Finance for Business: Financial Analysis of Emmerson Resources

VerifiedAdded on 2020/05/16

|17

|2700

|63

Report

AI Summary

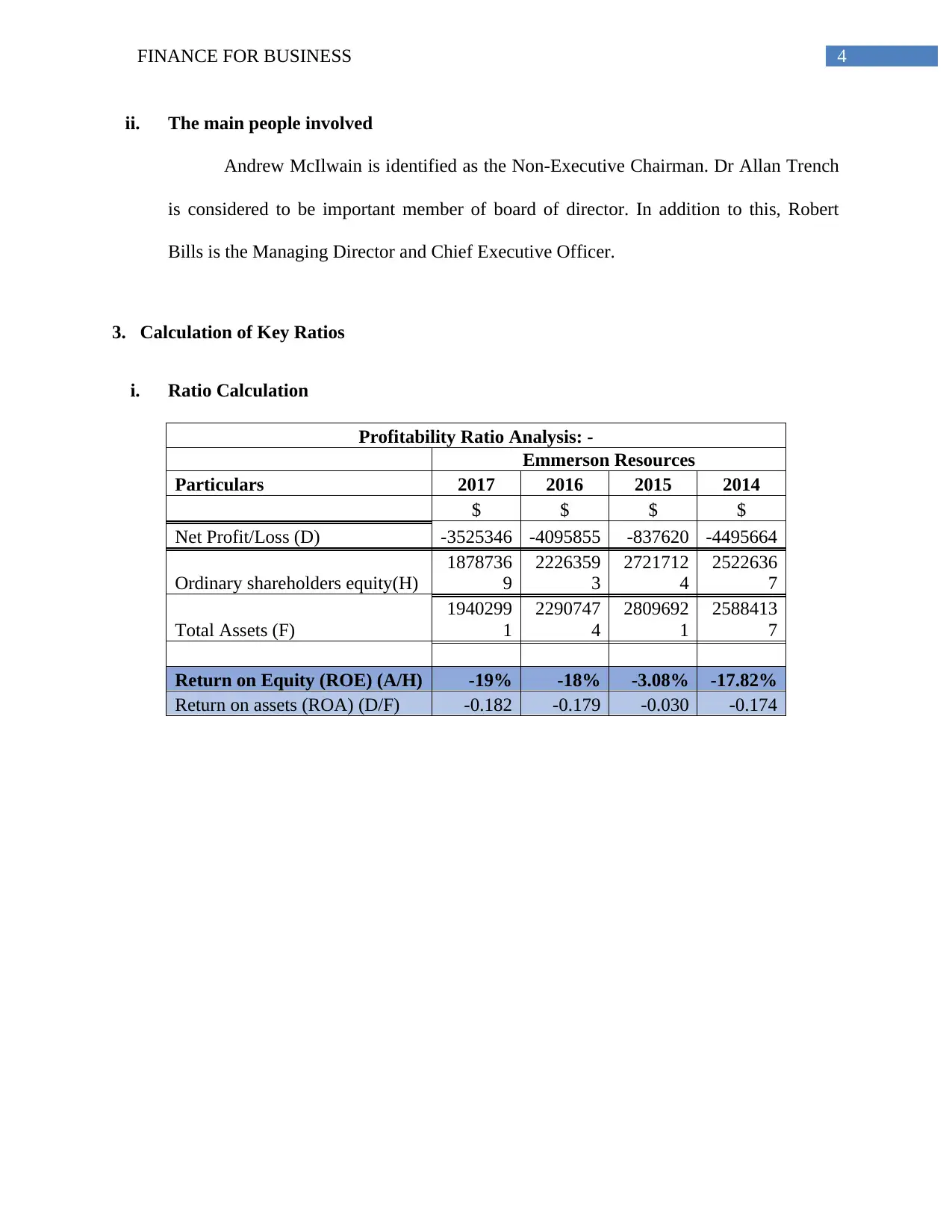

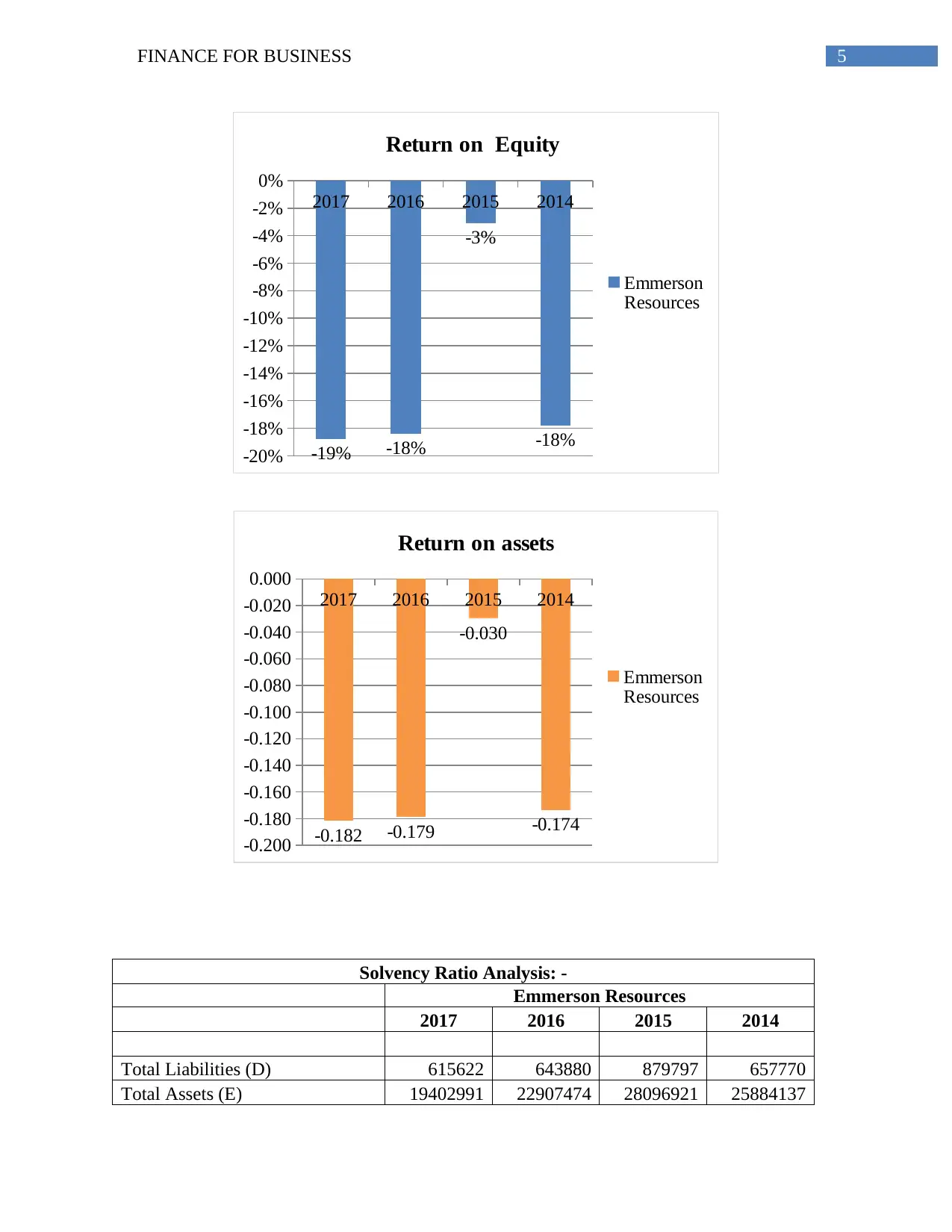

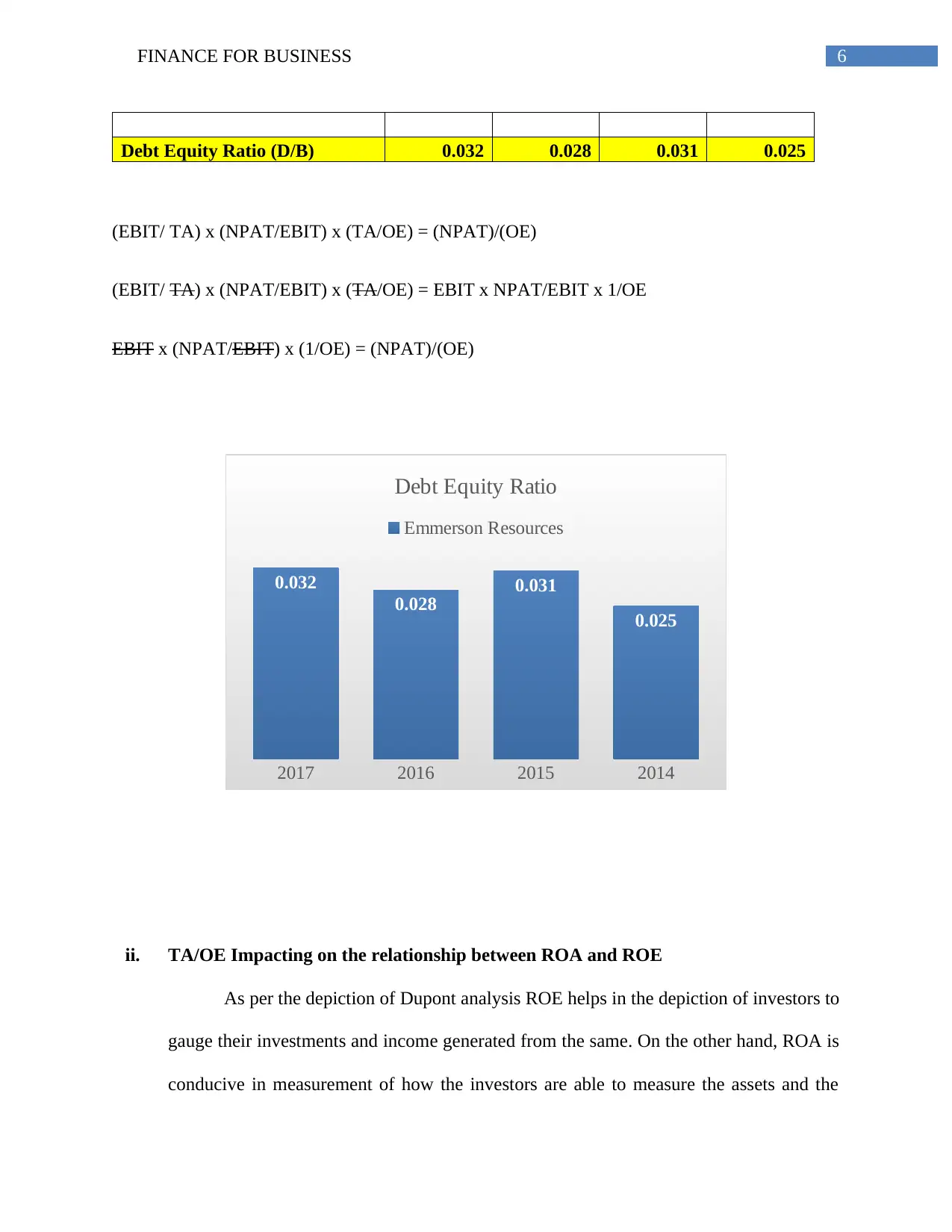

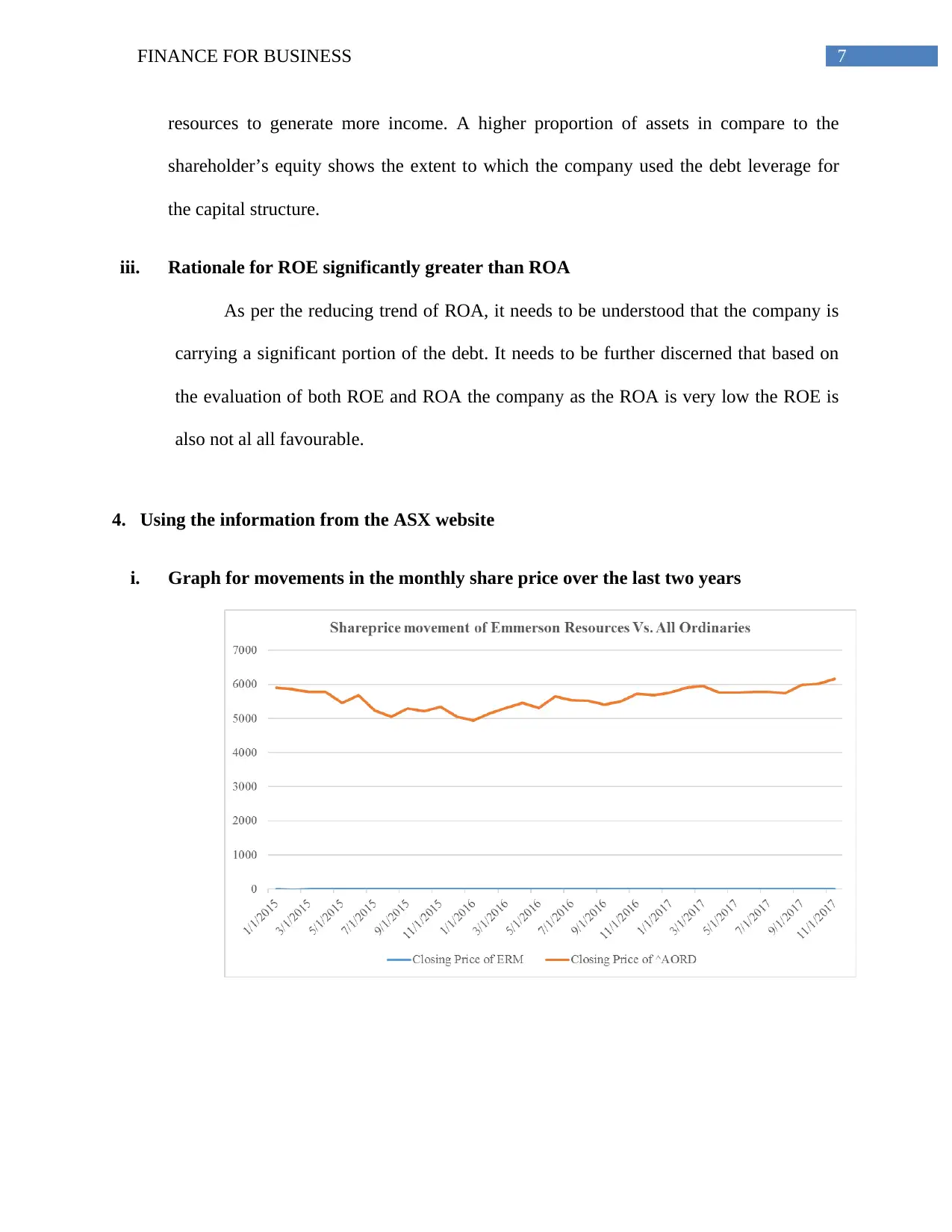

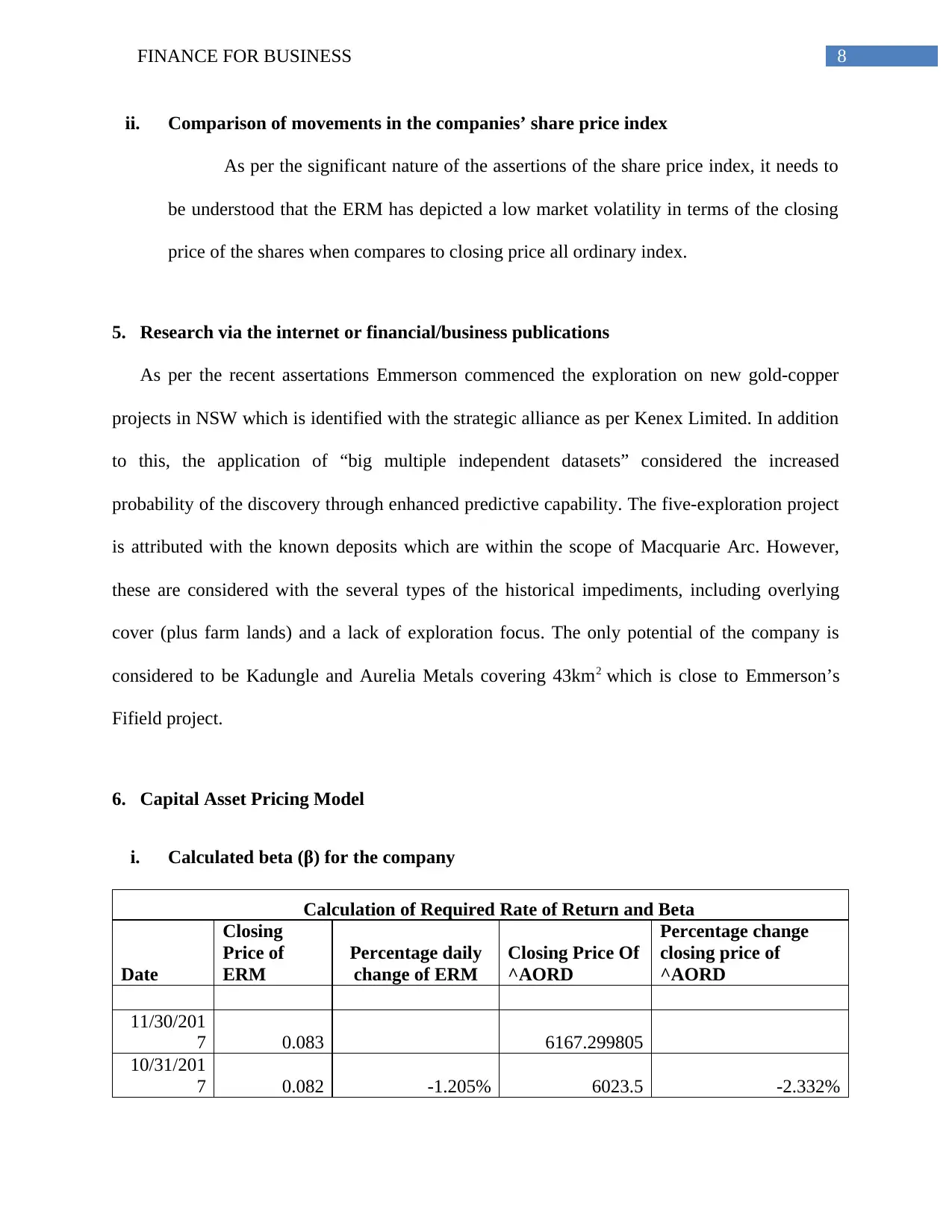

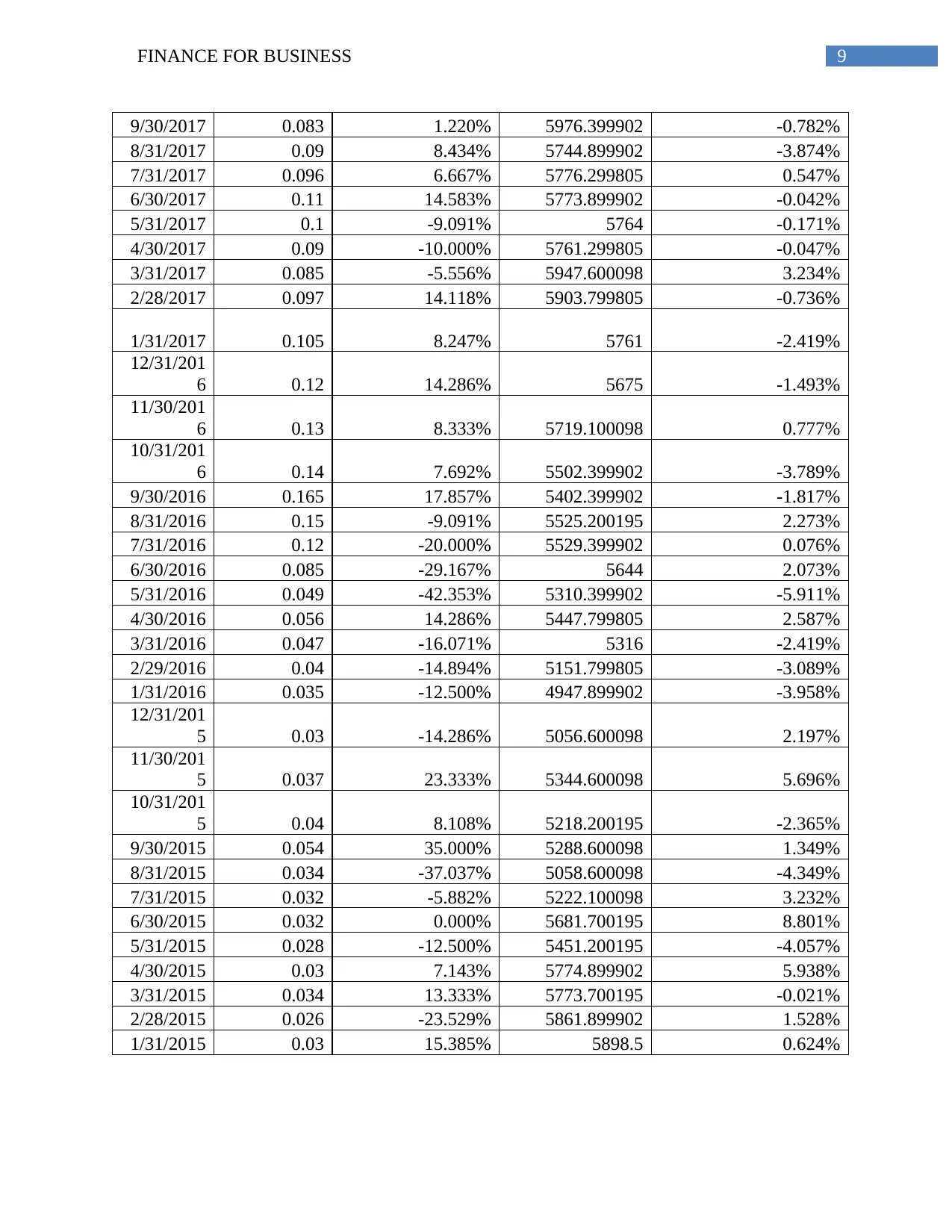

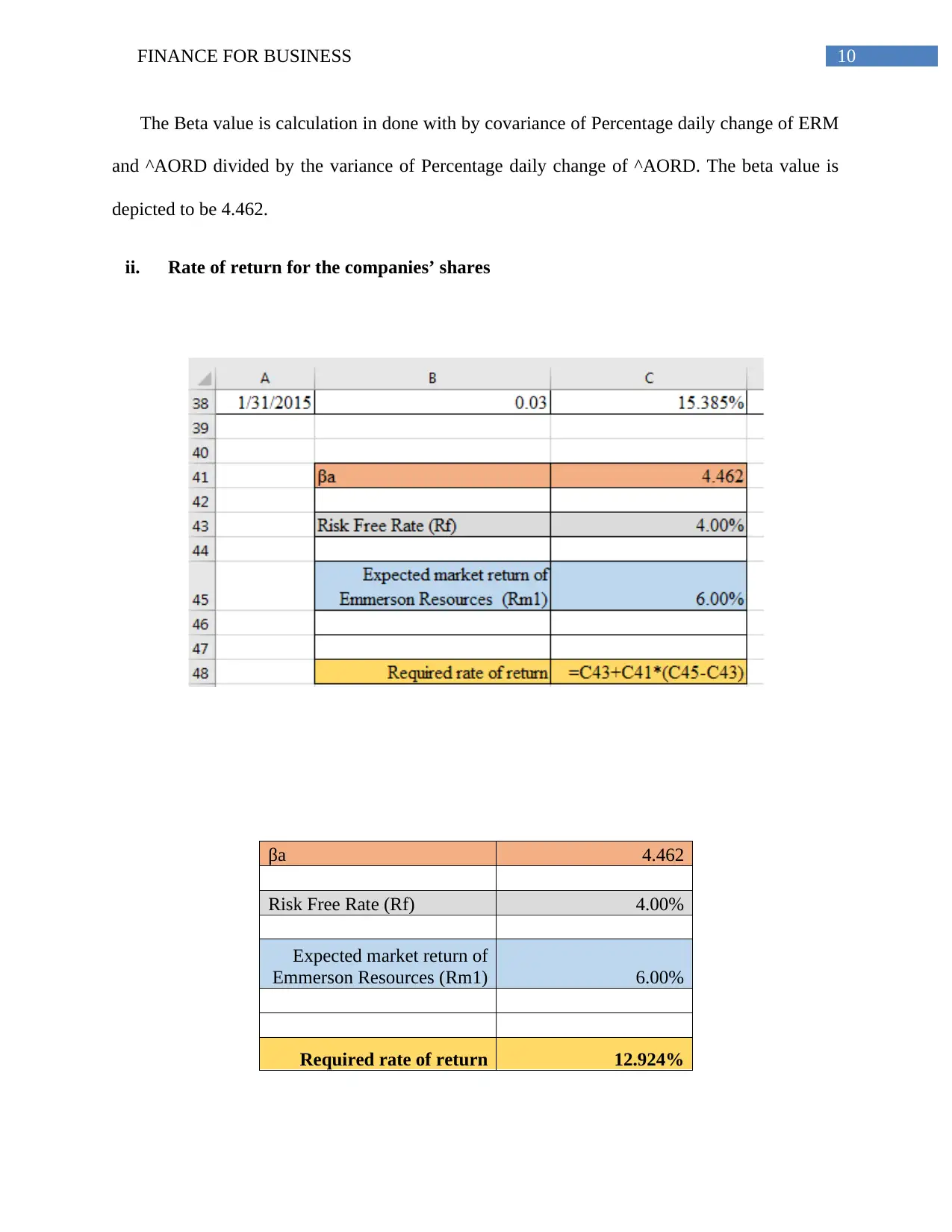

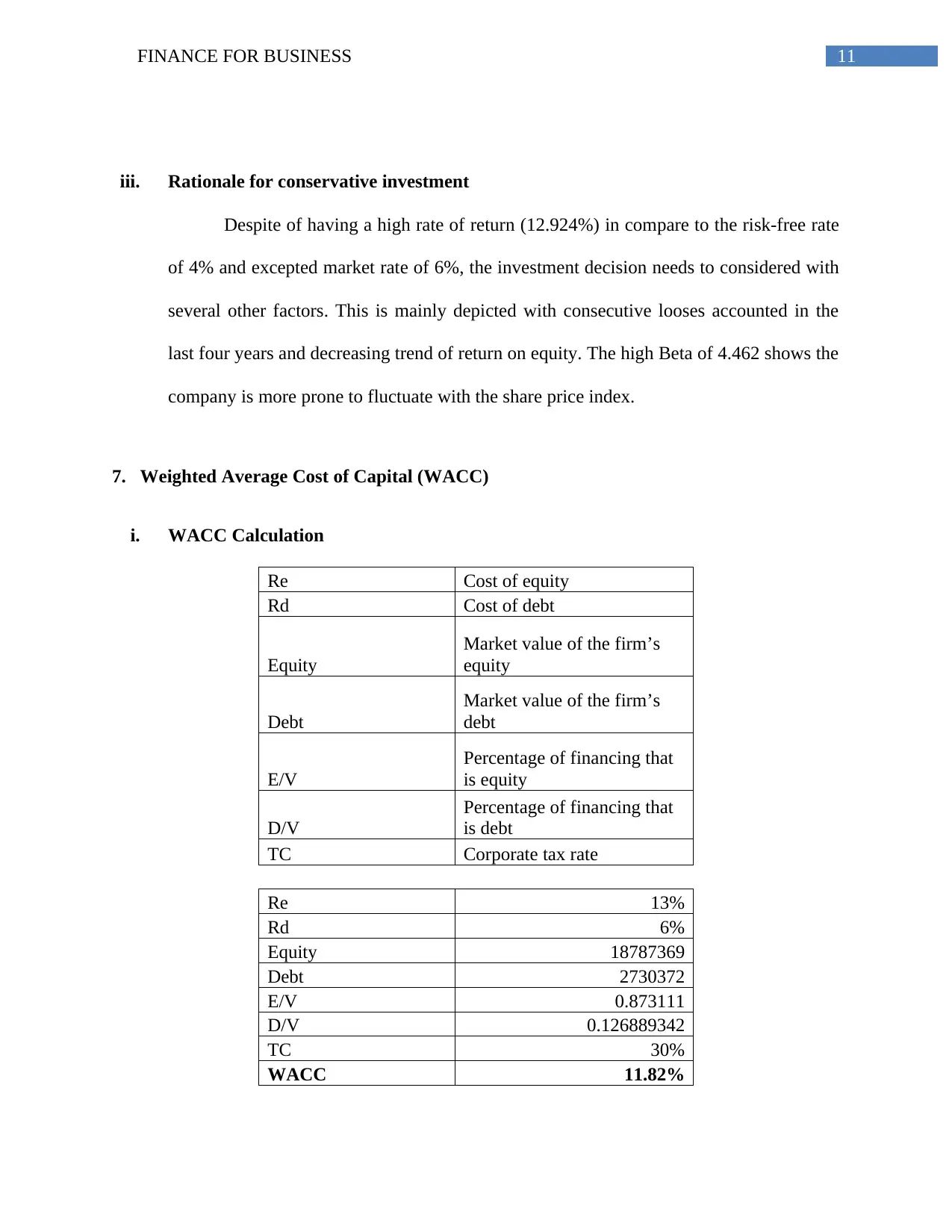

This report presents a comprehensive financial analysis of Emmerson Resources, a prominent Australian mineral field holder. The analysis includes a detailed overview of the company's operations, ownership structure, and key personnel. It delves into the calculation of key financial ratios such as ROE, ROA, and debt-equity ratio, providing insights into the company's profitability and solvency. The report also utilizes data from the ASX website to analyze share price movements and compare them to market indices. Furthermore, it incorporates the Capital Asset Pricing Model (CAPM) to calculate beta and the required rate of return, offering a rationale for investment decisions. The Weighted Average Cost of Capital (WACC) is evaluated, and the debt ratio is examined to assess the company's capital structure. The report also discusses the dividend policy and concludes with a letter of recommendation to a client, summarizing the investment potential and future prospects of Emmerson Resources.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.