ENT6A5 Entrepreneurship Finance: Venture Capital Valuation of Firms

VerifiedAdded on 2023/06/08

|10

|2260

|403

Report

AI Summary

This report provides a critical analysis of two major valuation models used in venture capital: comparable analysis and discounted cash flow (DCF). It explains their assumptions and applications, particularly in the context of the Oxford Instruments Venture case study. The report defines key terms like 'explicit forecast period' and 'terminal or horizon value,' illustrating them with graphs. Furthermore, it applies the venture capital method to determine the value of Oxford Instruments at the end of three years, including calculations to determine the present value and the percentage of ownership required to be relinquished for investment. The analysis includes cash flow, fair price, and market price methods, demonstrating the inverse relationship between the rate of return and the overall value of the venture.

ENT6A5

ENTRE-

PRENEURSHIP

FINANCE AND

VENTURE CAPITAL

ENTRE-

PRENEURSHIP

FINANCE AND

VENTURE CAPITAL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

Explanation the two valuation models in venture capital,their assumptions and applications...3

Define the terms..........................................................................................................................4

Application of the Venture Capital Methods..............................................................................6

Present Value of Oxford Instruments Venture when firm wants 30 % compound annual rate of

return...........................................................................................................................................8

Determination of % of ownership it have to loose in order to venture capitalist firm................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

Explanation the two valuation models in venture capital,their assumptions and applications...3

Define the terms..........................................................................................................................4

Application of the Venture Capital Methods..............................................................................6

Present Value of Oxford Instruments Venture when firm wants 30 % compound annual rate of

return...........................................................................................................................................8

Determination of % of ownership it have to loose in order to venture capitalist firm................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Venture capital is a important mode of obtaining financing for new established businesses

to satisfy their capital requirement. It is all about finance provided by the venture capitalists who

not only provided funds to the companies but also manage them in order to develop into

economic benefits (Bakos and et.al, 2019). This report presents critical analysis of two major

valuation models in venture capital along-with their assumptions and applications to the case

study of “Oxford Instruments Venture”. Two significant terms: Explicit forecast period and

Terminal or horizon value are thoroughly explained with the graph. Further, report includes

application of VC method to determine the value of Oxford Instruments at the end of 3 years.

Some important calculations are also done in order to determine present value of Oxford

Instruments Venture and % of ownership it required to give up for its investment.

TASK

Explanation the two valuation models in venture capital,their assumptions and applications

When a company valuing as a going concern there are three methods which is used by

industry. They are as follow-

DCF analysis

Comparable company analysis

Precedent transactions

These models are used in investment banking, equity research, private equity, corporate

development and merger and acquisitions. In this case study a venture capitalist firm wants to

invest in Oxford Instruments venture and comparable its value with Imperial research group so

that venture is used market approach. In this approach Comparable analysis and discounted cash

flow models are included (Bollaert and et.al, 2021).

1. Comparable Analysis- It is also called public market multiples and trading multiples.

Under this method the investors are able to compare the current value of a business to

other similar business. This information helps to determine the company value and

calculate ratios. This method is based on some assumptions they are as follow:

Growth rate always stable.

The company uses some ratio such as price earning ratio, enterprise value to sales, price

to book and price to sales.

Venture capital is a important mode of obtaining financing for new established businesses

to satisfy their capital requirement. It is all about finance provided by the venture capitalists who

not only provided funds to the companies but also manage them in order to develop into

economic benefits (Bakos and et.al, 2019). This report presents critical analysis of two major

valuation models in venture capital along-with their assumptions and applications to the case

study of “Oxford Instruments Venture”. Two significant terms: Explicit forecast period and

Terminal or horizon value are thoroughly explained with the graph. Further, report includes

application of VC method to determine the value of Oxford Instruments at the end of 3 years.

Some important calculations are also done in order to determine present value of Oxford

Instruments Venture and % of ownership it required to give up for its investment.

TASK

Explanation the two valuation models in venture capital,their assumptions and applications

When a company valuing as a going concern there are three methods which is used by

industry. They are as follow-

DCF analysis

Comparable company analysis

Precedent transactions

These models are used in investment banking, equity research, private equity, corporate

development and merger and acquisitions. In this case study a venture capitalist firm wants to

invest in Oxford Instruments venture and comparable its value with Imperial research group so

that venture is used market approach. In this approach Comparable analysis and discounted cash

flow models are included (Bollaert and et.al, 2021).

1. Comparable Analysis- It is also called public market multiples and trading multiples.

Under this method the investors are able to compare the current value of a business to

other similar business. This information helps to determine the company value and

calculate ratios. This method is based on some assumptions they are as follow:

Growth rate always stable.

The company uses some ratio such as price earning ratio, enterprise value to sales, price

to book and price to sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Earning value of the share is assume as of comparable firm.

Application- In this case the venture wants to invest in Oxford Instruments venture and compare

value of its company with Imperial research group, they use price earning ratio to determining

the value of its company and earning value and price of share are taken of Imperial research

group.

2. Discounted cash flow- It is another model to determine the value of its company. It is an

intrinsic value approach where the value of an investment based on its expected future cash flow.

This model is used by investors to take decision for acquiring a company or buying a stock

(Gompers, P.A., 2022). There are some assumptions when using discounted cash flow method

they are as:

Discount rate is used as comparable firm.

The time value of money assumes that a dollar today is worth more than in future.

This method is used only when a person paying money in present with expectations of

receiving more money in the future.

Application- In this case the venture invest the money in Oxford Instruments venture with

expectation of receiving profit in upcoming years. Discount rate is assume as Imperial Research

Group.

Define the terms

Explicit forecast period- It is a period of projecting cash flows when the company is

valued by discounted cash flow model. There is no fixed duration of the forecast period,

choosing a forecast period of 10 years. The value of the company can be determined by two

methods (Langley and et.al, 2020).

1. In the first method is to assume that the firm will be liquidated in the horizon year and

estimate the value of its assets in that year.

2. In second method is to assume that the firm will continue to grow up to infinity after the

horizon year that is used constant growth formula.

Application- In this case the venture wants to invest in Oxford Instruments venture and compare

value of its company with Imperial research group, they use price earning ratio to determining

the value of its company and earning value and price of share are taken of Imperial research

group.

2. Discounted cash flow- It is another model to determine the value of its company. It is an

intrinsic value approach where the value of an investment based on its expected future cash flow.

This model is used by investors to take decision for acquiring a company or buying a stock

(Gompers, P.A., 2022). There are some assumptions when using discounted cash flow method

they are as:

Discount rate is used as comparable firm.

The time value of money assumes that a dollar today is worth more than in future.

This method is used only when a person paying money in present with expectations of

receiving more money in the future.

Application- In this case the venture invest the money in Oxford Instruments venture with

expectation of receiving profit in upcoming years. Discount rate is assume as Imperial Research

Group.

Define the terms

Explicit forecast period- It is a period of projecting cash flows when the company is

valued by discounted cash flow model. There is no fixed duration of the forecast period,

choosing a forecast period of 10 years. The value of the company can be determined by two

methods (Langley and et.al, 2020).

1. In the first method is to assume that the firm will be liquidated in the horizon year and

estimate the value of its assets in that year.

2. In second method is to assume that the firm will continue to grow up to infinity after the

horizon year that is used constant growth formula.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the above graph shows that the company will continue till 10 years and the income

generates 1 to 3 years nil and in the fourth year Oxford instruments arise income 13.182 million

up to ten ten years.

Terminal or horizon value- It is also called continuing value because it is the value of

security at some future date beyond which more precise cash flow projection is not possible.

The terminal value calculation estimates the value of the company after the forecast period. It is

calculated the difference between discount rate and terminal growth rate is divided by the last

cash flow forecast (Maroufkhani and et.al, 2018). There are two components-

1. Forecast period- In this method the time period is to assume 3 to 5 years for a normal

business.

2. Terminal value- This method assumes the business will continue to generate free cash

flow at perpetuity.

Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

0

2

4

6

8

10

12

14

Column 1

generates 1 to 3 years nil and in the fourth year Oxford instruments arise income 13.182 million

up to ten ten years.

Terminal or horizon value- It is also called continuing value because it is the value of

security at some future date beyond which more precise cash flow projection is not possible.

The terminal value calculation estimates the value of the company after the forecast period. It is

calculated the difference between discount rate and terminal growth rate is divided by the last

cash flow forecast (Maroufkhani and et.al, 2018). There are two components-

1. Forecast period- In this method the time period is to assume 3 to 5 years for a normal

business.

2. Terminal value- This method assumes the business will continue to generate free cash

flow at perpetuity.

Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

0

2

4

6

8

10

12

14

Column 1

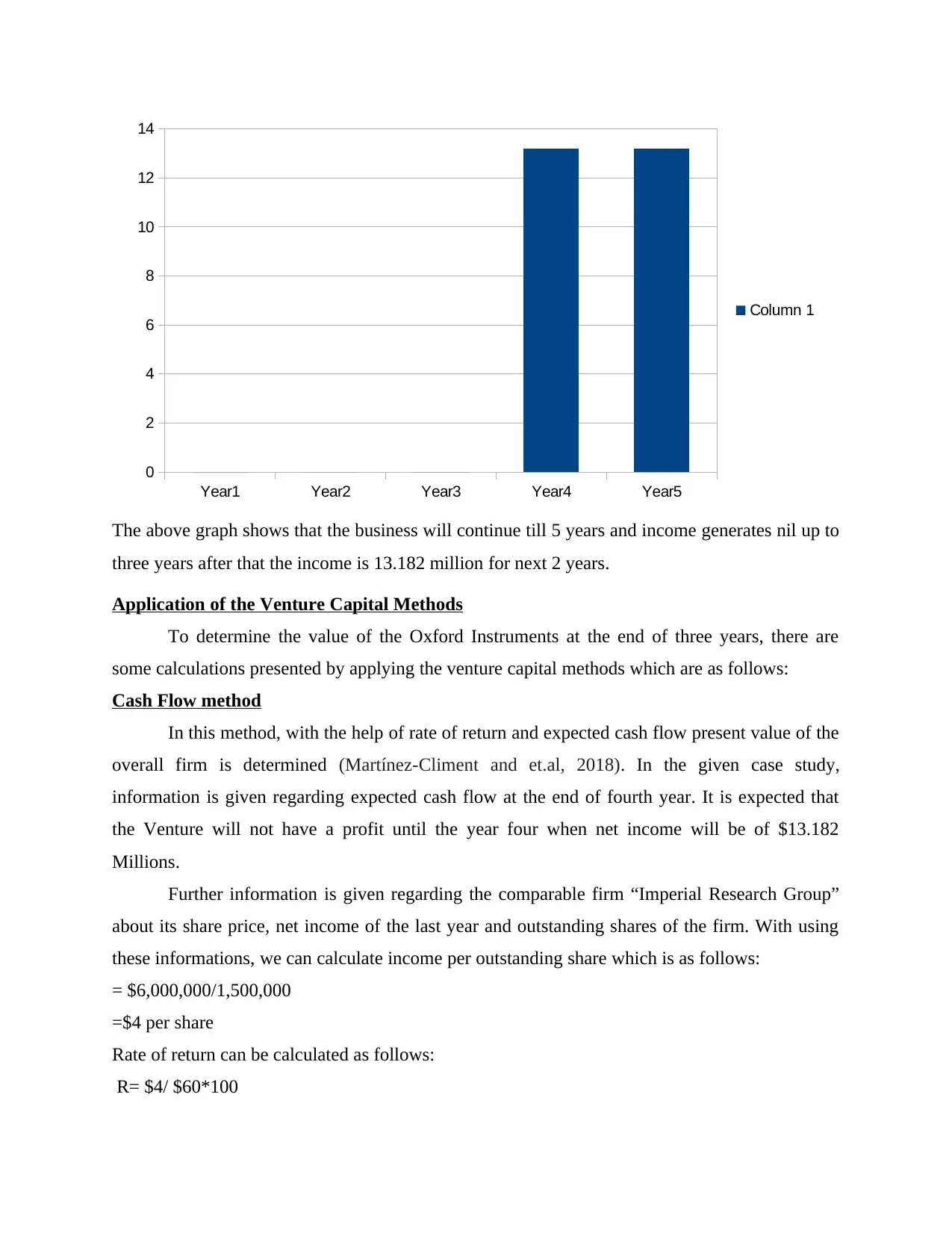

The above graph shows that the business will continue till 5 years and income generates nil up to

three years after that the income is 13.182 million for next 2 years.

Application of the Venture Capital Methods

To determine the value of the Oxford Instruments at the end of three years, there are

some calculations presented by applying the venture capital methods which are as follows:

Cash Flow method

In this method, with the help of rate of return and expected cash flow present value of the

overall firm is determined (Martínez-Climent and et.al, 2018). In the given case study,

information is given regarding expected cash flow at the end of fourth year. It is expected that

the Venture will not have a profit until the year four when net income will be of $13.182

Millions.

Further information is given regarding the comparable firm “Imperial Research Group”

about its share price, net income of the last year and outstanding shares of the firm. With using

these informations, we can calculate income per outstanding share which is as follows:

= $6,000,000/1,500,000

=$4 per share

Rate of return can be calculated as follows:

R= $4/ $60*100

Year1 Year2 Year3 Year4 Year5

0

2

4

6

8

10

12

14

Column 1

three years after that the income is 13.182 million for next 2 years.

Application of the Venture Capital Methods

To determine the value of the Oxford Instruments at the end of three years, there are

some calculations presented by applying the venture capital methods which are as follows:

Cash Flow method

In this method, with the help of rate of return and expected cash flow present value of the

overall firm is determined (Martínez-Climent and et.al, 2018). In the given case study,

information is given regarding expected cash flow at the end of fourth year. It is expected that

the Venture will not have a profit until the year four when net income will be of $13.182

Millions.

Further information is given regarding the comparable firm “Imperial Research Group”

about its share price, net income of the last year and outstanding shares of the firm. With using

these informations, we can calculate income per outstanding share which is as follows:

= $6,000,000/1,500,000

=$4 per share

Rate of return can be calculated as follows:

R= $4/ $60*100

Year1 Year2 Year3 Year4 Year5

0

2

4

6

8

10

12

14

Column 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 6.67%

Now, present value of the cash flows can be calculated as follows:

=$ 13.182 Million/ (1+0.0667)3

=$ 10.860615 Million

Assuming that the annual rate of return of the comparable firm will be accurate and most

similar to the annual rate of return of own firm present value of the Oxford Instruments is

calculated.

Fair Price method

In this method, valuation of the firm is determined on the basis of fair market value of the

outstanding shares of the firm (Velt and et.al, 2018). Fair market value of each of outstanding

shares is determined with the help of share price of the shares and net income per share of the

firm. In the given case, there is no information regarding no. of outstanding shares and their

share prices. Therefore, using the data of the comparable firm fair prices of the outstanding

shares can be determined which is as follows:

= $ 60 per share/ $ 4 per share

= $ 15 per share

Therefore fair price of the outstanding shares is $ 15 per share of “Imperial Research Group”.

Assuming that the similar shares are outstanding for the Oxford Instruments, its total market

value can be determined:

= 1,500,000 Shares * $ 15 per share

= $ 22,500,000.

Market Price method

In this method, valuation of the overall firm is determined on the basis of market price of

the outstanding shares. Assuming outstanding shares of Oxford Instruments is similar to its most

comparable firm which is 1,500,000 and share market price is of $ 60 per share. Value of the

firm will be determined as follows:

=1,500,000 shares * $ 60 per share

= $90,000,000.

Now, present value of the cash flows can be calculated as follows:

=$ 13.182 Million/ (1+0.0667)3

=$ 10.860615 Million

Assuming that the annual rate of return of the comparable firm will be accurate and most

similar to the annual rate of return of own firm present value of the Oxford Instruments is

calculated.

Fair Price method

In this method, valuation of the firm is determined on the basis of fair market value of the

outstanding shares of the firm (Velt and et.al, 2018). Fair market value of each of outstanding

shares is determined with the help of share price of the shares and net income per share of the

firm. In the given case, there is no information regarding no. of outstanding shares and their

share prices. Therefore, using the data of the comparable firm fair prices of the outstanding

shares can be determined which is as follows:

= $ 60 per share/ $ 4 per share

= $ 15 per share

Therefore fair price of the outstanding shares is $ 15 per share of “Imperial Research Group”.

Assuming that the similar shares are outstanding for the Oxford Instruments, its total market

value can be determined:

= 1,500,000 Shares * $ 15 per share

= $ 22,500,000.

Market Price method

In this method, valuation of the overall firm is determined on the basis of market price of

the outstanding shares. Assuming outstanding shares of Oxford Instruments is similar to its most

comparable firm which is 1,500,000 and share market price is of $ 60 per share. Value of the

firm will be determined as follows:

=1,500,000 shares * $ 60 per share

= $90,000,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present Value of Oxford Instruments Venture when firm wants 30 % compound annual

rate of return

Earlier rate of return is assumed similar of the annual rate of return of most comparable

firm that is Imperial Research Group. But now firm wants to have a 30% compound annual rate

of return on similar instruments so now the overall present value of Oxford Instruments will be

determined as follows:

= $ 13.182 Million/ (1+0.30)3

= $ 6,000,000.

The total present value of the venture Oxford Instruments will be of $ 6 million. Rate of

return have a inverse relationship with the value as higher will be the rate, lower will be the

value or vice-versa. It can be seen from the above calculations, when the rate of return is used as

of the comparable firm which is 6.67% annually, the overall value of the venture is of $

10.860615 Million and when annual rate is used as 30% the overall value of the firm determined

of $ 6 Million. There is a reduction in the value with 4.860615 million which is almost 45%.

therefore it can be said that annual rate of return and value have a inverse relationship which is

when one is higher the other will be lower and vice-versa.

Determination of % of ownership it have to loose in order to venture capitalist firm

To obtain funding in the form of venture capital, ventures required to offer a certain

percentage of the ownership. This can be either in only share of outstanding shares or in

combination with debt bonds or loan of the ventures (Wang and Wu 2020). Venture capitalist

firms would invest with a long term time horizon mindset usually. This investment in equity of

the firm would help the venture capitalist to involve in management participation to grow. This

creates a solid long term finance base for the ventures for future growth.

In the given case, in order to obtain investment of $ 30 million in the firm, Oxford

Instruments have to loose a fixed percentage of ownership which can be determined as follows:

Where the firm's market value is of $ 90 Million as per above calculation, out of it $ 30 Million

is obtained through the venture capitalist firm. Thus % of ownership given to them will be:

= $ 30 Million/ $ 90 Mllion

= 33.33%.

rate of return

Earlier rate of return is assumed similar of the annual rate of return of most comparable

firm that is Imperial Research Group. But now firm wants to have a 30% compound annual rate

of return on similar instruments so now the overall present value of Oxford Instruments will be

determined as follows:

= $ 13.182 Million/ (1+0.30)3

= $ 6,000,000.

The total present value of the venture Oxford Instruments will be of $ 6 million. Rate of

return have a inverse relationship with the value as higher will be the rate, lower will be the

value or vice-versa. It can be seen from the above calculations, when the rate of return is used as

of the comparable firm which is 6.67% annually, the overall value of the venture is of $

10.860615 Million and when annual rate is used as 30% the overall value of the firm determined

of $ 6 Million. There is a reduction in the value with 4.860615 million which is almost 45%.

therefore it can be said that annual rate of return and value have a inverse relationship which is

when one is higher the other will be lower and vice-versa.

Determination of % of ownership it have to loose in order to venture capitalist firm

To obtain funding in the form of venture capital, ventures required to offer a certain

percentage of the ownership. This can be either in only share of outstanding shares or in

combination with debt bonds or loan of the ventures (Wang and Wu 2020). Venture capitalist

firms would invest with a long term time horizon mindset usually. This investment in equity of

the firm would help the venture capitalist to involve in management participation to grow. This

creates a solid long term finance base for the ventures for future growth.

In the given case, in order to obtain investment of $ 30 million in the firm, Oxford

Instruments have to loose a fixed percentage of ownership which can be determined as follows:

Where the firm's market value is of $ 90 Million as per above calculation, out of it $ 30 Million

is obtained through the venture capitalist firm. Thus % of ownership given to them will be:

= $ 30 Million/ $ 90 Mllion

= 33.33%.

That shows that in order to obtain its $ 30 Million firm will have to loose 33.33% to the

venture capitalist firm.

CONCLUSION

In the above report, two major valuation model is described along-with required

assumptions and their application to the given case study. Explicit forecast period and terminal

value related to the venture's discounted cash flow valuation is also explained with their

respective graph showing the case study data. Further some calculations are also performed in

order to determine value of the Oxford Instruments and percentage of ownership it have to give

up to the venture capitalist firm.

venture capitalist firm.

CONCLUSION

In the above report, two major valuation model is described along-with required

assumptions and their application to the given case study. Explicit forecast period and terminal

value related to the venture's discounted cash flow valuation is also explained with their

respective graph showing the case study data. Further some calculations are also performed in

order to determine value of the Oxford Instruments and percentage of ownership it have to give

up to the venture capitalist firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bakos and et.al, 2019. Funding new ventures with digital tokens: Due diligence and token

tradability. NYU Stern School of Business.

Bollaert and et.al, 2021. Fintech and access to finance. Journal of corporate finance, 68.

pp.101941.

Gompers, P.A., 2022. Optimal investment, monitoring, and the staging of venture capital. In

Venture Capital (pp. 285-313). Routledge.

Langley and et.al, 2020. Crowdfunding cities: Social entrepreneurship, speculation and solidarity

in Berlin. Geoforum, 115. pp.11-20.

Maroufkhani and et.al, 2018. Entrepreneurial ecosystems: A systematic review. Journal of

Enterprising Communities: People and Places in the Global Economy.

Martínez-Climent and et.al, 2018. Financial return crowdfunding: literature review and

bibliometric analysis. International Entrepreneurship and Management Journal, 14(3).

pp.527-553.

Velt and et.al, 2018. The entrepreneurial ecosystem and born globals: The Estonian context.

Journal of Enterprising Communities: People and Places in the Global Economy.

Wang, R. and Wu, C., 2020. Politician as venture capitalist: Politically-connected VCs and IPO

activity in China. Journal of Corporate Finance, 64. pp.101632.

Books and Journals

Bakos and et.al, 2019. Funding new ventures with digital tokens: Due diligence and token

tradability. NYU Stern School of Business.

Bollaert and et.al, 2021. Fintech and access to finance. Journal of corporate finance, 68.

pp.101941.

Gompers, P.A., 2022. Optimal investment, monitoring, and the staging of venture capital. In

Venture Capital (pp. 285-313). Routledge.

Langley and et.al, 2020. Crowdfunding cities: Social entrepreneurship, speculation and solidarity

in Berlin. Geoforum, 115. pp.11-20.

Maroufkhani and et.al, 2018. Entrepreneurial ecosystems: A systematic review. Journal of

Enterprising Communities: People and Places in the Global Economy.

Martínez-Climent and et.al, 2018. Financial return crowdfunding: literature review and

bibliometric analysis. International Entrepreneurship and Management Journal, 14(3).

pp.527-553.

Velt and et.al, 2018. The entrepreneurial ecosystem and born globals: The Estonian context.

Journal of Enterprising Communities: People and Places in the Global Economy.

Wang, R. and Wu, C., 2020. Politician as venture capitalist: Politically-connected VCs and IPO

activity in China. Journal of Corporate Finance, 64. pp.101632.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.