Enron's Rise and Fall: Analyzing Business Ethics, Case Study

VerifiedAdded on 2021/05/31

|13

|2506

|57

Case Study

AI Summary

This case study examines the rise and fall of Enron, a major energy company, focusing on the internal and external factors that led to its collapse. It explores issues such as the non-consolidation of Special Purpose Entities (SPEs), accounting irregularities, and breaches of ethical conduct by accounting professionals and auditors. The study highlights the role of corporate culture, leadership failures, and the impact of unethical business practices on stakeholders and the economy. It delves into the failures of auditors, particularly Arthur Andersen, and the lack of effective oversight. Furthermore, the analysis emphasizes the importance of integrity, adherence to regulations, independent judgment, and industry knowledge for accounting professionals. The case study emphasizes the connections between leadership, management, and organizational culture in contributing to Enron's downfall, concluding with the negative effects of unethical business practices and the importance of ethical codes and leadership in preventing such failures.

Running Head: ENRON’S UPS AND DOWNS

Case Study

Student Name

Institution

Date

1

Case Study

Student Name

Institution

Date

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: ENRON’S UPS AND DOWNS

Table of Contents

1.0 Introduction..............................................................................................................................3

1.1 Background..............................................................................................................................3

2.0 The fall of Enron......................................................................................................................5

2.1 Accounting Professionals........................................................................................................5

2.2 Auditors and Accounting Regulations...................................................................................6

2.3 Breaches of accounting and ethical conduct in Enron.........................................................6

2.4 Corporate culture in Enron....................................................................................................7

2.5 Effects of unethical business practices...................................................................................7

2.6 Code of Ethics and Top Leadership.......................................................................................8

3.0 A Follow-Up.............................................................................................................................8

3.1 Integrity....................................................................................................................................8

3.2 Familiar with regulations and laws........................................................................................9

3.3 Independent judgment............................................................................................................9

3.4 Understand the nature of industry.......................................................................................10

4.0 Conclusion..............................................................................................................................10

2

Table of Contents

1.0 Introduction..............................................................................................................................3

1.1 Background..............................................................................................................................3

2.0 The fall of Enron......................................................................................................................5

2.1 Accounting Professionals........................................................................................................5

2.2 Auditors and Accounting Regulations...................................................................................6

2.3 Breaches of accounting and ethical conduct in Enron.........................................................6

2.4 Corporate culture in Enron....................................................................................................7

2.5 Effects of unethical business practices...................................................................................7

2.6 Code of Ethics and Top Leadership.......................................................................................8

3.0 A Follow-Up.............................................................................................................................8

3.1 Integrity....................................................................................................................................8

3.2 Familiar with regulations and laws........................................................................................9

3.3 Independent judgment............................................................................................................9

3.4 Understand the nature of industry.......................................................................................10

4.0 Conclusion..............................................................................................................................10

2

Running Head: ENRON’S UPS AND DOWNS

1.0 Introduction

Enron organization is a large firm that deals in energy and gas with special duty units which are

allies that keep accountabilities and money on several balance sheet with the aim of justifying

and evade losses, destruction and making monetary statement have a good look at the times of

obtaining cash. The company was damaged when there was an effort of archiving the accounting

annals relatively than the real commercial presentation achievement. Apart from the non-

consolidation problems of SPE, it was revealed in the case that principle of bookkeeping of

auction and reasonable worth had problems too that is based on report on power. Several internal

and external factors together with the triggers Enrol transformation from success to failure. E.g.

external auditing, management, GAAP and FASB.

1.1 Background

There was an indication that the newly appointed CEO, Skilling, to a huge range, reformed the

environment and the culture of Enron company. There was alteration of the organization`s

operations. There was a believe that Skilling tried to twist the rule so that it could favour him.

For instance, followed short-range act attainment and expanded more commercial in the field of

money rather than the initial commercial – gas and pipeline. In addition, the environment within

the Enron company was found to be around because of the strategies that were performance-

orientated plus the policy of inducements that becomes a significant to persons who try to reach

the target irrespective of the code of ethics.

3

1.0 Introduction

Enron organization is a large firm that deals in energy and gas with special duty units which are

allies that keep accountabilities and money on several balance sheet with the aim of justifying

and evade losses, destruction and making monetary statement have a good look at the times of

obtaining cash. The company was damaged when there was an effort of archiving the accounting

annals relatively than the real commercial presentation achievement. Apart from the non-

consolidation problems of SPE, it was revealed in the case that principle of bookkeeping of

auction and reasonable worth had problems too that is based on report on power. Several internal

and external factors together with the triggers Enrol transformation from success to failure. E.g.

external auditing, management, GAAP and FASB.

1.1 Background

There was an indication that the newly appointed CEO, Skilling, to a huge range, reformed the

environment and the culture of Enron company. There was alteration of the organization`s

operations. There was a believe that Skilling tried to twist the rule so that it could favour him.

For instance, followed short-range act attainment and expanded more commercial in the field of

money rather than the initial commercial – gas and pipeline. In addition, the environment within

the Enron company was found to be around because of the strategies that were performance-

orientated plus the policy of inducements that becomes a significant to persons who try to reach

the target irrespective of the code of ethics.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: ENRON’S UPS AND DOWNS

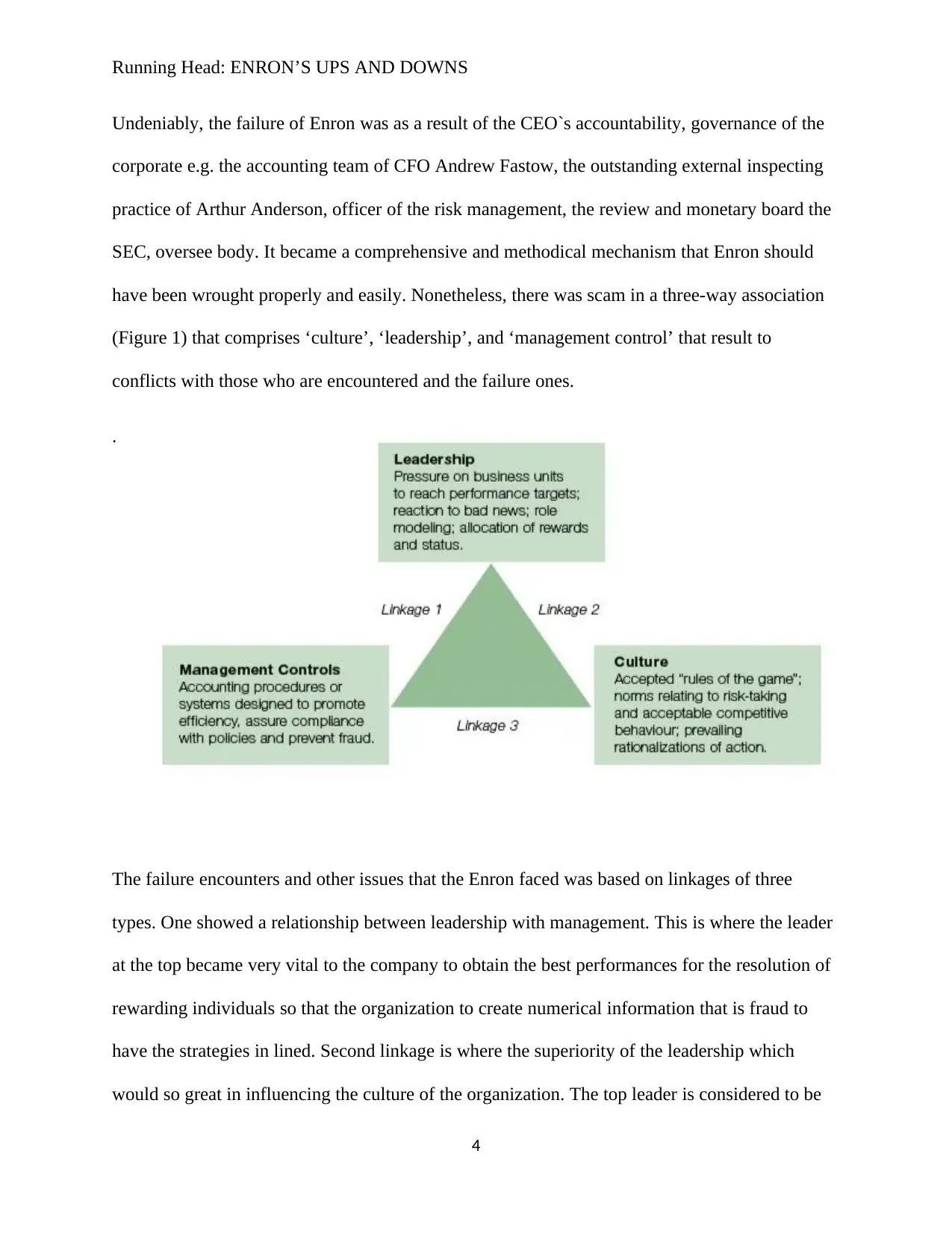

Undeniably, the failure of Enron was as a result of the CEO`s accountability, governance of the

corporate e.g. the accounting team of CFO Andrew Fastow, the outstanding external inspecting

practice of Arthur Anderson, officer of the risk management, the review and monetary board the

SEC, oversee body. It became a comprehensive and methodical mechanism that Enron should

have been wrought properly and easily. Nonetheless, there was scam in a three-way association

(Figure 1) that comprises ‘culture’, ‘leadership’, and ‘management control’ that result to

conflicts with those who are encountered and the failure ones.

.

The failure encounters and other issues that the Enron faced was based on linkages of three

types. One showed a relationship between leadership with management. This is where the leader

at the top became very vital to the company to obtain the best performances for the resolution of

rewarding individuals so that the organization to create numerical information that is fraud to

have the strategies in lined. Second linkage is where the superiority of the leadership which

would so great in influencing the culture of the organization. The top leader is considered to be

4

Undeniably, the failure of Enron was as a result of the CEO`s accountability, governance of the

corporate e.g. the accounting team of CFO Andrew Fastow, the outstanding external inspecting

practice of Arthur Anderson, officer of the risk management, the review and monetary board the

SEC, oversee body. It became a comprehensive and methodical mechanism that Enron should

have been wrought properly and easily. Nonetheless, there was scam in a three-way association

(Figure 1) that comprises ‘culture’, ‘leadership’, and ‘management control’ that result to

conflicts with those who are encountered and the failure ones.

.

The failure encounters and other issues that the Enron faced was based on linkages of three

types. One showed a relationship between leadership with management. This is where the leader

at the top became very vital to the company to obtain the best performances for the resolution of

rewarding individuals so that the organization to create numerical information that is fraud to

have the strategies in lined. Second linkage is where the superiority of the leadership which

would so great in influencing the culture of the organization. The top leader is considered to be

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: ENRON’S UPS AND DOWNS

vital for the company who are sanctioned to have the rules set for the games they desire to have

the management performed. The third linkage is the connection of the management controls and

culture that the followers could prefer to have an acceptance choice on ruling to take the risk to

doing erroneous stuffs that were acknowledged by the company`s own environment and culture.

5

vital for the company who are sanctioned to have the rules set for the games they desire to have

the management performed. The third linkage is the connection of the management controls and

culture that the followers could prefer to have an acceptance choice on ruling to take the risk to

doing erroneous stuffs that were acknowledged by the company`s own environment and culture.

5

Running Head: ENRON’S UPS AND DOWNS

2.0 The fall of Enron

2.1 Accounting Professionals

Accounting professionals were blamed for bankruptcy of the Eron company. Errors that are

related to the unfinished and less accurate monetary reports that led to a great loss in the

reaffirmed reports. there are identified issues that are associated to the accounting professional

that includes non-consolidating SPEs, inventory stock, accounting treatment, fair value

accounting and income recognition and the monetary reports that are disclosed.

In precise, for instance, investment gain of the Enron in SPE (JEDI) plus the acquisition of

CalPERS (known as JEDI as joint venture) which were eliminated only half in the monetary

reports consolidated even though it has to be eliminated fully. In addition, Enron had used the

SPEs to resist the negative info to be printed to the shareholder, that did distortion of the rule in

the accounting. In addition, Enron made that the mistakes are elementary in the accounting

treatment salary, where the income has to be recognized over several over a period of time of the

contract that is recorded directly as the present revenue. Moreover, there could be argument that

GAAP in an aspect that could not provide a precise direction for the company but Enron made

power to prance regulations. For example, despite GAAP not allowing increased record value of

the organization`s own records as an income where the company had a record gap of between the

higher fixed value in a strike price and contract in the bazaar as a gain in order to increase fund.

Seemingly, the bookkeeping faults, in form of the surfaces of method and scam, accounted for

large amount of the weakening.

6

2.0 The fall of Enron

2.1 Accounting Professionals

Accounting professionals were blamed for bankruptcy of the Eron company. Errors that are

related to the unfinished and less accurate monetary reports that led to a great loss in the

reaffirmed reports. there are identified issues that are associated to the accounting professional

that includes non-consolidating SPEs, inventory stock, accounting treatment, fair value

accounting and income recognition and the monetary reports that are disclosed.

In precise, for instance, investment gain of the Enron in SPE (JEDI) plus the acquisition of

CalPERS (known as JEDI as joint venture) which were eliminated only half in the monetary

reports consolidated even though it has to be eliminated fully. In addition, Enron had used the

SPEs to resist the negative info to be printed to the shareholder, that did distortion of the rule in

the accounting. In addition, Enron made that the mistakes are elementary in the accounting

treatment salary, where the income has to be recognized over several over a period of time of the

contract that is recorded directly as the present revenue. Moreover, there could be argument that

GAAP in an aspect that could not provide a precise direction for the company but Enron made

power to prance regulations. For example, despite GAAP not allowing increased record value of

the organization`s own records as an income where the company had a record gap of between the

higher fixed value in a strike price and contract in the bazaar as a gain in order to increase fund.

Seemingly, the bookkeeping faults, in form of the surfaces of method and scam, accounted for

large amount of the weakening.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: ENRON’S UPS AND DOWNS

2.2 Auditors and Accounting Regulations

Auditors have the responsibility of detecting the material that is miss stated in the in the financial

archives. Just as mentioned in the section two of the introduction part, the Enron organisation

had a mechanism that was confiscated to have the operation controlled that included committees

of auditing. Nevertheless, there was a revelation that the checkup committee that entailed many

professionals who failed or rather avoided to have the best performance procedure that is

sufficient to detecting problems. For example, in most meetings, there was no agender that had

been referred to the critical issues and the checkup committees that never had any queries of

SPEs plus the disagreement on some dubious businesses. it is obvious that the external practice

of auditing of Arthur Anderson was the biggest firm that failed to make its own execution on

duties. With the above faults, it becomes so hard to have an understanding how capable auditors

never had a chance to detect and have a suggestion on the accounting team to have them

corrected. Auditors have to bring out the suspicion within an organisation and have the ethical

procedures to get access to the proof and have the errors adjusted.

2.3 Breaches of accounting and ethical conduct in Enron

The breach of integrity was conducted but wrong behavior conducted by the accounting, this

required act of professional honesty and following the right principles that help in making of

skilled judgement and also dealing with relationship of other business partners. To be specific it

required that the skilled professions should be able to produce ‘true and fair’ financial statements

that do not have mistaken and errors and imitation of the information required. In addition, that

there was any arose of misconduct, it was to take action to avoid and also correct. In Enron’s

case evidence showed that professionals in accounting made intentional errors on some primary

and simple accounting issues, and also showed they failed to act honestly. In the meantime,

7

2.2 Auditors and Accounting Regulations

Auditors have the responsibility of detecting the material that is miss stated in the in the financial

archives. Just as mentioned in the section two of the introduction part, the Enron organisation

had a mechanism that was confiscated to have the operation controlled that included committees

of auditing. Nevertheless, there was a revelation that the checkup committee that entailed many

professionals who failed or rather avoided to have the best performance procedure that is

sufficient to detecting problems. For example, in most meetings, there was no agender that had

been referred to the critical issues and the checkup committees that never had any queries of

SPEs plus the disagreement on some dubious businesses. it is obvious that the external practice

of auditing of Arthur Anderson was the biggest firm that failed to make its own execution on

duties. With the above faults, it becomes so hard to have an understanding how capable auditors

never had a chance to detect and have a suggestion on the accounting team to have them

corrected. Auditors have to bring out the suspicion within an organisation and have the ethical

procedures to get access to the proof and have the errors adjusted.

2.3 Breaches of accounting and ethical conduct in Enron

The breach of integrity was conducted but wrong behavior conducted by the accounting, this

required act of professional honesty and following the right principles that help in making of

skilled judgement and also dealing with relationship of other business partners. To be specific it

required that the skilled professions should be able to produce ‘true and fair’ financial statements

that do not have mistaken and errors and imitation of the information required. In addition, that

there was any arose of misconduct, it was to take action to avoid and also correct. In Enron’s

case evidence showed that professionals in accounting made intentional errors on some primary

and simple accounting issues, and also showed they failed to act honestly. In the meantime,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: ENRON’S UPS AND DOWNS

objectivity should focus on Eron’s case. Professionals in accounting were required to have their

own ruling and not compromise the weight and bias. other organisation. Professional in

accounting lost the right ruling under the unmoral environment of Eron case, this simply attained

individual interest.

8

objectivity should focus on Eron’s case. Professionals in accounting were required to have their

own ruling and not compromise the weight and bias. other organisation. Professional in

accounting lost the right ruling under the unmoral environment of Eron case, this simply attained

individual interest.

8

Running Head: ENRON’S UPS AND DOWNS

2.4 Corporate culture in Enron

Eron was poor in risk management as indicated, this was the culture to expand the thing in

approach of reaching the edge. In persuasion of higher return, it took risking without considering

bad consequences. In the meantime, comparing industries of traditional energy, eversion of old

attempted and routine exploration of business in new ways, which focused on returns from the

trading financials instead of those from hard assets. Also, it invested on ‘fancy’ and other lavish

things e.g. image and advertisement in the operation of business. The unethical dilemma was

much pushed by the Enron’s negative transformation culture.

2.5 Effects of unethical business practices

The negative effects of illegal business bring harm to both society and community. This leads to

loss of confidence on the recorded firms and their financial statements as they are indicated from

the Enron’s fall. Although reports financials have comments of auditors and administrations, the

public would be reluctant in accepting the superiority of such financial reports. As such a

company is required to get more accredited and external statement which could turn to be

inefficient and costly in economical aspect. Also, there will be wastage of society resources, e.g.

Where public had invested money in the unethical firm like Enron. They could have deposit

money in the stable firms but ending up in the unstable companies, where resources are used in a

wasteful manner which can lead to the downfall of economy to a huge extent. The unethical

business consequences forced in the coming of the new polices that would cost firms to comply

with. This would reduce the development cost in business eventually this brings negative effects

of the improvement. On the other hand, mitigation of unethical behavior would be curbed by the

new regulations.

9

2.4 Corporate culture in Enron

Eron was poor in risk management as indicated, this was the culture to expand the thing in

approach of reaching the edge. In persuasion of higher return, it took risking without considering

bad consequences. In the meantime, comparing industries of traditional energy, eversion of old

attempted and routine exploration of business in new ways, which focused on returns from the

trading financials instead of those from hard assets. Also, it invested on ‘fancy’ and other lavish

things e.g. image and advertisement in the operation of business. The unethical dilemma was

much pushed by the Enron’s negative transformation culture.

2.5 Effects of unethical business practices

The negative effects of illegal business bring harm to both society and community. This leads to

loss of confidence on the recorded firms and their financial statements as they are indicated from

the Enron’s fall. Although reports financials have comments of auditors and administrations, the

public would be reluctant in accepting the superiority of such financial reports. As such a

company is required to get more accredited and external statement which could turn to be

inefficient and costly in economical aspect. Also, there will be wastage of society resources, e.g.

Where public had invested money in the unethical firm like Enron. They could have deposit

money in the stable firms but ending up in the unstable companies, where resources are used in a

wasteful manner which can lead to the downfall of economy to a huge extent. The unethical

business consequences forced in the coming of the new polices that would cost firms to comply

with. This would reduce the development cost in business eventually this brings negative effects

of the improvement. On the other hand, mitigation of unethical behavior would be curbed by the

new regulations.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: ENRON’S UPS AND DOWNS

2.6 Code of Ethics and Top Leadership

Leaders at the top could have some influence on the execution conduct or code of ethics. There

was a research mentioned the code of ethics highlighted in Eron, e.g. ‘we work …honestly and

sincerely’ and ‘we do not tolerate abusive or disrespectful treatment’ were confirmed reaffirmed

by employees each year. In addition, separated the power of supervision in a robust mechanism.

These infrastructures nevertheless were to window-dress what is inside the organisation. The

higher management not pay any attention to some of these issues. The fading efforts which

helped in setting up of the ethical code undermined the value of ethical code in Enron. Also, the

hierarchy and reinforced management helped the top officers to have strong powers that lead

them to exploit and change the value of code so as to accept their unethical conduct.

10

2.6 Code of Ethics and Top Leadership

Leaders at the top could have some influence on the execution conduct or code of ethics. There

was a research mentioned the code of ethics highlighted in Eron, e.g. ‘we work …honestly and

sincerely’ and ‘we do not tolerate abusive or disrespectful treatment’ were confirmed reaffirmed

by employees each year. In addition, separated the power of supervision in a robust mechanism.

These infrastructures nevertheless were to window-dress what is inside the organisation. The

higher management not pay any attention to some of these issues. The fading efforts which

helped in setting up of the ethical code undermined the value of ethical code in Enron. Also, the

hierarchy and reinforced management helped the top officers to have strong powers that lead

them to exploit and change the value of code so as to accept their unethical conduct.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: ENRON’S UPS AND DOWNS

3.0 A Follow-Up

3.1 Integrity

Basing on the Enron`s case, it shows that honesty became the main and vital characteristics for

the professionals that deal with accounting on critical and information confidentiality. Just the

way the accounting professionals had provided archives on finance, to stick with the decision

making from the stakeholders for honesty and integrity purposes to provide correct and info that

is fair. Enron also engrossed on attainment in numbers rather than real processes that had been

reports provided by the professionals of the accounting which didn’t replicate the actual state of

the organisation have the shareholders mislead.

3.2 Familiar with regulations and laws

Considering the Enron’s case, office experts were well rained, it still holds that they did not have

consciousness of the essentials of 8 laws and procedures. Rules and policies would be altered

with the change in environment and people’s wishes, the office experts are expected to have

information and be mindful on the field of policies that are connected to the corporate they

operated on. In case scenario where policies e.g., the inauguration of the law on the environment,

the office experts are supposed to have aware of it and make changes of connected operation and

financial records, this is to assure the superiority of info.

11

3.0 A Follow-Up

3.1 Integrity

Basing on the Enron`s case, it shows that honesty became the main and vital characteristics for

the professionals that deal with accounting on critical and information confidentiality. Just the

way the accounting professionals had provided archives on finance, to stick with the decision

making from the stakeholders for honesty and integrity purposes to provide correct and info that

is fair. Enron also engrossed on attainment in numbers rather than real processes that had been

reports provided by the professionals of the accounting which didn’t replicate the actual state of

the organisation have the shareholders mislead.

3.2 Familiar with regulations and laws

Considering the Enron’s case, office experts were well rained, it still holds that they did not have

consciousness of the essentials of 8 laws and procedures. Rules and policies would be altered

with the change in environment and people’s wishes, the office experts are expected to have

information and be mindful on the field of policies that are connected to the corporate they

operated on. In case scenario where policies e.g., the inauguration of the law on the environment,

the office experts are supposed to have aware of it and make changes of connected operation and

financial records, this is to assure the superiority of info.

11

Running Head: ENRON’S UPS AND DOWNS

3.3 Independent judgment

During working atmosphere, it is most preferred to work as a group to finish a certain duty.

Nonetheless it is probably you would be losing or give in your thought that you see is not much

of importance but it is. On Enron’s case it could be seen that office experts might have pressure

from higher administration or lacked to have their own verdict under the unsuitable functioning

atmosphere. Under this condition, the sovereign ruling becomes more of a value. In addition, it is

not wise to just count on others. According to office specialization, it is important to regularly

have a vivid route and also behave morally no matter what people may say or think.

3.4 Understand the nature of industry

The fall of Enron was comprised of the issues of norms or business revolution. Later 2000,

Enron left the ancient ship and discovered the new property of trading of merchandise which it

lastly got misfortune with. To be an expert in financial records, it is expected to be have

comprehension of the nature of professional and business so as to help in in utilization of

resources and perform the right thing.

12

3.3 Independent judgment

During working atmosphere, it is most preferred to work as a group to finish a certain duty.

Nonetheless it is probably you would be losing or give in your thought that you see is not much

of importance but it is. On Enron’s case it could be seen that office experts might have pressure

from higher administration or lacked to have their own verdict under the unsuitable functioning

atmosphere. Under this condition, the sovereign ruling becomes more of a value. In addition, it is

not wise to just count on others. According to office specialization, it is important to regularly

have a vivid route and also behave morally no matter what people may say or think.

3.4 Understand the nature of industry

The fall of Enron was comprised of the issues of norms or business revolution. Later 2000,

Enron left the ancient ship and discovered the new property of trading of merchandise which it

lastly got misfortune with. To be an expert in financial records, it is expected to be have

comprehension of the nature of professional and business so as to help in in utilization of

resources and perform the right thing.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.