Entrepreneurship Case Study: REACH Health Valuation and Hotmail

VerifiedAdded on 2023/06/13

|9

|1300

|370

Case Study

AI Summary

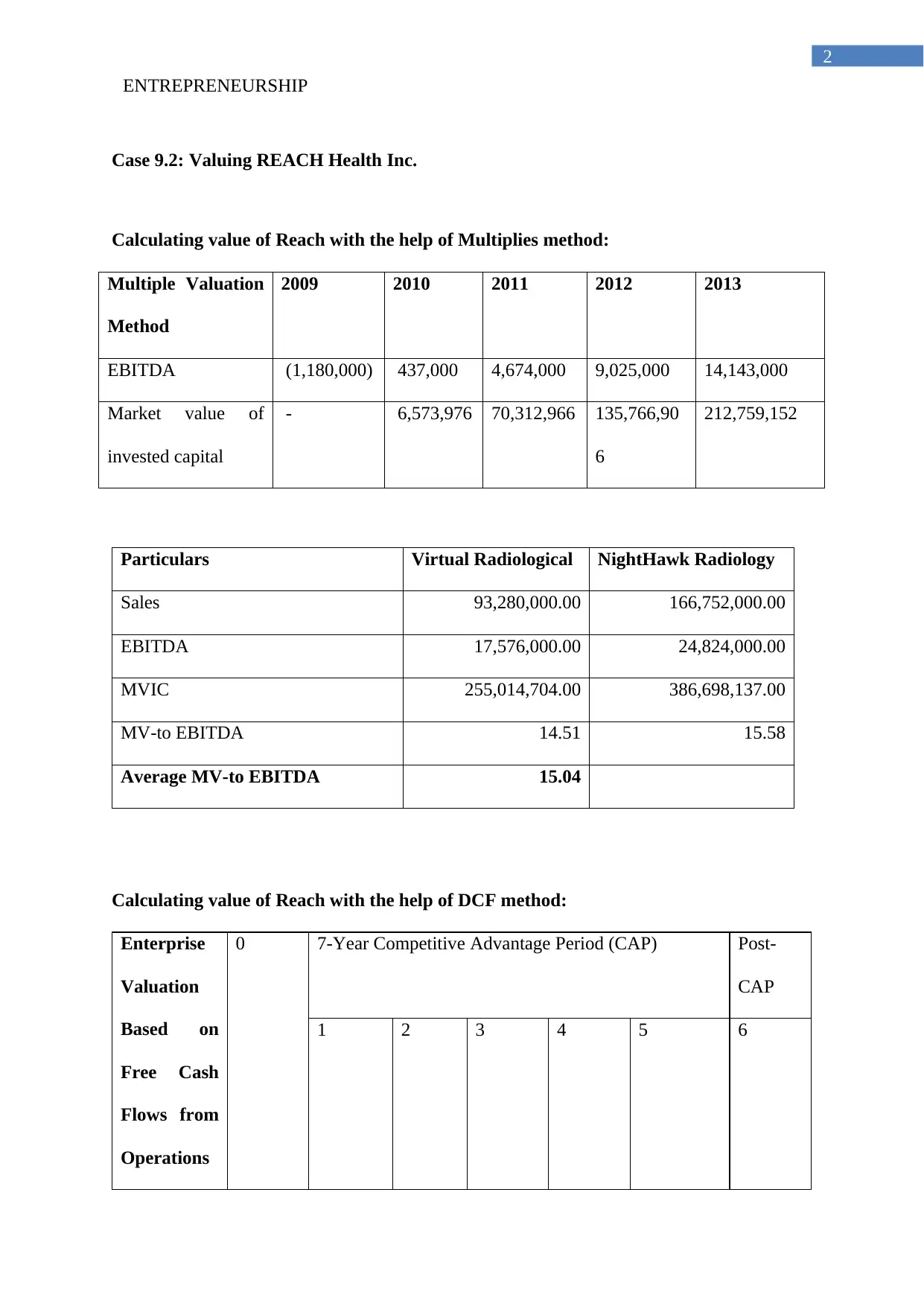

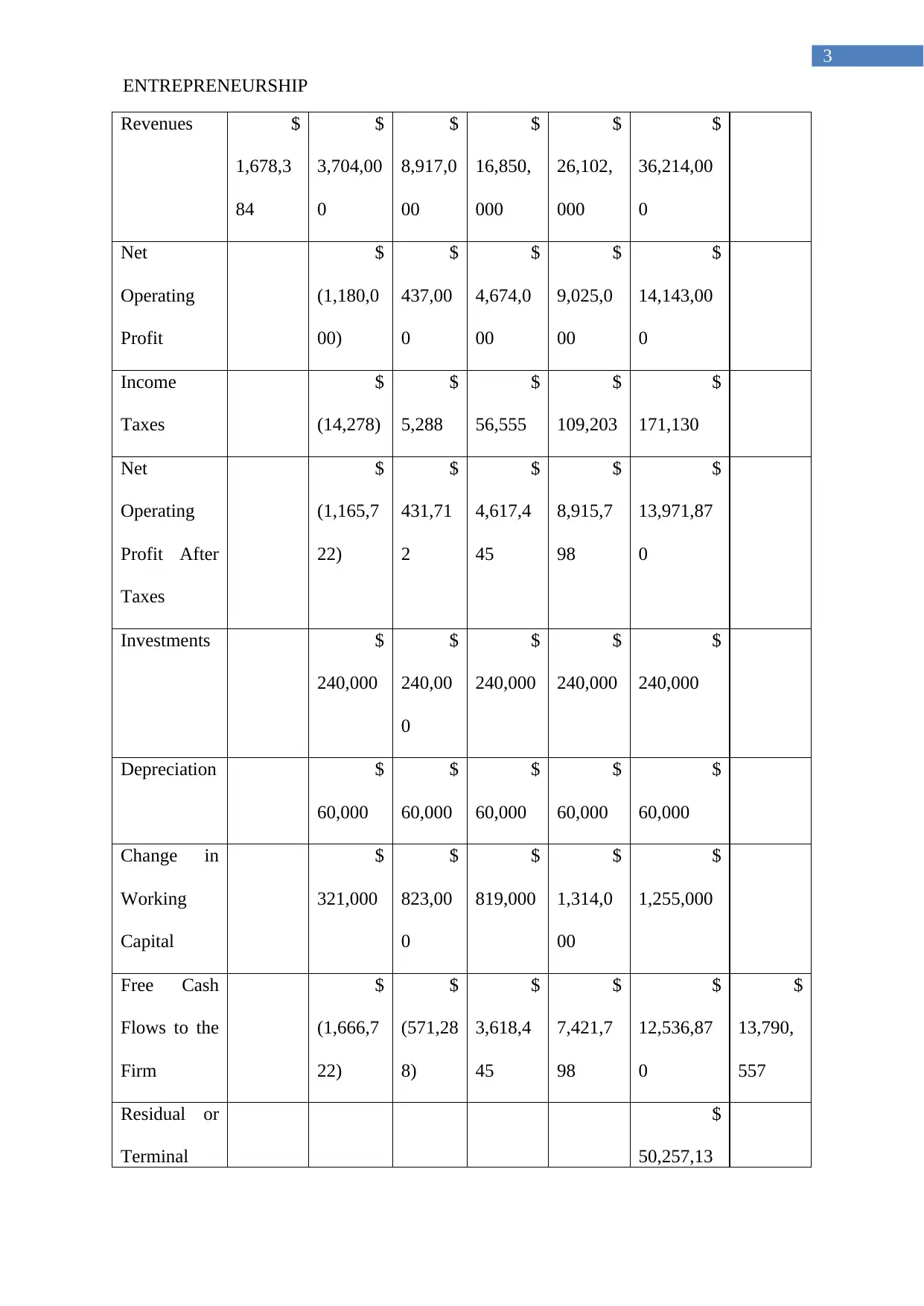

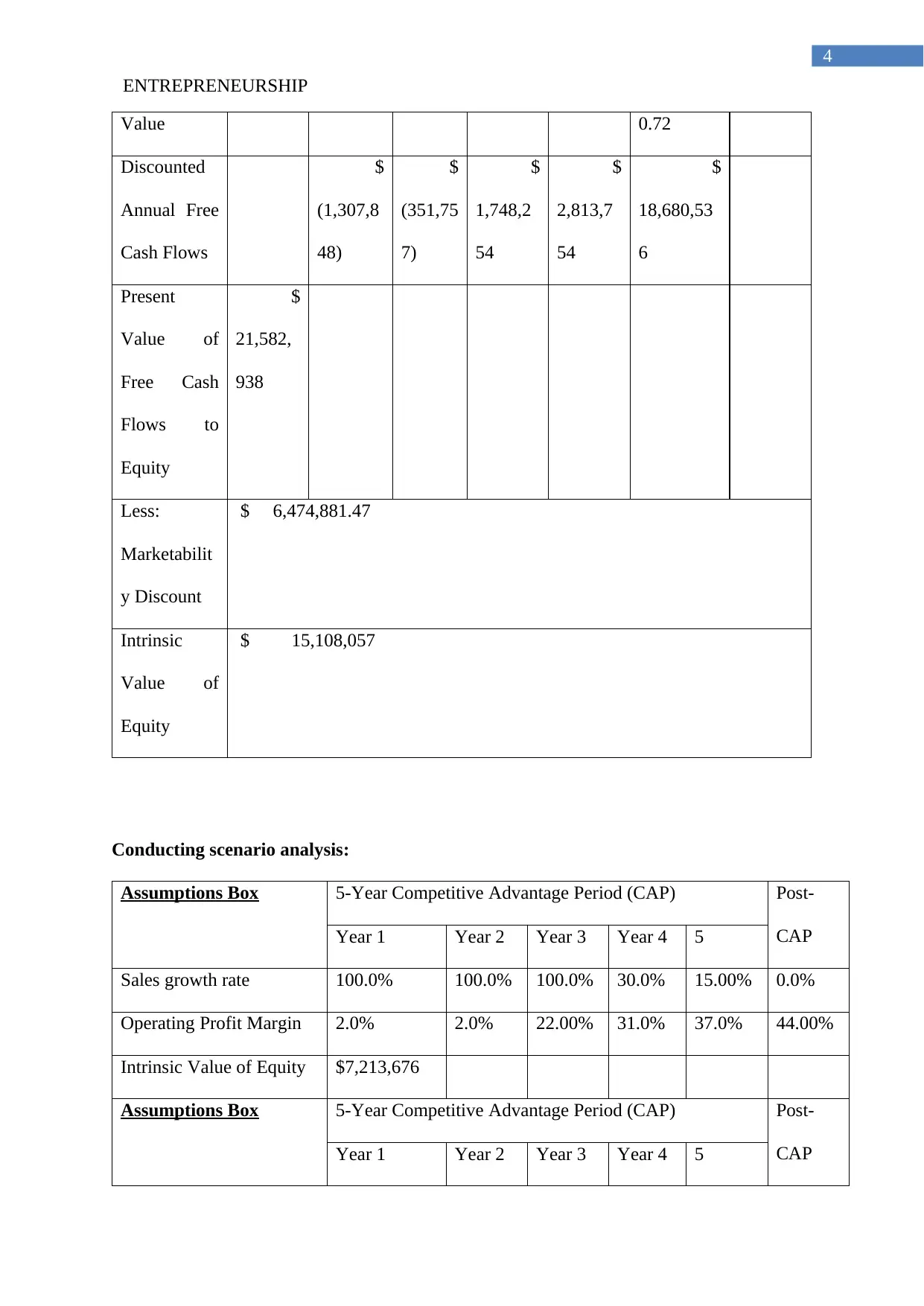

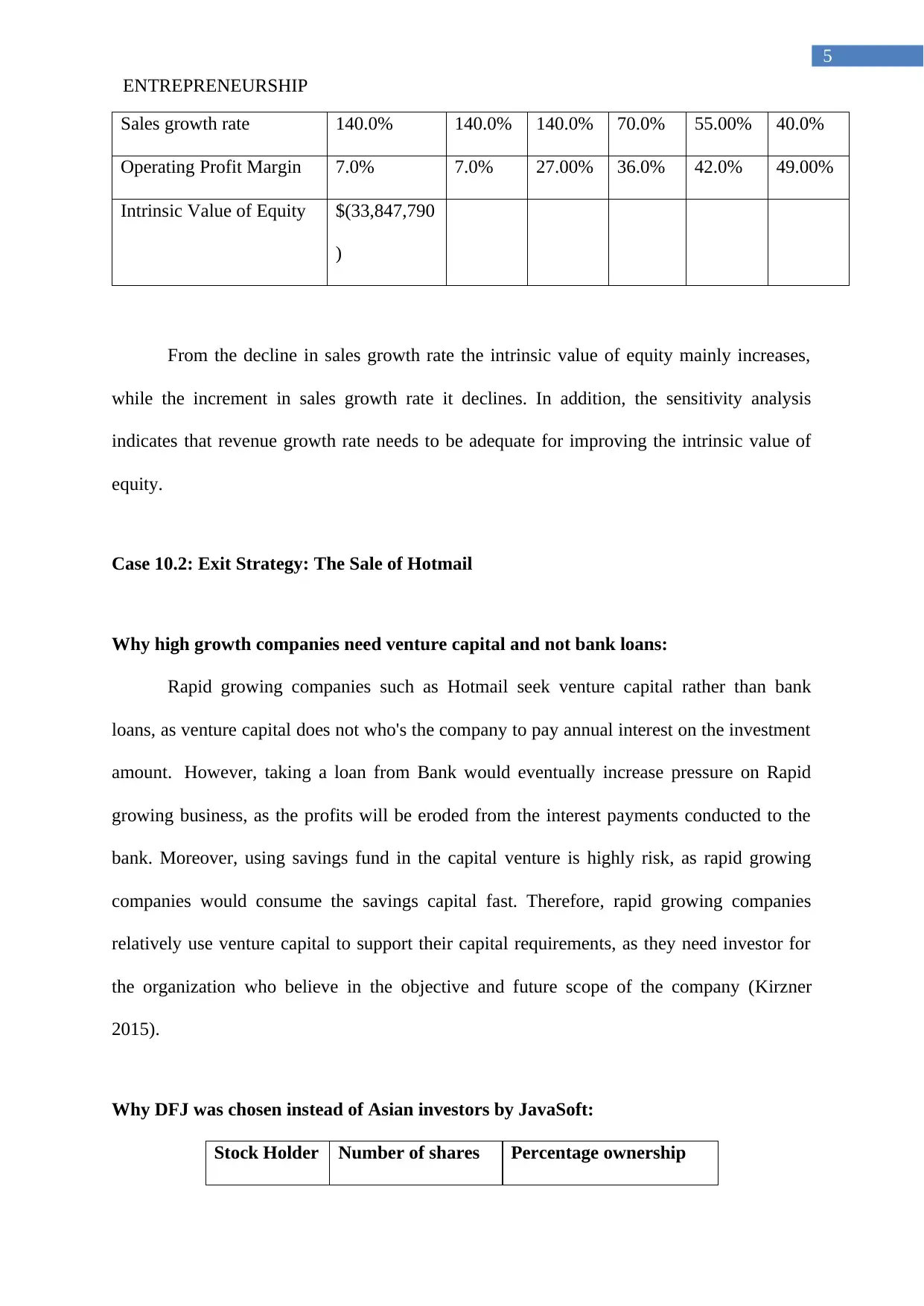

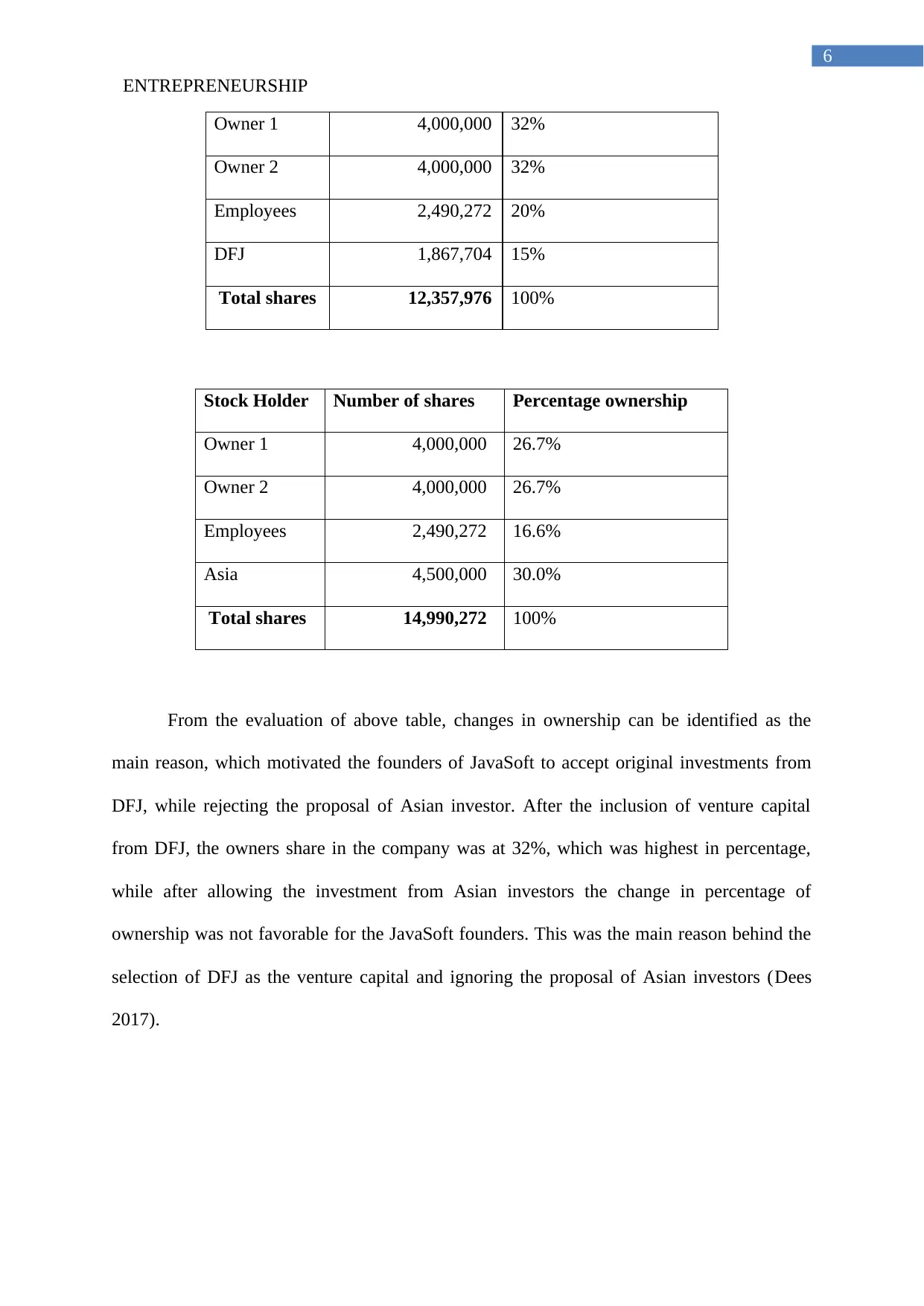

This case study analyzes REACH Health Inc.'s valuation using both multiples and discounted cash flow (DCF) methods, including scenario analysis to assess the impact of varying sales growth rates on equity value. It also examines Hotmail's exit strategy, detailing why the company chose venture capital over bank loans and DFJ over Asian investors, focusing on ownership and trust considerations. The analysis covers the significance of staged investments and the strategic rationale behind Microsoft's acquisition of Hotmail to counter Yahoo's market influence. Desklib provides access to similar solved assignments and study resources for students.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.