HI6026 Audit, Assurance & Compliance: Enhanced Reporting in Australia

VerifiedAdded on 2023/06/04

|15

|3403

|163

Report

AI Summary

This report assesses the roles and responsibilities of auditors in providing assurance for Origin Energy's financial statements. It analyzes audit independence, non-audit services, auditor remuneration, key audit matters, and the audit committee's role. The report examines the percentage change in audit remuneration from 2017 to 2018 and evaluates auditor responsibilities in assessing key audit matters, material subsequent events, and partially assessed material information. The analysis covers the auditor's adherence to independence standards, the impact of non-audit services, and the audit committee's oversight. Key audit matters, such as the carrying value of equity investments and accounting for derivative financial assets, are discussed in detail, along with the audit procedures used to address them. The report concludes by summarizing the findings and highlighting the importance of enhanced auditor reporting in Australia.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Executive Summary

The report has been developed with the intention to assess the roles and responsibilities of the

auditors in the process to provide assurance to the financial statements of Origin Energy.

Considering this purpose of the report, all the required part in the annual report of Origin

Energy related to the audit have been analyzed and evaluated. Various segments of auditing

covered by this report are audit independence, non-audit service, auditor’s remuneration, key

audit matters, audit committee, responsibility of the auditors and directors towards financial

reporting, assessment of the material subsequent event, partially assessed material information

and others. The report has shown the percentage change in the remuneration of audit in the

year 2018 from 2017. On the overall basis, the report has formed a basis for the evaluation of

the roles and responsibilities of auditors in the assessment of key audit matters.

Executive Summary

The report has been developed with the intention to assess the roles and responsibilities of the

auditors in the process to provide assurance to the financial statements of Origin Energy.

Considering this purpose of the report, all the required part in the annual report of Origin

Energy related to the audit have been analyzed and evaluated. Various segments of auditing

covered by this report are audit independence, non-audit service, auditor’s remuneration, key

audit matters, audit committee, responsibility of the auditors and directors towards financial

reporting, assessment of the material subsequent event, partially assessed material information

and others. The report has shown the percentage change in the remuneration of audit in the

year 2018 from 2017. On the overall basis, the report has formed a basis for the evaluation of

the roles and responsibilities of auditors in the assessment of key audit matters.

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Introduction.....................................................................................................................................3

Auditors’ Independence Requirement............................................................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matter..............................................................................................................................6

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Difference between Responsibilities.............................................................................................10

Material Subsequent Events..........................................................................................................10

Analysis of the Material Information by the Auditors...................................................................10

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................11

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

Table of Contents

Introduction.....................................................................................................................................3

Auditors’ Independence Requirement............................................................................................3

Non-Audit Services..........................................................................................................................4

Auditor’s Remuneration..................................................................................................................5

Key Audit Matter..............................................................................................................................6

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Difference between Responsibilities.............................................................................................10

Material Subsequent Events..........................................................................................................10

Analysis of the Material Information by the Auditors...................................................................10

Material Information Missing........................................................................................................11

Follow-up Questions......................................................................................................................11

Conclusion......................................................................................................................................12

References.....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

Introduction

It is the responsibility of the auditors to involve themselves in the inspection and

examination of the financial statements of their audit client companies and the aim of this

inspection of the financial statements is to ascertainment of material issue in those financial

statements (Sigauke 2013). For this reason, the auditor’s report is considered as a major tool

for the relevant stakeholders in order to get assurance of the fact that the financial statements

of the companies are free from material misstatements. In the presence of these reasons, it is

an utmost necessity for maintain and enhancing the quality of the auditor’s report. In the

recent years, the major accounting bodies like CPA, IAASB, AUASB and others have been

involved in the development of different initiatives that can lead to the enhancement of the

report of the auditors (Meuwissen 2014). Due to the implementation of some of these

initiatives, increase in responsibilities can be seen for both the companies and auditors in the

auditing process as it has become mandatory for them to mention the major material issue in

the financial statements of those companies that have been found while auditing them. More

specifically, key audit matters are needed to be reported in the required section of the annual

report. This report involves in the analysis of the latest annual report of Origin Energy, listed

under Australian Stock Exchange (ASX), with the aim to analyze the relevant audit sections.

Auditors’ Independence Requirement

Auditor’s independence can be regarded as the independence of the internal as well as

external auditor from the parties that can have financial interest in the audit clients; and thus,

the auditors are needed to maintain integrity as well as honesty in the audit profession. One of

Introduction

It is the responsibility of the auditors to involve themselves in the inspection and

examination of the financial statements of their audit client companies and the aim of this

inspection of the financial statements is to ascertainment of material issue in those financial

statements (Sigauke 2013). For this reason, the auditor’s report is considered as a major tool

for the relevant stakeholders in order to get assurance of the fact that the financial statements

of the companies are free from material misstatements. In the presence of these reasons, it is

an utmost necessity for maintain and enhancing the quality of the auditor’s report. In the

recent years, the major accounting bodies like CPA, IAASB, AUASB and others have been

involved in the development of different initiatives that can lead to the enhancement of the

report of the auditors (Meuwissen 2014). Due to the implementation of some of these

initiatives, increase in responsibilities can be seen for both the companies and auditors in the

auditing process as it has become mandatory for them to mention the major material issue in

the financial statements of those companies that have been found while auditing them. More

specifically, key audit matters are needed to be reported in the required section of the annual

report. This report involves in the analysis of the latest annual report of Origin Energy, listed

under Australian Stock Exchange (ASX), with the aim to analyze the relevant audit sections.

Auditors’ Independence Requirement

Auditor’s independence can be regarded as the independence of the internal as well as

external auditor from the parties that can have financial interest in the audit clients; and thus,

the auditors are needed to maintain integrity as well as honesty in the audit profession. One of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

the four big audit firms, KMPG, had the responsibility to conduct the audit of the financial

statements of Origin Energy for the year 2018. According to the Lead Auditor’s Independence

Declaration in the 2018 annual report of Origin Energy, the entire auditor’s independence

related standards and guiding principles of 307C of the Corporations Act 2001 have been

adhered to while providing the professional services in auditing (Originenergy.com.au 2018).

This indicates towards the full compliance with the requirements of auditor’s independence by

KPMG in the audit operation of Origin Energy. At the same time, the audit services did not

include any violation of the professional code of conduct of the audit profession

(Originenergy.com.au 2018).

Non-Audit Services

Non-audit services are considered as those professional services that the qualified

public auditors provide to the audit clients, but these services are not related to audit or the

financial statements of the audit client. According to the Auditor’s Remuneration report in the

latest annual report of Origin Energy, the company has mentioned about six types of non-audit

services received from KPMG. They are accounting advice, taxation services, legal services,

lattice relaxed services, advisory services and others (Originenergy.com.au 2018). The annual

report stated that the company has not received any accounting services in the year 2018, but

there is a mention of this service in the year 2017. At the same time, Origin Energy did not

receive any advisory services in the year 2017 (Originenergy.com.au 2018). It is needed for the

auditors to ensure the fact that there is not any negative impact on the integrity and objectivity

of the audit profession at the time of providing the non-audit services. According to the

the four big audit firms, KMPG, had the responsibility to conduct the audit of the financial

statements of Origin Energy for the year 2018. According to the Lead Auditor’s Independence

Declaration in the 2018 annual report of Origin Energy, the entire auditor’s independence

related standards and guiding principles of 307C of the Corporations Act 2001 have been

adhered to while providing the professional services in auditing (Originenergy.com.au 2018).

This indicates towards the full compliance with the requirements of auditor’s independence by

KPMG in the audit operation of Origin Energy. At the same time, the audit services did not

include any violation of the professional code of conduct of the audit profession

(Originenergy.com.au 2018).

Non-Audit Services

Non-audit services are considered as those professional services that the qualified

public auditors provide to the audit clients, but these services are not related to audit or the

financial statements of the audit client. According to the Auditor’s Remuneration report in the

latest annual report of Origin Energy, the company has mentioned about six types of non-audit

services received from KPMG. They are accounting advice, taxation services, legal services,

lattice relaxed services, advisory services and others (Originenergy.com.au 2018). The annual

report stated that the company has not received any accounting services in the year 2018, but

there is a mention of this service in the year 2017. At the same time, Origin Energy did not

receive any advisory services in the year 2017 (Originenergy.com.au 2018). It is needed for the

auditors to ensure the fact that there is not any negative impact on the integrity and objectivity

of the audit profession at the time of providing the non-audit services. According to the

5AUDIT, ASSURANCE AND COMPLIANCE

declaration of the Audit Committee Chairman, there is not any negative impact on the integrity

and honesty of the profession as Corporations Act 2001 is the standard that has been adhered

to (Originenergy.com.au 2018).

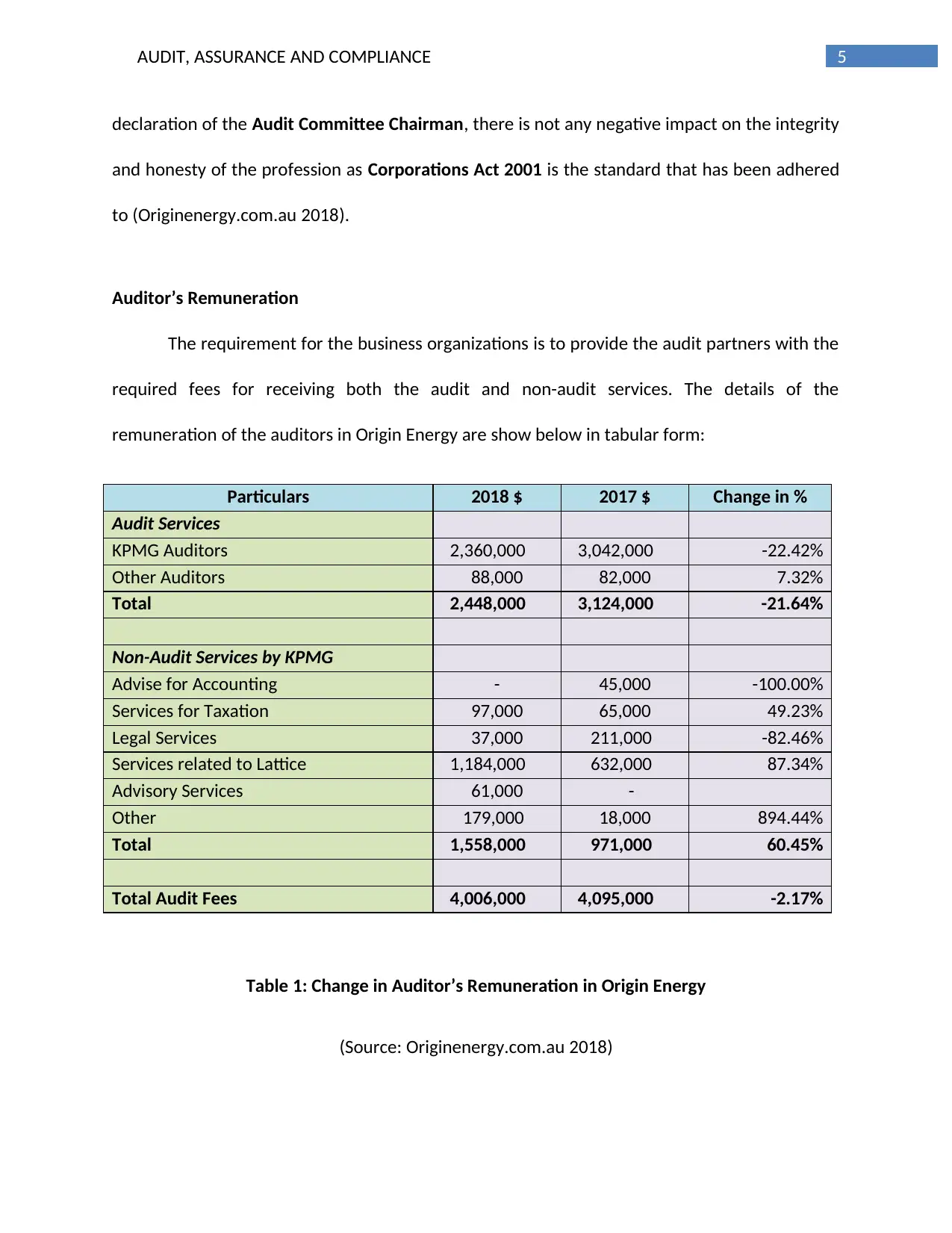

Auditor’s Remuneration

The requirement for the business organizations is to provide the audit partners with the

required fees for receiving both the audit and non-audit services. The details of the

remuneration of the auditors in Origin Energy are show below in tabular form:

Particulars 2018 $ 2017 $ Change in %

Audit Services

KPMG Auditors 2,360,000 3,042,000 -22.42%

Other Auditors 88,000 82,000 7.32%

Total 2,448,000 3,124,000 -21.64%

Non-Audit Services by KPMG

Advise for Accounting - 45,000 -100.00%

Services for Taxation 97,000 65,000 49.23%

Legal Services 37,000 211,000 -82.46%

Services related to Lattice 1,184,000 632,000 87.34%

Advisory Services 61,000 -

Other 179,000 18,000 894.44%

Total 1,558,000 971,000 60.45%

Total Audit Fees 4,006,000 4,095,000 -2.17%

Table 1: Change in Auditor’s Remuneration in Origin Energy

(Source: Originenergy.com.au 2018)

declaration of the Audit Committee Chairman, there is not any negative impact on the integrity

and honesty of the profession as Corporations Act 2001 is the standard that has been adhered

to (Originenergy.com.au 2018).

Auditor’s Remuneration

The requirement for the business organizations is to provide the audit partners with the

required fees for receiving both the audit and non-audit services. The details of the

remuneration of the auditors in Origin Energy are show below in tabular form:

Particulars 2018 $ 2017 $ Change in %

Audit Services

KPMG Auditors 2,360,000 3,042,000 -22.42%

Other Auditors 88,000 82,000 7.32%

Total 2,448,000 3,124,000 -21.64%

Non-Audit Services by KPMG

Advise for Accounting - 45,000 -100.00%

Services for Taxation 97,000 65,000 49.23%

Legal Services 37,000 211,000 -82.46%

Services related to Lattice 1,184,000 632,000 87.34%

Advisory Services 61,000 -

Other 179,000 18,000 894.44%

Total 1,558,000 971,000 60.45%

Total Audit Fees 4,006,000 4,095,000 -2.17%

Table 1: Change in Auditor’s Remuneration in Origin Energy

(Source: Originenergy.com.au 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

The above table discloses the remuneration to KPMG by Origin Energy for the audit and

non-audit services. As per the table, there is reduction in the total payment to KPMG for

providing audit services related to the review of financial statements and this remuneration is

decreased by 21.64 percent. However, as Origin Energy has received six types of non-audit

services, there is increase in the payment to KPMG for the non- audit services. The above table

shows that there is 60.45 percent increase in the payment for non-audit services. Thus, it can

be seen that the payment for audit services decreases while increase in the payment for non-

audit services is evident. Thus, in the presence of all these factors, there is a reduction in the

total audit fees paid to KPMG by Origin Energy for the year 2018 from 2017; and the

remuneration has decreased by 2.17 percent.

Key Audit Matter

Key audit matters are considered as those matters that have major significance in the

auditing of the financial statements and need significant judgment of the auditors. The four key

audit matters of Origin Energy are discussed below:

Carrying Value of the Equity Accounted Investment of Australia Pacific LNG: KPMG has

considered the recoverability of the ALPNG equity investment’s carrying value and the Ironbank

exploration assets as the key audit matter in the presence of certain reasons. The first reason is

the exposure of Origin Energy to the fluctuation in the commodity prices. The second reason is

the presence of inherent complexity in the process to estimate the future cash flows. The last

reason is the presence of adjustments in the historical carrying value (Originenergy.com.au

2018).

The above table discloses the remuneration to KPMG by Origin Energy for the audit and

non-audit services. As per the table, there is reduction in the total payment to KPMG for

providing audit services related to the review of financial statements and this remuneration is

decreased by 21.64 percent. However, as Origin Energy has received six types of non-audit

services, there is increase in the payment to KPMG for the non- audit services. The above table

shows that there is 60.45 percent increase in the payment for non-audit services. Thus, it can

be seen that the payment for audit services decreases while increase in the payment for non-

audit services is evident. Thus, in the presence of all these factors, there is a reduction in the

total audit fees paid to KPMG by Origin Energy for the year 2018 from 2017; and the

remuneration has decreased by 2.17 percent.

Key Audit Matter

Key audit matters are considered as those matters that have major significance in the

auditing of the financial statements and need significant judgment of the auditors. The four key

audit matters of Origin Energy are discussed below:

Carrying Value of the Equity Accounted Investment of Australia Pacific LNG: KPMG has

considered the recoverability of the ALPNG equity investment’s carrying value and the Ironbank

exploration assets as the key audit matter in the presence of certain reasons. The first reason is

the exposure of Origin Energy to the fluctuation in the commodity prices. The second reason is

the presence of inherent complexity in the process to estimate the future cash flows. The last

reason is the presence of adjustments in the historical carrying value (Originenergy.com.au

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

In order to address this issue, KPMG has assessed the accuracy of the forecast of the

previous cash flow. After that, the auditors have compared the forecasted cash flows that

include the model used by Origin Energy for the approval of the estimated and forecasted

future production profile. At the same time, KPMG has conducted the comparison of the used

assumptions by APLNG for the valuation of the assets and the verification of the assumptions.

These are the analytical procedures (Ruhnke and Schmidt 2014).

Accounting for Derivative Financial Assets and Liabilities: Due to the presence of inherent

complexity, the auditors of KPMG have considered this particular aspect as key audit matter.

There are some factors that contribute towards this key audit matters. One factor is the

requirement of the judgment by Origin Energy in order to estimate the fair value of certain

financial instruments with the company’s portfolio. The next factor is Origin Energy’s

application of the process of hedge accounting for specific risk exposures in the portfolio. The

next factors are the use of detailed spreadsheet by the company under the disclosure

requirement of AASB 7: Financial Instrument Disclosure. The last factor is the dependency of

Origin Energy on the operating effectiveness of the third party software system

(Originenergy.com.au 2018).

For addressing this matter, the used audit procedures are the evaluation of the

methodology of internal model for valuation with the help of valuation specialist; the testing of

the internally derived inputs with the help of valuation specialists; testing the valuation of the

hedge accounting results by the valuations specialists; testing the control of management

In order to address this issue, KPMG has assessed the accuracy of the forecast of the

previous cash flow. After that, the auditors have compared the forecasted cash flows that

include the model used by Origin Energy for the approval of the estimated and forecasted

future production profile. At the same time, KPMG has conducted the comparison of the used

assumptions by APLNG for the valuation of the assets and the verification of the assumptions.

These are the analytical procedures (Ruhnke and Schmidt 2014).

Accounting for Derivative Financial Assets and Liabilities: Due to the presence of inherent

complexity, the auditors of KPMG have considered this particular aspect as key audit matter.

There are some factors that contribute towards this key audit matters. One factor is the

requirement of the judgment by Origin Energy in order to estimate the fair value of certain

financial instruments with the company’s portfolio. The next factor is Origin Energy’s

application of the process of hedge accounting for specific risk exposures in the portfolio. The

next factors are the use of detailed spreadsheet by the company under the disclosure

requirement of AASB 7: Financial Instrument Disclosure. The last factor is the dependency of

Origin Energy on the operating effectiveness of the third party software system

(Originenergy.com.au 2018).

For addressing this matter, the used audit procedures are the evaluation of the

methodology of internal model for valuation with the help of valuation specialist; the testing of

the internally derived inputs with the help of valuation specialists; testing the valuation of the

hedge accounting results by the valuations specialists; testing the control of management

8AUDIT, ASSURANCE AND COMPLIANCE

authorization and suggestions and others. These procedures are the examples of test of control

procedures (Gerakos and Syverson 2015).

Unbilled Revenue: KPMG has considered the estimation of the unbilled revenues as the key

audit matter in the presence of uncertainty in the estimation for the determination of the

energy volume. This aspect also includes some key factors. These factors are the presence of

different product offerings and customer rates in different markets; the complex nature of the

process to estimate the demand of the customers and the loss of physical energy between the

purchase and delivery of energy (Originenergy.com.au 2018).

The substantive audit procedures to address these issue are the assessment of the

historical accuracy of the process to estimate subsequent billings; testing the wholesale energy

volume purchased by Origin Energy to the AEMO sample; reconciliation of the purchase

volumes to the recognition of revenue volumes and challenging the estimation of the current

period by the comparison of the unbilled revenues and others. These can be considered as test

of details and analytical procedures (Kilgore, Harrison and Radich 2014).

Unbilled Network Expenses: The auditors of KPMG have considered this as a key audit matter

in the presence of the uncertainty to estimate the volume of energy purchased for catering to

the demand of the customers of the company. The presence of two key factors can be seen in

this issue. They are the customer demand and physical energy loss levels that are related to the

issue of unbilled revenue and the amount of the volume of energy supplied to the customer

between the dates of last invoice (Originenergy.com.au 2018).

authorization and suggestions and others. These procedures are the examples of test of control

procedures (Gerakos and Syverson 2015).

Unbilled Revenue: KPMG has considered the estimation of the unbilled revenues as the key

audit matter in the presence of uncertainty in the estimation for the determination of the

energy volume. This aspect also includes some key factors. These factors are the presence of

different product offerings and customer rates in different markets; the complex nature of the

process to estimate the demand of the customers and the loss of physical energy between the

purchase and delivery of energy (Originenergy.com.au 2018).

The substantive audit procedures to address these issue are the assessment of the

historical accuracy of the process to estimate subsequent billings; testing the wholesale energy

volume purchased by Origin Energy to the AEMO sample; reconciliation of the purchase

volumes to the recognition of revenue volumes and challenging the estimation of the current

period by the comparison of the unbilled revenues and others. These can be considered as test

of details and analytical procedures (Kilgore, Harrison and Radich 2014).

Unbilled Network Expenses: The auditors of KPMG have considered this as a key audit matter

in the presence of the uncertainty to estimate the volume of energy purchased for catering to

the demand of the customers of the company. The presence of two key factors can be seen in

this issue. They are the customer demand and physical energy loss levels that are related to the

issue of unbilled revenue and the amount of the volume of energy supplied to the customer

between the dates of last invoice (Originenergy.com.au 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

For addressing this issue, the substantive audit procedures performed are the

assessment of the historical accuracy by Origin Energy against the payments for the

distributors; testing the wholesale purchase energy volume against the AEMO invoice; the

reconciliation of the volume of purchase with the recognized revenue and challenging the

current period estimation used by the comparison of unbilled network expenses and checking

for the consistency of the correlation of the estimated volumes. These can be classified as

substantive audit tests (Arruñada 2013).

Audit Committee

The Board of Directors of Origin Energy has an Audit Committee and this audit

committee comprises of four non-executive directors of the company. They are Maxine Benner,

Gordon Cairns, Teresa Engelhard and Scott Perkins (Originenergy.com.au 2018). This audit

committee looks into the matters related to the structures and systems of management

designed for the protection of corporate reporting integrity. The responsibility of the audit

committee is to review the half-yearly and full year financial reports of Origin Energy with the

aim to provide recommendation of the financial statements. Moreover, there is not any audit

committee charter in the board of the company (Brennan and Kirwan 2015).

Audit Opinion

Some specific facts can be noticed from the opinion of the auditors of Origin Energy.

First, all the financial statements and reports of Origin Energy are in accordance with the

Corporations Act 2001 that assist the company in providing the true and fair view of the

For addressing this issue, the substantive audit procedures performed are the

assessment of the historical accuracy by Origin Energy against the payments for the

distributors; testing the wholesale purchase energy volume against the AEMO invoice; the

reconciliation of the volume of purchase with the recognized revenue and challenging the

current period estimation used by the comparison of unbilled network expenses and checking

for the consistency of the correlation of the estimated volumes. These can be classified as

substantive audit tests (Arruñada 2013).

Audit Committee

The Board of Directors of Origin Energy has an Audit Committee and this audit

committee comprises of four non-executive directors of the company. They are Maxine Benner,

Gordon Cairns, Teresa Engelhard and Scott Perkins (Originenergy.com.au 2018). This audit

committee looks into the matters related to the structures and systems of management

designed for the protection of corporate reporting integrity. The responsibility of the audit

committee is to review the half-yearly and full year financial reports of Origin Energy with the

aim to provide recommendation of the financial statements. Moreover, there is not any audit

committee charter in the board of the company (Brennan and Kirwan 2015).

Audit Opinion

Some specific facts can be noticed from the opinion of the auditors of Origin Energy.

First, all the financial statements and reports of Origin Energy are in accordance with the

Corporations Act 2001 that assist the company in providing the true and fair view of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

financial position of them as at 30 June 2018. Second, the financial statements are in

accordance with the Australian Accounting Standard and Corporate Regulations 2001. Third,

the main components of the financial reports of Origin Energy consists of consolidated

statement of financial position, income statement, comprehensive statement of comprehensive

income, consolidated statement of change in equity and consolidated statement of cash flows

(Originenergy.com.au 2018).

Difference between Responsibilities

The responsibilities of the directors are management are to follow Australian

Accounting Standard and Corporations Act 2001 for the preparation of financial statements, to

implement the necessary internal control and to assess the ability of Origin Energy to continue

as going concern (Skaife, Veenman and Wangerin 2013). The responsibilities of the auditors are

to obtain reasonable assurance on the material misstatement factor in the financial statements

and to promise the report of the auditors including the audit opinion (In'airat 2015).

Material Subsequent Events

As per the latest annual report of Origin Energy for the year 2018, the auditors have

declared that there is not any event of material nature in the financial statements since 30 June

2018 (Originenergy.com.au 2018).

Analysis of the Material Information by the Auditors

It is very easy for a third part stakeholder to gain understanding about the material

information reported by KPMG in the latest annual report of Origin Energy. The auditors have

financial position of them as at 30 June 2018. Second, the financial statements are in

accordance with the Australian Accounting Standard and Corporate Regulations 2001. Third,

the main components of the financial reports of Origin Energy consists of consolidated

statement of financial position, income statement, comprehensive statement of comprehensive

income, consolidated statement of change in equity and consolidated statement of cash flows

(Originenergy.com.au 2018).

Difference between Responsibilities

The responsibilities of the directors are management are to follow Australian

Accounting Standard and Corporations Act 2001 for the preparation of financial statements, to

implement the necessary internal control and to assess the ability of Origin Energy to continue

as going concern (Skaife, Veenman and Wangerin 2013). The responsibilities of the auditors are

to obtain reasonable assurance on the material misstatement factor in the financial statements

and to promise the report of the auditors including the audit opinion (In'airat 2015).

Material Subsequent Events

As per the latest annual report of Origin Energy for the year 2018, the auditors have

declared that there is not any event of material nature in the financial statements since 30 June

2018 (Originenergy.com.au 2018).

Analysis of the Material Information by the Auditors

It is very easy for a third part stakeholder to gain understanding about the material

information reported by KPMG in the latest annual report of Origin Energy. The auditors have

11AUDIT, ASSURANCE AND COMPLIANCE

reported the key audit maters in the tabular form that also includes the applied substantive

audit procedures for addressing the key audit matters. The auditors have used simple English

language for providing the information related to the key audit matters. The third party

stakeholders can also asses all the relevant audit sections for determining the role and

responsibilities of the auditors (Power and Gendron 2015).

Material Information Missing

It is evident from the analysis of all the audit related section of the annual report of

Origin Energy that KPMG has clearly reported about four key audit matters from the financial

statements of the company. Moreover, the auditors have also mentioned the fact that there is

not any material subsequent event in the company. Lastly, KPMG has adhered to all the

required standards and guiding principles of audit profession. It can be said based on the above

that KPMG has not missed any material information of the company (Meuwissen 2014).

Follow-up Questions

In the follow up questions, one can ask the auditor about the outcome of the discussion

with the internal auditor of Origin Energy. Next, one can ask about the process for the

determination of the materiality level in the audit of Origin Energy. After that, one can ask the

auditors about any back-up plan as well as future plan of the audit process in Origin Energy. All

these questions can easily be asked in the Annual General Meeting (Gaynor et al. 2016).

reported the key audit maters in the tabular form that also includes the applied substantive

audit procedures for addressing the key audit matters. The auditors have used simple English

language for providing the information related to the key audit matters. The third party

stakeholders can also asses all the relevant audit sections for determining the role and

responsibilities of the auditors (Power and Gendron 2015).

Material Information Missing

It is evident from the analysis of all the audit related section of the annual report of

Origin Energy that KPMG has clearly reported about four key audit matters from the financial

statements of the company. Moreover, the auditors have also mentioned the fact that there is

not any material subsequent event in the company. Lastly, KPMG has adhered to all the

required standards and guiding principles of audit profession. It can be said based on the above

that KPMG has not missed any material information of the company (Meuwissen 2014).

Follow-up Questions

In the follow up questions, one can ask the auditor about the outcome of the discussion

with the internal auditor of Origin Energy. Next, one can ask about the process for the

determination of the materiality level in the audit of Origin Energy. After that, one can ask the

auditors about any back-up plan as well as future plan of the audit process in Origin Energy. All

these questions can easily be asked in the Annual General Meeting (Gaynor et al. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.