University Canadian Tax Calculation - ACCT-3610 Summer 2019

VerifiedAdded on 2022/12/29

|9

|809

|3

Homework Assignment

AI Summary

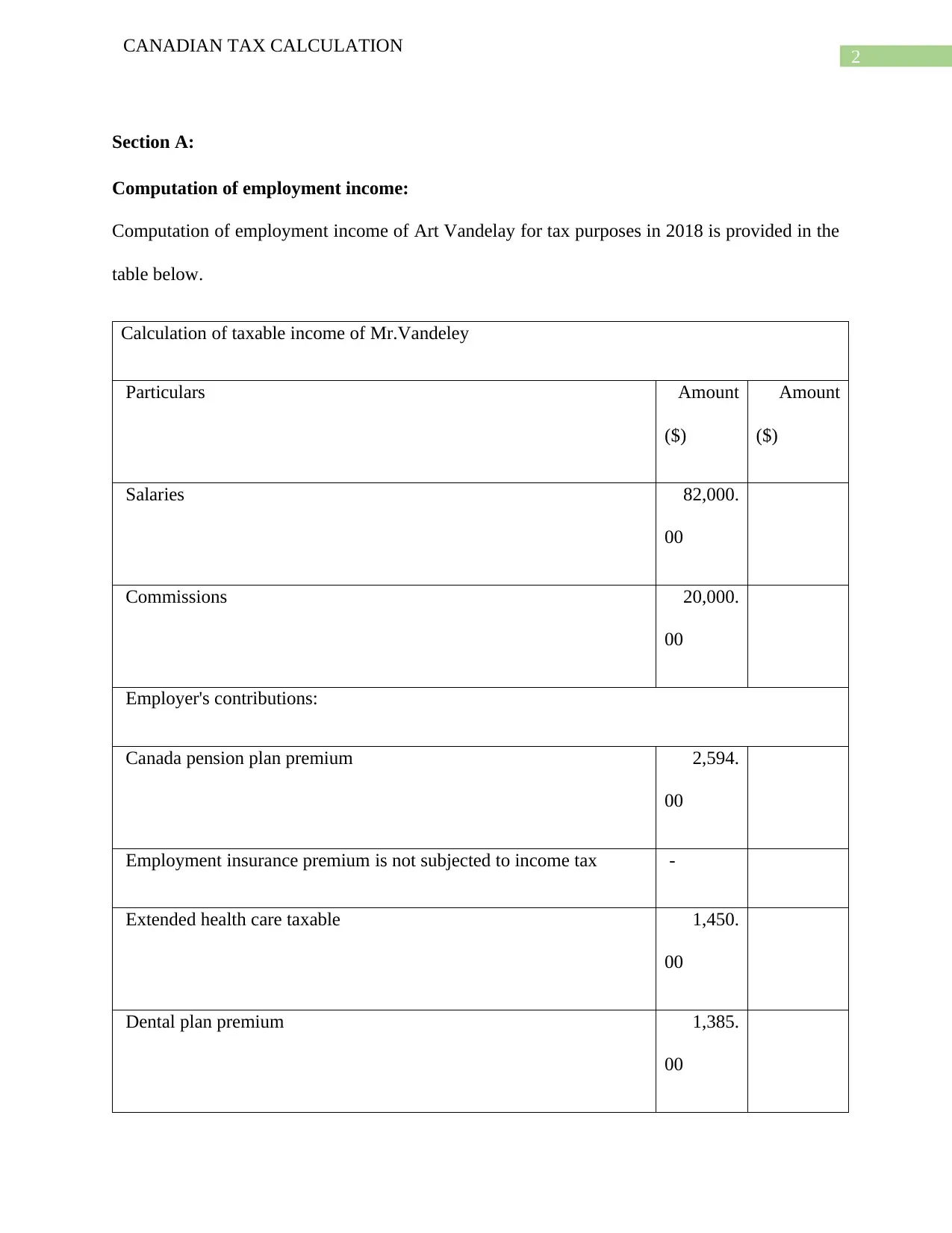

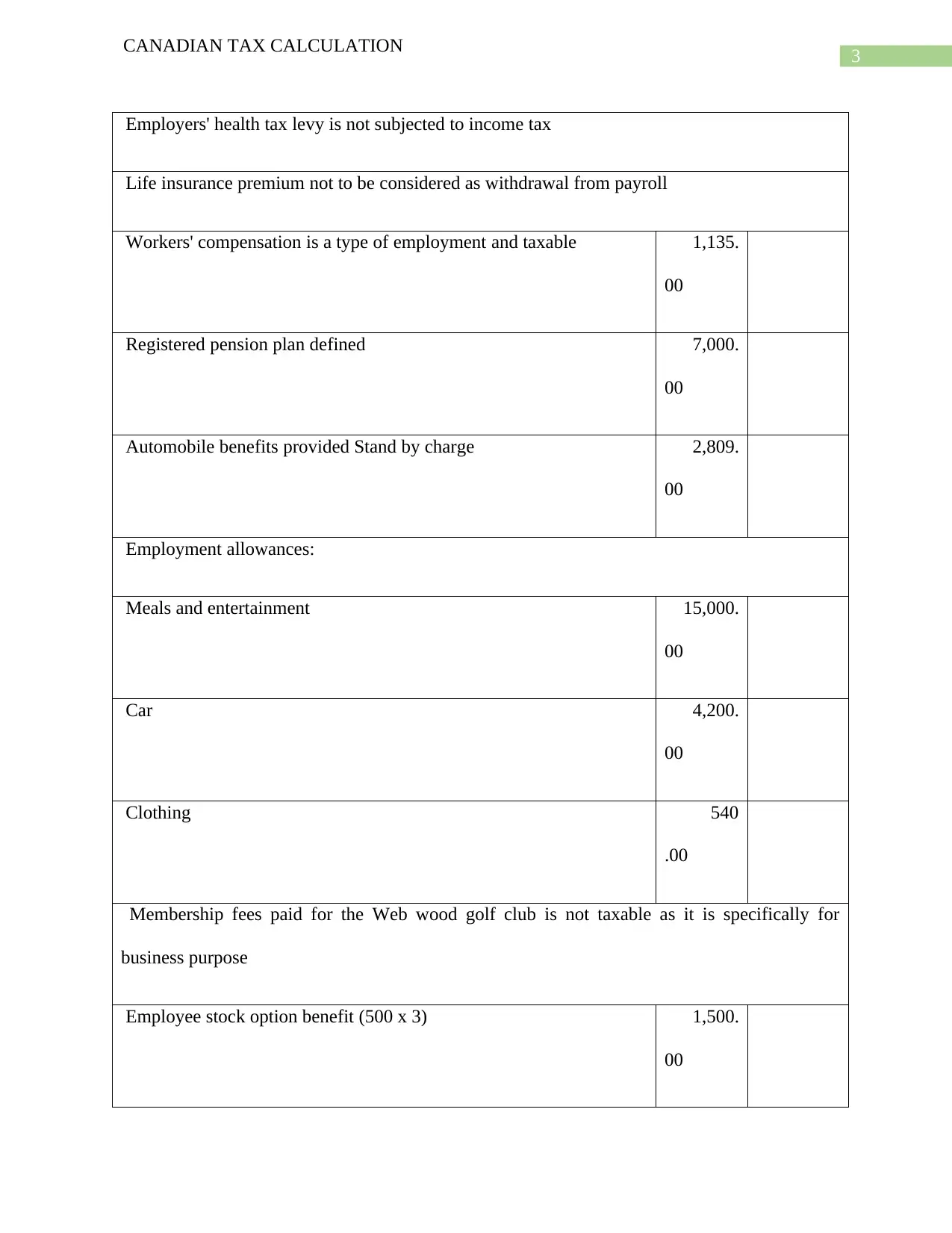

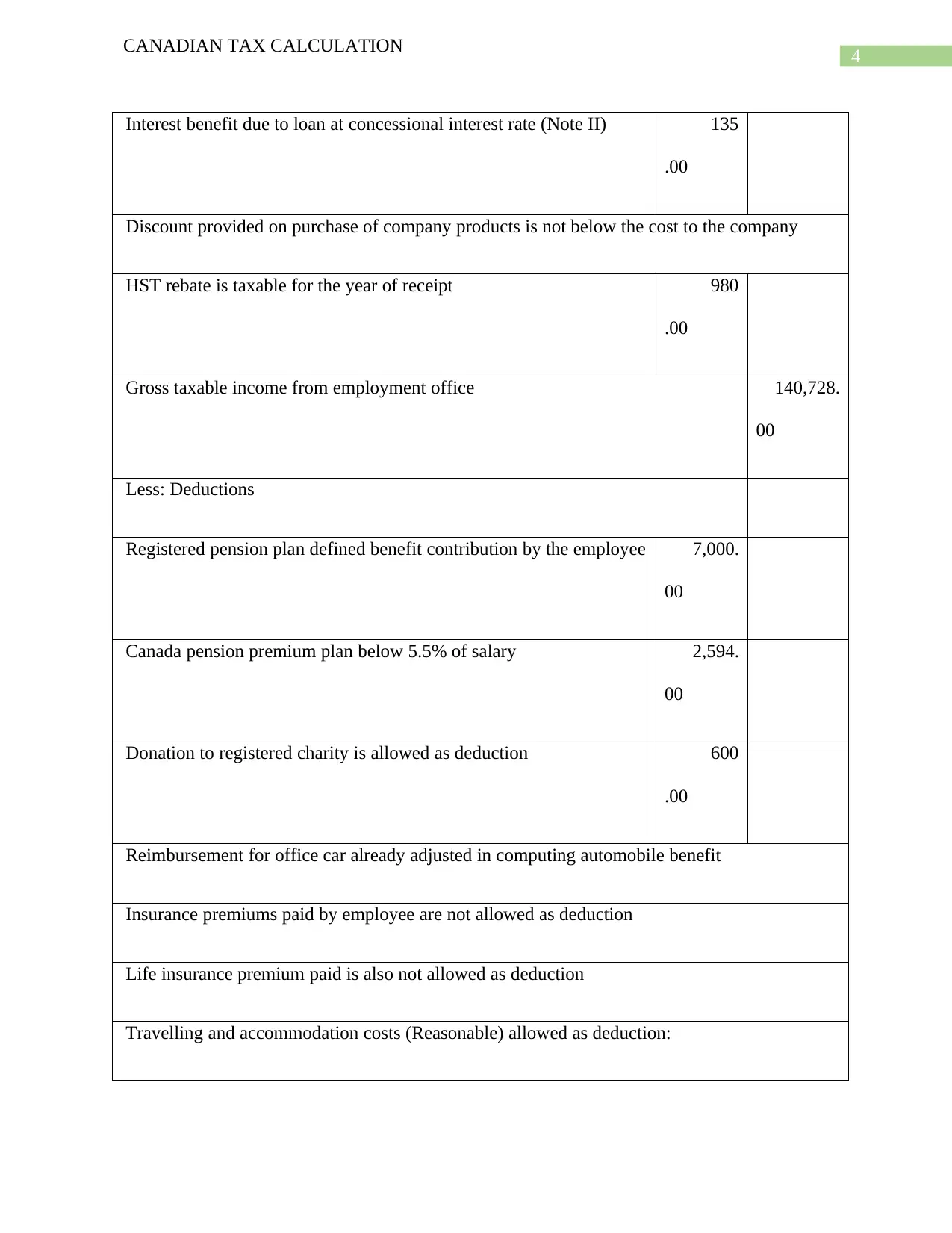

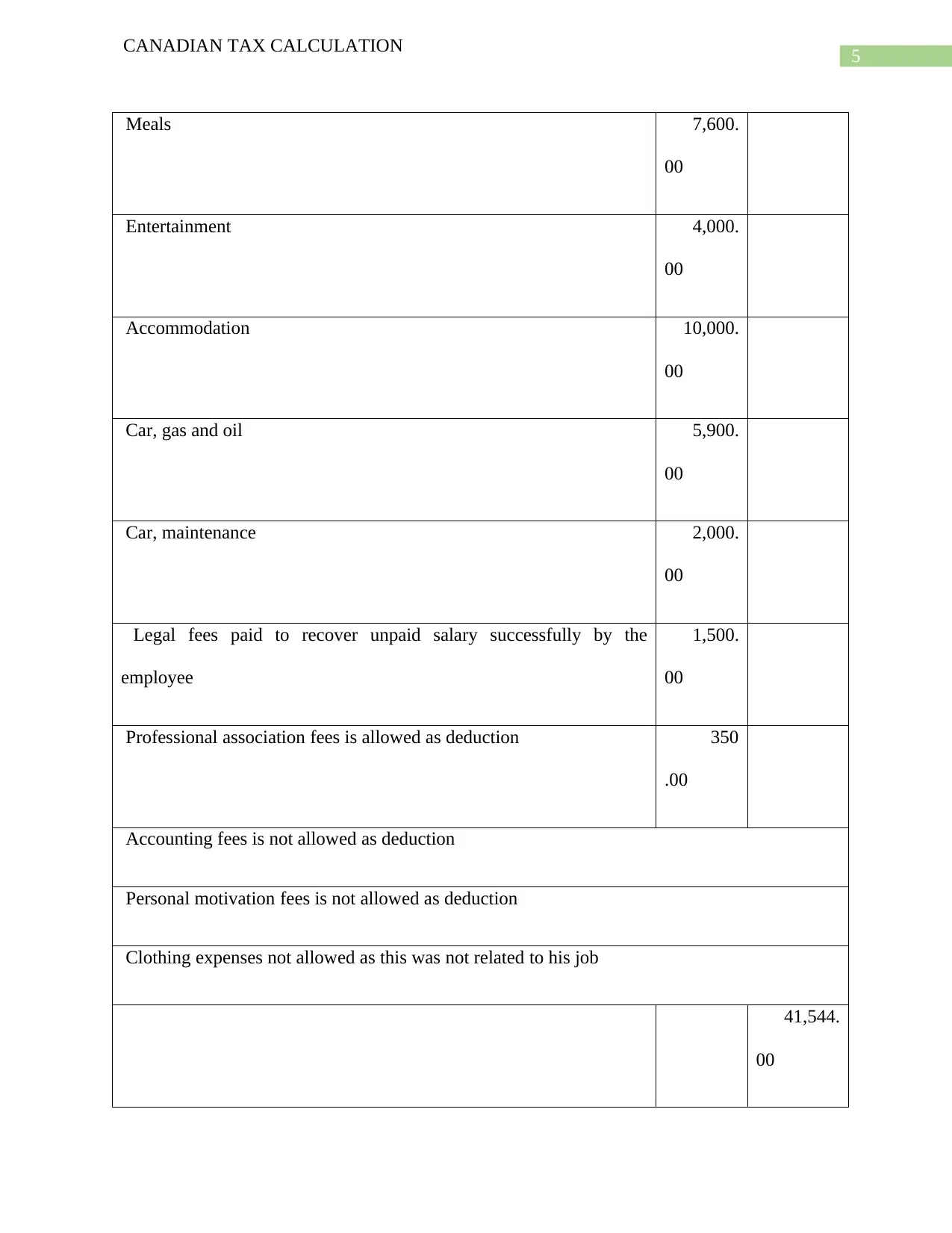

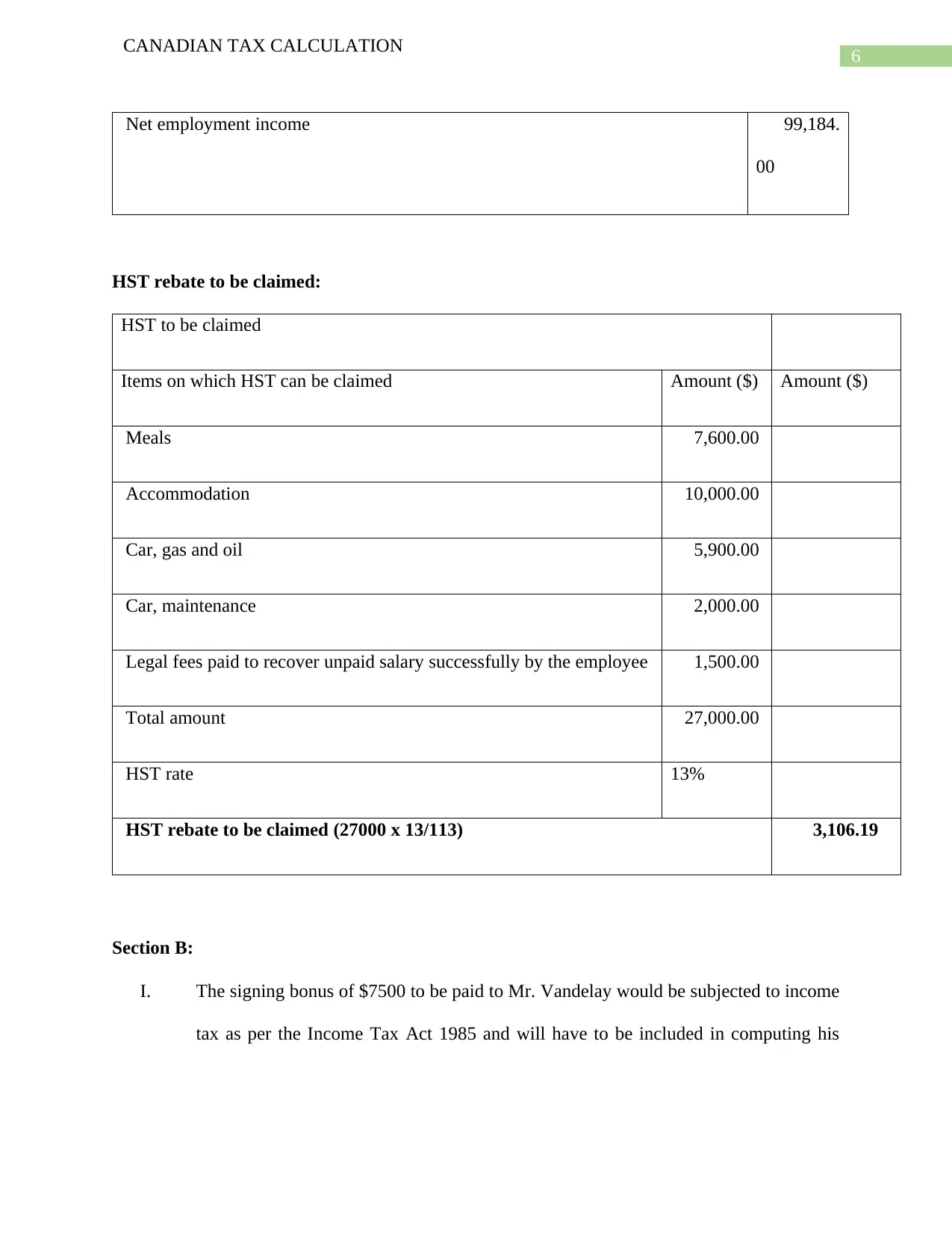

This document presents a comprehensive solution to a Canadian tax calculation assignment for the 2018 tax year. It begins by calculating the employment income of Art Vandelay, detailing various components such as salaries, commissions, employer contributions, and employment allowances. The calculation includes adjustments for taxable and non-taxable benefits, such as automobile benefits, and deductions for items like registered pension plan contributions and charitable donations. The assignment also determines the HST rebate to be claimed. Furthermore, it explores the tax implications of a signing bonus, moving allowances, interest-free loans, and non-compete agreements. The solution references the Income Tax Act and relevant Canadian Revenue Agency publications, providing a thorough understanding of the tax calculations and their underlying principles.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.