Analysis of Expansionary Monetary Policy on Australian Economy: Report

VerifiedAdded on 2020/04/07

|10

|2013

|40

Report

AI Summary

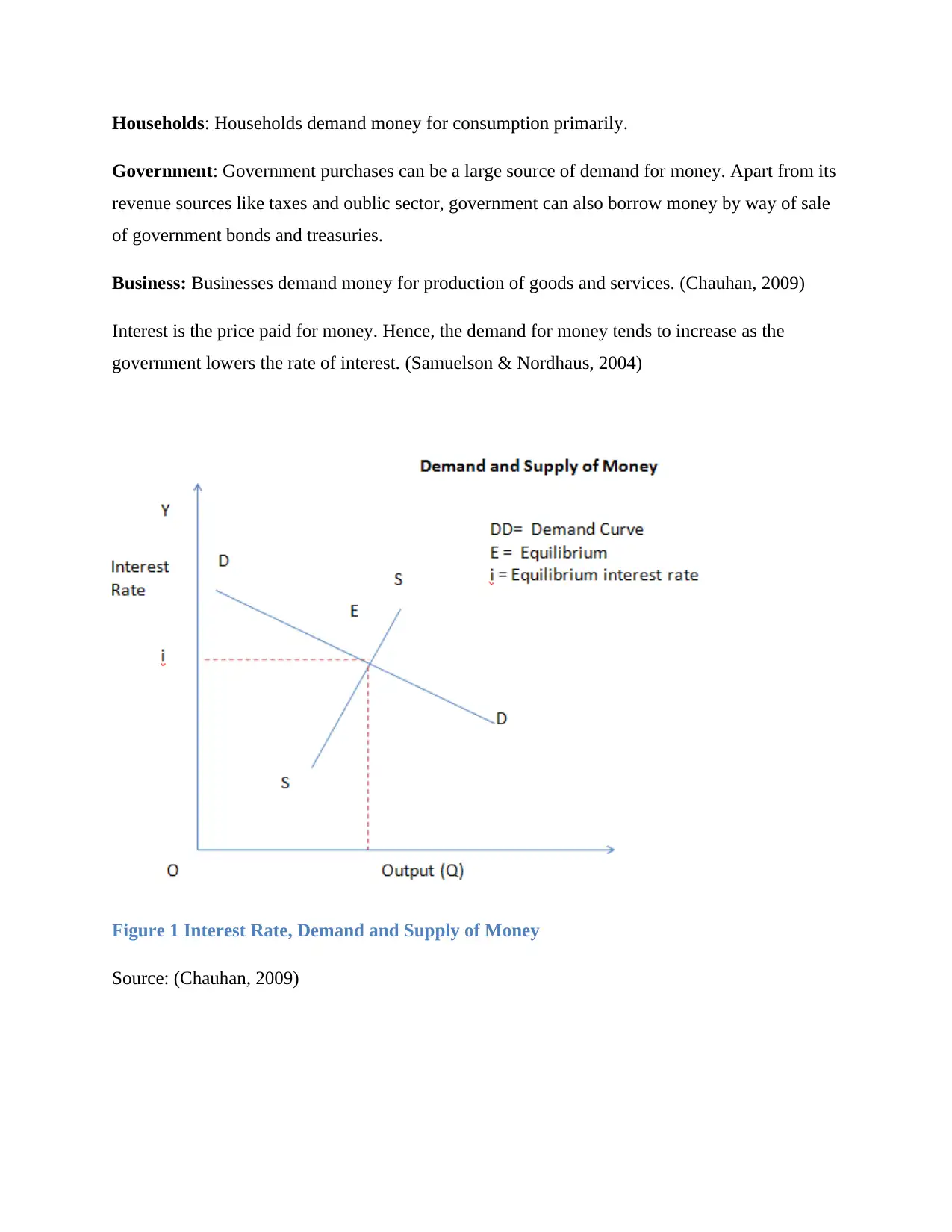

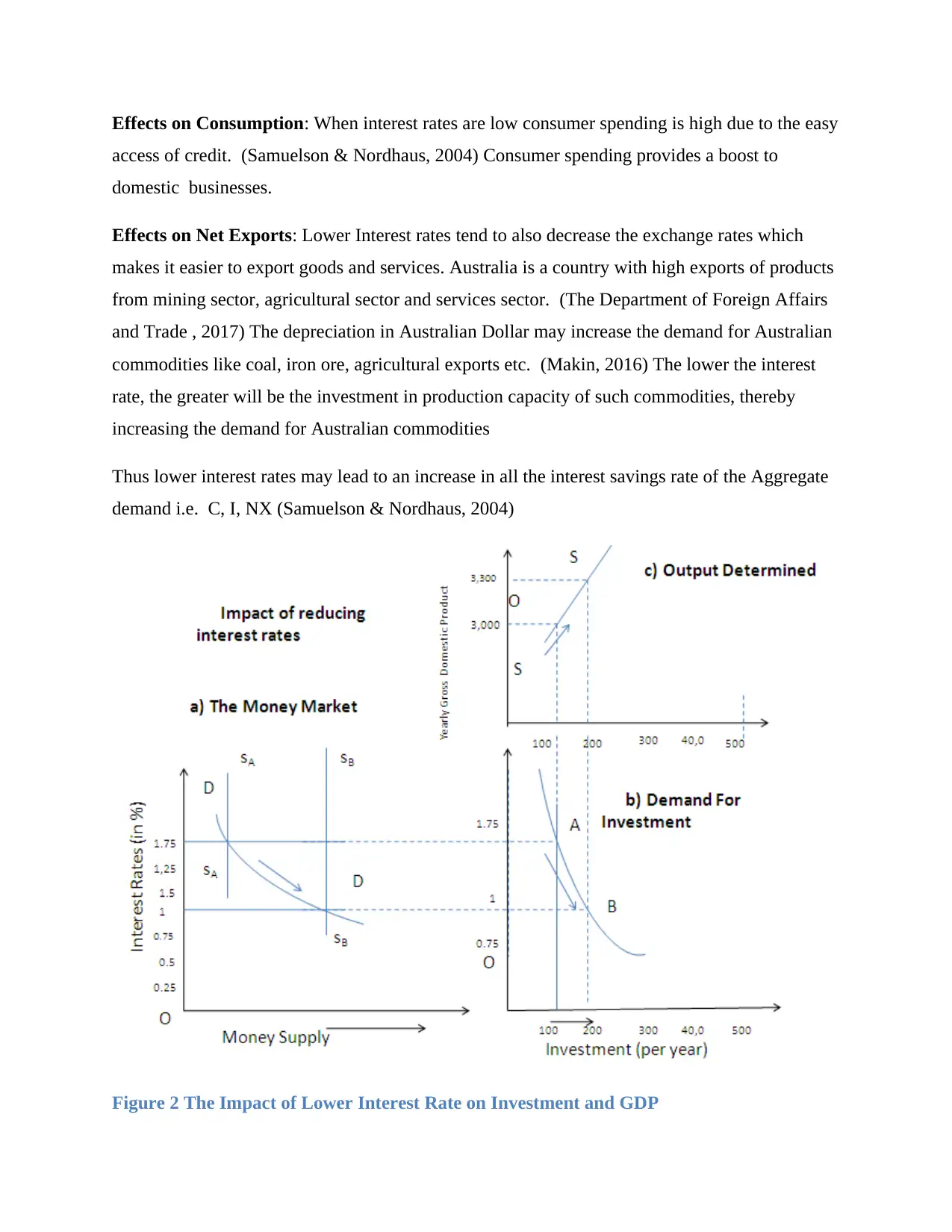

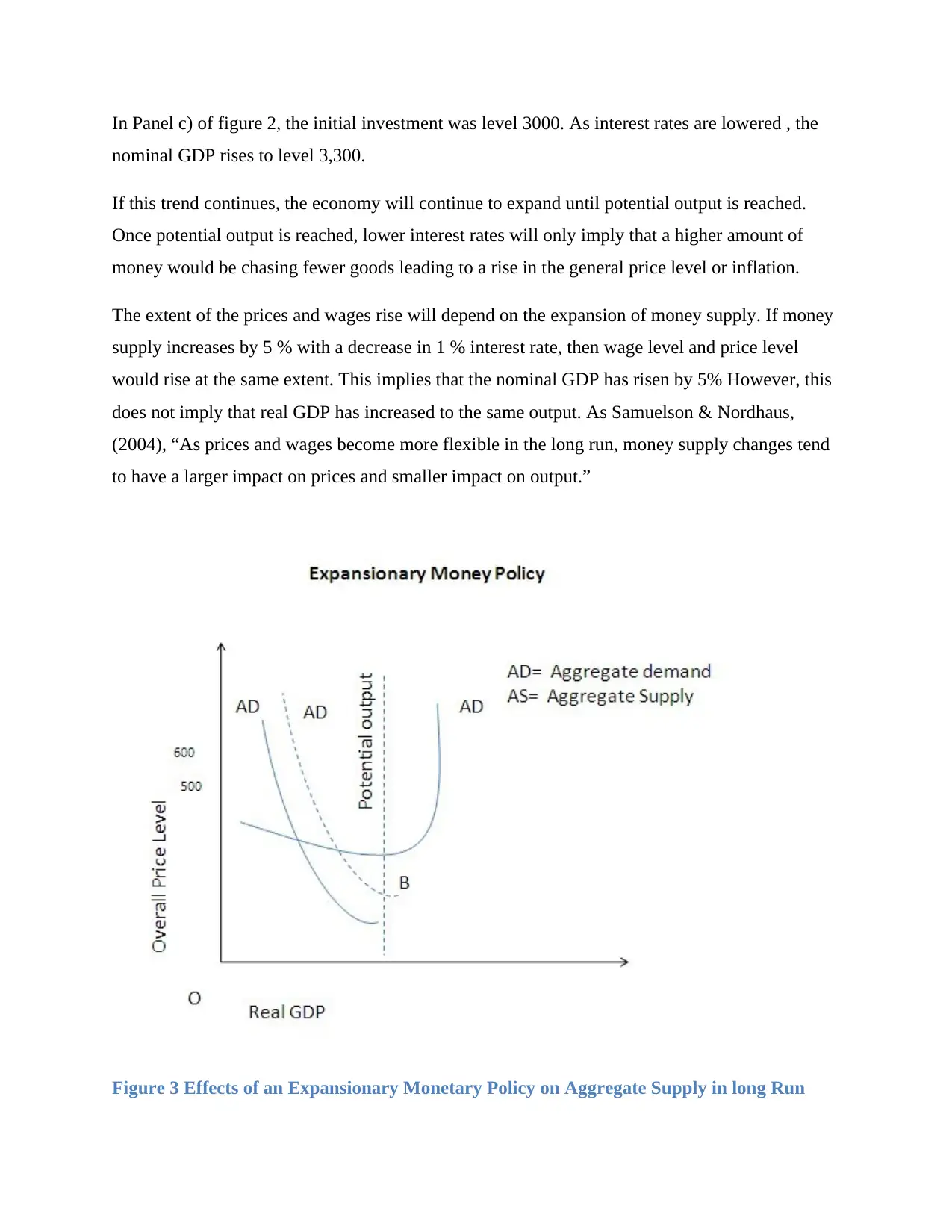

This report analyzes the effects of expansionary monetary policy on the Australian economy, focusing on the impact of reduced cash rates on GDP, price levels, and wages. The analysis begins by examining the demand and supply of money, considering factors such as household savings, government purchases, and business investments. The report then explores how lower interest rates influence aggregate demand through consumption, investment, government purchases, and net exports. It further investigates the short-run effects on GDP, including impacts on business investment, housing, and consumer spending. The study also delves into the multiplier effects of low-interest rates, leading to rises in wages and price levels. It concludes by discussing the potential consequences of expansionary monetary policy, including the possibility of increased asset prices, referencing key economic theories and empirical data to support its findings. The report highlights the Reserve Bank of Australia's role in managing monetary policy and its effects on various sectors of the economy.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.