Entertainment Business Finance: Pro Forma Income Statement Project

VerifiedAdded on 2019/10/18

|24

|8569

|197

Homework Assignment

AI Summary

This assignment focuses on creating a pro forma income statement for a new entertainment business. It guides students through the process of identifying start-up costs, forecasting revenue based on target markets and pricing strategies, and differentiating between fixed and variable expenses. The project requires extensive research, including analysis of competitors and industry averages, to refine profitability and management effectiveness. Students are tasked with establishing a break-even point, accounting for financing, and considering the real-world implications of financial planning. The assignment emphasizes the importance of detailed financial planning, including the separation of start-up costs from operating expenses, to avoid distorting future financial comparisons. The document provides resources and information to help students prepare their pro forma income statements in an industry-standard format, including an Excel worksheet template. The goal is to create a comprehensive financial forecast that considers all aspects of launching and operating an entertainment business.

Entertainment

Business Finance

Pro Forma Resources

Creating Your Pro Forma

Income Statement

Copyright 2016 Full Sail University

Business Finance

Pro Forma Resources

Creating Your Pro Forma

Income Statement

Copyright 2016 Full Sail University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(This page left intentionally blank)

Introduction

In preparing your Pro Forma Income Statement, you are faced with several immediate

and obvious questions. How can I predict what my company’s sales will be the first year

for my new business? How do I know what my rent will be? What types of insurance

coverage will I need for my business, and what will be the cost of that coverage? How

can I estimate utility and other expenses? So many questions! So little time!

Part of the purpose of this exercise is for you to think through these and other questions

relating to starting your business. If you were not attending Full Sail and taking this

course, how would you identify the costs associated with

starting your business? Naturally, you would do some

research regarding the area where you intend to locate, talk to

commercial leasing agents regarding potential office

locations, check utility rates, talk to other small business

owners, and so on. That is precisely the process you should

be in right now. The purpose of this handout is to provide

you with additional information that may be useful in

preparing your pro forma income statement and to allow you

sufficient time to complete your draft for submission.

Be sure that your name and the company name are stated clearly on the worksheet

submission.

The Mission

You have been asked to create a pro forma income statement for your new company, with

the assumption that you will complete all required pre-planning activities this year, so

that you can open for business in January. For this exercise, you have been asked to

create a pro forma income statement by month. You have been provided a sample

income statement format in the form of an Excel worksheet. This is only a sample. It

should be modified as necessary to reflect the needs of your company and include your

important revenue and expense categories. Be sure to add your company name and

change any revenue and expense headings to include descriptions that best communicate

your company’s sales and operating expenses.

In preparing your Pro Forma Income Statement, you are faced with several immediate

and obvious questions. How can I predict what my company’s sales will be the first year

for my new business? How do I know what my rent will be? What types of insurance

coverage will I need for my business, and what will be the cost of that coverage? How

can I estimate utility and other expenses? So many questions! So little time!

Part of the purpose of this exercise is for you to think through these and other questions

relating to starting your business. If you were not attending Full Sail and taking this

course, how would you identify the costs associated with

starting your business? Naturally, you would do some

research regarding the area where you intend to locate, talk to

commercial leasing agents regarding potential office

locations, check utility rates, talk to other small business

owners, and so on. That is precisely the process you should

be in right now. The purpose of this handout is to provide

you with additional information that may be useful in

preparing your pro forma income statement and to allow you

sufficient time to complete your draft for submission.

Be sure that your name and the company name are stated clearly on the worksheet

submission.

The Mission

You have been asked to create a pro forma income statement for your new company, with

the assumption that you will complete all required pre-planning activities this year, so

that you can open for business in January. For this exercise, you have been asked to

create a pro forma income statement by month. You have been provided a sample

income statement format in the form of an Excel worksheet. This is only a sample. It

should be modified as necessary to reflect the needs of your company and include your

important revenue and expense categories. Be sure to add your company name and

change any revenue and expense headings to include descriptions that best communicate

your company’s sales and operating expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research Requirement

For the Pro-Forma Financial Statement Project, you will be required to conduct extensive

research in order to address each of the issues listed below. In addition to the research

resources provided in this project assignment and resources document, students are

expected to utilize all available reference sources, including company and other websites,

the EBSCO Host database and other similar available database resources, industry trade

association and other publications, filings with the Securities and Exchange Commission

(SEC), relevant business periodicals, and other electronic and printed materials.

If referenced in your formal report presentation, you must provide the proper citation

(using APA format). In your submission, you must:

Identify and separate the costs associated with starting and operating your

business

Establish a break even point for your business that includes the recovery of

the appropriate startup expenses

Determine and account for all the necessary operating expenses for your

company, including both administrative expenses and cost of goods sold

Identify your company’s operating cash requirements for the first year of

operation and up until the time your company reaches the break even point

Determine the most appropriate sources and forms of financing given the

nature of your company

Identify what portion of equity in your company, if any, you are willing to

offer an investor or investors in exchange for their substantial equity

investment in your new business

Properly account for your company’s cost of debt based on the determined

financial structure of the company

Generate a forecast for future demand by identifying a target market

Establish price estimates that incorporate how your customers will pay for

your product or service

Compare your company’s financial performance measures to your

competitors and the industry average to fine tune profitability, efficiency,

and management effectiveness, and liquidity

Consider the real-world implications of a failure to adequately plan for the

expenses you will encounter in your business

Please read the accompanying document for detailed resources and information

that will be crucial in preparing your pro forma income statement in a format

that is considered the industry standard.

For the Pro-Forma Financial Statement Project, you will be required to conduct extensive

research in order to address each of the issues listed below. In addition to the research

resources provided in this project assignment and resources document, students are

expected to utilize all available reference sources, including company and other websites,

the EBSCO Host database and other similar available database resources, industry trade

association and other publications, filings with the Securities and Exchange Commission

(SEC), relevant business periodicals, and other electronic and printed materials.

If referenced in your formal report presentation, you must provide the proper citation

(using APA format). In your submission, you must:

Identify and separate the costs associated with starting and operating your

business

Establish a break even point for your business that includes the recovery of

the appropriate startup expenses

Determine and account for all the necessary operating expenses for your

company, including both administrative expenses and cost of goods sold

Identify your company’s operating cash requirements for the first year of

operation and up until the time your company reaches the break even point

Determine the most appropriate sources and forms of financing given the

nature of your company

Identify what portion of equity in your company, if any, you are willing to

offer an investor or investors in exchange for their substantial equity

investment in your new business

Properly account for your company’s cost of debt based on the determined

financial structure of the company

Generate a forecast for future demand by identifying a target market

Establish price estimates that incorporate how your customers will pay for

your product or service

Compare your company’s financial performance measures to your

competitors and the industry average to fine tune profitability, efficiency,

and management effectiveness, and liquidity

Consider the real-world implications of a failure to adequately plan for the

expenses you will encounter in your business

Please read the accompanying document for detailed resources and information

that will be crucial in preparing your pro forma income statement in a format

that is considered the industry standard.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Start-Up Costs

Virtually all new businesses require considerable planning and preparation prior to

actually opening for business. In fact, one reason some

small businesses fail is their failure to complete proper

financial planning, including the creation of pro forma

financial statements such as the pro forma income

statement, which is the subject of this exercise. Even

the simplest online virtual business may likely require

that at least some initial start-up expenses be incurred

prior to the business securing its first customer and

generating any sales revenue. With that in mind, and

for the purpose of this exercise in particular, you are

asked to identify and separate your start-up business

costs from your first year financial statement, such that these costs do not distort your

ongoing operating expenses.

Start-up costs are those expenses that are incurred and which must be paid prior to the

business actually opening and accepting customers. Examples include legal fees relative

to business formation, marketing expenses prior to opening, and so on. You must isolate

any such projected expenses and develop a detailed listing and budget for these costs that

will be presented in summary form.

We separate these costs since, because the business is not yet actually operating, we are

unable to match revenues and expenses, a key goal of business accounting. Just because

they are separated to prevent distortion in future financial comparisons, they are not

simply set aside and forgotten! In business, these costs must be the subject of our

constant focus and attention, such that they are properly accounted for in our calculation

of breakeven and are paid off as the business begins to show a profit. Generally, we will

reflect the recovery of these pre-opening start-up expenses below the Net Income (profit)

line and identify their recovery as amortization of start-up costs. These expenses must be

fully-recovered prior to any distributions to business stakeholders. Just as we are always

careful to repay our debts promptly, we must also “repay” these start-up expenses by

accounting for their complete recovery prior to claiming a true profit for our business.

For the purpose of this exercise you must establish a breakeven point for your business

that includes the recovery of all startup expenses, with the exception of any assets

acquired via a mortgage or other long-term debt. For those assets, your calculation of

breakeven must include the current interest payment as a fixed expense, which must be

covered before profits can be claimed.

Virtually all new businesses require considerable planning and preparation prior to

actually opening for business. In fact, one reason some

small businesses fail is their failure to complete proper

financial planning, including the creation of pro forma

financial statements such as the pro forma income

statement, which is the subject of this exercise. Even

the simplest online virtual business may likely require

that at least some initial start-up expenses be incurred

prior to the business securing its first customer and

generating any sales revenue. With that in mind, and

for the purpose of this exercise in particular, you are

asked to identify and separate your start-up business

costs from your first year financial statement, such that these costs do not distort your

ongoing operating expenses.

Start-up costs are those expenses that are incurred and which must be paid prior to the

business actually opening and accepting customers. Examples include legal fees relative

to business formation, marketing expenses prior to opening, and so on. You must isolate

any such projected expenses and develop a detailed listing and budget for these costs that

will be presented in summary form.

We separate these costs since, because the business is not yet actually operating, we are

unable to match revenues and expenses, a key goal of business accounting. Just because

they are separated to prevent distortion in future financial comparisons, they are not

simply set aside and forgotten! In business, these costs must be the subject of our

constant focus and attention, such that they are properly accounted for in our calculation

of breakeven and are paid off as the business begins to show a profit. Generally, we will

reflect the recovery of these pre-opening start-up expenses below the Net Income (profit)

line and identify their recovery as amortization of start-up costs. These expenses must be

fully-recovered prior to any distributions to business stakeholders. Just as we are always

careful to repay our debts promptly, we must also “repay” these start-up expenses by

accounting for their complete recovery prior to claiming a true profit for our business.

For the purpose of this exercise you must establish a breakeven point for your business

that includes the recovery of all startup expenses, with the exception of any assets

acquired via a mortgage or other long-term debt. For those assets, your calculation of

breakeven must include the current interest payment as a fixed expense, which must be

covered before profits can be claimed.

Revenue (Sales)

Creating your pro forma income statement begins with a basic forecast. A forecast is a

quantifiable estimate of future demand. An estimate of the demand for your product or

service begins with a few logical questions:

What is your target market? Identifying your specific target market, including a

narrow focus on the customer demographics for the market that will most

logically need and want your products and services, will help to quantify potential

demand. Identifying how you will position and distinguish yourself within your

defined target is essential in estimating what you can accomplish in terms of

market penetration.

How will you price your products? You must establish

price estimates, considering issues such as pricing

versus the competition, quantity and other discounts,

special offers and packages, and so on. In other courses

during your EBMS curriculum, you will learn a variety

of very detailed pricing methods, considerations and

other factors. For now, your basic pricing

considerations should include covering the costs

associated with providing your product or service (such

that your gross profit is at least sufficient to cover your

operating expenses) and proper positioning against

customer expectations and competitive pressures.

How will your customers pay for your products? Will you extend credit, or will

customers be expected to pay at the time an order is placed? Remember – we

extend credit to customers only in situations where doing so may increase our

sales. There is no other reason for extending credit. Of course, if our competitors

offer credit and we do not, obviously our sales will be adversely impacted.

As you wrestle with these and other issues relative to forecasting your sales, also keep in

mind that sales for most new businesses generally see a “ramp-up” period during the

initial year, as customers in your identified market begin to find and recognize your

company and “the word gets out”. One would logically expect to see sales growth from

month to month during the first year (allowing for any seasonal factors), with customer

trial and eventual acceptance fueling sales increases following the business’s inception.

Creating your pro forma income statement begins with a basic forecast. A forecast is a

quantifiable estimate of future demand. An estimate of the demand for your product or

service begins with a few logical questions:

What is your target market? Identifying your specific target market, including a

narrow focus on the customer demographics for the market that will most

logically need and want your products and services, will help to quantify potential

demand. Identifying how you will position and distinguish yourself within your

defined target is essential in estimating what you can accomplish in terms of

market penetration.

How will you price your products? You must establish

price estimates, considering issues such as pricing

versus the competition, quantity and other discounts,

special offers and packages, and so on. In other courses

during your EBMS curriculum, you will learn a variety

of very detailed pricing methods, considerations and

other factors. For now, your basic pricing

considerations should include covering the costs

associated with providing your product or service (such

that your gross profit is at least sufficient to cover your

operating expenses) and proper positioning against

customer expectations and competitive pressures.

How will your customers pay for your products? Will you extend credit, or will

customers be expected to pay at the time an order is placed? Remember – we

extend credit to customers only in situations where doing so may increase our

sales. There is no other reason for extending credit. Of course, if our competitors

offer credit and we do not, obviously our sales will be adversely impacted.

As you wrestle with these and other issues relative to forecasting your sales, also keep in

mind that sales for most new businesses generally see a “ramp-up” period during the

initial year, as customers in your identified market begin to find and recognize your

company and “the word gets out”. One would logically expect to see sales growth from

month to month during the first year (allowing for any seasonal factors), with customer

trial and eventual acceptance fueling sales increases following the business’s inception.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed vs. Variable Expenses

Any operating business has numerous operating expenses, from the basic Cost of Goods

Sold (COGS) related directly to the production of goods and services to a variety of fixed

and variable costs, some of which may be unique to the particular business. In

determining your cost of goods sold, keep in mind that these are expenses related directly

to the production of your product, and which are only incurred when one or more units of

the product are produced. These expenses include the cost of

any raw materials, product packaging, the cost of shipping to

get the raw materials to us for further production, and so on.

In cases where we can isolate the cost of the labor to

assemble our product and where we would not have incurred

the labor cost had we not produced the item, direct

“assembly-line wages” are also considered part of COGS.

Other examples might also include commission-only

salespeople who are only paid if a sale is made; this would

not apply to regular salaried sales personnel. If the labor is not directly tied to the

production of the product (manager’s salary, accounting or human resource staff, etc.)

those salaries and wages are shown under operating expenses as Salaries & Wages.

In looking at the various expense categories applicable to your business, first consider

which expenses are fixed, and which will likely vary based on your sales volume. Fixed

expenses are those costs we incur regardless of whether we sell one item or 100.

Examples include our rent (or mortgage payment), insurance, utilities and any other

expense where we are contractually committed to payment regardless of sales (vehicle or

equipment lease payments, etc.).

Variable expenses include line items such as marketing, travel, entertainment, office

supplies, printing of promotional materials, postage and other costs that we control and

which we would logically expect to increase as we sell more products and services to

more customers. Think about it this way: if you sell twice as much in your second month

as you did in the first, which expenses will need to be increased and by what amounts?

In order to sell more of your product or service and in addition to increases in your cost

of goods sold, will attracting more customers mean more advertising, going to more

industry trade shows and mailing out more proposals? For that reason, your expenses

may fluctuate month to month.

Any operating business has numerous operating expenses, from the basic Cost of Goods

Sold (COGS) related directly to the production of goods and services to a variety of fixed

and variable costs, some of which may be unique to the particular business. In

determining your cost of goods sold, keep in mind that these are expenses related directly

to the production of your product, and which are only incurred when one or more units of

the product are produced. These expenses include the cost of

any raw materials, product packaging, the cost of shipping to

get the raw materials to us for further production, and so on.

In cases where we can isolate the cost of the labor to

assemble our product and where we would not have incurred

the labor cost had we not produced the item, direct

“assembly-line wages” are also considered part of COGS.

Other examples might also include commission-only

salespeople who are only paid if a sale is made; this would

not apply to regular salaried sales personnel. If the labor is not directly tied to the

production of the product (manager’s salary, accounting or human resource staff, etc.)

those salaries and wages are shown under operating expenses as Salaries & Wages.

In looking at the various expense categories applicable to your business, first consider

which expenses are fixed, and which will likely vary based on your sales volume. Fixed

expenses are those costs we incur regardless of whether we sell one item or 100.

Examples include our rent (or mortgage payment), insurance, utilities and any other

expense where we are contractually committed to payment regardless of sales (vehicle or

equipment lease payments, etc.).

Variable expenses include line items such as marketing, travel, entertainment, office

supplies, printing of promotional materials, postage and other costs that we control and

which we would logically expect to increase as we sell more products and services to

more customers. Think about it this way: if you sell twice as much in your second month

as you did in the first, which expenses will need to be increased and by what amounts?

In order to sell more of your product or service and in addition to increases in your cost

of goods sold, will attracting more customers mean more advertising, going to more

industry trade shows and mailing out more proposals? For that reason, your expenses

may fluctuate month to month.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Salaries and Wages

Staffing a new business can quite an undertaking, especially if your business plan

requires employees beyond the business owners themselves.

In thinking of staffing and salaries and wages for your new business, one consideration

must be thoughtful discussion regarding the absolute minimum staffing requirements for

the company – the level at which we can produce and sell just one unit of our product or

service. The reason we do this is to establish a

“bare bones” approach to staffing the business and

to create a “zero-based” philosophy in evaluating

adding any payroll expense to the business. Each

additional payroll dollar must be expected to pay

for itself in additional sales, otherwise no

additional staffing should be considered.

Not too surprisingly, a new business that is well-staffed in anticipation of immediate sales

success may quickly find itself in a tough cash flow situation when salaries and wages

must be paid, while sales grow takes time to materialize and credit sales may see the

company receiving payment well after the sale is made. With these factors in mind, a

very cautious and conservative approach to staffing is recommended for a start-up

enterprise.

Should we, as owners, take a salary, or simply wait and take our share of profits when

they do finally come? This frequently asked question requires further study. If your

team of founding owners does not take a salary, how will you pay your (personal) bills?

Will you need outside investors to provide funding for your business, or will you use only

your own money to launch the new company? Simply put, if you expect to need outside

investment, it is wise for you to take a nominal salary, such that you are able to devote

100% of your time and attention toward making the business successful. In that situation,

your investor sees that as reasonable, provided the salary is not excessive and also

provided the investor receives an appropriate return on his or her investment prior to you

and the other owners taking any share of profits. This is also logical, since the investors’

cash infusion should entitle them to receive preferential treatment for the first profit

dollars from the successful business.

If, on the other hand, you intend to fund your business solely with your own personal

funds and/or a secured loan from a traditional lender (bank), forgoing a salary for

yourself and waiting to reap the rewards until a profit is available for distribution may

seem to make sense. But always remember that salaries for both you and your employees

are deductible expenses for tax purposes! If you are not taking a salary, then how are you

paying your personal bills?

For this exercise, be careful as you plug in payroll in the form of salaries for you and any

partner(s) you may have. Think of it as if you were starting the business on your own as

a sole proprietorship. Why allocate more salaries to manage the business than you might

have doing it as a single owner? Justify every payroll dollar you include in your plan.

Staffing a new business can quite an undertaking, especially if your business plan

requires employees beyond the business owners themselves.

In thinking of staffing and salaries and wages for your new business, one consideration

must be thoughtful discussion regarding the absolute minimum staffing requirements for

the company – the level at which we can produce and sell just one unit of our product or

service. The reason we do this is to establish a

“bare bones” approach to staffing the business and

to create a “zero-based” philosophy in evaluating

adding any payroll expense to the business. Each

additional payroll dollar must be expected to pay

for itself in additional sales, otherwise no

additional staffing should be considered.

Not too surprisingly, a new business that is well-staffed in anticipation of immediate sales

success may quickly find itself in a tough cash flow situation when salaries and wages

must be paid, while sales grow takes time to materialize and credit sales may see the

company receiving payment well after the sale is made. With these factors in mind, a

very cautious and conservative approach to staffing is recommended for a start-up

enterprise.

Should we, as owners, take a salary, or simply wait and take our share of profits when

they do finally come? This frequently asked question requires further study. If your

team of founding owners does not take a salary, how will you pay your (personal) bills?

Will you need outside investors to provide funding for your business, or will you use only

your own money to launch the new company? Simply put, if you expect to need outside

investment, it is wise for you to take a nominal salary, such that you are able to devote

100% of your time and attention toward making the business successful. In that situation,

your investor sees that as reasonable, provided the salary is not excessive and also

provided the investor receives an appropriate return on his or her investment prior to you

and the other owners taking any share of profits. This is also logical, since the investors’

cash infusion should entitle them to receive preferential treatment for the first profit

dollars from the successful business.

If, on the other hand, you intend to fund your business solely with your own personal

funds and/or a secured loan from a traditional lender (bank), forgoing a salary for

yourself and waiting to reap the rewards until a profit is available for distribution may

seem to make sense. But always remember that salaries for both you and your employees

are deductible expenses for tax purposes! If you are not taking a salary, then how are you

paying your personal bills?

For this exercise, be careful as you plug in payroll in the form of salaries for you and any

partner(s) you may have. Think of it as if you were starting the business on your own as

a sole proprietorship. Why allocate more salaries to manage the business than you might

have doing it as a single owner? Justify every payroll dollar you include in your plan.

Payroll Taxes and Employee Benefits

Often referred to as PT & EB in business parlance, payroll taxes and employee benefits

must be considered in any business where we have employees and their resulting payroll

expense. Federal law strictly regulates the definition of an “employee”, and wage and

hour laws preclude businesses from treating employees as “independent contractors” in

order to avoid payroll taxes or overtime compensation. For information on the Fair

Labor Standards Act (FSLA) and other important regulations regarding employment,

visit the U.S. Department of Labor and search the Wage and Hour Regulations.

Federal and state wage and hour laws regulate the payment of wages to employees and

have significant implications for payroll departments. These laws regulate the method of

payment of wages, the payment of wages upon termination of employment, allowable

deductions from employee paychecks, the withholding and payment of employment

taxes, wage garnishments, recordkeeping, and the

maintenance of payroll records. Employers must

withhold from employee paychecks certain tax

payments including federal and state income taxes

and FICA. To determine the proper withholding for

federal and state income taxes, employees must

complete a Form W-4 and provide the employer with

their Social Security Number. At the end of each year,

employers are required to report on a Form W-2 each

employee’s earnings and the taxes withheld.

Employers must also have an employer identification number for reporting and paying

federal and state unemployment and payroll taxes. In addition, since 1996, employers

have been required to report new hire information to a state directory as part of federal

legislation on welfare reform.

For the purpose of this exercise, you should assume that payroll taxes will be

approximately 10% of salaries and wages. Keep in mind that, while your business will

also withhold the employee’s portion of the payroll tax, your income statement will only

reflect the portion the company pays.

Source: Business and Legal Reports.com

You are not required to offer your employees specific benefits, although common

business practices include basic vacation and sick pay, holiday pay, and so on. In

addition, of course, many employers offer employer-subsidized medical and other

insurance coverage, 401K and other retirement plans, and so on. As a business just

starting out, generally it is advisable to limit the additional benefits for your employees

until such time as the business can reasonably afford to provide them, provided you are

able to attract and retain the staff you need.

Often referred to as PT & EB in business parlance, payroll taxes and employee benefits

must be considered in any business where we have employees and their resulting payroll

expense. Federal law strictly regulates the definition of an “employee”, and wage and

hour laws preclude businesses from treating employees as “independent contractors” in

order to avoid payroll taxes or overtime compensation. For information on the Fair

Labor Standards Act (FSLA) and other important regulations regarding employment,

visit the U.S. Department of Labor and search the Wage and Hour Regulations.

Federal and state wage and hour laws regulate the payment of wages to employees and

have significant implications for payroll departments. These laws regulate the method of

payment of wages, the payment of wages upon termination of employment, allowable

deductions from employee paychecks, the withholding and payment of employment

taxes, wage garnishments, recordkeeping, and the

maintenance of payroll records. Employers must

withhold from employee paychecks certain tax

payments including federal and state income taxes

and FICA. To determine the proper withholding for

federal and state income taxes, employees must

complete a Form W-4 and provide the employer with

their Social Security Number. At the end of each year,

employers are required to report on a Form W-2 each

employee’s earnings and the taxes withheld.

Employers must also have an employer identification number for reporting and paying

federal and state unemployment and payroll taxes. In addition, since 1996, employers

have been required to report new hire information to a state directory as part of federal

legislation on welfare reform.

For the purpose of this exercise, you should assume that payroll taxes will be

approximately 10% of salaries and wages. Keep in mind that, while your business will

also withhold the employee’s portion of the payroll tax, your income statement will only

reflect the portion the company pays.

Source: Business and Legal Reports.com

You are not required to offer your employees specific benefits, although common

business practices include basic vacation and sick pay, holiday pay, and so on. In

addition, of course, many employers offer employer-subsidized medical and other

insurance coverage, 401K and other retirement plans, and so on. As a business just

starting out, generally it is advisable to limit the additional benefits for your employees

until such time as the business can reasonably afford to provide them, provided you are

able to attract and retain the staff you need.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rent

In starting a business, it is not uncommon for an individual or team to simply work from

home initially in order to save money and especially if the business does not require

direct customer contact that requires a specific central office location. Zoning and other

local legal restrictions, however, may preclude you from running an active business from

your home, particularly in cases where direct customer

traffic may increase beyond residential community

tolerance, product deliveries or outgoing shipments are

frequent, and so on. While these restrictions may not

typically apply to a web-based, virtual company

environment, always consult local regulations regarding

business licensure just to be safe. Once you decide an office location is needed, naturally

it is up to you to determine the optimal location to best serve your needs and still keep

your initial expenses to a minimum.

Of course, you may want to weigh available options for actually purchasing and owning

your business location or office instead of leasing. Since that is generally not a viable

option for many new businesses, this document will focus predominantly on leased space,

at least during the first few years of operation.

In order to estimate rent for your office, you will need to first estimate the square footage

you will require. Consider the intended use for the space. Will you be meeting

customers at the office, conducting business face-to-face with clients, or just using the

office as a base of operations? Will manufacturing or storage space be required? The

level of potential direct customer contact at an office location will help you determine the

need for facilities such as conference rooms, convenient and available parking, restroom

facilities and so on.

Once you have an estimate of your square footage requirement and concept for the

optimal layout (floor plan) for the space, you may consider contacting a commercial real

estate broker in the area where you wish to locate to check current typical lease rates and

terms. You will want to learn what the annual lease rate might be on a square foot basis

and whether there are any additional fees involved (charges for “common area

maintenance”, trash collection, and so on). What does the lease include? Are any

utilities included? Are there any restrictions regarding access, parking, signage, hours of

operation, etc.?

NOTE: IN MAKING RESEARCH CALLS TO LEASING AGENTS OR ANY

OTHER OUTSIDE SOURCE RELATIVE TO SCHOOL PROJECTS, ALWAYS

IDENTIFY YOURSELF AS A STUDENT LOOKING FOR ASSISTANCE ON A

CLASS PROJECT. NEVER POSE AS A SERIOUS POTENTIAL PROSPECT

UNLESS IT IS REALLY YOUR INTENTION TO PURSUE THE PROJECT

FOLLOWING GRADUATION. THIS IS JUST PROFESSIONAL COURTESY.

In starting a business, it is not uncommon for an individual or team to simply work from

home initially in order to save money and especially if the business does not require

direct customer contact that requires a specific central office location. Zoning and other

local legal restrictions, however, may preclude you from running an active business from

your home, particularly in cases where direct customer

traffic may increase beyond residential community

tolerance, product deliveries or outgoing shipments are

frequent, and so on. While these restrictions may not

typically apply to a web-based, virtual company

environment, always consult local regulations regarding

business licensure just to be safe. Once you decide an office location is needed, naturally

it is up to you to determine the optimal location to best serve your needs and still keep

your initial expenses to a minimum.

Of course, you may want to weigh available options for actually purchasing and owning

your business location or office instead of leasing. Since that is generally not a viable

option for many new businesses, this document will focus predominantly on leased space,

at least during the first few years of operation.

In order to estimate rent for your office, you will need to first estimate the square footage

you will require. Consider the intended use for the space. Will you be meeting

customers at the office, conducting business face-to-face with clients, or just using the

office as a base of operations? Will manufacturing or storage space be required? The

level of potential direct customer contact at an office location will help you determine the

need for facilities such as conference rooms, convenient and available parking, restroom

facilities and so on.

Once you have an estimate of your square footage requirement and concept for the

optimal layout (floor plan) for the space, you may consider contacting a commercial real

estate broker in the area where you wish to locate to check current typical lease rates and

terms. You will want to learn what the annual lease rate might be on a square foot basis

and whether there are any additional fees involved (charges for “common area

maintenance”, trash collection, and so on). What does the lease include? Are any

utilities included? Are there any restrictions regarding access, parking, signage, hours of

operation, etc.?

NOTE: IN MAKING RESEARCH CALLS TO LEASING AGENTS OR ANY

OTHER OUTSIDE SOURCE RELATIVE TO SCHOOL PROJECTS, ALWAYS

IDENTIFY YOURSELF AS A STUDENT LOOKING FOR ASSISTANCE ON A

CLASS PROJECT. NEVER POSE AS A SERIOUS POTENTIAL PROSPECT

UNLESS IT IS REALLY YOUR INTENTION TO PURSUE THE PROJECT

FOLLOWING GRADUATION. THIS IS JUST PROFESSIONAL COURTESY.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Lease or Not to Lease: Things to Know

As you consider the proper location for your business and the alternatives for purchasing

or leasing an office or other facility, you will need to consider your budget and

availability of funds to purchase or lease your office

space. Naturally, if your business plan requires a

purpose-built facility or other unique requirements

where modifying an existing or standard office structure

simply does not make sense, you may want to consider a

purchase option. Otherwise, generally leasing space

may be the best alternative for a new business.

If you will be looking to lease space for your business,

here are some helpful tips in negotiating your lease.

Get the Answers

Here are some questions to ask before signing a lease:

1. Does the lease specifically state the square footage of the premises? The total

rentable square footage of the building?

2. Is the tenant's share of expenses based on total square footage of the building or

the square footage leased by the landlord? Your share may be lower if it's based

on the total square footage.

3. Do the base year expenses reflect full occupancy or are they adjusted to full

occupancy (i.e., base year real estate taxes on an unfinished building are lower

than in subsequent years)?

4. Must the landlord provide a detailed list of expenses, prepared by a CPA, to

support increases?

5. Does the lease clearly give the tenant the right to audit the landlord's books or

records?

6. If use of the building is interrupted, does the lease define the remedies available to

the tenant, such as rent abatement or lease cancellation?

7. If the landlord does not meet repair responsibilities, can the tenant make the

repairs, after notice to the landlord, and deduct the cost from the rent?

8. Is the landlord required to obtain non-disturbance agreements from current and

future lenders?

9. Does the lease clearly define how disputes will be decided?

Source: 327 Questions to Ask Before You Sign a Lease, by B. Alan Whitson (B. Alan

Whitson Co.

As you consider the proper location for your business and the alternatives for purchasing

or leasing an office or other facility, you will need to consider your budget and

availability of funds to purchase or lease your office

space. Naturally, if your business plan requires a

purpose-built facility or other unique requirements

where modifying an existing or standard office structure

simply does not make sense, you may want to consider a

purchase option. Otherwise, generally leasing space

may be the best alternative for a new business.

If you will be looking to lease space for your business,

here are some helpful tips in negotiating your lease.

Get the Answers

Here are some questions to ask before signing a lease:

1. Does the lease specifically state the square footage of the premises? The total

rentable square footage of the building?

2. Is the tenant's share of expenses based on total square footage of the building or

the square footage leased by the landlord? Your share may be lower if it's based

on the total square footage.

3. Do the base year expenses reflect full occupancy or are they adjusted to full

occupancy (i.e., base year real estate taxes on an unfinished building are lower

than in subsequent years)?

4. Must the landlord provide a detailed list of expenses, prepared by a CPA, to

support increases?

5. Does the lease clearly give the tenant the right to audit the landlord's books or

records?

6. If use of the building is interrupted, does the lease define the remedies available to

the tenant, such as rent abatement or lease cancellation?

7. If the landlord does not meet repair responsibilities, can the tenant make the

repairs, after notice to the landlord, and deduct the cost from the rent?

8. Is the landlord required to obtain non-disturbance agreements from current and

future lenders?

9. Does the lease clearly define how disputes will be decided?

Source: 327 Questions to Ask Before You Sign a Lease, by B. Alan Whitson (B. Alan

Whitson Co.

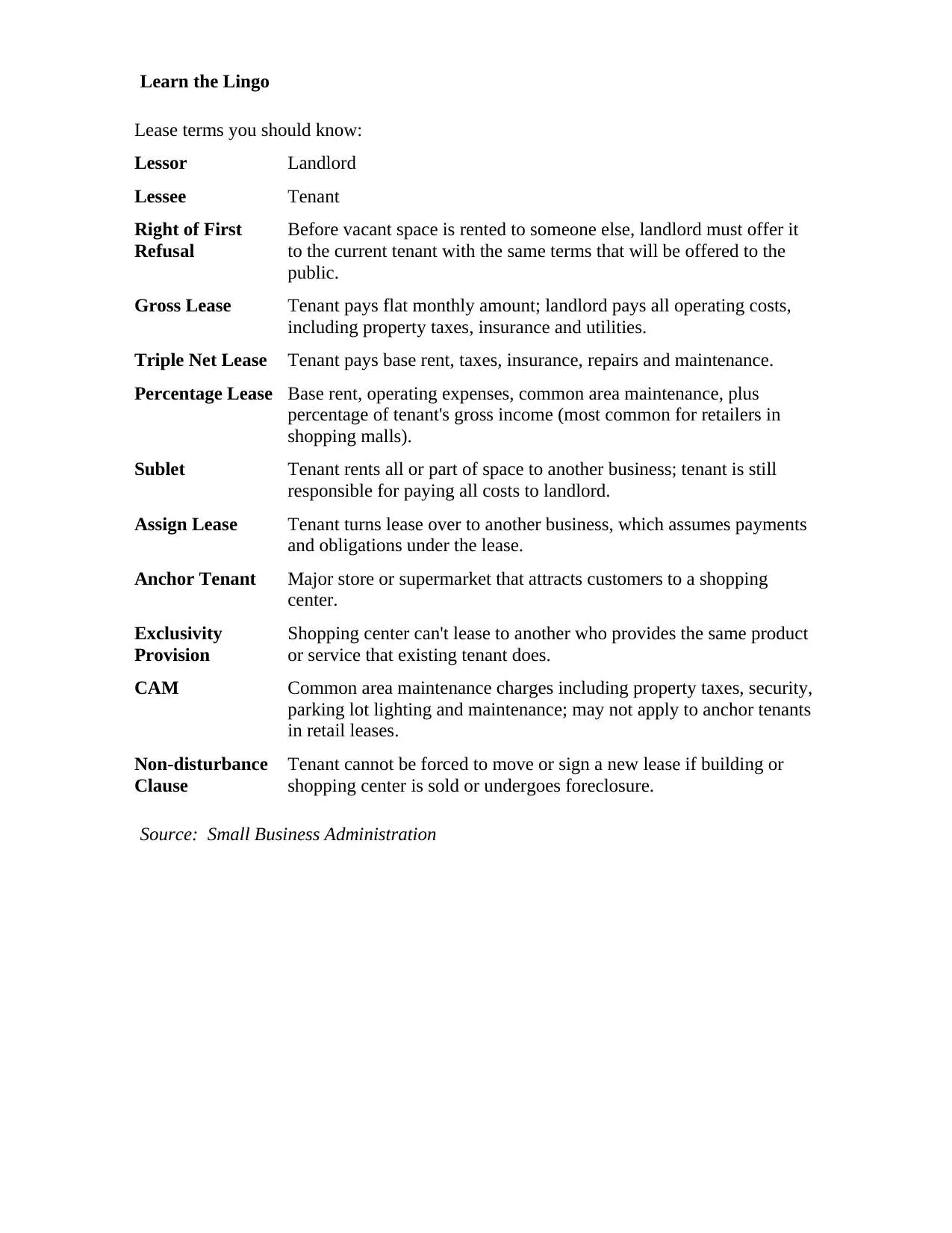

Learn the Lingo

Lease terms you should know:

Lessor Landlord

Lessee Tenant

Right of First

Refusal

Before vacant space is rented to someone else, landlord must offer it

to the current tenant with the same terms that will be offered to the

public.

Gross Lease Tenant pays flat monthly amount; landlord pays all operating costs,

including property taxes, insurance and utilities.

Triple Net Lease Tenant pays base rent, taxes, insurance, repairs and maintenance.

Percentage Lease Base rent, operating expenses, common area maintenance, plus

percentage of tenant's gross income (most common for retailers in

shopping malls).

Sublet Tenant rents all or part of space to another business; tenant is still

responsible for paying all costs to landlord.

Assign Lease Tenant turns lease over to another business, which assumes payments

and obligations under the lease.

Anchor Tenant Major store or supermarket that attracts customers to a shopping

center.

Exclusivity

Provision

Shopping center can't lease to another who provides the same product

or service that existing tenant does.

CAM Common area maintenance charges including property taxes, security,

parking lot lighting and maintenance; may not apply to anchor tenants

in retail leases.

Non-disturbance

Clause

Tenant cannot be forced to move or sign a new lease if building or

shopping center is sold or undergoes foreclosure.

Source: Small Business Administration

Lease terms you should know:

Lessor Landlord

Lessee Tenant

Right of First

Refusal

Before vacant space is rented to someone else, landlord must offer it

to the current tenant with the same terms that will be offered to the

public.

Gross Lease Tenant pays flat monthly amount; landlord pays all operating costs,

including property taxes, insurance and utilities.

Triple Net Lease Tenant pays base rent, taxes, insurance, repairs and maintenance.

Percentage Lease Base rent, operating expenses, common area maintenance, plus

percentage of tenant's gross income (most common for retailers in

shopping malls).

Sublet Tenant rents all or part of space to another business; tenant is still

responsible for paying all costs to landlord.

Assign Lease Tenant turns lease over to another business, which assumes payments

and obligations under the lease.

Anchor Tenant Major store or supermarket that attracts customers to a shopping

center.

Exclusivity

Provision

Shopping center can't lease to another who provides the same product

or service that existing tenant does.

CAM Common area maintenance charges including property taxes, security,

parking lot lighting and maintenance; may not apply to anchor tenants

in retail leases.

Non-disturbance

Clause

Tenant cannot be forced to move or sign a new lease if building or

shopping center is sold or undergoes foreclosure.

Source: Small Business Administration

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.