HI6026 Audit Assurance: Enhanced Auditor Reporting - AGL Limited

VerifiedAdded on 2023/06/04

|13

|3580

|203

Report

AI Summary

This report provides a detailed analysis of how enhanced auditor reporting is being embraced in Australia, focusing on AGL Limited as a case study. It examines the auditor's compliance with independence requirements, the provision of non-audit services, and an analysis of the auditor's remuneration. The report identifies key audit matters, such as unbilled revenue and distribution costs, and the audit procedures performed to address them. It also discusses the composition and responsibilities of the audit committee, the type of audit opinion expressed, and a comparison of directors' and management's responsibilities with those of the auditor. The report concludes by noting the absence of material subsequent events and provides an overview of the audit process and findings related to AGL Limited's financial reporting.

Topic: How is Enhanced Auditor Reporting being embraced in

Australia?

Australia?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The following words is completely related to the observation of auditing practice presented by an

organisation selected to be the AGL Limited. There has been quite expensive evaluation of work

done in the following work related to every specific information that an organisation must

consider to expand their success rate in future period of time. The following work has analysed

the ways by which auditing information as well as documents that are required by any company

is clearly provided by a g l Limited or not. Specific consideration of work regarding the

remuneration sheet as well as the amount spent against the top tier management group of the

organisation is provided evident source.

The following words is completely related to the observation of auditing practice presented by an

organisation selected to be the AGL Limited. There has been quite expensive evaluation of work

done in the following work related to every specific information that an organisation must

consider to expand their success rate in future period of time. The following work has analysed

the ways by which auditing information as well as documents that are required by any company

is clearly provided by a g l Limited or not. Specific consideration of work regarding the

remuneration sheet as well as the amount spent against the top tier management group of the

organisation is provided evident source.

Table of Contents

Introduction 2

Analysis 2

Providing an analysis of the Auditor’s remuneration and explanations of the remuneration. 3

What type of Audit Opinion was expressed? 6

Conclusion 9

Introduction 2

Analysis 2

Providing an analysis of the Auditor’s remuneration and explanations of the remuneration. 3

What type of Audit Opinion was expressed? 6

Conclusion 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The study shall mainly take the consideration of carrying out a detailed analysis of the annual

reports of a company. For the convenience of the study, The AGL Limited Group has been

chosen. It is an Australia based organization which is related to the energy and power services

Industry. It procures and supplies power, electricity and Gas and supplies them for residential

and another different kind of commercial use. Documents such as the Auditor’s Independence

Declaration, Non-Audit services performed by the Auditor, Auditors’ remuneration and the

Independent auditor’s report has been studied and different kind of information has been

gathered from them. The auditor’s compliance with the Independence needs have been checked,

then the provision of various non-audit services have been taken into account. Things such as

detailed study about auditor's remuneration, Key audit matters, details about the Audit

Committee, various kinds of audit opinions, Director’s responsibilities with that of Auditor’s

responsibilities, details about materials events and testing of material information. The study has

shall take an end with the different questions that could have been asked to the auditors and then

at the last, with an ending note of Concluding remarks.

Analysis

Auditor’s compliance with Independence requirements

It can be said that the Auditor has complied with all of the Independence requirements. It has

been clearly mentioned in the Auditor's Independence declaration that the auditing has been

conducted and the reporting has been done in compliance to the section 307C of the

Corporations Act 2001 (www.cpa australia.com, 2018).

The study shall mainly take the consideration of carrying out a detailed analysis of the annual

reports of a company. For the convenience of the study, The AGL Limited Group has been

chosen. It is an Australia based organization which is related to the energy and power services

Industry. It procures and supplies power, electricity and Gas and supplies them for residential

and another different kind of commercial use. Documents such as the Auditor’s Independence

Declaration, Non-Audit services performed by the Auditor, Auditors’ remuneration and the

Independent auditor’s report has been studied and different kind of information has been

gathered from them. The auditor’s compliance with the Independence needs have been checked,

then the provision of various non-audit services have been taken into account. Things such as

detailed study about auditor's remuneration, Key audit matters, details about the Audit

Committee, various kinds of audit opinions, Director’s responsibilities with that of Auditor’s

responsibilities, details about materials events and testing of material information. The study has

shall take an end with the different questions that could have been asked to the auditors and then

at the last, with an ending note of Concluding remarks.

Analysis

Auditor’s compliance with Independence requirements

It can be said that the Auditor has complied with all of the Independence requirements. It has

been clearly mentioned in the Auditor's Independence declaration that the auditing has been

conducted and the reporting has been done in compliance to the section 307C of the

Corporations Act 2001 (www.cpa australia.com, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 1: Auditor compliance with independence requirements

(Source: Auasb.gov.au. 2018)

The auditor in the declaration ha clearly stated that all the compliances have been made with

Corporations Act and the applicable codes and professional conduct in relation to the audit has

also been attained. Thus it can be clearly said that the Audit has been done as per the Australian

Accounting standards and further, it has been stated that they were independent and away from

the influences of the AGL Group. They had functioned as per the auditor’s independence

requirements of the Corporations Act, 2001 and also as per the needs of the Accounting

Professionals and Ethical Standards Board’s APES 110 Code of Ethics for Professional

Accountants (www.auasb.gov.au, 2018). Thus it can be concluded that all the things were done

in compliance with accounting standards as well as other legal things prevailing in the land of

Australia.

With no provision for non-audit services, providing the description of the overall nature of

such services

The board follows a kind of formal approach in the provision of non-audit services to the

company. It can be said that the external auditor cannot provide such nature of services which

can threaten the independence and defy the overall assurance and compliance role. Semi-annual

reports on the cases related to auditing and related services are provided to the Board with the

overall help and aid of the Audit and Risk Management Committee (Beck, Dumay and Frost,

2017.). No non-audit services have been provided by the external auditor the whole of the

(Source: Auasb.gov.au. 2018)

The auditor in the declaration ha clearly stated that all the compliances have been made with

Corporations Act and the applicable codes and professional conduct in relation to the audit has

also been attained. Thus it can be clearly said that the Audit has been done as per the Australian

Accounting standards and further, it has been stated that they were independent and away from

the influences of the AGL Group. They had functioned as per the auditor’s independence

requirements of the Corporations Act, 2001 and also as per the needs of the Accounting

Professionals and Ethical Standards Board’s APES 110 Code of Ethics for Professional

Accountants (www.auasb.gov.au, 2018). Thus it can be concluded that all the things were done

in compliance with accounting standards as well as other legal things prevailing in the land of

Australia.

With no provision for non-audit services, providing the description of the overall nature of

such services

The board follows a kind of formal approach in the provision of non-audit services to the

company. It can be said that the external auditor cannot provide such nature of services which

can threaten the independence and defy the overall assurance and compliance role. Semi-annual

reports on the cases related to auditing and related services are provided to the Board with the

overall help and aid of the Audit and Risk Management Committee (Beck, Dumay and Frost,

2017.). No non-audit services have been provided by the external auditor the whole of the

financial year. A rotation policy has also been agreed upon for the senior Auditor Of the

Auditing agency, that is Deloitte. The non-audit services that were provided to the company were

mainly of a free nature. It is done and comes with the overall remuneration of auditing that is

paid to the committee by the Directors and the whole of the company.

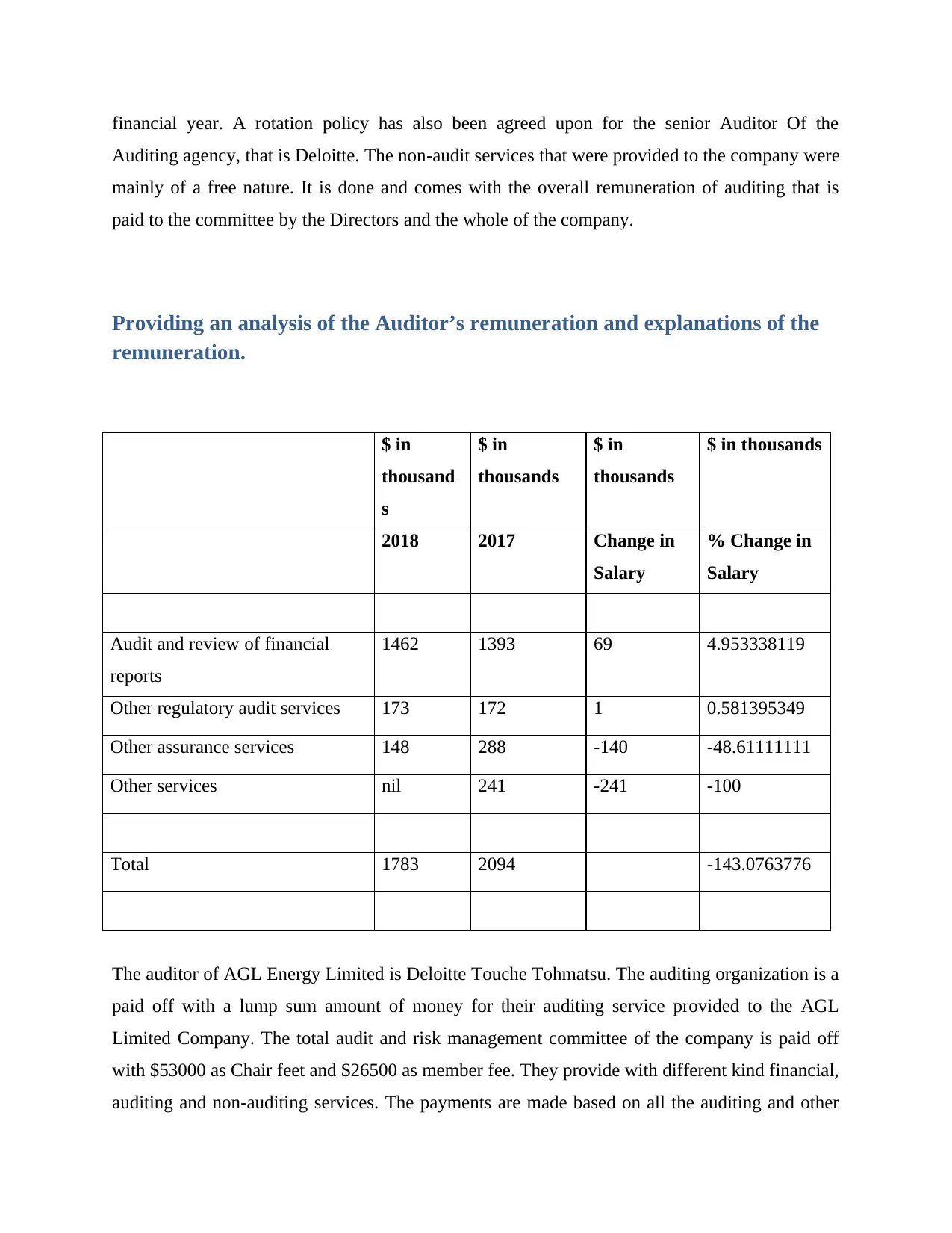

Providing an analysis of the Auditor’s remuneration and explanations of the

remuneration.

$ in

thousand

s

$ in

thousands

$ in

thousands

$ in thousands

2018 2017 Change in

Salary

% Change in

Salary

Audit and review of financial

reports

1462 1393 69 4.953338119

Other regulatory audit services 173 172 1 0.581395349

Other assurance services 148 288 -140 -48.61111111

Other services nil 241 -241 -100

Total 1783 2094 -143.0763776

The auditor of AGL Energy Limited is Deloitte Touche Tohmatsu. The auditing organization is a

paid off with a lump sum amount of money for their auditing service provided to the AGL

Limited Company. The total audit and risk management committee of the company is paid off

with $53000 as Chair feet and $26500 as member fee. They provide with different kind financial,

auditing and non-auditing services. The payments are made based on all the auditing and other

Auditing agency, that is Deloitte. The non-audit services that were provided to the company were

mainly of a free nature. It is done and comes with the overall remuneration of auditing that is

paid to the committee by the Directors and the whole of the company.

Providing an analysis of the Auditor’s remuneration and explanations of the

remuneration.

$ in

thousand

s

$ in

thousands

$ in

thousands

$ in thousands

2018 2017 Change in

Salary

% Change in

Salary

Audit and review of financial

reports

1462 1393 69 4.953338119

Other regulatory audit services 173 172 1 0.581395349

Other assurance services 148 288 -140 -48.61111111

Other services nil 241 -241 -100

Total 1783 2094 -143.0763776

The auditor of AGL Energy Limited is Deloitte Touche Tohmatsu. The auditing organization is a

paid off with a lump sum amount of money for their auditing service provided to the AGL

Limited Company. The total audit and risk management committee of the company is paid off

with $53000 as Chair feet and $26500 as member fee. They provide with different kind financial,

auditing and non-auditing services. The payments are made based on all the auditing and other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

related services given by them to the company. The remuneration for external audit and review

of financial reports have increased in the year 2018 as compared to that of the previous year. The

amount for other audit regulatory services has also increased. However, the number of other

assurance services and other services have drastically fallen (directory.libsyn.com, 2018). This

may due to the change in the rates set for auditing by Deloitte. The company has paid off based

on the new rates set by Deloitte. The overall remuneration, however, has fallen by more than

143%. This may be also related to fall in the economic condition of AGL LImited.

In relation to the key audit matters, the audit procedures that were performed to provide

assurance over each matter (Summarise and paraphrase each key audit matter. Correctly

classify each audit procedure listed as tests of controls, substantive tests of detail, a substantive

test of balances or analytical procedures.)

The key audit matters reported by the auditor in the report are as follows:

1. Unbilled revenue: There is has been uncertainty over the unbilled electricity consumption

of customer in the year 2017 that amounts to 938 million due to variance in meter

readings dates (Reid and Wettenhall, 2015).

2. Unbilled distribution cost: the auditor has also identified the matter related to unbilled

distribution cost for network supply result due to improper estimations.

On this contrary, the auditors provided a substantive procedure for mitigation of these matters

and investigate clearly on the matter to solve the following. The methods followed by the

firmware as follows:

1. Billings of meter readings and historical data relating to it was checked for confirmation

of the unbilled revenue (Sarens, 2015).

2. The physical setting of matter amounts was done in order ensures no misstatement was

involved.

3. Cost per units as determined in accordance with companies and well as industrial rates to

mitigate such situations.

Presence of an Audit committee, non-executive directors on the audit committee, the Audit

Committee Charter.

of financial reports have increased in the year 2018 as compared to that of the previous year. The

amount for other audit regulatory services has also increased. However, the number of other

assurance services and other services have drastically fallen (directory.libsyn.com, 2018). This

may due to the change in the rates set for auditing by Deloitte. The company has paid off based

on the new rates set by Deloitte. The overall remuneration, however, has fallen by more than

143%. This may be also related to fall in the economic condition of AGL LImited.

In relation to the key audit matters, the audit procedures that were performed to provide

assurance over each matter (Summarise and paraphrase each key audit matter. Correctly

classify each audit procedure listed as tests of controls, substantive tests of detail, a substantive

test of balances or analytical procedures.)

The key audit matters reported by the auditor in the report are as follows:

1. Unbilled revenue: There is has been uncertainty over the unbilled electricity consumption

of customer in the year 2017 that amounts to 938 million due to variance in meter

readings dates (Reid and Wettenhall, 2015).

2. Unbilled distribution cost: the auditor has also identified the matter related to unbilled

distribution cost for network supply result due to improper estimations.

On this contrary, the auditors provided a substantive procedure for mitigation of these matters

and investigate clearly on the matter to solve the following. The methods followed by the

firmware as follows:

1. Billings of meter readings and historical data relating to it was checked for confirmation

of the unbilled revenue (Sarens, 2015).

2. The physical setting of matter amounts was done in order ensures no misstatement was

involved.

3. Cost per units as determined in accordance with companies and well as industrial rates to

mitigate such situations.

Presence of an Audit committee, non-executive directors on the audit committee, the Audit

Committee Charter.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Composition of the different committees and boards of the organization

(Source: Annual Reports AGL Limited, 2018)

The audit committee of the company, comprises of a number of specified knowledgeable

members. The main structure of the Audit committee can be mainly divided into parts, The

external auditors and the internal auditors. Mr John Stanhope acts as the chairman as well as the

executive director (the main person) of the whole of the Auditing Committee. He takes all the

decision after being guided by the main Chairperson of the Group/Organization.

The Audit Committee is mainly responsible for undertaking the auditing of the whole company

and its accounts. The committee is also liable for strategic risk profile scrutiny and warning the

company ahead of any issues or problems. The office of the audit committee is managed by the

chairman that is Mr Stanhope. Under him, there are various of the important officials (Non-

Executive directors) such as Jacqueline Hey, Les Hosking and Belinda Hutchinson. All these

people in a joint and collaborative manner manage and run the Auditing Committee. Under them,

several of the auditors work for the company (Hoffmann et al. 2014). They also help and guide

the external auditors in any kind of need or if any such kind of situation arises. The committee

works in unison and scrutinized s the whole accounting of the company and vouchers and

verifies them. Different kind of important steps are also taken by the committee I need to

different kind of situation and emergencies arising out in the company.

What type of Audit Opinion was expressed?

A kind of positive opinion was expressed in the whole scene of auditing. The whole of the

auditors has expressed their feeling that the auditing was righteously done and all the standards

(Source: Annual Reports AGL Limited, 2018)

The audit committee of the company, comprises of a number of specified knowledgeable

members. The main structure of the Audit committee can be mainly divided into parts, The

external auditors and the internal auditors. Mr John Stanhope acts as the chairman as well as the

executive director (the main person) of the whole of the Auditing Committee. He takes all the

decision after being guided by the main Chairperson of the Group/Organization.

The Audit Committee is mainly responsible for undertaking the auditing of the whole company

and its accounts. The committee is also liable for strategic risk profile scrutiny and warning the

company ahead of any issues or problems. The office of the audit committee is managed by the

chairman that is Mr Stanhope. Under him, there are various of the important officials (Non-

Executive directors) such as Jacqueline Hey, Les Hosking and Belinda Hutchinson. All these

people in a joint and collaborative manner manage and run the Auditing Committee. Under them,

several of the auditors work for the company (Hoffmann et al. 2014). They also help and guide

the external auditors in any kind of need or if any such kind of situation arises. The committee

works in unison and scrutinized s the whole accounting of the company and vouchers and

verifies them. Different kind of important steps are also taken by the committee I need to

different kind of situation and emergencies arising out in the company.

What type of Audit Opinion was expressed?

A kind of positive opinion was expressed in the whole scene of auditing. The whole of the

auditors has expressed their feeling that the auditing was righteously done and all the standards

and the policies have been followed up. The whole of the auditing has been done in compliance

with the Australian Accounting Standards and terms of the Companies Act 2004 (Ball et al.

2015). It was also expressed by the auditors that they had made the reports and conducted the

auditing on an independent basis. However, some of the items such as Unbilled revenue of $938

million, Unbilled distribution costs of $412 million. There were also other things which declared

in the reports prepared by the auditors related to the different things that were not declared by all

of the auditors on a per-hand basis.

The comparison of Directors’ and Management’s responsibilities with that of the Auditor’s

responsibilities in accord to the financial report

The Directors and Management's responsibilities are to see through that the company is properly

run and all the operations are properly taken care off (Mayne, 2017). They have the sole

responsibility of running the company and taking care of each of its affairs starting from

accounting, auditing (internal), to arranging for remunerations of the various staffs as well as

auditing committees, taking decisions for the company and making any kind of declarations and

provisions for the company (McKee, 2015). They mainly held a meeting where major decisions

regarding the company are taken forth by them. On the other hand, Auditors, mainly the external

auditors get remunerations from the company. They have the sole responsibility to review and

check for the accounts bookkeeping done by the company and find faults in it and report it

(Adams, 2017). They have the full responsibility to conduct the audit and report any kind of

omissions or material misstatements done by the specific organization. The internal auditors

have the responsibility to access the materials and warn the company about any material

misstatements, errors or manipulation that has been done by the accountants before it gets

scrutinized by the External Auditors (Chiu and Vasarhelyi, 2018). They also hold positions in the

company and attends a different kind of board meetings and take up an active part in the

Executive and non-executive duties in the company.

Presence of any material subsequent events

In the above sections, it has been seen that the auditor in the auditor report has reviewed a fair

decision over the financial reports created by the firm in the current years. It can be said that as a

Fair view over the financial review has been given by the auditor it cannot be said that there was

any, materiality or misstatement involved in the financials of AGI limited. Although for purpose

with the Australian Accounting Standards and terms of the Companies Act 2004 (Ball et al.

2015). It was also expressed by the auditors that they had made the reports and conducted the

auditing on an independent basis. However, some of the items such as Unbilled revenue of $938

million, Unbilled distribution costs of $412 million. There were also other things which declared

in the reports prepared by the auditors related to the different things that were not declared by all

of the auditors on a per-hand basis.

The comparison of Directors’ and Management’s responsibilities with that of the Auditor’s

responsibilities in accord to the financial report

The Directors and Management's responsibilities are to see through that the company is properly

run and all the operations are properly taken care off (Mayne, 2017). They have the sole

responsibility of running the company and taking care of each of its affairs starting from

accounting, auditing (internal), to arranging for remunerations of the various staffs as well as

auditing committees, taking decisions for the company and making any kind of declarations and

provisions for the company (McKee, 2015). They mainly held a meeting where major decisions

regarding the company are taken forth by them. On the other hand, Auditors, mainly the external

auditors get remunerations from the company. They have the sole responsibility to review and

check for the accounts bookkeeping done by the company and find faults in it and report it

(Adams, 2017). They have the full responsibility to conduct the audit and report any kind of

omissions or material misstatements done by the specific organization. The internal auditors

have the responsibility to access the materials and warn the company about any material

misstatements, errors or manipulation that has been done by the accountants before it gets

scrutinized by the External Auditors (Chiu and Vasarhelyi, 2018). They also hold positions in the

company and attends a different kind of board meetings and take up an active part in the

Executive and non-executive duties in the company.

Presence of any material subsequent events

In the above sections, it has been seen that the auditor in the auditor report has reviewed a fair

decision over the financial reports created by the firm in the current years. It can be said that as a

Fair view over the financial review has been given by the auditor it cannot be said that there was

any, materiality or misstatement involved in the financials of AGI limited. Although for purpose

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of making communication of matter in which the auditor suspected that can are mortality was

reported under the audit matter report (Podger, 2018). This showed that there are some key audit

matters investigated by the auditor to be suspected to have materiality but in such cases, the

following were solved by the organization. It can be said that thus there was only some matter

concerning the auditor remaining to which there were no such major accounts in which

materiality was suspected hence it can be said that there not event leading to materiality involved

within the financial reports of the firm (Hoffmann et al. 2014).

As an interested third party stakeholder, making an assessment of the effectiveness of the

material information reported by the Auditor in the conclusion.

The material information provided by the organization can be said to be much effective and

detailed. It has been able to describe all the situations and the things that have been done in the

overall accounts of the organization. The changes in accounting policies and practices in some

places have also been clear and in detail reported in the declaration put forth by the business

organization (Vanclay, 2015). It can be noted that many of the things have been clearly

mentioned and specified by the board of the auditors. However, things related to the roles of the

auditors and details related to the provisions have not been made in detail. It has to be kept in

mind that most of the times, the different of the business organization makes some changes or

manipulations in their amount and heads of the different provisions. Thus, it can be said that the

auditing committee should have cross checked and analysed the details related to the different

kind of provisions that have been made and considered in the annual reports of the company.

Considering whether there was any material information which could be missing, under-

reported and/or not fully explained or disclosed in an effective way for the intended users

It can be said that there was very negligible kind of material misstatements to be found in the

whole of the work. It can be said that fewer instances of material information being missing as

such and under-reported can be seen. However, there were some wrong reporting related to the

unbilled revenue, unbilled distribution costs and there was also information misleading and

missing related to the financial instruments held onto and possessed by the business organization.

All these things were clear and in detail reported by the auditor of the organization (Griffiths,

2016). The material information related to the overall role of the difference of the members of

reported under the audit matter report (Podger, 2018). This showed that there are some key audit

matters investigated by the auditor to be suspected to have materiality but in such cases, the

following were solved by the organization. It can be said that thus there was only some matter

concerning the auditor remaining to which there were no such major accounts in which

materiality was suspected hence it can be said that there not event leading to materiality involved

within the financial reports of the firm (Hoffmann et al. 2014).

As an interested third party stakeholder, making an assessment of the effectiveness of the

material information reported by the Auditor in the conclusion.

The material information provided by the organization can be said to be much effective and

detailed. It has been able to describe all the situations and the things that have been done in the

overall accounts of the organization. The changes in accounting policies and practices in some

places have also been clear and in detail reported in the declaration put forth by the business

organization (Vanclay, 2015). It can be noted that many of the things have been clearly

mentioned and specified by the board of the auditors. However, things related to the roles of the

auditors and details related to the provisions have not been made in detail. It has to be kept in

mind that most of the times, the different of the business organization makes some changes or

manipulations in their amount and heads of the different provisions. Thus, it can be said that the

auditing committee should have cross checked and analysed the details related to the different

kind of provisions that have been made and considered in the annual reports of the company.

Considering whether there was any material information which could be missing, under-

reported and/or not fully explained or disclosed in an effective way for the intended users

It can be said that there was very negligible kind of material misstatements to be found in the

whole of the work. It can be said that fewer instances of material information being missing as

such and under-reported can be seen. However, there were some wrong reporting related to the

unbilled revenue, unbilled distribution costs and there was also information misleading and

missing related to the financial instruments held onto and possessed by the business organization.

All these things were clear and in detail reported by the auditor of the organization (Griffiths,

2016). The material information related to the overall role of the difference of the members of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the auditing committee could have been provided in a much detailed manner. It can be said that

the members and their designations have been pointed out in the annual reports, but, their

individual roles and responsibilities have not been clearly defined as per the need. These things

could have easily been done.

Different follow-up questions that could be asked to the Auditor at the company’s Annual

General Meeting

Questions relating to the overall efficiency of the auditors could be asked. The individual role

played each of the authors at the auditing committee could have easily been interrogated. It can

be seen that the auditors have done the auditing but specifically, they have not mentioned how

and in which manner they have conducted the same. Questions related to the cross-checking of

the accounts could have been made (Lenz and Hahn, 2015). Further what kind of more

provisions have to be made and mentioned in the annual reports of the organization also needed

to be asked by the auditors. Questions related to the declaration of the authenticity of each of the

books made and maintained by the company could also have been made from them. How the

bills of the revenue from the gas could be settled should have been asked of them. Further, the

unbilled and not written down distribution costs and their overfall aftermaths could also have

been asked by the boards of the auditors of the company (Chiang, 2016). By asking all these

questions, the actual state of affairs of the company could have been perceived.

Conclusion

The details related to the annual report has been considered and related to different parts of the

study. It can be concluded that some material information has been missed out in the annual

report and its different sections made by the company. It has to be ensured that such kind of

missing information should be provided in order to give proper information to the different

stakeholders of the company.

the members and their designations have been pointed out in the annual reports, but, their

individual roles and responsibilities have not been clearly defined as per the need. These things

could have easily been done.

Different follow-up questions that could be asked to the Auditor at the company’s Annual

General Meeting

Questions relating to the overall efficiency of the auditors could be asked. The individual role

played each of the authors at the auditing committee could have easily been interrogated. It can

be seen that the auditors have done the auditing but specifically, they have not mentioned how

and in which manner they have conducted the same. Questions related to the cross-checking of

the accounts could have been made (Lenz and Hahn, 2015). Further what kind of more

provisions have to be made and mentioned in the annual reports of the organization also needed

to be asked by the auditors. Questions related to the declaration of the authenticity of each of the

books made and maintained by the company could also have been made from them. How the

bills of the revenue from the gas could be settled should have been asked of them. Further, the

unbilled and not written down distribution costs and their overfall aftermaths could also have

been asked by the boards of the auditors of the company (Chiang, 2016). By asking all these

questions, the actual state of affairs of the company could have been perceived.

Conclusion

The details related to the annual report has been considered and related to different parts of the

study. It can be concluded that some material information has been missed out in the annual

report and its different sections made by the company. It has to be ensured that such kind of

missing information should be provided in order to give proper information to the different

stakeholders of the company.

References

Beck, C., Dumay, J. and Frost, G., 2017. In pursuit of a ‘single source of truth’: from threatened

legitimacy to integrated reporting. Journal of Business Ethics, 141(1), pp.191-205.

Ball, F., Tyler, J. and Wells, P., 2015. Is audit quality impacted by auditor relationships?.

Journal of Contemporary Accounting & Economics, 11(2), pp.166-181.

McKee, D., 2015. New external audit report standards are game-changing. Governance

Directions, 67(4), p.222.

Chiu, V. and Vasarhelyi, M.A., 2018. The Development and Intellectual Structure of Continuous

Auditing Research 1. In Continuous Auditing: Theory and Application (pp. 53-85). Emerald

Publishing Limited.

Vanclay, F., 2015. The potential application of qualitative evaluation methods in European

regional development: Reflections on the use of performance story reporting in Australian

natural resource management. Regional Studies, 49(8), pp.1326-1339.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

Chiang, C., 2016. Conceptualising the linkage between professional scepticism and auditor

independence. Pacific Accounting Review, 28(2), pp.180-200.

Mayne, J., 2017. Evaluation for accountability: myth or reality?. In Making Accountability Work

(pp. 81-102). Routledge.

Adams, C.A., 2017. Conceptualising the contemporary corporate value creation process.

Accounting, Auditing & Accountability Journal, 30(4), pp.906-931.

Hoffmann, T., English, T. and Glasziou, P., 2014. Reporting of interventions in randomised

trials: an audit of journal instructions to authors. Trials, 15(1), p.20.

Annual Reports AGL Limited (2018). Annual Reports, 2018. [online] Available at:

https://www.2018annualreport.agl.com.au/xmlpages/resources/TXP/agl_energy/finrep/pdf/

AGL_Energy_Annual_Report_2018.pdf [Accessed 19 Sep. 2018].

Auasb.gov.au. (2018). Auditor Reporting. [online] Available at:

https://www.auasb.gov.au/Publications/Auditor-Reporting-FAQs.aspx [Accessed 19 Sep. 2018].

Beck, C., Dumay, J. and Frost, G., 2017. In pursuit of a ‘single source of truth’: from threatened

legitimacy to integrated reporting. Journal of Business Ethics, 141(1), pp.191-205.

Ball, F., Tyler, J. and Wells, P., 2015. Is audit quality impacted by auditor relationships?.

Journal of Contemporary Accounting & Economics, 11(2), pp.166-181.

McKee, D., 2015. New external audit report standards are game-changing. Governance

Directions, 67(4), p.222.

Chiu, V. and Vasarhelyi, M.A., 2018. The Development and Intellectual Structure of Continuous

Auditing Research 1. In Continuous Auditing: Theory and Application (pp. 53-85). Emerald

Publishing Limited.

Vanclay, F., 2015. The potential application of qualitative evaluation methods in European

regional development: Reflections on the use of performance story reporting in Australian

natural resource management. Regional Studies, 49(8), pp.1326-1339.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

Chiang, C., 2016. Conceptualising the linkage between professional scepticism and auditor

independence. Pacific Accounting Review, 28(2), pp.180-200.

Mayne, J., 2017. Evaluation for accountability: myth or reality?. In Making Accountability Work

(pp. 81-102). Routledge.

Adams, C.A., 2017. Conceptualising the contemporary corporate value creation process.

Accounting, Auditing & Accountability Journal, 30(4), pp.906-931.

Hoffmann, T., English, T. and Glasziou, P., 2014. Reporting of interventions in randomised

trials: an audit of journal instructions to authors. Trials, 15(1), p.20.

Annual Reports AGL Limited (2018). Annual Reports, 2018. [online] Available at:

https://www.2018annualreport.agl.com.au/xmlpages/resources/TXP/agl_energy/finrep/pdf/

AGL_Energy_Annual_Report_2018.pdf [Accessed 19 Sep. 2018].

Auasb.gov.au. (2018). Auditor Reporting. [online] Available at:

https://www.auasb.gov.au/Publications/Auditor-Reporting-FAQs.aspx [Accessed 19 Sep. 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.