Business Ethics: Enron's Accounting Fraud and Ethical Implications

VerifiedAdded on 2020/04/15

|8

|2601

|77

Essay

AI Summary

This essay provides a comprehensive analysis of the Enron scandal, examining the company's unethical business practices and their devastating consequences. The essay begins with an introduction to business ethics and corporate social responsibility, highlighting the importance of ethical conduct in business operations. It then delves into the specifics of the Enron scandal, detailing the company's accounting fraud, including the use of mark-to-market accounting and special purpose vehicles to manipulate financial statements. The essay explores the impact of the scandal on various stakeholders, including shareholders, employees, and the government, illustrating the significant financial and personal losses suffered. Furthermore, the essay discusses the legal obligations and regulatory changes that followed the scandal, emphasizing the importance of corporate accountability and ethical leadership. Ultimately, the essay concludes by underscoring the critical need for ethical behavior and transparency in business to prevent future scandals and protect stakeholders.

RUNNING HEAD: Business ethics 0

0

Enron

Business ethics

0

Enron

Business ethics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business ethics 1

Contents

Introduction.................................................................................................................................................2

About Enron................................................................................................................................................2

Accounting practices & scandal...................................................................................................................2

Effect on Stakeholders.................................................................................................................................4

Legal obligations..........................................................................................................................................5

Conclusion...................................................................................................................................................5

References...................................................................................................................................................6

Contents

Introduction.................................................................................................................................................2

About Enron................................................................................................................................................2

Accounting practices & scandal...................................................................................................................2

Effect on Stakeholders.................................................................................................................................4

Legal obligations..........................................................................................................................................5

Conclusion...................................................................................................................................................5

References...................................................................................................................................................6

Business ethics 2

Introduction

"Many critics of the concept of corporate responsibility have criticized business interests for

their lack of ethics throughout their operations."

Business ethics is set of rules that tell how business operates, how business decisions are

made, how people (employees, competitors, suppliers, stakeholders, shareholders & customers)

are treated. Ethical business behaviour improves productivity & living standards (Crane &

Matten, 2016). Business ethics is all about doing good things & ignoring bad things at work place.

Business ethics includes all ethics related issues that come while we conduct business activities.

Corporate social responsibility (CSR) is subset of business ethics. It is company’s responsibility

towards the environment, in which it operates. Once a person go through the CSR of company,

can know the mission & responsibility of organisation towards society & economy. It takes care

of human rights & environment protection. It is important to increase competitive advantage & to

build trust with customers & employees (Schmitz & Schrader, 2015). It aims to ensure that a

company operates it’s activities in an ethical way. Many companies publish their information on

their CSR activity on their website. In this assignment ethical issue of Enron is taken. Enron was

an American energy, commodities & services company. The practices & scandal that led to the

issue are explained. Impact on shareholders, employees & government is also discussed as a result

of ethical issue.

About Enron

Enron was America’s seventh largest corporation. The company was established in 1985, by

the merger of Houston natural gas & Inter North. Initially Enron started as Pipeline Company,

expanded with launching broadband services & online website for trading commodities in 1999.

It was the largest business online site & the company was getting 90% of income from the

transactions over Enron online. In 2000 the growth of the company was fast & the annual profits

reached to $100 billion. The stock price peaked at $90. But in 2001, the company’s condition

started deteriorating. In the October the company revealed a loss of $618 million. The company

become bankrupted on December 2, 2001. It was the biggest case of bankruptcy in US and

revealed that it’s financial condition was sustained by well-planned accounting fraud, known as

Enron scandal. Around 5600 employees lost their job. The company ended it’s bankruptcy in

Nov, 2004.

Accounting practices & scandal

Accounting scandals arises from manipulation of financial statements. Accounting practices are

intention manipulation of accounting records in order to make a company’s financial condition

better. They always have adverse effect on the business. Accounting policies are implemented by

accounting practices. These are illegal activities & include misusing funds, understating

expenses, overstating revenue, under recording liabilities, misappropriation of assets & not

taking book keeping seriously enough (Hoàng Văn, 2014). Mark to market accounting and

special purpose vehicle are some techniques used to conduct such illegal activities. In the mark

Introduction

"Many critics of the concept of corporate responsibility have criticized business interests for

their lack of ethics throughout their operations."

Business ethics is set of rules that tell how business operates, how business decisions are

made, how people (employees, competitors, suppliers, stakeholders, shareholders & customers)

are treated. Ethical business behaviour improves productivity & living standards (Crane &

Matten, 2016). Business ethics is all about doing good things & ignoring bad things at work place.

Business ethics includes all ethics related issues that come while we conduct business activities.

Corporate social responsibility (CSR) is subset of business ethics. It is company’s responsibility

towards the environment, in which it operates. Once a person go through the CSR of company,

can know the mission & responsibility of organisation towards society & economy. It takes care

of human rights & environment protection. It is important to increase competitive advantage & to

build trust with customers & employees (Schmitz & Schrader, 2015). It aims to ensure that a

company operates it’s activities in an ethical way. Many companies publish their information on

their CSR activity on their website. In this assignment ethical issue of Enron is taken. Enron was

an American energy, commodities & services company. The practices & scandal that led to the

issue are explained. Impact on shareholders, employees & government is also discussed as a result

of ethical issue.

About Enron

Enron was America’s seventh largest corporation. The company was established in 1985, by

the merger of Houston natural gas & Inter North. Initially Enron started as Pipeline Company,

expanded with launching broadband services & online website for trading commodities in 1999.

It was the largest business online site & the company was getting 90% of income from the

transactions over Enron online. In 2000 the growth of the company was fast & the annual profits

reached to $100 billion. The stock price peaked at $90. But in 2001, the company’s condition

started deteriorating. In the October the company revealed a loss of $618 million. The company

become bankrupted on December 2, 2001. It was the biggest case of bankruptcy in US and

revealed that it’s financial condition was sustained by well-planned accounting fraud, known as

Enron scandal. Around 5600 employees lost their job. The company ended it’s bankruptcy in

Nov, 2004.

Accounting practices & scandal

Accounting scandals arises from manipulation of financial statements. Accounting practices are

intention manipulation of accounting records in order to make a company’s financial condition

better. They always have adverse effect on the business. Accounting policies are implemented by

accounting practices. These are illegal activities & include misusing funds, understating

expenses, overstating revenue, under recording liabilities, misappropriation of assets & not

taking book keeping seriously enough (Hoàng Văn, 2014). Mark to market accounting and

special purpose vehicle are some techniques used to conduct such illegal activities. In the mark

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business ethics 3

to market accounting, assets & liabilities are valued at current price instead of book value. At the

end of financial year, business estimates how much the assets worth is. Special purpose vehicle

is subsidiary of company & protects even when the parental company goes bankrupt. Financial

gain is the aim of such scandals & practices. It includes involvement of employees, financial

advisor or the organisation itself to mislead investors & shareholders. When an organisation

practices such activities then that is charged to loss of reputation, civil & criminal penalties and

loss of human capital (Qi-he, 2013). Enron & it’s accounting firm Arthur Andersen were

involved in the financial scandal, that is known as Enron scandal revealed at the end of 2001.

The chief financial officer Andrew Fastow tried to fake the record of company, made it look like

the company was growing with huge profits and made the future value accounting. Future value

accounting was used to predict the future of Enron that the company was going to make in future

& was considered to be the part of profits of shareholders. As a result, people started to take

interest in company & started buying the shares. In 1990 the company hired Jeffrey Skilling to a

new division Enron finance corp. He involved practices such as, mark to market accounting and

special purpose vehicles to hide huge debt & assets from investors. Special purpose vehicle

(SPVs) is a subsidiary company that makes it’s obligation protected even when the parent

company goes bankrupt. The purpose of this practice was to mislead financial statements rather

than operating results. The company used SPV’s to reduce risks & hide debt to make company’s

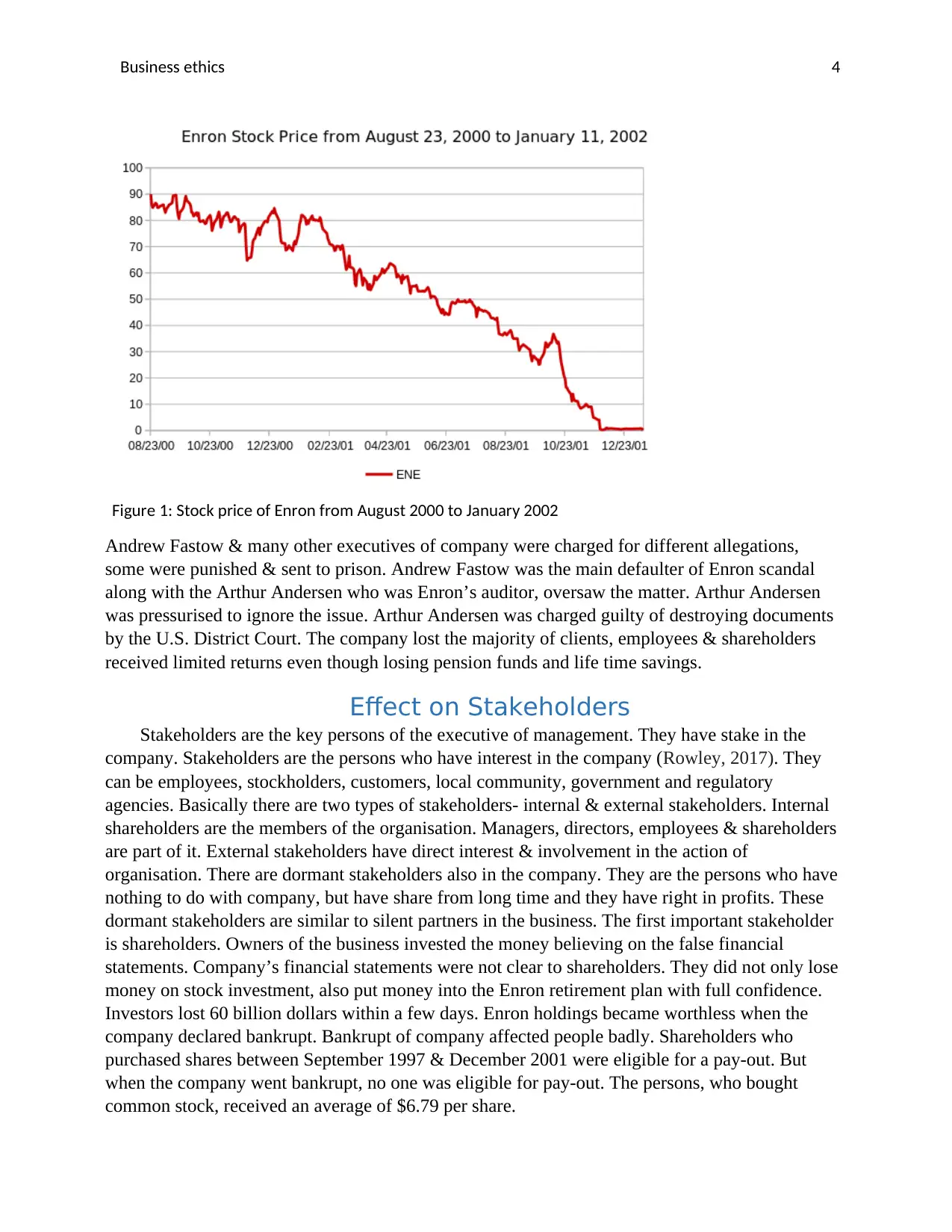

financial statements look better. As the scandal progressed, share prices of Enron decreased from

$90.56 to just $1. The company believed that it’s stock price will keep on increasing but it

declined. The value of SPVs also declined and then the guarantees were forced to play. So, the

company disclosed financial statements and balance sheets of the company. The U.S. Securities

and Exchange Commission initiated an investigation & the rivalry player Dynergy gave an offer

to purchase the company (Nascimento, 2014). The deal failed on December 2, 2001 because the

price offered was very low. Enron filed for bankruptcy under U.S. Bankruptcy Code. It was the

largest bankruptcy case in the U.S. history.

to market accounting, assets & liabilities are valued at current price instead of book value. At the

end of financial year, business estimates how much the assets worth is. Special purpose vehicle

is subsidiary of company & protects even when the parental company goes bankrupt. Financial

gain is the aim of such scandals & practices. It includes involvement of employees, financial

advisor or the organisation itself to mislead investors & shareholders. When an organisation

practices such activities then that is charged to loss of reputation, civil & criminal penalties and

loss of human capital (Qi-he, 2013). Enron & it’s accounting firm Arthur Andersen were

involved in the financial scandal, that is known as Enron scandal revealed at the end of 2001.

The chief financial officer Andrew Fastow tried to fake the record of company, made it look like

the company was growing with huge profits and made the future value accounting. Future value

accounting was used to predict the future of Enron that the company was going to make in future

& was considered to be the part of profits of shareholders. As a result, people started to take

interest in company & started buying the shares. In 1990 the company hired Jeffrey Skilling to a

new division Enron finance corp. He involved practices such as, mark to market accounting and

special purpose vehicles to hide huge debt & assets from investors. Special purpose vehicle

(SPVs) is a subsidiary company that makes it’s obligation protected even when the parent

company goes bankrupt. The purpose of this practice was to mislead financial statements rather

than operating results. The company used SPV’s to reduce risks & hide debt to make company’s

financial statements look better. As the scandal progressed, share prices of Enron decreased from

$90.56 to just $1. The company believed that it’s stock price will keep on increasing but it

declined. The value of SPVs also declined and then the guarantees were forced to play. So, the

company disclosed financial statements and balance sheets of the company. The U.S. Securities

and Exchange Commission initiated an investigation & the rivalry player Dynergy gave an offer

to purchase the company (Nascimento, 2014). The deal failed on December 2, 2001 because the

price offered was very low. Enron filed for bankruptcy under U.S. Bankruptcy Code. It was the

largest bankruptcy case in the U.S. history.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business ethics 4

Figure 1: Stock price of Enron from August 2000 to January 2002

Andrew Fastow & many other executives of company were charged for different allegations,

some were punished & sent to prison. Andrew Fastow was the main defaulter of Enron scandal

along with the Arthur Andersen who was Enron’s auditor, oversaw the matter. Arthur Andersen

was pressurised to ignore the issue. Arthur Andersen was charged guilty of destroying documents

by the U.S. District Court. The company lost the majority of clients, employees & shareholders

received limited returns even though losing pension funds and life time savings.

Effect on Stakeholders

Stakeholders are the key persons of the executive of management. They have stake in the

company. Stakeholders are the persons who have interest in the company (Rowley, 2017). They

can be employees, stockholders, customers, local community, government and regulatory

agencies. Basically there are two types of stakeholders- internal & external stakeholders. Internal

shareholders are the members of the organisation. Managers, directors, employees & shareholders

are part of it. External stakeholders have direct interest & involvement in the action of

organisation. There are dormant stakeholders also in the company. They are the persons who have

nothing to do with company, but have share from long time and they have right in profits. These

dormant stakeholders are similar to silent partners in the business. The first important stakeholder

is shareholders. Owners of the business invested the money believing on the false financial

statements. Company’s financial statements were not clear to shareholders. They did not only lose

money on stock investment, also put money into the Enron retirement plan with full confidence.

Investors lost 60 billion dollars within a few days. Enron holdings became worthless when the

company declared bankrupt. Bankrupt of company affected people badly. Shareholders who

purchased shares between September 1997 & December 2001 were eligible for a pay-out. But

when the company went bankrupt, no one was eligible for pay-out. The persons, who bought

common stock, received an average of $6.79 per share.

Figure 1: Stock price of Enron from August 2000 to January 2002

Andrew Fastow & many other executives of company were charged for different allegations,

some were punished & sent to prison. Andrew Fastow was the main defaulter of Enron scandal

along with the Arthur Andersen who was Enron’s auditor, oversaw the matter. Arthur Andersen

was pressurised to ignore the issue. Arthur Andersen was charged guilty of destroying documents

by the U.S. District Court. The company lost the majority of clients, employees & shareholders

received limited returns even though losing pension funds and life time savings.

Effect on Stakeholders

Stakeholders are the key persons of the executive of management. They have stake in the

company. Stakeholders are the persons who have interest in the company (Rowley, 2017). They

can be employees, stockholders, customers, local community, government and regulatory

agencies. Basically there are two types of stakeholders- internal & external stakeholders. Internal

shareholders are the members of the organisation. Managers, directors, employees & shareholders

are part of it. External stakeholders have direct interest & involvement in the action of

organisation. There are dormant stakeholders also in the company. They are the persons who have

nothing to do with company, but have share from long time and they have right in profits. These

dormant stakeholders are similar to silent partners in the business. The first important stakeholder

is shareholders. Owners of the business invested the money believing on the false financial

statements. Company’s financial statements were not clear to shareholders. They did not only lose

money on stock investment, also put money into the Enron retirement plan with full confidence.

Investors lost 60 billion dollars within a few days. Enron holdings became worthless when the

company declared bankrupt. Bankrupt of company affected people badly. Shareholders who

purchased shares between September 1997 & December 2001 were eligible for a pay-out. But

when the company went bankrupt, no one was eligible for pay-out. The persons, who bought

common stock, received an average of $6.79 per share.

Business ethics 5

Employees struggled to meet their ends. Those who were working from years lost their job in

a movement plus the rewards which were pending. Employees invested their money in Enron

shares, expecting higher prices in future. The price of share was $90.75 but after the bankruptcy

the price of share falls down to $0.67. They did not only lose the job, they lose health care, life

savings & also the old age security (Schermer & Pinxten, 2014). The only mistake that employees

committed was being loyal to their company & wanting their own share & return in future.

Employees had faith in company’s growth & increasing shares of prices (Snellman, 2015). Most

of the employees were given just thirty minutes to empty desk and leave the company. Most of

the employees used to take part in Enron 401 k plan, absolutely got nothing. They move to their

old farmhouse. Employees give up their income to think company will resolve the matter soon

(Petit, 2014). Company’s auditor Arthur Andersen lost it’s accreditation. The board of directors

were also not attentive to company’s book of accounts created by Enron. Directors did not paid

attention to employees because they don’t consider any responsibility towards employees. They

found themselves representatives of shareholders only (Turner, 2015). This thing affected greatly

the long term value of the shareholder’s investment. Workers did not even receive any notice of

lock down, they could not even sell the stock. A worker of the company wanted to sell the shares,

but told that they had been locked out. In 2004, employees of Enron won a suit case of $85

million from their pension fund. By this agreement, an employee received almost $3100 (Preuss,

2013). In the next year shareholders received a wholesome amount of $4.2 billion from banks. In

2008, shareholders amount reached to $7.2 billion from $40 billion lawsuit.

The government set out the regulations & need of the business to do well to keep the

economy healthy (Trevino & Nelson, 2016). The interest of citizens destroyed in American

economic system. They had to face certain economic challenges. Inflation began to rise & it was

hard for them to survive. The livelihood of many individuals affected in the society. It cost the

economy by raising the cost of goods & services. Andersen’s firm was considered with no

intention of providing financial services.

Legal obligations

From the above incident government announced that high level management employees will be

held responsible for the workings of the company (McMillan, 2017). This incident changed the

relationship between American corporations & the American public. One post Enron plan was

also announced by the president. This plan was to make financial statements more clear &

representative by the management. This plan also included high level of corporate social

responsibility also financial responsibility for accountants, CEO’s & auditors (Muller, 2014). The

aim of government was to take strict action but not to put pressure on honest accountants of the

economy. When federal & state laws deal with fraud & other practices, then they don’t follow

ABA model rules rather they adopt culpable & reckless conduct. Culpable & reckless conduct

deals according to the situation & stands for criminal acts. Minimum requirements of culpability

are defined in section 305 that is limitations on scope of culpability requirements. Under federal

securities, there are criminal liability & civil liability which could alter the situation while

investigation.

Employees struggled to meet their ends. Those who were working from years lost their job in

a movement plus the rewards which were pending. Employees invested their money in Enron

shares, expecting higher prices in future. The price of share was $90.75 but after the bankruptcy

the price of share falls down to $0.67. They did not only lose the job, they lose health care, life

savings & also the old age security (Schermer & Pinxten, 2014). The only mistake that employees

committed was being loyal to their company & wanting their own share & return in future.

Employees had faith in company’s growth & increasing shares of prices (Snellman, 2015). Most

of the employees were given just thirty minutes to empty desk and leave the company. Most of

the employees used to take part in Enron 401 k plan, absolutely got nothing. They move to their

old farmhouse. Employees give up their income to think company will resolve the matter soon

(Petit, 2014). Company’s auditor Arthur Andersen lost it’s accreditation. The board of directors

were also not attentive to company’s book of accounts created by Enron. Directors did not paid

attention to employees because they don’t consider any responsibility towards employees. They

found themselves representatives of shareholders only (Turner, 2015). This thing affected greatly

the long term value of the shareholder’s investment. Workers did not even receive any notice of

lock down, they could not even sell the stock. A worker of the company wanted to sell the shares,

but told that they had been locked out. In 2004, employees of Enron won a suit case of $85

million from their pension fund. By this agreement, an employee received almost $3100 (Preuss,

2013). In the next year shareholders received a wholesome amount of $4.2 billion from banks. In

2008, shareholders amount reached to $7.2 billion from $40 billion lawsuit.

The government set out the regulations & need of the business to do well to keep the

economy healthy (Trevino & Nelson, 2016). The interest of citizens destroyed in American

economic system. They had to face certain economic challenges. Inflation began to rise & it was

hard for them to survive. The livelihood of many individuals affected in the society. It cost the

economy by raising the cost of goods & services. Andersen’s firm was considered with no

intention of providing financial services.

Legal obligations

From the above incident government announced that high level management employees will be

held responsible for the workings of the company (McMillan, 2017). This incident changed the

relationship between American corporations & the American public. One post Enron plan was

also announced by the president. This plan was to make financial statements more clear &

representative by the management. This plan also included high level of corporate social

responsibility also financial responsibility for accountants, CEO’s & auditors (Muller, 2014). The

aim of government was to take strict action but not to put pressure on honest accountants of the

economy. When federal & state laws deal with fraud & other practices, then they don’t follow

ABA model rules rather they adopt culpable & reckless conduct. Culpable & reckless conduct

deals according to the situation & stands for criminal acts. Minimum requirements of culpability

are defined in section 305 that is limitations on scope of culpability requirements. Under federal

securities, there are criminal liability & civil liability which could alter the situation while

investigation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business ethics 6

Conclusion

The practices done by Andrew Fastow, Jeffrey Skilling and Arthur Andersen once gave them financial

gain. But ultimately these manipulative practices led to the failure of organisation. Bankruptcy of

organisation shook the entire system. Not only financial advisor & auditor, bankers also contribute to

the downfall of Enron. Financial statements & profits were over shown by the organisation, which

helped organisation to gain customer’s interest & attracted many investors. But bankruptcy of

organisation could not give the return expected by them. The employees lost their job & retirement

savings & affected badly.

References

Crane, A. and Matten, D., 2016. Business ethics: Managing corporate citizenship and

sustainability in the age of globalization. Oxford University Press.

Hoàng Văn, T., 2014. ACCOUNTING ETHICS AND ITS IMPORTANT ROLE FOR REDUCTION

OF ACCOUNTING FRAUD: AN EMPIRICAL STUDY IN HANOI (Doctoral dissertation).

McMillan, C., 2017. Exploring the Strategic Business Processes Senior Leadership use to Enable

Successful Ethical Practice within Their Organization (Doctoral dissertation, Colorado Technical

University).

Muller, A., 2014. Corporate social responsibility. Wiley Encyclopedia of Management.

Nascimento, A., 2014. Ethics and Social Responsability-An agenda for interdisciplinary and

international research on borderless net business ethics. Revista de EDUCAÇÃO do

Cogeime, 17(32/33), pp.235-244.

Petit, E., 2014. The Ethics of Care and Pro-Environmental Behavior. REVUE D ECONOMIE

POLITIQUE, 124(2), pp.243-267.

Preuss, L., 2013. Corporate social responsibility. In Encyclopedia of corporate social

responsibility (pp. 579-587). Springer Berlin Heidelberg.

Qi-he, H.U.A., 2013. Climate Responsibility: What Responsibility. Journal of Huazhong

University of Science and Technology (Social Science Edition), 3, p.021.

Conclusion

The practices done by Andrew Fastow, Jeffrey Skilling and Arthur Andersen once gave them financial

gain. But ultimately these manipulative practices led to the failure of organisation. Bankruptcy of

organisation shook the entire system. Not only financial advisor & auditor, bankers also contribute to

the downfall of Enron. Financial statements & profits were over shown by the organisation, which

helped organisation to gain customer’s interest & attracted many investors. But bankruptcy of

organisation could not give the return expected by them. The employees lost their job & retirement

savings & affected badly.

References

Crane, A. and Matten, D., 2016. Business ethics: Managing corporate citizenship and

sustainability in the age of globalization. Oxford University Press.

Hoàng Văn, T., 2014. ACCOUNTING ETHICS AND ITS IMPORTANT ROLE FOR REDUCTION

OF ACCOUNTING FRAUD: AN EMPIRICAL STUDY IN HANOI (Doctoral dissertation).

McMillan, C., 2017. Exploring the Strategic Business Processes Senior Leadership use to Enable

Successful Ethical Practice within Their Organization (Doctoral dissertation, Colorado Technical

University).

Muller, A., 2014. Corporate social responsibility. Wiley Encyclopedia of Management.

Nascimento, A., 2014. Ethics and Social Responsability-An agenda for interdisciplinary and

international research on borderless net business ethics. Revista de EDUCAÇÃO do

Cogeime, 17(32/33), pp.235-244.

Petit, E., 2014. The Ethics of Care and Pro-Environmental Behavior. REVUE D ECONOMIE

POLITIQUE, 124(2), pp.243-267.

Preuss, L., 2013. Corporate social responsibility. In Encyclopedia of corporate social

responsibility (pp. 579-587). Springer Berlin Heidelberg.

Qi-he, H.U.A., 2013. Climate Responsibility: What Responsibility. Journal of Huazhong

University of Science and Technology (Social Science Edition), 3, p.021.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business ethics 7

Rowley, T.J., 2017. The Power of and in Stakeholder Networks. In Stakeholder Management (pp.

101-122). Emerald Publishing Limited.

Schermer, M. and Pinxten, W. eds., 2014. Ethics, health policy and (anti-) aging: mixed

blessings (Vol. 1). Springer Science & Business Media.

Schmitz, J. and Schrader, J., 2015. Corporate social responsibility: A microeconomic review of

the literature. Journal of Economic Surveys, 29(1), pp.27-45.

Snellman, C.L., 2015. Ethics ManagEMEnt: how to achiEvE Ethical organizations and

ManagEMEnt?. Business, Management and Education, 13(2), p.336.

Trevino, L.K. and Nelson, K.A., 2016. Managing business ethics: Straight talk about how to do it

right. John Wiley & Sons.

Turner, O.D., 2015. Outsourcing decision making: A case study of a small marketing company's

decision to outsource(Doctoral dissertation, University of Phoenix).

Rowley, T.J., 2017. The Power of and in Stakeholder Networks. In Stakeholder Management (pp.

101-122). Emerald Publishing Limited.

Schermer, M. and Pinxten, W. eds., 2014. Ethics, health policy and (anti-) aging: mixed

blessings (Vol. 1). Springer Science & Business Media.

Schmitz, J. and Schrader, J., 2015. Corporate social responsibility: A microeconomic review of

the literature. Journal of Economic Surveys, 29(1), pp.27-45.

Snellman, C.L., 2015. Ethics ManagEMEnt: how to achiEvE Ethical organizations and

ManagEMEnt?. Business, Management and Education, 13(2), p.336.

Trevino, L.K. and Nelson, K.A., 2016. Managing business ethics: Straight talk about how to do it

right. John Wiley & Sons.

Turner, O.D., 2015. Outsourcing decision making: A case study of a small marketing company's

decision to outsource(Doctoral dissertation, University of Phoenix).

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.