HI6026 Audit, Assurance & Compliance: Enhanced Auditor Reporting

VerifiedAdded on 2023/06/07

|10

|3429

|66

Report

AI Summary

This report examines the adoption of enhanced auditor reporting in Australia, focusing on key audit matters and compliance with independence requirements. It reviews an auditor's report from Wesfarmers Limited, analyzing non-audit services, auditor remuneration, and the role of the audit committee. Key audit matters such as impairment of non-current assets, supplier rebates, and accounting for acquisitions are discussed in detail, along with the audit procedures used to address them. The report also considers the responsibilities of both management and auditors, material subsequent events, and the effectiveness of material information disclosed. The analysis concludes with a discussion of follow-up questions for the auditor and an overall assessment of the enhanced reporting practices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

As the title of the report is enhanced auditor reporting, the whole report has been revolved

around the matters which have enhanced the value of the audit report being issued by the

company. The report has been framed with four major objectives. The first objective is to review

the report of the auditor annexed in the annual report of the company in detail. The second

objective is to differentiate between what type of services has been provided by the auditor

including non audit services. The third objective is to identify the key audit matters reported in

the auditor’s report and how the same have improved the quality of the auditor report. The last

objective is to ascertain whether the stakeholders shall invest in the company or not. With these

aims and objectives the report has been framed with different sections and chapters.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................2

DETAILS OF THE COMPANY.................................................................................................................3

AUDITOR COMPLIANCE WITH INDEPENDENCE REQUIREMENTS...............................................3

NON AUDIT SERVICES...........................................................................................................................4

ANALYSIS OF AUDITORS REMUNERATION......................................................................................4

KEY AUDIT MATTERS............................................................................................................................4

AUDIT COMMITTEE AND ITS CHARTER............................................................................................5

AUDIT OPINION.......................................................................................................................................7

DIFFERENCE IN AUDITORS AND MANAGEMENT’S RESPONSIBILITIES.....................................7

MATERIAL SUBSEQUENT EVENTS......................................................................................................7

EFFECTIVENESS OF MATERIAL INFORMATION..............................................................................7

MISSING MATERIAL INFORMATION...................................................................................................7

FOLLOW UP QUESTIONS FROM AUDITOR.........................................................................................8

CONCLUSION...........................................................................................................................................8

REFERENCES............................................................................................................................................8

APPENDICES.............................................................................................................................................9

As the title of the report is enhanced auditor reporting, the whole report has been revolved

around the matters which have enhanced the value of the audit report being issued by the

company. The report has been framed with four major objectives. The first objective is to review

the report of the auditor annexed in the annual report of the company in detail. The second

objective is to differentiate between what type of services has been provided by the auditor

including non audit services. The third objective is to identify the key audit matters reported in

the auditor’s report and how the same have improved the quality of the auditor report. The last

objective is to ascertain whether the stakeholders shall invest in the company or not. With these

aims and objectives the report has been framed with different sections and chapters.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................2

DETAILS OF THE COMPANY.................................................................................................................3

AUDITOR COMPLIANCE WITH INDEPENDENCE REQUIREMENTS...............................................3

NON AUDIT SERVICES...........................................................................................................................4

ANALYSIS OF AUDITORS REMUNERATION......................................................................................4

KEY AUDIT MATTERS............................................................................................................................4

AUDIT COMMITTEE AND ITS CHARTER............................................................................................5

AUDIT OPINION.......................................................................................................................................7

DIFFERENCE IN AUDITORS AND MANAGEMENT’S RESPONSIBILITIES.....................................7

MATERIAL SUBSEQUENT EVENTS......................................................................................................7

EFFECTIVENESS OF MATERIAL INFORMATION..............................................................................7

MISSING MATERIAL INFORMATION...................................................................................................7

FOLLOW UP QUESTIONS FROM AUDITOR.........................................................................................8

CONCLUSION...........................................................................................................................................8

REFERENCES............................................................................................................................................8

APPENDICES.............................................................................................................................................9

INTRODUCTION

The audit report has gained the importance for the last decade across the globe. The reason has

been the economic crisis that has occurred due to the sudden collapses of the businesses. The

major collapse has been due to the unreported accounting frauds and mismanagement of the

company. The audit report plays the very important role in every type of industry as it provides

the details of the working of the company and provides the factor on the basis of which the users

of the financial statements as well as the stakeholders takes the decision. For the purpose of this

report, the company – Wesfarmers Limited has been selected out of the ASX listed companies.

The report has started with the compliance of the auditor with the independence requirements

and identifying the nature of the non audit services provided during the year. Then the

remuneration of the auditor has been analysed with the percentage change and the key audit

matters as reported has been discussed in detail with respect to the audit procedures adopted to

substantiate the observation. Then the composition of the audit and risk committee so formed by

the company has been analysed and its charter has been analysed. The responsibilities of the

management and the auditor has been analysed in detail with regard to the financial report of the

company. Lastly the subsequent events and the material information if it has been reported or

unreported during the year have been analysed. Along with this, some questions have been

mentioned which are required to be asked from the auditor as for follow up from the earlier

years. The report has then ended up with the appropriate conclusion.

DETAILS OF THE COMPANY

The company has been into its existence for the last hundred plus years. It has come into

existence in the year of nineteen hundred and fourteen and as the cooperative society of farmers.

The company has its headquarters in the country of Australia and is into the retail sector and has

the chain of departmental stores offering different type of products namely home improvement,

chemicals, office supplies, fertilizers and safety products and coal. At the starting of its business

the company has kept its main motive as to give the return to the shareholders at its satisfaction.

The company is the Australia’s largest retail chain employing more than two lacs employees and

having the base of the shareholder more than five lacs.

AUDITOR COMPLIANCE WITH INDEPENDENCE REQUIREMENTS

Yes, in accordance with the independent auditor’s report of the company, the auditor has

complied with the independence requirements. As per the provisions of the Corporations Act,

2001, the auditor is said to be independent if the following conditions are satisfied:

- He does not influence the policies of the company in relation to finance and operations.

- He does not participate in any manner in the activities relating to the business or

professional matter of the company (Knechel and Salterio, 2016).

The audit report has gained the importance for the last decade across the globe. The reason has

been the economic crisis that has occurred due to the sudden collapses of the businesses. The

major collapse has been due to the unreported accounting frauds and mismanagement of the

company. The audit report plays the very important role in every type of industry as it provides

the details of the working of the company and provides the factor on the basis of which the users

of the financial statements as well as the stakeholders takes the decision. For the purpose of this

report, the company – Wesfarmers Limited has been selected out of the ASX listed companies.

The report has started with the compliance of the auditor with the independence requirements

and identifying the nature of the non audit services provided during the year. Then the

remuneration of the auditor has been analysed with the percentage change and the key audit

matters as reported has been discussed in detail with respect to the audit procedures adopted to

substantiate the observation. Then the composition of the audit and risk committee so formed by

the company has been analysed and its charter has been analysed. The responsibilities of the

management and the auditor has been analysed in detail with regard to the financial report of the

company. Lastly the subsequent events and the material information if it has been reported or

unreported during the year have been analysed. Along with this, some questions have been

mentioned which are required to be asked from the auditor as for follow up from the earlier

years. The report has then ended up with the appropriate conclusion.

DETAILS OF THE COMPANY

The company has been into its existence for the last hundred plus years. It has come into

existence in the year of nineteen hundred and fourteen and as the cooperative society of farmers.

The company has its headquarters in the country of Australia and is into the retail sector and has

the chain of departmental stores offering different type of products namely home improvement,

chemicals, office supplies, fertilizers and safety products and coal. At the starting of its business

the company has kept its main motive as to give the return to the shareholders at its satisfaction.

The company is the Australia’s largest retail chain employing more than two lacs employees and

having the base of the shareholder more than five lacs.

AUDITOR COMPLIANCE WITH INDEPENDENCE REQUIREMENTS

Yes, in accordance with the independent auditor’s report of the company, the auditor has

complied with the independence requirements. As per the provisions of the Corporations Act,

2001, the auditor is said to be independent if the following conditions are satisfied:

- He does not influence the policies of the company in relation to finance and operations.

- He does not participate in any manner in the activities relating to the business or

professional matter of the company (Knechel and Salterio, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

- He does not have any form of the financial arrangement with the company in relation to

the accounting and the auditing practice other than the professional fees which is not

dependent on the profits or sales of the company (Beetham, 2004).

The auditor of the company – Ernst and Young has not deviated from the independence and has

issued the audit report in an unbiased and an independent manner.

NON AUDIT SERVICES

Yes, the audit firm has provided the non audit services. The total amount of non audit services

which have been obtained is $2307 thousands. The nature of the services is related to the

compliance and other matters in relation to the tax and the other matters which is neither linked

with the audit nor linked with the services which lead them to participate in the decision making

function of the company (Duncan and Whittington,2014).

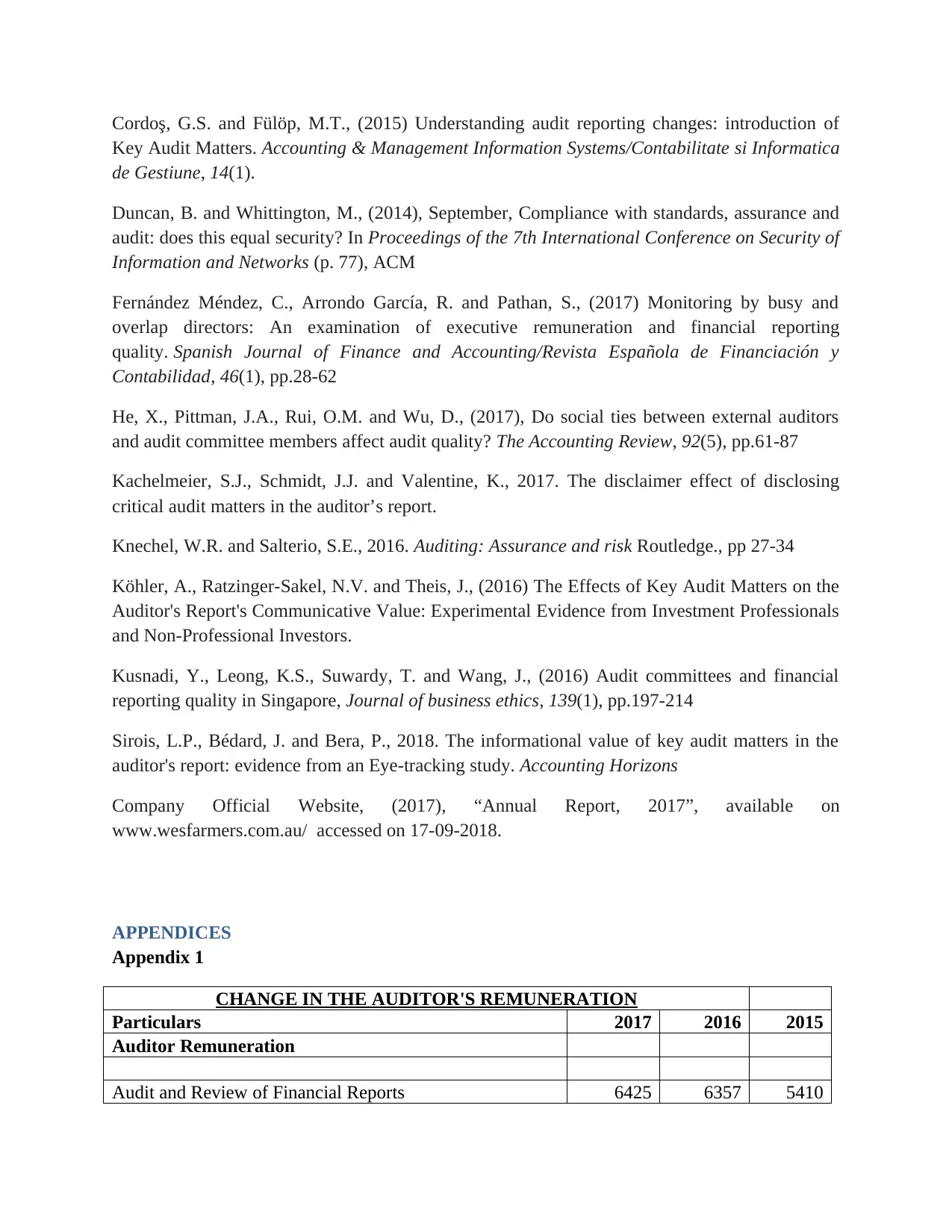

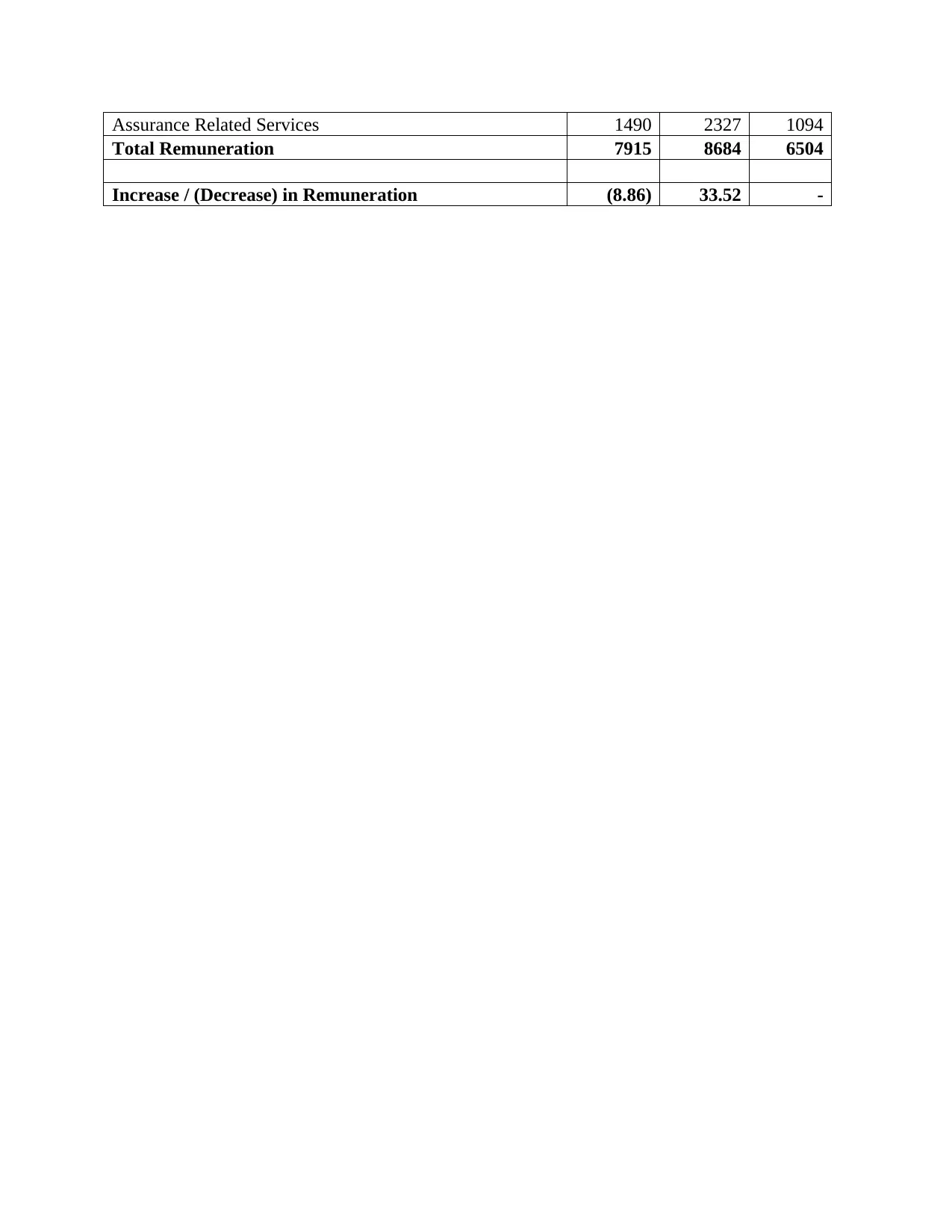

ANALYSIS OF AUDITORS REMUNERATION

As per Appendix 1 of the report, it has been observed that the auditor’s remuneration has been

increased by 33.52% in the year of 2016 as compared to the year of 2015 as the base and in the

subsequent year of 2017 the auditor’s remuneration has been decreased by 8.86%. The decreased

in the remuneration has been encountered by the auditor even when the company is in the profit

of $2873 million in the year of 2017 as compared to $407 millions in the year of 2016 and $2440

millions in the year of 2015. It shows that although the remuneration is not linked either with the

profits or with the sales but it is clear that the remuneration is being fluctuated and is not related

with the business done by the company during the audit.

KEY AUDIT MATTERS

Key audit matters are the matters which are mentioned in the auditor’s report separately and are

regarded as the most significant matter to be reported in the financial report. These matters

consist of only the manner in which auditor has addressed and accordingly the procedures have

been mentioned as to how they have preceded with the key audit matters. Following are the key

audit matters for the year ending 30th of June 2017:

1. Impairment of Non Current Assets including Intangible Assets – It has been selected as the

key audit matter because of the fact that the calculation and the identification of recoverable

amounts of the property plant and equipment depends majorly on the judgment adopted by

the group and also it is regarded as the typical process which includes the application of

different assumptions and estimates (Köhler, Ratzinger-Sakel and Theis,2016). During the

year sensitiveness of the impairment calculation of Curragh has been considered as it is more

sensitive to the changes in the rate of discount and cash flows which has been forecasted

(Bédard, Gonthier, and Schatt,2014). The auditor has adopted the procedure of checking the

feasibility of the assumptions made by the company with regard to the rate of discount, rate

the accounting and the auditing practice other than the professional fees which is not

dependent on the profits or sales of the company (Beetham, 2004).

The auditor of the company – Ernst and Young has not deviated from the independence and has

issued the audit report in an unbiased and an independent manner.

NON AUDIT SERVICES

Yes, the audit firm has provided the non audit services. The total amount of non audit services

which have been obtained is $2307 thousands. The nature of the services is related to the

compliance and other matters in relation to the tax and the other matters which is neither linked

with the audit nor linked with the services which lead them to participate in the decision making

function of the company (Duncan and Whittington,2014).

ANALYSIS OF AUDITORS REMUNERATION

As per Appendix 1 of the report, it has been observed that the auditor’s remuneration has been

increased by 33.52% in the year of 2016 as compared to the year of 2015 as the base and in the

subsequent year of 2017 the auditor’s remuneration has been decreased by 8.86%. The decreased

in the remuneration has been encountered by the auditor even when the company is in the profit

of $2873 million in the year of 2017 as compared to $407 millions in the year of 2016 and $2440

millions in the year of 2015. It shows that although the remuneration is not linked either with the

profits or with the sales but it is clear that the remuneration is being fluctuated and is not related

with the business done by the company during the audit.

KEY AUDIT MATTERS

Key audit matters are the matters which are mentioned in the auditor’s report separately and are

regarded as the most significant matter to be reported in the financial report. These matters

consist of only the manner in which auditor has addressed and accordingly the procedures have

been mentioned as to how they have preceded with the key audit matters. Following are the key

audit matters for the year ending 30th of June 2017:

1. Impairment of Non Current Assets including Intangible Assets – It has been selected as the

key audit matter because of the fact that the calculation and the identification of recoverable

amounts of the property plant and equipment depends majorly on the judgment adopted by

the group and also it is regarded as the typical process which includes the application of

different assumptions and estimates (Köhler, Ratzinger-Sakel and Theis,2016). During the

year sensitiveness of the impairment calculation of Curragh has been considered as it is more

sensitive to the changes in the rate of discount and cash flows which has been forecasted

(Bédard, Gonthier, and Schatt,2014). The auditor has adopted the procedure of checking the

feasibility of the assumptions made by the company with regard to the rate of discount, rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of growth, foreign exchange rate and more importantly the determination of the cash

generating units. It exhibits that the auditor has adopted substantive and compliance

procedures and also have taken the view of the third party by engaging the valuation

specialists.

2. Supplier Rebates – These are the benefits received from the suppliers and the company treats

the same as commission income in the financial report. It has been selected as the key audit

matter because of the reason that the income recognized during the year is very high and

there are number of factors which affects the correct amount of recognition (Sirois, Bédard

and Bera, 2018). These are terms for rebate, timing when it will be recognized, nature of the

income and its compliance and consideration with the accounting standards. The auditor has

adopted the substantive procedures which includes understanding of each of the income,

testing the terms of the supplier agreement whether the same is being followed or not,

checking the design and effectiveness of the internal controls placed in this regard and the

checking and verifying the credits if any has been given by the suppliers (Cordoş and Fülöp,

2015).

3. Accounting of Home base Acquisition – It has been regarded as the last key audit matters

due to the fact of having the huge size of the acquisition and the management judgment used

in analyzing and determining the fair value of the associated assets and liabilities. At first the

auditor has appointed and involved the valuation and the tax specialists for assessing the

value. Then the key judgments and the assumptions involved have been verified. Thus, the

auditor has adopted the substantive procedures and the test of transactions (Kachelmeier,

Schmidt and Valentine, 2017).

AUDIT COMMITTEE AND ITS CHARTER

Yes, the company has the audit committee. There are two non executive directors on the audit

committee. Its composition is as follows:

- Tony Howarth – Independent Director and Chairman of the Audit committee.

- Diane Smith Gander

- Jennifer Westacott

Yes, the company has the audit committee charter. Following are the main points relating to the

charter:

- Structure – As per Clause 2 of the charter, the audit committee shall comprise of the

directors which are non executive, shall be at least three members, the majority of the

members shall be of independent directors who can exercise their judgment

independently and the members shall have the necessary and requisite knowledge and

generating units. It exhibits that the auditor has adopted substantive and compliance

procedures and also have taken the view of the third party by engaging the valuation

specialists.

2. Supplier Rebates – These are the benefits received from the suppliers and the company treats

the same as commission income in the financial report. It has been selected as the key audit

matter because of the reason that the income recognized during the year is very high and

there are number of factors which affects the correct amount of recognition (Sirois, Bédard

and Bera, 2018). These are terms for rebate, timing when it will be recognized, nature of the

income and its compliance and consideration with the accounting standards. The auditor has

adopted the substantive procedures which includes understanding of each of the income,

testing the terms of the supplier agreement whether the same is being followed or not,

checking the design and effectiveness of the internal controls placed in this regard and the

checking and verifying the credits if any has been given by the suppliers (Cordoş and Fülöp,

2015).

3. Accounting of Home base Acquisition – It has been regarded as the last key audit matters

due to the fact of having the huge size of the acquisition and the management judgment used

in analyzing and determining the fair value of the associated assets and liabilities. At first the

auditor has appointed and involved the valuation and the tax specialists for assessing the

value. Then the key judgments and the assumptions involved have been verified. Thus, the

auditor has adopted the substantive procedures and the test of transactions (Kachelmeier,

Schmidt and Valentine, 2017).

AUDIT COMMITTEE AND ITS CHARTER

Yes, the company has the audit committee. There are two non executive directors on the audit

committee. Its composition is as follows:

- Tony Howarth – Independent Director and Chairman of the Audit committee.

- Diane Smith Gander

- Jennifer Westacott

Yes, the company has the audit committee charter. Following are the main points relating to the

charter:

- Structure – As per Clause 2 of the charter, the audit committee shall comprise of the

directors which are non executive, shall be at least three members, the majority of the

members shall be of independent directors who can exercise their judgment

independently and the members shall have the necessary and requisite knowledge and

skills with accounting and financial expertise in order to serve the purpose and the

objective of the formation of the committee effectively (Badolato, Donelson and Ege,

2014). One major requirement for the structure is that at least one member shall have the

qualification and experience relating to the respective field. The chairman of the

committee is duly appointed by the board.

- Functions and Responsibilities – The major function of the committee is to assist the

board of the company in the matters relating to the finalization of the financial report and

also assist in setting the parameters wherein the different kinds of risk can be estimated

and judged and accordingly the necessary actions can be taken. There are five major

responsibilities of the committee. These are as follows:

o Integrity of financial statements and reporting – it reviews the financial statements

and recommends the board to approve the draft of the annual and the interim if

any financial statements and other related information which are likely to be

disclosed at the Australian Stock Exchange and for the benefit of the stakeholders.

It also includes the reviewing of the policies and procedures for maintaining the

effectiveness and efficiency of the reporting system of the company. It also

reviews the material changes in any accounting or reporting requirements so as to

assess any effect of the same in the financial statements under consideration

(Fernández, Arrondo, and Pathan, 2017).

o Engagement with external auditors – Its next responsibility is to maintain relation

with the external auditors of the company and assessee whether they are

effectively discharging their duties and responsibilities or not. It reviews and

discusses the findings and the observations of the external auditors and takes

decision on the same.

o Internal controls and risk management – It is considered as the major

responsibility as it helps the board in assessing the internal controls that are

present in the organization and informs the board whether it has been designed

correctly and operating effectively of nor. Along with this it also assists the board

in assessing the risk in different areas and the ways to manage the same (Kusnadi,

Leong, Suwardy and Wang, 2016).

o Internal Audit – At first it approves the charter of the internal audit function and

then includes the resources in the internal audit function, approves its budget and

reviews its functions and the reports on the regular basis. It establishes the level of

relation that the internal audit function is liable to maintain with the external

auditors of the company (He, Pittman, Rui and Wu, 2017).

o Legal and Regulatory Compliance – First of all it reviews and assesses the

effectiveness of the compliance program of the company under which all the

compliances are checked and verified on the regular basis. Internal processes of

the group are checked and ensured that it meets the policies and procedures

maintained by the group.

objective of the formation of the committee effectively (Badolato, Donelson and Ege,

2014). One major requirement for the structure is that at least one member shall have the

qualification and experience relating to the respective field. The chairman of the

committee is duly appointed by the board.

- Functions and Responsibilities – The major function of the committee is to assist the

board of the company in the matters relating to the finalization of the financial report and

also assist in setting the parameters wherein the different kinds of risk can be estimated

and judged and accordingly the necessary actions can be taken. There are five major

responsibilities of the committee. These are as follows:

o Integrity of financial statements and reporting – it reviews the financial statements

and recommends the board to approve the draft of the annual and the interim if

any financial statements and other related information which are likely to be

disclosed at the Australian Stock Exchange and for the benefit of the stakeholders.

It also includes the reviewing of the policies and procedures for maintaining the

effectiveness and efficiency of the reporting system of the company. It also

reviews the material changes in any accounting or reporting requirements so as to

assess any effect of the same in the financial statements under consideration

(Fernández, Arrondo, and Pathan, 2017).

o Engagement with external auditors – Its next responsibility is to maintain relation

with the external auditors of the company and assessee whether they are

effectively discharging their duties and responsibilities or not. It reviews and

discusses the findings and the observations of the external auditors and takes

decision on the same.

o Internal controls and risk management – It is considered as the major

responsibility as it helps the board in assessing the internal controls that are

present in the organization and informs the board whether it has been designed

correctly and operating effectively of nor. Along with this it also assists the board

in assessing the risk in different areas and the ways to manage the same (Kusnadi,

Leong, Suwardy and Wang, 2016).

o Internal Audit – At first it approves the charter of the internal audit function and

then includes the resources in the internal audit function, approves its budget and

reviews its functions and the reports on the regular basis. It establishes the level of

relation that the internal audit function is liable to maintain with the external

auditors of the company (He, Pittman, Rui and Wu, 2017).

o Legal and Regulatory Compliance – First of all it reviews and assesses the

effectiveness of the compliance program of the company under which all the

compliances are checked and verified on the regular basis. Internal processes of

the group are checked and ensured that it meets the policies and procedures

maintained by the group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

o Other necessary areas – It reviews and assess the adequacy of the insurance policy

if any taken for the key managerial personnel, holds separate sessions with the

chief financial officer and senior management officials to discuss any important

matters with them and includes any other activity which the committee is required

to undertake on the request of the board.

AUDIT OPINION

The audit opinion issued by the auditor is unqualified. The auditor’s opinion states that the

financial report of the group is in accordance with the provisions of the Corporations Act 2001

and represents the true and fair view of the financial position and the financial performance.

DIFFERENCE IN AUDITORS AND MANAGEMENT’S RESPONSIBILITIES

The responsibilities of the auditor and the directors and management are different. Auditor has

the responsibility of issuing the opinion only on the financial report of the company as to

whether it represents the true and fair view of the financial health and the financial performance

of the company. Secondly auditor is liable to obtain the reasonable assurance that the financial

report as a whole is free from the material misstatement and free from error. It identifies the risk

of material misstatement and obtains the necessary understanding of the internal control and

evaluates the appropriateness of the accounting policies used and applied.

On the other side, the management responsibility is of the preparation of the financial report

which shall give the true and fair view in accordance with the Australian Accounting Standards

and the Corporations Act 2001 and secondly for the internal controls which helps in the

preparation of the financial report. The third responsibility is for assessing the ability of the

group to continue the company as ongoing concern basis.

MATERIAL SUBSEQUENT EVENTS

There is no material subsequent event for the period under consideration.

EFFECTIVENESS OF MATERIAL INFORMATION

As the third party stakeholder, the material information contained in the financial report is

effective and useful as all the necessary information has been embedded in the financial

statements of the company. The matters which requires the attention of the management of the

company has been mentioned as the key audit matters.

if any taken for the key managerial personnel, holds separate sessions with the

chief financial officer and senior management officials to discuss any important

matters with them and includes any other activity which the committee is required

to undertake on the request of the board.

AUDIT OPINION

The audit opinion issued by the auditor is unqualified. The auditor’s opinion states that the

financial report of the group is in accordance with the provisions of the Corporations Act 2001

and represents the true and fair view of the financial position and the financial performance.

DIFFERENCE IN AUDITORS AND MANAGEMENT’S RESPONSIBILITIES

The responsibilities of the auditor and the directors and management are different. Auditor has

the responsibility of issuing the opinion only on the financial report of the company as to

whether it represents the true and fair view of the financial health and the financial performance

of the company. Secondly auditor is liable to obtain the reasonable assurance that the financial

report as a whole is free from the material misstatement and free from error. It identifies the risk

of material misstatement and obtains the necessary understanding of the internal control and

evaluates the appropriateness of the accounting policies used and applied.

On the other side, the management responsibility is of the preparation of the financial report

which shall give the true and fair view in accordance with the Australian Accounting Standards

and the Corporations Act 2001 and secondly for the internal controls which helps in the

preparation of the financial report. The third responsibility is for assessing the ability of the

group to continue the company as ongoing concern basis.

MATERIAL SUBSEQUENT EVENTS

There is no material subsequent event for the period under consideration.

EFFECTIVENESS OF MATERIAL INFORMATION

As the third party stakeholder, the material information contained in the financial report is

effective and useful as all the necessary information has been embedded in the financial

statements of the company. The matters which requires the attention of the management of the

company has been mentioned as the key audit matters.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MISSING MATERIAL INFORMATION

There is no missing information which is material for the presentation of the financial statements

of the company.

FOLLOW UP QUESTIONS FROM AUDITOR

Following questions have been asked from the auditor of the company as follow up:

- Whether the accounting policy so adopted is in consistent with the earlier years.

- Whether the accounting policies so adopted commensurate the nature of business of the

company.

- Whether the Internal controls are effective in relation to the risks identified by the

company.

CONCLUSION

The report has analysed the annual report of the company – Wesfarmers Limited for the year

ending 30th of June 2017. The major focus has been on the points relating to the auditor and its

independence and the observations mentioned in the auditor’s report. The report has majorly

framed on three aspects – key audit matters, audit committee and audit opinion. All three aspects

have been discussed in detail. Light has also been thrown on the audit committee charter and

finds it very important for the effective functioning of the finance operations. In order to

conclude the report, the financial report of the company is detailed and exhaustive and the

company is complying with the rules and regulations as prescribed by the Corporations Act 2001

and Australian accounting standards and also the company is regularly estimating the risks and

vulnerabilities and the ways to manage and mitigate the same.

REFERENCES

Badolato, P.G., Donelson, D.C. and Ege, M., (2014), Audit committee financial expertise and

earnings management: The role of status, Journal of Accounting and Economics, 58(2-3),

pp.208-230

Bédard, J., Gonthier-Besacier, N. and Schatt, A., (2014), January, Costs and benefits of reporting

Key Audit Matters in the audit report: The French experience, In International Symposium on

Audit Research. Available at: http://documents. escdijon.

Eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT.

pdf.accessed on 17-09-2018

Beetham, D., (2004), Key principles and indices for a democratic audit, SAGE MODERN

POLITICS SERIES, 36, pp.25-25.

There is no missing information which is material for the presentation of the financial statements

of the company.

FOLLOW UP QUESTIONS FROM AUDITOR

Following questions have been asked from the auditor of the company as follow up:

- Whether the accounting policy so adopted is in consistent with the earlier years.

- Whether the accounting policies so adopted commensurate the nature of business of the

company.

- Whether the Internal controls are effective in relation to the risks identified by the

company.

CONCLUSION

The report has analysed the annual report of the company – Wesfarmers Limited for the year

ending 30th of June 2017. The major focus has been on the points relating to the auditor and its

independence and the observations mentioned in the auditor’s report. The report has majorly

framed on three aspects – key audit matters, audit committee and audit opinion. All three aspects

have been discussed in detail. Light has also been thrown on the audit committee charter and

finds it very important for the effective functioning of the finance operations. In order to

conclude the report, the financial report of the company is detailed and exhaustive and the

company is complying with the rules and regulations as prescribed by the Corporations Act 2001

and Australian accounting standards and also the company is regularly estimating the risks and

vulnerabilities and the ways to manage and mitigate the same.

REFERENCES

Badolato, P.G., Donelson, D.C. and Ege, M., (2014), Audit committee financial expertise and

earnings management: The role of status, Journal of Accounting and Economics, 58(2-3),

pp.208-230

Bédard, J., Gonthier-Besacier, N. and Schatt, A., (2014), January, Costs and benefits of reporting

Key Audit Matters in the audit report: The French experience, In International Symposium on

Audit Research. Available at: http://documents. escdijon.

Eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT.

pdf.accessed on 17-09-2018

Beetham, D., (2004), Key principles and indices for a democratic audit, SAGE MODERN

POLITICS SERIES, 36, pp.25-25.

Cordoş, G.S. and Fülöp, M.T., (2015) Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si Informatica

de Gestiune, 14(1).

Duncan, B. and Whittington, M., (2014), September, Compliance with standards, assurance and

audit: does this equal security? In Proceedings of the 7th International Conference on Security of

Information and Networks (p. 77), ACM

Fernández Méndez, C., Arrondo García, R. and Pathan, S., (2017) Monitoring by busy and

overlap directors: An examination of executive remuneration and financial reporting

quality. Spanish Journal of Finance and Accounting/Revista Española de Financiación y

Contabilidad, 46(1), pp.28-62

He, X., Pittman, J.A., Rui, O.M. and Wu, D., (2017), Do social ties between external auditors

and audit committee members affect audit quality? The Accounting Review, 92(5), pp.61-87

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk Routledge., pp 27-34

Köhler, A., Ratzinger-Sakel, N.V. and Theis, J., (2016) The Effects of Key Audit Matters on the

Auditor's Report's Communicative Value: Experimental Evidence from Investment Professionals

and Non-Professional Investors.

Kusnadi, Y., Leong, K.S., Suwardy, T. and Wang, J., (2016) Audit committees and financial

reporting quality in Singapore, Journal of business ethics, 139(1), pp.197-214

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: evidence from an Eye-tracking study. Accounting Horizons

Company Official Website, (2017), “Annual Report, 2017”, available on

www.wesfarmers.com.au/ accessed on 17-09-2018.

APPENDICES

Appendix 1

CHANGE IN THE AUDITOR'S REMUNERATION

Particulars 2017 2016 2015

Auditor Remuneration

Audit and Review of Financial Reports 6425 6357 5410

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si Informatica

de Gestiune, 14(1).

Duncan, B. and Whittington, M., (2014), September, Compliance with standards, assurance and

audit: does this equal security? In Proceedings of the 7th International Conference on Security of

Information and Networks (p. 77), ACM

Fernández Méndez, C., Arrondo García, R. and Pathan, S., (2017) Monitoring by busy and

overlap directors: An examination of executive remuneration and financial reporting

quality. Spanish Journal of Finance and Accounting/Revista Española de Financiación y

Contabilidad, 46(1), pp.28-62

He, X., Pittman, J.A., Rui, O.M. and Wu, D., (2017), Do social ties between external auditors

and audit committee members affect audit quality? The Accounting Review, 92(5), pp.61-87

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk Routledge., pp 27-34

Köhler, A., Ratzinger-Sakel, N.V. and Theis, J., (2016) The Effects of Key Audit Matters on the

Auditor's Report's Communicative Value: Experimental Evidence from Investment Professionals

and Non-Professional Investors.

Kusnadi, Y., Leong, K.S., Suwardy, T. and Wang, J., (2016) Audit committees and financial

reporting quality in Singapore, Journal of business ethics, 139(1), pp.197-214

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: evidence from an Eye-tracking study. Accounting Horizons

Company Official Website, (2017), “Annual Report, 2017”, available on

www.wesfarmers.com.au/ accessed on 17-09-2018.

APPENDICES

Appendix 1

CHANGE IN THE AUDITOR'S REMUNERATION

Particulars 2017 2016 2015

Auditor Remuneration

Audit and Review of Financial Reports 6425 6357 5410

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assurance Related Services 1490 2327 1094

Total Remuneration 7915 8684 6504

Increase / (Decrease) in Remuneration (8.86) 33.52 -

Total Remuneration 7915 8684 6504

Increase / (Decrease) in Remuneration (8.86) 33.52 -

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.