Enron's Collapse: A Case Study on Auditing and Implications

VerifiedAdded on 2023/06/04

|7

|254

|407

Case Study

AI Summary

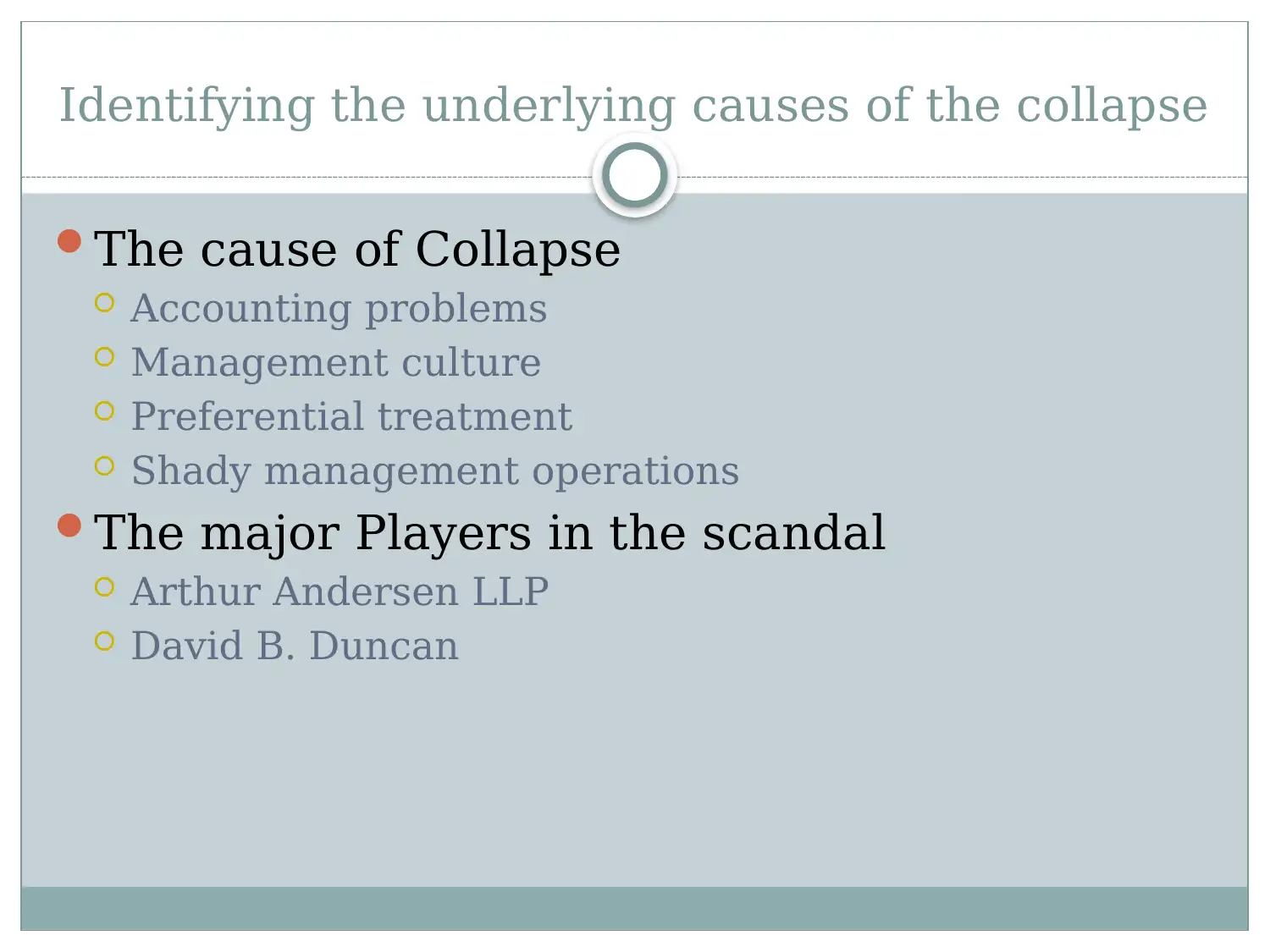

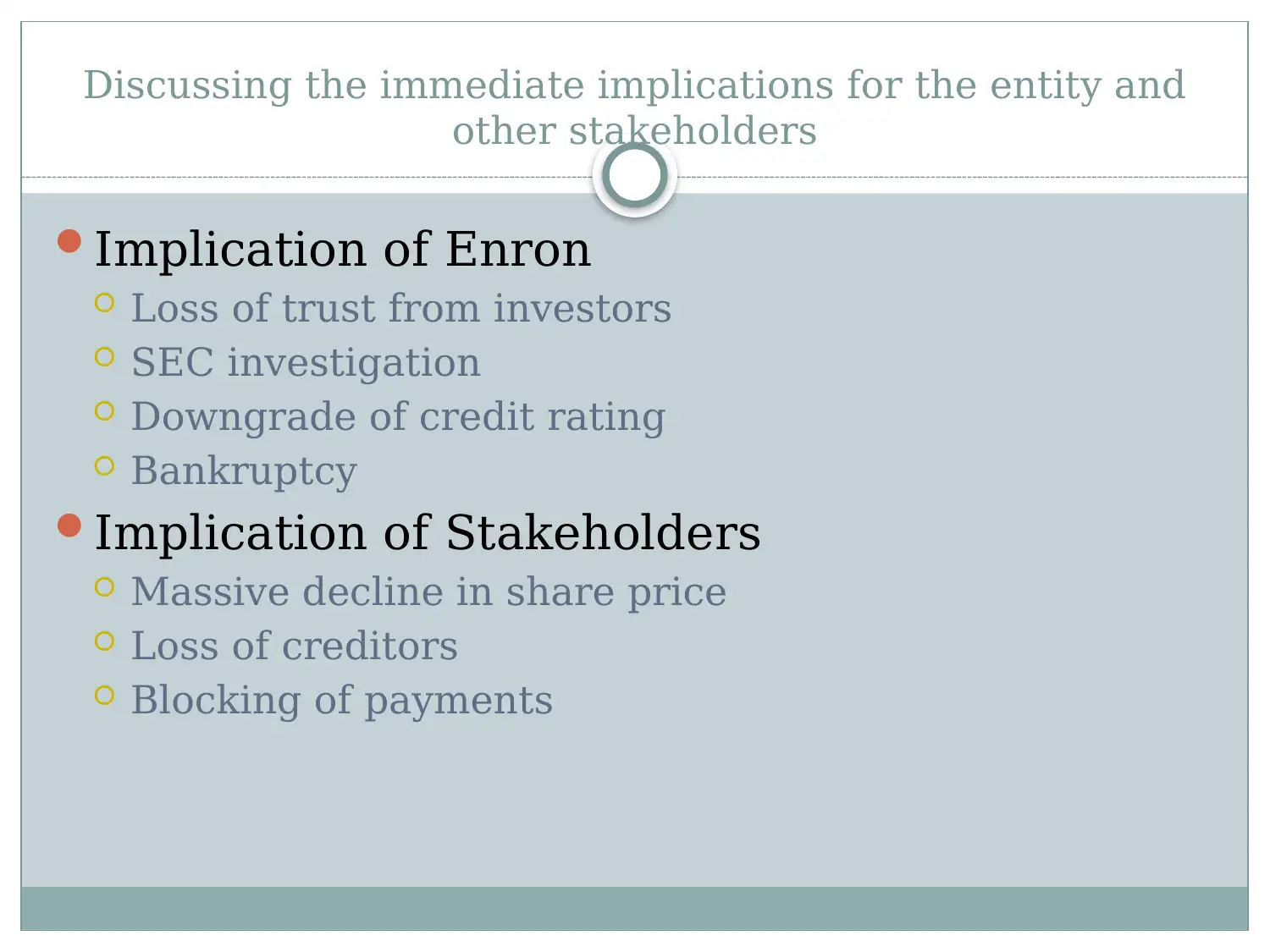

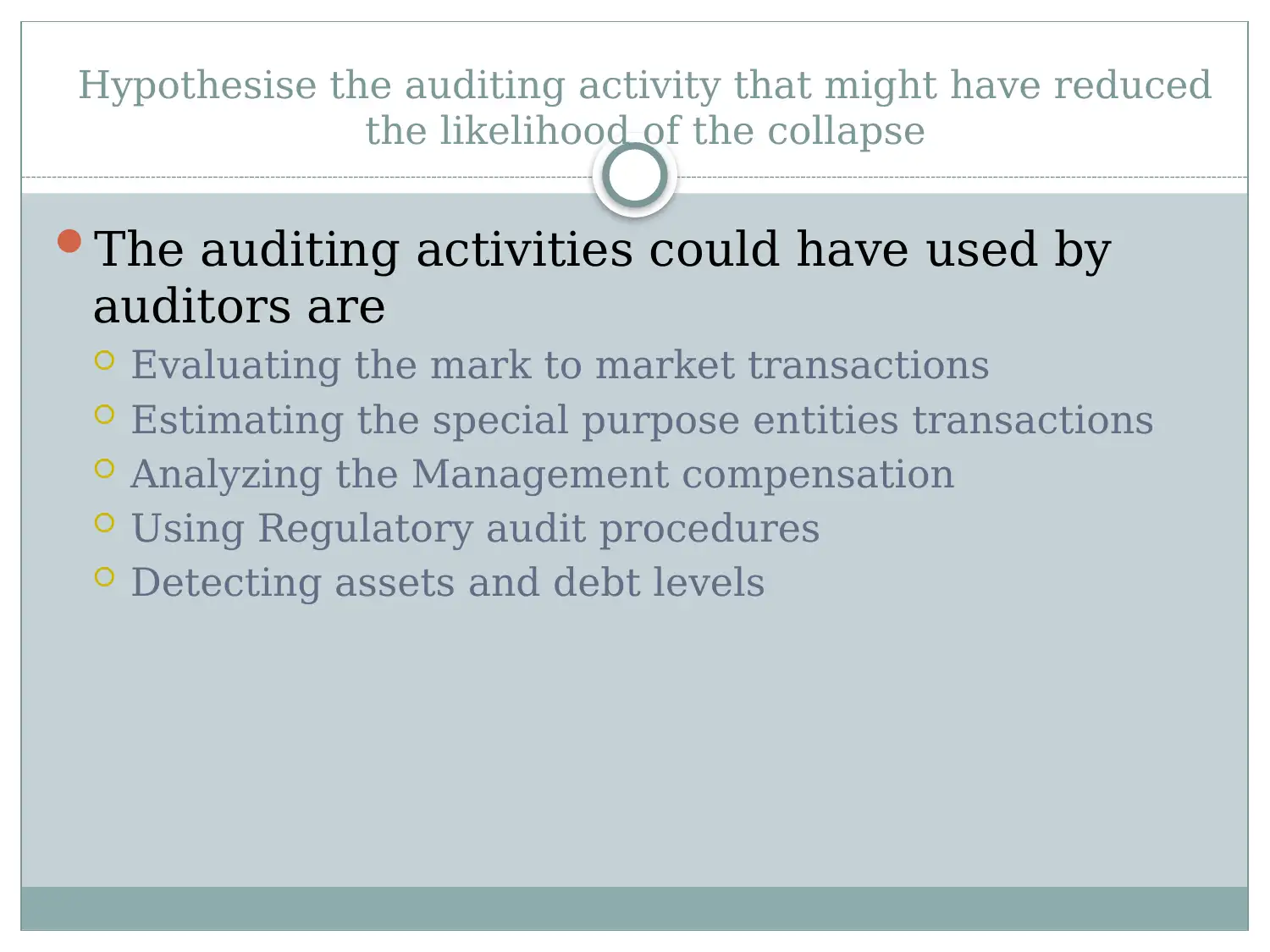

This case study delves into the Enron scandal, dissecting the underlying causes of its collapse, including accounting problems, management culture, preferential treatment, and shady management operations. It identifies key players like Arthur Andersen LLP and David B. Duncan, discussing the immediate implications for Enron and its stakeholders, such as loss of investor trust, SEC investigations, credit rating downgrades, bankruptcy, and massive decline in share price. Furthermore, the study explores broader implications for the corporate world, including the introduction of the Sarbanes-Oxley Act, increased capital market volatility, and reduced investor trust. It also hypothesizes auditing activities that might have reduced the likelihood of the collapse, such as evaluating mark-to-market transactions, estimating special purpose entities transactions, analyzing management compensation, using regulatory audit procedures, and detecting asset and debt levels.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.