Financial Accounting and Reporting: Analysis and Reporting for EL Ltd

VerifiedAdded on 2020/02/03

|21

|5486

|59

Report

AI Summary

This report provides a comprehensive analysis of financial accounting and reporting practices for EL Ltd, a domestic electrical services provider. The report begins by identifying various users of financial information, such as managers, employees, suppliers, the government, and customers, along with their respective needs. It then explores the legal and regulatory influences on financial statements, including the role of the Financial Reporting Council (FRC) and relevant legislation like the Companies Act 2006. The report assesses the implications of these regulations for stakeholders and how accounting standards address different laws. Furthermore, it includes the preparation of financial statements, starting with an unadjusted trial balance and progressing to adjusted trial balances, income statements, and balance sheets. The report also covers the preparation of financial statements from incomplete records and the calculation and interpretation of accounting ratios. The report concludes by summarizing the information needs of different user groups and provides a detailed financial analysis of EL Ltd's performance, incorporating key accounting principles and practices.

Financial Accounting and

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

1.1Different users of financial information and their needs.......................................................4

1.2 Legal and regulatory influences on financial statements......................................................5

1.3 Assess the implications for the users....................................................................................6

1.4 How different laws/ regulations are dealt with by accounting and reporting standards.......6

TASK 2............................................................................................................................................7

2.1 Prepare financial statements for a variety of business with trail balance..............................7

2.2 Prepare financial statements from incomplete records.......................................................10

2.3 Prepare a consolidated balance sheet and profit and loss statement ..................................11

TASK 3..........................................................................................................................................12

3.1 Summarize the information needs of different user groups ...............................................12

3.2 Prepare financial statements by sole trader, partnership and limited company..................13

TASK 4..........................................................................................................................................13

4.1 Calculate accounting ratios.................................................................................................13

4.2 Report incorporating and interpreting accounting ratios....................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

1.1Different users of financial information and their needs.......................................................4

1.2 Legal and regulatory influences on financial statements......................................................5

1.3 Assess the implications for the users....................................................................................6

1.4 How different laws/ regulations are dealt with by accounting and reporting standards.......6

TASK 2............................................................................................................................................7

2.1 Prepare financial statements for a variety of business with trail balance..............................7

2.2 Prepare financial statements from incomplete records.......................................................10

2.3 Prepare a consolidated balance sheet and profit and loss statement ..................................11

TASK 3..........................................................................................................................................12

3.1 Summarize the information needs of different user groups ...............................................12

3.2 Prepare financial statements by sole trader, partnership and limited company..................13

TASK 4..........................................................................................................................................13

4.1 Calculate accounting ratios.................................................................................................13

4.2 Report incorporating and interpreting accounting ratios....................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting and reporting consists of summarizing, analysis and reporting

financial transactions related to a business. It is mandatory for an organisation to prepare

financial statements that depict true and fair picture of the business. There are many stakeholders

which are associated with a business such as suppliers, shareholders, banks, employees,

government etc (Anderson and et.al., 2015). They have interest in the company and they need the

information for decision making. There are certain domestic and international accounting

standards which provides framework and guidelines for all the companies in UK (Ingram,

LaForge and Williams, 2012). The present report is based on EL Ltd which has been in the

business for more than 10 years. They provide domestic electrical services to homes and

business units in the country. There are some laws and regulation which affect the accounting

and reporting standards. Furthermore, it is essential for the company to understand the formats of

financial statements. Apart from this, interpretation of the financial information using accounting

ratios has also been included in the report.

TASK 1

1.1Different users of financial information and their needs

Financial information helps an individual to understand the business of EL Ltd. It can be

used to analyse the growth opportunities of the firm in the future. All the individuals and groups

which are associated with the company are known as stakeholders (Brigham and Ehrhardt,

2013). It is essential for EL Ltd to protect the interest of their stakeholders. Different users of

information and their needs are given below:

Managers: They need financial information to assess the position and performance of the

company (De Groot, Alkemade, Braat and Willemen, 2010.). The managers of EL Ltd take

business decisions on the basis of this. It helps them to manage the affairs of the organisation in

the long run.

Employees: Employees of EL Ltd are completely dependent on the company for their

remuneration (Minichilli, Corbetta and MacMillan, 2010). The profitability of the company can

affect their job security and compensation. They need financial statements to evaluate the future

of the company in the industry.

Suppliers: Suppliers provide goods on credit to EL Ltd. They have to assess their

financial statement to see their credit worthiness. The financial health of the company is used to

Financial accounting and reporting consists of summarizing, analysis and reporting

financial transactions related to a business. It is mandatory for an organisation to prepare

financial statements that depict true and fair picture of the business. There are many stakeholders

which are associated with a business such as suppliers, shareholders, banks, employees,

government etc (Anderson and et.al., 2015). They have interest in the company and they need the

information for decision making. There are certain domestic and international accounting

standards which provides framework and guidelines for all the companies in UK (Ingram,

LaForge and Williams, 2012). The present report is based on EL Ltd which has been in the

business for more than 10 years. They provide domestic electrical services to homes and

business units in the country. There are some laws and regulation which affect the accounting

and reporting standards. Furthermore, it is essential for the company to understand the formats of

financial statements. Apart from this, interpretation of the financial information using accounting

ratios has also been included in the report.

TASK 1

1.1Different users of financial information and their needs

Financial information helps an individual to understand the business of EL Ltd. It can be

used to analyse the growth opportunities of the firm in the future. All the individuals and groups

which are associated with the company are known as stakeholders (Brigham and Ehrhardt,

2013). It is essential for EL Ltd to protect the interest of their stakeholders. Different users of

information and their needs are given below:

Managers: They need financial information to assess the position and performance of the

company (De Groot, Alkemade, Braat and Willemen, 2010.). The managers of EL Ltd take

business decisions on the basis of this. It helps them to manage the affairs of the organisation in

the long run.

Employees: Employees of EL Ltd are completely dependent on the company for their

remuneration (Minichilli, Corbetta and MacMillan, 2010). The profitability of the company can

affect their job security and compensation. They need financial statements to evaluate the future

of the company in the industry.

Suppliers: Suppliers provide goods on credit to EL Ltd. They have to assess their

financial statement to see their credit worthiness. The financial health of the company is used to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

formulate the terms of credit (Minichilli, Corbetta and MacMillan, 2010). Banks also analyse the

credit position of a business before granting a loan to them.

Government: UK government needs financial statements to make sure that EL Ltd has

presented true and fair picture of the business to its stakeholders (Bovée and Thill, 2014). They

also ensure that the company is paying its tax returns and helping in the economic growth of the

country. The government keeps a track that the business in following all rules and regulations.

Customers: Customers need financial statements to evaluate the performance of the

company and its future (Bazerman and Moore, 2012). It allows to see whether EL Ltd have the

potential to supply the goods and services according to the demands.

1.2 Legal and regulatory influences on financial statements

It is the responsibility of Financial Reporting Council (FRC) to provide framework for

financial reporting (Broadbent and Cullen, 2012). It is essential for all the companies to follow

the rules and regulations of the government. EL Ltd has to change their strategies in order to

comply with the legal and regulatory framework of the government. Different organisations

prepare their statements according to their suitability. It helps them tot reflect the true picture of

the business. For example, Joint Stock Companies Act (1844), Company Act (1900) and limited

liability consolidation (1844) made it compulsory for the companies to create audited balance

sheets (Coombs, 2014). As per the legislation of UK, all the business entities have to abide by

the rules whether it is a sole proprietor, partnership or public limited company. They have to

present their financial report at the end of each year. The main authorities are UK Accounting

Standards Board, International Accounting Standards (IAS) and Company Act 2006 (Epstein and

Buhovac, 2014). It has allowed the government to keep a track on the business activities of

different companies in UK. It has helped them to protect the rights of the stakeholders. It is

essential for EL Ltd to disclose all the material facts of the company that can affect the decision

making of the stakeholders. Apart from this, the financial statements should be should not

contain any technical languages which cannot be understood by the people (Kaplan and

Atkinson, 2011). It should be simple language and notes should be included in the balance sheet.

These notes should contain in depth details of different transactions which cannot be included in

the balance sheet.

credit position of a business before granting a loan to them.

Government: UK government needs financial statements to make sure that EL Ltd has

presented true and fair picture of the business to its stakeholders (Bovée and Thill, 2014). They

also ensure that the company is paying its tax returns and helping in the economic growth of the

country. The government keeps a track that the business in following all rules and regulations.

Customers: Customers need financial statements to evaluate the performance of the

company and its future (Bazerman and Moore, 2012). It allows to see whether EL Ltd have the

potential to supply the goods and services according to the demands.

1.2 Legal and regulatory influences on financial statements

It is the responsibility of Financial Reporting Council (FRC) to provide framework for

financial reporting (Broadbent and Cullen, 2012). It is essential for all the companies to follow

the rules and regulations of the government. EL Ltd has to change their strategies in order to

comply with the legal and regulatory framework of the government. Different organisations

prepare their statements according to their suitability. It helps them tot reflect the true picture of

the business. For example, Joint Stock Companies Act (1844), Company Act (1900) and limited

liability consolidation (1844) made it compulsory for the companies to create audited balance

sheets (Coombs, 2014). As per the legislation of UK, all the business entities have to abide by

the rules whether it is a sole proprietor, partnership or public limited company. They have to

present their financial report at the end of each year. The main authorities are UK Accounting

Standards Board, International Accounting Standards (IAS) and Company Act 2006 (Epstein and

Buhovac, 2014). It has allowed the government to keep a track on the business activities of

different companies in UK. It has helped them to protect the rights of the stakeholders. It is

essential for EL Ltd to disclose all the material facts of the company that can affect the decision

making of the stakeholders. Apart from this, the financial statements should be should not

contain any technical languages which cannot be understood by the people (Kaplan and

Atkinson, 2011). It should be simple language and notes should be included in the balance sheet.

These notes should contain in depth details of different transactions which cannot be included in

the balance sheet.

1.3 Assess the implications for the users

Legal and regulatory framework of UK has significant implications of the stakeholders.

They can use the financial statements to assess the position and performance of EL Ltd. The

main aim of the government is to protect the interests of the consumers and other stakeholders

(Kaplan and Atkinson, 2011). But still many people believed that there are many loopholes in the

preparation of the financial reports. The financial reports of the company are very complicated.

Many companies have provided extremely detailed information which extends to more than 100

pages. Even though, all the material information have been presented in the report but it is

impossible for the users to understand it due to unimportant complexities (Ledgerwood, 2014).

Furthermore, the management of EL Ltd can opt for those accounting treatments that is in favour

of their business. It can distort the entire picture which can influence the decision making of the

people. There are certain rules and regulations which have to followed by the companies. The

overall impact on the users of the financial statements have been positive. It has allowed them to

rely on the financial reports while taking investments decisions (Lusardi, 2011). They can use

credit details, cash inflow and outflows for future decision making. The government also

analyses the statements of EL Ltd to see whether they have been working for the benefits of the

society or not. It gives them details for their income, profitability, liquidity, solvency and credit

worthiness. Financial Reporting Council (FRC) makes sure that all the companies follow the

regulations and prepare their statements accordingly (Madura, 2011). This protects the investors

and stakeholders from any unfair practices adopted by a business.

1.4 How different laws/ regulations are dealt with by accounting and reporting standards

Accounting and reporting standards are changed by the government according to the

requirements. These changes are made so as to improve transparency in the business activities of

various companies in UK. The Security and Exchange Commission has restricted instability of

stocks in the market because it ensures that generally accepted accounting principles are

followed (Ingram, LaForge and Williams, 2012). It is the responsibility of Financial Accounting

Standards Board (FASB) to form standards for the preparation of financial statements. It protects

the interest of the investors and shareholders. Furthermore, it acts as a shield for the investors

and protects them from frauds and concealment of facts. UK has Internal accounting standards

which was established to assist in comprehensive financial accounting reports. Government

Accounting Standards Board (GASB) has made guidelines which are mandatory to be followed

Legal and regulatory framework of UK has significant implications of the stakeholders.

They can use the financial statements to assess the position and performance of EL Ltd. The

main aim of the government is to protect the interests of the consumers and other stakeholders

(Kaplan and Atkinson, 2011). But still many people believed that there are many loopholes in the

preparation of the financial reports. The financial reports of the company are very complicated.

Many companies have provided extremely detailed information which extends to more than 100

pages. Even though, all the material information have been presented in the report but it is

impossible for the users to understand it due to unimportant complexities (Ledgerwood, 2014).

Furthermore, the management of EL Ltd can opt for those accounting treatments that is in favour

of their business. It can distort the entire picture which can influence the decision making of the

people. There are certain rules and regulations which have to followed by the companies. The

overall impact on the users of the financial statements have been positive. It has allowed them to

rely on the financial reports while taking investments decisions (Lusardi, 2011). They can use

credit details, cash inflow and outflows for future decision making. The government also

analyses the statements of EL Ltd to see whether they have been working for the benefits of the

society or not. It gives them details for their income, profitability, liquidity, solvency and credit

worthiness. Financial Reporting Council (FRC) makes sure that all the companies follow the

regulations and prepare their statements accordingly (Madura, 2011). This protects the investors

and stakeholders from any unfair practices adopted by a business.

1.4 How different laws/ regulations are dealt with by accounting and reporting standards

Accounting and reporting standards are changed by the government according to the

requirements. These changes are made so as to improve transparency in the business activities of

various companies in UK. The Security and Exchange Commission has restricted instability of

stocks in the market because it ensures that generally accepted accounting principles are

followed (Ingram, LaForge and Williams, 2012). It is the responsibility of Financial Accounting

Standards Board (FASB) to form standards for the preparation of financial statements. It protects

the interest of the investors and shareholders. Furthermore, it acts as a shield for the investors

and protects them from frauds and concealment of facts. UK has Internal accounting standards

which was established to assist in comprehensive financial accounting reports. Government

Accounting Standards Board (GASB) has made guidelines which are mandatory to be followed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Minichilli, Corbetta and MacMillan, 2010). It has helped the investors to understand different

aspects and entries in the reports. This has not only increased the reliability but transparency has

also improved in the country. Many committees have been formed which look after this prospect

of the country. In the year 1969, UK ICAEW came up with a statement that sowed the intent of

accounting standards. It made clear that there are four goals of the standards which have to be

followed by all companies (Kaplan and Atkinson, 2011). It will help in the reduction of

dissimilarities in the accounting principles. Furthermore, it was aimed to disclose the basics of

accounting and reporting. UK government has been working on the development and I

improvement in the accounting and reporting standards of the country. They want that all the

companies should follow the guidelines of the authority and prepare statements accordingly

(Crilly and Ioannou, 2014).

TASK 2

2.1 Prepare financial statements for a variety of business with trail balance

Preparation of unadjusted trial balance is simple. All the balances of the account are

transferred from ledger to the trial balance (Business Finance, 2014). The debit balances appear

on the left side while credit balances on the right side column. Unadjusted trial balance for EL

Ltd is as follows:

EL Ltd

Unadjusted Trial Balance

December 31, 2015

Account Debit Credit

Cash 32800

Accounts receivables 300

Inventory 39800

Leasehold Property 100000

Accounts payable 49000

Long term liabilities 99500

Common Stock 10000

aspects and entries in the reports. This has not only increased the reliability but transparency has

also improved in the country. Many committees have been formed which look after this prospect

of the country. In the year 1969, UK ICAEW came up with a statement that sowed the intent of

accounting standards. It made clear that there are four goals of the standards which have to be

followed by all companies (Kaplan and Atkinson, 2011). It will help in the reduction of

dissimilarities in the accounting principles. Furthermore, it was aimed to disclose the basics of

accounting and reporting. UK government has been working on the development and I

improvement in the accounting and reporting standards of the country. They want that all the

companies should follow the guidelines of the authority and prepare statements accordingly

(Crilly and Ioannou, 2014).

TASK 2

2.1 Prepare financial statements for a variety of business with trail balance

Preparation of unadjusted trial balance is simple. All the balances of the account are

transferred from ledger to the trial balance (Business Finance, 2014). The debit balances appear

on the left side while credit balances on the right side column. Unadjusted trial balance for EL

Ltd is as follows:

EL Ltd

Unadjusted Trial Balance

December 31, 2015

Account Debit Credit

Cash 32800

Accounts receivables 300

Inventory 39800

Leasehold Property 100000

Accounts payable 49000

Long term liabilities 99500

Common Stock 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

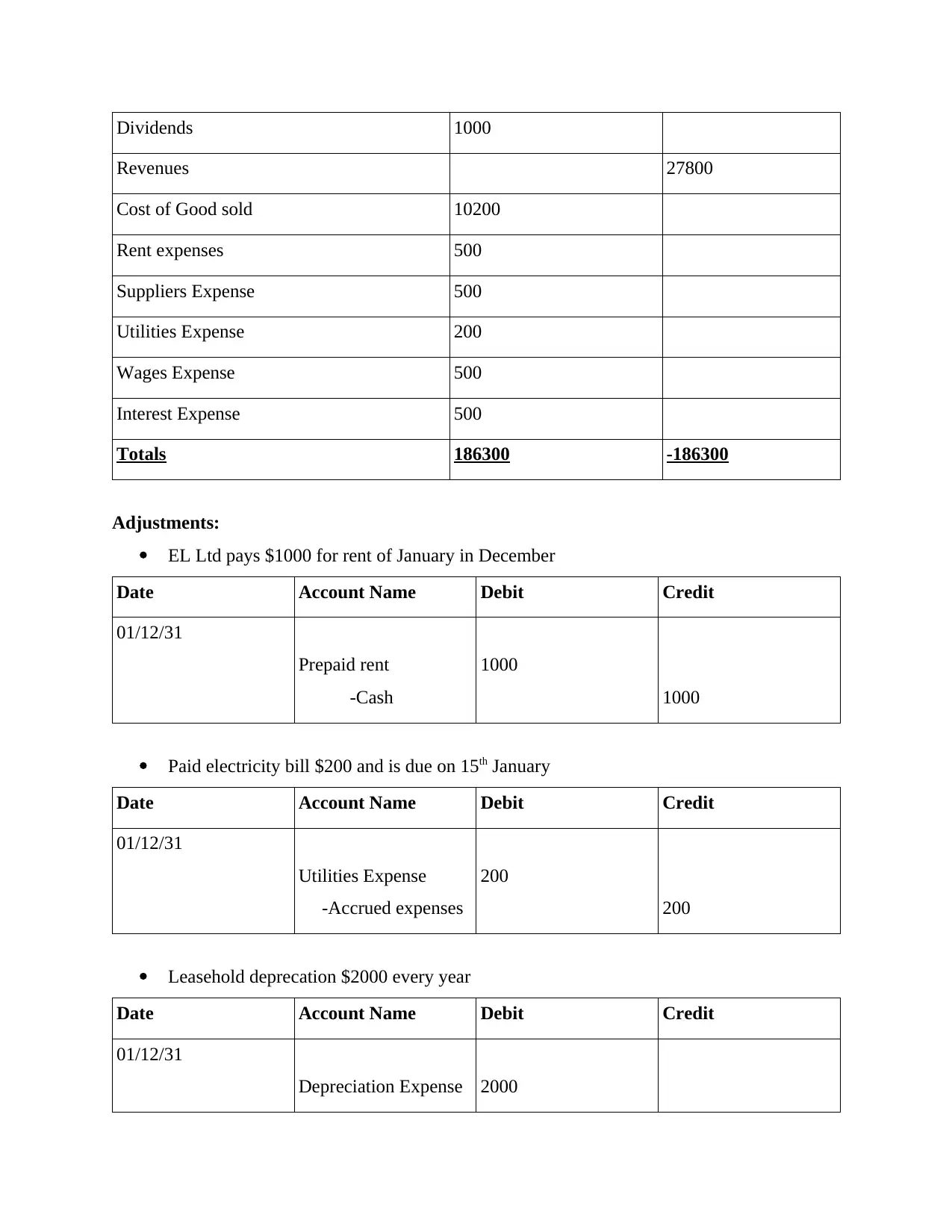

Dividends 1000

Revenues 27800

Cost of Good sold 10200

Rent expenses 500

Suppliers Expense 500

Utilities Expense 200

Wages Expense 500

Interest Expense 500

Totals 186300 -186300

Adjustments:

EL Ltd pays $1000 for rent of January in December

Date Account Name Debit Credit

01/12/31

Prepaid rent

-Cash

1000

1000

Paid electricity bill $200 and is due on 15th January

Date Account Name Debit Credit

01/12/31

Utilities Expense

-Accrued expenses

200

200

Leasehold deprecation $2000 every year

Date Account Name Debit Credit

01/12/31

Depreciation Expense 2000

Revenues 27800

Cost of Good sold 10200

Rent expenses 500

Suppliers Expense 500

Utilities Expense 200

Wages Expense 500

Interest Expense 500

Totals 186300 -186300

Adjustments:

EL Ltd pays $1000 for rent of January in December

Date Account Name Debit Credit

01/12/31

Prepaid rent

-Cash

1000

1000

Paid electricity bill $200 and is due on 15th January

Date Account Name Debit Credit

01/12/31

Utilities Expense

-Accrued expenses

200

200

Leasehold deprecation $2000 every year

Date Account Name Debit Credit

01/12/31

Depreciation Expense 2000

-Accumulated

deprecation

2000

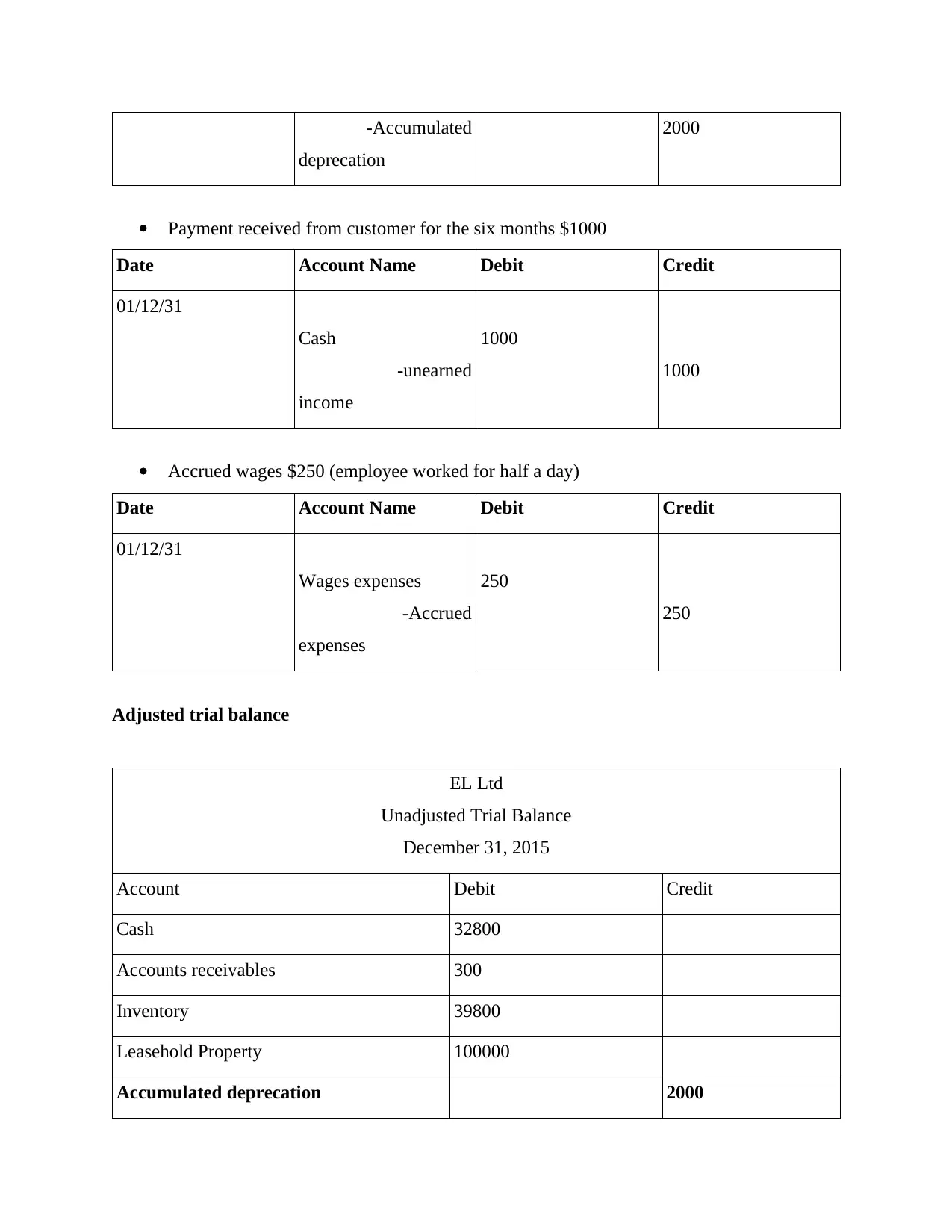

Payment received from customer for the six months $1000

Date Account Name Debit Credit

01/12/31

Cash

-unearned

income

1000

1000

Accrued wages $250 (employee worked for half a day)

Date Account Name Debit Credit

01/12/31

Wages expenses

-Accrued

expenses

250

250

Adjusted trial balance

EL Ltd

Unadjusted Trial Balance

December 31, 2015

Account Debit Credit

Cash 32800

Accounts receivables 300

Inventory 39800

Leasehold Property 100000

Accumulated deprecation 2000

deprecation

2000

Payment received from customer for the six months $1000

Date Account Name Debit Credit

01/12/31

Cash

-unearned

income

1000

1000

Accrued wages $250 (employee worked for half a day)

Date Account Name Debit Credit

01/12/31

Wages expenses

-Accrued

expenses

250

250

Adjusted trial balance

EL Ltd

Unadjusted Trial Balance

December 31, 2015

Account Debit Credit

Cash 32800

Accounts receivables 300

Inventory 39800

Leasehold Property 100000

Accumulated deprecation 2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

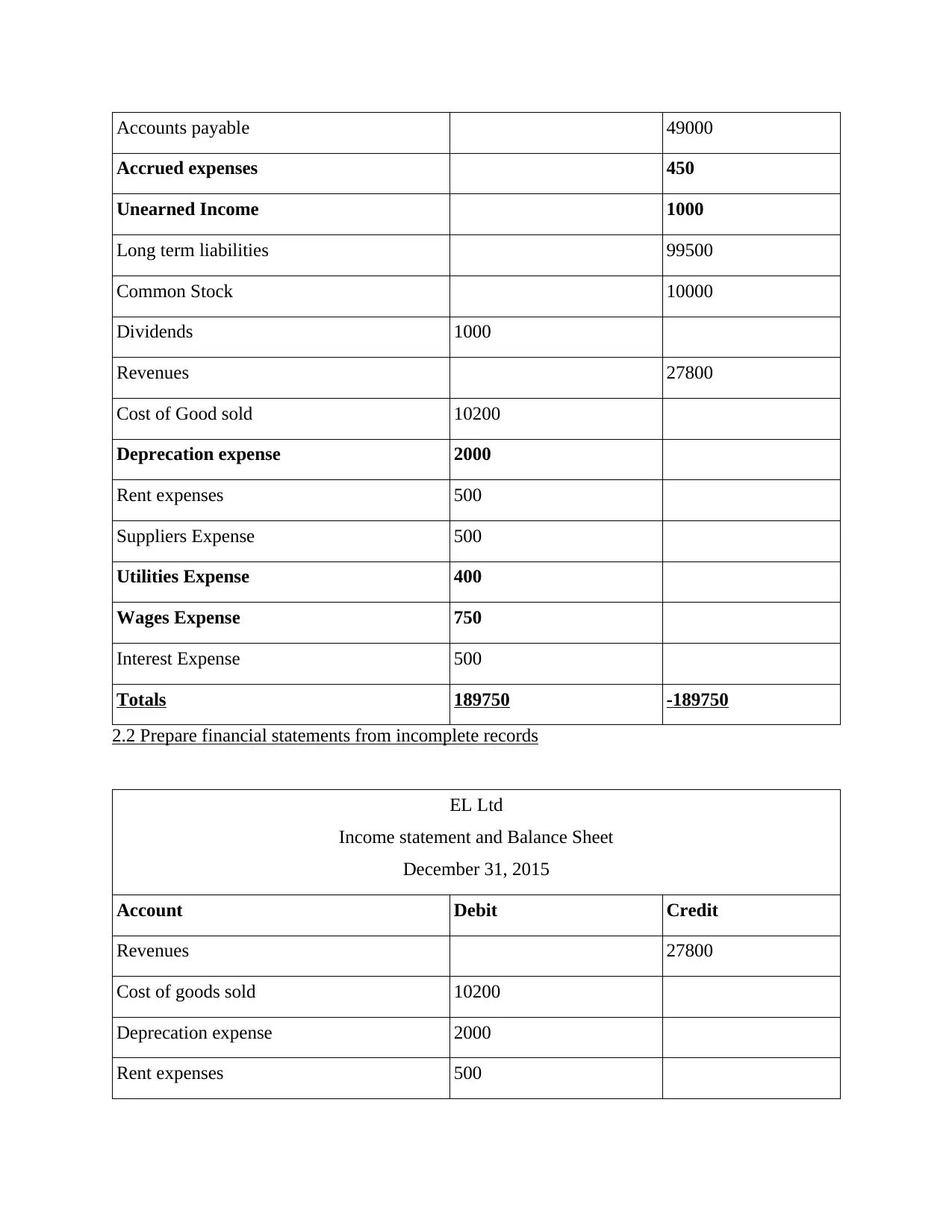

Accounts payable 49000

Accrued expenses 450

Unearned Income 1000

Long term liabilities 99500

Common Stock 10000

Dividends 1000

Revenues 27800

Cost of Good sold 10200

Deprecation expense 2000

Rent expenses 500

Suppliers Expense 500

Utilities Expense 400

Wages Expense 750

Interest Expense 500

Totals 189750 -189750

2.2 Prepare financial statements from incomplete records

EL Ltd

Income statement and Balance Sheet

December 31, 2015

Account Debit Credit

Revenues 27800

Cost of goods sold 10200

Deprecation expense 2000

Rent expenses 500

Accrued expenses 450

Unearned Income 1000

Long term liabilities 99500

Common Stock 10000

Dividends 1000

Revenues 27800

Cost of Good sold 10200

Deprecation expense 2000

Rent expenses 500

Suppliers Expense 500

Utilities Expense 400

Wages Expense 750

Interest Expense 500

Totals 189750 -189750

2.2 Prepare financial statements from incomplete records

EL Ltd

Income statement and Balance Sheet

December 31, 2015

Account Debit Credit

Revenues 27800

Cost of goods sold 10200

Deprecation expense 2000

Rent expenses 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

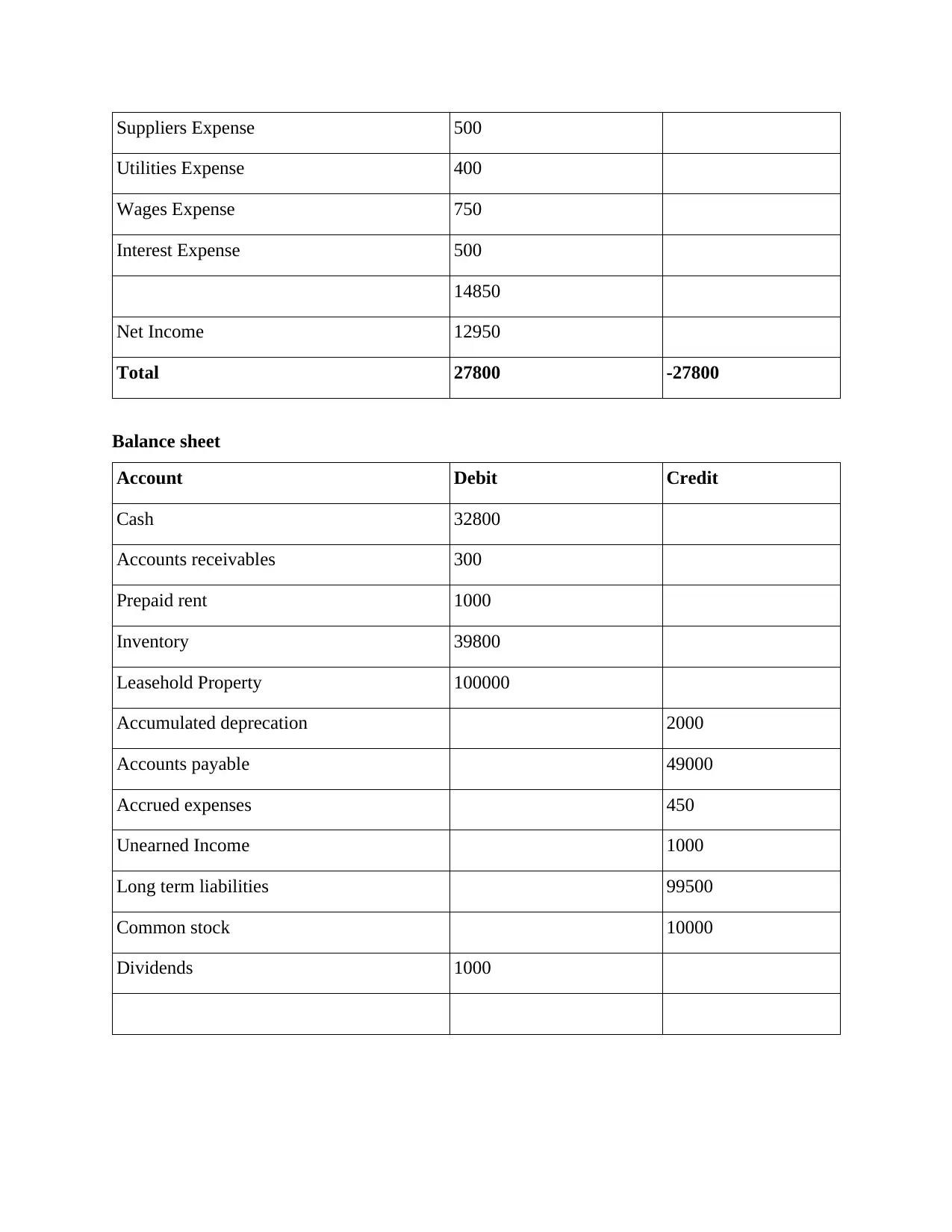

Suppliers Expense 500

Utilities Expense 400

Wages Expense 750

Interest Expense 500

14850

Net Income 12950

Total 27800 -27800

Balance sheet

Account Debit Credit

Cash 32800

Accounts receivables 300

Prepaid rent 1000

Inventory 39800

Leasehold Property 100000

Accumulated deprecation 2000

Accounts payable 49000

Accrued expenses 450

Unearned Income 1000

Long term liabilities 99500

Common stock 10000

Dividends 1000

Utilities Expense 400

Wages Expense 750

Interest Expense 500

14850

Net Income 12950

Total 27800 -27800

Balance sheet

Account Debit Credit

Cash 32800

Accounts receivables 300

Prepaid rent 1000

Inventory 39800

Leasehold Property 100000

Accumulated deprecation 2000

Accounts payable 49000

Accrued expenses 450

Unearned Income 1000

Long term liabilities 99500

Common stock 10000

Dividends 1000

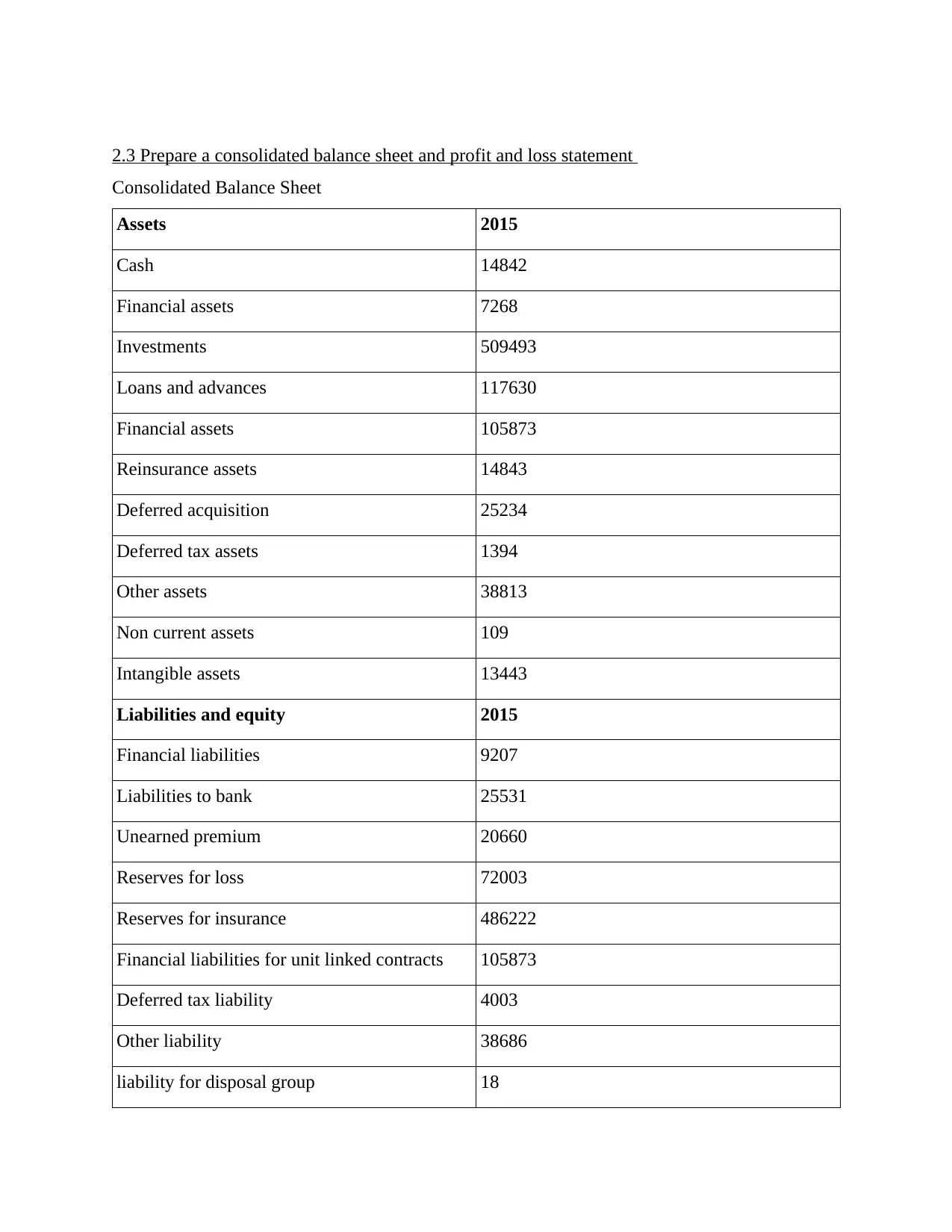

2.3 Prepare a consolidated balance sheet and profit and loss statement

Consolidated Balance Sheet

Assets 2015

Cash 14842

Financial assets 7268

Investments 509493

Loans and advances 117630

Financial assets 105873

Reinsurance assets 14843

Deferred acquisition 25234

Deferred tax assets 1394

Other assets 38813

Non current assets 109

Intangible assets 13443

Liabilities and equity 2015

Financial liabilities 9207

Liabilities to bank 25531

Unearned premium 20660

Reserves for loss 72003

Reserves for insurance 486222

Financial liabilities for unit linked contracts 105873

Deferred tax liability 4003

Other liability 38686

liability for disposal group 18

Consolidated Balance Sheet

Assets 2015

Cash 14842

Financial assets 7268

Investments 509493

Loans and advances 117630

Financial assets 105873

Reinsurance assets 14843

Deferred acquisition 25234

Deferred tax assets 1394

Other assets 38813

Non current assets 109

Intangible assets 13443

Liabilities and equity 2015

Financial liabilities 9207

Liabilities to bank 25531

Unearned premium 20660

Reserves for loss 72003

Reserves for insurance 486222

Financial liabilities for unit linked contracts 105873

Deferred tax liability 4003

Other liability 38686

liability for disposal group 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.