Financial Performance, Expansion, and Finance for Elton Plc Report

VerifiedAdded on 2020/01/23

|18

|6146

|117

Report

AI Summary

This report offers a comprehensive financial analysis of Elton Plc, a computer hardware manufacturer, evaluating its performance through ratio analysis of its financial statements. The analysis covers profitability, liquidity, efficiency, and solvency ratios, revealing trends in sales, costs, and asset utilization. The report further assesses the viability of business expansion using investment appraisal techniques, advising the board of directors on non-monetary factors crucial for international market entry. It also identifies potential sources of finance for the expansion project, including equity and debt options, and concludes with strategic recommendations for improving financial health and performance. The report highlights the importance of strategic financial decision-making for maximizing profitability and achieving sustainable growth, with specific recommendations on inventory management, credit policies, and cost control. The report also provides insights into the company's investment in fixed assets and its impact on overall financial performance.

Financial Decision Making

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

PART 1..................................................................................................................................................4

Stating the financial performance of Elton Plc by making analysis of final accounts via ratio

analysis ............................................................................................................................................4

Part 2.....................................................................................................................................................9

Assessing the viability of business expansion through investment appraisal techniques................9

Giving advise to the Board of Directors about the non-monetary factors which company needs to

undertake before entering in international market.........................................................................11

Stating the sources of finance available to Elton Plc for its expansion project.............................12

CONCLUSION..................................................................................................................................13

References..........................................................................................................................................14

2

INTRODUCTION................................................................................................................................4

PART 1..................................................................................................................................................4

Stating the financial performance of Elton Plc by making analysis of final accounts via ratio

analysis ............................................................................................................................................4

Part 2.....................................................................................................................................................9

Assessing the viability of business expansion through investment appraisal techniques................9

Giving advise to the Board of Directors about the non-monetary factors which company needs to

undertake before entering in international market.........................................................................11

Stating the sources of finance available to Elton Plc for its expansion project.............................12

CONCLUSION..................................................................................................................................13

References..........................................................................................................................................14

2

Executive summary

In the business organization, manager has responsibility to make most effectual decision

which aid in the productivity and profitability of firm. Investment, product development etc. are the

main decisions which are highly associated with the financial aspect of firm. In this, manager has

accountability to take decision by making in-depth analysis of proposed investment. This report is

based on Elton Plc which manufactures computer hardware and equipments namely PC, laptop,

tablets etc. It can be summarized that it is required for Elton Plc to makes changes in their existing

strategic and policy framework. Through this, business unit can enhance its financial health and

performance to the significant level. Further, it can be inferred from the investment appraisal tools

that company will not enjoy high level of financial benefits by expanding business in Asian,

African, South eastern and North American. It can be stated that Elton Plc needs to issue shares and

make use of retained profit for fulfil its financial need and thereby expands business operations

more effectively.

3

In the business organization, manager has responsibility to make most effectual decision

which aid in the productivity and profitability of firm. Investment, product development etc. are the

main decisions which are highly associated with the financial aspect of firm. In this, manager has

accountability to take decision by making in-depth analysis of proposed investment. This report is

based on Elton Plc which manufactures computer hardware and equipments namely PC, laptop,

tablets etc. It can be summarized that it is required for Elton Plc to makes changes in their existing

strategic and policy framework. Through this, business unit can enhance its financial health and

performance to the significant level. Further, it can be inferred from the investment appraisal tools

that company will not enjoy high level of financial benefits by expanding business in Asian,

African, South eastern and North American. It can be stated that Elton Plc needs to issue shares and

make use of retained profit for fulfil its financial need and thereby expands business operations

more effectively.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making refers to the process in which company makes judgement in

relation to the expansion, investment etc. The main motive behind this aspect is maximization of

profitability of the firm. In this regard, the present report will describe the financial position of

Elton Plc which deals in the computer hardware and accessories. Further, it will also shed light on

the extent to which techniques of investment appraisal facilitate profitable decision making. This

report will also develop understanding about the varied sources of finance along with their

implications.

PART 1

Business Performance Analysis

Stating the financial performance of Elton Plc by making analysis of final accounts via ratio

analysis

Interpreting the statement of profit and loss through the following ratios

Profitability ratios: Gross and net profit ratios are the most effectual measures which assist Elton

Plc and its stakeholders in evaluating the profit earned by the firm during the year.

Sales

From the given financial statements, it has been assessed that 30% growth has taken place in

the sales of Elton Plc. This is good indicator which entails customers prefer to invest money in the

laptops and tablet of the company to the large extent by considering the aspects such as affordable

prices and highly quality. In the present era, there is the high level of trend towards the use of

laptops and tablet. This is one of the main reasons due to which sales of Elton Plc increased in

2015.

Gross profit ratio

This measure helps in assessing the extent to which company has generated high sales

revenue by incurring the direct expenses (Agarwal and Mazumder, 2013). From the above table, it

has been analyzed that gross profit margin of Elton Plc declined from 25.57% to 21.57% in the

accounting year 2015. Due to rise in the direct expenses such as material, labour etc. GP margin of

the firm decreased. Thus, Elton Plc needs to make focus on offering laptop and tablets which are

innovatively designed. In this way, company can entice sales by influencing the decision making

aspect or demand of the customers. Further, business unit also needs to exert control on direct

expenses such as carriage inward, wages etc. Hence, by working on all the above mentioned aspects

Elton Plc can enhance its financial performance.

Overheads

4

Financial decision making refers to the process in which company makes judgement in

relation to the expansion, investment etc. The main motive behind this aspect is maximization of

profitability of the firm. In this regard, the present report will describe the financial position of

Elton Plc which deals in the computer hardware and accessories. Further, it will also shed light on

the extent to which techniques of investment appraisal facilitate profitable decision making. This

report will also develop understanding about the varied sources of finance along with their

implications.

PART 1

Business Performance Analysis

Stating the financial performance of Elton Plc by making analysis of final accounts via ratio

analysis

Interpreting the statement of profit and loss through the following ratios

Profitability ratios: Gross and net profit ratios are the most effectual measures which assist Elton

Plc and its stakeholders in evaluating the profit earned by the firm during the year.

Sales

From the given financial statements, it has been assessed that 30% growth has taken place in

the sales of Elton Plc. This is good indicator which entails customers prefer to invest money in the

laptops and tablet of the company to the large extent by considering the aspects such as affordable

prices and highly quality. In the present era, there is the high level of trend towards the use of

laptops and tablet. This is one of the main reasons due to which sales of Elton Plc increased in

2015.

Gross profit ratio

This measure helps in assessing the extent to which company has generated high sales

revenue by incurring the direct expenses (Agarwal and Mazumder, 2013). From the above table, it

has been analyzed that gross profit margin of Elton Plc declined from 25.57% to 21.57% in the

accounting year 2015. Due to rise in the direct expenses such as material, labour etc. GP margin of

the firm decreased. Thus, Elton Plc needs to make focus on offering laptop and tablets which are

innovatively designed. In this way, company can entice sales by influencing the decision making

aspect or demand of the customers. Further, business unit also needs to exert control on direct

expenses such as carriage inward, wages etc. Hence, by working on all the above mentioned aspects

Elton Plc can enhance its financial performance.

Overheads

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administration expenses: Adm expenses of the firm declined by 30.06% in the accounting

year 2015. It indicates that company manages its operations with the high level of efficiency.

This in turn may help in enhancing the profitability aspect of firm. Distribution cost: In 2015, distribution cost of Elton Plc increased from 40% which in turn

influence the profit margin of the firm in negative direction. Due to the rise in fuel and high

level of distance distribution cost was significantly inclined in 2015. Thus, company is

required to assess the alternative ways of distribution which will help them in making

control on cost to the significant level.

Net profit ratio

Company can evaluate the profitability aspect which is available for offering dividend to the

shareholders via net profit margin. Through this, business unit can evaluate the extent to which

profit is generated by them over the indirect expenses (Tosun, 2013). The above mentioned analysis

presents that net profit margin of Elton Plc inclined from 4.06% to 6.08%. This aspect shows that

profitability aspect of the firm inclined in 2015 a compared to 2015. On the basis of this aspect, it

can be said that in 2015, company had made better control on indirect expenditure. Hence, Elton Plc

needs to make competent strategies for making control on expenses. This in turn helps business

organization in enhancing its profitability aspects. In this way, by offering enough or high dividend

Elton Plc can build distinct image in the mind of shareholders.

Statement of financial position

Non-current assets: In the accounting year 2015, Elton Plc has made high investment on property,

plant and equipment in terms of 49%. Further, development cost also inclined from 270 to 300 at

the end of 2015. Hence, it can be said that in 2015 company invested money in fixed assets for

ensuring the smooth functioning of business operations. Due to the increase in demand for such

products Elton plc has purchased the latest machinery and equipments for manufacturing laptops

and tablet phones at low cost.

Current assets: Financial statements of 2015 presents that due to the inventory and trade receivables

current assets of Elton Plc increased from 507 to 758.

Inventories: Closing stock of Elton plc increased from 120 to 290 in the financial year 2015. In this

regard, it can be stated that high closing inventory may result into more holding and storage cost.

Thus, business unit needs to frame competent strategies which helps them in exert control on

inventory and total cost to the significant level. High closing inventory presents that company

failed to make proper estimation regarding the tablets and mobile phone which they need to

manufacture. This in turn may result into high closing inventory at the end of accounting year 2015.

Trade and other receivables: Bills receivables from debtor inclined from 253 to 468. This aspect

5

year 2015. It indicates that company manages its operations with the high level of efficiency.

This in turn may help in enhancing the profitability aspect of firm. Distribution cost: In 2015, distribution cost of Elton Plc increased from 40% which in turn

influence the profit margin of the firm in negative direction. Due to the rise in fuel and high

level of distance distribution cost was significantly inclined in 2015. Thus, company is

required to assess the alternative ways of distribution which will help them in making

control on cost to the significant level.

Net profit ratio

Company can evaluate the profitability aspect which is available for offering dividend to the

shareholders via net profit margin. Through this, business unit can evaluate the extent to which

profit is generated by them over the indirect expenses (Tosun, 2013). The above mentioned analysis

presents that net profit margin of Elton Plc inclined from 4.06% to 6.08%. This aspect shows that

profitability aspect of the firm inclined in 2015 a compared to 2015. On the basis of this aspect, it

can be said that in 2015, company had made better control on indirect expenditure. Hence, Elton Plc

needs to make competent strategies for making control on expenses. This in turn helps business

organization in enhancing its profitability aspects. In this way, by offering enough or high dividend

Elton Plc can build distinct image in the mind of shareholders.

Statement of financial position

Non-current assets: In the accounting year 2015, Elton Plc has made high investment on property,

plant and equipment in terms of 49%. Further, development cost also inclined from 270 to 300 at

the end of 2015. Hence, it can be said that in 2015 company invested money in fixed assets for

ensuring the smooth functioning of business operations. Due to the increase in demand for such

products Elton plc has purchased the latest machinery and equipments for manufacturing laptops

and tablet phones at low cost.

Current assets: Financial statements of 2015 presents that due to the inventory and trade receivables

current assets of Elton Plc increased from 507 to 758.

Inventories: Closing stock of Elton plc increased from 120 to 290 in the financial year 2015. In this

regard, it can be stated that high closing inventory may result into more holding and storage cost.

Thus, business unit needs to frame competent strategies which helps them in exert control on

inventory and total cost to the significant level. High closing inventory presents that company

failed to make proper estimation regarding the tablets and mobile phone which they need to

manufacture. This in turn may result into high closing inventory at the end of accounting year 2015.

Trade and other receivables: Bills receivables from debtor inclined from 253 to 468. This aspect

5

entails that Elton Plc has made high sales on credit in 2015 as compared to previous year. Moreover,

receivables of the firm are closely associated with the credit sale made by the business organization.

Thus, business unit requires making changes in its existing credit policy. This in turn helps company

in improving its cash position to the great extent.

Cash and cash equivalents: Cash aspect of Elton plc is NIL in 2015 due to making investment in

the fixed assets. In this way, cash and its equivalents are highly affected in the negative manner.

Equity and Liabilities: Elton Plc issued shares in 2015 for meting the financial needs. Along with,

long term borrowing of the firm also inclined from 100 to 250. Along with this, trade payable and

overdraft also inclined in 2015 as compared to 2014. Due to the purchasing of material on credit

terms high trade payables inclined from 138 to 245. Along with this, for investing money in the

property, plant and equipment as well as developmental aspect company had fulfilled its finnacial

requirements through bank overdraft and by issuing the shares. Thus, company needs to make

control on its obligations which helps them in improving its financial and solvency position.

Liquidity ratios: These ratios provide deeper insight to the firm in relation to it capability for

meeting the financial obligations over current assets (Uechi and et.al., 2015). In this, by making

analysis of current and quick ratio Elton Plc can evaluate its financial capability to the large extent.

Current ratio

By doing ratio analysis, it has been identified that Elton Plc has ability in relation to the

meeting of its current obligations. In the accounting year 2015, current ratio of Elton Plc declined

from 3.67:1 to 2.50. This aspect clearly shows that current ratio of the business organization is very

near to the ideal ratio which is 2:1. Hence, by considering such aspects business unit can said to be

highly liquid.

Quick ratio

With the help of this ratio business enterprise can determine the level to which it has quick

assets which can be easily converted into cash (Togashi and et.al., 2015). By analyzing the

statement of financial position it has been found that quick ratio of the firm declined from 2.80:1 to

1.5:1 which is good for the firm. However, still firm needs to reduce its quick ratio for getting the

ideal ratio which is .5:1. Thus, it is required for Elton Plc to make investment in the profitable

projects which helps them in enhance their profitability aspect.

Efficiency ratio: This measure informs company about the efficiency aspect of personnel. Along

with this, such ratio also helps business organization in evaluating the extent to which strategies had

made contribution in the effective utilization of company's assets (Hu and et.al., 2012). In this way,

efficiency aspect can easily be measured by the business enterprise through fixed, net assets and

inventory turnover ratio.

6

receivables of the firm are closely associated with the credit sale made by the business organization.

Thus, business unit requires making changes in its existing credit policy. This in turn helps company

in improving its cash position to the great extent.

Cash and cash equivalents: Cash aspect of Elton plc is NIL in 2015 due to making investment in

the fixed assets. In this way, cash and its equivalents are highly affected in the negative manner.

Equity and Liabilities: Elton Plc issued shares in 2015 for meting the financial needs. Along with,

long term borrowing of the firm also inclined from 100 to 250. Along with this, trade payable and

overdraft also inclined in 2015 as compared to 2014. Due to the purchasing of material on credit

terms high trade payables inclined from 138 to 245. Along with this, for investing money in the

property, plant and equipment as well as developmental aspect company had fulfilled its finnacial

requirements through bank overdraft and by issuing the shares. Thus, company needs to make

control on its obligations which helps them in improving its financial and solvency position.

Liquidity ratios: These ratios provide deeper insight to the firm in relation to it capability for

meeting the financial obligations over current assets (Uechi and et.al., 2015). In this, by making

analysis of current and quick ratio Elton Plc can evaluate its financial capability to the large extent.

Current ratio

By doing ratio analysis, it has been identified that Elton Plc has ability in relation to the

meeting of its current obligations. In the accounting year 2015, current ratio of Elton Plc declined

from 3.67:1 to 2.50. This aspect clearly shows that current ratio of the business organization is very

near to the ideal ratio which is 2:1. Hence, by considering such aspects business unit can said to be

highly liquid.

Quick ratio

With the help of this ratio business enterprise can determine the level to which it has quick

assets which can be easily converted into cash (Togashi and et.al., 2015). By analyzing the

statement of financial position it has been found that quick ratio of the firm declined from 2.80:1 to

1.5:1 which is good for the firm. However, still firm needs to reduce its quick ratio for getting the

ideal ratio which is .5:1. Thus, it is required for Elton Plc to make investment in the profitable

projects which helps them in enhance their profitability aspect.

Efficiency ratio: This measure informs company about the efficiency aspect of personnel. Along

with this, such ratio also helps business organization in evaluating the extent to which strategies had

made contribution in the effective utilization of company's assets (Hu and et.al., 2012). In this way,

efficiency aspect can easily be measured by the business enterprise through fixed, net assets and

inventory turnover ratio.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Asset turnover ratio

Ratio analysis presents that in 2015, Elton Plc did not make effectual use of its assets in

comparison to the previous years. In 2014, total asset turnover ratio of Elton Plc was 1.71 whereas,

it reached on 1.59 at the end of 2015. Thus, business organization needs to lay emphasis on

organizing program which facilitate effectual management of human resources. In this, by evolving

high level of satisfaction and confidence among the personnel business unit can ensure optimum

utilization of net assets.

Fixed asset turnover ratio

In the financial year 2015, fixed asset turnover ratio of Elton Plc reduced from 3.02 to 2.94.

In this, it can be assessed that business enterprise failed to make effectual use of fixed assets such

as plant and machinery etc. while performing the business activities and functions. Thus, business

entity needs to frame competent strategies which encourage the personnel significantly. In this way,

by making improvement in fixed asset turnover ratio Elton Plc can also maximize its profit aspect to

the large level.

Interest coverage ratio

On the basis of interest coverage ratio Elton Plc it can be said that business unit has ability

in relation to making interest payment associated with outstanding debt. In 2015, interest coverage

ratio of business unit was 9.2 which is neither too high nor too lower. Thus, business enterprise

needs to enhance its ability in relation to making payment of interest on time. This in turn enhances

company's creditworthiness to the large extent.

Inventory turnover ratio

This aspect of the corporation reduced from 16.85 to 9.07 during the financial year 2015. In

this, by taking into consideration the output it has been determined that company sold its inventory

more frequently. This aspect shows that there is high level of demand for the laptop and tablet

which are manufactured by Elton Plc. In this, company also needs to place advertisement on social

sites such as Facebook, Twitter etc. Hence, by developing awareness in mind of large of number of

potential customers company can enhance its sales revenue.

Solvency ratio: Company can evaluate its solvency aspect by measuring the debt-equity ratio. This

ratio clearly serves information about the level to which business organization has undertaken debt

and equity sources for meeting the financial needs (Gamble and et.al., 2014).

Deb-equity ratio

In 2015, debt-equity ratio of the firm inclined from .11 to .22. This aspect entails that in the

accounting year 2015, Elton Plc issued debt instruments for raising finance. However, still debt-

equity ratio of Elton Plc is far from the ideal; ratio which is .5:1. Thus, for making balancing

7

Ratio analysis presents that in 2015, Elton Plc did not make effectual use of its assets in

comparison to the previous years. In 2014, total asset turnover ratio of Elton Plc was 1.71 whereas,

it reached on 1.59 at the end of 2015. Thus, business organization needs to lay emphasis on

organizing program which facilitate effectual management of human resources. In this, by evolving

high level of satisfaction and confidence among the personnel business unit can ensure optimum

utilization of net assets.

Fixed asset turnover ratio

In the financial year 2015, fixed asset turnover ratio of Elton Plc reduced from 3.02 to 2.94.

In this, it can be assessed that business enterprise failed to make effectual use of fixed assets such

as plant and machinery etc. while performing the business activities and functions. Thus, business

entity needs to frame competent strategies which encourage the personnel significantly. In this way,

by making improvement in fixed asset turnover ratio Elton Plc can also maximize its profit aspect to

the large level.

Interest coverage ratio

On the basis of interest coverage ratio Elton Plc it can be said that business unit has ability

in relation to making interest payment associated with outstanding debt. In 2015, interest coverage

ratio of business unit was 9.2 which is neither too high nor too lower. Thus, business enterprise

needs to enhance its ability in relation to making payment of interest on time. This in turn enhances

company's creditworthiness to the large extent.

Inventory turnover ratio

This aspect of the corporation reduced from 16.85 to 9.07 during the financial year 2015. In

this, by taking into consideration the output it has been determined that company sold its inventory

more frequently. This aspect shows that there is high level of demand for the laptop and tablet

which are manufactured by Elton Plc. In this, company also needs to place advertisement on social

sites such as Facebook, Twitter etc. Hence, by developing awareness in mind of large of number of

potential customers company can enhance its sales revenue.

Solvency ratio: Company can evaluate its solvency aspect by measuring the debt-equity ratio. This

ratio clearly serves information about the level to which business organization has undertaken debt

and equity sources for meeting the financial needs (Gamble and et.al., 2014).

Deb-equity ratio

In 2015, debt-equity ratio of the firm inclined from .11 to .22. This aspect entails that in the

accounting year 2015, Elton Plc issued debt instruments for raising finance. However, still debt-

equity ratio of Elton Plc is far from the ideal; ratio which is .5:1. Thus, for making balancing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

structure company requires issuing 1 debt instrument in against to 2 equity shares.

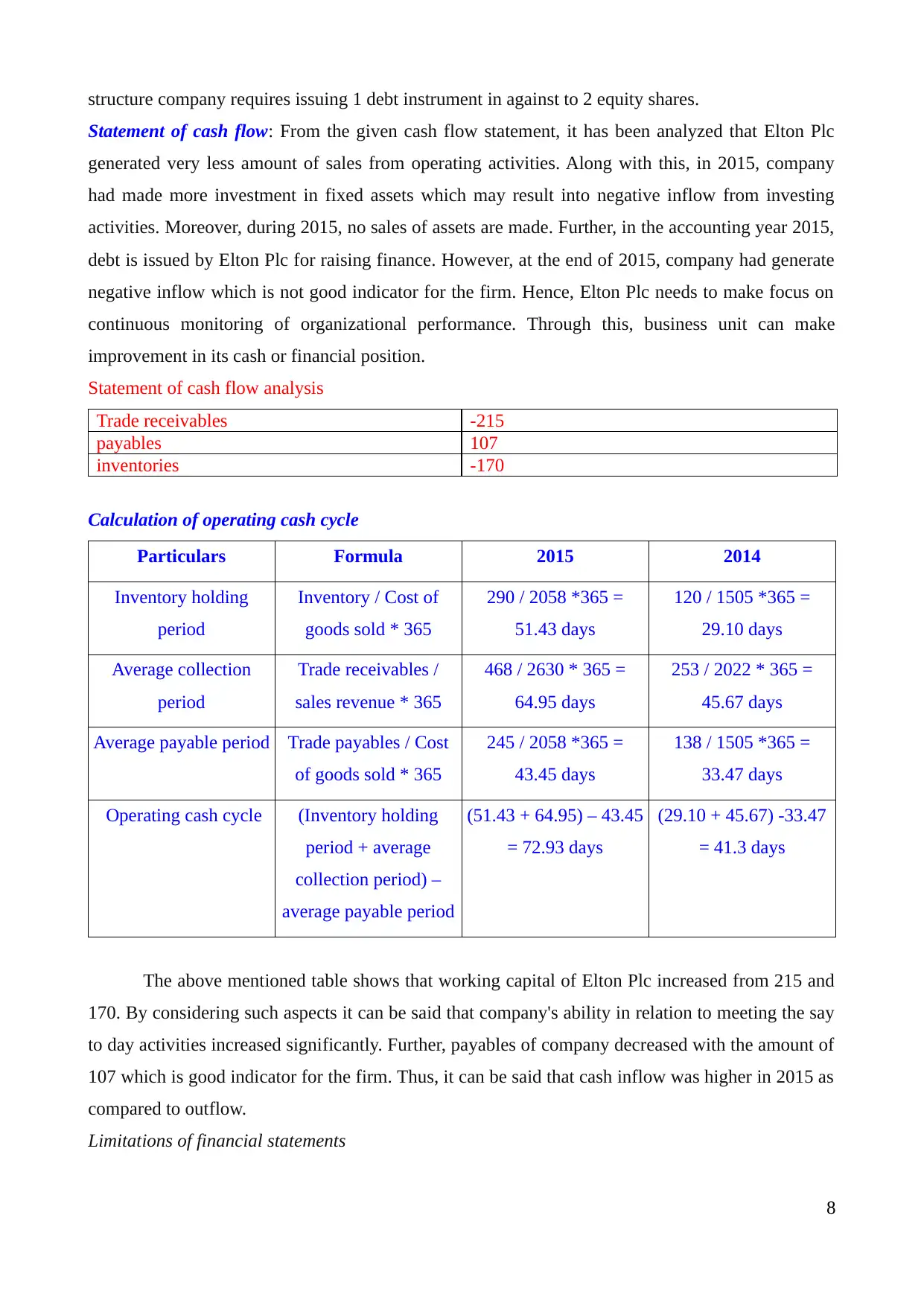

Statement of cash flow: From the given cash flow statement, it has been analyzed that Elton Plc

generated very less amount of sales from operating activities. Along with this, in 2015, company

had made more investment in fixed assets which may result into negative inflow from investing

activities. Moreover, during 2015, no sales of assets are made. Further, in the accounting year 2015,

debt is issued by Elton Plc for raising finance. However, at the end of 2015, company had generate

negative inflow which is not good indicator for the firm. Hence, Elton Plc needs to make focus on

continuous monitoring of organizational performance. Through this, business unit can make

improvement in its cash or financial position.

Statement of cash flow analysis

Trade receivables -215

payables 107

inventories -170

Calculation of operating cash cycle

Particulars Formula 2015 2014

Inventory holding

period

Inventory / Cost of

goods sold * 365

290 / 2058 *365 =

51.43 days

120 / 1505 *365 =

29.10 days

Average collection

period

Trade receivables /

sales revenue * 365

468 / 2630 * 365 =

64.95 days

253 / 2022 * 365 =

45.67 days

Average payable period Trade payables / Cost

of goods sold * 365

245 / 2058 *365 =

43.45 days

138 / 1505 *365 =

33.47 days

Operating cash cycle (Inventory holding

period + average

collection period) –

average payable period

(51.43 + 64.95) – 43.45

= 72.93 days

(29.10 + 45.67) -33.47

= 41.3 days

The above mentioned table shows that working capital of Elton Plc increased from 215 and

170. By considering such aspects it can be said that company's ability in relation to meeting the say

to day activities increased significantly. Further, payables of company decreased with the amount of

107 which is good indicator for the firm. Thus, it can be said that cash inflow was higher in 2015 as

compared to outflow.

Limitations of financial statements

8

Statement of cash flow: From the given cash flow statement, it has been analyzed that Elton Plc

generated very less amount of sales from operating activities. Along with this, in 2015, company

had made more investment in fixed assets which may result into negative inflow from investing

activities. Moreover, during 2015, no sales of assets are made. Further, in the accounting year 2015,

debt is issued by Elton Plc for raising finance. However, at the end of 2015, company had generate

negative inflow which is not good indicator for the firm. Hence, Elton Plc needs to make focus on

continuous monitoring of organizational performance. Through this, business unit can make

improvement in its cash or financial position.

Statement of cash flow analysis

Trade receivables -215

payables 107

inventories -170

Calculation of operating cash cycle

Particulars Formula 2015 2014

Inventory holding

period

Inventory / Cost of

goods sold * 365

290 / 2058 *365 =

51.43 days

120 / 1505 *365 =

29.10 days

Average collection

period

Trade receivables /

sales revenue * 365

468 / 2630 * 365 =

64.95 days

253 / 2022 * 365 =

45.67 days

Average payable period Trade payables / Cost

of goods sold * 365

245 / 2058 *365 =

43.45 days

138 / 1505 *365 =

33.47 days

Operating cash cycle (Inventory holding

period + average

collection period) –

average payable period

(51.43 + 64.95) – 43.45

= 72.93 days

(29.10 + 45.67) -33.47

= 41.3 days

The above mentioned table shows that working capital of Elton Plc increased from 215 and

170. By considering such aspects it can be said that company's ability in relation to meeting the say

to day activities increased significantly. Further, payables of company decreased with the amount of

107 which is good indicator for the firm. Thus, it can be said that cash inflow was higher in 2015 as

compared to outflow.

Limitations of financial statements

8

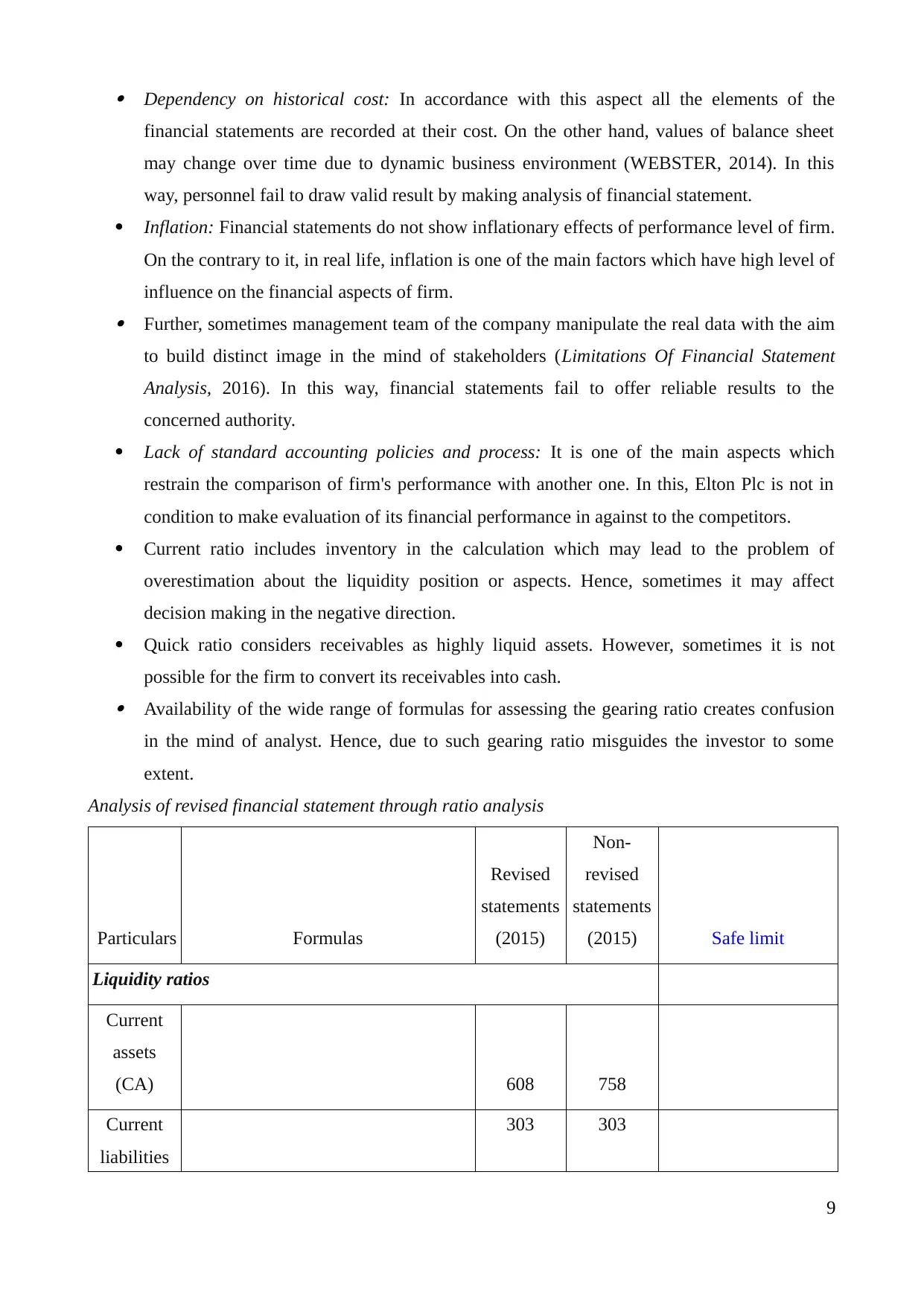

Dependency on historical cost: In accordance with this aspect all the elements of the

financial statements are recorded at their cost. On the other hand, values of balance sheet

may change over time due to dynamic business environment (WEBSTER, 2014). In this

way, personnel fail to draw valid result by making analysis of financial statement.

Inflation: Financial statements do not show inflationary effects of performance level of firm.

On the contrary to it, in real life, inflation is one of the main factors which have high level of

influence on the financial aspects of firm. Further, sometimes management team of the company manipulate the real data with the aim

to build distinct image in the mind of stakeholders (Limitations Of Financial Statement

Analysis, 2016). In this way, financial statements fail to offer reliable results to the

concerned authority.

Lack of standard accounting policies and process: It is one of the main aspects which

restrain the comparison of firm's performance with another one. In this, Elton Plc is not in

condition to make evaluation of its financial performance in against to the competitors.

Current ratio includes inventory in the calculation which may lead to the problem of

overestimation about the liquidity position or aspects. Hence, sometimes it may affect

decision making in the negative direction.

Quick ratio considers receivables as highly liquid assets. However, sometimes it is not

possible for the firm to convert its receivables into cash. Availability of the wide range of formulas for assessing the gearing ratio creates confusion

in the mind of analyst. Hence, due to such gearing ratio misguides the investor to some

extent.

Analysis of revised financial statement through ratio analysis

Particulars Formulas

Revised

statements

(2015)

Non-

revised

statements

(2015) Safe limit

Liquidity ratios

Current

assets

(CA) 608 758

Current

liabilities

303 303

9

financial statements are recorded at their cost. On the other hand, values of balance sheet

may change over time due to dynamic business environment (WEBSTER, 2014). In this

way, personnel fail to draw valid result by making analysis of financial statement.

Inflation: Financial statements do not show inflationary effects of performance level of firm.

On the contrary to it, in real life, inflation is one of the main factors which have high level of

influence on the financial aspects of firm. Further, sometimes management team of the company manipulate the real data with the aim

to build distinct image in the mind of stakeholders (Limitations Of Financial Statement

Analysis, 2016). In this way, financial statements fail to offer reliable results to the

concerned authority.

Lack of standard accounting policies and process: It is one of the main aspects which

restrain the comparison of firm's performance with another one. In this, Elton Plc is not in

condition to make evaluation of its financial performance in against to the competitors.

Current ratio includes inventory in the calculation which may lead to the problem of

overestimation about the liquidity position or aspects. Hence, sometimes it may affect

decision making in the negative direction.

Quick ratio considers receivables as highly liquid assets. However, sometimes it is not

possible for the firm to convert its receivables into cash. Availability of the wide range of formulas for assessing the gearing ratio creates confusion

in the mind of analyst. Hence, due to such gearing ratio misguides the investor to some

extent.

Analysis of revised financial statement through ratio analysis

Particulars Formulas

Revised

statements

(2015)

Non-

revised

statements

(2015) Safe limit

Liquidity ratios

Current

assets

(CA) 608 758

Current

liabilities

303 303

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

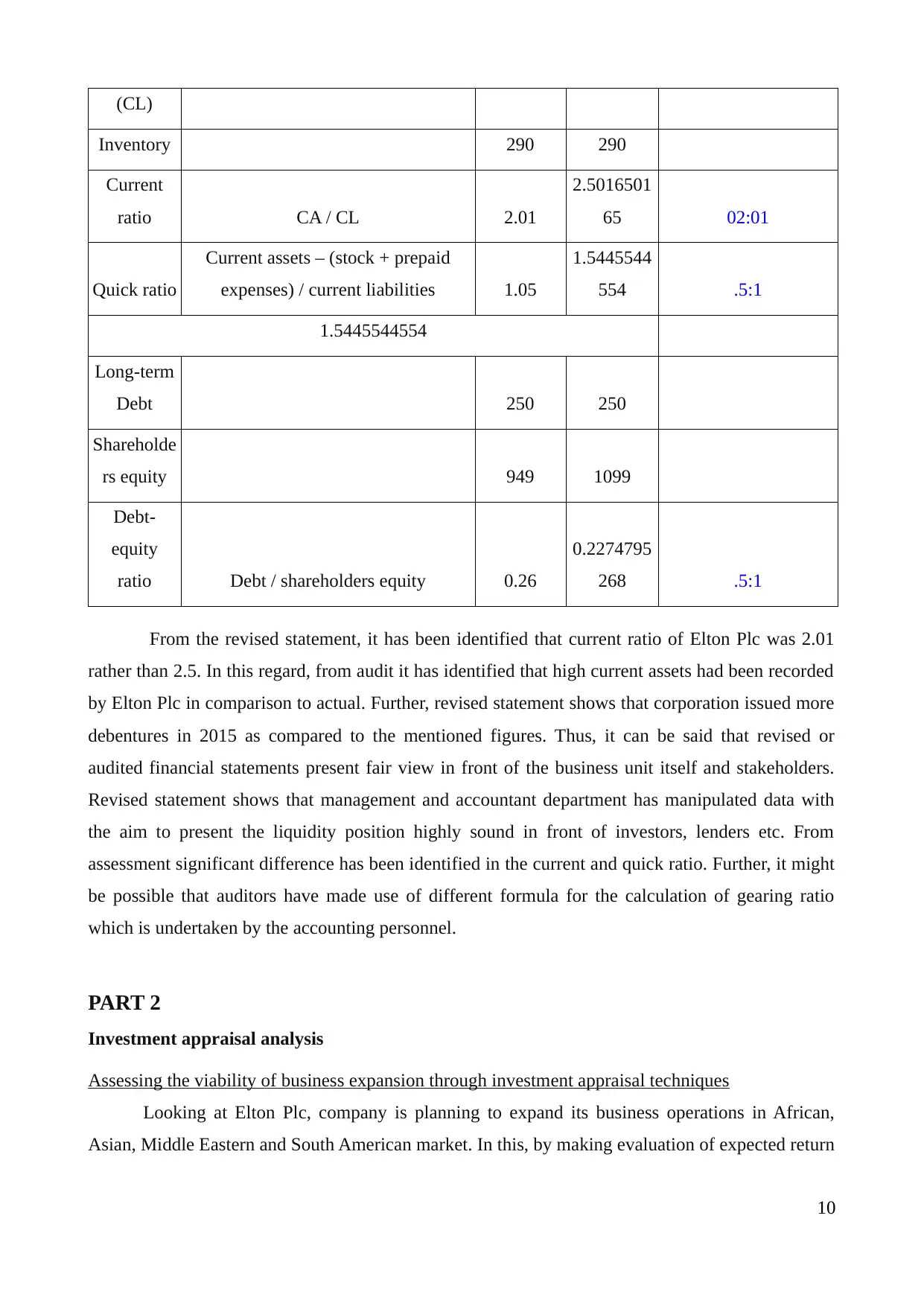

(CL)

Inventory 290 290

Current

ratio CA / CL 2.01

2.5016501

65 02:01

Quick ratio

Current assets – (stock + prepaid

expenses) / current liabilities 1.05

1.5445544

554 .5:1

1.5445544554

Long-term

Debt 250 250

Shareholde

rs equity 949 1099

Debt-

equity

ratio Debt / shareholders equity 0.26

0.2274795

268 .5:1

From the revised statement, it has been identified that current ratio of Elton Plc was 2.01

rather than 2.5. In this regard, from audit it has identified that high current assets had been recorded

by Elton Plc in comparison to actual. Further, revised statement shows that corporation issued more

debentures in 2015 as compared to the mentioned figures. Thus, it can be said that revised or

audited financial statements present fair view in front of the business unit itself and stakeholders.

Revised statement shows that management and accountant department has manipulated data with

the aim to present the liquidity position highly sound in front of investors, lenders etc. From

assessment significant difference has been identified in the current and quick ratio. Further, it might

be possible that auditors have made use of different formula for the calculation of gearing ratio

which is undertaken by the accounting personnel.

PART 2

Investment appraisal analysis

Assessing the viability of business expansion through investment appraisal techniques

Looking at Elton Plc, company is planning to expand its business operations in African,

Asian, Middle Eastern and South American market. In this, by making evaluation of expected return

10

Inventory 290 290

Current

ratio CA / CL 2.01

2.5016501

65 02:01

Quick ratio

Current assets – (stock + prepaid

expenses) / current liabilities 1.05

1.5445544

554 .5:1

1.5445544554

Long-term

Debt 250 250

Shareholde

rs equity 949 1099

Debt-

equity

ratio Debt / shareholders equity 0.26

0.2274795

268 .5:1

From the revised statement, it has been identified that current ratio of Elton Plc was 2.01

rather than 2.5. In this regard, from audit it has identified that high current assets had been recorded

by Elton Plc in comparison to actual. Further, revised statement shows that corporation issued more

debentures in 2015 as compared to the mentioned figures. Thus, it can be said that revised or

audited financial statements present fair view in front of the business unit itself and stakeholders.

Revised statement shows that management and accountant department has manipulated data with

the aim to present the liquidity position highly sound in front of investors, lenders etc. From

assessment significant difference has been identified in the current and quick ratio. Further, it might

be possible that auditors have made use of different formula for the calculation of gearing ratio

which is undertaken by the accounting personnel.

PART 2

Investment appraisal analysis

Assessing the viability of business expansion through investment appraisal techniques

Looking at Elton Plc, company is planning to expand its business operations in African,

Asian, Middle Eastern and South American market. In this, by making evaluation of expected return

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earned and level of expenses made finance personnel can assess the viability of project. In this, by

making comparison of the project in against to its life business entity can evaluate the extent to

which the proposed project will make contribution in the success in terms of financial aspects. Elton

Plc can evaluate the viability of expansion project or plan by taking into consideration the following

tools or techniques are:

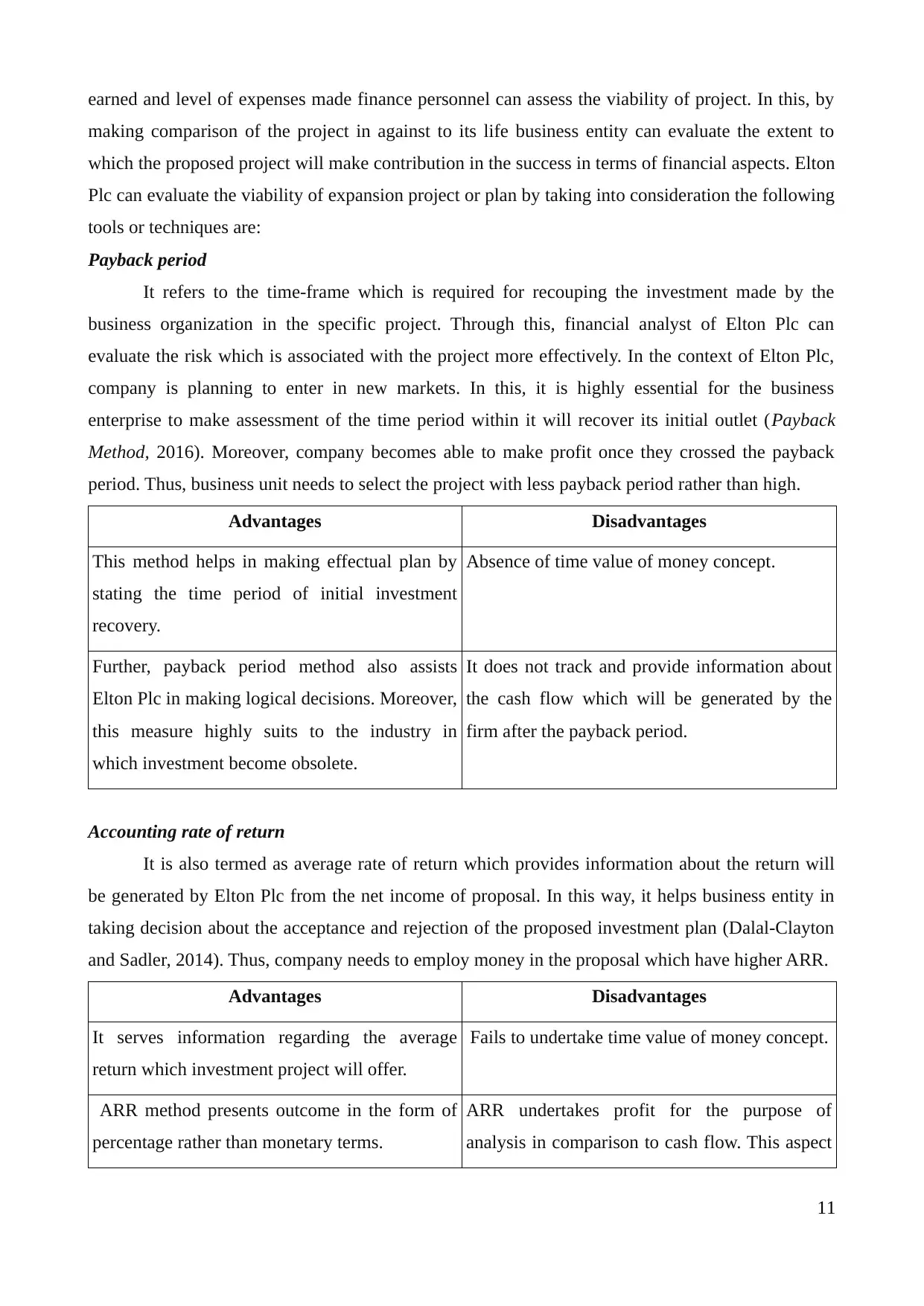

Payback period

It refers to the time-frame which is required for recouping the investment made by the

business organization in the specific project. Through this, financial analyst of Elton Plc can

evaluate the risk which is associated with the project more effectively. In the context of Elton Plc,

company is planning to enter in new markets. In this, it is highly essential for the business

enterprise to make assessment of the time period within it will recover its initial outlet (Payback

Method, 2016). Moreover, company becomes able to make profit once they crossed the payback

period. Thus, business unit needs to select the project with less payback period rather than high.

Advantages Disadvantages

This method helps in making effectual plan by

stating the time period of initial investment

recovery.

Absence of time value of money concept.

Further, payback period method also assists

Elton Plc in making logical decisions. Moreover,

this measure highly suits to the industry in

which investment become obsolete.

It does not track and provide information about

the cash flow which will be generated by the

firm after the payback period.

Accounting rate of return

It is also termed as average rate of return which provides information about the return will

be generated by Elton Plc from the net income of proposal. In this way, it helps business entity in

taking decision about the acceptance and rejection of the proposed investment plan (Dalal-Clayton

and Sadler, 2014). Thus, company needs to employ money in the proposal which have higher ARR.

Advantages Disadvantages

It serves information regarding the average

return which investment project will offer.

Fails to undertake time value of money concept.

ARR method presents outcome in the form of

percentage rather than monetary terms.

ARR undertakes profit for the purpose of

analysis in comparison to cash flow. This aspect

11

making comparison of the project in against to its life business entity can evaluate the extent to

which the proposed project will make contribution in the success in terms of financial aspects. Elton

Plc can evaluate the viability of expansion project or plan by taking into consideration the following

tools or techniques are:

Payback period

It refers to the time-frame which is required for recouping the investment made by the

business organization in the specific project. Through this, financial analyst of Elton Plc can

evaluate the risk which is associated with the project more effectively. In the context of Elton Plc,

company is planning to enter in new markets. In this, it is highly essential for the business

enterprise to make assessment of the time period within it will recover its initial outlet (Payback

Method, 2016). Moreover, company becomes able to make profit once they crossed the payback

period. Thus, business unit needs to select the project with less payback period rather than high.

Advantages Disadvantages

This method helps in making effectual plan by

stating the time period of initial investment

recovery.

Absence of time value of money concept.

Further, payback period method also assists

Elton Plc in making logical decisions. Moreover,

this measure highly suits to the industry in

which investment become obsolete.

It does not track and provide information about

the cash flow which will be generated by the

firm after the payback period.

Accounting rate of return

It is also termed as average rate of return which provides information about the return will

be generated by Elton Plc from the net income of proposal. In this way, it helps business entity in

taking decision about the acceptance and rejection of the proposed investment plan (Dalal-Clayton

and Sadler, 2014). Thus, company needs to employ money in the proposal which have higher ARR.

Advantages Disadvantages

It serves information regarding the average

return which investment project will offer.

Fails to undertake time value of money concept.

ARR method presents outcome in the form of

percentage rather than monetary terms.

ARR undertakes profit for the purpose of

analysis in comparison to cash flow. This aspect

11

limits the significance of this method to the large

extent.

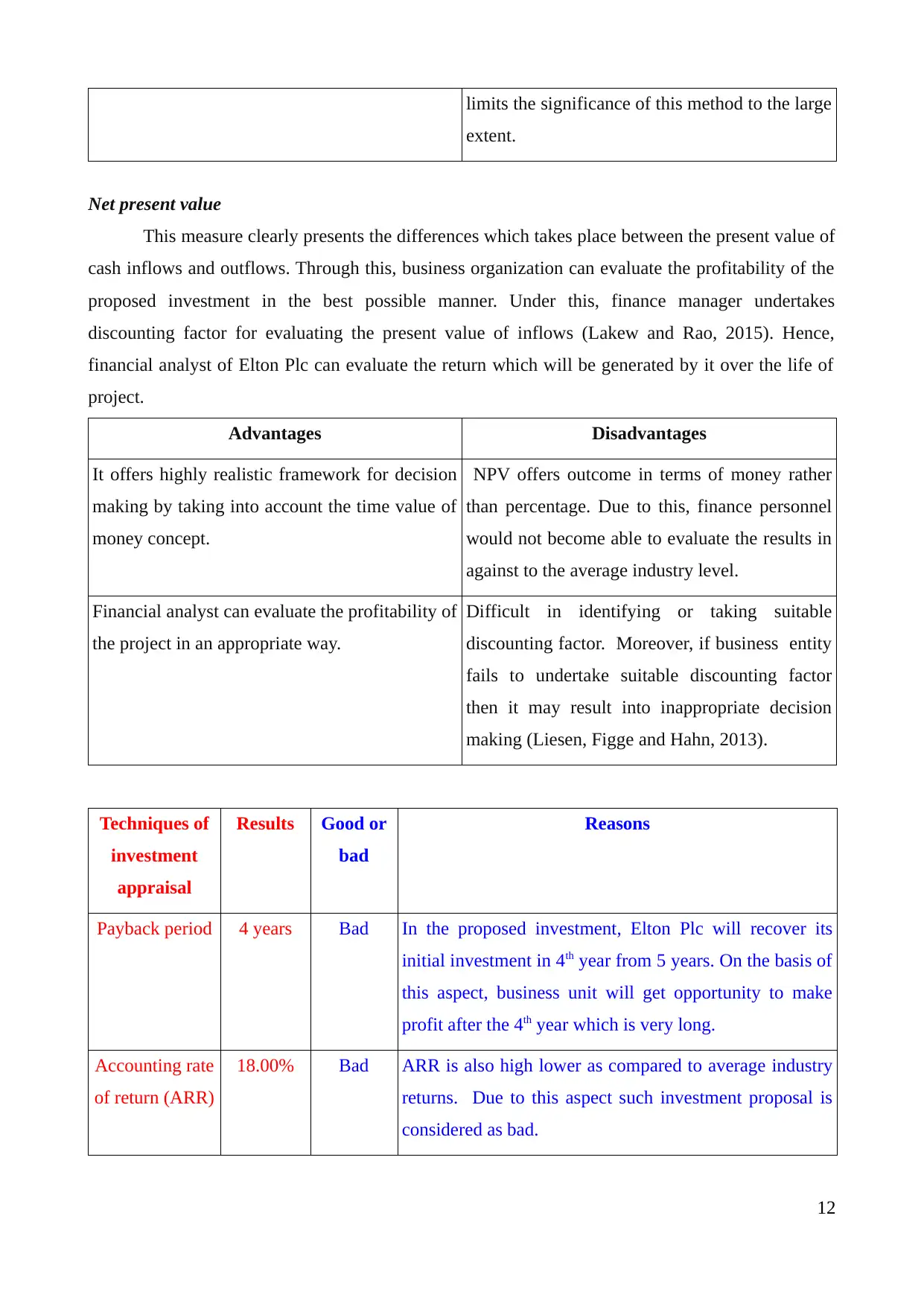

Net present value

This measure clearly presents the differences which takes place between the present value of

cash inflows and outflows. Through this, business organization can evaluate the profitability of the

proposed investment in the best possible manner. Under this, finance manager undertakes

discounting factor for evaluating the present value of inflows (Lakew and Rao, 2015). Hence,

financial analyst of Elton Plc can evaluate the return which will be generated by it over the life of

project.

Advantages Disadvantages

It offers highly realistic framework for decision

making by taking into account the time value of

money concept.

NPV offers outcome in terms of money rather

than percentage. Due to this, finance personnel

would not become able to evaluate the results in

against to the average industry level.

Financial analyst can evaluate the profitability of

the project in an appropriate way.

Difficult in identifying or taking suitable

discounting factor. Moreover, if business entity

fails to undertake suitable discounting factor

then it may result into inappropriate decision

making (Liesen, Figge and Hahn, 2013).

Techniques of

investment

appraisal

Results Good or

bad

Reasons

Payback period 4 years Bad In the proposed investment, Elton Plc will recover its

initial investment in 4th year from 5 years. On the basis of

this aspect, business unit will get opportunity to make

profit after the 4th year which is very long.

Accounting rate

of return (ARR)

18.00% Bad ARR is also high lower as compared to average industry

returns. Due to this aspect such investment proposal is

considered as bad.

12

extent.

Net present value

This measure clearly presents the differences which takes place between the present value of

cash inflows and outflows. Through this, business organization can evaluate the profitability of the

proposed investment in the best possible manner. Under this, finance manager undertakes

discounting factor for evaluating the present value of inflows (Lakew and Rao, 2015). Hence,

financial analyst of Elton Plc can evaluate the return which will be generated by it over the life of

project.

Advantages Disadvantages

It offers highly realistic framework for decision

making by taking into account the time value of

money concept.

NPV offers outcome in terms of money rather

than percentage. Due to this, finance personnel

would not become able to evaluate the results in

against to the average industry level.

Financial analyst can evaluate the profitability of

the project in an appropriate way.

Difficult in identifying or taking suitable

discounting factor. Moreover, if business entity

fails to undertake suitable discounting factor

then it may result into inappropriate decision

making (Liesen, Figge and Hahn, 2013).

Techniques of

investment

appraisal

Results Good or

bad

Reasons

Payback period 4 years Bad In the proposed investment, Elton Plc will recover its

initial investment in 4th year from 5 years. On the basis of

this aspect, business unit will get opportunity to make

profit after the 4th year which is very long.

Accounting rate

of return (ARR)

18.00% Bad ARR is also high lower as compared to average industry

returns. Due to this aspect such investment proposal is

considered as bad.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.