Engineering Economics Assignment: Investment Analysis and NPV

VerifiedAdded on 2022/09/10

|8

|1107

|15

Homework Assignment

AI Summary

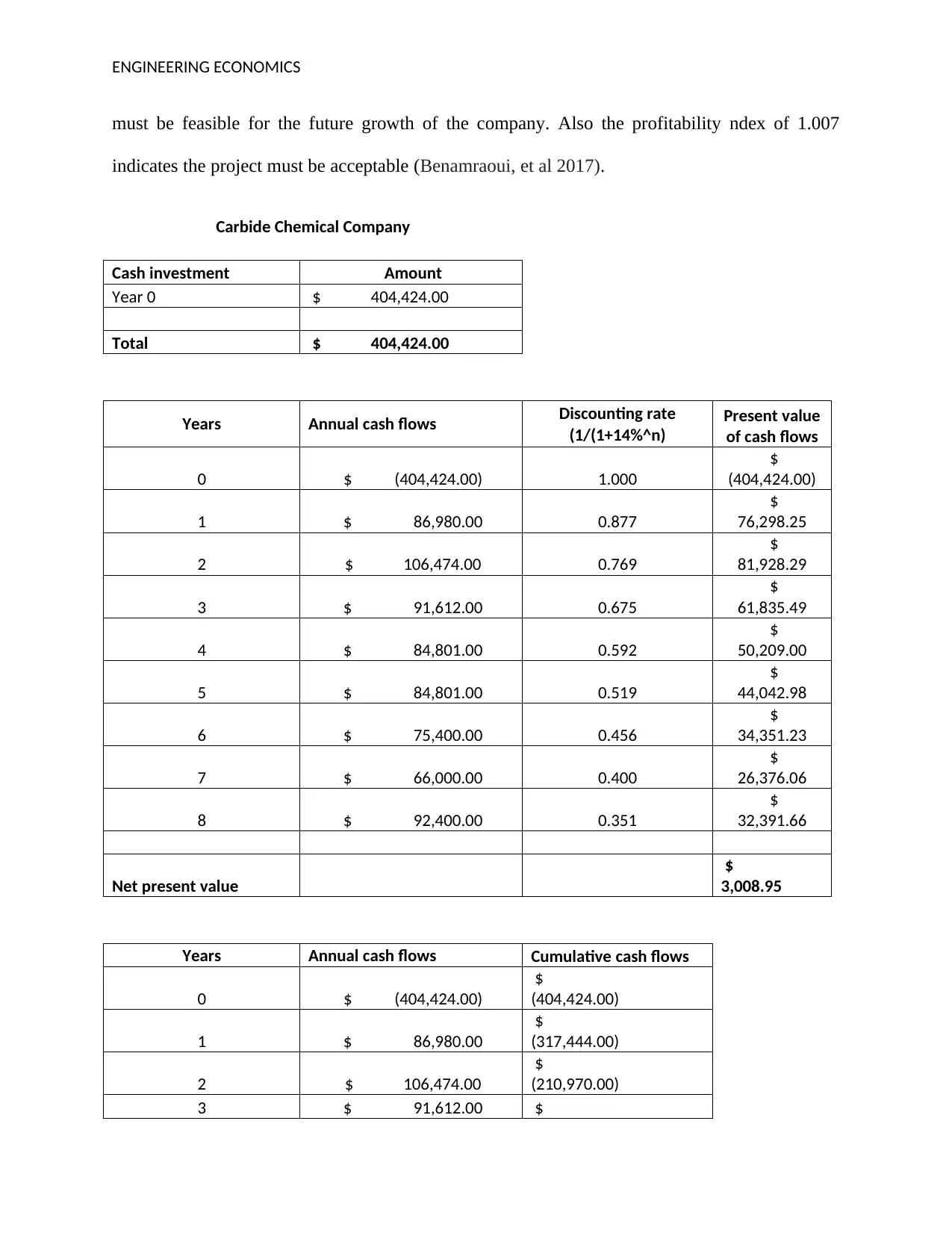

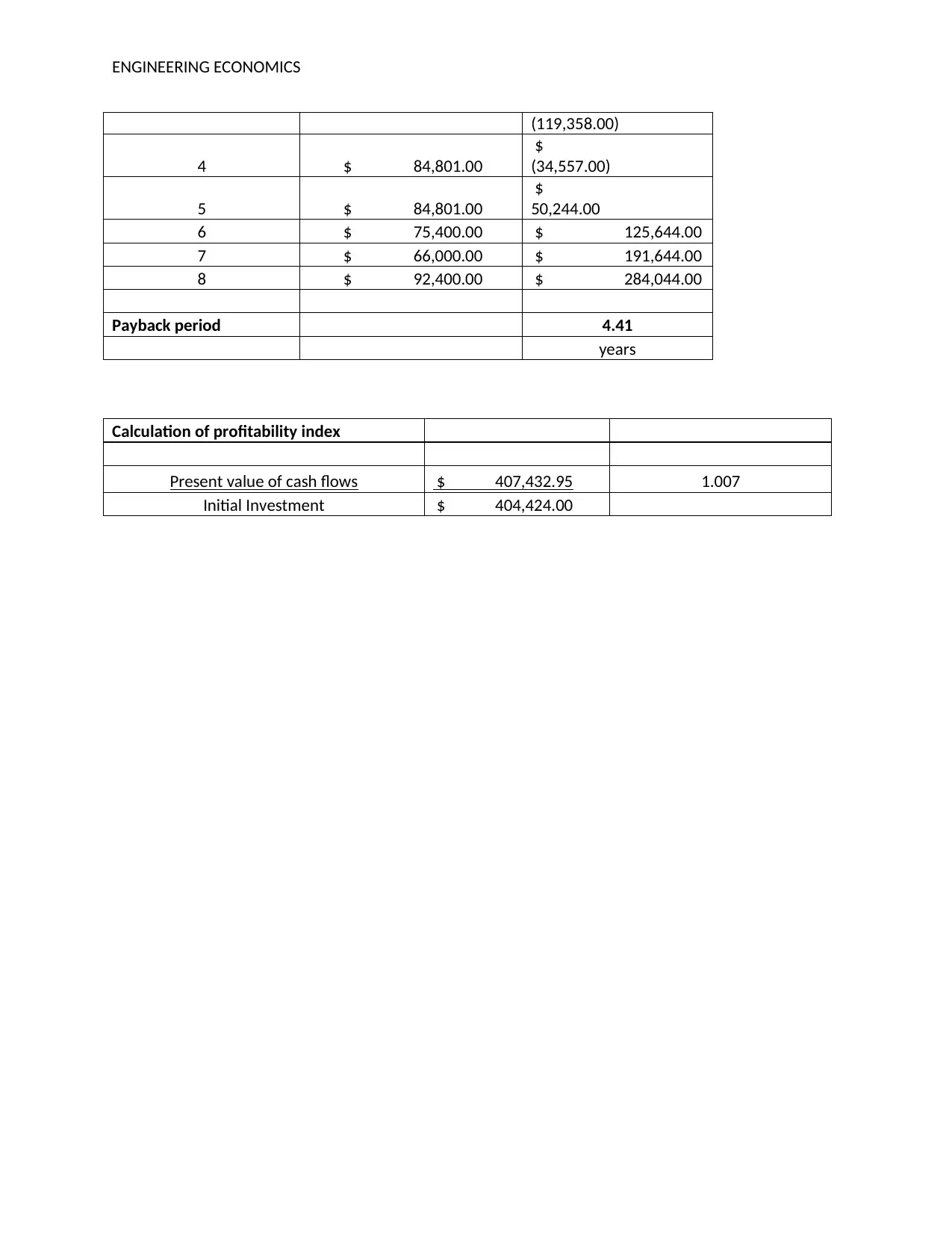

This Engineering Economics assignment analyzes various investment scenarios using techniques like Net Present Value (NPV), Payback Period, and Profitability Index. The assignment begins with a cash flow analysis, considering inflows and outflows to determine the net cash flow over a five-year period. The second question evaluates the Briarcliff Stove Company's new product line, calculating its NPV, payback period, and profitability index under different discount rates. The analysis indicates the project's feasibility based on the financial metrics. Finally, the third question assesses the Carbide Chemical Company's machine replacement proposal, determining its NPV, payback period, and profitability index to evaluate the project's acceptability. The solutions include detailed calculations, tables, and interpretations of the financial results, providing a comprehensive understanding of the investment decision-making process. The assignment demonstrates the application of economic principles in engineering projects.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.