HA 3011 Advanced Financial Accounting: A Case Study on Enron's Fall

VerifiedAdded on 2023/06/05

|12

|2952

|85

Case Study

AI Summary

This case study delves into the downfall of Enron, examining the accounting practices that led to its collapse. It focuses on the use of mark-to-market accounting, special purpose entities (SPEs), and stock options, highlighting how these mechanisms were manipulated to misrepresent the company's financial health. The report references an article by Paul M. Healy and Krishna G. Palepu, providing a detailed analysis of Enron's fraudulent activities and their impact on investors. Additionally, the study compares International Financial Reporting Standards (IFRS) with US Generally Accepted Accounting Principles (GAAP), using Wesfarmers Ltd and Mackay Golf Club as examples to illustrate the differences in financial statement presentation and valuation methods. The analysis concludes that while both IFRS and US GAAP have their strengths, IFRS offers simpler and more understandable methods for recognizing and measuring assets and liabilities.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

HA 3011 Advanced Financial Accounting Assessment item 2 —

Assignment

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

HA 3011 Advanced Financial Accounting Assessment item 2 —

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Fall of Enron

Executive Summary

The downfall of Enron can be defined as one of the greatest fall that wiped huge wealth of the

investors. The management of the company portrayed rosy pictures that led to the depiction

of wrong information and lead to duping of the innocent investors. The current report ss

based on the downfall of Enron that is studies in the light of the article provided by Paul M.

Healy and Krishna G. Palepu.

2

Executive Summary

The downfall of Enron can be defined as one of the greatest fall that wiped huge wealth of the

investors. The management of the company portrayed rosy pictures that led to the depiction

of wrong information and lead to duping of the innocent investors. The current report ss

based on the downfall of Enron that is studies in the light of the article provided by Paul M.

Healy and Krishna G. Palepu.

2

The Fall of Enron

Contents

Introduction...........................................................................................................................................4

a) Mark-to-market strategy...............................................................................................................4

b) SPE or special purpose entities......................................................................................................4

c) Stock options.................................................................................................................................5

Conclusion.............................................................................................................................................7

Part B.....................................................................................................................................................8

References...........................................................................................................................................12

3

Contents

Introduction...........................................................................................................................................4

a) Mark-to-market strategy...............................................................................................................4

b) SPE or special purpose entities......................................................................................................4

c) Stock options.................................................................................................................................5

Conclusion.............................................................................................................................................7

Part B.....................................................................................................................................................8

References...........................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Fall of Enron

Introduction

From the article of Paul M. Healy and Krishna G. Palepu, it is notable that Enron undertook

massive risks while presenting its financial statements that resulted in its downfall. The

accounting standards were used by the Enron in a wrong manner that led to the reflection of

wrong details. The mark-to-market mechanism was used to fool the public followed by the

wrong usage of SPE and then using the stock options in a complex manner.

a) Mark-to-market strategy

In relation to fair value accounting, mark-to-market strategy is more likely to be

regarded as such fair value accounting of liabilities and assets that relies on the market

prices. Further, in such accounting measure, the present market prices are accounted

for as the primary base of every transaction and the same is also prone to immense

fluctuations owing to the volatility in market. Nonetheless, this strategy is utilized by

the organization in association with the long-term contracts in association with mark-

to-market accounting. In addition to this, the expenses and income for long-term

contracts are also accounted for by depending on the present value of the future flow

of cash (Healy & Palepu, 2003). Therefore, when the prices are more volatile in the

market in the sense that they decrease or increase, the same cannot be properly

adjusted or aligned in the company’s books. Overall, the flaws in company’s profits

were huge in the sense that resulted in the downfall of Enron and its misguiding

financial statements. In addition, Enron also ascertained its revenues as the fair values

of all inflows of cash in the upcoming tenures and the booked expenses on a whole.

The losses and gains were also unrealized in the upcoming years when that happened.

Nonetheless, the company was involved in various long-term business contracts that

reflected the present value of all future flows of cash as the income and present value

of expenses to be incurred during the overall contract as the service cost.

Nevertheless, there were various contracts that also failed to pass the viability test in

the upcoming year of the contract that permitted Enron to depict a false picture of its

financial performance (Hoffelder, 2012).

b) SPE or special purpose entities

4

Introduction

From the article of Paul M. Healy and Krishna G. Palepu, it is notable that Enron undertook

massive risks while presenting its financial statements that resulted in its downfall. The

accounting standards were used by the Enron in a wrong manner that led to the reflection of

wrong details. The mark-to-market mechanism was used to fool the public followed by the

wrong usage of SPE and then using the stock options in a complex manner.

a) Mark-to-market strategy

In relation to fair value accounting, mark-to-market strategy is more likely to be

regarded as such fair value accounting of liabilities and assets that relies on the market

prices. Further, in such accounting measure, the present market prices are accounted

for as the primary base of every transaction and the same is also prone to immense

fluctuations owing to the volatility in market. Nonetheless, this strategy is utilized by

the organization in association with the long-term contracts in association with mark-

to-market accounting. In addition to this, the expenses and income for long-term

contracts are also accounted for by depending on the present value of the future flow

of cash (Healy & Palepu, 2003). Therefore, when the prices are more volatile in the

market in the sense that they decrease or increase, the same cannot be properly

adjusted or aligned in the company’s books. Overall, the flaws in company’s profits

were huge in the sense that resulted in the downfall of Enron and its misguiding

financial statements. In addition, Enron also ascertained its revenues as the fair values

of all inflows of cash in the upcoming tenures and the booked expenses on a whole.

The losses and gains were also unrealized in the upcoming years when that happened.

Nonetheless, the company was involved in various long-term business contracts that

reflected the present value of all future flows of cash as the income and present value

of expenses to be incurred during the overall contract as the service cost.

Nevertheless, there were various contracts that also failed to pass the viability test in

the upcoming year of the contract that permitted Enron to depict a false picture of its

financial performance (Hoffelder, 2012).

b) SPE or special purpose entities

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Fall of Enron

SPE or special purpose entities are defined as that shell firms that can be framed by

the sponsor but its funding is facilitated through independent equity investors.

Besides, this can also happen through debt financing. Further, such entities are used

for various motives like sharing of risk, transfer of assets, financing, loan

securitization, etc (Gay & Simnet, 2005). In relation to the company, it has framed

various SPE’s to facilitate financing of forward contracts so that financial reporting

goals can be addressed. The company endeavoured to buy the partner share in a joint

venture agreement but it had no motive to disclose the amount of debts from the

acquisition transaction or from the agreement in the financial statement (Berensen,

Richard & Oppel, 2001). Moreover, the controlling strength of such special purpose

entity was controlled or procured by the company’s executive (Chewco) who had

raised a guarantee of debt. Further, the firm had used such acquired debts for the

motive of procuring the relationship of joint venture agreement. Nevertheless, the

structure was made in such a manner that nothing associated to the debt transaction

was being portrayed in the financial statements of the company, thereby making it

easier for it to procure the partnership in relation to the joint venture agreement.

Besides, the special purpose entity on the part of Chewco also resulted in the violation

of several standards of accounting and hence, the company made attempts to prohibit

itself from consolidating its accounts with that of Chewco. This resulted in the

overstatement of equity and earnings and understatement of liabilities and debts.

c) Stock options

The company’s top most authority was provided additional rewards in the form of

compensation that also comprised of stock options. They were obtained the same

because it could facilitate in attracting both shareholders and management. Further,

employees were also provided the same because a variation in decision-making can be

attained so that a false picture of the company’s performance can be reflected. Such

stock options were offered without any limitations on further resale that was a major

issue (Healy & Palepu, 2003). Besides, the management was in no requirement for

such stock options and therefore, it sheds light on such fraudulent activity undertaken

on behalf of the company. Agency theory can be reflected through such activity

undertaken by Enron because it also attempted to maximize its wealth for maximizing

self-interest objectives. Thus, to address the assumption of such issue, the agent is

5

SPE or special purpose entities are defined as that shell firms that can be framed by

the sponsor but its funding is facilitated through independent equity investors.

Besides, this can also happen through debt financing. Further, such entities are used

for various motives like sharing of risk, transfer of assets, financing, loan

securitization, etc (Gay & Simnet, 2005). In relation to the company, it has framed

various SPE’s to facilitate financing of forward contracts so that financial reporting

goals can be addressed. The company endeavoured to buy the partner share in a joint

venture agreement but it had no motive to disclose the amount of debts from the

acquisition transaction or from the agreement in the financial statement (Berensen,

Richard & Oppel, 2001). Moreover, the controlling strength of such special purpose

entity was controlled or procured by the company’s executive (Chewco) who had

raised a guarantee of debt. Further, the firm had used such acquired debts for the

motive of procuring the relationship of joint venture agreement. Nevertheless, the

structure was made in such a manner that nothing associated to the debt transaction

was being portrayed in the financial statements of the company, thereby making it

easier for it to procure the partnership in relation to the joint venture agreement.

Besides, the special purpose entity on the part of Chewco also resulted in the violation

of several standards of accounting and hence, the company made attempts to prohibit

itself from consolidating its accounts with that of Chewco. This resulted in the

overstatement of equity and earnings and understatement of liabilities and debts.

c) Stock options

The company’s top most authority was provided additional rewards in the form of

compensation that also comprised of stock options. They were obtained the same

because it could facilitate in attracting both shareholders and management. Further,

employees were also provided the same because a variation in decision-making can be

attained so that a false picture of the company’s performance can be reflected. Such

stock options were offered without any limitations on further resale that was a major

issue (Healy & Palepu, 2003). Besides, the management was in no requirement for

such stock options and therefore, it sheds light on such fraudulent activity undertaken

on behalf of the company. Agency theory can be reflected through such activity

undertaken by Enron because it also attempted to maximize its wealth for maximizing

self-interest objectives. Thus, to address the assumption of such issue, the agent is

5

The Fall of Enron

bound to operate from one side. In other words, he can either work in alignment with

the principles to enhance the wealth or can compromise the work for self-interest

motives (Anthony, Shelley & Catanach, 2003). Similarly, the top most authorities

were also offered compensation like the agents and that included stock options as

well.

6

bound to operate from one side. In other words, he can either work in alignment with

the principles to enhance the wealth or can compromise the work for self-interest

motives (Anthony, Shelley & Catanach, 2003). Similarly, the top most authorities

were also offered compensation like the agents and that included stock options as

well.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Fall of Enron

Conclusion

It was the requirement to increase public wealth but Enron only inflated its development or

performance in a false way and public wealth was not at all affected. In relation to the

company, it has framed various SPE’s to facilitate financing of forward contracts so that

financial reporting goals can be addressed. Therefore, the study clearly emphasizes that

Enron used different mechanism to depict a false picture to the public.

7

Conclusion

It was the requirement to increase public wealth but Enron only inflated its development or

performance in a false way and public wealth was not at all affected. In relation to the

company, it has framed various SPE’s to facilitate financing of forward contracts so that

financial reporting goals can be addressed. Therefore, the study clearly emphasizes that

Enron used different mechanism to depict a false picture to the public.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Fall of Enron

Part B

Based on the framework of International Financial Reporting Standards, it must be

noted that there are five elements of conceptual framework for financial reporting

namely assets, liabilities, equity, expenses, and income. Furthermore, based on

measurement of these elements, different companies implement different methods of

measurement like fair value accounting, current cost accounting basis, historical

method, etc.

1. The elements of financial statements can be determined through various measures.

The most perfect example in relation to such can be visible in the case of

Wesfarmers Ltd that is listed on the Australian Stock Exchange. In relation to the

annual report of the company, the computation of revenues has been conducted at

the received consideration or consideration that is receivable. Further, the

computation of inventories is being undertaken based on net realizable value or

cost whichever is lower, and such cost is ascertained as per the requirements of

weighted average method (Kaplan, 2011). It can also be seen from the annual

report of the company that its trade and other receivables are being valued at fair

value and thereafter, determined at amortized cost by using the strategy of

effective interest and in alignment to this, a deduction is being facilitated for the

allowance part. Moreover, in association with the fixed assets of the company like

Property, Plant, and Equipment, such measurement has been undertaken at cost

minus the depreciation. Moreover, the amount of depreciation has been computed

based on the requirements of straight-line basis over the useful life of the asset for

the rest of its life (Geoffrey, Joleen, Kelli & Davied, 2016). Nonetheless, the

borrowings of the company are being valued at their fair values with lower

transactions and are amortized afterwards. Overall, the distinction betwixt these

two is clearly visible in the financial statements of the company.

Income statement

For the motive of comparison, a company from United States is being taken into evaluation

that has adopted and implemented US GAAP standard into its framework for financial

reporting. In relation to this, Mackay Golf Club has been opted for a better understanding and

8

Part B

Based on the framework of International Financial Reporting Standards, it must be

noted that there are five elements of conceptual framework for financial reporting

namely assets, liabilities, equity, expenses, and income. Furthermore, based on

measurement of these elements, different companies implement different methods of

measurement like fair value accounting, current cost accounting basis, historical

method, etc.

1. The elements of financial statements can be determined through various measures.

The most perfect example in relation to such can be visible in the case of

Wesfarmers Ltd that is listed on the Australian Stock Exchange. In relation to the

annual report of the company, the computation of revenues has been conducted at

the received consideration or consideration that is receivable. Further, the

computation of inventories is being undertaken based on net realizable value or

cost whichever is lower, and such cost is ascertained as per the requirements of

weighted average method (Kaplan, 2011). It can also be seen from the annual

report of the company that its trade and other receivables are being valued at fair

value and thereafter, determined at amortized cost by using the strategy of

effective interest and in alignment to this, a deduction is being facilitated for the

allowance part. Moreover, in association with the fixed assets of the company like

Property, Plant, and Equipment, such measurement has been undertaken at cost

minus the depreciation. Moreover, the amount of depreciation has been computed

based on the requirements of straight-line basis over the useful life of the asset for

the rest of its life (Geoffrey, Joleen, Kelli & Davied, 2016). Nonetheless, the

borrowings of the company are being valued at their fair values with lower

transactions and are amortized afterwards. Overall, the distinction betwixt these

two is clearly visible in the financial statements of the company.

Income statement

For the motive of comparison, a company from United States is being taken into evaluation

that has adopted and implemented US GAAP standard into its framework for financial

reporting. In relation to this, Mackay Golf Club has been opted for a better understanding and

8

The Fall of Enron

difference betwixt the requirements of IFRS and US GAAP. Based on this company, the

revenue recognition is being undertaken based on the percentage of completion method and

such strategy is being calculated based on the input method. This method is also undertaken

for the recognition of expenses of the company. In addition, the inventories measurement is

being done or undertaken at their respective market prices or cost and the ones with the

lowest is also evaluated. Further, ascertainment of cost is facilitated through two ways

namely FIFO for determining raw materials and finished goods or work in progress for

determining manufacturing costs. In addition, the trade and other receivables of the company

is measured on the basis of their current values that have been estimated (Matthew, 2015).

Further, the company’s fixed assets like property, plant, and equipment are measured through

the system of straight-line basis over the useful life of an asset. Nevertheless, the company’s

annual report depicts crucial details in various segments.

2. In association with the previously mentioned companies, it can be seen that there

are two distinct measures for the presentation of financial statements of

companies. It cannot be stated with primary efficiency that which method is more

advantageous than the other. Further, it can be stated that the measurement

recognition of one strategy is primarily superior or beneficial than the other

method (Pilbeam, 2009). Besides, there is one segment wherein the second matter

is more beneficial than the first method. Hence, for such purpose, different

examples are being taken into evaluation that plays a key role in portraying the

various recognition methods used by companies. Further, if the revenue

measurement is being undertaken by accounting for the International Financial

Reporting Standards, they it may become simpler or effective to ascertain the

statement of income when compared to the US GAAP measure. The reason

behind this can be attributed to the fact that IFRS has been playing a relevant role

in using the most usual method of recognition of revenues. Nevertheless, going

through the US GAAP principle, it can also be observed that the classification or

segregation of costs are done based on function and in the case of IFRS, the same

is done through two ways that is function and nature of such expenses. This makes

it simpler and easier for users to understand the financial information if the same

has been reported through implementation of IFRS standards. Nonetheless, when

it comes to reflection of financial information in the annual report of companies

under the US GAAP principle, there are various strict needs that must be given

9

difference betwixt the requirements of IFRS and US GAAP. Based on this company, the

revenue recognition is being undertaken based on the percentage of completion method and

such strategy is being calculated based on the input method. This method is also undertaken

for the recognition of expenses of the company. In addition, the inventories measurement is

being done or undertaken at their respective market prices or cost and the ones with the

lowest is also evaluated. Further, ascertainment of cost is facilitated through two ways

namely FIFO for determining raw materials and finished goods or work in progress for

determining manufacturing costs. In addition, the trade and other receivables of the company

is measured on the basis of their current values that have been estimated (Matthew, 2015).

Further, the company’s fixed assets like property, plant, and equipment are measured through

the system of straight-line basis over the useful life of an asset. Nevertheless, the company’s

annual report depicts crucial details in various segments.

2. In association with the previously mentioned companies, it can be seen that there

are two distinct measures for the presentation of financial statements of

companies. It cannot be stated with primary efficiency that which method is more

advantageous than the other. Further, it can be stated that the measurement

recognition of one strategy is primarily superior or beneficial than the other

method (Pilbeam, 2009). Besides, there is one segment wherein the second matter

is more beneficial than the first method. Hence, for such purpose, different

examples are being taken into evaluation that plays a key role in portraying the

various recognition methods used by companies. Further, if the revenue

measurement is being undertaken by accounting for the International Financial

Reporting Standards, they it may become simpler or effective to ascertain the

statement of income when compared to the US GAAP measure. The reason

behind this can be attributed to the fact that IFRS has been playing a relevant role

in using the most usual method of recognition of revenues. Nevertheless, going

through the US GAAP principle, it can also be observed that the classification or

segregation of costs are done based on function and in the case of IFRS, the same

is done through two ways that is function and nature of such expenses. This makes

it simpler and easier for users to understand the financial information if the same

has been reported through implementation of IFRS standards. Nonetheless, when

it comes to reflection of financial information in the annual report of companies

under the US GAAP principle, there are various strict needs that must be given

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Fall of Enron

due consideration and that makes it inferior to the IFRS standard (Ross et. al,

2014). Overall, through the provision of remaining illustrations, the recognition

and measurement of assets and liabilities under the system of IFRS are simpler

and more understandable in nature in comparison to the US GAAP principle.

Besides, this can play a key role on the part of users in their decision-making

process.

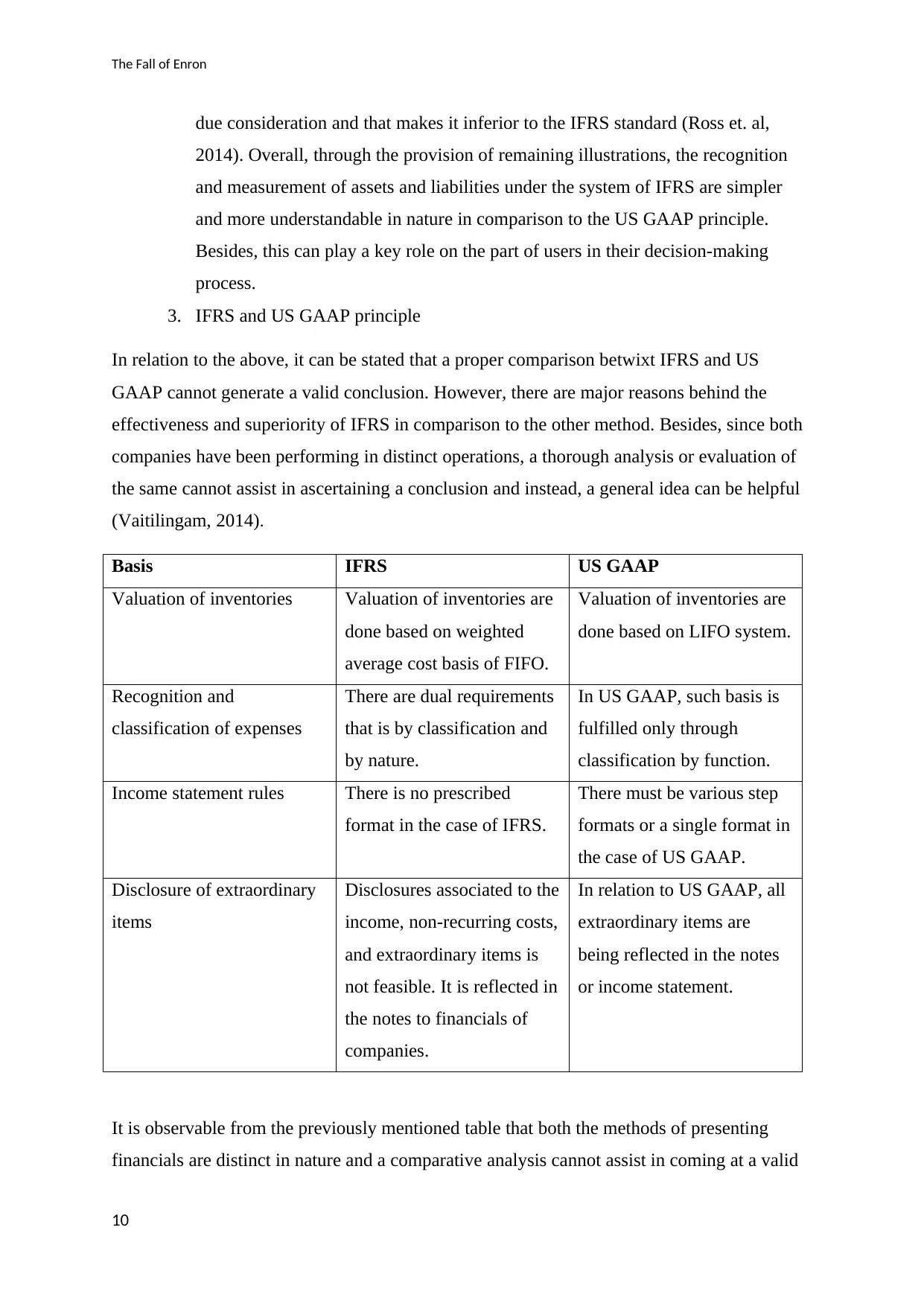

3. IFRS and US GAAP principle

In relation to the above, it can be stated that a proper comparison betwixt IFRS and US

GAAP cannot generate a valid conclusion. However, there are major reasons behind the

effectiveness and superiority of IFRS in comparison to the other method. Besides, since both

companies have been performing in distinct operations, a thorough analysis or evaluation of

the same cannot assist in ascertaining a conclusion and instead, a general idea can be helpful

(Vaitilingam, 2014).

Basis IFRS US GAAP

Valuation of inventories Valuation of inventories are

done based on weighted

average cost basis of FIFO.

Valuation of inventories are

done based on LIFO system.

Recognition and

classification of expenses

There are dual requirements

that is by classification and

by nature.

In US GAAP, such basis is

fulfilled only through

classification by function.

Income statement rules There is no prescribed

format in the case of IFRS.

There must be various step

formats or a single format in

the case of US GAAP.

Disclosure of extraordinary

items

Disclosures associated to the

income, non-recurring costs,

and extraordinary items is

not feasible. It is reflected in

the notes to financials of

companies.

In relation to US GAAP, all

extraordinary items are

being reflected in the notes

or income statement.

It is observable from the previously mentioned table that both the methods of presenting

financials are distinct in nature and a comparative analysis cannot assist in coming at a valid

10

due consideration and that makes it inferior to the IFRS standard (Ross et. al,

2014). Overall, through the provision of remaining illustrations, the recognition

and measurement of assets and liabilities under the system of IFRS are simpler

and more understandable in nature in comparison to the US GAAP principle.

Besides, this can play a key role on the part of users in their decision-making

process.

3. IFRS and US GAAP principle

In relation to the above, it can be stated that a proper comparison betwixt IFRS and US

GAAP cannot generate a valid conclusion. However, there are major reasons behind the

effectiveness and superiority of IFRS in comparison to the other method. Besides, since both

companies have been performing in distinct operations, a thorough analysis or evaluation of

the same cannot assist in ascertaining a conclusion and instead, a general idea can be helpful

(Vaitilingam, 2014).

Basis IFRS US GAAP

Valuation of inventories Valuation of inventories are

done based on weighted

average cost basis of FIFO.

Valuation of inventories are

done based on LIFO system.

Recognition and

classification of expenses

There are dual requirements

that is by classification and

by nature.

In US GAAP, such basis is

fulfilled only through

classification by function.

Income statement rules There is no prescribed

format in the case of IFRS.

There must be various step

formats or a single format in

the case of US GAAP.

Disclosure of extraordinary

items

Disclosures associated to the

income, non-recurring costs,

and extraordinary items is

not feasible. It is reflected in

the notes to financials of

companies.

In relation to US GAAP, all

extraordinary items are

being reflected in the notes

or income statement.

It is observable from the previously mentioned table that both the methods of presenting

financials are distinct in nature and a comparative analysis cannot assist in coming at a valid

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Fall of Enron

conclusion. However, it is clearly observable that IFRS requirements are not so stern in

nature in comparison to the US GAAP principles. This makes it easier for users to understand

the IFRS presented financial information in a better way. In addition, the measurement or

valuation of financial statements can be easily conducted in the prevalence of minimal

requirements like in the case of IFRS. Therefore, it can be stated that IFRS is a better

measure when talked about the utilization of US GAAP principle. Moreover, since

understanding and evaluation of information is easier in the IFRS requirements, users can

take maximum benefits out of the same for making decisions based on their interconnections

with the company. This is the major reason why IFRS standard is primarily superior to the

US GAAP method and users or companies can attain maximum efficacies from the usage of

such method for presentation and preparation of their financial data (Vaitilingam, 2014).

11

conclusion. However, it is clearly observable that IFRS requirements are not so stern in

nature in comparison to the US GAAP principles. This makes it easier for users to understand

the IFRS presented financial information in a better way. In addition, the measurement or

valuation of financial statements can be easily conducted in the prevalence of minimal

requirements like in the case of IFRS. Therefore, it can be stated that IFRS is a better

measure when talked about the utilization of US GAAP principle. Moreover, since

understanding and evaluation of information is easier in the IFRS requirements, users can

take maximum benefits out of the same for making decisions based on their interconnections

with the company. This is the major reason why IFRS standard is primarily superior to the

US GAAP method and users or companies can attain maximum efficacies from the usage of

such method for presentation and preparation of their financial data (Vaitilingam, 2014).

11

The Fall of Enron

References

Anthony H., Shelley, C,J., & Catanach, R. (2003). Enron: A Financial Reporting Failure.

Available from: https://digitalcommons.law.villanova.edu/cgi/viewcontent.cgi?

article=1339&context=vlr [Accessed 26 September 2018]

Berensen, A.,Richard, A., and Oppel, JR. (2001) Once-Mighty Enron Strains Under Scrutiny.

Available from https://www.nytimes.com/2001/10/28/business/once-mighty-enron-strains-

under-scrutiny.html [Accessed 26 September 2018]

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K, Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online] 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309

[Accessed 26 September 2018]

Healy, P.M & Palepu, K.G. (2003) The Fall of Enron. Journal of Economic Perspectives.

17(2), 3-26. Available from: https://www.aeaweb.org/articles?

id=10.1257/089533003765888403

Hoffelder, K. (2012) New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011) Accounting scholarship that advances professional knowledge and

practice. The Accounting Review [online]. 86(2), pp. 367–383. Available from

https://doi.org/10.2308/accr.00000031 [Accessed 26 September 2018]

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 26 September 2018]

Pilbeam, K. (2009) Finance and Financial Markets. Palgrave Macmillan

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. an Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall

12

References

Anthony H., Shelley, C,J., & Catanach, R. (2003). Enron: A Financial Reporting Failure.

Available from: https://digitalcommons.law.villanova.edu/cgi/viewcontent.cgi?

article=1339&context=vlr [Accessed 26 September 2018]

Berensen, A.,Richard, A., and Oppel, JR. (2001) Once-Mighty Enron Strains Under Scrutiny.

Available from https://www.nytimes.com/2001/10/28/business/once-mighty-enron-strains-

under-scrutiny.html [Accessed 26 September 2018]

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K, Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. [online] 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309

[Accessed 26 September 2018]

Healy, P.M & Palepu, K.G. (2003) The Fall of Enron. Journal of Economic Perspectives.

17(2), 3-26. Available from: https://www.aeaweb.org/articles?

id=10.1257/089533003765888403

Hoffelder, K. (2012) New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011) Accounting scholarship that advances professional knowledge and

practice. The Accounting Review [online]. 86(2), pp. 367–383. Available from

https://doi.org/10.2308/accr.00000031 [Accessed 26 September 2018]

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 26 September 2018]

Pilbeam, K. (2009) Finance and Financial Markets. Palgrave Macmillan

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. an Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.