ACC3TAX S1 2018: Comprehensive Taxation Law Analysis of Emily Baff

VerifiedAdded on 2023/06/12

|7

|977

|244

Report

AI Summary

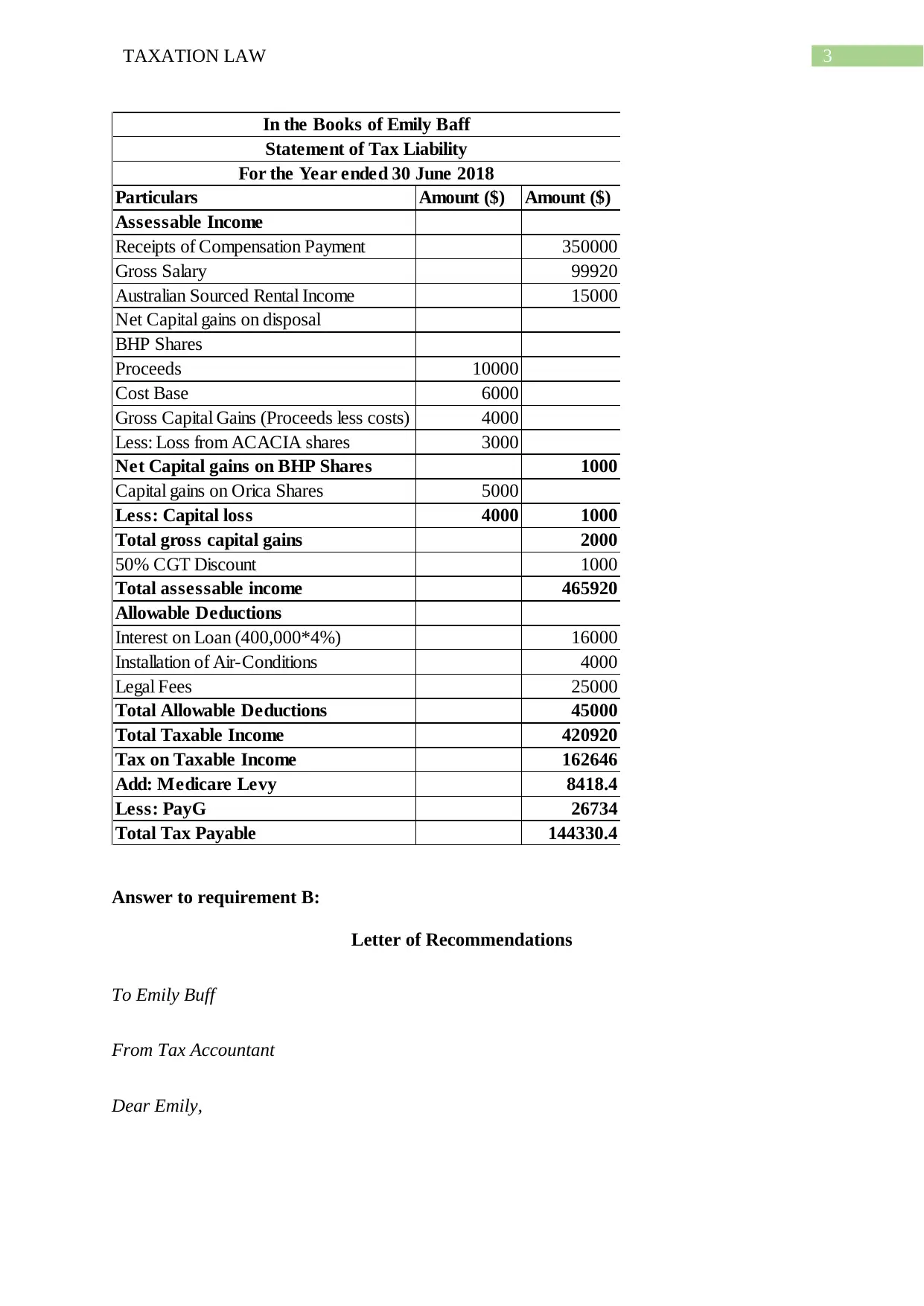

This report provides a detailed analysis of Emily Baff's tax liability for the year ended 30th June 2018. It examines her assessable income, including salary, rental income, and capital gains, and identifies allowable deductions such as interest on loans and legal fees. The report also addresses non-allowable deductions, like expenses for home mortgage payments and capital improvements to the rental property. Additionally, it includes a letter of recommendation addressing the tax implications of compensation payments and legal fees incurred from a lawsuit against her employer, referencing relevant sections of the ITAA 1997 and case law. The final calculation of Emily's taxable income is $420,920, with a total tax liability of $144,330.4.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.