HI6026 Audit, Assurance and Compliance: Enhanced Auditor Reporting

VerifiedAdded on 2023/06/04

|17

|3396

|279

Report

AI Summary

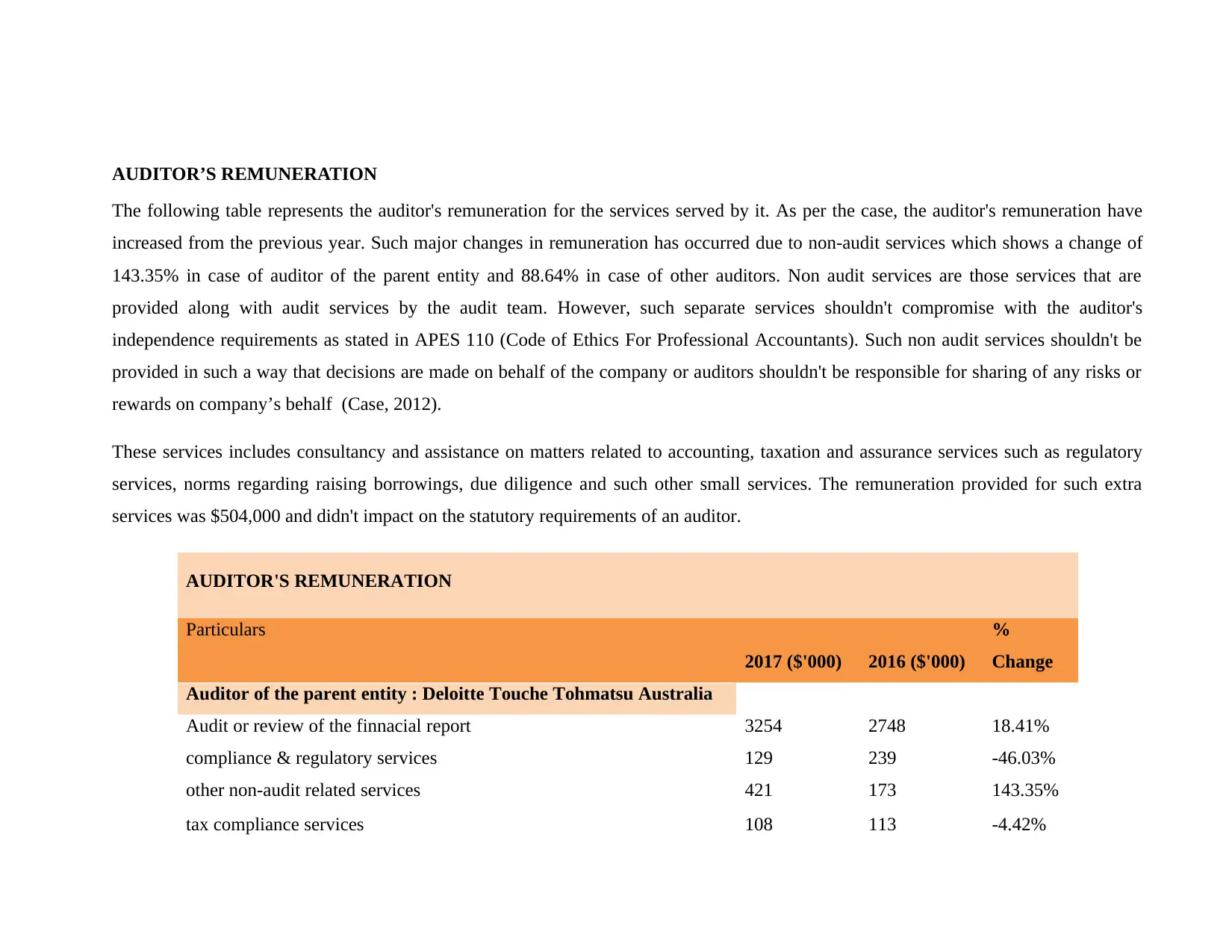

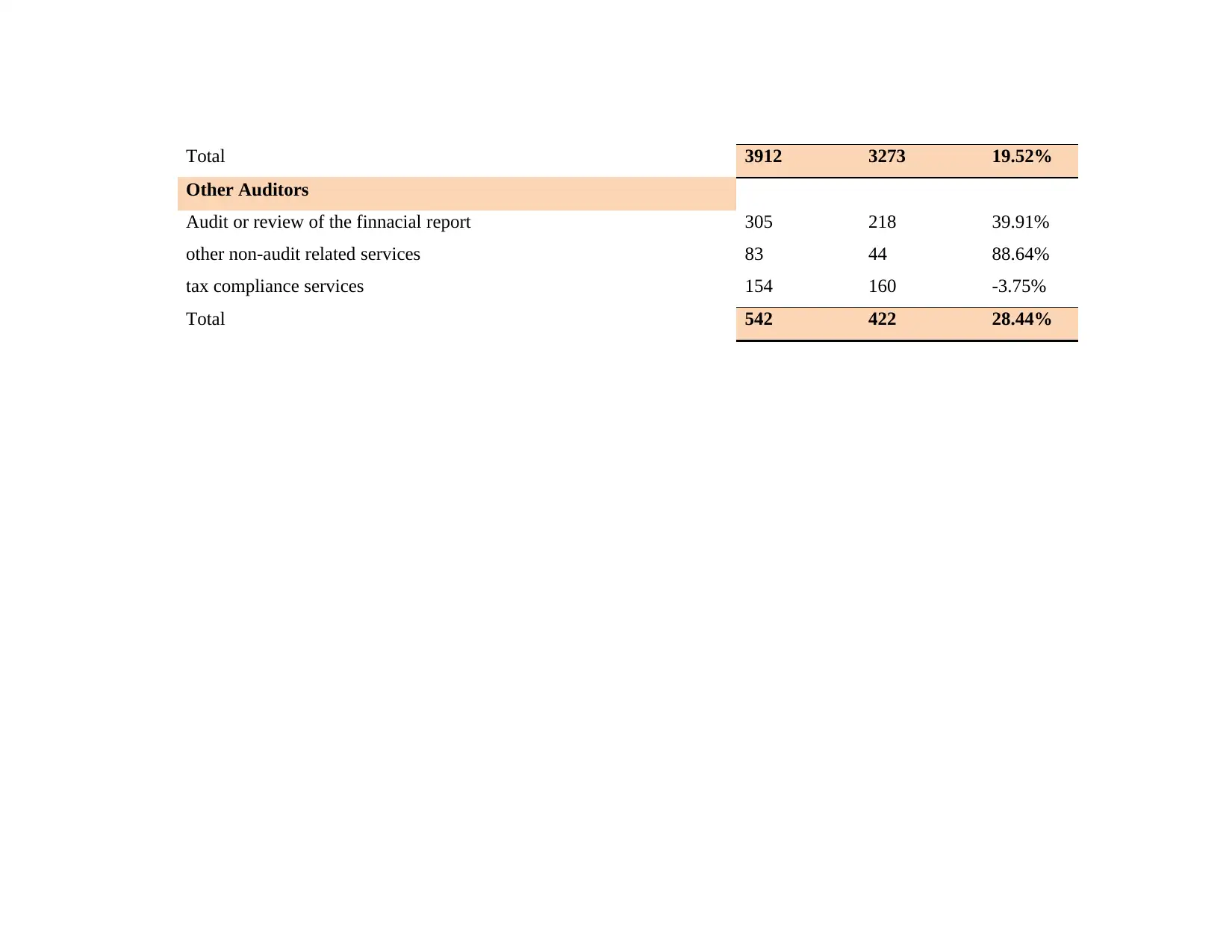

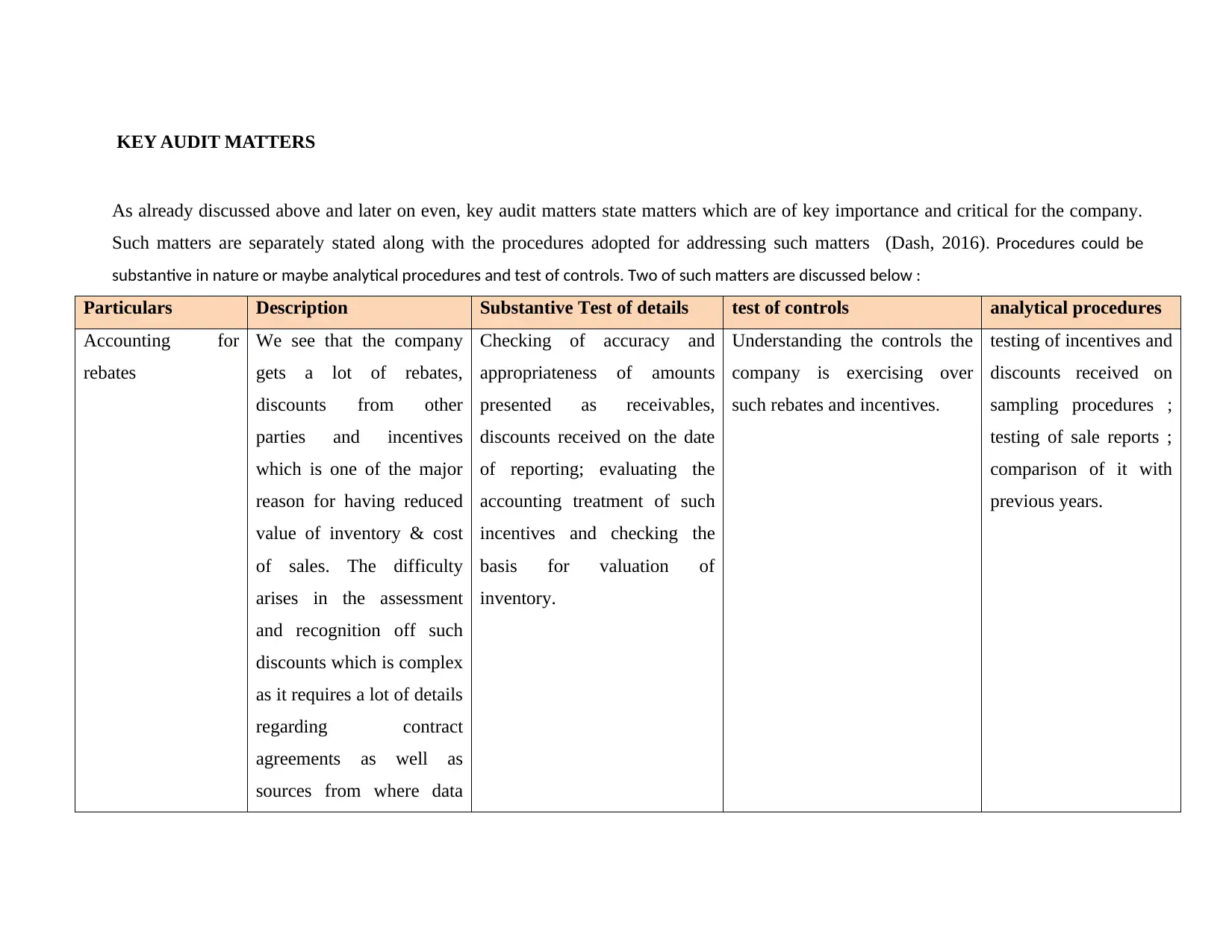

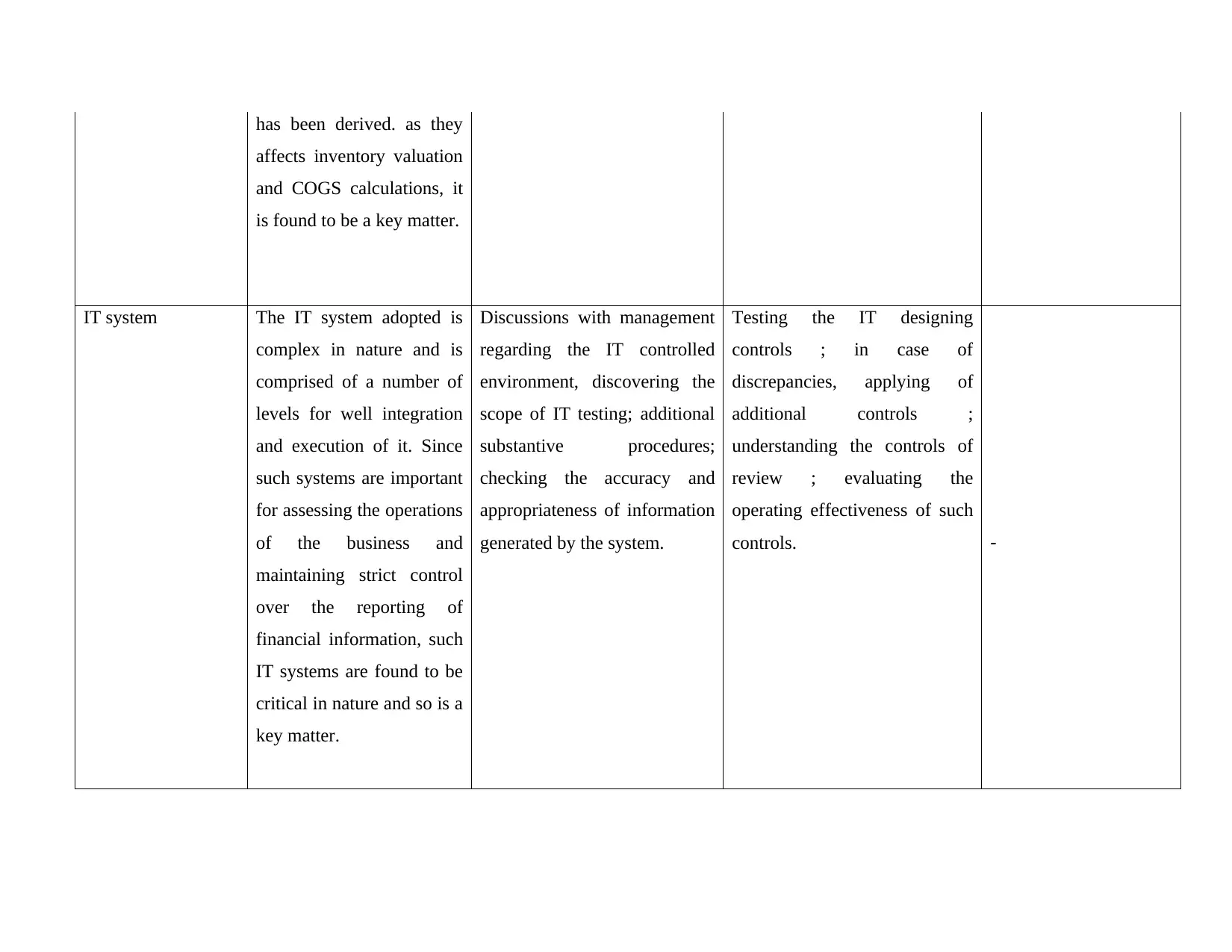

This report provides an executive summary of audit, assurance, and compliance practices, focusing on the enhanced auditor reporting implemented in Australia since 2016. It examines the introduction of 'key audit matters' in auditor's reports to improve transparency and the use of 'plain English' to communicate critical issues. The report analyzes the audit of Woolworths Limited, discussing auditor's remuneration, the importance of the audit committee charter, and the auditor's opinion. It also explores the responsibilities of management and auditors, subsequent events, and the concept of a true and fair view. The report highlights the significance of key audit matters, such as accounting rebates and IT systems, and their impact on financial reporting. Furthermore, it delves into the role of the audit committee and its charter in ensuring quality and compliance. The report concludes with an overview of the auditor's opinion, management and auditor responsibilities, and the relevance of subsequent events in financial reporting, providing a comprehensive understanding of the evolving landscape of audit practices in Australia. This report is a valuable resource for students, available on Desklib, which offers past papers and solved assignments to aid in their studies.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.