EFB344 Risk Management & Derivatives: VaR & Hedging Analysis

VerifiedAdded on 2023/06/03

|15

|2387

|260

Report

AI Summary

This report focuses on calculating Value at Risk (VaR) for a portfolio of Qantas and Fairfax Media shares and analyzing hedging strategies using derivatives. It compares VaR estimates using normal distribution with a rolling window, EWMA, and historical simulation, selecting the best model based on Basel traffic lights. The report also details beta calculation, the number of future contracts needed for hedging, and the valuation of put options, including a six-step put option valuation. Finally, it includes a profit diagram illustrating the potential payoff from the investment strategy. Desklib provides access to similar solved assignments and study tools for students.

Running head: RISK MANAGEMENT

Risk Management

Name of the Student

Name of the University

Authors Note

Course ID

Risk Management

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

RISK MANAGEMENT

Table of contents

1. Choosing adequate VAR with a confidence level of 99%:....................................................2

2.1 Calculating VAR with normal distribution based on 252 rolling window:.........................2

2.2 Calculating normal distribution with EWMA:.....................................................................2

2.3 Calculating historical simulation based on 252 days:..........................................................3

3. Selecting the best model for selecting required VAR (10, 99%) for January 3, 2016:..........5

4. Calculating the hedging strategy:...........................................................................................6

4.1 Beta calculation:...................................................................................................................6

4.2 Number of future contract:...................................................................................................6

4.3 VAR of the portfolio:...........................................................................................................8

4.4 Valuation of Put option:.......................................................................................................8

4.5 Valuation of six step put option:..........................................................................................9

4.5 Profit diagram:...................................................................................................................12

Bibliography:............................................................................................................................13

RISK MANAGEMENT

Table of contents

1. Choosing adequate VAR with a confidence level of 99%:....................................................2

2.1 Calculating VAR with normal distribution based on 252 rolling window:.........................2

2.2 Calculating normal distribution with EWMA:.....................................................................2

2.3 Calculating historical simulation based on 252 days:..........................................................3

3. Selecting the best model for selecting required VAR (10, 99%) for January 3, 2016:..........5

4. Calculating the hedging strategy:...........................................................................................6

4.1 Beta calculation:...................................................................................................................6

4.2 Number of future contract:...................................................................................................6

4.3 VAR of the portfolio:...........................................................................................................8

4.4 Valuation of Put option:.......................................................................................................8

4.5 Valuation of six step put option:..........................................................................................9

4.5 Profit diagram:...................................................................................................................12

Bibliography:............................................................................................................................13

2

RISK MANAGEMENT

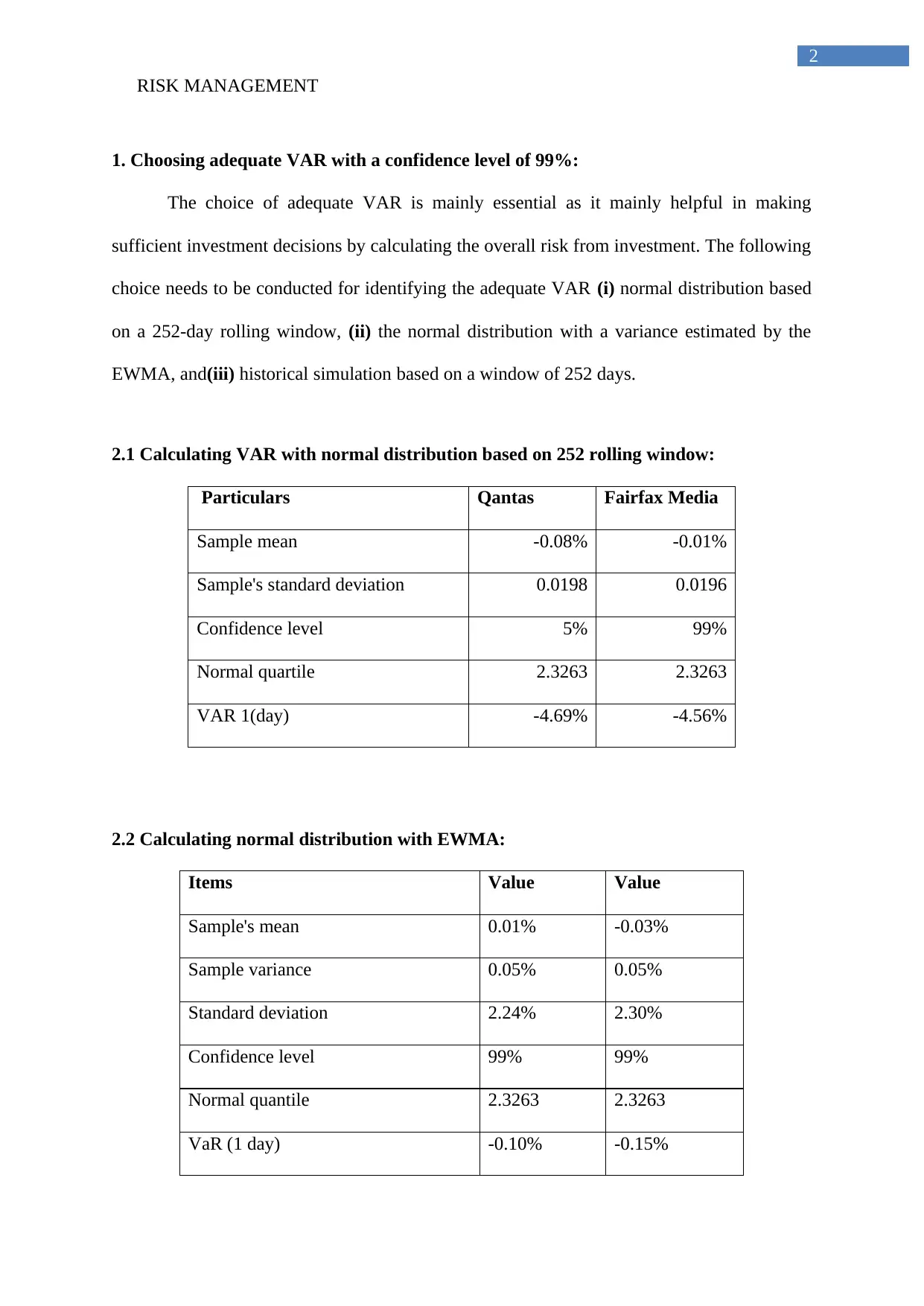

1. Choosing adequate VAR with a confidence level of 99%:

The choice of adequate VAR is mainly essential as it mainly helpful in making

sufficient investment decisions by calculating the overall risk from investment. The following

choice needs to be conducted for identifying the adequate VAR (i) normal distribution based

on a 252-day rolling window, (ii) the normal distribution with a variance estimated by the

EWMA, and(iii) historical simulation based on a window of 252 days.

2.1 Calculating VAR with normal distribution based on 252 rolling window:

Particulars Qantas Fairfax Media

Sample mean -0.08% -0.01%

Sample's standard deviation 0.0198 0.0196

Confidence level 5% 99%

Normal quartile 2.3263 2.3263

VAR 1(day) -4.69% -4.56%

2.2 Calculating normal distribution with EWMA:

Items Value Value

Sample's mean 0.01% -0.03%

Sample variance 0.05% 0.05%

Standard deviation 2.24% 2.30%

Confidence level 99% 99%

Normal quantile 2.3263 2.3263

VaR (1 day) -0.10% -0.15%

RISK MANAGEMENT

1. Choosing adequate VAR with a confidence level of 99%:

The choice of adequate VAR is mainly essential as it mainly helpful in making

sufficient investment decisions by calculating the overall risk from investment. The following

choice needs to be conducted for identifying the adequate VAR (i) normal distribution based

on a 252-day rolling window, (ii) the normal distribution with a variance estimated by the

EWMA, and(iii) historical simulation based on a window of 252 days.

2.1 Calculating VAR with normal distribution based on 252 rolling window:

Particulars Qantas Fairfax Media

Sample mean -0.08% -0.01%

Sample's standard deviation 0.0198 0.0196

Confidence level 5% 99%

Normal quartile 2.3263 2.3263

VAR 1(day) -4.69% -4.56%

2.2 Calculating normal distribution with EWMA:

Items Value Value

Sample's mean 0.01% -0.03%

Sample variance 0.05% 0.05%

Standard deviation 2.24% 2.30%

Confidence level 99% 99%

Normal quantile 2.3263 2.3263

VaR (1 day) -0.10% -0.15%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

RISK MANAGEMENT

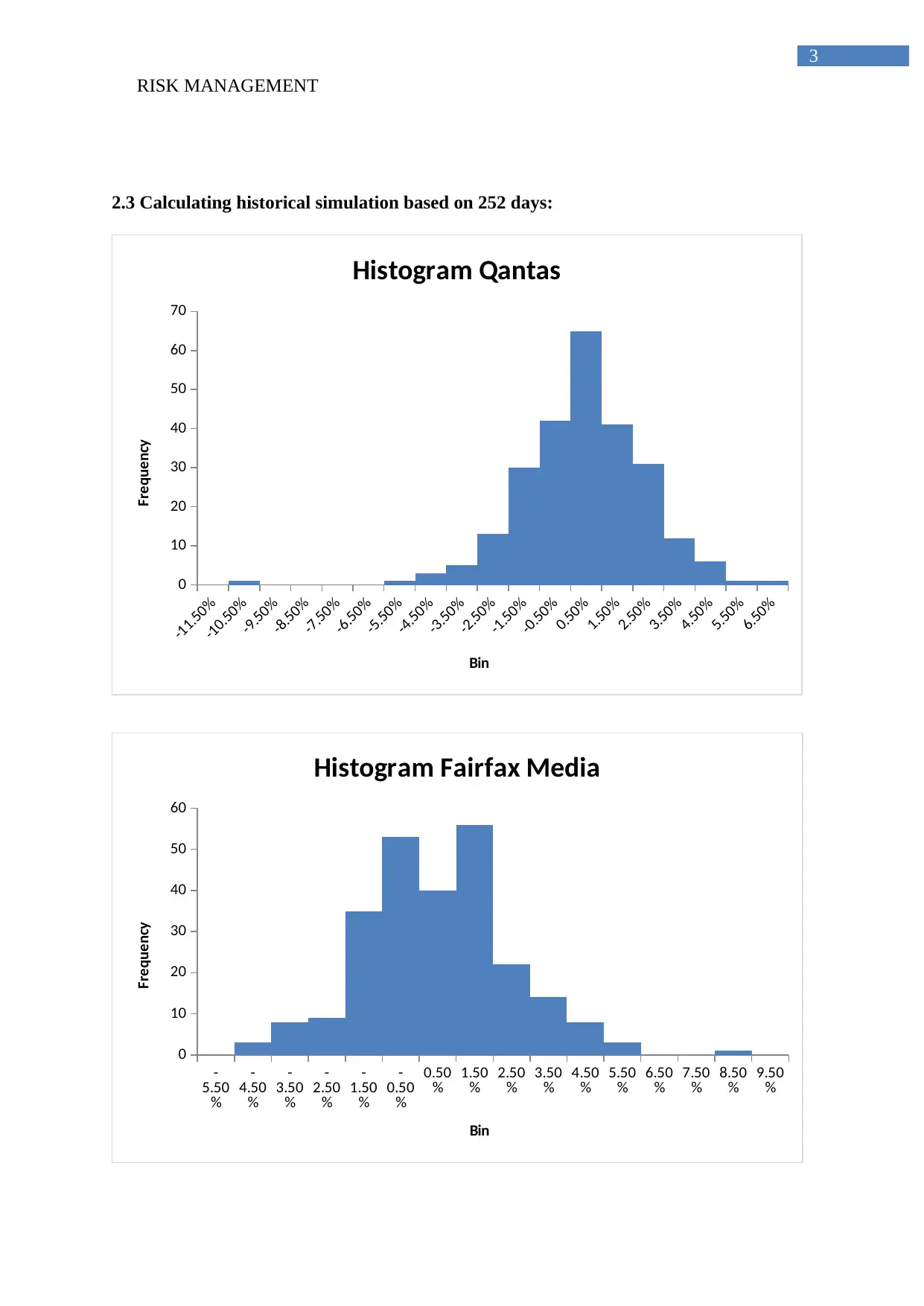

2.3 Calculating historical simulation based on 252 days:

-11.50%

-10.50%

-9.50%

-8.50%

-7.50%

-6.50%

-5.50%

-4.50%

-3.50%

-2.50%

-1.50%

-0.50%

0.50%

1.50%

2.50%

3.50%

4.50%

5.50%

6.50%

0

10

20

30

40

50

60

70

Histogram Qantas

Bin

Frequency

-

5.50

%

-

4.50

%

-

3.50

%

-

2.50

%

-

1.50

%

-

0.50

%

0.50

% 1.50

% 2.50

% 3.50

% 4.50

% 5.50

% 6.50

% 7.50

% 8.50

% 9.50

%

0

10

20

30

40

50

60

Histogram Fairfax Media

Bin

Frequency

RISK MANAGEMENT

2.3 Calculating historical simulation based on 252 days:

-11.50%

-10.50%

-9.50%

-8.50%

-7.50%

-6.50%

-5.50%

-4.50%

-3.50%

-2.50%

-1.50%

-0.50%

0.50%

1.50%

2.50%

3.50%

4.50%

5.50%

6.50%

0

10

20

30

40

50

60

70

Histogram Qantas

Bin

Frequency

-

5.50

%

-

4.50

%

-

3.50

%

-

2.50

%

-

1.50

%

-

0.50

%

0.50

% 1.50

% 2.50

% 3.50

% 4.50

% 5.50

% 6.50

% 7.50

% 8.50

% 9.50

%

0

10

20

30

40

50

60

Histogram Fairfax Media

Bin

Frequency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

RISK MANAGEMENT

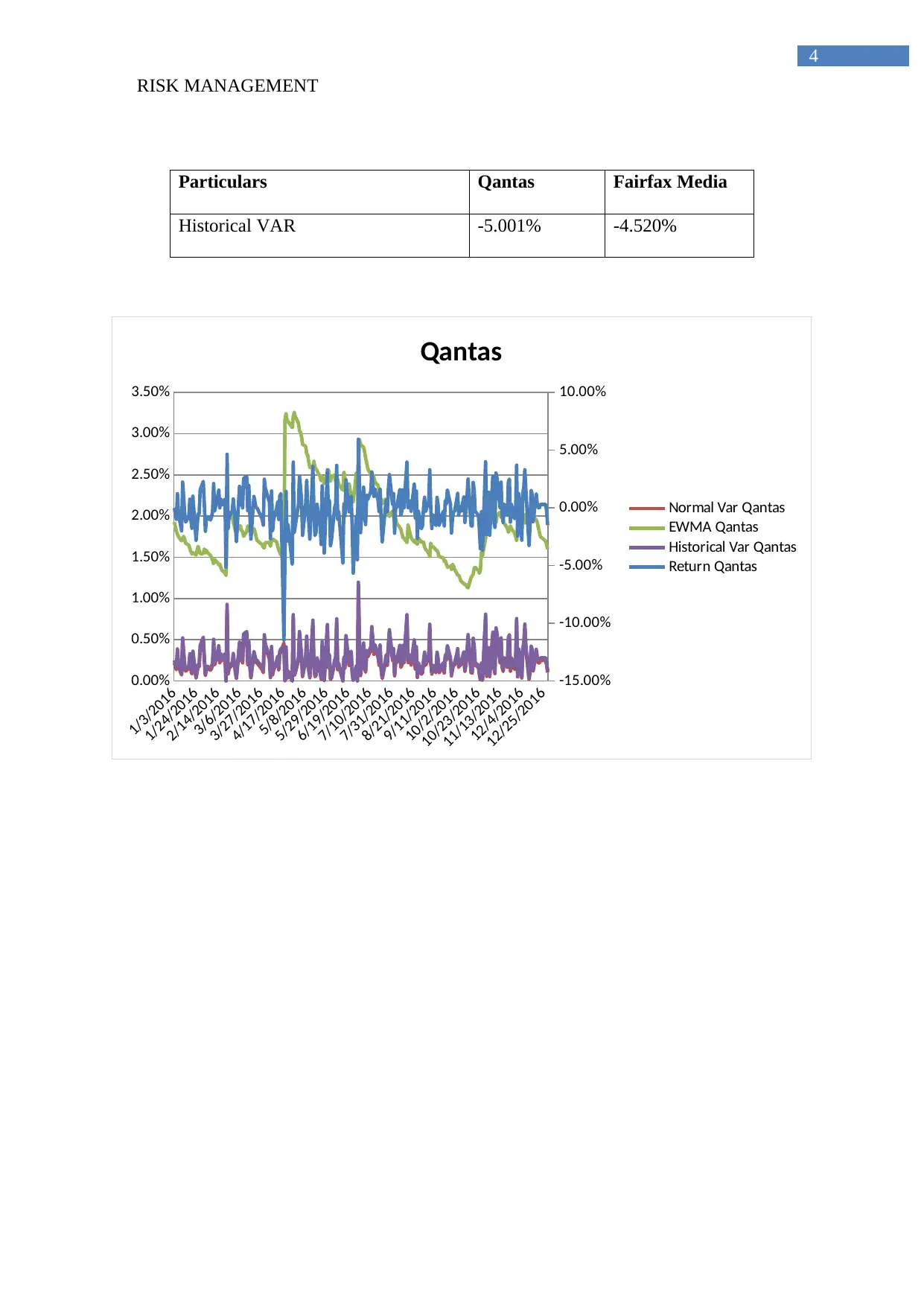

Particulars Qantas Fairfax Media

Historical VAR -5.001% -4.520%

1/3/2016

1/24/2016

2/14/2016

3/6/2016

3/27/2016

4/17/2016

5/8/2016

5/29/2016

6/19/2016

7/10/2016

7/31/2016

8/21/2016

9/11/2016

10/2/2016

10/23/2016

11/13/2016

12/4/2016

12/25/2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

Qantas

Normal Var Qantas

EWMA Qantas

Historical Var Qantas

Return Qantas

RISK MANAGEMENT

Particulars Qantas Fairfax Media

Historical VAR -5.001% -4.520%

1/3/2016

1/24/2016

2/14/2016

3/6/2016

3/27/2016

4/17/2016

5/8/2016

5/29/2016

6/19/2016

7/10/2016

7/31/2016

8/21/2016

9/11/2016

10/2/2016

10/23/2016

11/13/2016

12/4/2016

12/25/2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

Qantas

Normal Var Qantas

EWMA Qantas

Historical Var Qantas

Return Qantas

5

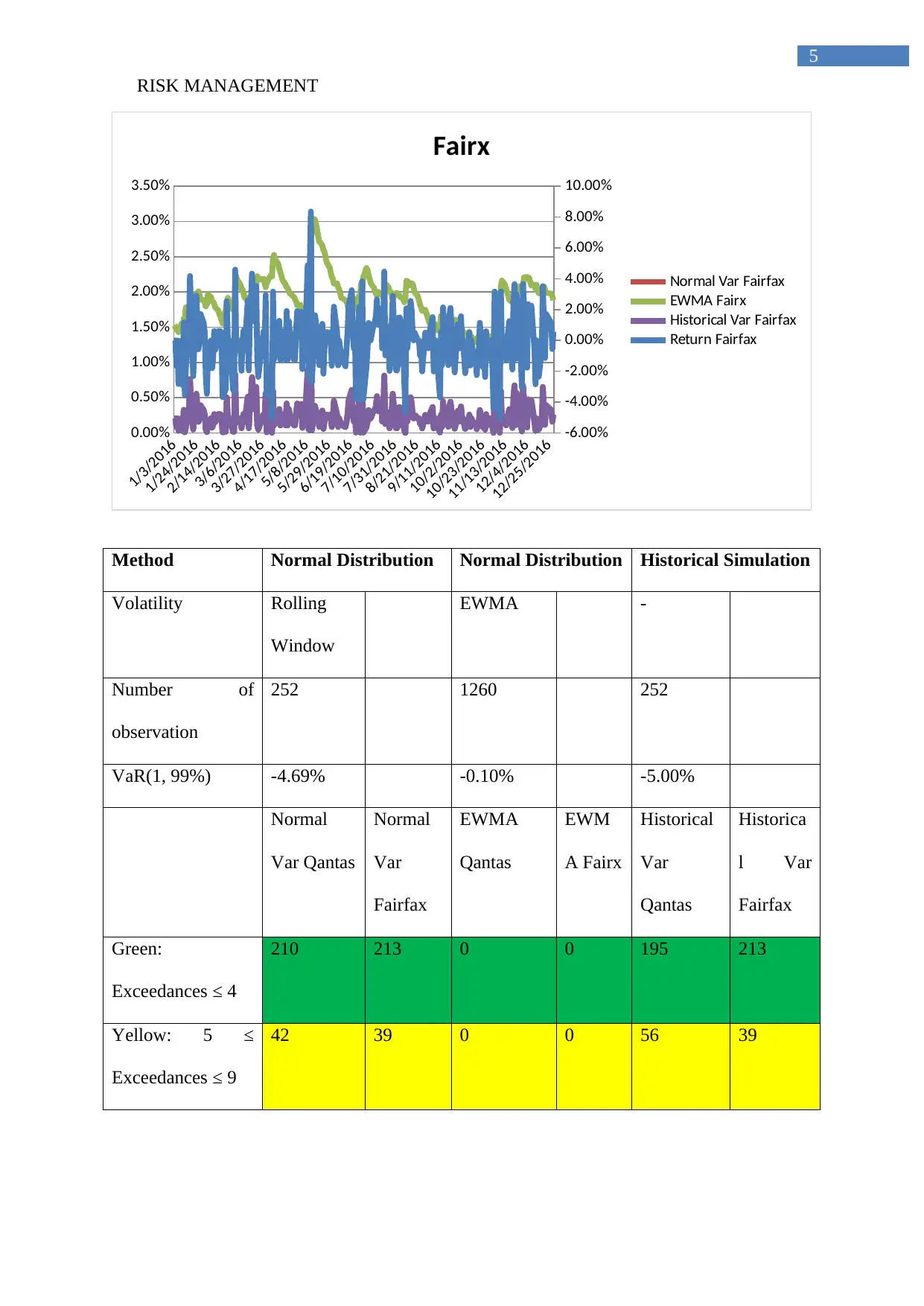

RISK MANAGEMENT

1/3/2016

1/24/2016

2/14/2016

3/6/2016

3/27/2016

4/17/2016

5/8/2016

5/29/2016

6/19/2016

7/10/2016

7/31/2016

8/21/2016

9/11/2016

10/2/2016

10/23/2016

11/13/2016

12/4/2016

12/25/2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Fairx

Normal Var Fairfax

EWMA Fairx

Historical Var Fairfax

Return Fairfax

Method Normal Distribution Normal Distribution Historical Simulation

Volatility Rolling

Window

EWMA -

Number of

observation

252 1260 252

VaR(1, 99%) -4.69% -0.10% -5.00%

Normal

Var Qantas

Normal

Var

Fairfax

EWMA

Qantas

EWM

A Fairx

Historical

Var

Qantas

Historica

l Var

Fairfax

Green:

Exceedances ≤ 4

210 213 0 0 195 213

Yellow: 5 ≤

Exceedances ≤ 9

42 39 0 0 56 39

RISK MANAGEMENT

1/3/2016

1/24/2016

2/14/2016

3/6/2016

3/27/2016

4/17/2016

5/8/2016

5/29/2016

6/19/2016

7/10/2016

7/31/2016

8/21/2016

9/11/2016

10/2/2016

10/23/2016

11/13/2016

12/4/2016

12/25/2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Fairx

Normal Var Fairfax

EWMA Fairx

Historical Var Fairfax

Return Fairfax

Method Normal Distribution Normal Distribution Historical Simulation

Volatility Rolling

Window

EWMA -

Number of

observation

252 1260 252

VaR(1, 99%) -4.69% -0.10% -5.00%

Normal

Var Qantas

Normal

Var

Fairfax

EWMA

Qantas

EWM

A Fairx

Historical

Var

Qantas

Historica

l Var

Fairfax

Green:

Exceedances ≤ 4

210 213 0 0 195 213

Yellow: 5 ≤

Exceedances ≤ 9

42 39 0 0 56 39

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

RISK MANAGEMENT

Red: 10 ≥

Exceedances

1 1 253 253 2 1

The above table mainly depicts the relevant Basel traffic lights, which could help in

identifying the most adequate technique that could be used in discovering adequate VAR.

From the overall evaluation, historical simulation is mainly depicted as the most viable

approach, which could be used in detecting the overall VAR calculation.

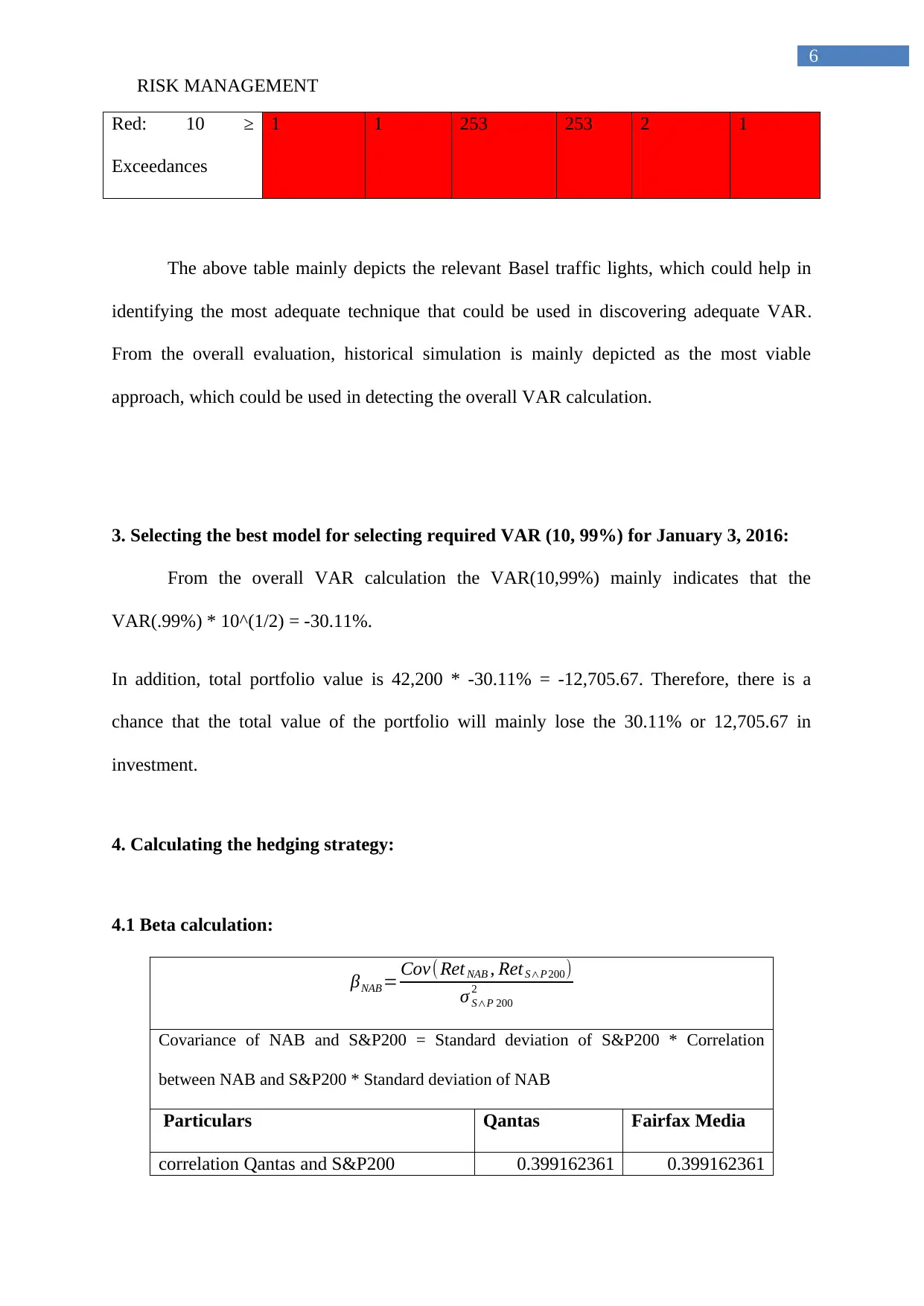

3. Selecting the best model for selecting required VAR (10, 99%) for January 3, 2016:

From the overall VAR calculation the VAR(10,99%) mainly indicates that the

VAR(.99%) * 10^(1/2) = -30.11%.

In addition, total portfolio value is 42,200 * -30.11% = -12,705.67. Therefore, there is a

chance that the total value of the portfolio will mainly lose the 30.11% or 12,705.67 in

investment.

4. Calculating the hedging strategy:

4.1 Beta calculation:

βNAB= Cov(Ret NAB , Ret S∧P 200)

σ S∧P 200

2

Covariance of NAB and S&P200 = Standard deviation of S&P200 * Correlation

between NAB and S&P200 * Standard deviation of NAB

Particulars Qantas Fairfax Media

correlation Qantas and S&P200 0.399162361 0.399162361

RISK MANAGEMENT

Red: 10 ≥

Exceedances

1 1 253 253 2 1

The above table mainly depicts the relevant Basel traffic lights, which could help in

identifying the most adequate technique that could be used in discovering adequate VAR.

From the overall evaluation, historical simulation is mainly depicted as the most viable

approach, which could be used in detecting the overall VAR calculation.

3. Selecting the best model for selecting required VAR (10, 99%) for January 3, 2016:

From the overall VAR calculation the VAR(10,99%) mainly indicates that the

VAR(.99%) * 10^(1/2) = -30.11%.

In addition, total portfolio value is 42,200 * -30.11% = -12,705.67. Therefore, there is a

chance that the total value of the portfolio will mainly lose the 30.11% or 12,705.67 in

investment.

4. Calculating the hedging strategy:

4.1 Beta calculation:

βNAB= Cov(Ret NAB , Ret S∧P 200)

σ S∧P 200

2

Covariance of NAB and S&P200 = Standard deviation of S&P200 * Correlation

between NAB and S&P200 * Standard deviation of NAB

Particulars Qantas Fairfax Media

correlation Qantas and S&P200 0.399162361 0.399162361

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RISK MANAGEMENT

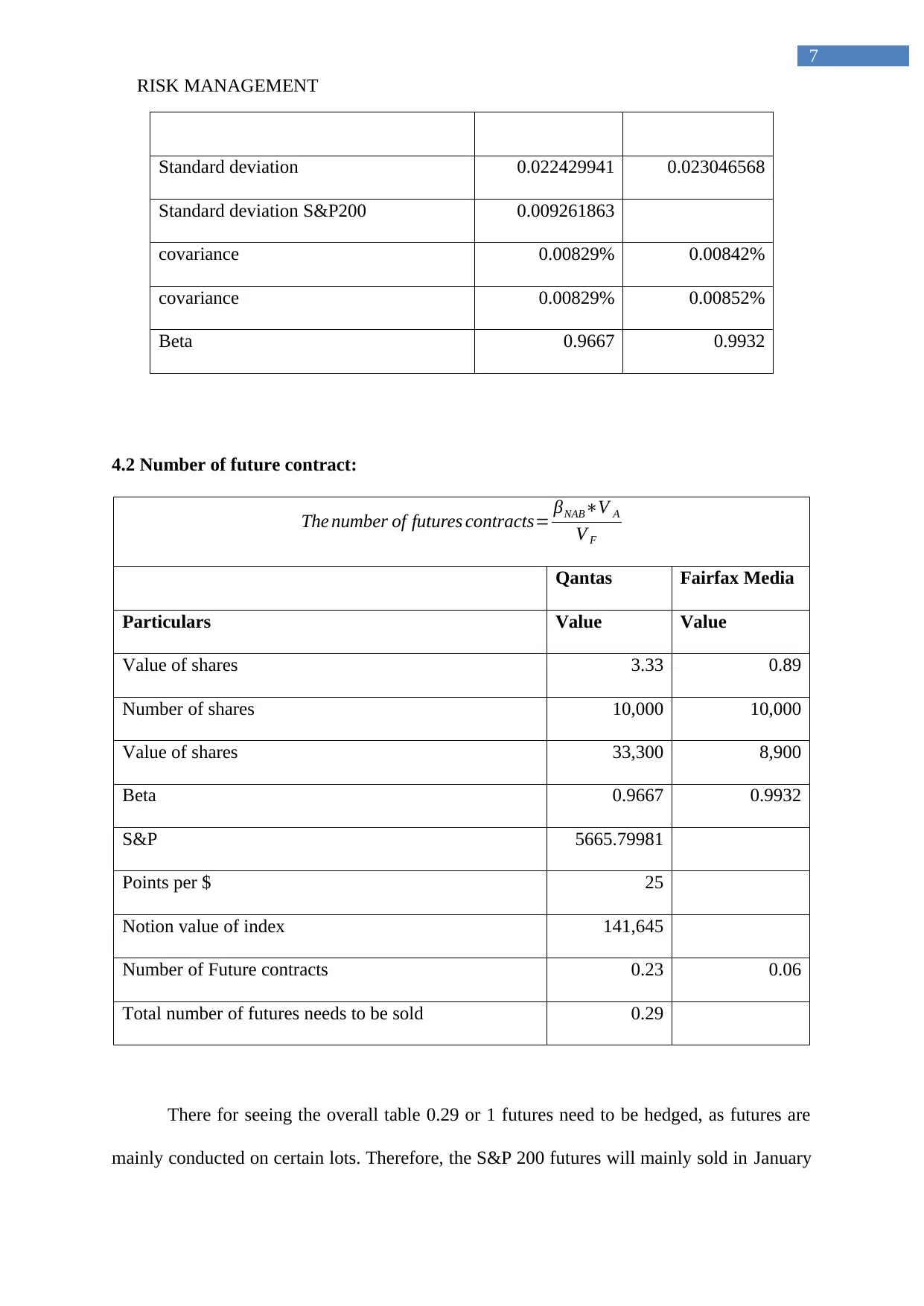

Standard deviation 0.022429941 0.023046568

Standard deviation S&P200 0.009261863

covariance 0.00829% 0.00842%

covariance 0.00829% 0.00852%

Beta 0.9667 0.9932

4.2 Number of future contract:

The number of futures contracts= βNAB∗V A

V F

Qantas Fairfax Media

Particulars Value Value

Value of shares 3.33 0.89

Number of shares 10,000 10,000

Value of shares 33,300 8,900

Beta 0.9667 0.9932

S&P 5665.79981

Points per $ 25

Notion value of index 141,645

Number of Future contracts 0.23 0.06

Total number of futures needs to be sold 0.29

There for seeing the overall table 0.29 or 1 futures need to be hedged, as futures are

mainly conducted on certain lots. Therefore, the S&P 200 futures will mainly sold in January

RISK MANAGEMENT

Standard deviation 0.022429941 0.023046568

Standard deviation S&P200 0.009261863

covariance 0.00829% 0.00842%

covariance 0.00829% 0.00852%

Beta 0.9667 0.9932

4.2 Number of future contract:

The number of futures contracts= βNAB∗V A

V F

Qantas Fairfax Media

Particulars Value Value

Value of shares 3.33 0.89

Number of shares 10,000 10,000

Value of shares 33,300 8,900

Beta 0.9667 0.9932

S&P 5665.79981

Points per $ 25

Notion value of index 141,645

Number of Future contracts 0.23 0.06

Total number of futures needs to be sold 0.29

There for seeing the overall table 0.29 or 1 futures need to be hedged, as futures are

mainly conducted on certain lots. Therefore, the S&P 200 futures will mainly sold in January

8

RISK MANAGEMENT

3, 2017 and then bought in January 16, 2017. This time horizon will mainly help in depicting

the relevant profits and reduction in risk that might be conducted with the hedge.

Particulars Value Value

Shorting 0.29

Selling 1 contract at January 3, 2017 5736.3999 143,410.00

Buying 1 contract at January 16, 2017 5699.3999 142,485.00

Cost of holding 42,200

Profit on futures 925.00

Net cost of NAB shares with futures contracts 41,275.00

Therefore, after using short hedge the overall profits attained from investment is

mainly at 925. In addition, the overall use of hedge has mainly helped in reducing the

systematic risk that might affect the overall value of portfolio.

4.3 VAR of the portfolio:

Particulars Value

Expected return of the portfolio 0.0103%

Expected return of Qantas 0.0148%

Expected return of Fairfax -0.0297%

Expected return of the index 0.0117%

Covariance of Oantas and Fairfax 0.0065%

Covariance of Oantas and S&P 500 0.0002%

Covariance of Fairfax and S&P 500 0.0002%

Normal quantile at 99% confidence level 2.3263

RISK MANAGEMENT

3, 2017 and then bought in January 16, 2017. This time horizon will mainly help in depicting

the relevant profits and reduction in risk that might be conducted with the hedge.

Particulars Value Value

Shorting 0.29

Selling 1 contract at January 3, 2017 5736.3999 143,410.00

Buying 1 contract at January 16, 2017 5699.3999 142,485.00

Cost of holding 42,200

Profit on futures 925.00

Net cost of NAB shares with futures contracts 41,275.00

Therefore, after using short hedge the overall profits attained from investment is

mainly at 925. In addition, the overall use of hedge has mainly helped in reducing the

systematic risk that might affect the overall value of portfolio.

4.3 VAR of the portfolio:

Particulars Value

Expected return of the portfolio 0.0103%

Expected return of Qantas 0.0148%

Expected return of Fairfax -0.0297%

Expected return of the index 0.0117%

Covariance of Oantas and Fairfax 0.0065%

Covariance of Oantas and S&P 500 0.0002%

Covariance of Fairfax and S&P 500 0.0002%

Normal quantile at 99% confidence level 2.3263

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

RISK MANAGEMENT

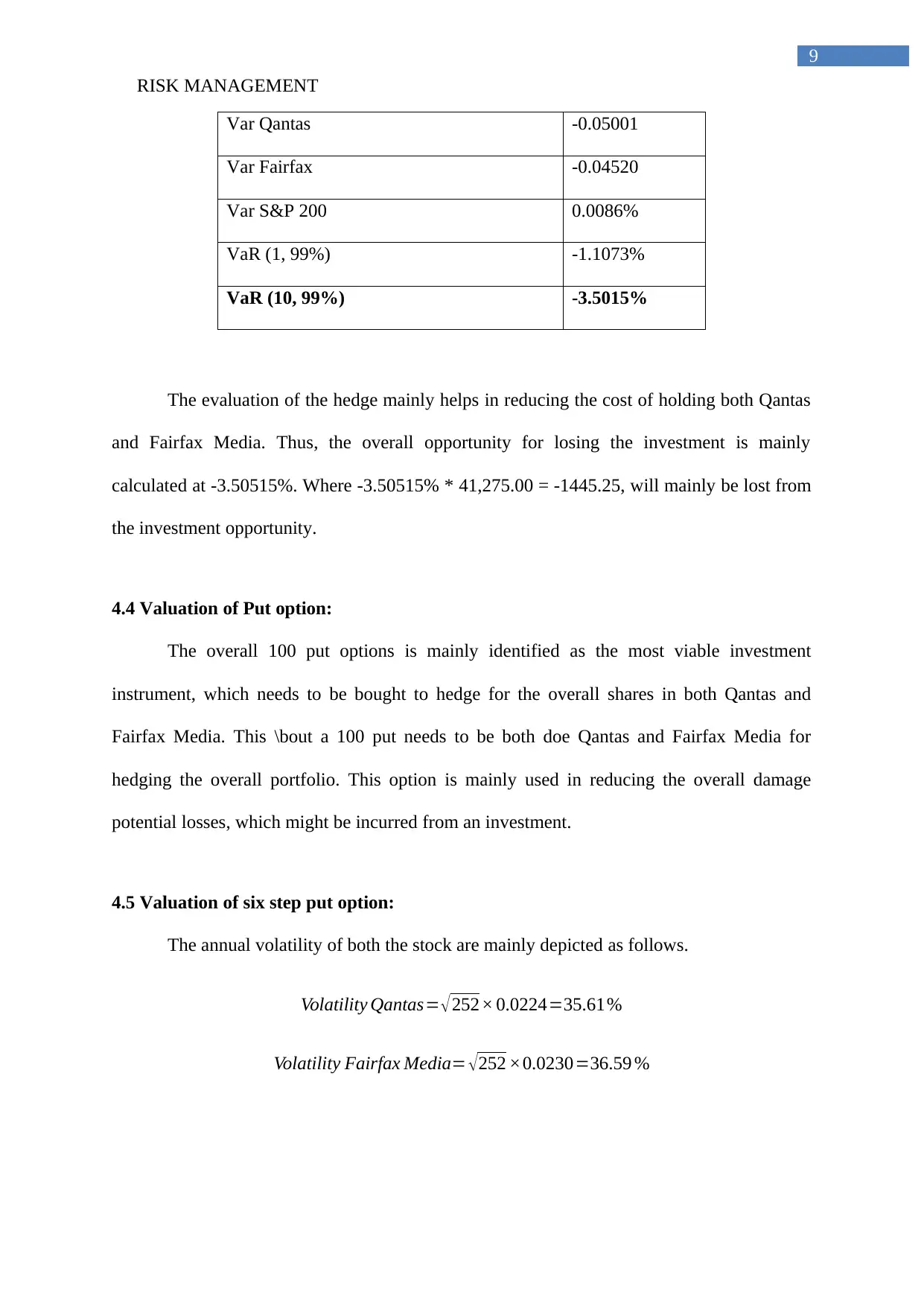

Var Qantas -0.05001

Var Fairfax -0.04520

Var S&P 200 0.0086%

VaR (1, 99%) -1.1073%

VaR (10, 99%) -3.5015%

The evaluation of the hedge mainly helps in reducing the cost of holding both Qantas

and Fairfax Media. Thus, the overall opportunity for losing the investment is mainly

calculated at -3.50515%. Where -3.50515% * 41,275.00 = -1445.25, will mainly be lost from

the investment opportunity.

4.4 Valuation of Put option:

The overall 100 put options is mainly identified as the most viable investment

instrument, which needs to be bought to hedge for the overall shares in both Qantas and

Fairfax Media. This \bout a 100 put needs to be both doe Qantas and Fairfax Media for

hedging the overall portfolio. This option is mainly used in reducing the overall damage

potential losses, which might be incurred from an investment.

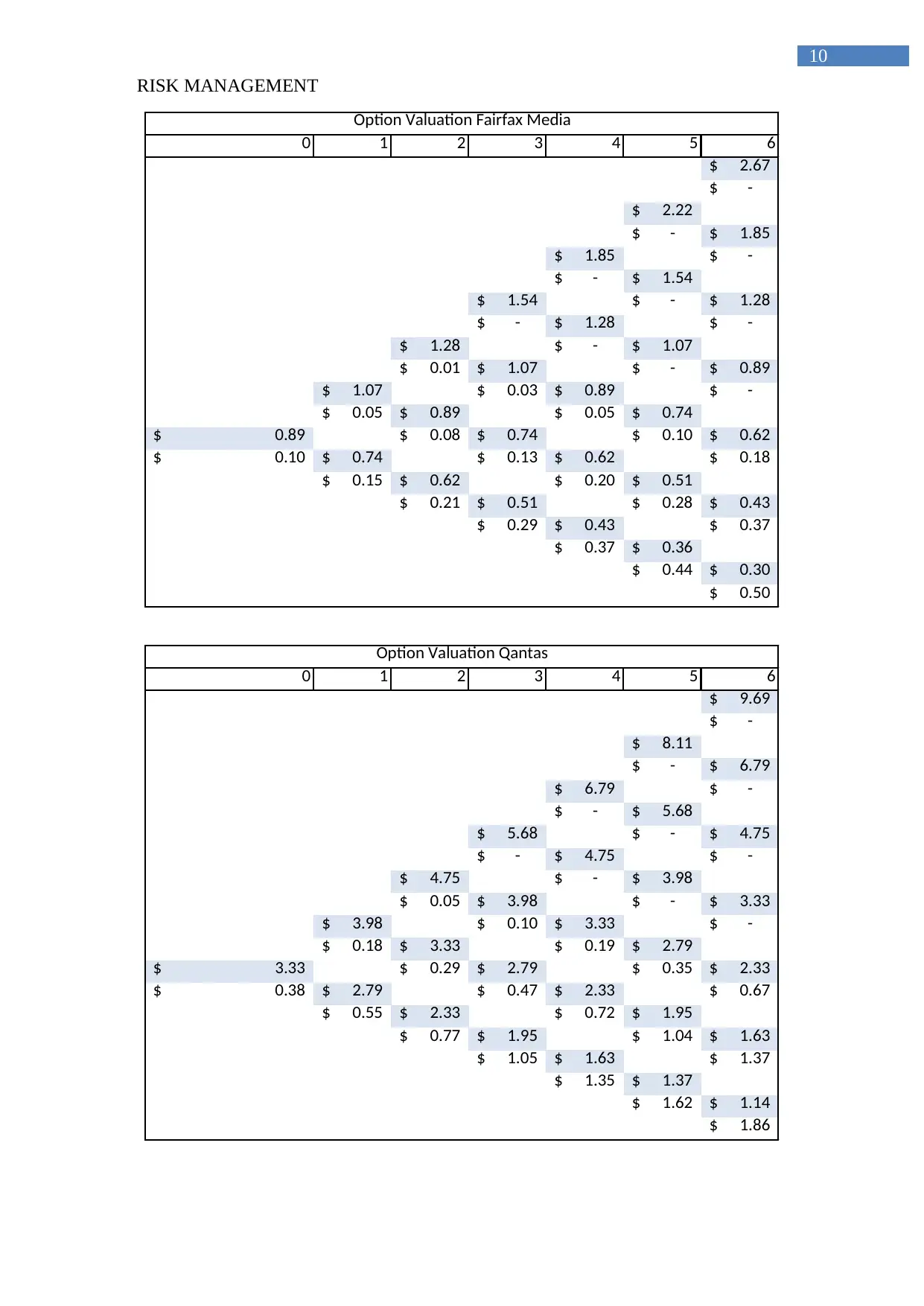

4.5 Valuation of six step put option:

The annual volatility of both the stock are mainly depicted as follows.

Volatility Qantas= √252× 0.0224=35.61%

Volatility Fairfax Media= √252 ×0.0230=36.59 %

RISK MANAGEMENT

Var Qantas -0.05001

Var Fairfax -0.04520

Var S&P 200 0.0086%

VaR (1, 99%) -1.1073%

VaR (10, 99%) -3.5015%

The evaluation of the hedge mainly helps in reducing the cost of holding both Qantas

and Fairfax Media. Thus, the overall opportunity for losing the investment is mainly

calculated at -3.50515%. Where -3.50515% * 41,275.00 = -1445.25, will mainly be lost from

the investment opportunity.

4.4 Valuation of Put option:

The overall 100 put options is mainly identified as the most viable investment

instrument, which needs to be bought to hedge for the overall shares in both Qantas and

Fairfax Media. This \bout a 100 put needs to be both doe Qantas and Fairfax Media for

hedging the overall portfolio. This option is mainly used in reducing the overall damage

potential losses, which might be incurred from an investment.

4.5 Valuation of six step put option:

The annual volatility of both the stock are mainly depicted as follows.

Volatility Qantas= √252× 0.0224=35.61%

Volatility Fairfax Media= √252 ×0.0230=36.59 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

RISK MANAGEMENT

0 1 2 3 4 5 6

2.67$

-$

2.22$

-$ 1.85$

1.85$ -$

-$ 1.54$

1.54$ -$ 1.28$

-$ 1.28$ -$

1.28$ -$ 1.07$

0.01$ 1.07$ -$ 0.89$

1.07$ 0.03$ 0.89$ -$

0.05$ 0.89$ 0.05$ 0.74$

0.89$ 0.08$ 0.74$ 0.10$ 0.62$

0.10$ 0.74$ 0.13$ 0.62$ 0.18$

0.15$ 0.62$ 0.20$ 0.51$

0.21$ 0.51$ 0.28$ 0.43$

0.29$ 0.43$ 0.37$

0.37$ 0.36$

0.44$ 0.30$

0.50$

Option Valuation Fairfax Media

0 1 2 3 4 5 6

9.69$

-$

8.11$

-$ 6.79$

6.79$ -$

-$ 5.68$

5.68$ -$ 4.75$

-$ 4.75$ -$

4.75$ -$ 3.98$

0.05$ 3.98$ -$ 3.33$

3.98$ 0.10$ 3.33$ -$

0.18$ 3.33$ 0.19$ 2.79$

3.33$ 0.29$ 2.79$ 0.35$ 2.33$

0.38$ 2.79$ 0.47$ 2.33$ 0.67$

0.55$ 2.33$ 0.72$ 1.95$

0.77$ 1.95$ 1.04$ 1.63$

1.05$ 1.63$ 1.37$

1.35$ 1.37$

1.62$ 1.14$

1.86$

Option Valuation Qantas

RISK MANAGEMENT

0 1 2 3 4 5 6

2.67$

-$

2.22$

-$ 1.85$

1.85$ -$

-$ 1.54$

1.54$ -$ 1.28$

-$ 1.28$ -$

1.28$ -$ 1.07$

0.01$ 1.07$ -$ 0.89$

1.07$ 0.03$ 0.89$ -$

0.05$ 0.89$ 0.05$ 0.74$

0.89$ 0.08$ 0.74$ 0.10$ 0.62$

0.10$ 0.74$ 0.13$ 0.62$ 0.18$

0.15$ 0.62$ 0.20$ 0.51$

0.21$ 0.51$ 0.28$ 0.43$

0.29$ 0.43$ 0.37$

0.37$ 0.36$

0.44$ 0.30$

0.50$

Option Valuation Fairfax Media

0 1 2 3 4 5 6

9.69$

-$

8.11$

-$ 6.79$

6.79$ -$

-$ 5.68$

5.68$ -$ 4.75$

-$ 4.75$ -$

4.75$ -$ 3.98$

0.05$ 3.98$ -$ 3.33$

3.98$ 0.10$ 3.33$ -$

0.18$ 3.33$ 0.19$ 2.79$

3.33$ 0.29$ 2.79$ 0.35$ 2.33$

0.38$ 2.79$ 0.47$ 2.33$ 0.67$

0.55$ 2.33$ 0.72$ 1.95$

0.77$ 1.95$ 1.04$ 1.63$

1.05$ 1.63$ 1.37$

1.35$ 1.37$

1.62$ 1.14$

1.86$

Option Valuation Qantas

11

RISK MANAGEMENT

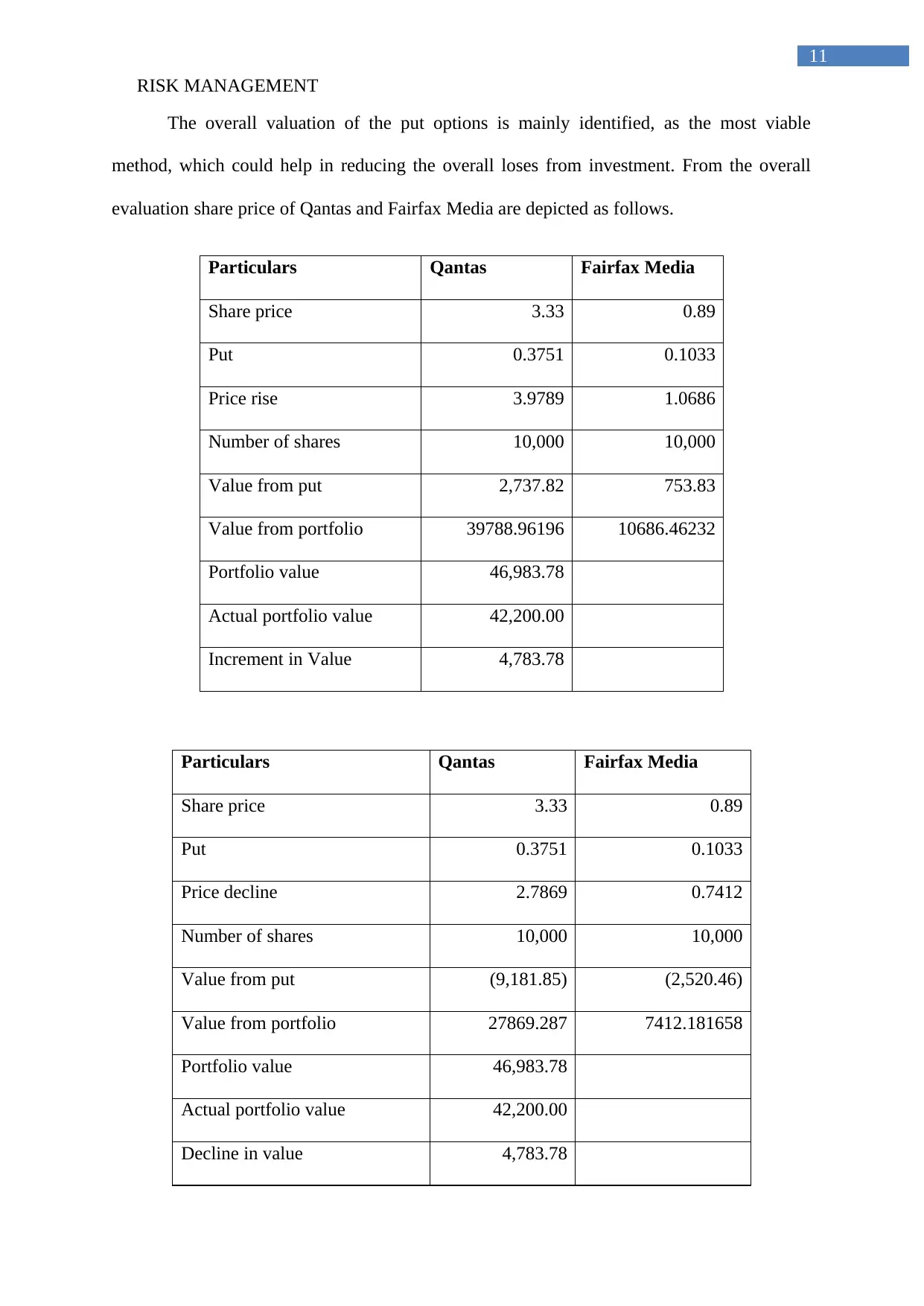

The overall valuation of the put options is mainly identified, as the most viable

method, which could help in reducing the overall loses from investment. From the overall

evaluation share price of Qantas and Fairfax Media are depicted as follows.

Particulars Qantas Fairfax Media

Share price 3.33 0.89

Put 0.3751 0.1033

Price rise 3.9789 1.0686

Number of shares 10,000 10,000

Value from put 2,737.82 753.83

Value from portfolio 39788.96196 10686.46232

Portfolio value 46,983.78

Actual portfolio value 42,200.00

Increment in Value 4,783.78

Particulars Qantas Fairfax Media

Share price 3.33 0.89

Put 0.3751 0.1033

Price decline 2.7869 0.7412

Number of shares 10,000 10,000

Value from put (9,181.85) (2,520.46)

Value from portfolio 27869.287 7412.181658

Portfolio value 46,983.78

Actual portfolio value 42,200.00

Decline in value 4,783.78

RISK MANAGEMENT

The overall valuation of the put options is mainly identified, as the most viable

method, which could help in reducing the overall loses from investment. From the overall

evaluation share price of Qantas and Fairfax Media are depicted as follows.

Particulars Qantas Fairfax Media

Share price 3.33 0.89

Put 0.3751 0.1033

Price rise 3.9789 1.0686

Number of shares 10,000 10,000

Value from put 2,737.82 753.83

Value from portfolio 39788.96196 10686.46232

Portfolio value 46,983.78

Actual portfolio value 42,200.00

Increment in Value 4,783.78

Particulars Qantas Fairfax Media

Share price 3.33 0.89

Put 0.3751 0.1033

Price decline 2.7869 0.7412

Number of shares 10,000 10,000

Value from put (9,181.85) (2,520.46)

Value from portfolio 27869.287 7412.181658

Portfolio value 46,983.78

Actual portfolio value 42,200.00

Decline in value 4,783.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.