Financial Accounting Problem Set #1: Burberry, Accruals, Revenue

VerifiedAdded on 2020/12/09

|13

|1932

|235

Homework Assignment

AI Summary

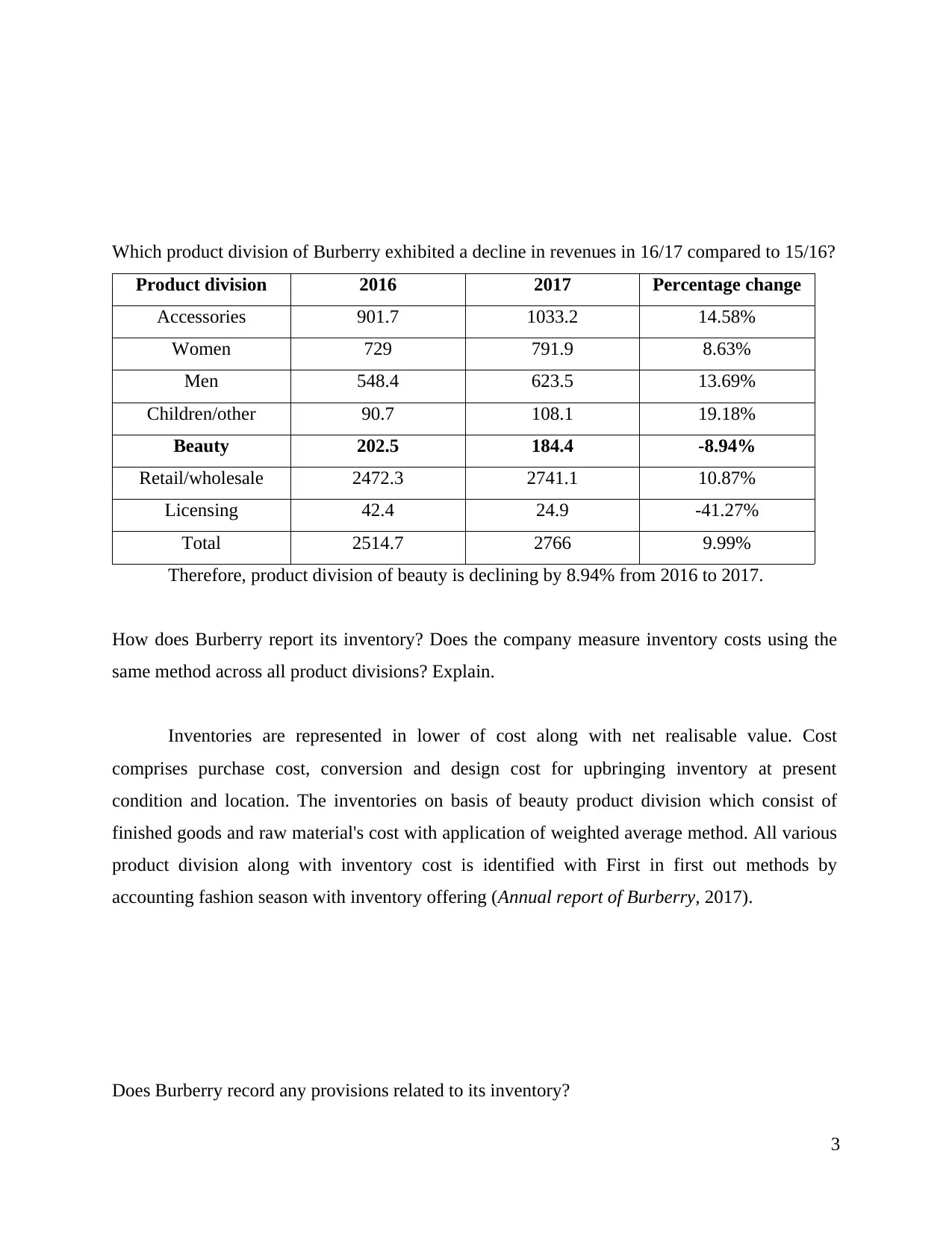

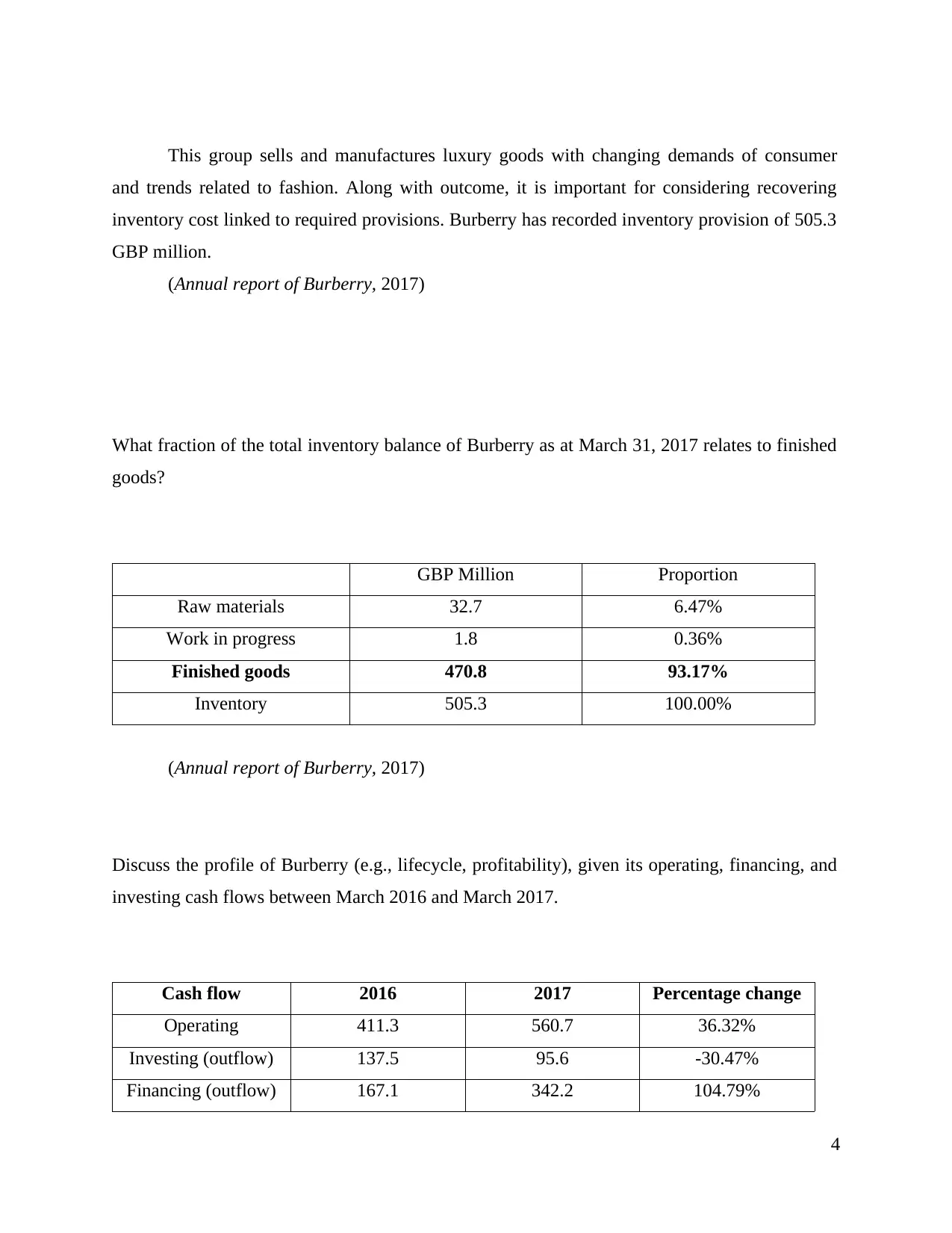

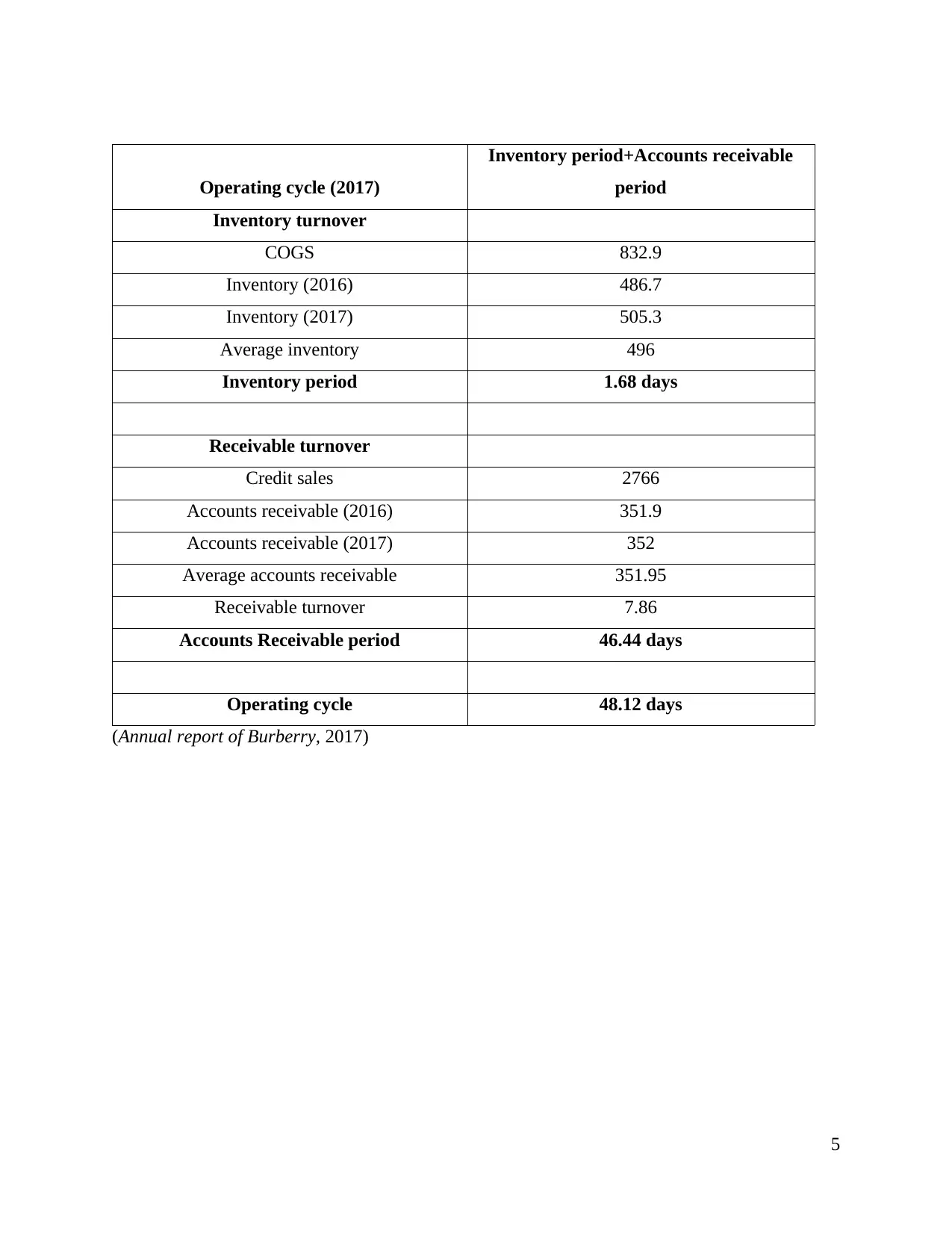

This financial accounting problem set analyzes Burberry's financial statements, focusing on accounts receivable, inventory, and revenue recognition. It examines Burberry's disclosure of receivables, bad debt expense, and inventory valuation methods. The assignment further explores accruals and earnings management through a case study involving Lamek Photography plc, discussing the impact of accounting manipulations. Finally, the problem set delves into long-term revenue recognition using the percentage-of-completion method, applying it to a construction contract and comparing it to the completed contract method. The solution provides detailed calculations and answers, offering a comprehensive understanding of financial accounting principles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.