurate level of inventory.

P2. Explain different methods used for management accounting reporting.

Management accounting reports helps an organisation to record their actual performance some of

them is given below:. These reports in the organisations are prepared as per the requirements.

Various types of reports which an organisation uses are as follows :

Budget reports : These reports are prepared for the prediction about the companies

future financial condition. Edwards is required to prepare this report in order to compare their

actual budget with the estimated one so that the company can evaluate their performance and can

determine the amount of expenses to be done during a year. These reports those which provides

an overview about the objectives of the companies and are also termed as the future reports for

the firms objective.

Inventory reports : This report contain the all the necessary information in detailed

about the stock that is currently present in organisation. In Edwards this will helps the

management to analysis the cost which is related with the quantity and price of raw material.

This document helps the organisation to maintain current level of inventory that helps to achieve

their targets. Moreover this helps an organisation to order required stock to its suppliers.

Performance reports : These reports are prepared in order to measure the performance

of employees as well as organisation's. The company like Edwards will be beneficial if they

prepare this report will provide them blueprint of the performance which can be compared to the

standard one (Gond and et.al ., 2012.). It will also help Edwards in identifying the areas which

are needed to be improve and will also allow them to take corrective measures. By measuring the

performance the Edwards company can enhance their productivity and profitability.

Cost managerial accounting reports : These reports are prepared to know the amount

of cost that incurs while performing the task. For The company like Edwards it is importance

focus on preparing this report as this reports will provide them the idea of amount that is to be

invested and the amount of cost that has incurred in carrying out the operations. It will also help

the company to control the overall cost of the operations and will also leads to decrease in their

unnecessary expenses .It also provides the detail about the income statement, balance sheets and

inflow and outflow of the cash so that the firm can make their investments accordingly.

barcode scanners and other devices to determine the accurate level of inventory.

P2. Explain different methods used for management accounting reporting.

Management accounting reports helps an organisation to record their actual performance some of

them is given below:. These reports in the organisations are prepared as per the requirements.

Various types of reports which an organisation uses are as follows :

Budget reports : These reports are prepared for the prediction about the companies

future financial condition. Edwards is required to prepare this report in order to compare their

actual budget with the estimated one so that the company can evaluate their performance and can

determine the amount of expenses to be done during a year. These reports those which provides

an overview about the objectives of the companies and are also termed as the future reports for

the firms objective.

Inventory reports : This report contain the all the necessary information in detailed

about the stock that is currently present in organisation. In Edwards this will helps the

management to analysis the cost which is related with the quantity and price of raw material.

This document helps the organisation to maintain current level of inventory that helps to achieve

their targets. Moreover this helps an organisation to order required stock to its suppliers.

Performance reports : These reports are prepared in order to measure the performance

of employees as well as organisation's. The company like Edwards will be beneficial if they

prepare this report will provide them blueprint of the performance which can be compared to the

standard one (Gond and et.al ., 2012.). It will also help Edwards in identifying the areas which

are needed to be improve and will also allow them to take corrective measures. By measuring the

performance the Edwards company can enhance their productivity and profitability.

Cost managerial accounting reports : These reports are prepared to know the amount

of cost that incurs while performing the task. For The company like Edwards it is importance

focus on preparing this report as this reports will provide them the idea of amount that is to be

invested and the amount of cost that has incurred in carrying out the operations. It will also help

the company to control the overall cost of the operations and will also leads to decrease in their

unnecessary expenses .It also provides the detail about the income statement, balance sheets and

inflow and outflow of the cash so that the firm can make their investments accordingly.

Account receivable ageing reports : Account Receivables are the expected payments

due from the customers (Klychova, Faskhutdinova and Sadrieva, 2014. ). Accounts receivable

ageing report is a list of customers of the organization that provides necessary informations about

sum of amount due from the customers, due dates for receipts, over due receivables' dates,

interest on due amount, contact details of debtors, bad-debt and other important details regarding

payments from the customers of selected organization . The management of respective firm

Edwards prepares accounts receivable reports on a regular basis so that it can manage records of

its debtors and decide the potency of its credit collection period as this will give them a idea of

all their debt and credits.

M1 Examine the benefits of management accounting systems with their applications in

organisational context.

Management accounting system is to give assistance to the management team for

improving the quality of decisions. Management accounting systems proved helpful in planning

each and every attribute as per the future demands in market. After prepare financial plans

organisation control it with help of management accounting systems that are proved beneficial to

get right kinds of output for Edwards. So it proved helpful to deliver right kind of value to their

ultimate consumer base. In that aspect management accounting system helps in accumulating

cost in better way and price optimisation helps in evaluate prices according to the various

attributes.

D1 Critically evaluate management accounting system and management accounting reporting

integrated with organisational process.

Management accounting system and management accounting reporting closely related

with each other and provide desirable outcomes in organisational growth and enhancement. It

proved helpful in providing ERP solutions which are robust in nature. It gives assurance to

getting a right response and with it management accounting get full support with complete access

to potential outcomes in context of Edwards. Sometimes integration of both these objects hinders

self interest of an organisation that it create chaos in organisational managing objects. There are

great relation in system and accounting report that after evaluating system organisation can be

able to build a suitable accounting report to get right kind of outputs in an organisation.

due from the customers (Klychova, Faskhutdinova and Sadrieva, 2014. ). Accounts receivable

ageing report is a list of customers of the organization that provides necessary informations about

sum of amount due from the customers, due dates for receipts, over due receivables' dates,

interest on due amount, contact details of debtors, bad-debt and other important details regarding

payments from the customers of selected organization . The management of respective firm

Edwards prepares accounts receivable reports on a regular basis so that it can manage records of

its debtors and decide the potency of its credit collection period as this will give them a idea of

all their debt and credits.

M1 Examine the benefits of management accounting systems with their applications in

organisational context.

Management accounting system is to give assistance to the management team for

improving the quality of decisions. Management accounting systems proved helpful in planning

each and every attribute as per the future demands in market. After prepare financial plans

organisation control it with help of management accounting systems that are proved beneficial to

get right kinds of output for Edwards. So it proved helpful to deliver right kind of value to their

ultimate consumer base. In that aspect management accounting system helps in accumulating

cost in better way and price optimisation helps in evaluate prices according to the various

attributes.

D1 Critically evaluate management accounting system and management accounting reporting

integrated with organisational process.

Management accounting system and management accounting reporting closely related

with each other and provide desirable outcomes in organisational growth and enhancement. It

proved helpful in providing ERP solutions which are robust in nature. It gives assurance to

getting a right response and with it management accounting get full support with complete access

to potential outcomes in context of Edwards. Sometimes integration of both these objects hinders

self interest of an organisation that it create chaos in organisational managing objects. There are

great relation in system and accounting report that after evaluating system organisation can be

able to build a suitable accounting report to get right kind of outputs in an organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3. Computation of costs as per Marginal and Absorption Costing techniques

Costs form an integral part of every organisation and enable the business managers to

easily measure the strengths as well as weaknesses in the form of bottlenecks in an effective

manner (Moser, 2012. ). Based on the nature, size and type of organisations, costs can be

mainly divided in the form of direct and indirect costs, materials and expenses.

Costing techniques have been utilised to indicate optimal transparency as well as

exercise effective control for decision-making purposes (Pavlatos, 2015. ). Mainly,

organisations employ marginal and absorption costing techniques so as to prepare important

financial statements such as Income Statements and Balance Sheet among others. These have

been discussed as under:

Marginal Costing Method:

Under this technique, fixed and variable costs are distinguished in order to determine the

additional, or marginal, cost incurred on the production of an additional unit of output.

Generally, this costing technique is employed by the organisation in order to ascertain the impact

of changes in input as well as output on the overall profit earned by the organisation. The main

purpose served through the utilisation of this technique is that the contribution of product cost in

terms of one unit is obtained by the business manager (Salterio, 2015 ). It is important to note

that under this methodology, fixed costs are not considered. Marginal Costing can be mainly

expressed in the terms of contribution earned per unit of output produced. Here, the variable cost

is represented by the product cost whereas fixed cost is assumed as period cost.

Annex (A)

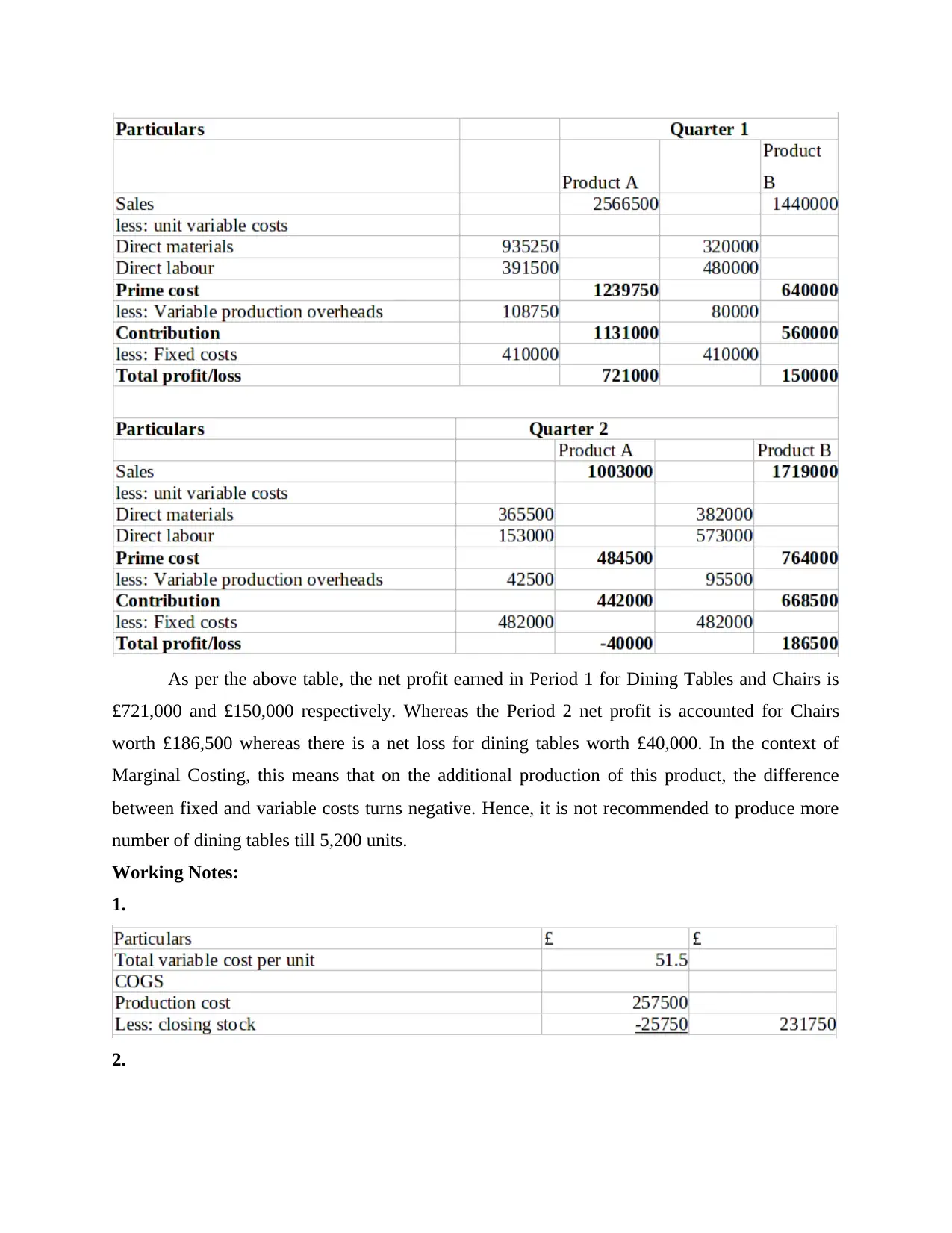

Income Statement under Marginal Costing Method:

As per this technique, the income statement includes gross sales, calculates variable costs

of goods sold as well as selling expenses. The following table indicates the calculation of Net

Profit (or Loss) for two products A and B viz. Tables and Chairs relating to two time periods viz.

Quarter 1 and Quarter 2:

P3. Computation of costs as per Marginal and Absorption Costing techniques

Costs form an integral part of every organisation and enable the business managers to

easily measure the strengths as well as weaknesses in the form of bottlenecks in an effective

manner (Moser, 2012. ). Based on the nature, size and type of organisations, costs can be

mainly divided in the form of direct and indirect costs, materials and expenses.

Costing techniques have been utilised to indicate optimal transparency as well as

exercise effective control for decision-making purposes (Pavlatos, 2015. ). Mainly,

organisations employ marginal and absorption costing techniques so as to prepare important

financial statements such as Income Statements and Balance Sheet among others. These have

been discussed as under:

Marginal Costing Method:

Under this technique, fixed and variable costs are distinguished in order to determine the

additional, or marginal, cost incurred on the production of an additional unit of output.

Generally, this costing technique is employed by the organisation in order to ascertain the impact

of changes in input as well as output on the overall profit earned by the organisation. The main

purpose served through the utilisation of this technique is that the contribution of product cost in

terms of one unit is obtained by the business manager (Salterio, 2015 ). It is important to note

that under this methodology, fixed costs are not considered. Marginal Costing can be mainly

expressed in the terms of contribution earned per unit of output produced. Here, the variable cost

is represented by the product cost whereas fixed cost is assumed as period cost.

Annex (A)

Income Statement under Marginal Costing Method:

As per this technique, the income statement includes gross sales, calculates variable costs

of goods sold as well as selling expenses. The following table indicates the calculation of Net

Profit (or Loss) for two products A and B viz. Tables and Chairs relating to two time periods viz.

Quarter 1 and Quarter 2:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per the above table, the net profit earned in Period 1 for Dining Tables and Chairs is

£721,000 and £150,000 respectively. Whereas the Period 2 net profit is accounted for Chairs

worth £186,500 whereas there is a net loss for dining tables worth £40,000. In the context of

Marginal Costing, this means that on the additional production of this product, the difference

between fixed and variable costs turns negative. Hence, it is not recommended to produce more

number of dining tables till 5,200 units.

Working Notes:

1.

2.

£721,000 and £150,000 respectively. Whereas the Period 2 net profit is accounted for Chairs

worth £186,500 whereas there is a net loss for dining tables worth £40,000. In the context of

Marginal Costing, this means that on the additional production of this product, the difference

between fixed and variable costs turns negative. Hence, it is not recommended to produce more

number of dining tables till 5,200 units.

Working Notes:

1.

2.

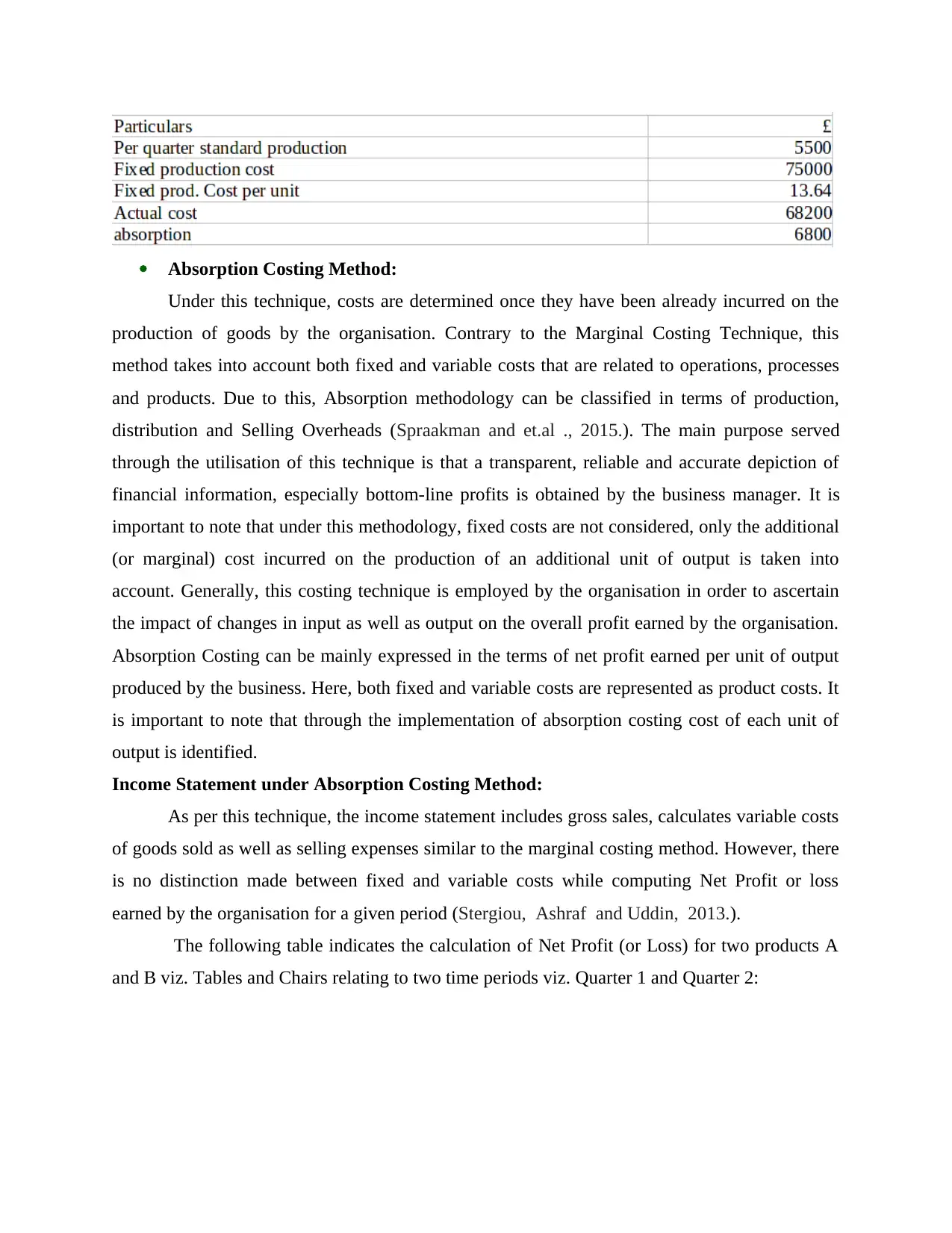

Absorption Costing Method:

Under this technique, costs are determined once they have been already incurred on the

production of goods by the organisation. Contrary to the Marginal Costing Technique, this

method takes into account both fixed and variable costs that are related to operations, processes

and products. Due to this, Absorption methodology can be classified in terms of production,

distribution and Selling Overheads (Spraakman and et.al ., 2015.). The main purpose served

through the utilisation of this technique is that a transparent, reliable and accurate depiction of

financial information, especially bottom-line profits is obtained by the business manager. It is

important to note that under this methodology, fixed costs are not considered, only the additional

(or marginal) cost incurred on the production of an additional unit of output is taken into

account. Generally, this costing technique is employed by the organisation in order to ascertain

the impact of changes in input as well as output on the overall profit earned by the organisation.

Absorption Costing can be mainly expressed in the terms of net profit earned per unit of output

produced by the business. Here, both fixed and variable costs are represented as product costs. It

is important to note that through the implementation of absorption costing cost of each unit of

output is identified.

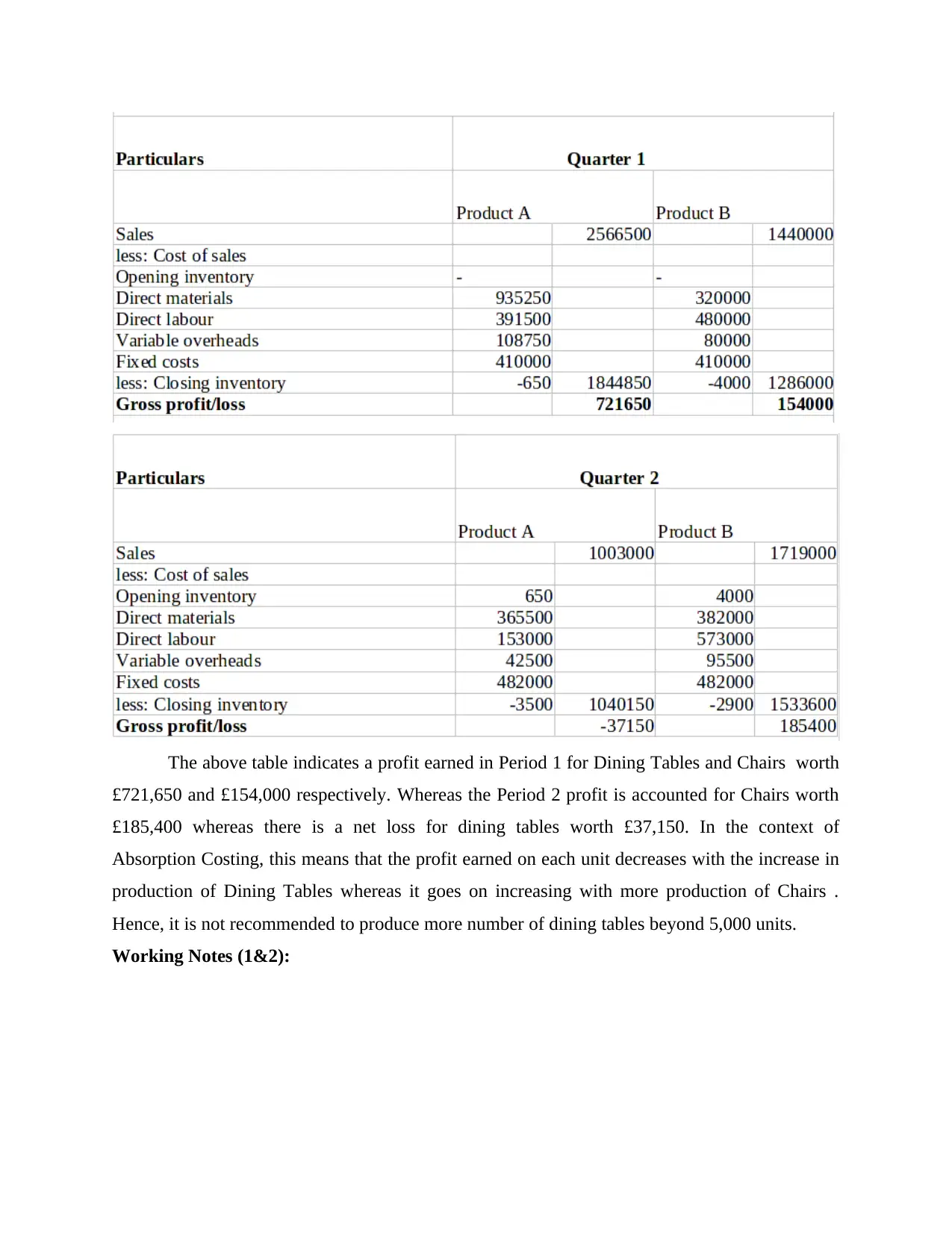

Income Statement under Absorption Costing Method:

As per this technique, the income statement includes gross sales, calculates variable costs

of goods sold as well as selling expenses similar to the marginal costing method. However, there

is no distinction made between fixed and variable costs while computing Net Profit or loss

earned by the organisation for a given period (Stergiou, Ashraf and Uddin, 2013.).

The following table indicates the calculation of Net Profit (or Loss) for two products A

and B viz. Tables and Chairs relating to two time periods viz. Quarter 1 and Quarter 2:

Under this technique, costs are determined once they have been already incurred on the

production of goods by the organisation. Contrary to the Marginal Costing Technique, this

method takes into account both fixed and variable costs that are related to operations, processes

and products. Due to this, Absorption methodology can be classified in terms of production,

distribution and Selling Overheads (Spraakman and et.al ., 2015.). The main purpose served

through the utilisation of this technique is that a transparent, reliable and accurate depiction of

financial information, especially bottom-line profits is obtained by the business manager. It is

important to note that under this methodology, fixed costs are not considered, only the additional

(or marginal) cost incurred on the production of an additional unit of output is taken into

account. Generally, this costing technique is employed by the organisation in order to ascertain

the impact of changes in input as well as output on the overall profit earned by the organisation.

Absorption Costing can be mainly expressed in the terms of net profit earned per unit of output

produced by the business. Here, both fixed and variable costs are represented as product costs. It

is important to note that through the implementation of absorption costing cost of each unit of

output is identified.

Income Statement under Absorption Costing Method:

As per this technique, the income statement includes gross sales, calculates variable costs

of goods sold as well as selling expenses similar to the marginal costing method. However, there

is no distinction made between fixed and variable costs while computing Net Profit or loss

earned by the organisation for a given period (Stergiou, Ashraf and Uddin, 2013.).

The following table indicates the calculation of Net Profit (or Loss) for two products A

and B viz. Tables and Chairs relating to two time periods viz. Quarter 1 and Quarter 2:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above table indicates a profit earned in Period 1 for Dining Tables and Chairs worth

£721,650 and £154,000 respectively. Whereas the Period 2 profit is accounted for Chairs worth

£185,400 whereas there is a net loss for dining tables worth £37,150. In the context of

Absorption Costing, this means that the profit earned on each unit decreases with the increase in

production of Dining Tables whereas it goes on increasing with more production of Chairs .

Hence, it is not recommended to produce more number of dining tables beyond 5,000 units.

Working Notes (1&2):

£721,650 and £154,000 respectively. Whereas the Period 2 profit is accounted for Chairs worth

£185,400 whereas there is a net loss for dining tables worth £37,150. In the context of

Absorption Costing, this means that the profit earned on each unit decreases with the increase in

production of Dining Tables whereas it goes on increasing with more production of Chairs .

Hence, it is not recommended to produce more number of dining tables beyond 5,000 units.

Working Notes (1&2):

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

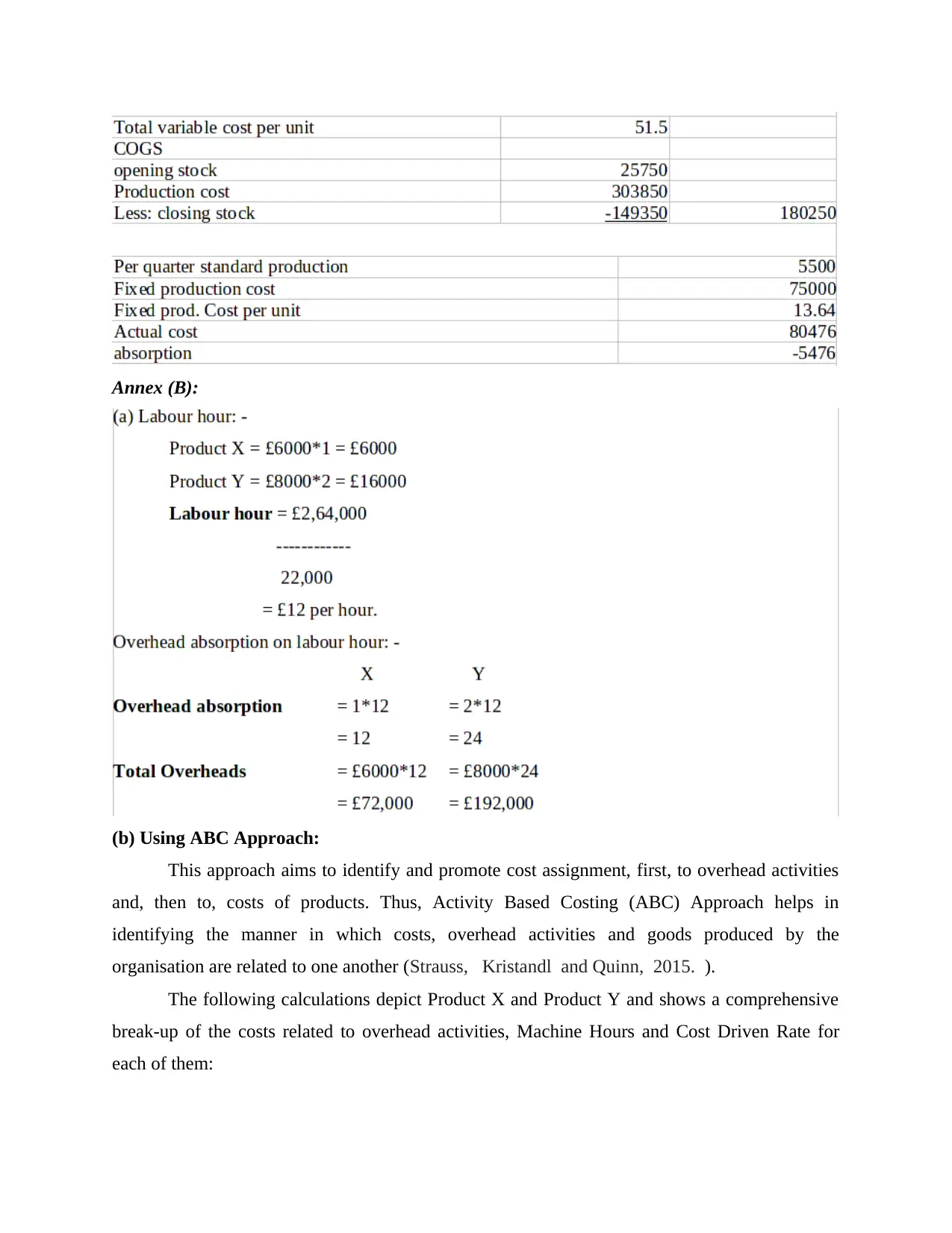

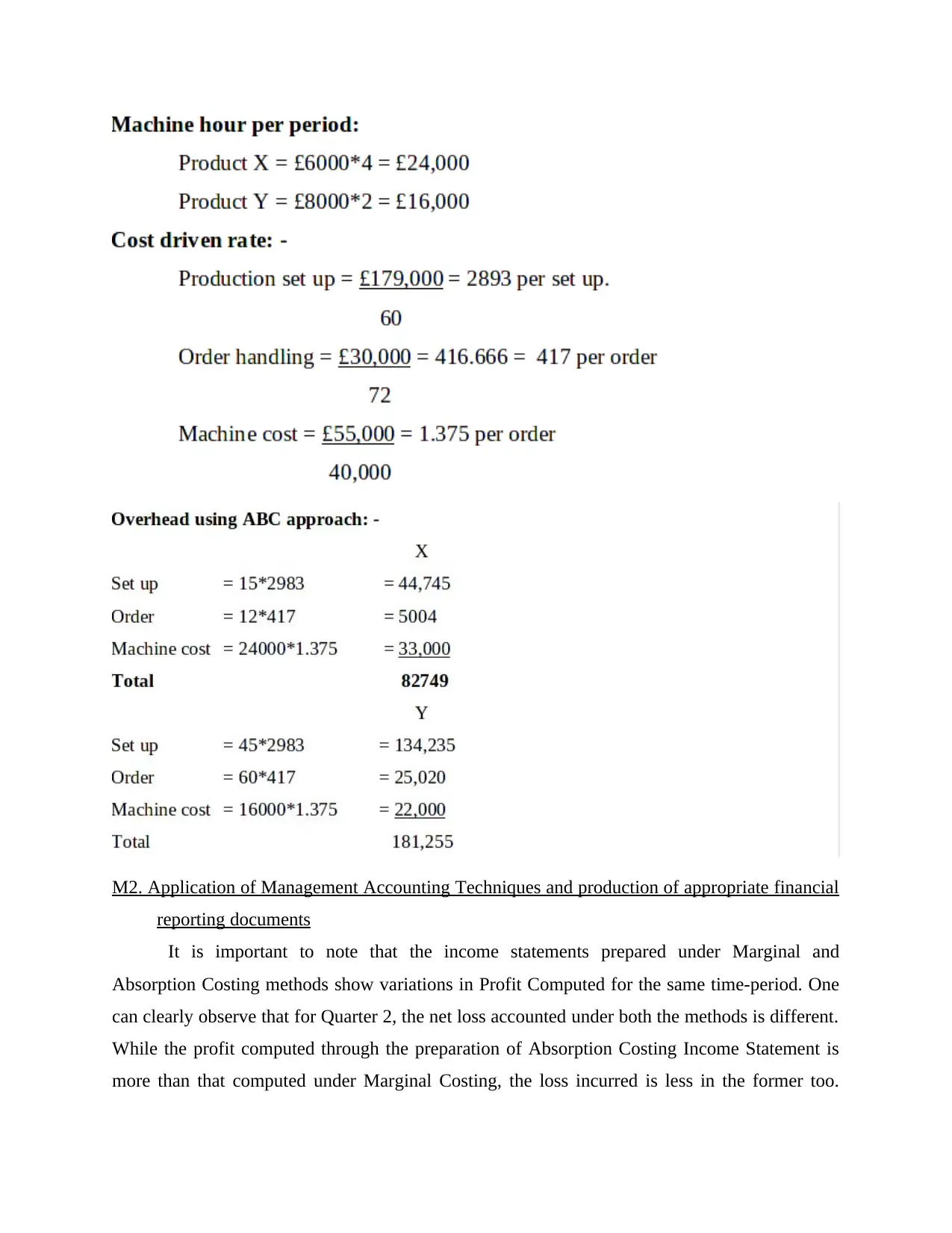

Annex (B):

(b) Using ABC Approach:

This approach aims to identify and promote cost assignment, first, to overhead activities

and, then to, costs of products. Thus, Activity Based Costing (ABC) Approach helps in

identifying the manner in which costs, overhead activities and goods produced by the

organisation are related to one another (Strauss, Kristandl and Quinn, 2015. ).

The following calculations depict Product X and Product Y and shows a comprehensive

break-up of the costs related to overhead activities, Machine Hours and Cost Driven Rate for

each of them:

(b) Using ABC Approach:

This approach aims to identify and promote cost assignment, first, to overhead activities

and, then to, costs of products. Thus, Activity Based Costing (ABC) Approach helps in

identifying the manner in which costs, overhead activities and goods produced by the

organisation are related to one another (Strauss, Kristandl and Quinn, 2015. ).

The following calculations depict Product X and Product Y and shows a comprehensive

break-up of the costs related to overhead activities, Machine Hours and Cost Driven Rate for

each of them:

M2. Application of Management Accounting Techniques and production of appropriate financial

reporting documents

It is important to note that the income statements prepared under Marginal and

Absorption Costing methods show variations in Profit Computed for the same time-period. One

can clearly observe that for Quarter 2, the net loss accounted under both the methods is different.

While the profit computed through the preparation of Absorption Costing Income Statement is

more than that computed under Marginal Costing, the loss incurred is less in the former too.

reporting documents

It is important to note that the income statements prepared under Marginal and

Absorption Costing methods show variations in Profit Computed for the same time-period. One

can clearly observe that for Quarter 2, the net loss accounted under both the methods is different.

While the profit computed through the preparation of Absorption Costing Income Statement is

more than that computed under Marginal Costing, the loss incurred is less in the former too.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.