Unethical Practices at Enron: An Analysis of Business Ethical Dilemmas

VerifiedAdded on 2022/09/06

|14

|3452

|31

Report

AI Summary

This report provides a comprehensive analysis of the Enron ethical dilemma, exploring the company's unethical practices and their implications. The report begins with an executive summary and table of contents, followed by an introduction that defines ethical dilemmas and highlights the importance of ethical behavior in organizations. It then delves into a discussion contrasting the ethical theories of egoism and deontology, applying them to the Enron case to illustrate how Enron's actions aligned with egoistic principles while violating deontological duties. The report further applies the AAA model of ethical decision-making, outlining the steps accountants should take to make ethical choices in similar situations. Finally, it applies the Ferrell, Fraedrich, and Ferrell model to the Enron case, providing a structured framework for understanding the factors that contributed to the company's downfall. The conclusion summarizes the key findings, emphasizing the importance of ethical conduct and the consequences of unethical behavior in business. The report references relevant literature to support its analysis and findings.

Running head: ETHICAL DILEMMA OF ENRON

ETHICAL DILEMMA OF ENRON

Name of Student

Name of the University

Author Note

ETHICAL DILEMMA OF ENRON

Name of Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ETHICAL DILEMMA OF ENRON

Executive Summary

Ethical activities or behaviours refer to all those activities of individuals that are in

accordance with the social norms and also in accordance with different ethical principles.

Organizations are required to behave in an ethical manner and are required to take into

consideration the triple bottom line while carrying out their activities in order to become

successful in the long run. The company selected for the purpose of the study was Enron. The

main objective of the paper was to discuss about the unethical activities at Enron. The paper

therefore discussed about the different ethical theories, application of the AAA model of ethical

decision making and also the showed the application of the Ferrell, Fraedrich and Ferrell model

in the case of Enron.

Executive Summary

Ethical activities or behaviours refer to all those activities of individuals that are in

accordance with the social norms and also in accordance with different ethical principles.

Organizations are required to behave in an ethical manner and are required to take into

consideration the triple bottom line while carrying out their activities in order to become

successful in the long run. The company selected for the purpose of the study was Enron. The

main objective of the paper was to discuss about the unethical activities at Enron. The paper

therefore discussed about the different ethical theories, application of the AAA model of ethical

decision making and also the showed the application of the Ferrell, Fraedrich and Ferrell model

in the case of Enron.

2ETHICAL DILEMMA OF ENRON

Table of Contents

Introduction..........................................................................................................................3

Discussion............................................................................................................................3

Part A: Contrast between the ethical theories of egoism and deontology and application

of the same to the case of Enron..................................................................................................3

Part B: Application of the AAA model that should be used by accountants for the

purpose of obtaining an ethical decision making........................................................................6

Part C: Application of the Ferrell, Fraedrich and Ferrell model in the case of Enron.....8

Conclusion.........................................................................................................................11

References..........................................................................................................................11

Table of Contents

Introduction..........................................................................................................................3

Discussion............................................................................................................................3

Part A: Contrast between the ethical theories of egoism and deontology and application

of the same to the case of Enron..................................................................................................3

Part B: Application of the AAA model that should be used by accountants for the

purpose of obtaining an ethical decision making........................................................................6

Part C: Application of the Ferrell, Fraedrich and Ferrell model in the case of Enron.....8

Conclusion.........................................................................................................................11

References..........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ETHICAL DILEMMA OF ENRON

Introduction

Ethical dilemma refers to a problem of decision making where there are more than two

alternatives and none of the alternatives are morally acceptable. Moreover it includes situation of

conflict where if an individual goes for one particular alternative it results in transgressing

another alternative. Therefore in this respect it is necessary to understand the different ethical

theories such as deontology and also that of ethical theory of Egoism. An ethical behavior

includes behaving in accordance with the socially accepted values and also includes respecting

moral principles of honesty, integrity, equality, dignity and similar others. Further there are

certain fields of study which require compliance with certain guidelines for the purpose of

conducting ethical activities (Sims & Brinkmann, 2003). The company selected for the purpose

of this study includes Enron Company. Enron is one such company based in US that had been

engaged in unethical activities or behavior and also failed to comply with the accounting

guidelines. The main aim of the paper is to identify and discuss about unethical behavior and

also the guidelines that Enron was required to follow. The paper will discuss about the ethical

theories of Deontology, Egoism, application of the AAA model by the accountants and also

includes- making application of Ferrell, Fraedrich and Ferrell model.

Discussion

Part A: Contrast between the ethical theories of egoism and deontology and

application of the same to the case of Enron

The theory of egoism is based on the principle that everyone should act for their own

self-interest. The ethical theory of egoism can further be understood from three main

perspectives- individual, personal and also universal. The PERSONAL ETHICAL EGOISM is

Introduction

Ethical dilemma refers to a problem of decision making where there are more than two

alternatives and none of the alternatives are morally acceptable. Moreover it includes situation of

conflict where if an individual goes for one particular alternative it results in transgressing

another alternative. Therefore in this respect it is necessary to understand the different ethical

theories such as deontology and also that of ethical theory of Egoism. An ethical behavior

includes behaving in accordance with the socially accepted values and also includes respecting

moral principles of honesty, integrity, equality, dignity and similar others. Further there are

certain fields of study which require compliance with certain guidelines for the purpose of

conducting ethical activities (Sims & Brinkmann, 2003). The company selected for the purpose

of this study includes Enron Company. Enron is one such company based in US that had been

engaged in unethical activities or behavior and also failed to comply with the accounting

guidelines. The main aim of the paper is to identify and discuss about unethical behavior and

also the guidelines that Enron was required to follow. The paper will discuss about the ethical

theories of Deontology, Egoism, application of the AAA model by the accountants and also

includes- making application of Ferrell, Fraedrich and Ferrell model.

Discussion

Part A: Contrast between the ethical theories of egoism and deontology and

application of the same to the case of Enron

The theory of egoism is based on the principle that everyone should act for their own

self-interest. The ethical theory of egoism can further be understood from three main

perspectives- individual, personal and also universal. The PERSONAL ETHICAL EGOISM is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ETHICAL DILEMMA OF ENRON

based on the belief that individuals should behave and act for the purpose of their own self-

interest and also this theory fails to discuss about the motives or interest that other people should

consider while acting. However PERSONAL ETHICAL EGOISM suffers from certain

drawbacks such as it cannot be considered as a theory because it cannot be applied to everyone

or it cannot be generalised. And therefore this theory cannot be recommended for other people.

The second perspective of the ethical egoism theory comprises of Individual ethical egoism

theory. The individual ethical egoism is based on the belief that everyone should serve only one

person’s self-interest (Broad, 2014). This perspective also cannot be called as a theory because it

cannot be universalised and therefore it is a doctrine. Moreover this doctrine is faced with a

drawback that it is only consistent to one person and to nobody else. Therefore this doctrine is

somewhat similar to the theory of solipsism. The third perspective of the ethical egoism theory

comprises of the Universal Ethical egoism. This perspective is based on the assumption that all

individuals need to behave and act according to their own self-interest exclusively. Therefore

according to the ethical egoism theory, Enron behaved ethically as it fulfils all the required

parameters for becoming an organization that follows ethical egoism. Enron is one such

company that puts more emphasis on list own corporate culture than the code of ethics or any

other similar ethical codes (Longenecker, McKinney & Moore, 1988). The company has a deep

rooted organizational culture and it is the organizational culture that determines ethics in Enron.

Therefore the activities of the employees are determined by their organizational culture and not

by some code of ethics. Therefore the organizational culture of Enron is similar to the ethical

egoism theory because according to the theory, organizations or individuals are required to work

and act for their self-interest and the motives or interests of other people are not taken into

consideration according to the theory. Therefore according to the ethical egoism theory, Enron

based on the belief that individuals should behave and act for the purpose of their own self-

interest and also this theory fails to discuss about the motives or interest that other people should

consider while acting. However PERSONAL ETHICAL EGOISM suffers from certain

drawbacks such as it cannot be considered as a theory because it cannot be applied to everyone

or it cannot be generalised. And therefore this theory cannot be recommended for other people.

The second perspective of the ethical egoism theory comprises of Individual ethical egoism

theory. The individual ethical egoism is based on the belief that everyone should serve only one

person’s self-interest (Broad, 2014). This perspective also cannot be called as a theory because it

cannot be universalised and therefore it is a doctrine. Moreover this doctrine is faced with a

drawback that it is only consistent to one person and to nobody else. Therefore this doctrine is

somewhat similar to the theory of solipsism. The third perspective of the ethical egoism theory

comprises of the Universal Ethical egoism. This perspective is based on the assumption that all

individuals need to behave and act according to their own self-interest exclusively. Therefore

according to the ethical egoism theory, Enron behaved ethically as it fulfils all the required

parameters for becoming an organization that follows ethical egoism. Enron is one such

company that puts more emphasis on list own corporate culture than the code of ethics or any

other similar ethical codes (Longenecker, McKinney & Moore, 1988). The company has a deep

rooted organizational culture and it is the organizational culture that determines ethics in Enron.

Therefore the activities of the employees are determined by their organizational culture and not

by some code of ethics. Therefore the organizational culture of Enron is similar to the ethical

egoism theory because according to the theory, organizations or individuals are required to work

and act for their self-interest and the motives or interests of other people are not taken into

consideration according to the theory. Therefore according to the ethical egoism theory, Enron

5ETHICAL DILEMMA OF ENRON

acted ethically because it was working for its own interest exclusively. Moreover the

organizational culture of Enron was based on Schein’s theory of organizational culture.

According to the same, the basic assumptions of individuals lay down the basis for values and it

is the values that lay down the basis for behaviour and practices within the organization and

therefore the same is reflected in the organizational culture (Lee & Fargher, 2017). This is how

the organizational culture at Enron was based on the basic assumptions of the top executives and

the same framed the behaviour. Enron adopted a culture of cleverness after the deregulation of

the energy industry. This deregulation led the employees to think innovatively and also to carry

out different types of experimentation by exploring into new fields. In various interviews it was

also confirmed by the employees that the culture created by the then president led the employees

to break rules because of the increasing pressure on them.

On the other hand, the ethical theory of deontology is based on the assumption that

people are required to fulfil their duties and obligations towards others and therefore in case of

decision making, an individual should take into consideration their ethical obligation towards

others. Moreover according to the theory of deontology, people are required to fulfil their

responsibility and obligation towards others including the society in order to ethically correct.

This is so because individuals are required to uphold their duties towards others. That is

according to the theory; an individual is required to follow the law and also to keep their

promises. Further an individual who acts according to the ethical theory of deontology will are

decisions that are in consistence with their duties and responsibilities. Therefore according to the

deontology theory, Enron acted unethically because they did not fulfil their responsibilities

towards others- their shareholders, employees or the society in general. The company acted in a

way that resulted in increasing their benefits and that only looked after their own interest and

acted ethically because it was working for its own interest exclusively. Moreover the

organizational culture of Enron was based on Schein’s theory of organizational culture.

According to the same, the basic assumptions of individuals lay down the basis for values and it

is the values that lay down the basis for behaviour and practices within the organization and

therefore the same is reflected in the organizational culture (Lee & Fargher, 2017). This is how

the organizational culture at Enron was based on the basic assumptions of the top executives and

the same framed the behaviour. Enron adopted a culture of cleverness after the deregulation of

the energy industry. This deregulation led the employees to think innovatively and also to carry

out different types of experimentation by exploring into new fields. In various interviews it was

also confirmed by the employees that the culture created by the then president led the employees

to break rules because of the increasing pressure on them.

On the other hand, the ethical theory of deontology is based on the assumption that

people are required to fulfil their duties and obligations towards others and therefore in case of

decision making, an individual should take into consideration their ethical obligation towards

others. Moreover according to the theory of deontology, people are required to fulfil their

responsibility and obligation towards others including the society in order to ethically correct.

This is so because individuals are required to uphold their duties towards others. That is

according to the theory; an individual is required to follow the law and also to keep their

promises. Further an individual who acts according to the ethical theory of deontology will are

decisions that are in consistence with their duties and responsibilities. Therefore according to the

deontology theory, Enron acted unethically because they did not fulfil their responsibilities

towards others- their shareholders, employees or the society in general. The company acted in a

way that resulted in increasing their benefits and that only looked after their own interest and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ETHICAL DILEMMA OF ENRON

failed to take into consideration the interest of the society at large. The organization had a

responsibility to inform its shareholders about the actual financial position of the organization

and moreover it also had the responsibility to inform the society and also the employees about

everything however it failed to do the same. Therefore the company failed to fulfil its

responsibilities.

Part B: Application of the AAA model that should be used by accountants for the

purpose of obtaining an ethical decision making

The AMERICAN ACCOUNTING ASSOCIATION (AAA) mode of accounting

includes promotion of accounting practices, education and research. Moreover the AMERICAN

ACCOUNTING ASSOCIATION has the FINANCIAL REPORTING POLICY COMMITTEE

in its section of financial accounting and reporting. The Committee has the responsibility to

respond to exposure drafts of reporting issues and financial accounting. There are several

policies related to revenue recognition. Therefore the committee requires entities to report on

issues such as amount, revenue uncertainty and also the timing of the same and takes into

consideration the information related to cash flows to the ultimate customers. The main aim of

the exposure draft is to provide information that is represented faithfully, can be estimated and

measured and also includes proper disclosure of all information.

The AAA model of ethical decision making includes seven main stages comprising of-

discussion on the case facts, the ethical issues of the case, the norms and principles related to the

case, alternatives available, selection of the best course of action in compliance with the

principles, the consequences of each course of action and also the final decision. The AAA

model of decision making starts with description of the facts of the case such in case of Enron

the facts of the case includes- fraudulent practices being carried out by the company for showing

failed to take into consideration the interest of the society at large. The organization had a

responsibility to inform its shareholders about the actual financial position of the organization

and moreover it also had the responsibility to inform the society and also the employees about

everything however it failed to do the same. Therefore the company failed to fulfil its

responsibilities.

Part B: Application of the AAA model that should be used by accountants for the

purpose of obtaining an ethical decision making

The AMERICAN ACCOUNTING ASSOCIATION (AAA) mode of accounting

includes promotion of accounting practices, education and research. Moreover the AMERICAN

ACCOUNTING ASSOCIATION has the FINANCIAL REPORTING POLICY COMMITTEE

in its section of financial accounting and reporting. The Committee has the responsibility to

respond to exposure drafts of reporting issues and financial accounting. There are several

policies related to revenue recognition. Therefore the committee requires entities to report on

issues such as amount, revenue uncertainty and also the timing of the same and takes into

consideration the information related to cash flows to the ultimate customers. The main aim of

the exposure draft is to provide information that is represented faithfully, can be estimated and

measured and also includes proper disclosure of all information.

The AAA model of ethical decision making includes seven main stages comprising of-

discussion on the case facts, the ethical issues of the case, the norms and principles related to the

case, alternatives available, selection of the best course of action in compliance with the

principles, the consequences of each course of action and also the final decision. The AAA

model of decision making starts with description of the facts of the case such in case of Enron

the facts of the case includes- fraudulent practices being carried out by the company for showing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ETHICAL DILEMMA OF ENRON

a better financial position in front of the public and also all the other stakeholders. Moreover it

was able to do the same with the help of its auditors. Moreover some of the other important facts

includes- the inability of the auditors to comply with all the accounting principles and standards.

The second stage of the AAA model of ethical decision-making includes- identification of the

ethical issues of the company is being faced with. In case of Enron, the main ethical issue was

the conduct of fraudulent practices by the auditors of the company in order to show a financially

stable position of the company in front of the stakeholders and also for the purpose of taking

advantage of higher stock prices in the market and therefore becoming one of the most

successful companies of that era. Moreover another major ethical issue includes- the failure of

the Chief executive officer, the president along with other top executive to inform about the

actual information to the board of directors, the employees and also the audit committee.

Moreover they also forced the owners of the auditing company from ignoring all the fraudulent

accounting practices for the purpose of gaining undue advantage.

Therefore the company was unable to carry out its responsibilities towards the

stakeholders properly and therefore it carried out unethical activities according to the ethical

theory of deontology or Utilitarianism. According to the theory of deontology, individuals and

organizations have some responsibility and obligation towards the stakeholders. Moreover

according to the ethical theory of Utilitarianism organizations or individuals are required to act in

a way those results in greater good for all. The norms, values and principles that are related to

this case is that the company was required to conduct their activities with honesty, integrity,

fairness, trustworthiness and also by respecting others. Enron was unable to fulfil its

responsibility towards the society, they were not honest in their approach, the leaders were not

fair in their dealings, moreover the company also lost its trust after the scandal. The company

a better financial position in front of the public and also all the other stakeholders. Moreover it

was able to do the same with the help of its auditors. Moreover some of the other important facts

includes- the inability of the auditors to comply with all the accounting principles and standards.

The second stage of the AAA model of ethical decision-making includes- identification of the

ethical issues of the company is being faced with. In case of Enron, the main ethical issue was

the conduct of fraudulent practices by the auditors of the company in order to show a financially

stable position of the company in front of the stakeholders and also for the purpose of taking

advantage of higher stock prices in the market and therefore becoming one of the most

successful companies of that era. Moreover another major ethical issue includes- the failure of

the Chief executive officer, the president along with other top executive to inform about the

actual information to the board of directors, the employees and also the audit committee.

Moreover they also forced the owners of the auditing company from ignoring all the fraudulent

accounting practices for the purpose of gaining undue advantage.

Therefore the company was unable to carry out its responsibilities towards the

stakeholders properly and therefore it carried out unethical activities according to the ethical

theory of deontology or Utilitarianism. According to the theory of deontology, individuals and

organizations have some responsibility and obligation towards the stakeholders. Moreover

according to the ethical theory of Utilitarianism organizations or individuals are required to act in

a way those results in greater good for all. The norms, values and principles that are related to

this case is that the company was required to conduct their activities with honesty, integrity,

fairness, trustworthiness and also by respecting others. Enron was unable to fulfil its

responsibility towards the society, they were not honest in their approach, the leaders were not

fair in their dealings, moreover the company also lost its trust after the scandal. The company

8ETHICAL DILEMMA OF ENRON

was engaged in carrying out various fraudulent accounting practices, they were lacking financial

disclosures, the next step of the AAA ethical decision making model includes- identifying

alternative courses of action. In case of Enron also, the company requires to set a code of

conduct for their auditors which will provide the paper to the auditors for performing unbiased

auditing activities and this will ensure that the higher management of the company is not

influencing the activities of the auditors. On the other hand, leadership could be changed by

bringing a change leader who could have changed the ethical scenario being faced by the

company. He could have changed the entire organizational culture by reflecting integrity,

honesty in his activities that would help in changing the behaviour of the employees of the

company and ultimately would have helped in changing the entire scenario (Pergola & Walters,

2017). The final stage of the AAA model of ethical decision making includes- taking a decision.

The consequence of changing the leadership and the organizational leader includes- changing the

overall organizational culture that could have helped the company in conducting ethical

activities. And the consequence of changing the code of conduct to be followed includes-

conducting auditing activities independently without the influence of the leader. Therefore the

decisions that would have been selected by an accountant who supports ethical activities

includes- selection of a change leader who could have helped in changing the entire

organizational scenario by being able to change the organizational culture and climate.

Part C: Application of the Ferrell, Fraedrich and Ferrell model in the case of Enron

According to the Ferrell, Fraedrich and Ferrell model of ethical decision making, it is

necessary to understand the different ethical theories and standards that needs to be used by

business. However there are various other factors that also needs to be taken into consideration

as that can helps an individual in understanding how they make decisions and it can also help in

was engaged in carrying out various fraudulent accounting practices, they were lacking financial

disclosures, the next step of the AAA ethical decision making model includes- identifying

alternative courses of action. In case of Enron also, the company requires to set a code of

conduct for their auditors which will provide the paper to the auditors for performing unbiased

auditing activities and this will ensure that the higher management of the company is not

influencing the activities of the auditors. On the other hand, leadership could be changed by

bringing a change leader who could have changed the ethical scenario being faced by the

company. He could have changed the entire organizational culture by reflecting integrity,

honesty in his activities that would help in changing the behaviour of the employees of the

company and ultimately would have helped in changing the entire scenario (Pergola & Walters,

2017). The final stage of the AAA model of ethical decision making includes- taking a decision.

The consequence of changing the leadership and the organizational leader includes- changing the

overall organizational culture that could have helped the company in conducting ethical

activities. And the consequence of changing the code of conduct to be followed includes-

conducting auditing activities independently without the influence of the leader. Therefore the

decisions that would have been selected by an accountant who supports ethical activities

includes- selection of a change leader who could have helped in changing the entire

organizational scenario by being able to change the organizational culture and climate.

Part C: Application of the Ferrell, Fraedrich and Ferrell model in the case of Enron

According to the Ferrell, Fraedrich and Ferrell model of ethical decision making, it is

necessary to understand the different ethical theories and standards that needs to be used by

business. However there are various other factors that also needs to be taken into consideration

as that can helps an individual in understanding how they make decisions and it can also help in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ETHICAL DILEMMA OF ENRON

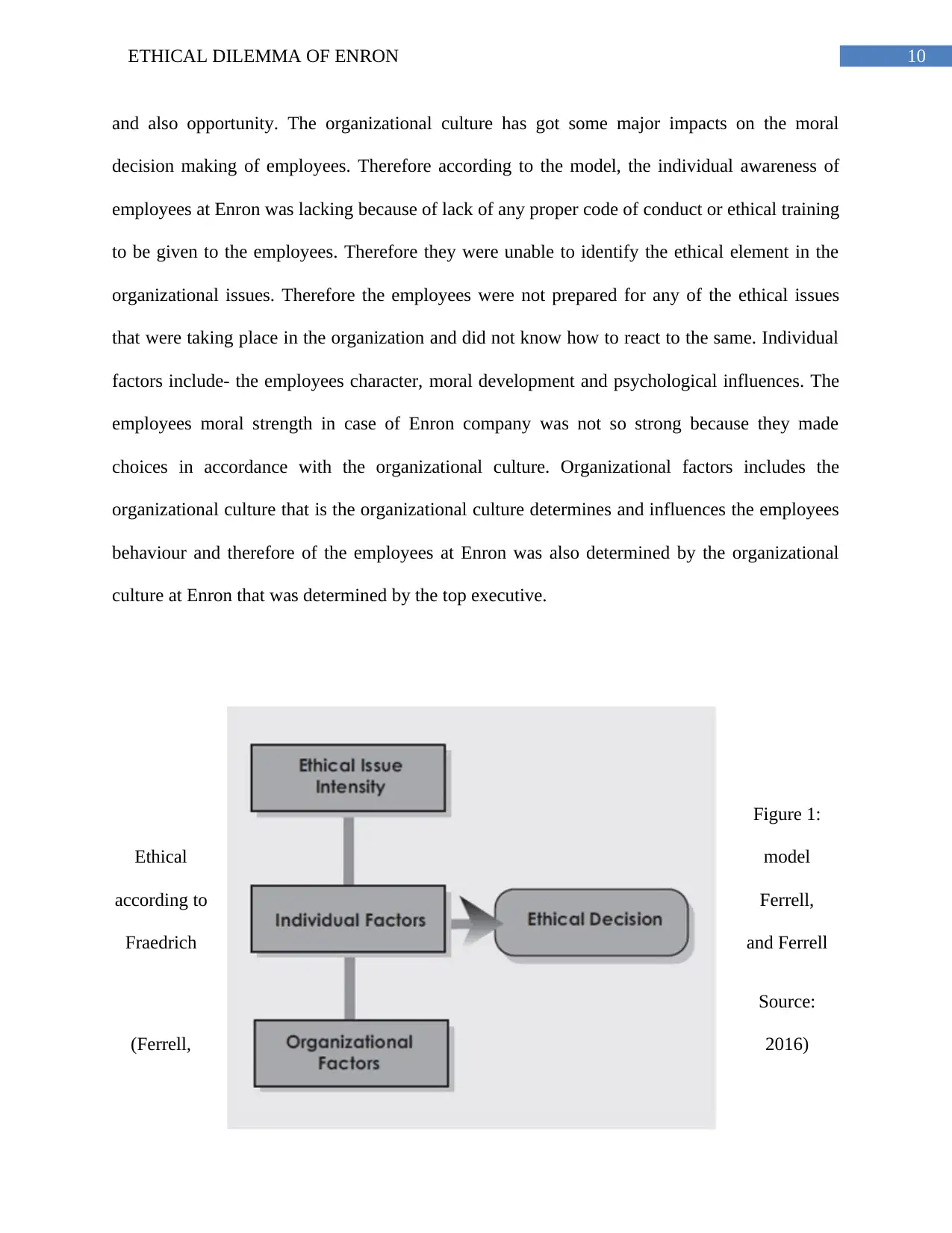

understanding the way the decision making of the other employees, the manager and other

stakeholders take place. The model aims at understanding all those factors that makes

professionals behave unethically (Barlev, Citron & Haddad, 2017). The model can be understood

by taking into consideration three main factors that is ethical issue intensity, individual factors

and also organizational factors. The ethical issue intensity includes- employee’s awareness about

the presence of ethical elements in certain issues. It includes consideration of the importance of

the issues for an organization and also takes into consideration the employees behave when such

issues arise. This awareness among the employees can be created through training in ethics,

actions and communication from top-down. Individual factors on the other hand include-

psychological influences, moral development and the character (Crossler et al., 2016). Character

includes the moral strength of the employees which is further dependent upon their pattern of

behaviour over a period of time. A person is said to be having strong character when he always

respects everyone’s rights. Ethical decision making in organization is dependent upon two major

psychological factors that is commitment and conformity.

Conformity refers to the desire of an individual to be seen as a part of the group and not

as someone different from the group. Commitment is also related to conformity. Commitment

refers to the ability of the employees to confirm closely to the organizational goals. And the

third main component of individual factors is moral development includes the level of

sophistication that is portrayed by an individual while determining if the action is morally right

(Wittmer, 2016). The organizational factors on the other hand includes- the way in which

organizations can influence the behaviour of the employees and thereby influencing the

employees to behave in a manner that is completely different from their own values (Haswell &

Evans, 2018). Therefore the organizational factors include- organizational culture, work groups

understanding the way the decision making of the other employees, the manager and other

stakeholders take place. The model aims at understanding all those factors that makes

professionals behave unethically (Barlev, Citron & Haddad, 2017). The model can be understood

by taking into consideration three main factors that is ethical issue intensity, individual factors

and also organizational factors. The ethical issue intensity includes- employee’s awareness about

the presence of ethical elements in certain issues. It includes consideration of the importance of

the issues for an organization and also takes into consideration the employees behave when such

issues arise. This awareness among the employees can be created through training in ethics,

actions and communication from top-down. Individual factors on the other hand include-

psychological influences, moral development and the character (Crossler et al., 2016). Character

includes the moral strength of the employees which is further dependent upon their pattern of

behaviour over a period of time. A person is said to be having strong character when he always

respects everyone’s rights. Ethical decision making in organization is dependent upon two major

psychological factors that is commitment and conformity.

Conformity refers to the desire of an individual to be seen as a part of the group and not

as someone different from the group. Commitment is also related to conformity. Commitment

refers to the ability of the employees to confirm closely to the organizational goals. And the

third main component of individual factors is moral development includes the level of

sophistication that is portrayed by an individual while determining if the action is morally right

(Wittmer, 2016). The organizational factors on the other hand includes- the way in which

organizations can influence the behaviour of the employees and thereby influencing the

employees to behave in a manner that is completely different from their own values (Haswell &

Evans, 2018). Therefore the organizational factors include- organizational culture, work groups

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ETHICAL DILEMMA OF ENRON

and also opportunity. The organizational culture has got some major impacts on the moral

decision making of employees. Therefore according to the model, the individual awareness of

employees at Enron was lacking because of lack of any proper code of conduct or ethical training

to be given to the employees. Therefore they were unable to identify the ethical element in the

organizational issues. Therefore the employees were not prepared for any of the ethical issues

that were taking place in the organization and did not know how to react to the same. Individual

factors include- the employees character, moral development and psychological influences. The

employees moral strength in case of Enron company was not so strong because they made

choices in accordance with the organizational culture. Organizational factors includes the

organizational culture that is the organizational culture determines and influences the employees

behaviour and therefore of the employees at Enron was also determined by the organizational

culture at Enron that was determined by the top executive.

Figure 1:

Ethical model

according to Ferrell,

Fraedrich and Ferrell

Source:

(Ferrell, 2016)

and also opportunity. The organizational culture has got some major impacts on the moral

decision making of employees. Therefore according to the model, the individual awareness of

employees at Enron was lacking because of lack of any proper code of conduct or ethical training

to be given to the employees. Therefore they were unable to identify the ethical element in the

organizational issues. Therefore the employees were not prepared for any of the ethical issues

that were taking place in the organization and did not know how to react to the same. Individual

factors include- the employees character, moral development and psychological influences. The

employees moral strength in case of Enron company was not so strong because they made

choices in accordance with the organizational culture. Organizational factors includes the

organizational culture that is the organizational culture determines and influences the employees

behaviour and therefore of the employees at Enron was also determined by the organizational

culture at Enron that was determined by the top executive.

Figure 1:

Ethical model

according to Ferrell,

Fraedrich and Ferrell

Source:

(Ferrell, 2016)

11ETHICAL DILEMMA OF ENRON

Therefore from the above diagram, the three main factors that needs to be considered

while taking an ethical decision can be understood such as- ethical issue intensity, individual

factors and organizational factors.

Conclusion

Therefore, from the above discussion, it can be concluded that organizations are required

to conduct their activities in an ethical manner for the purpose of fulfilling their responsibility

towards the different stakeholders. Moreover organizations that are engaged in carrying out

accounting activities are required to follow the different accounting guidelines. From the paper

the contrast between the different ethical theories of deontology and egoism has been understood

and the way the same has an application to the Enron case has been discussed. Moreover from

the paper, the way the AAA model should be made use by the accountant has also been

understood. The AAA model of accounting discusses about guidelines related to conducting

auditing activities. From the paper it has clearly been understood that when organizations fail to

comply with the accounting guidelines it results in unethical activities and behaviors on part of

the organization. Moreover from the paper it has been seen that the model of Ferrell, Fraedrich

and Ferrell can help organizations in taking ethical decision by taking into consideration the

different factors of ethical issue intensity, individual factors and also organizational factors.

Therefore from the above diagram, the three main factors that needs to be considered

while taking an ethical decision can be understood such as- ethical issue intensity, individual

factors and organizational factors.

Conclusion

Therefore, from the above discussion, it can be concluded that organizations are required

to conduct their activities in an ethical manner for the purpose of fulfilling their responsibility

towards the different stakeholders. Moreover organizations that are engaged in carrying out

accounting activities are required to follow the different accounting guidelines. From the paper

the contrast between the different ethical theories of deontology and egoism has been understood

and the way the same has an application to the Enron case has been discussed. Moreover from

the paper, the way the AAA model should be made use by the accountant has also been

understood. The AAA model of accounting discusses about guidelines related to conducting

auditing activities. From the paper it has clearly been understood that when organizations fail to

comply with the accounting guidelines it results in unethical activities and behaviors on part of

the organization. Moreover from the paper it has been seen that the model of Ferrell, Fraedrich

and Ferrell can help organizations in taking ethical decision by taking into consideration the

different factors of ethical issue intensity, individual factors and also organizational factors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.