Evaluation of Accounting Standards for Emission Allowances: A Report

VerifiedAdded on 2020/04/01

|15

|2666

|37

Report

AI Summary

This report provides a comprehensive evaluation of accounting standards and methods used for emission allowances. It addresses the absence of universally accepted standards and explores different accounting models, such as the intangible asset and inventory models, used to account for emission credits. The report includes examples of journal entries for emission allowances, illustrating how these transactions are recorded under various methods, including IAS38 and the revaluation model. It also examines the consequences of emission allowances on financial statements, including the balance sheet, income statement, and cash flow statement. The report highlights the impact on assets, liabilities, and income recognition, offering a detailed analysis of this increasingly important area of financial accounting. It concludes by summarizing the key findings and emphasizing the implications of emission allowances on environmental sustainability and financial reporting practices.

Name of student:

Registration number:

Unit Title:

Unit code:

Name of supervisor:

Date due:

Registration number:

Unit Title:

Unit code:

Name of supervisor:

Date due:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report evaluates the accounting standards and methods used to account for

emission allowances in companies. The increasing need for companies to be

environmentally stable has brought about a self regulatory mechanism known as

emission allowance. In this program, companies are paid for emitting less carbon into

the atmosphere. There are currently no universally accepted standards and method of

accounting for this item. There exist different methods such as intangible asset

technique and the inventory model. This paper also evaluates how journal entries are

recorded for emission allowances. The examples and illustrations are given. The

consequences of emission allowances for balance sheet are that they have an influence

on assets and liabilities (Veith, 2010). It also affects the income statements since they

are sometimes recorded as expenses or revenue based on whether the company is

buying or selling the credits.

This report evaluates the accounting standards and methods used to account for

emission allowances in companies. The increasing need for companies to be

environmentally stable has brought about a self regulatory mechanism known as

emission allowance. In this program, companies are paid for emitting less carbon into

the atmosphere. There are currently no universally accepted standards and method of

accounting for this item. There exist different methods such as intangible asset

technique and the inventory model. This paper also evaluates how journal entries are

recorded for emission allowances. The examples and illustrations are given. The

consequences of emission allowances for balance sheet are that they have an influence

on assets and liabilities (Veith, 2010). It also affects the income statements since they

are sometimes recorded as expenses or revenue based on whether the company is

buying or selling the credits.

Table of Contents

Introduction............................................................................................................................................4

Nature of carbon allowances and justification........................................................................................4

Accounting for emission credits or allowances.......................................................................................5

Examples of emission allowance journal entries using various methods................................................7

Accounting for emissions using IAS38 model......................................................................................7

Accounting using the revaluation model.............................................................................................8

Consequences of emission allowances on financial statements...........................................................10

Conclusion.............................................................................................................................................11

References............................................................................................................................................ 13

Introduction............................................................................................................................................4

Nature of carbon allowances and justification........................................................................................4

Accounting for emission credits or allowances.......................................................................................5

Examples of emission allowance journal entries using various methods................................................7

Accounting for emissions using IAS38 model......................................................................................7

Accounting using the revaluation model.............................................................................................8

Consequences of emission allowances on financial statements...........................................................10

Conclusion.............................................................................................................................................11

References............................................................................................................................................ 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Currently, there are no universally accepted standards of accounting for emission

allowances in organizations. There is no accepted method of measuring and

recognizing emission allowances and this has created a misunderstanding on the

standards for accounting for this item in the financial report. However, this has not

prevented organizations from trading and developing carbon markets. Many countries

especially in Europe, South Korea, and Australia have made significant steps in trying

to set uniform emission allowance measurement standards for companies in their

countries (Skjrseth & Eikeland, 2013). The definitions given by the Global accounting

standards body indicates that carbon allowances should be treated as assets since they

are resource being controlled by the organization and they have economic value. A

proposal for revision on the regulation of financial instrumentsrecognizes emissions

as part of an organizations instruments of finance.(Fusaro & James, 2013). When it

comes to accounting, allowances from emissions are not treated as financial

instruments..

The report discusses the emission allowances and provides justification for the

discussions that follows. The report evaluates the measurement of emission

allowances and the journal entries for this transaction are entered to illustrate how the

instruments are accounted for. The final section of the report discusses the

consequences of allowances issued on emissions on the financial statements which

includes the balance sheet, income statement and the statement of cash flow.

Nature of carbon allowances and justification

The first reason European Commission has established that “classification of the

emission allowances for accounting reasons depends on the criteria set by recognized

accounting standards body only”(Perkins, 2011). Since no accounting standards body

Currently, there are no universally accepted standards of accounting for emission

allowances in organizations. There is no accepted method of measuring and

recognizing emission allowances and this has created a misunderstanding on the

standards for accounting for this item in the financial report. However, this has not

prevented organizations from trading and developing carbon markets. Many countries

especially in Europe, South Korea, and Australia have made significant steps in trying

to set uniform emission allowance measurement standards for companies in their

countries (Skjrseth & Eikeland, 2013). The definitions given by the Global accounting

standards body indicates that carbon allowances should be treated as assets since they

are resource being controlled by the organization and they have economic value. A

proposal for revision on the regulation of financial instrumentsrecognizes emissions

as part of an organizations instruments of finance.(Fusaro & James, 2013). When it

comes to accounting, allowances from emissions are not treated as financial

instruments..

The report discusses the emission allowances and provides justification for the

discussions that follows. The report evaluates the measurement of emission

allowances and the journal entries for this transaction are entered to illustrate how the

instruments are accounted for. The final section of the report discusses the

consequences of allowances issued on emissions on the financial statements which

includes the balance sheet, income statement and the statement of cash flow.

Nature of carbon allowances and justification

The first reason European Commission has established that “classification of the

emission allowances for accounting reasons depends on the criteria set by recognized

accounting standards body only”(Perkins, 2011). Since no accounting standards body

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has been able to put in place strategies to account for the emission allowances in

financial reports.

The U.S GAAP has established uniform systems of accounting which provides

guidance to companies to account for emission allowance. It provides that emission

allowances should be reported at historical cost and are classified as inventory in the

balance sheet. Allowances that are being bought are recorded at the buying price

while those received from EPA are recorded at zero price. Weighted average cost

method is recommended and the calculations should be done on a monthly.

The financial Accounting Standards Board (FASB) works hand in hand International

Accounting Standards Board (IASB) to solve the issue of accounting for carbon

emission schemes (Antes, Hansjürgens, & Letmathe, 2006) . In USA certain

companies mostly in the power and energy industries which are viewed as

contributing greatly to pollution are needed to engage in established programs on

emissions. The absence of a clearly defined strategy and methods for measuring the

emission credits has resulted to the rise of the following practices in various

industries; renewable energy certificates, emission offsets and credit on emissions.

Accounting for emission credits or allowances

In a survey conducted in USA for publicly registered companies with yearly revenues

of between $1.1 billion and $100 billion between Jan 2009 and September

2009(Taticchi,Carbone& Albino, 2013). Of all the companies registered in this

program, more than 29 companies indicated that they had an accounting policy related

to emission credits.

One of the models used in accounting for carbon emission allowances is intangible

assets accounting model. The company’s measure emission credits and allowances

financial reports.

The U.S GAAP has established uniform systems of accounting which provides

guidance to companies to account for emission allowance. It provides that emission

allowances should be reported at historical cost and are classified as inventory in the

balance sheet. Allowances that are being bought are recorded at the buying price

while those received from EPA are recorded at zero price. Weighted average cost

method is recommended and the calculations should be done on a monthly.

The financial Accounting Standards Board (FASB) works hand in hand International

Accounting Standards Board (IASB) to solve the issue of accounting for carbon

emission schemes (Antes, Hansjürgens, & Letmathe, 2006) . In USA certain

companies mostly in the power and energy industries which are viewed as

contributing greatly to pollution are needed to engage in established programs on

emissions. The absence of a clearly defined strategy and methods for measuring the

emission credits has resulted to the rise of the following practices in various

industries; renewable energy certificates, emission offsets and credit on emissions.

Accounting for emission credits or allowances

In a survey conducted in USA for publicly registered companies with yearly revenues

of between $1.1 billion and $100 billion between Jan 2009 and September

2009(Taticchi,Carbone& Albino, 2013). Of all the companies registered in this

program, more than 29 companies indicated that they had an accounting policy related

to emission credits.

One of the models used in accounting for carbon emission allowances is intangible

assets accounting model. The company’s measure emission credits and allowances

issued to them and bought in the market by comparing with the cost of emissions. If a

company is therefore issued with emission credits, it has a nominal zero cost. When a

company buys carbon credits, it has costs associated with them which are the buying

price of the carbon credits (Watchman, 2008). Under this technique, it is possible to

value emission credits that have been issued at a fair value immediately they are

received. Emission credits are subject to impairment under the intangible assets model

impairment model and the assets that are fixed model to the point of amortization of

the carbon credits (Newell, Boykoff & Boyd, 2012).

The carbon credits can also be accounted for under the inventory model. Under this

model, the emission credits are measured using the weighted-average cost. Emission

credits issued by relevant bodies in charge of carbon credits have zero costs attached

to them. Weighted average cost of carbon emissions for a particularly period of time

is valued by estimating the cost of fuel. Under this model, the emission allowances are

ranked as inventory in a company’s balance sheet and in the cash flow statements,

they are classified as operating activities.

The emission credits are also accounted as liability and gain recognition. In this, a

company does nor recognize the obligation to deliver carbon credits to concerned

bodies until the real level of carbon emissions for a particular period is more than the

credit recorded on the balance sheet. A gain is usually recognized in the period in

which the credits have been sold. Some companies however defers the income if the

emissions were given for a future vintage year and they happen to be sold in the

current year (Chen, Liu& Hua, 2013). The gain in this case is considered as not

realized since the company may fail to cover its emissions in the future vintage year

due to the credits sold in the previous year.

company is therefore issued with emission credits, it has a nominal zero cost. When a

company buys carbon credits, it has costs associated with them which are the buying

price of the carbon credits (Watchman, 2008). Under this technique, it is possible to

value emission credits that have been issued at a fair value immediately they are

received. Emission credits are subject to impairment under the intangible assets model

impairment model and the assets that are fixed model to the point of amortization of

the carbon credits (Newell, Boykoff & Boyd, 2012).

The carbon credits can also be accounted for under the inventory model. Under this

model, the emission credits are measured using the weighted-average cost. Emission

credits issued by relevant bodies in charge of carbon credits have zero costs attached

to them. Weighted average cost of carbon emissions for a particularly period of time

is valued by estimating the cost of fuel. Under this model, the emission allowances are

ranked as inventory in a company’s balance sheet and in the cash flow statements,

they are classified as operating activities.

The emission credits are also accounted as liability and gain recognition. In this, a

company does nor recognize the obligation to deliver carbon credits to concerned

bodies until the real level of carbon emissions for a particular period is more than the

credit recorded on the balance sheet. A gain is usually recognized in the period in

which the credits have been sold. Some companies however defers the income if the

emissions were given for a future vintage year and they happen to be sold in the

current year (Chen, Liu& Hua, 2013). The gain in this case is considered as not

realized since the company may fail to cover its emissions in the future vintage year

due to the credits sold in the previous year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

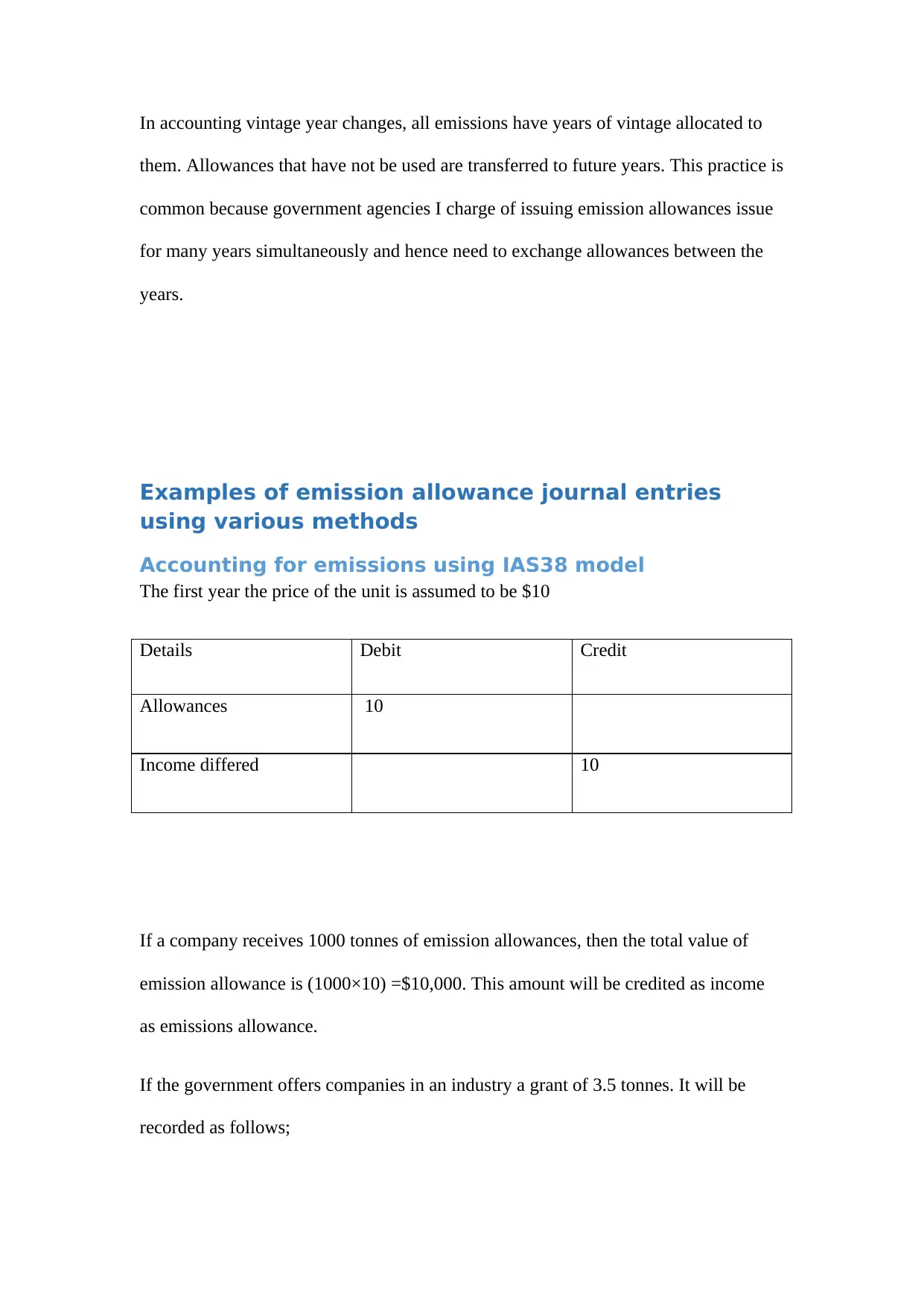

In accounting vintage year changes, all emissions have years of vintage allocated to

them. Allowances that have not be used are transferred to future years. This practice is

common because government agencies I charge of issuing emission allowances issue

for many years simultaneously and hence need to exchange allowances between the

years.

Examples of emission allowance journal entries

using various methods

Accounting for emissions using IAS38 model

The first year the price of the unit is assumed to be $10

Details Debit Credit

Allowances 10

Income differed 10

If a company receives 1000 tonnes of emission allowances, then the total value of

emission allowance is (1000×10) =$10,000. This amount will be credited as income

as emissions allowance.

If the government offers companies in an industry a grant of 3.5 tonnes. It will be

recorded as follows;

them. Allowances that have not be used are transferred to future years. This practice is

common because government agencies I charge of issuing emission allowances issue

for many years simultaneously and hence need to exchange allowances between the

years.

Examples of emission allowance journal entries

using various methods

Accounting for emissions using IAS38 model

The first year the price of the unit is assumed to be $10

Details Debit Credit

Allowances 10

Income differed 10

If a company receives 1000 tonnes of emission allowances, then the total value of

emission allowance is (1000×10) =$10,000. This amount will be credited as income

as emissions allowance.

If the government offers companies in an industry a grant of 3.5 tonnes. It will be

recorded as follows;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

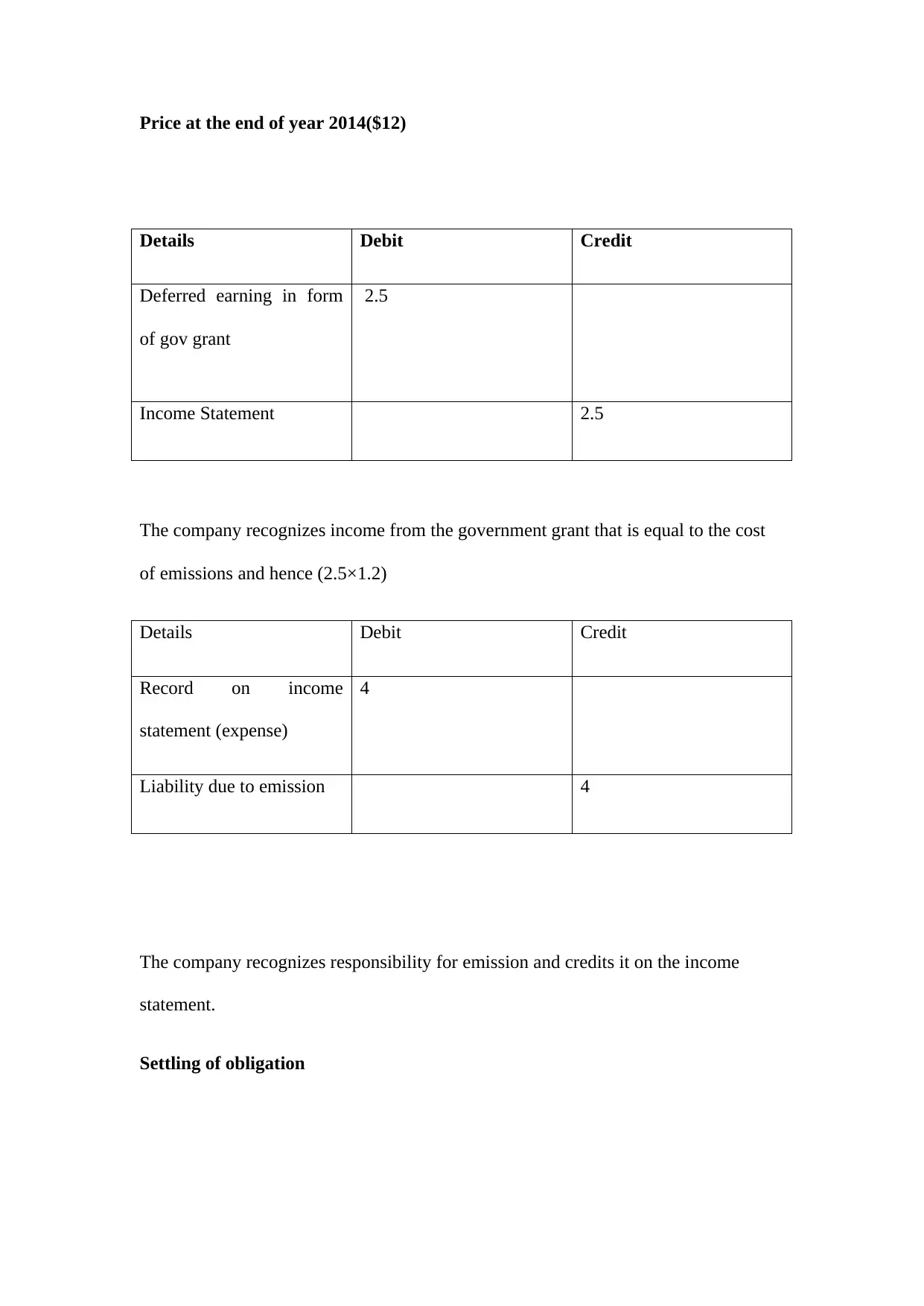

Price at the end of year 2014($12)

Details Debit Credit

Deferred earning in form

of gov grant

2.5

Income Statement 2.5

The company recognizes income from the government grant that is equal to the cost

of emissions and hence (2.5×1.2)

Details Debit Credit

Record on income

statement (expense)

4

Liability due to emission 4

The company recognizes responsibility for emission and credits it on the income

statement.

Settling of obligation

Details Debit Credit

Deferred earning in form

of gov grant

2.5

Income Statement 2.5

The company recognizes income from the government grant that is equal to the cost

of emissions and hence (2.5×1.2)

Details Debit Credit

Record on income

statement (expense)

4

Liability due to emission 4

The company recognizes responsibility for emission and credits it on the income

statement.

Settling of obligation

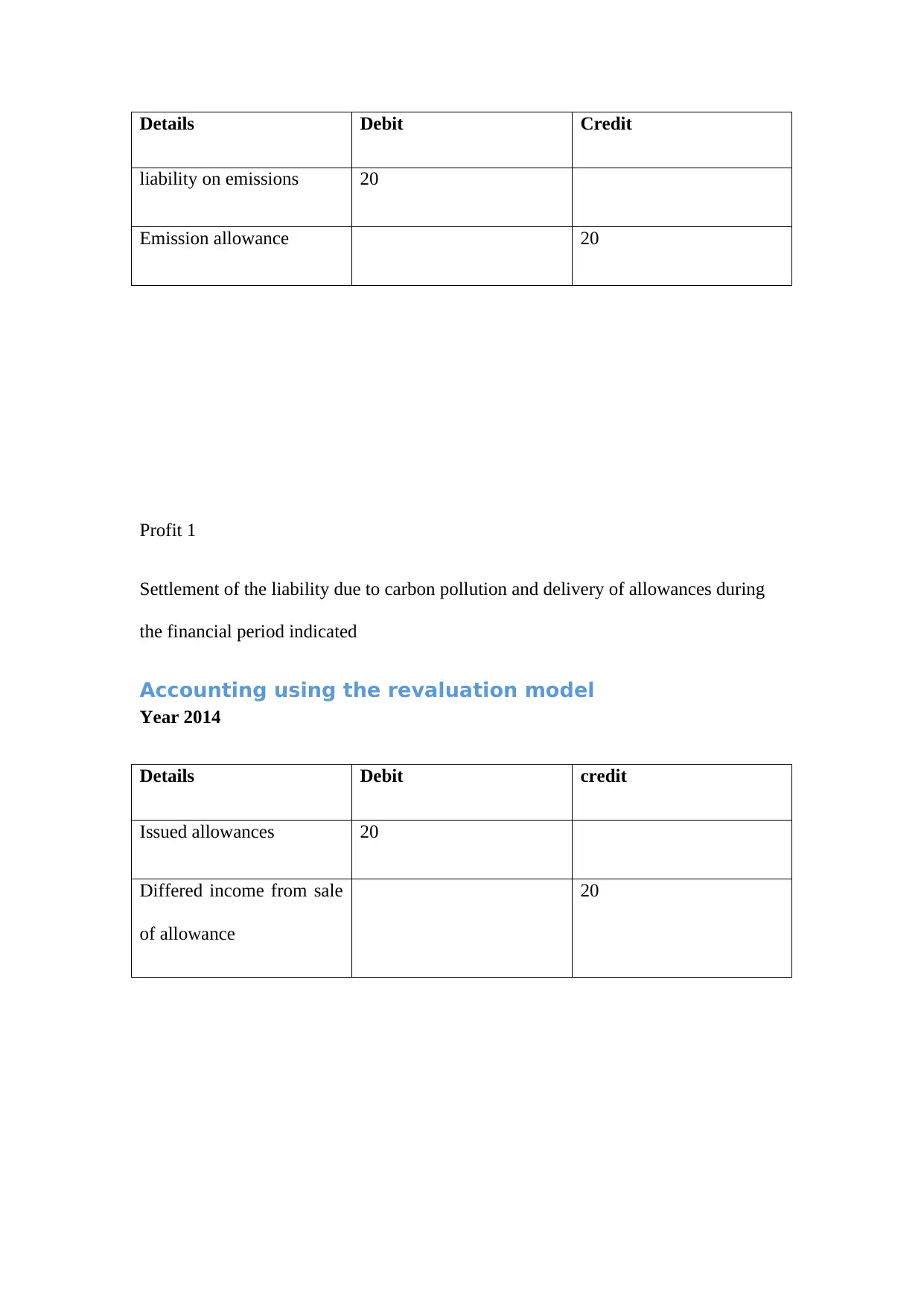

Details Debit Credit

liability on emissions 20

Emission allowance 20

Profit 1

Settlement of the liability due to carbon pollution and delivery of allowances during

the financial period indicated

Accounting using the revaluation model

Year 2014

Details Debit credit

Issued allowances 20

Differed income from sale

of allowance

20

liability on emissions 20

Emission allowance 20

Profit 1

Settlement of the liability due to carbon pollution and delivery of allowances during

the financial period indicated

Accounting using the revaluation model

Year 2014

Details Debit credit

Issued allowances 20

Differed income from sale

of allowance

20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

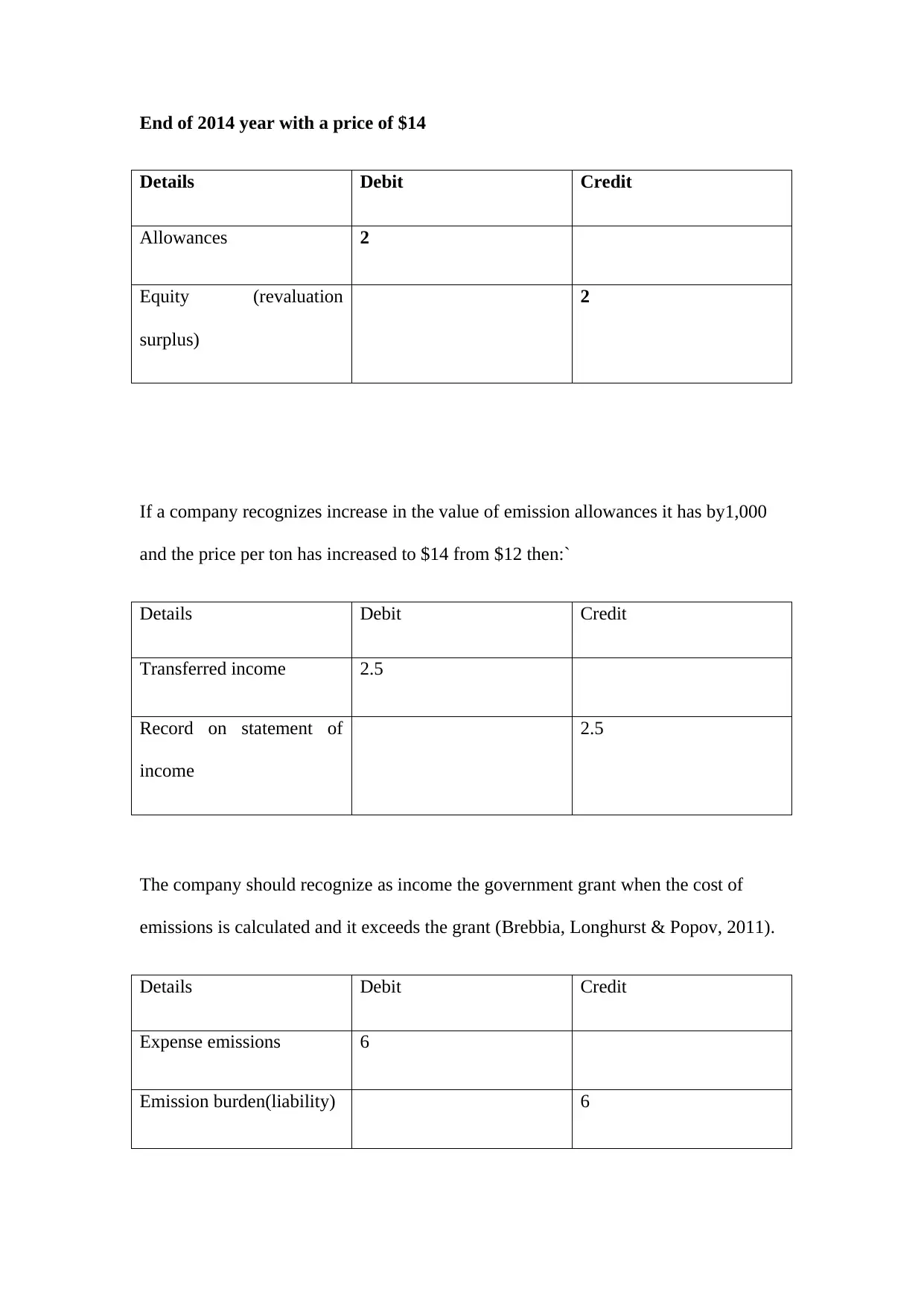

End of 2014 year with a price of $14

Details Debit Credit

Allowances 2

Equity (revaluation

surplus)

2

If a company recognizes increase in the value of emission allowances it has by1,000

and the price per ton has increased to $14 from $12 then:`

Details Debit Credit

Transferred income 2.5

Record on statement of

income

2.5

The company should recognize as income the government grant when the cost of

emissions is calculated and it exceeds the grant (Brebbia, Longhurst & Popov, 2011).

Details Debit Credit

Expense emissions 6

Emission burden(liability) 6

Details Debit Credit

Allowances 2

Equity (revaluation

surplus)

2

If a company recognizes increase in the value of emission allowances it has by1,000

and the price per ton has increased to $14 from $12 then:`

Details Debit Credit

Transferred income 2.5

Record on statement of

income

2.5

The company should recognize as income the government grant when the cost of

emissions is calculated and it exceeds the grant (Brebbia, Longhurst & Popov, 2011).

Details Debit Credit

Expense emissions 6

Emission burden(liability) 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company recognizes the burden for emission (4,000 ton /4 x 1= 1000 ton x €12

=€12000). The burden on emission in this case is calculated at fair value.

Consequences of emission allowances on financial

statements

The recording of emission allowances affects financial statement in various ways. The

first reason why they affect financial statements is that they may bring a new aspect in

the recording of financial information. The following is an evaluation of the

consequences of emission allowances on specific financial records:

Currently held emission allowances should be recorded as assets on the balance sheet.

This is because a company expects to derive future benefits from holding an

allowance since it will enable the company to produce high amount of GHG in the

production of goods and services (Bostan, 2009). Furthermore, a company may decide

to sell the allowance and generate cash which is an asset for the business.

A purchase of emission allowance by a company should be recorded as an allowance

asset. It increases the allowance asset and reduces the cash asset on the balance sheet.

If it is on credit, it increases accounts payable. When a company uses the emission

allowance by emitting the quantity of emission authorized, the allowance asset should

be decreased to indicate a reduction in an asset. A corresponding allowance expense

should be recorded to decrease net income in the income statement of the company.

This is listed as the cost of pollution in most income statements of companies.

Companies should make adjustments at the end of the year to the carrying value

=€12000). The burden on emission in this case is calculated at fair value.

Consequences of emission allowances on financial

statements

The recording of emission allowances affects financial statement in various ways. The

first reason why they affect financial statements is that they may bring a new aspect in

the recording of financial information. The following is an evaluation of the

consequences of emission allowances on specific financial records:

Currently held emission allowances should be recorded as assets on the balance sheet.

This is because a company expects to derive future benefits from holding an

allowance since it will enable the company to produce high amount of GHG in the

production of goods and services (Bostan, 2009). Furthermore, a company may decide

to sell the allowance and generate cash which is an asset for the business.

A purchase of emission allowance by a company should be recorded as an allowance

asset. It increases the allowance asset and reduces the cash asset on the balance sheet.

If it is on credit, it increases accounts payable. When a company uses the emission

allowance by emitting the quantity of emission authorized, the allowance asset should

be decreased to indicate a reduction in an asset. A corresponding allowance expense

should be recorded to decrease net income in the income statement of the company.

This is listed as the cost of pollution in most income statements of companies.

Companies should make adjustments at the end of the year to the carrying value

allowance asset accounts to bring it to the market value. Increase in price in the

market, the “Allowance asset” account should be increased by the change in

price(Daniel Lieberman, 2010).The equity account named “Unrealized gain on

Allowances” of the company should also be increased by same amount (Bonham &

Ernst & Young. 2008). When a company emits more carbon than its current

allowance held. It should be recorded as an accrued expense which is a liability for

the business. The company will then need to pay a fine or purchase additional carbon

credits.

Conclusion

The report evaluates and describes the subject of emissions allowances. Emissions

allowances is becoming popular means of ensuring environmental sustainability

through the counting of carbon foot prints which can then be sold to other producers.

This report evaluates the accounting methods used to account for emissions among

various companies in different countries. There are no universally accepted standards

on accounting for emission allowances and therefore the standards and accounting

practices in this regard. Some of the common and most popular methods used by

companies vary from country and a company has a choice on which accounting

methods to use in this regard. One of the models used in accounting for carbon

emission allowances is intangible assets accounting model. The company’s measure

emission credits and allowances issued to them and acquired in the market at cost and

this cost is assumed to be the value of the emissions for that accounting period. The

report analyzes the journal entries resulting from accounting for emissions and uses

examples to illustrate how the item is recorded in the financial statement. The

consequences of the emission allowances on the financial records is that they increase

the “emissions allowance account” when they are bought and in turn decrease the

market, the “Allowance asset” account should be increased by the change in

price(Daniel Lieberman, 2010).The equity account named “Unrealized gain on

Allowances” of the company should also be increased by same amount (Bonham &

Ernst & Young. 2008). When a company emits more carbon than its current

allowance held. It should be recorded as an accrued expense which is a liability for

the business. The company will then need to pay a fine or purchase additional carbon

credits.

Conclusion

The report evaluates and describes the subject of emissions allowances. Emissions

allowances is becoming popular means of ensuring environmental sustainability

through the counting of carbon foot prints which can then be sold to other producers.

This report evaluates the accounting methods used to account for emissions among

various companies in different countries. There are no universally accepted standards

on accounting for emission allowances and therefore the standards and accounting

practices in this regard. Some of the common and most popular methods used by

companies vary from country and a company has a choice on which accounting

methods to use in this regard. One of the models used in accounting for carbon

emission allowances is intangible assets accounting model. The company’s measure

emission credits and allowances issued to them and acquired in the market at cost and

this cost is assumed to be the value of the emissions for that accounting period. The

report analyzes the journal entries resulting from accounting for emissions and uses

examples to illustrate how the item is recorded in the financial statement. The

consequences of the emission allowances on the financial records is that they increase

the “emissions allowance account” when they are bought and in turn decrease the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.