Engineering Management: Financial Analysis & Real Estate Valuation

VerifiedAdded on 2023/06/03

|14

|2695

|145

Report

AI Summary

This report presents a financial analysis of a residential complex development project, utilizing real estate valuation principles. It considers development costs, revenue escalation, and finance costs to determine future cash flows from the developer's perspective, including the potential sale to John Wiley Pty Ltd. The analysis evaluates the developer's profit and return, incorporating scenario analysis (optimistic and pessimistic) and assessing the impact of changing debt-equity ratios. Key findings include the total development cost of $486.07 million, a project financing cost based on a 12% interest rate, and an initial project development yield of 36%. The report also examines the potential sale of the facility for $900 million after 10 years, resulting in a net present value of $1052 million for John Wiley Pty Ltd. Risk factors such as financial risk, cost escalation, and macroeconomic conditions are discussed, with a sensitivity analysis conducted to assess the impact of revenue fluctuations.

Running head: Engineering Management

Engineering Management

Name of the Student:

Name of the University:

Author’s Note:

Engineering Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ENGINEERING MANAGEMENT

Executive Summary

The aim of the project is to conduct a financial analysis of a Development project where the

same is executed with the real estate valuation principles and techniques. The development

cost and the other key input costs were taken into account while the cash flows associated

with the same were revaluated. The project was analysed from the developers prospective and

the sale of the asset class was also shown to John Wiley Pty Ltd. The developers profit ad the

return generated by each of them is evaluated. The scenario analysis and the changing debt

effect has helped us evaluate the key sensitive components of the project.

Executive Summary

The aim of the project is to conduct a financial analysis of a Development project where the

same is executed with the real estate valuation principles and techniques. The development

cost and the other key input costs were taken into account while the cash flows associated

with the same were revaluated. The project was analysed from the developers prospective and

the sale of the asset class was also shown to John Wiley Pty Ltd. The developers profit ad the

return generated by each of them is evaluated. The scenario analysis and the changing debt

effect has helped us evaluate the key sensitive components of the project.

2ENGINEERING MANAGEMENT

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................7

Part C......................................................................................................................................9

Part D.....................................................................................................................................9

Part E....................................................................................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................7

Part C......................................................................................................................................9

Part D.....................................................................................................................................9

Part E....................................................................................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ENGINEERING MANAGEMENT

Introduction

The Financial evaluation and analysis has helped us evaluate the key concept of real

estate valuation. The proposed Sub Division Residential Complex Development Project

evaluation composed of evaluating the total development costs and the same was accounted

using factors given like annual escalation in revenue and costs and the same was used for

determining the future cash flows for the company. The key assumption used in the project

was the total development cost to be considered as the final and all total cost for the

development of the project basis on which the finance costs was also computed. The scenario

analysis has two factors evaluated one is the optimistic level scenario and the other is the

pessimistic scenario (Yeh and Hsu 2018).

Discussion

Part A

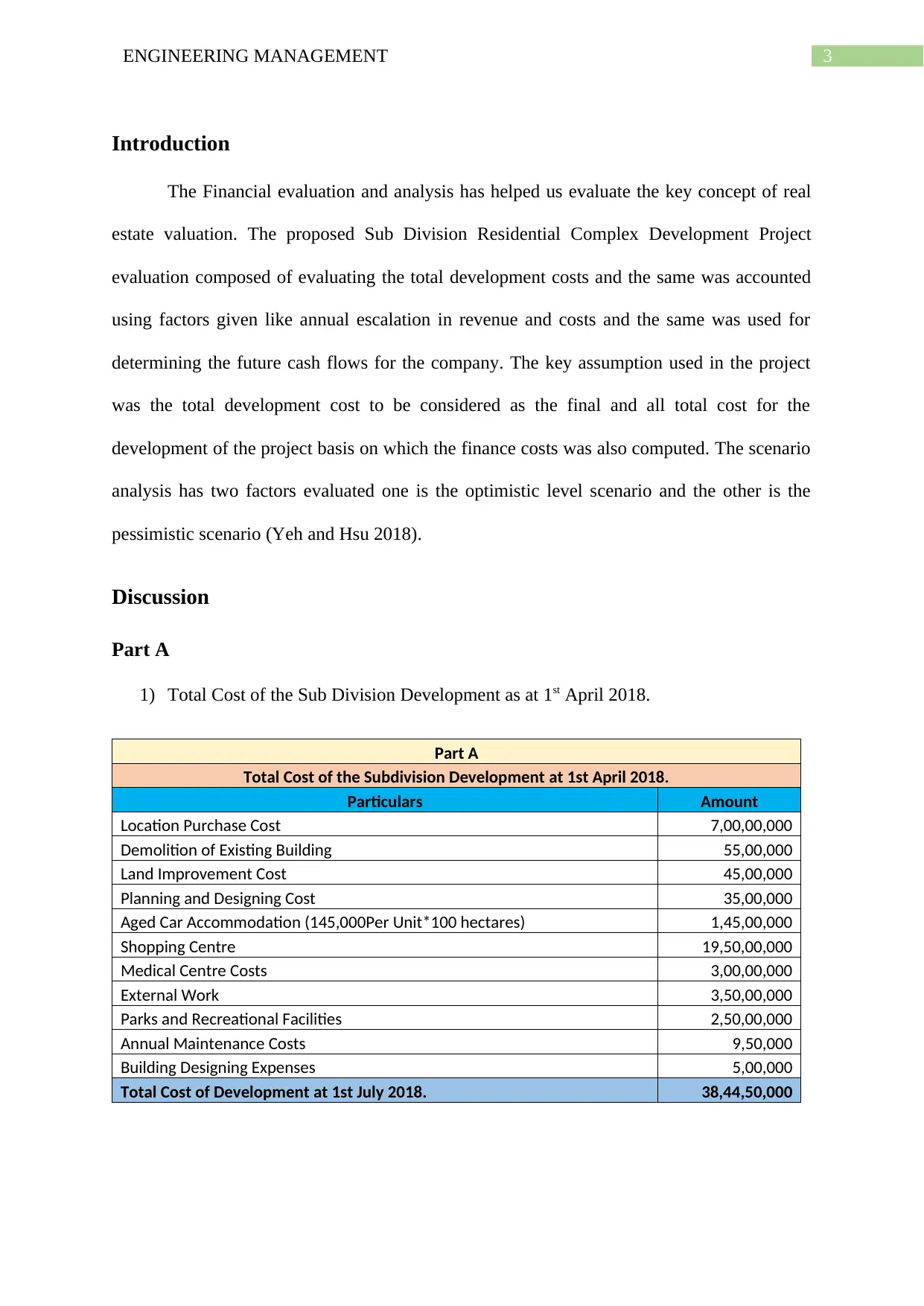

1) Total Cost of the Sub Division Development as at 1st April 2018.

Part A

Total Cost of the Subdivision Development at 1st April 2018.

Particulars Amount

Location Purchase Cost 7,00,00,000

Demolition of Existing Building 55,00,000

Land Improvement Cost 45,00,000

Planning and Designing Cost 35,00,000

Aged Car Accommodation (145,000Per Unit*100 hectares) 1,45,00,000

Shopping Centre 19,50,00,000

Medical Centre Costs 3,00,00,000

External Work 3,50,00,000

Parks and Recreational Facilities 2,50,00,000

Annual Maintenance Costs 9,50,000

Building Designing Expenses 5,00,000

Total Cost of Development at 1st July 2018. 38,44,50,000

Introduction

The Financial evaluation and analysis has helped us evaluate the key concept of real

estate valuation. The proposed Sub Division Residential Complex Development Project

evaluation composed of evaluating the total development costs and the same was accounted

using factors given like annual escalation in revenue and costs and the same was used for

determining the future cash flows for the company. The key assumption used in the project

was the total development cost to be considered as the final and all total cost for the

development of the project basis on which the finance costs was also computed. The scenario

analysis has two factors evaluated one is the optimistic level scenario and the other is the

pessimistic scenario (Yeh and Hsu 2018).

Discussion

Part A

1) Total Cost of the Sub Division Development as at 1st April 2018.

Part A

Total Cost of the Subdivision Development at 1st April 2018.

Particulars Amount

Location Purchase Cost 7,00,00,000

Demolition of Existing Building 55,00,000

Land Improvement Cost 45,00,000

Planning and Designing Cost 35,00,000

Aged Car Accommodation (145,000Per Unit*100 hectares) 1,45,00,000

Shopping Centre 19,50,00,000

Medical Centre Costs 3,00,00,000

External Work 3,50,00,000

Parks and Recreational Facilities 2,50,00,000

Annual Maintenance Costs 9,50,000

Building Designing Expenses 5,00,000

Total Cost of Development at 1st July 2018. 38,44,50,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ENGINEERING MANAGEMENT

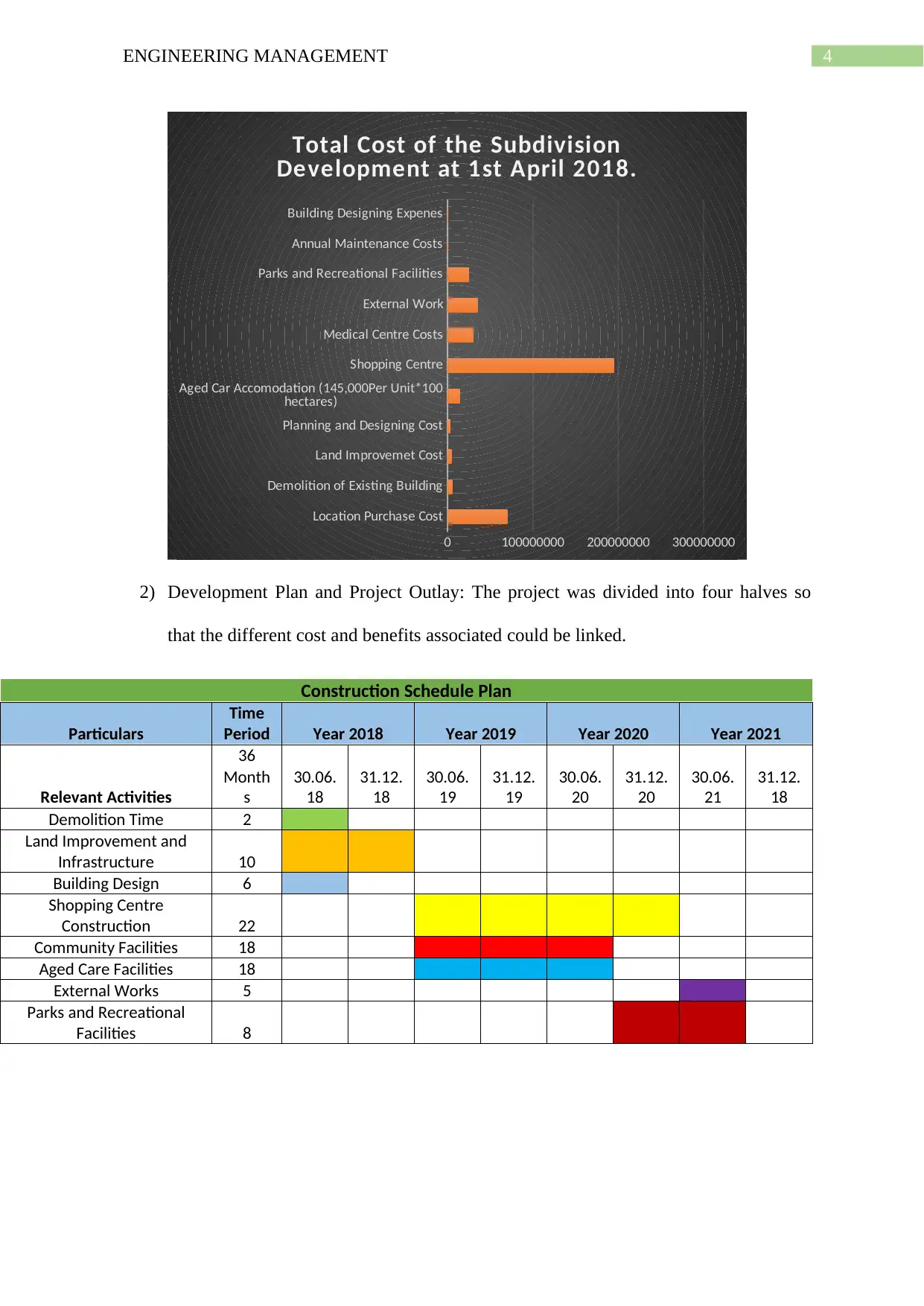

Location Purchase Cost

Demolition of Existing Building

Land Improvemet Cost

Planning and Designing Cost

Aged Car Accomodation (145,000Per Unit*100

hectares)

Shopping Centre

Medical Centre Costs

External Work

Parks and Recreational Facilities

Annual Maintenance Costs

Building Designing Expenes

0 100000000 200000000 300000000

Total Cost of the Subdivision

Development at 1st April 2018.

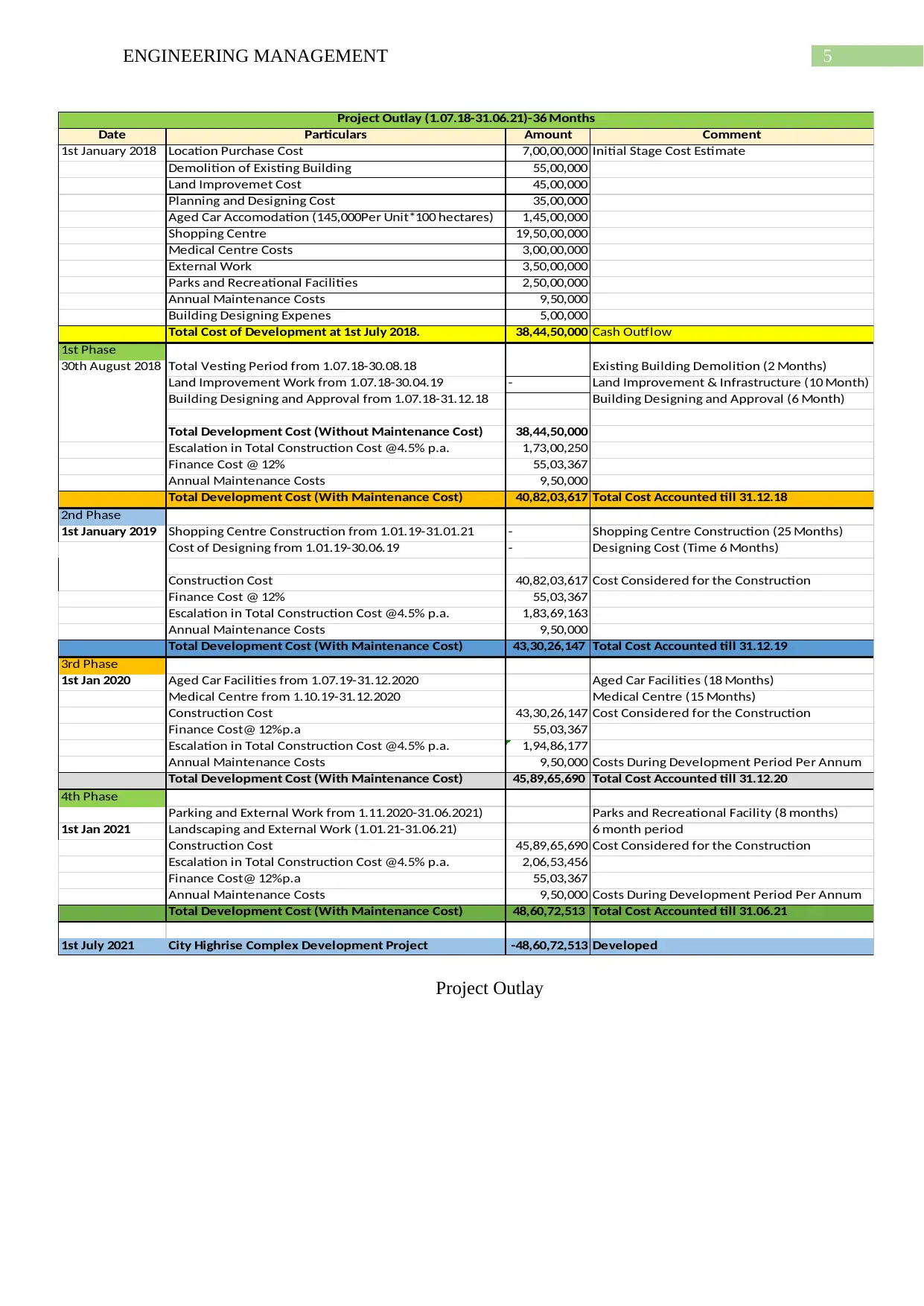

2) Development Plan and Project Outlay: The project was divided into four halves so

that the different cost and benefits associated could be linked.

Construction Schedule Plan

Particulars

Time

Period Year 2018 Year 2019 Year 2020 Year 2021

Relevant Activities

36

Month

s

30.06.

18

31.12.

18

30.06.

19

31.12.

19

30.06.

20

31.12.

20

30.06.

21

31.12.

18

Demolition Time 2

Land Improvement and

Infrastructure 10

Building Design 6

Shopping Centre

Construction 22

Community Facilities 18

Aged Care Facilities 18

External Works 5

Parks and Recreational

Facilities 8

Location Purchase Cost

Demolition of Existing Building

Land Improvemet Cost

Planning and Designing Cost

Aged Car Accomodation (145,000Per Unit*100

hectares)

Shopping Centre

Medical Centre Costs

External Work

Parks and Recreational Facilities

Annual Maintenance Costs

Building Designing Expenes

0 100000000 200000000 300000000

Total Cost of the Subdivision

Development at 1st April 2018.

2) Development Plan and Project Outlay: The project was divided into four halves so

that the different cost and benefits associated could be linked.

Construction Schedule Plan

Particulars

Time

Period Year 2018 Year 2019 Year 2020 Year 2021

Relevant Activities

36

Month

s

30.06.

18

31.12.

18

30.06.

19

31.12.

19

30.06.

20

31.12.

20

30.06.

21

31.12.

18

Demolition Time 2

Land Improvement and

Infrastructure 10

Building Design 6

Shopping Centre

Construction 22

Community Facilities 18

Aged Care Facilities 18

External Works 5

Parks and Recreational

Facilities 8

5ENGINEERING MANAGEMENT

Project Outlay

Date Particulars Amount Comment

1st January 2018 Location Purchase Cost 7,00,00,000 Initial Stage Cost Estimate

Demolition of Existing Building 55,00,000

Land Improvemet Cost 45,00,000

Planning and Designing Cost 35,00,000

Aged Car Accomodation (145,000Per Unit*100 hectares) 1,45,00,000

Shopping Centre 19,50,00,000

Medical Centre Costs 3,00,00,000

External Work 3,50,00,000

Parks and Recreational Facilities 2,50,00,000

Annual Maintenance Costs 9,50,000

Building Designing Expenes 5,00,000

Total Cost of Development at 1st July 2018. 38,44,50,000 Cash Outflow

1st Phase

30th August 2018 Total Vesting Period from 1.07.18-30.08.18 Existing Building Demolition (2 Months)

Land Improvement Work from 1.07.18-30.04.19 - Land Improvement & Infrastructure (10 Month)

Building Designing and Approval from 1.07.18-31.12.18 Building Designing and Approval (6 Month)

Total Development Cost (Without Maintenance Cost) 38,44,50,000

Escalation in Total Construction Cost @4.5% p.a. 1,73,00,250

Finance Cost @ 12% 55,03,367

Annual Maintenance Costs 9,50,000

Total Development Cost (With Maintenance Cost) 40,82,03,617 Total Cost Accounted till 31.12.18

2nd Phase

1st January 2019 Shopping Centre Construction from 1.01.19-31.01.21 - Shopping Centre Construction (25 Months)

Cost of Designing from 1.01.19-30.06.19 - Designing Cost (Time 6 Months)

Construction Cost 40,82,03,617 Cost Considered for the Construction

Finance Cost @ 12% 55,03,367

Escalation in Total Construction Cost @4.5% p.a. 1,83,69,163

Annual Maintenance Costs 9,50,000

Total Development Cost (With Maintenance Cost) 43,30,26,147 Total Cost Accounted till 31.12.19

3rd Phase

1st Jan 2020 Aged Car Facilities from 1.07.19-31.12.2020 Aged Car Facilities (18 Months)

Medical Centre from 1.10.19-31.12.2020 Medical Centre (15 Months)

Construction Cost 43,30,26,147 Cost Considered for the Construction

Finance Cost@ 12%p.a 55,03,367

Escalation in Total Construction Cost @4.5% p.a. 1,94,86,177

Annual Maintenance Costs 9,50,000 Costs During Development Period Per Annum

Total Development Cost (With Maintenance Cost) 45,89,65,690 Total Cost Accounted till 31.12.20

4th Phase

Parking and External Work from 1.11.2020-31.06.2021) Parks and Recreational Facility (8 months)

1st Jan 2021 Landscaping and External Work (1.01.21-31.06.21) 6 month period

Construction Cost 45,89,65,690 Cost Considered for the Construction

Escalation in Total Construction Cost @4.5% p.a. 2,06,53,456

Finance Cost@ 12%p.a 55,03,367

Annual Maintenance Costs 9,50,000 Costs During Development Period Per Annum

Total Development Cost (With Maintenance Cost) 48,60,72,513 Total Cost Accounted till 31.06.21

1st July 2021 City Highrise Complex Development Project -48,60,72,513 Developed

Project Outlay (1.07.18-31.06.21)-36 Months

Project Outlay

Date Particulars Amount Comment

1st January 2018 Location Purchase Cost 7,00,00,000 Initial Stage Cost Estimate

Demolition of Existing Building 55,00,000

Land Improvemet Cost 45,00,000

Planning and Designing Cost 35,00,000

Aged Car Accomodation (145,000Per Unit*100 hectares) 1,45,00,000

Shopping Centre 19,50,00,000

Medical Centre Costs 3,00,00,000

External Work 3,50,00,000

Parks and Recreational Facilities 2,50,00,000

Annual Maintenance Costs 9,50,000

Building Designing Expenes 5,00,000

Total Cost of Development at 1st July 2018. 38,44,50,000 Cash Outflow

1st Phase

30th August 2018 Total Vesting Period from 1.07.18-30.08.18 Existing Building Demolition (2 Months)

Land Improvement Work from 1.07.18-30.04.19 - Land Improvement & Infrastructure (10 Month)

Building Designing and Approval from 1.07.18-31.12.18 Building Designing and Approval (6 Month)

Total Development Cost (Without Maintenance Cost) 38,44,50,000

Escalation in Total Construction Cost @4.5% p.a. 1,73,00,250

Finance Cost @ 12% 55,03,367

Annual Maintenance Costs 9,50,000

Total Development Cost (With Maintenance Cost) 40,82,03,617 Total Cost Accounted till 31.12.18

2nd Phase

1st January 2019 Shopping Centre Construction from 1.01.19-31.01.21 - Shopping Centre Construction (25 Months)

Cost of Designing from 1.01.19-30.06.19 - Designing Cost (Time 6 Months)

Construction Cost 40,82,03,617 Cost Considered for the Construction

Finance Cost @ 12% 55,03,367

Escalation in Total Construction Cost @4.5% p.a. 1,83,69,163

Annual Maintenance Costs 9,50,000

Total Development Cost (With Maintenance Cost) 43,30,26,147 Total Cost Accounted till 31.12.19

3rd Phase

1st Jan 2020 Aged Car Facilities from 1.07.19-31.12.2020 Aged Car Facilities (18 Months)

Medical Centre from 1.10.19-31.12.2020 Medical Centre (15 Months)

Construction Cost 43,30,26,147 Cost Considered for the Construction

Finance Cost@ 12%p.a 55,03,367

Escalation in Total Construction Cost @4.5% p.a. 1,94,86,177

Annual Maintenance Costs 9,50,000 Costs During Development Period Per Annum

Total Development Cost (With Maintenance Cost) 45,89,65,690 Total Cost Accounted till 31.12.20

4th Phase

Parking and External Work from 1.11.2020-31.06.2021) Parks and Recreational Facility (8 months)

1st Jan 2021 Landscaping and External Work (1.01.21-31.06.21) 6 month period

Construction Cost 45,89,65,690 Cost Considered for the Construction

Escalation in Total Construction Cost @4.5% p.a. 2,06,53,456

Finance Cost@ 12%p.a 55,03,367

Annual Maintenance Costs 9,50,000 Costs During Development Period Per Annum

Total Development Cost (With Maintenance Cost) 48,60,72,513 Total Cost Accounted till 31.06.21

1st July 2021 City Highrise Complex Development Project -48,60,72,513 Developed

Project Outlay (1.07.18-31.06.21)-36 Months

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ENGINEERING MANAGEMENT

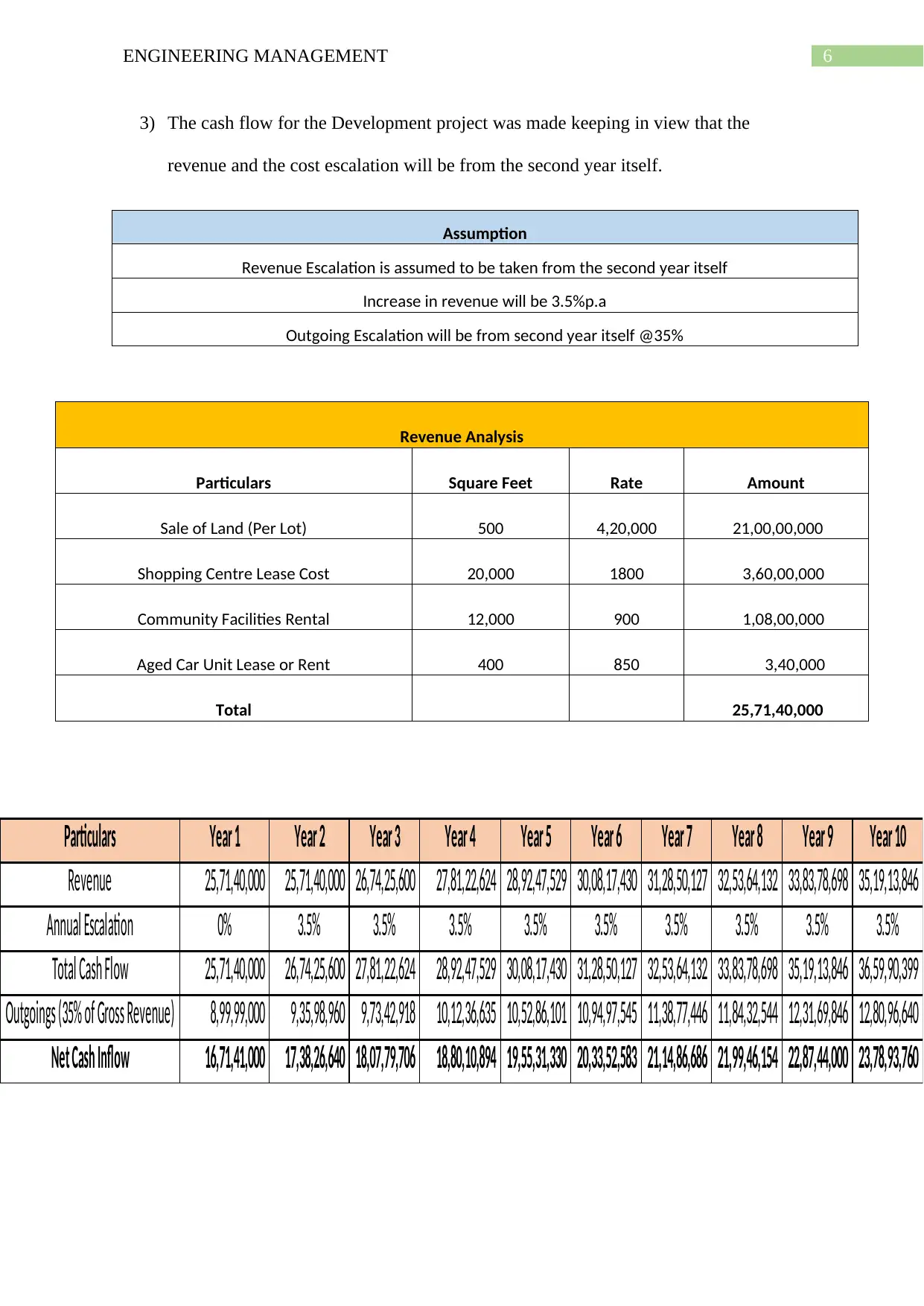

3) The cash flow for the Development project was made keeping in view that the

revenue and the cost escalation will be from the second year itself.

Assumption

Revenue Escalation is assumed to be taken from the second year itself

Increase in revenue will be 3.5%p.a

Outgoing Escalation will be from second year itself @35%

Revenue Analysis

Particulars Square Feet Rate Amount

Sale of Land (Per Lot) 500 4,20,000 21,00,00,000

Shopping Centre Lease Cost 20,000 1800 3,60,00,000

Community Facilities Rental 12,000 900 1,08,00,000

Aged Car Unit Lease or Rent 400 850 3,40,000

Total 25,71,40,000

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 23,78,93,760

3) The cash flow for the Development project was made keeping in view that the

revenue and the cost escalation will be from the second year itself.

Assumption

Revenue Escalation is assumed to be taken from the second year itself

Increase in revenue will be 3.5%p.a

Outgoing Escalation will be from second year itself @35%

Revenue Analysis

Particulars Square Feet Rate Amount

Sale of Land (Per Lot) 500 4,20,000 21,00,00,000

Shopping Centre Lease Cost 20,000 1800 3,60,00,000

Community Facilities Rental 12,000 900 1,08,00,000

Aged Car Unit Lease or Rent 400 850 3,40,000

Total 25,71,40,000

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 23,78,93,760

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ENGINEERING MANAGEMENT

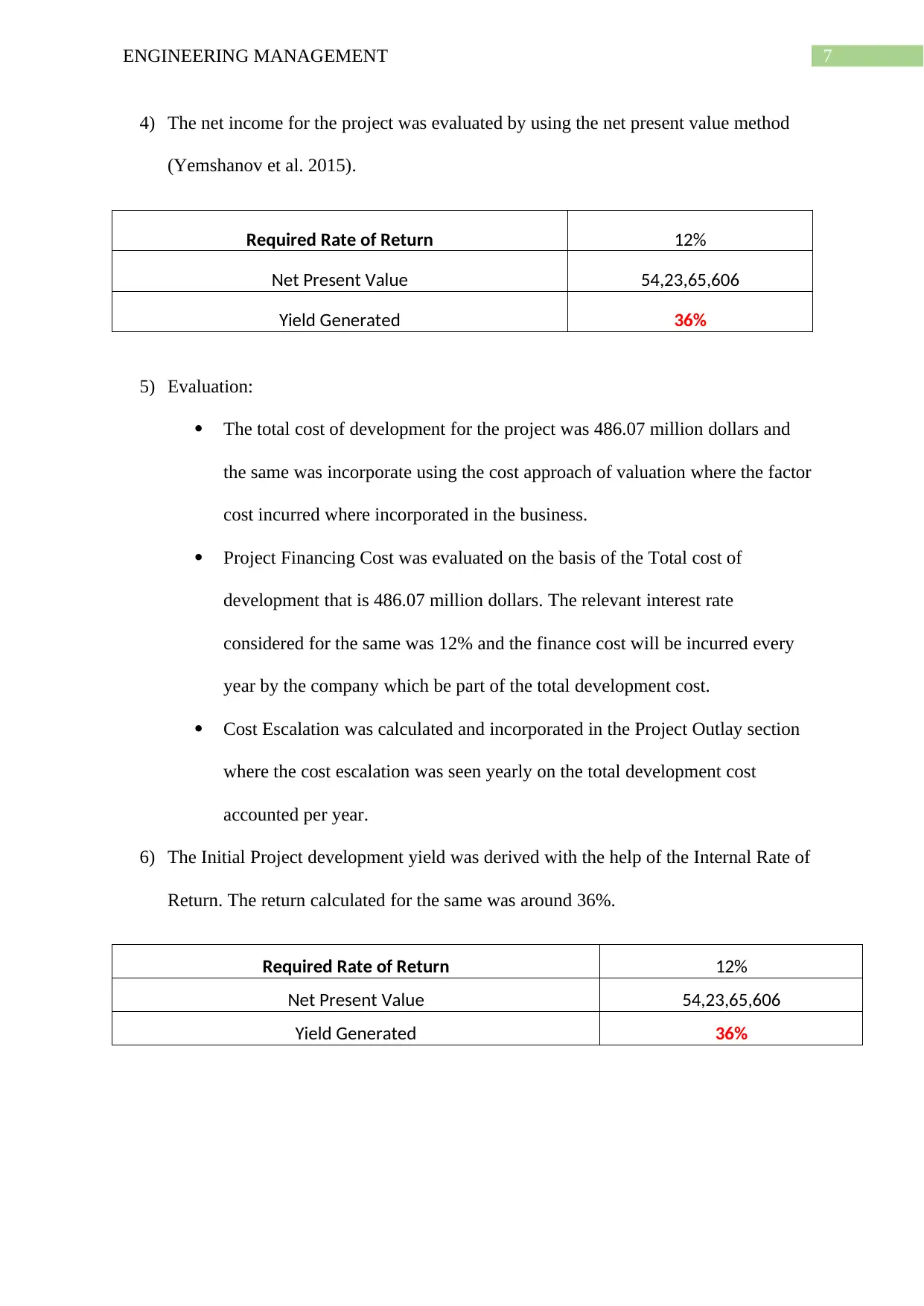

4) The net income for the project was evaluated by using the net present value method

(Yemshanov et al. 2015).

Required Rate of Return 12%

Net Present Value 54,23,65,606

Yield Generated 36%

5) Evaluation:

The total cost of development for the project was 486.07 million dollars and

the same was incorporate using the cost approach of valuation where the factor

cost incurred where incorporated in the business.

Project Financing Cost was evaluated on the basis of the Total cost of

development that is 486.07 million dollars. The relevant interest rate

considered for the same was 12% and the finance cost will be incurred every

year by the company which be part of the total development cost.

Cost Escalation was calculated and incorporated in the Project Outlay section

where the cost escalation was seen yearly on the total development cost

accounted per year.

6) The Initial Project development yield was derived with the help of the Internal Rate of

Return. The return calculated for the same was around 36%.

Required Rate of Return 12%

Net Present Value 54,23,65,606

Yield Generated 36%

4) The net income for the project was evaluated by using the net present value method

(Yemshanov et al. 2015).

Required Rate of Return 12%

Net Present Value 54,23,65,606

Yield Generated 36%

5) Evaluation:

The total cost of development for the project was 486.07 million dollars and

the same was incorporate using the cost approach of valuation where the factor

cost incurred where incorporated in the business.

Project Financing Cost was evaluated on the basis of the Total cost of

development that is 486.07 million dollars. The relevant interest rate

considered for the same was 12% and the finance cost will be incurred every

year by the company which be part of the total development cost.

Cost Escalation was calculated and incorporated in the Project Outlay section

where the cost escalation was seen yearly on the total development cost

accounted per year.

6) The Initial Project development yield was derived with the help of the Internal Rate of

Return. The return calculated for the same was around 36%.

Required Rate of Return 12%

Net Present Value 54,23,65,606

Yield Generated 36%

8ENGINEERING MANAGEMENT

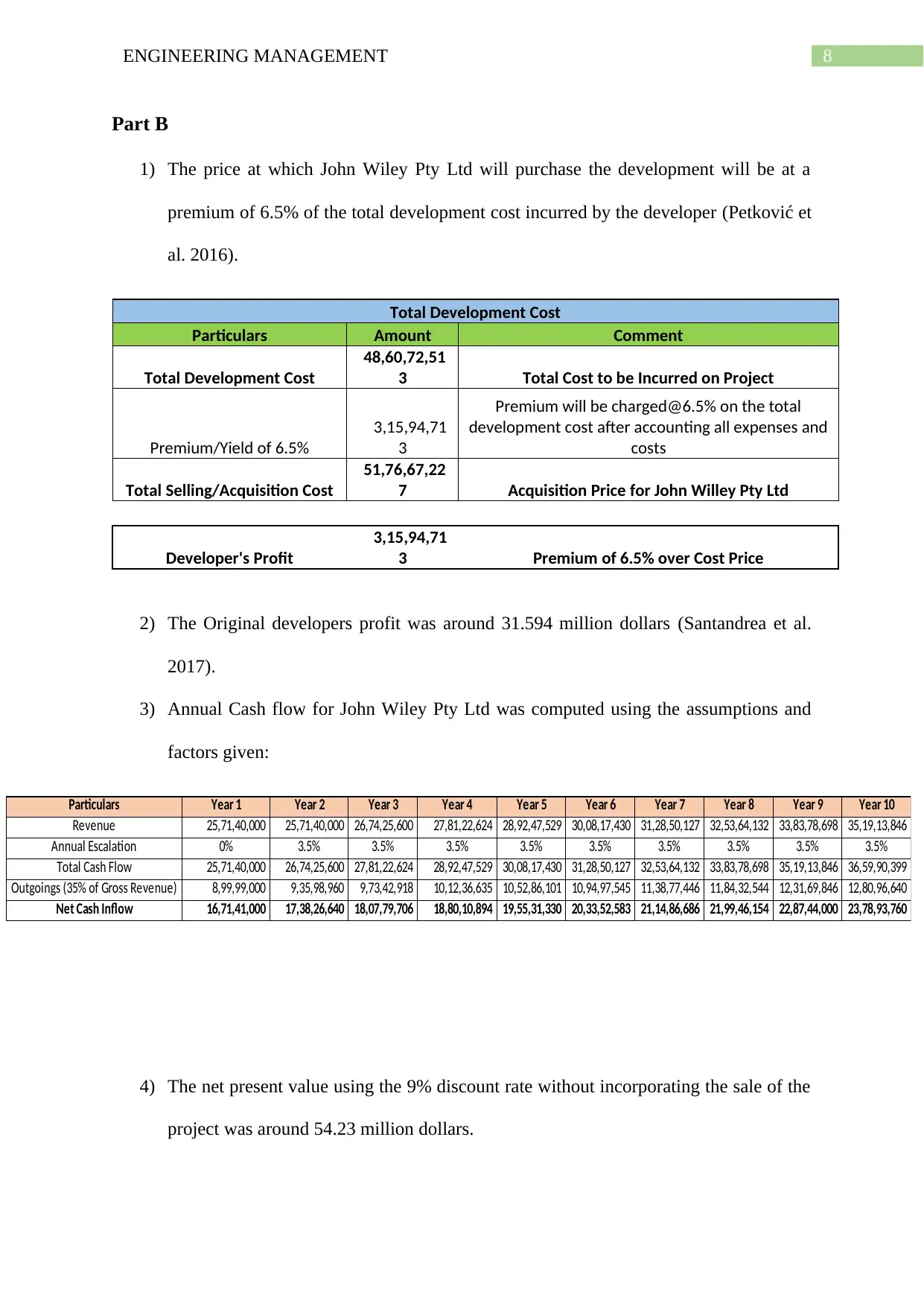

Part B

1) The price at which John Wiley Pty Ltd will purchase the development will be at a

premium of 6.5% of the total development cost incurred by the developer (Petković et

al. 2016).

Total Development Cost

Particulars Amount Comment

Total Development Cost

48,60,72,51

3 Total Cost to be Incurred on Project

Premium/Yield of 6.5%

3,15,94,71

3

Premium will be charged@6.5% on the total

development cost after accounting all expenses and

costs

Total Selling/Acquisition Cost

51,76,67,22

7 Acquisition Price for John Willey Pty Ltd

Developer's Profit

3,15,94,71

3 Premium of 6.5% over Cost Price

2) The Original developers profit was around 31.594 million dollars (Santandrea et al.

2017).

3) Annual Cash flow for John Wiley Pty Ltd was computed using the assumptions and

factors given:

4) The net present value using the 9% discount rate without incorporating the sale of the

project was around 54.23 million dollars.

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 23,78,93,760

Part B

1) The price at which John Wiley Pty Ltd will purchase the development will be at a

premium of 6.5% of the total development cost incurred by the developer (Petković et

al. 2016).

Total Development Cost

Particulars Amount Comment

Total Development Cost

48,60,72,51

3 Total Cost to be Incurred on Project

Premium/Yield of 6.5%

3,15,94,71

3

Premium will be charged@6.5% on the total

development cost after accounting all expenses and

costs

Total Selling/Acquisition Cost

51,76,67,22

7 Acquisition Price for John Willey Pty Ltd

Developer's Profit

3,15,94,71

3 Premium of 6.5% over Cost Price

2) The Original developers profit was around 31.594 million dollars (Santandrea et al.

2017).

3) Annual Cash flow for John Wiley Pty Ltd was computed using the assumptions and

factors given:

4) The net present value using the 9% discount rate without incorporating the sale of the

project was around 54.23 million dollars.

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 23,78,93,760

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ENGINEERING MANAGEMENT

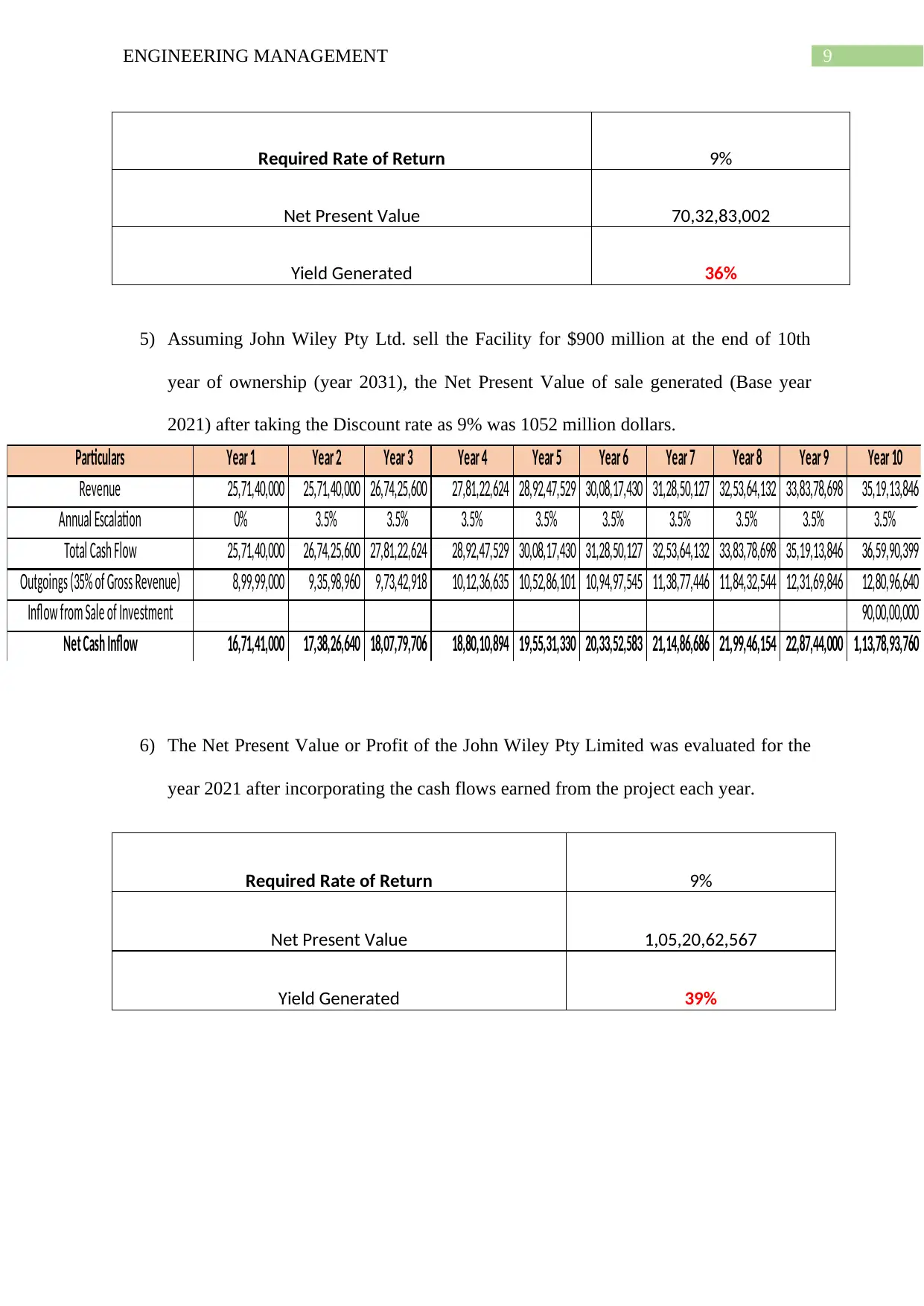

Required Rate of Return 9%

Net Present Value 70,32,83,002

Yield Generated 36%

5) Assuming John Wiley Pty Ltd. sell the Facility for $900 million at the end of 10th

year of ownership (year 2031), the Net Present Value of sale generated (Base year

2021) after taking the Discount rate as 9% was 1052 million dollars.

6) The Net Present Value or Profit of the John Wiley Pty Limited was evaluated for the

year 2021 after incorporating the cash flows earned from the project each year.

Required Rate of Return 9%

Net Present Value 1,05,20,62,567

Yield Generated 39%

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Inflow from Sale of Investment 90,00,00,000

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 1,13,78,93,760

Required Rate of Return 9%

Net Present Value 70,32,83,002

Yield Generated 36%

5) Assuming John Wiley Pty Ltd. sell the Facility for $900 million at the end of 10th

year of ownership (year 2031), the Net Present Value of sale generated (Base year

2021) after taking the Discount rate as 9% was 1052 million dollars.

6) The Net Present Value or Profit of the John Wiley Pty Limited was evaluated for the

year 2021 after incorporating the cash flows earned from the project each year.

Required Rate of Return 9%

Net Present Value 1,05,20,62,567

Yield Generated 39%

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Revenue 25,71,40,000 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846

Annual Escalation 0% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

Total Cash Flow 25,71,40,000 26,74,25,600 27,81,22,624 28,92,47,529 30,08,17,430 31,28,50,127 32,53,64,132 33,83,78,698 35,19,13,846 36,59,90,399

Outgoings (35% of Gross Revenue) 8,99,99,000 9,35,98,960 9,73,42,918 10,12,36,635 10,52,86,101 10,94,97,545 11,38,77,446 11,84,32,544 12,31,69,846 12,80,96,640

Inflow from Sale of Investment 90,00,00,000

Net Cash Inflow 16,71,41,000 17,38,26,640 18,07,79,706 18,80,10,894 19,55,31,330 20,33,52,583 21,14,86,686 21,99,46,154 22,87,44,000 1,13,78,93,760

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ENGINEERING MANAGEMENT

Part C

After a careful analysis of the various scenarios we found out scenario 1 to be more positive

as the same will create wealth for the company and yield better returns (Ng and Beruvides,

2015).

Part D

If the debt: equity ratio structure of the company changes from 80:20 to 50:50 the company

will be able to save the finance costs that is spent each year on the total development costs.

The interest rate @ 12% is too high for the company implying that the finance cost for the

company plays a dominant role (Donovan 2015). The change in the debt equity structure of

the company will also help the company reduce the financial risk of the project as the project

suffers from business risk due to operations in real estate sector which is highly correlated to

the macro economic conditions of an economy.

Part E

1) The possible risk associated with the project that may influence the development

personal of the project is the financial risk of the project, cost escalation in the project

and the correlation of the business activity with the macro economic conditions like

inflation. Annual maintenance costs and rate of escalation assumed for evaluation

assumed for the project are also crucial part as the growth rate in revenue may rise or

fall depending upon the demand and class of asset or project (Aizenman and Jinjarak

2014).

2) The three key risks that needs further evaluation is the financial risk, escalation of

costs and the inflation factor in the project (Aizenman and Jinjarak 2014).

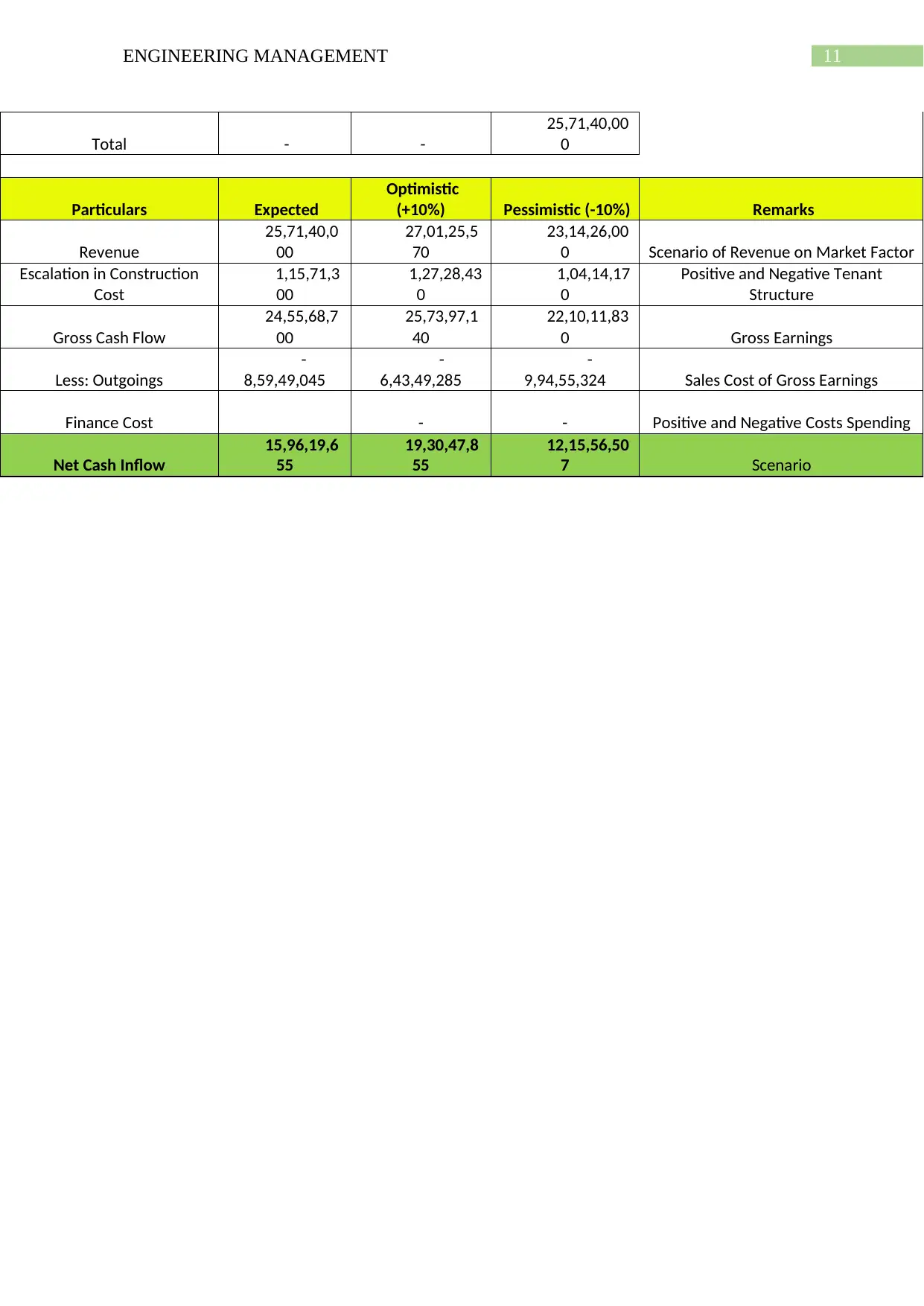

3) Sensitivity Analysis.

Total Revenue

Particulars Square Feet Average Rate Amount

Part C

After a careful analysis of the various scenarios we found out scenario 1 to be more positive

as the same will create wealth for the company and yield better returns (Ng and Beruvides,

2015).

Part D

If the debt: equity ratio structure of the company changes from 80:20 to 50:50 the company

will be able to save the finance costs that is spent each year on the total development costs.

The interest rate @ 12% is too high for the company implying that the finance cost for the

company plays a dominant role (Donovan 2015). The change in the debt equity structure of

the company will also help the company reduce the financial risk of the project as the project

suffers from business risk due to operations in real estate sector which is highly correlated to

the macro economic conditions of an economy.

Part E

1) The possible risk associated with the project that may influence the development

personal of the project is the financial risk of the project, cost escalation in the project

and the correlation of the business activity with the macro economic conditions like

inflation. Annual maintenance costs and rate of escalation assumed for evaluation

assumed for the project are also crucial part as the growth rate in revenue may rise or

fall depending upon the demand and class of asset or project (Aizenman and Jinjarak

2014).

2) The three key risks that needs further evaluation is the financial risk, escalation of

costs and the inflation factor in the project (Aizenman and Jinjarak 2014).

3) Sensitivity Analysis.

Total Revenue

Particulars Square Feet Average Rate Amount

11ENGINEERING MANAGEMENT

Total - -

25,71,40,00

0

Particulars Expected

Optimistic

(+10%) Pessimistic (-10%) Remarks

Revenue

25,71,40,0

00

27,01,25,5

70

23,14,26,00

0 Scenario of Revenue on Market Factor

Escalation in Construction

Cost

1,15,71,3

00

1,27,28,43

0

1,04,14,17

0

Positive and Negative Tenant

Structure

Gross Cash Flow

24,55,68,7

00

25,73,97,1

40

22,10,11,83

0 Gross Earnings

Less: Outgoings

-

8,59,49,045

-

6,43,49,285

-

9,94,55,324 Sales Cost of Gross Earnings

Finance Cost - - Positive and Negative Costs Spending

Net Cash Inflow

15,96,19,6

55

19,30,47,8

55

12,15,56,50

7 Scenario

Total - -

25,71,40,00

0

Particulars Expected

Optimistic

(+10%) Pessimistic (-10%) Remarks

Revenue

25,71,40,0

00

27,01,25,5

70

23,14,26,00

0 Scenario of Revenue on Market Factor

Escalation in Construction

Cost

1,15,71,3

00

1,27,28,43

0

1,04,14,17

0

Positive and Negative Tenant

Structure

Gross Cash Flow

24,55,68,7

00

25,73,97,1

40

22,10,11,83

0 Gross Earnings

Less: Outgoings

-

8,59,49,045

-

6,43,49,285

-

9,94,55,324 Sales Cost of Gross Earnings

Finance Cost - - Positive and Negative Costs Spending

Net Cash Inflow

15,96,19,6

55

19,30,47,8

55

12,15,56,50

7 Scenario

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.