EIN 6357 - Advanced Engineering Economy: Homework Assignment Solution

VerifiedAdded on 2023/01/19

|8

|1792

|61

Homework Assignment

AI Summary

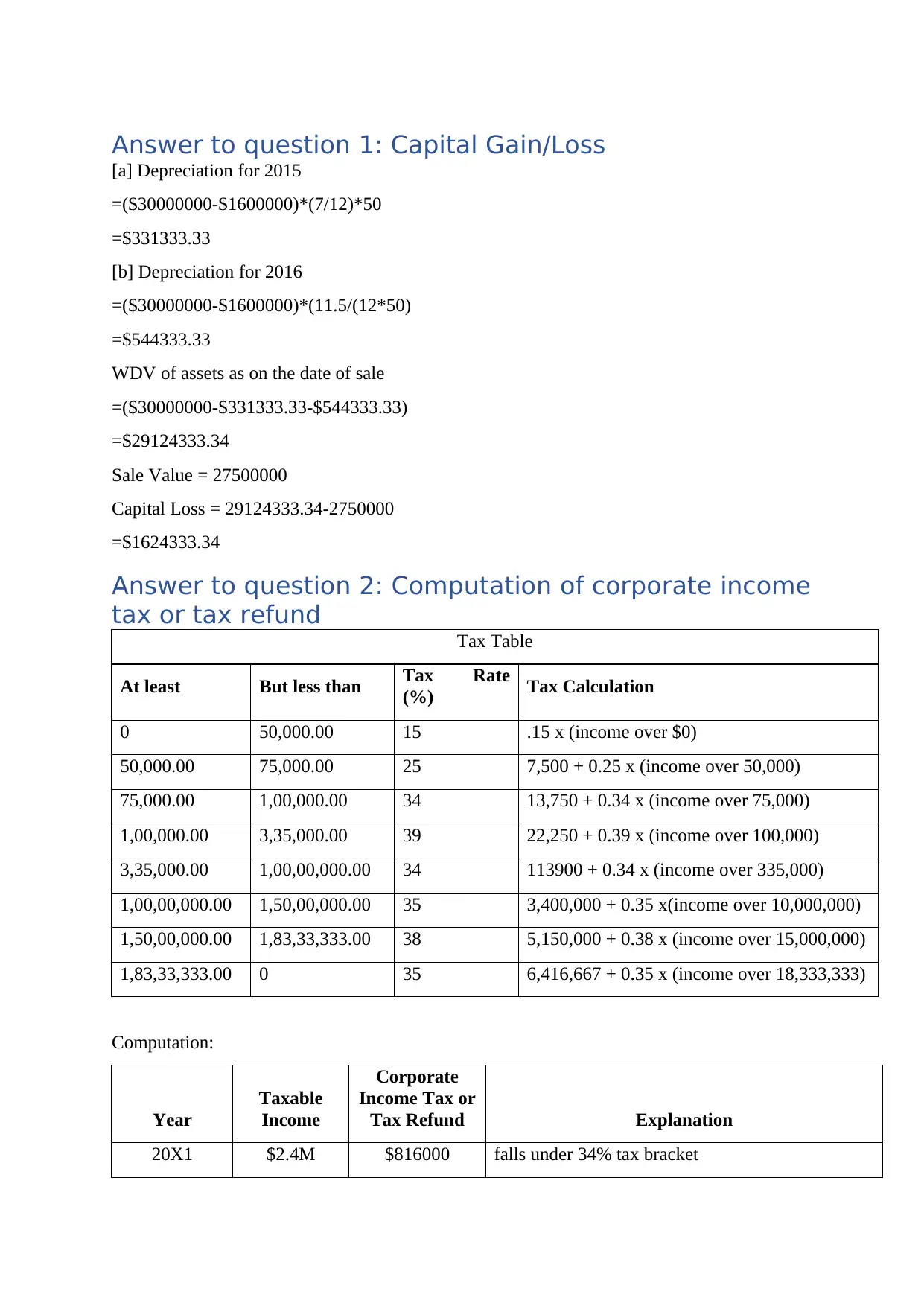

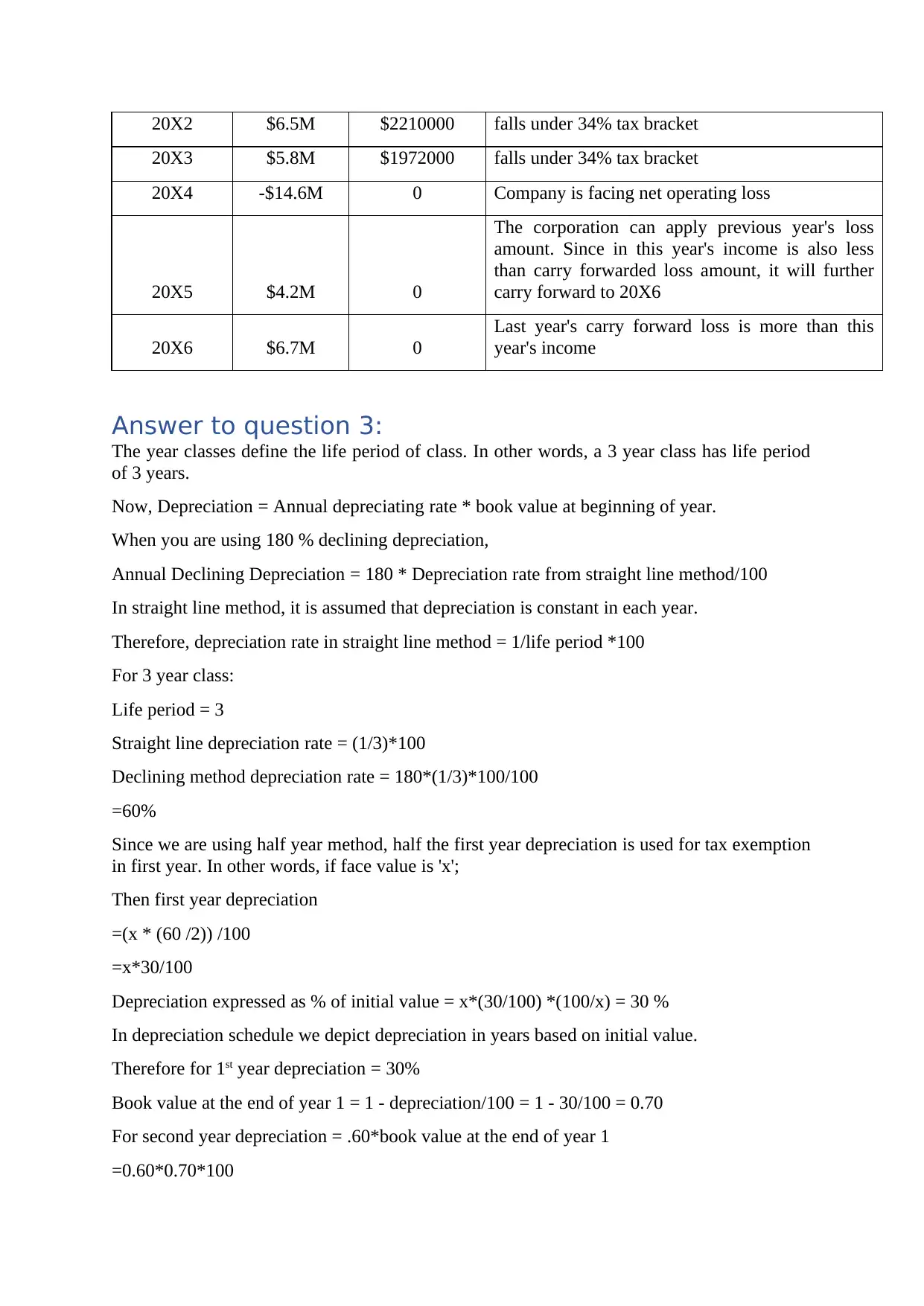

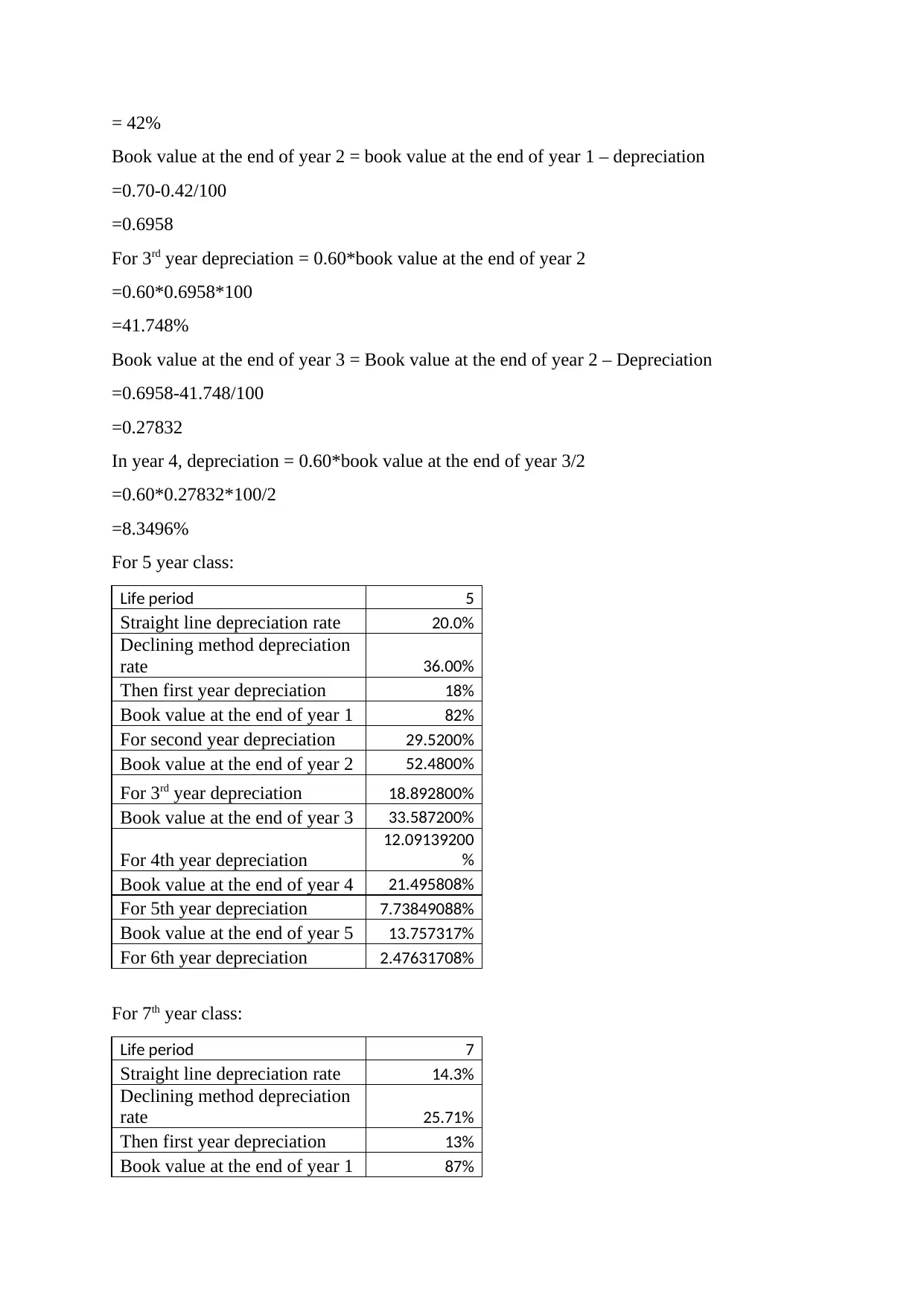

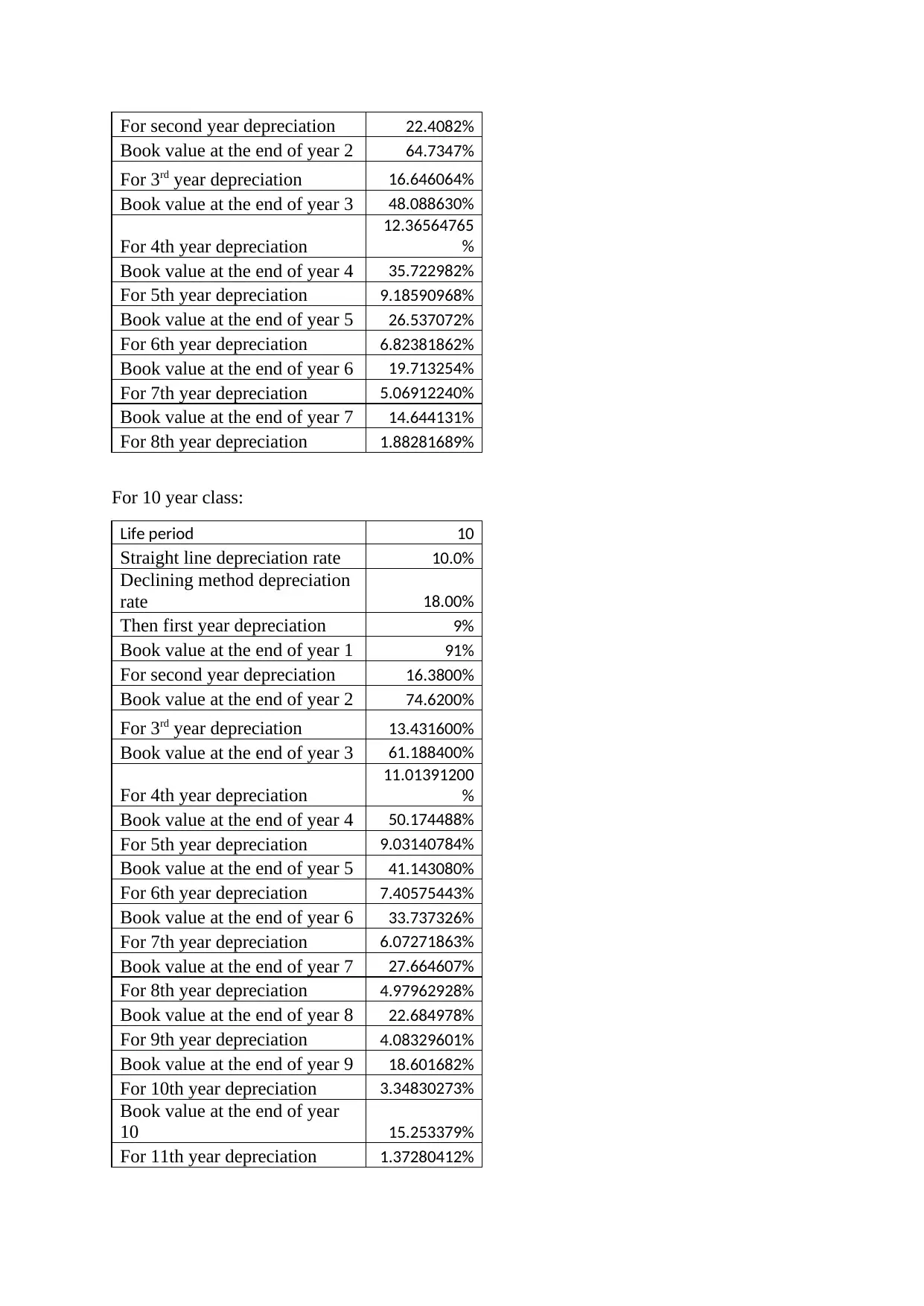

This document presents a comprehensive solution to an EIN 6357 Advanced Engineering Economy assignment. The solution addresses multiple questions, beginning with calculations of depreciation and capital gains/losses for a warehouse, considering half-month conventions. It then delves into corporate income tax calculations for a company over several years, utilizing graduated tax rates. The assignment further explores depreciation methods, including the 200% declining balance method for various asset classes, and demonstrates the calculation of depreciation rates and book values. Additional problems cover bond yield calculations, including nominal and effective annual yields, and the determination of monthly payments and principal paid on a loan. Finally, the solution analyzes stock performance, including the calculation of dividend growth rate, beta, and the application of the Capital Asset Pricing Model (CAPM) to determine expected returns and dividend yield. This assignment provides a detailed understanding of financial concepts and calculations relevant to engineering economy.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.