Empirical Analysis of Non-GAAP and GAAP Earnings in Australia

VerifiedAdded on 2023/06/04

|14

|2929

|84

Report

AI Summary

This report presents an empirical analysis of non-GAAP versus GAAP earnings, focusing on two Australian firms: Treasury Wine Estates (TWE) and Tassel Group Limited (TGR). The study investigates the impact of financial decisions and announcements on market performance, comparing GAAP and non-GAAP earnings. The analysis utilizes the event study method to assess market reactions to changes in both earnings types, considering factors like announcement dates and subsequent market movements. The report further explores the relationship between operational performance, financial decision-making, and how non-GAAP earnings provide insights beyond traditional GAAP measures. The study concludes that non-GAAP earnings are crucial for evaluating actual financial health and operational performance, even though they are not always included in financial disclosures. The report also includes a research proposal outlining potential future research directions in this area.

0

Running head: EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Name of the Student

Name of the University

Author’s Note

Running head: EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Executive Summary

Every business firm prefers to incorporate changes in their financial system in order to

restructure the accountability of the organizational performance and ensure that the objective of

the firms are moving towards accomplishment after encountering industrial fluctuation as well as

the risks associated with market uncertainties. It is been seen that due to the fact that all the firms

are part of the industry hence new announcements regarding changes in their business activities

as well as financial decision making impacts upon the overall market. The significance of that

impact is important to analyze in order to support the understanding of the investors and realize

the market trends. Organizational take overs, new leases, earnings announcements, dividend

changes, consistent GAAP adjustments as well as changes in the non-GAAP earnings, etc. all

information contribute in creating variations in the market performance. Hence, it is required to

understand the nature of change that takes place in the market after new announcements made by

different firms as well as examine that whether there exists any abnormal market effect based

upon that. In other terms further proposal can be developed based on the event study or

accounting changes to research upon the issue and light upon new sphere or genre of financial

functioning of the businesses that runs within market. The study investigated the changes that

took place in case of Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) in the form

of announcements or undertaking of important financial decisions that significantly influenced or

brought difference in the market. Estimation are done based on the comparison of the Non-

GAAP and GAAP earnings and evaluation is made based on the annual reports of the companies

followed by understanding how the market has reacted upon the financial decision makings.

Executive Summary

Every business firm prefers to incorporate changes in their financial system in order to

restructure the accountability of the organizational performance and ensure that the objective of

the firms are moving towards accomplishment after encountering industrial fluctuation as well as

the risks associated with market uncertainties. It is been seen that due to the fact that all the firms

are part of the industry hence new announcements regarding changes in their business activities

as well as financial decision making impacts upon the overall market. The significance of that

impact is important to analyze in order to support the understanding of the investors and realize

the market trends. Organizational take overs, new leases, earnings announcements, dividend

changes, consistent GAAP adjustments as well as changes in the non-GAAP earnings, etc. all

information contribute in creating variations in the market performance. Hence, it is required to

understand the nature of change that takes place in the market after new announcements made by

different firms as well as examine that whether there exists any abnormal market effect based

upon that. In other terms further proposal can be developed based on the event study or

accounting changes to research upon the issue and light upon new sphere or genre of financial

functioning of the businesses that runs within market. The study investigated the changes that

took place in case of Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) in the form

of announcements or undertaking of important financial decisions that significantly influenced or

brought difference in the market. Estimation are done based on the comparison of the Non-

GAAP and GAAP earnings and evaluation is made based on the annual reports of the companies

followed by understanding how the market has reacted upon the financial decision makings.

2EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Table of Contents

Executive Summary.........................................................................................................................1

PART I.............................................................................................................................................3

Introduction..................................................................................................................................3

Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) Data Analysis.........................3

Conclusion...................................................................................................................................6

PART II...........................................................................................................................................8

Introduction..................................................................................................................................8

Research Questions......................................................................................................................8

Research Hypothesis....................................................................................................................8

Review of Literature....................................................................................................................9

Materials & Methods.................................................................................................................10

Limitations of the Research.......................................................................................................10

Future of the Research...............................................................................................................11

Gantt chart.................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Executive Summary.........................................................................................................................1

PART I.............................................................................................................................................3

Introduction..................................................................................................................................3

Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) Data Analysis.........................3

Conclusion...................................................................................................................................6

PART II...........................................................................................................................................8

Introduction..................................................................................................................................8

Research Questions......................................................................................................................8

Research Hypothesis....................................................................................................................8

Review of Literature....................................................................................................................9

Materials & Methods.................................................................................................................10

Limitations of the Research.......................................................................................................10

Future of the Research...............................................................................................................11

Gantt chart.................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

PART I

Introduction

Treasury Wine Estates Ltd (TWE) demerged from Foster’s Group in 2011 and became a

global wine company based in Australia. Being within the top five wine producers throughout

the world it is the owner of a portfolio that is inclusive of Pinfold’s & Wolf Bass, 19 Crimes,

Maison de Grand Esprit as well as US wines like St Jean and Sterling. The company owns a

treasury with nearby 13000 planted hectares having over 130 wineries. It remained on track

through hitting a 25 % operating income growth by the end of the fiscal year 2017. On the other

hand Tassel Group Limited (TGR) has its engagement in farming, hatching and marketing of

Tasmanian grown smoked, frozen and canned Atlantic salmon where it integrated the seafood

processor and salmon growers along with marketers and bottom line sellers. It produces almost

10 million smelt per year through its operation over 3 hatcheries. 15.4 kilograms of final

products are produced per minute which added up to 3050 tons on average every year.

Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) Data Analysis

The data represented below provides the changes in the GAAP and Non-GAAP earnings

of the company and based on the market beta, the respective abnormal returns are shown as

follows:

PART I

Introduction

Treasury Wine Estates Ltd (TWE) demerged from Foster’s Group in 2011 and became a

global wine company based in Australia. Being within the top five wine producers throughout

the world it is the owner of a portfolio that is inclusive of Pinfold’s & Wolf Bass, 19 Crimes,

Maison de Grand Esprit as well as US wines like St Jean and Sterling. The company owns a

treasury with nearby 13000 planted hectares having over 130 wineries. It remained on track

through hitting a 25 % operating income growth by the end of the fiscal year 2017. On the other

hand Tassel Group Limited (TGR) has its engagement in farming, hatching and marketing of

Tasmanian grown smoked, frozen and canned Atlantic salmon where it integrated the seafood

processor and salmon growers along with marketers and bottom line sellers. It produces almost

10 million smelt per year through its operation over 3 hatcheries. 15.4 kilograms of final

products are produced per minute which added up to 3050 tons on average every year.

Treasury Wine Estates (TWE) & Tassel Group Limited (TGR) Data Analysis

The data represented below provides the changes in the GAAP and Non-GAAP earnings

of the company and based on the market beta, the respective abnormal returns are shown as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

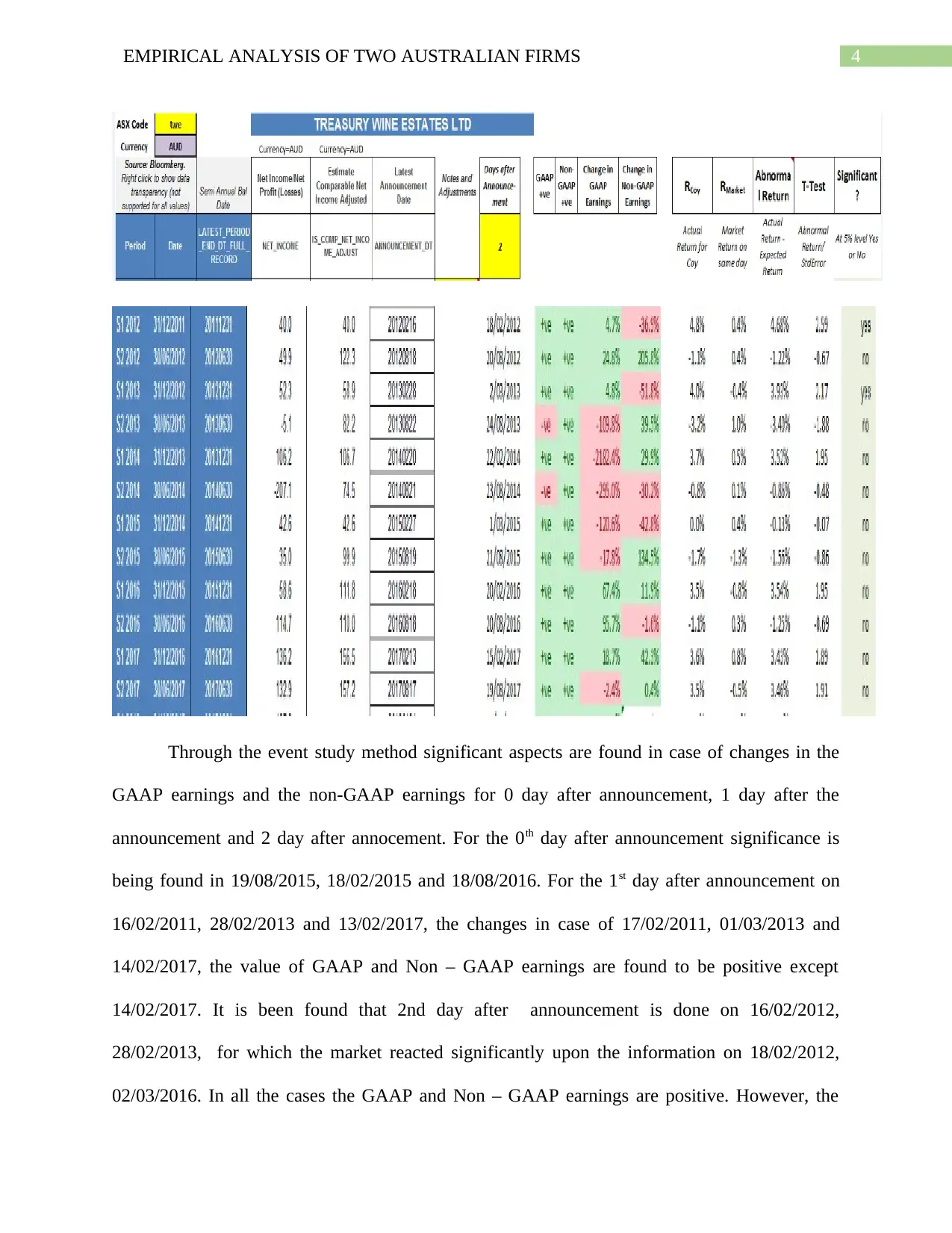

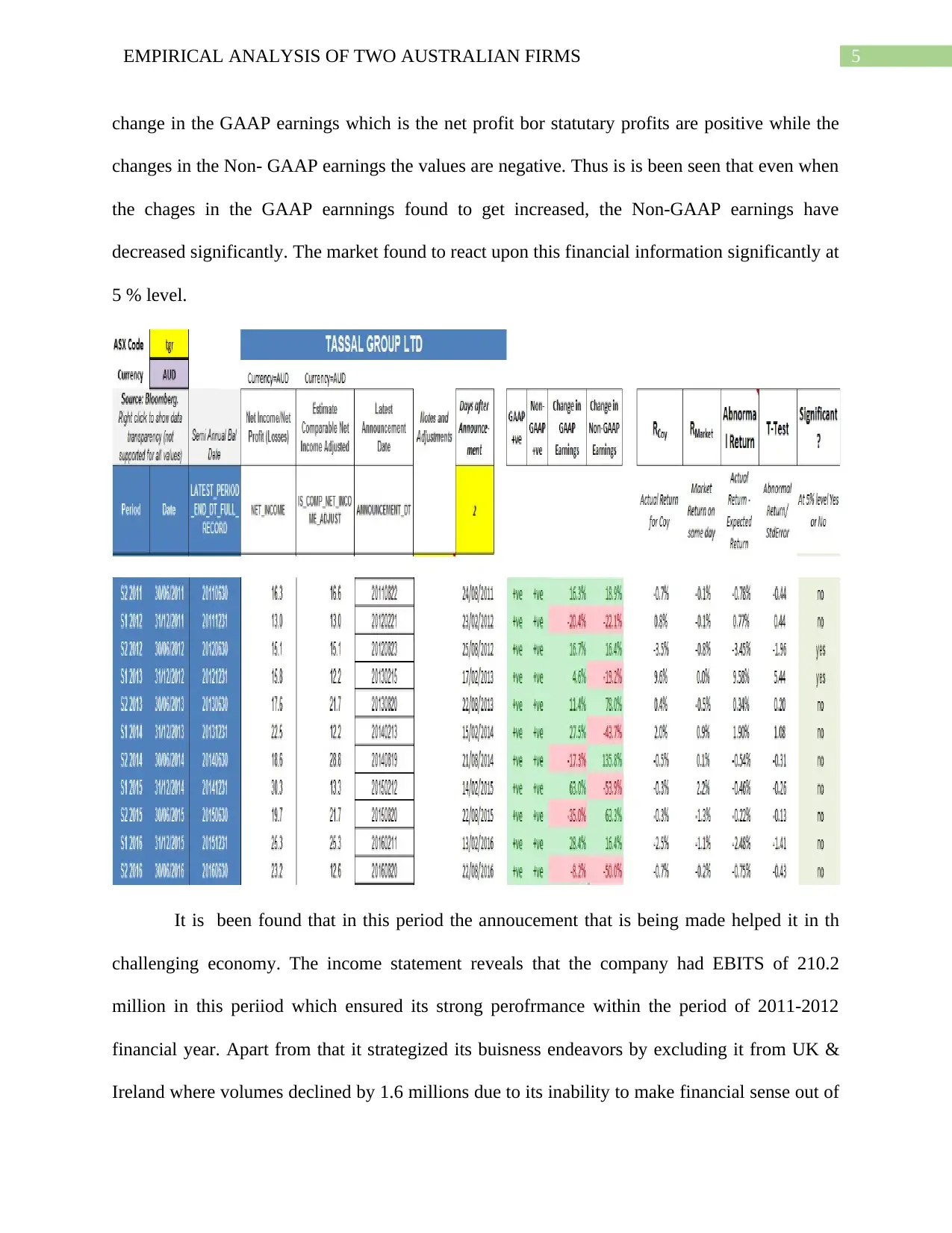

Through the event study method significant aspects are found in case of changes in the

GAAP earnings and the non-GAAP earnings for 0 day after announcement, 1 day after the

announcement and 2 day after annocement. For the 0th day after announcement significance is

being found in 19/08/2015, 18/02/2015 and 18/08/2016. For the 1st day after announcement on

16/02/2011, 28/02/2013 and 13/02/2017, the changes in case of 17/02/2011, 01/03/2013 and

14/02/2017, the value of GAAP and Non – GAAP earnings are found to be positive except

14/02/2017. It is been found that 2nd day after announcement is done on 16/02/2012,

28/02/2013, for which the market reacted significantly upon the information on 18/02/2012,

02/03/2016. In all the cases the GAAP and Non – GAAP earnings are positive. However, the

Through the event study method significant aspects are found in case of changes in the

GAAP earnings and the non-GAAP earnings for 0 day after announcement, 1 day after the

announcement and 2 day after annocement. For the 0th day after announcement significance is

being found in 19/08/2015, 18/02/2015 and 18/08/2016. For the 1st day after announcement on

16/02/2011, 28/02/2013 and 13/02/2017, the changes in case of 17/02/2011, 01/03/2013 and

14/02/2017, the value of GAAP and Non – GAAP earnings are found to be positive except

14/02/2017. It is been found that 2nd day after announcement is done on 16/02/2012,

28/02/2013, for which the market reacted significantly upon the information on 18/02/2012,

02/03/2016. In all the cases the GAAP and Non – GAAP earnings are positive. However, the

5EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

change in the GAAP earnings which is the net profit bor statutary profits are positive while the

changes in the Non- GAAP earnings the values are negative. Thus is is been seen that even when

the chages in the GAAP earnnings found to get increased, the Non-GAAP earnings have

decreased significantly. The market found to react upon this financial information significantly at

5 % level.

It is been found that in this period the annoucement that is being made helped it in th

challenging economy. The income statement reveals that the company had EBITS of 210.2

million in this periiod which ensured its strong perofrmance within the period of 2011-2012

financial year. Apart from that it strategized its buisness endeavors by excluding it from UK &

Ireland where volumes declined by 1.6 millions due to its inability to make financial sense out of

change in the GAAP earnings which is the net profit bor statutary profits are positive while the

changes in the Non- GAAP earnings the values are negative. Thus is is been seen that even when

the chages in the GAAP earnnings found to get increased, the Non-GAAP earnings have

decreased significantly. The market found to react upon this financial information significantly at

5 % level.

It is been found that in this period the annoucement that is being made helped it in th

challenging economy. The income statement reveals that the company had EBITS of 210.2

million in this periiod which ensured its strong perofrmance within the period of 2011-2012

financial year. Apart from that it strategized its buisness endeavors by excluding it from UK &

Ireland where volumes declined by 1.6 millions due to its inability to make financial sense out of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

its investments. The change in 2016 in TWE took place due to its acquisition of Diageo’s Wine

potfolio while tye cchange in 2-011 w, 2012 as well as 2013 impacted the market price after their

announcement of demergeer with Foster Wine. Tassal group on the other hand have its merger

formation where retailers supported sales and non-current inventory raised by 84 % which

improved the NSR by 1.6 %. The rise in EPS is 14.8 % per share which contributed for a ful

year dividend of 13 %. Moreover, net debt was down by 34.4 million due to its operational and

strategic flexibility. The volatility in the European economy was thus surpassed though

maintaining an increase in GAAP earnings by 17.3 % million (Clinch et al., 2018). Thus the

financial decisions where freed from its oerational performance or tax environments. Howevrer,

the true performance of the company are being revealed by the Non – GAAP earnings which

included cash earnings, adjusted EPS, operating earnings and adjusted operating income of

Treasury Wine Estates (TWE). Moreover, in case of Tassel Group Limited (TGR) the non

GAAP earnings have a positive change in few periods where the non GAAP values have risen.

However, in those periods the GAAP earnings have and the net profit after tax has confronted a

minute declination. This shows that the operating expenses and profit actually reverses the

GAAP accounting distortion across the companies on a consistent basis.

Conclusion

It can be concluded based on the analysis that the Non-GAAP earnings are the

measurements of profit for both the companies in actual terms and for this reason this ar not

always included in the financial disclosure. The GAAP earnings are reflects of net profit or

statutory profits. However, Non-GAAP earnings reflects the best possible figures and the actual

financial health of a company towards its investors. Based on the GAAP rules, the quarterly

financial reports provides investors a composite representation of the company’s cash flow and

its investments. The change in 2016 in TWE took place due to its acquisition of Diageo’s Wine

potfolio while tye cchange in 2-011 w, 2012 as well as 2013 impacted the market price after their

announcement of demergeer with Foster Wine. Tassal group on the other hand have its merger

formation where retailers supported sales and non-current inventory raised by 84 % which

improved the NSR by 1.6 %. The rise in EPS is 14.8 % per share which contributed for a ful

year dividend of 13 %. Moreover, net debt was down by 34.4 million due to its operational and

strategic flexibility. The volatility in the European economy was thus surpassed though

maintaining an increase in GAAP earnings by 17.3 % million (Clinch et al., 2018). Thus the

financial decisions where freed from its oerational performance or tax environments. Howevrer,

the true performance of the company are being revealed by the Non – GAAP earnings which

included cash earnings, adjusted EPS, operating earnings and adjusted operating income of

Treasury Wine Estates (TWE). Moreover, in case of Tassel Group Limited (TGR) the non

GAAP earnings have a positive change in few periods where the non GAAP values have risen.

However, in those periods the GAAP earnings have and the net profit after tax has confronted a

minute declination. This shows that the operating expenses and profit actually reverses the

GAAP accounting distortion across the companies on a consistent basis.

Conclusion

It can be concluded based on the analysis that the Non-GAAP earnings are the

measurements of profit for both the companies in actual terms and for this reason this ar not

always included in the financial disclosure. The GAAP earnings are reflects of net profit or

statutory profits. However, Non-GAAP earnings reflects the best possible figures and the actual

financial health of a company towards its investors. Based on the GAAP rules, the quarterly

financial reports provides investors a composite representation of the company’s cash flow and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

other financial transactions. Whereas the non-GAAP earnings includes more credible results

which excludes the impact of the large non-recurring events as for example the sales or purchase

of major assets. The non-GAAP earnings provides a way of evaluation of the operational

performance of the companies under consideration which are not dependent upon its financial

decisions.

other financial transactions. Whereas the non-GAAP earnings includes more credible results

which excludes the impact of the large non-recurring events as for example the sales or purchase

of major assets. The non-GAAP earnings provides a way of evaluation of the operational

performance of the companies under consideration which are not dependent upon its financial

decisions.

8EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

PART II

Introduction

The GAAP earnings are utilized to provide an overview of any company’s financial

performance. In this process the financial statements renders information based on the existing

financial health of the company and being abided by the GAAP rules (Venter et al., 2014).

However, the non GAAP earnings are the parametric factor which help investors to delve into

the depth of the financial state of any company (Isidro & Marques, 2015). In the present case the

companies undertaken are Treasury Wine Estates (TWE) & Tassel Group Limited (TGR).

Through the GAAP and Non-GAAP earnings the obtained information provides sufficient details

to the investors regarding the operational performance of the company which are not influenced

by the financial decisions undertaken by TWE & TGR. In order to investigate on the

relationship between operational aspects of the company which are latent. However, the financial

decisions are revealed due to non-GAAP earnings. Research needs to conduct over the

relationship between non-GAAP earnings and how the operational performance becomes latent

due to financial decision making which is the objective of the research.

Research Questions

The research questions for the study can be incorporated as follows:

1. Does the operating profit reverses the GAAP accounting distortion across the companies

on a consistent basis?

Research Hypothesis

The null hypothesis can be reflected as follows:

H0 = Operating profit reverses the GAAP accounting distortion across the companies on a

consistent basis

PART II

Introduction

The GAAP earnings are utilized to provide an overview of any company’s financial

performance. In this process the financial statements renders information based on the existing

financial health of the company and being abided by the GAAP rules (Venter et al., 2014).

However, the non GAAP earnings are the parametric factor which help investors to delve into

the depth of the financial state of any company (Isidro & Marques, 2015). In the present case the

companies undertaken are Treasury Wine Estates (TWE) & Tassel Group Limited (TGR).

Through the GAAP and Non-GAAP earnings the obtained information provides sufficient details

to the investors regarding the operational performance of the company which are not influenced

by the financial decisions undertaken by TWE & TGR. In order to investigate on the

relationship between operational aspects of the company which are latent. However, the financial

decisions are revealed due to non-GAAP earnings. Research needs to conduct over the

relationship between non-GAAP earnings and how the operational performance becomes latent

due to financial decision making which is the objective of the research.

Research Questions

The research questions for the study can be incorporated as follows:

1. Does the operating profit reverses the GAAP accounting distortion across the companies

on a consistent basis?

Research Hypothesis

The null hypothesis can be reflected as follows:

H0 = Operating profit reverses the GAAP accounting distortion across the companies on a

consistent basis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

The alternative hypothesis can be incorporated as follows:

H1 = Operating profit does not reverses the GAAP accounting distortion across the companies on

a consistent basis.

Review of Literature

According to Ciesielski & Henry (2017) the real estate companies requires extensive use

of representing their adjusted earnings which do not highlight the true scenario of the

organizational financial performance. GAAP earnings maintains a uniformity within companies

regarding their financial reports. On the other hand the non-GAAP earnings provides a high

quality information as it excludes the impact of one-time items or unusual items. The paper

basically incorporates the fundamental aspects of the income statement where in case the non-

GAAP earnings plays a better role than only the GAAP earnings.

According to Charitou et al., (2018) non GAAP earnings provides privilege to the

company based on their local authoritarian needs of preparing financial statements or for

incorporating local regulations or for adding new management perspectives for betterment of the

company. Since non-recurring items like restructuring charges, one-off gains or losses in major

assets, goodwill impairments, etc. are excluded in the non-GAAP earnings hence it provides a

better reliable and comparable financial information.

In accordance with Black et al., (2017) from conceptual perspective of the financial

information it is a fact that the non-GAAP earnings provide a better information regarding the

financial state of some companies though it lacks in merit for providing a clearly understandable

reporting once it becomes more frequent or regular in use. The GAAP provides a uniform

financial information in this respect that is acceptable and understandable from all respect.

The alternative hypothesis can be incorporated as follows:

H1 = Operating profit does not reverses the GAAP accounting distortion across the companies on

a consistent basis.

Review of Literature

According to Ciesielski & Henry (2017) the real estate companies requires extensive use

of representing their adjusted earnings which do not highlight the true scenario of the

organizational financial performance. GAAP earnings maintains a uniformity within companies

regarding their financial reports. On the other hand the non-GAAP earnings provides a high

quality information as it excludes the impact of one-time items or unusual items. The paper

basically incorporates the fundamental aspects of the income statement where in case the non-

GAAP earnings plays a better role than only the GAAP earnings.

According to Charitou et al., (2018) non GAAP earnings provides privilege to the

company based on their local authoritarian needs of preparing financial statements or for

incorporating local regulations or for adding new management perspectives for betterment of the

company. Since non-recurring items like restructuring charges, one-off gains or losses in major

assets, goodwill impairments, etc. are excluded in the non-GAAP earnings hence it provides a

better reliable and comparable financial information.

In accordance with Black et al., (2017) from conceptual perspective of the financial

information it is a fact that the non-GAAP earnings provide a better information regarding the

financial state of some companies though it lacks in merit for providing a clearly understandable

reporting once it becomes more frequent or regular in use. The GAAP provides a uniform

financial information in this respect that is acceptable and understandable from all respect.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Moreover, the non-GAAP earnings across companies lacks in providing standard definitions that

are consistent throughout all companies.

According to Bhattacharya et al., (2015) investors are found to give more focus upon the

non-GAAP measure rather than the GAAP figures which makes the less – sophisticated investors

to become at more risk to get misled. It was also reflected in the study that the true motivation of

the mangers for reporting certain numbers in financial terms are understood for their desire to

beat the expectations of the analysts as well as for avoiding decreases in earnings. The paper

revealed that the non-GAAP earnings help the investors to communicate better with the financial

state of the companies though it lacks in keeping a uniformity across the industry.

Materials & Methods

The data collection procedure based on quantitative research design can be utilized as an

effective way to conduct the research. Information from different secondary sources may be

utilized followed by annual reports of companies. The secondary data and information thus

obtained will be further analyzed with the help of statistical tools to understand the nature of

relationship that exists between the operational performances and financial decision making of

the companies that uses GAAP rules for revealing financial information.

Limitations of the Research

The research paper also needs to examine that whether the true profitability is better

understood by the investors through the non-GAAP earnings measurements and whether the non-

GAAP earnings use rules by inflating the reports of growth and profitability of any organization.

These are not thoroughly reflected through this study but further research is needed on this

aspect (Leung & Veenman, 2018).

Moreover, the non-GAAP earnings across companies lacks in providing standard definitions that

are consistent throughout all companies.

According to Bhattacharya et al., (2015) investors are found to give more focus upon the

non-GAAP measure rather than the GAAP figures which makes the less – sophisticated investors

to become at more risk to get misled. It was also reflected in the study that the true motivation of

the mangers for reporting certain numbers in financial terms are understood for their desire to

beat the expectations of the analysts as well as for avoiding decreases in earnings. The paper

revealed that the non-GAAP earnings help the investors to communicate better with the financial

state of the companies though it lacks in keeping a uniformity across the industry.

Materials & Methods

The data collection procedure based on quantitative research design can be utilized as an

effective way to conduct the research. Information from different secondary sources may be

utilized followed by annual reports of companies. The secondary data and information thus

obtained will be further analyzed with the help of statistical tools to understand the nature of

relationship that exists between the operational performances and financial decision making of

the companies that uses GAAP rules for revealing financial information.

Limitations of the Research

The research paper also needs to examine that whether the true profitability is better

understood by the investors through the non-GAAP earnings measurements and whether the non-

GAAP earnings use rules by inflating the reports of growth and profitability of any organization.

These are not thoroughly reflected through this study but further research is needed on this

aspect (Leung & Veenman, 2018).

11EMPIRICAL ANALYSIS OF TWO AUSTRALIAN FIRMS

Future of the Research

The research will provide scope on understanding the flaws and fortes of the non-GAAP

earnings and how it can help the investors to understand the financial condition of organization

that behaves in similar manner due to uniformity of the GAAP rules implemented upon them for

financial understanding of information regarding the company’s financial health. This paper will

reflect will rejuvenate the existing relationship between operational health and financial health of

the companies and will reveal the true financial state that becomes latent due to implementation

of GAAP rules in their financial statements.

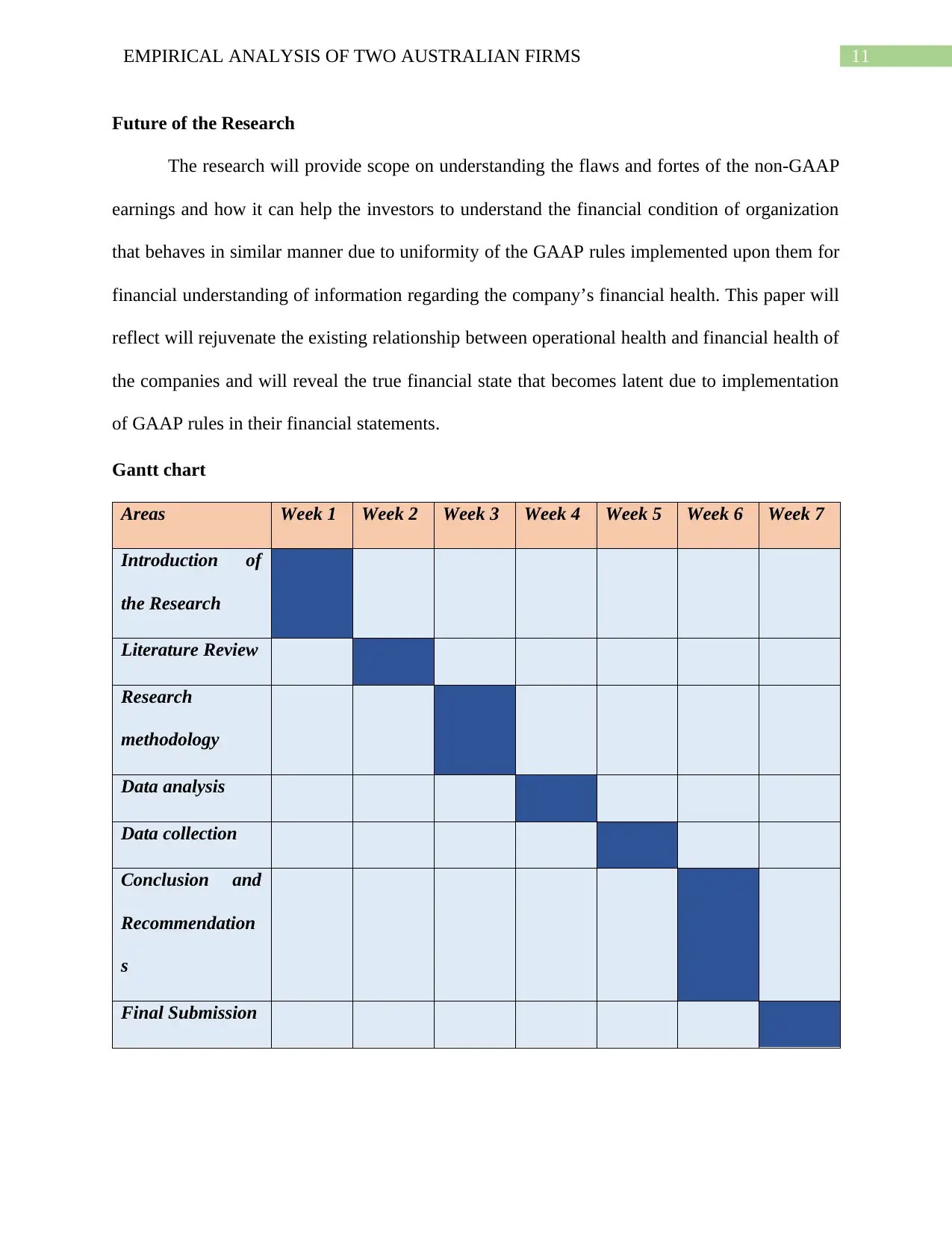

Gantt chart

Areas Week 1 Week 2 Week 3 Week 4 Week 5 Week 6 Week 7

Introduction of

the Research

Literature Review

Research

methodology

Data analysis

Data collection

Conclusion and

Recommendation

s

Final Submission

Future of the Research

The research will provide scope on understanding the flaws and fortes of the non-GAAP

earnings and how it can help the investors to understand the financial condition of organization

that behaves in similar manner due to uniformity of the GAAP rules implemented upon them for

financial understanding of information regarding the company’s financial health. This paper will

reflect will rejuvenate the existing relationship between operational health and financial health of

the companies and will reveal the true financial state that becomes latent due to implementation

of GAAP rules in their financial statements.

Gantt chart

Areas Week 1 Week 2 Week 3 Week 4 Week 5 Week 6 Week 7

Introduction of

the Research

Literature Review

Research

methodology

Data analysis

Data collection

Conclusion and

Recommendation

s

Final Submission

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.