Case Study: Accounting System Implementation at Elegant Firm

VerifiedAdded on 2024/06/03

|10

|1824

|262

Case Study

AI Summary

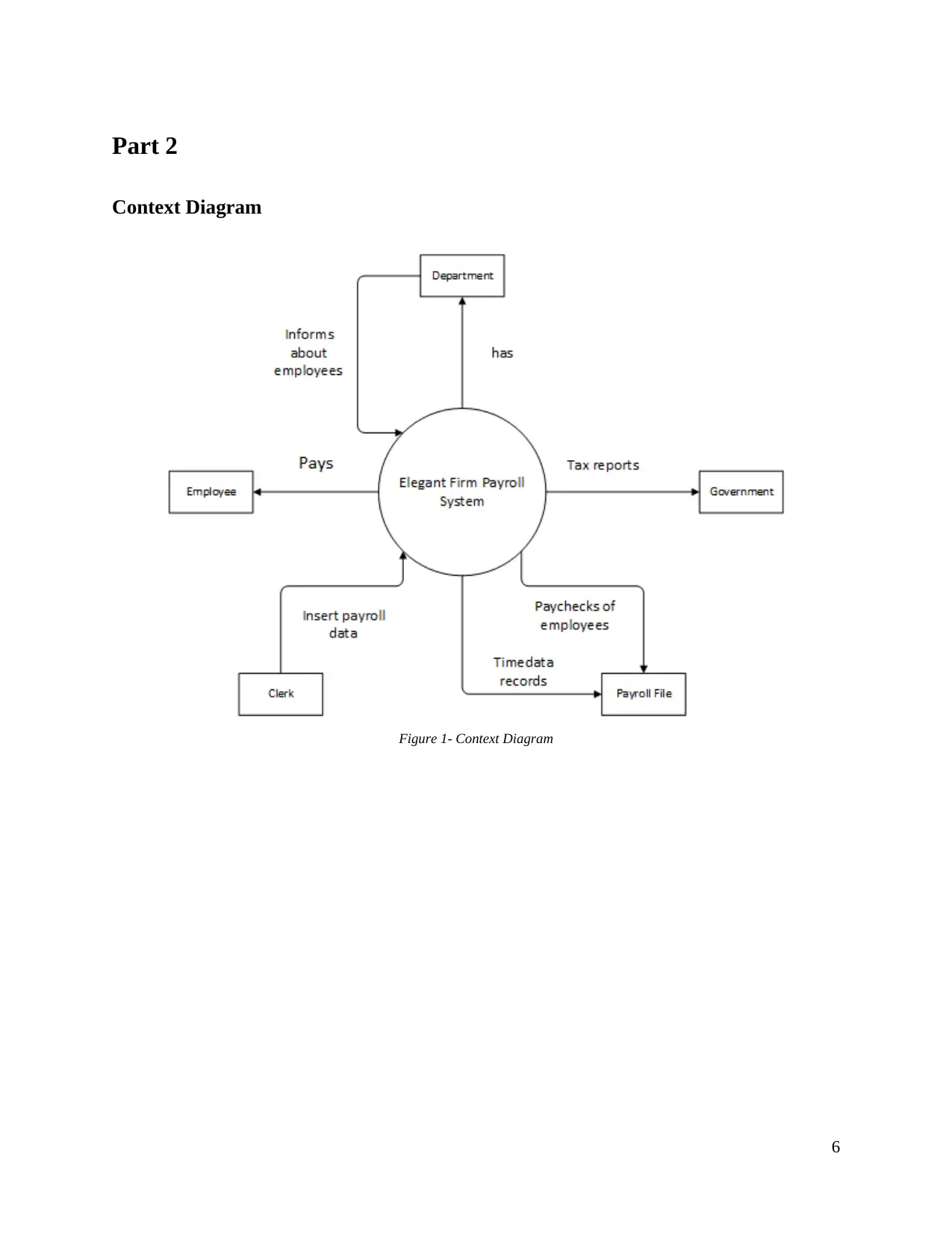

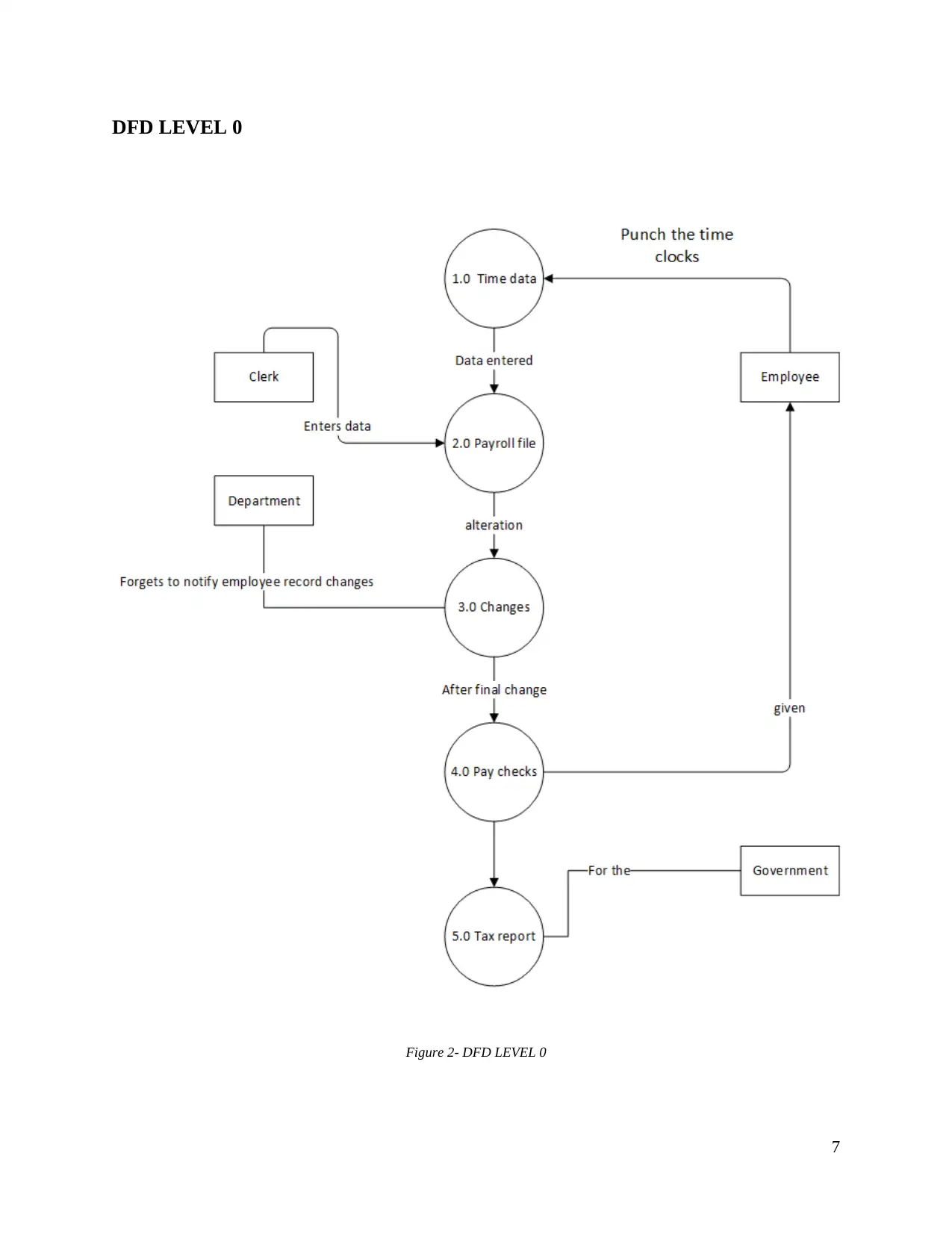

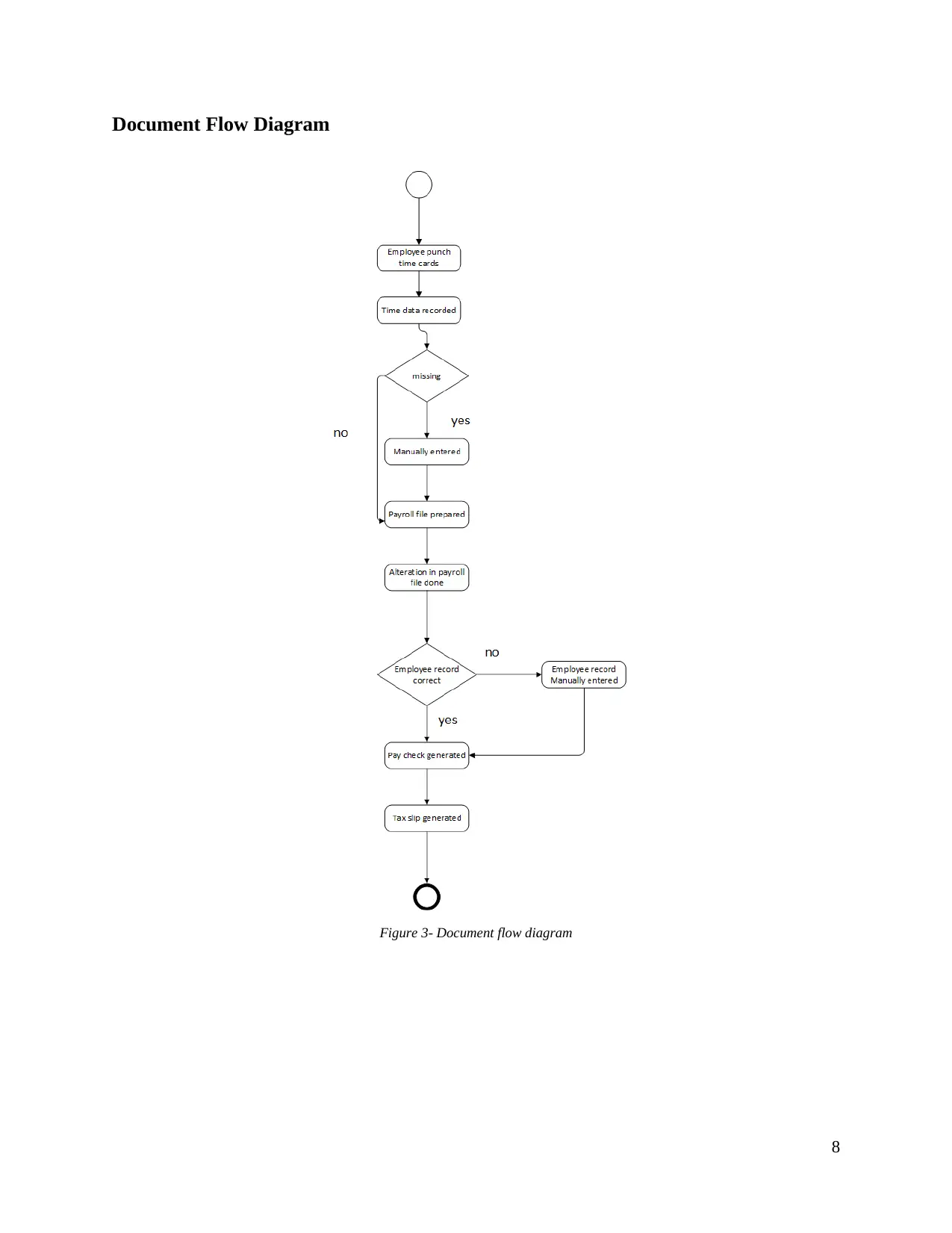

This case study examines the implementation of a new accounting information system (AIS) at Elegant Firm, focusing on the roles of management and employees in the selection and implementation process. It contrasts the benefits of the new system, which utilizes a life cycle approach, with the drawbacks of the existing file-oriented system, such as data redundancy and poor data isolation. The study details the roles of accountants, managers, and business analysts in analyzing the system, emphasizing the importance of gathering information, system selection, implementation, and continuous operation. The document includes context and data flow diagrams illustrating the system's architecture and document flow. This resource provides a comprehensive overview for understanding the complexities of transitioning to a new accounting system and is available for students on Desklib, a platform offering various study tools and solved assignments.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.