BFA715: Environment Disclosure and Sustainability Report

VerifiedAdded on 2022/10/13

|16

|4046

|10

Report

AI Summary

This research report provides a comprehensive overview of environment disclosure and sustainability in financial reporting, emphasizing its significance in preventing and detecting accounting scandals. It defines the concept, highlights its application, and explores the role of environment disclosure and sustainability in the modern corporate world. The report includes a literature review of five key articles, which highlight the importance of this topic. The research also outlines the methods for implementing environment disclosure and sustainability reporting. The report concludes by summarizing the main findings and implications of the research proposal, emphasizing the growing importance of environment disclosure and sustainability in the corporate sector and its role in promoting corporate social responsibility.

Running head: ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN

FINANCIAL REPORTING

Environment disclosure and sustainability in financial reporting

Name of the Student

Name of the University

Author note

FINANCIAL REPORTING

Environment disclosure and sustainability in financial reporting

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Table of Contents

Background................................................................................................................................2

Motivation and justification.......................................................................................................6

Research aim..............................................................................................................................7

Literature review........................................................................................................................9

Research design and method....................................................................................................13

Expectation on findings............................................................................................................14

Reference..................................................................................................................................15

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Table of Contents

Background................................................................................................................................2

Motivation and justification.......................................................................................................6

Research aim..............................................................................................................................7

Literature review........................................................................................................................9

Research design and method....................................................................................................13

Expectation on findings............................................................................................................14

Reference..................................................................................................................................15

2

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Executive summary

The aim of the research report is to give a brief explanation of the concept of environment

disclosure and sustainability in financial reporting in the prevention and detection of

accounting scandals. The research report explains the definition and usage of the environment

disclosure and sustainability in financial reporting with a literature review on five important

articles that explains the importance of environment disclosure and sustainability in financial

reporting in the modern corporate world. The research report also contains the methods that

are used to explain the implementation of environment disclosure and sustainability reporting

and in conclusion it states the main findings that can be reflected from this research proposal.

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Executive summary

The aim of the research report is to give a brief explanation of the concept of environment

disclosure and sustainability in financial reporting in the prevention and detection of

accounting scandals. The research report explains the definition and usage of the environment

disclosure and sustainability in financial reporting with a literature review on five important

articles that explains the importance of environment disclosure and sustainability in financial

reporting in the modern corporate world. The research report also contains the methods that

are used to explain the implementation of environment disclosure and sustainability reporting

and in conclusion it states the main findings that can be reflected from this research proposal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Background

In the modern days the environment disclosure and sustainability in financial

reporting has been given the highest priority. The environment disclosure and sustainability

in financial reporting has become a major tool in the corporate sector which will lead to the

implementation of the corporate social responsibility programs in an organisation. In the

current corporate world environmental issues are gradually increasing, and the prevention

and the detection of such activities become very difficult due to the complexities in the

operation process of any business. The environment disclosure and sustainability in financial

reporting helps in solving the problems that are related with the sustainable development and

environment related problems that happen in an organization. This reporting system usually

requires the analysis, inspection, investigation and the questioning process in order to find out

the reason for the occurrence of pollution and to get expert opinion regarding the steps that

are essential for the prevention of such activities that causes pollution. Environment

disclosure and sustainability in financial reporting concentrate on the prevention and the

detection of the fraud and the investigation of frauds in the financial statements. The

environment disclosure and sustainability in financial reporting system requires both the

application of the theory and practical aspect of accounting and for that reason it become

popular among the organizations and the managers used to implement the environment

disclosure and sustainability in financial reporting system to ensure that the organisation

does not effect the environment and along with earning profit it also serve its duty towards

the society.

The main reason for selecting this area is due to the growing demand of the use of the

environment disclosure and sustainability in financial reporting and as the environment

disclosure and sustainability in financial reporting requires high level of analytical and

investigative skills. The scope of environment disclosure and sustainability reporting is very

wide and requires in depth research and analysis along with acquiring knowledge so that it

can be possible to detect the possible factors of environment pollution and to find out the

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Background

In the modern days the environment disclosure and sustainability in financial

reporting has been given the highest priority. The environment disclosure and sustainability

in financial reporting has become a major tool in the corporate sector which will lead to the

implementation of the corporate social responsibility programs in an organisation. In the

current corporate world environmental issues are gradually increasing, and the prevention

and the detection of such activities become very difficult due to the complexities in the

operation process of any business. The environment disclosure and sustainability in financial

reporting helps in solving the problems that are related with the sustainable development and

environment related problems that happen in an organization. This reporting system usually

requires the analysis, inspection, investigation and the questioning process in order to find out

the reason for the occurrence of pollution and to get expert opinion regarding the steps that

are essential for the prevention of such activities that causes pollution. Environment

disclosure and sustainability in financial reporting concentrate on the prevention and the

detection of the fraud and the investigation of frauds in the financial statements. The

environment disclosure and sustainability in financial reporting system requires both the

application of the theory and practical aspect of accounting and for that reason it become

popular among the organizations and the managers used to implement the environment

disclosure and sustainability in financial reporting system to ensure that the organisation

does not effect the environment and along with earning profit it also serve its duty towards

the society.

The main reason for selecting this area is due to the growing demand of the use of the

environment disclosure and sustainability in financial reporting and as the environment

disclosure and sustainability in financial reporting requires high level of analytical and

investigative skills. The scope of environment disclosure and sustainability reporting is very

wide and requires in depth research and analysis along with acquiring knowledge so that it

can be possible to detect the possible factors of environment pollution and to find out the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

process to solve the problems that arise due to environment degradation, it is a concept that

requires high quality analysis and for that reason this area has been selected for the research.

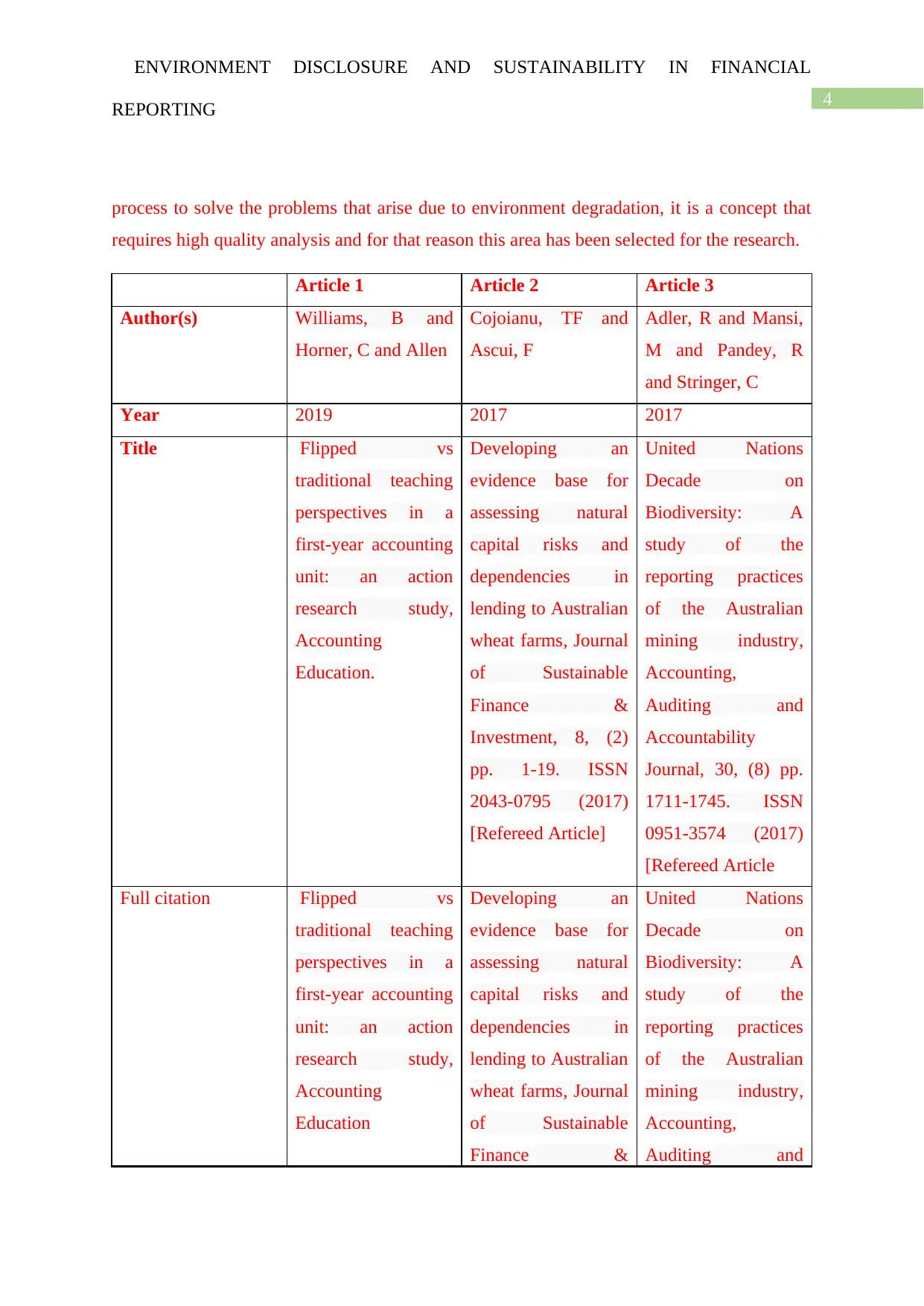

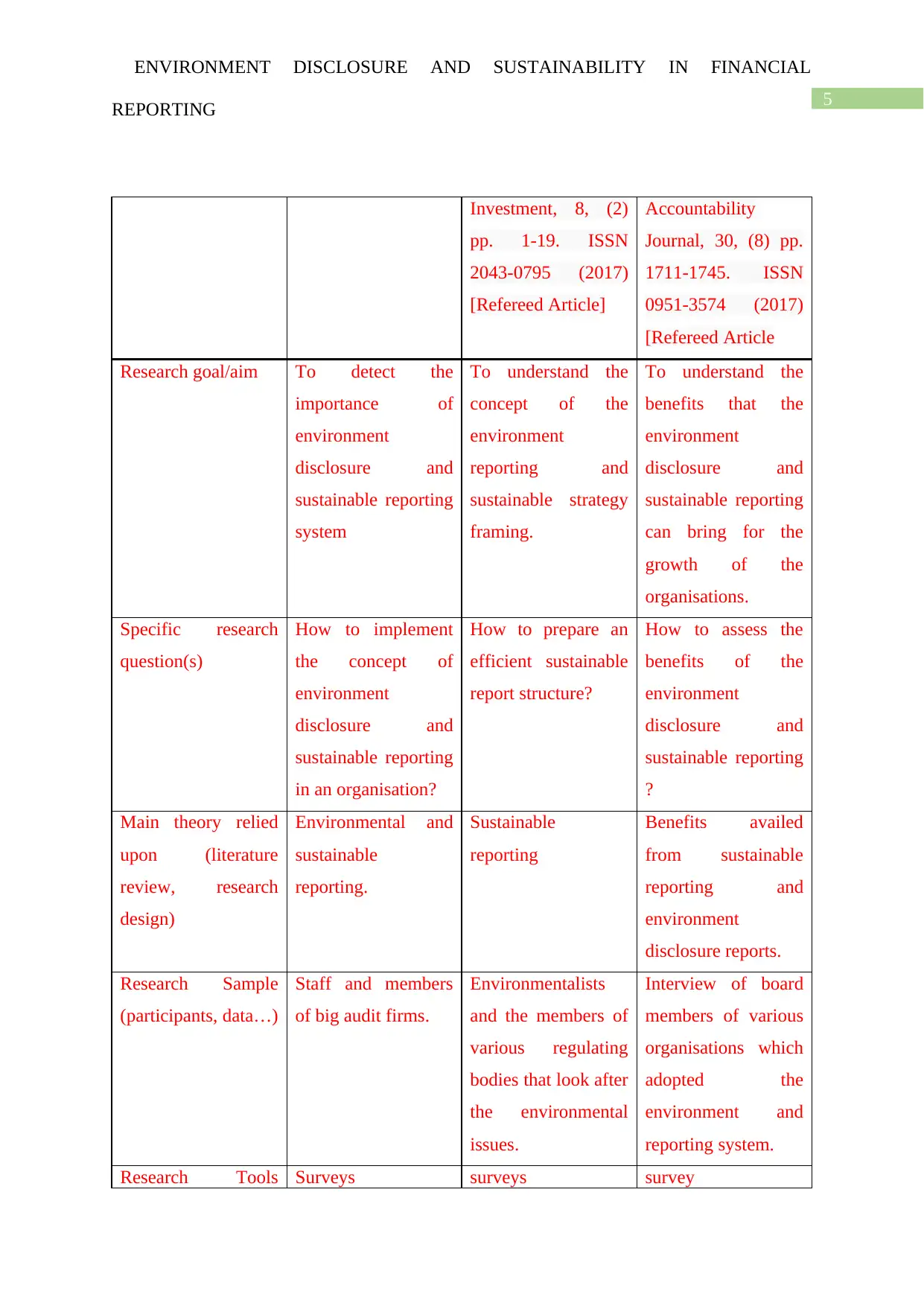

Article 1 Article 2 Article 3

Author(s) Williams, B and

Horner, C and Allen

Cojoianu, TF and

Ascui, F

Adler, R and Mansi,

M and Pandey, R

and Stringer, C

Year 2019 2017 2017

Title Flipped vs

traditional teaching

perspectives in a

first-year accounting

unit: an action

research study,

Accounting

Education.

Developing an

evidence base for

assessing natural

capital risks and

dependencies in

lending to Australian

wheat farms, Journal

of Sustainable

Finance &

Investment, 8, (2)

pp. 1-19. ISSN

2043-0795 (2017)

[Refereed Article]

United Nations

Decade on

Biodiversity: A

study of the

reporting practices

of the Australian

mining industry,

Accounting,

Auditing and

Accountability

Journal, 30, (8) pp.

1711-1745. ISSN

0951-3574 (2017)

[Refereed Article

Full citation Flipped vs

traditional teaching

perspectives in a

first-year accounting

unit: an action

research study,

Accounting

Education

Developing an

evidence base for

assessing natural

capital risks and

dependencies in

lending to Australian

wheat farms, Journal

of Sustainable

Finance &

United Nations

Decade on

Biodiversity: A

study of the

reporting practices

of the Australian

mining industry,

Accounting,

Auditing and

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

process to solve the problems that arise due to environment degradation, it is a concept that

requires high quality analysis and for that reason this area has been selected for the research.

Article 1 Article 2 Article 3

Author(s) Williams, B and

Horner, C and Allen

Cojoianu, TF and

Ascui, F

Adler, R and Mansi,

M and Pandey, R

and Stringer, C

Year 2019 2017 2017

Title Flipped vs

traditional teaching

perspectives in a

first-year accounting

unit: an action

research study,

Accounting

Education.

Developing an

evidence base for

assessing natural

capital risks and

dependencies in

lending to Australian

wheat farms, Journal

of Sustainable

Finance &

Investment, 8, (2)

pp. 1-19. ISSN

2043-0795 (2017)

[Refereed Article]

United Nations

Decade on

Biodiversity: A

study of the

reporting practices

of the Australian

mining industry,

Accounting,

Auditing and

Accountability

Journal, 30, (8) pp.

1711-1745. ISSN

0951-3574 (2017)

[Refereed Article

Full citation Flipped vs

traditional teaching

perspectives in a

first-year accounting

unit: an action

research study,

Accounting

Education

Developing an

evidence base for

assessing natural

capital risks and

dependencies in

lending to Australian

wheat farms, Journal

of Sustainable

Finance &

United Nations

Decade on

Biodiversity: A

study of the

reporting practices

of the Australian

mining industry,

Accounting,

Auditing and

5

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Investment, 8, (2)

pp. 1-19. ISSN

2043-0795 (2017)

[Refereed Article]

Accountability

Journal, 30, (8) pp.

1711-1745. ISSN

0951-3574 (2017)

[Refereed Article

Research goal/aim To detect the

importance of

environment

disclosure and

sustainable reporting

system

To understand the

concept of the

environment

reporting and

sustainable strategy

framing.

To understand the

benefits that the

environment

disclosure and

sustainable reporting

can bring for the

growth of the

organisations.

Specific research

question(s)

How to implement

the concept of

environment

disclosure and

sustainable reporting

in an organisation?

How to prepare an

efficient sustainable

report structure?

How to assess the

benefits of the

environment

disclosure and

sustainable reporting

?

Main theory relied

upon (literature

review, research

design)

Environmental and

sustainable

reporting.

Sustainable

reporting

Benefits availed

from sustainable

reporting and

environment

disclosure reports.

Research Sample

(participants, data…)

Staff and members

of big audit firms.

Environmentalists

and the members of

various regulating

bodies that look after

the environmental

issues.

Interview of board

members of various

organisations which

adopted the

environment and

reporting system.

Research Tools Surveys surveys survey

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Investment, 8, (2)

pp. 1-19. ISSN

2043-0795 (2017)

[Refereed Article]

Accountability

Journal, 30, (8) pp.

1711-1745. ISSN

0951-3574 (2017)

[Refereed Article

Research goal/aim To detect the

importance of

environment

disclosure and

sustainable reporting

system

To understand the

concept of the

environment

reporting and

sustainable strategy

framing.

To understand the

benefits that the

environment

disclosure and

sustainable reporting

can bring for the

growth of the

organisations.

Specific research

question(s)

How to implement

the concept of

environment

disclosure and

sustainable reporting

in an organisation?

How to prepare an

efficient sustainable

report structure?

How to assess the

benefits of the

environment

disclosure and

sustainable reporting

?

Main theory relied

upon (literature

review, research

design)

Environmental and

sustainable

reporting.

Sustainable

reporting

Benefits availed

from sustainable

reporting and

environment

disclosure reports.

Research Sample

(participants, data…)

Staff and members

of big audit firms.

Environmentalists

and the members of

various regulating

bodies that look after

the environmental

issues.

Interview of board

members of various

organisations which

adopted the

environment and

reporting system.

Research Tools Surveys surveys survey

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

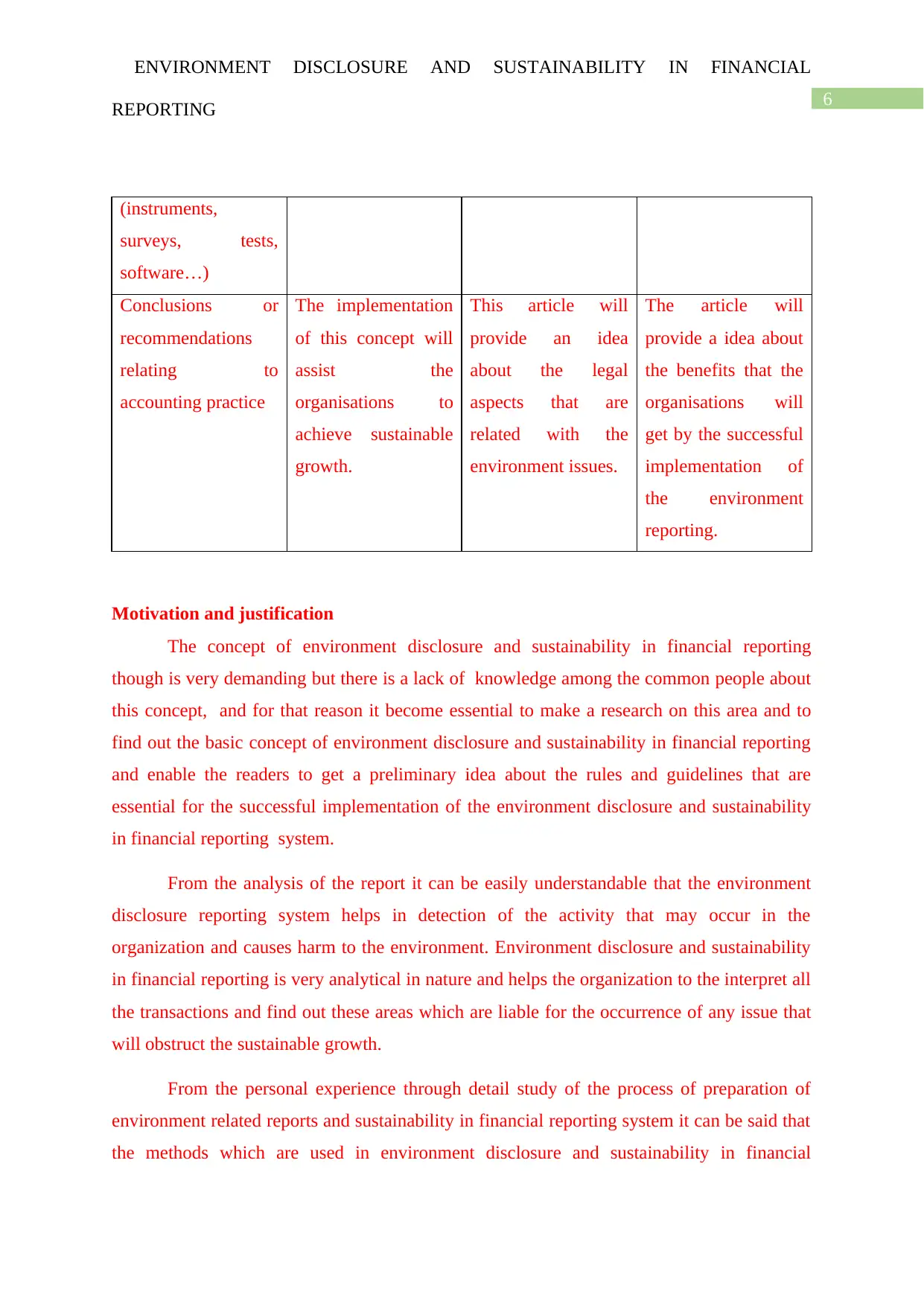

(instruments,

surveys, tests,

software…)

Conclusions or

recommendations

relating to

accounting practice

The implementation

of this concept will

assist the

organisations to

achieve sustainable

growth.

This article will

provide an idea

about the legal

aspects that are

related with the

environment issues.

The article will

provide a idea about

the benefits that the

organisations will

get by the successful

implementation of

the environment

reporting.

Motivation and justification

The concept of environment disclosure and sustainability in financial reporting

though is very demanding but there is a lack of knowledge among the common people about

this concept, and for that reason it become essential to make a research on this area and to

find out the basic concept of environment disclosure and sustainability in financial reporting

and enable the readers to get a preliminary idea about the rules and guidelines that are

essential for the successful implementation of the environment disclosure and sustainability

in financial reporting system.

From the analysis of the report it can be easily understandable that the environment

disclosure reporting system helps in detection of the activity that may occur in the

organization and causes harm to the environment. Environment disclosure and sustainability

in financial reporting is very analytical in nature and helps the organization to the interpret all

the transactions and find out these areas which are liable for the occurrence of any issue that

will obstruct the sustainable growth.

From the personal experience through detail study of the process of preparation of

environment related reports and sustainability in financial reporting system it can be said that

the methods which are used in environment disclosure and sustainability in financial

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

(instruments,

surveys, tests,

software…)

Conclusions or

recommendations

relating to

accounting practice

The implementation

of this concept will

assist the

organisations to

achieve sustainable

growth.

This article will

provide an idea

about the legal

aspects that are

related with the

environment issues.

The article will

provide a idea about

the benefits that the

organisations will

get by the successful

implementation of

the environment

reporting.

Motivation and justification

The concept of environment disclosure and sustainability in financial reporting

though is very demanding but there is a lack of knowledge among the common people about

this concept, and for that reason it become essential to make a research on this area and to

find out the basic concept of environment disclosure and sustainability in financial reporting

and enable the readers to get a preliminary idea about the rules and guidelines that are

essential for the successful implementation of the environment disclosure and sustainability

in financial reporting system.

From the analysis of the report it can be easily understandable that the environment

disclosure reporting system helps in detection of the activity that may occur in the

organization and causes harm to the environment. Environment disclosure and sustainability

in financial reporting is very analytical in nature and helps the organization to the interpret all

the transactions and find out these areas which are liable for the occurrence of any issue that

will obstruct the sustainable growth.

From the personal experience through detail study of the process of preparation of

environment related reports and sustainability in financial reporting system it can be said that

the methods which are used in environment disclosure and sustainability in financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

reporting mixes an understanding of accounting principles with the techniques of

investigation to identify whether the actions behind financial records and statements are

suspicious. Individuals specialized to accomplish environment disclosure and sustainability in

financial reporting process and frame a strategy so that the organisations can attain its

financial and social aim. The main reason for the research is that it helps in the development

of awareness in the usage of environment disclosure report process and sustainability in

financial reporting in an organization and to inspire the organizations to increase the usage of

environment disclosure and sustainability in financial reporting so that it can be possible for

the company to achieve sustainable growth in the future. The basic need of the research in

this particular area is to enhance the usage of environment disclosure and sustainability in

financial reporting and to assist in developing the general concept of this process.

Research aim

The main problem that has been observed during the research process is the lack of

knowledge among the organization about the concept of the environment disclosure and

sustainability in financial reporting as this concept is a new one and the users does not

possess basic concept knowledge about the concept of environment disclosure and

sustainability in financial reporting it become a problem to get relevant information from the

users which creates obstacle in the research process.

The main question that arise from the problem statements is, whether the users of

environment disclosure and sustainability in financial reporting have adequate knowledge

about the environment disclosure and sustainability in financial reporting?

Before raising the over arching research question, it is also essential to discuss some

of the preliminary questions which are listed below:

Is the environment disclosure and sustainability in financial reporting provide enough

information during the litigation?

Is environment disclosure and sustainability in financial reporting being the right process to

detect any manipulation of the accounting system?

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

reporting mixes an understanding of accounting principles with the techniques of

investigation to identify whether the actions behind financial records and statements are

suspicious. Individuals specialized to accomplish environment disclosure and sustainability in

financial reporting process and frame a strategy so that the organisations can attain its

financial and social aim. The main reason for the research is that it helps in the development

of awareness in the usage of environment disclosure report process and sustainability in

financial reporting in an organization and to inspire the organizations to increase the usage of

environment disclosure and sustainability in financial reporting so that it can be possible for

the company to achieve sustainable growth in the future. The basic need of the research in

this particular area is to enhance the usage of environment disclosure and sustainability in

financial reporting and to assist in developing the general concept of this process.

Research aim

The main problem that has been observed during the research process is the lack of

knowledge among the organization about the concept of the environment disclosure and

sustainability in financial reporting as this concept is a new one and the users does not

possess basic concept knowledge about the concept of environment disclosure and

sustainability in financial reporting it become a problem to get relevant information from the

users which creates obstacle in the research process.

The main question that arise from the problem statements is, whether the users of

environment disclosure and sustainability in financial reporting have adequate knowledge

about the environment disclosure and sustainability in financial reporting?

Before raising the over arching research question, it is also essential to discuss some

of the preliminary questions which are listed below:

Is the environment disclosure and sustainability in financial reporting provide enough

information during the litigation?

Is environment disclosure and sustainability in financial reporting being the right process to

detect any manipulation of the accounting system?

8

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Can environment disclosure and sustainability in financial reporting detect the acceptance

and offering of bribes or any monetary benefits from or to any third party?

Is it being possible for the environment disclosure and sustainability in financial reporting

system to detect the possible areas from which environment pollution occurs?

Will it be possible to identify the deliberate misrepresentation of the organisation in the

application of the environment disclosure and sustainability in financial reporting?

Is its is possible for the environmental disclosure and sustainability in financial reporting

system to disclose all the activities that the management take to protect the environment and

in the improvement of the society?

The research title is critical review of environment disclosure and sustainability in financial

reporting.

Literature review

The trustworthiness of the financial statements that are made by the boards of the

limited liability companies and audited by the external auditors remains the primary source of

information for the shareholders to make an idea about the financial position of the company.

The article states that environment disclosure and sustainability in financial reporting helps in

detecting the areas where the management should take care of for the development of the

environment and prevention of pollution, and prevent the management from doing such type

of activity that will affect the environment negatively. Environment disclosure and

sustainability in financial reporting is not just a technique to prevent environment pollution

but it also helps in the formulation of an internal control system in the accounting process that

will ensure that all the affairs of the business are recorded properly and the interest of the

society and the environment are safeguarded.

The article further provides that environment and sustainability reporting system

require high level of knowledge and skill and the professionals that are rendering the service

of environment disclosure and sustainability in financial reporting should have high level of

expertise so that they can easily detect the activity that is responsible for polluting the

climate and protect the interest of the stakeholders. With the implementation of the

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Can environment disclosure and sustainability in financial reporting detect the acceptance

and offering of bribes or any monetary benefits from or to any third party?

Is it being possible for the environment disclosure and sustainability in financial reporting

system to detect the possible areas from which environment pollution occurs?

Will it be possible to identify the deliberate misrepresentation of the organisation in the

application of the environment disclosure and sustainability in financial reporting?

Is its is possible for the environmental disclosure and sustainability in financial reporting

system to disclose all the activities that the management take to protect the environment and

in the improvement of the society?

The research title is critical review of environment disclosure and sustainability in financial

reporting.

Literature review

The trustworthiness of the financial statements that are made by the boards of the

limited liability companies and audited by the external auditors remains the primary source of

information for the shareholders to make an idea about the financial position of the company.

The article states that environment disclosure and sustainability in financial reporting helps in

detecting the areas where the management should take care of for the development of the

environment and prevention of pollution, and prevent the management from doing such type

of activity that will affect the environment negatively. Environment disclosure and

sustainability in financial reporting is not just a technique to prevent environment pollution

but it also helps in the formulation of an internal control system in the accounting process that

will ensure that all the affairs of the business are recorded properly and the interest of the

society and the environment are safeguarded.

The article further provides that environment and sustainability reporting system

require high level of knowledge and skill and the professionals that are rendering the service

of environment disclosure and sustainability in financial reporting should have high level of

expertise so that they can easily detect the activity that is responsible for polluting the

climate and protect the interest of the stakeholders. With the implementation of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

environment and sustainability financial reporting it has been observed that the percentage of

environment pollution has declined and most of the companies has adopted this financial

reporting process in order to fight against the degradation of the environment. The

investigation process of the environment disclosure and sustainability in financial reporting is

so scientific that it can easily detect the factors and find out the probable reason for the

occurrence of such activities that causes pollution in the environment and create obstacle in

the sustainable growth of the organisation and the persons who are responsible for such

activities. The environment disclosure reporting become a tool which helps the organizations

to carry their business in a transparent process and maintain a clean image in the society

(Williams Horner and Allen 2019).

The article further provides that the environment disclosure and sustainability in

financial reporting can be defined as the use of the accounting, auditing and investigative

skills to help in legal matters. One of the big audit firm PWC states that in order to detect

serious social crime like encouraging the process of pollution or corruption simple

knowledge will not be sufficient and the organizations has to adopt speedy sensitivity

detection and also a very profound knowledge base so that it can be possible to find out any

kind of activity that is causing environment pollution and take necessary actions against such

activities. In the modern days with the usage of modern technologies and harmful chemicals

the rate of pollution from industrial wastes increased rapidly and it become very difficult to

control this kind of activity without having sufficient skill and knowledge in this context the

environment disclosure and sustainability in financial reporting system plays a important role

and help the organizations to find out such complex issues and provide solutions to prevent

the occurrence of social crime. The different type of environment pollution like air pollution,

water pollution, noise pollution and many different types of manipulative methods that are

applied to hide the actions that cause harm for the environment can be easily be discovered

by applying the environment disclosure and sustainability in financial reporting. So, in the

modern days to fight against the advanced methods of pollution the organizations largely

depend on the environment disclosure and sustainability in financial reporting system as it is

the only method that helps in the detection of the complex environment pollution activities

and prevent the occurrence of environment pollution and help the company to attain

sustainable growth.

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

environment and sustainability financial reporting it has been observed that the percentage of

environment pollution has declined and most of the companies has adopted this financial

reporting process in order to fight against the degradation of the environment. The

investigation process of the environment disclosure and sustainability in financial reporting is

so scientific that it can easily detect the factors and find out the probable reason for the

occurrence of such activities that causes pollution in the environment and create obstacle in

the sustainable growth of the organisation and the persons who are responsible for such

activities. The environment disclosure reporting become a tool which helps the organizations

to carry their business in a transparent process and maintain a clean image in the society

(Williams Horner and Allen 2019).

The article further provides that the environment disclosure and sustainability in

financial reporting can be defined as the use of the accounting, auditing and investigative

skills to help in legal matters. One of the big audit firm PWC states that in order to detect

serious social crime like encouraging the process of pollution or corruption simple

knowledge will not be sufficient and the organizations has to adopt speedy sensitivity

detection and also a very profound knowledge base so that it can be possible to find out any

kind of activity that is causing environment pollution and take necessary actions against such

activities. In the modern days with the usage of modern technologies and harmful chemicals

the rate of pollution from industrial wastes increased rapidly and it become very difficult to

control this kind of activity without having sufficient skill and knowledge in this context the

environment disclosure and sustainability in financial reporting system plays a important role

and help the organizations to find out such complex issues and provide solutions to prevent

the occurrence of social crime. The different type of environment pollution like air pollution,

water pollution, noise pollution and many different types of manipulative methods that are

applied to hide the actions that cause harm for the environment can be easily be discovered

by applying the environment disclosure and sustainability in financial reporting. So, in the

modern days to fight against the advanced methods of pollution the organizations largely

depend on the environment disclosure and sustainability in financial reporting system as it is

the only method that helps in the detection of the complex environment pollution activities

and prevent the occurrence of environment pollution and help the company to attain

sustainable growth.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Environment pollution causes a major harm in the economic development of any

country and this is required to be prevented. The environment disclosure and sustainability in

financial reporting system provides the guidelines to the organisations to protect the economy

from the effect of environment pollution and maintain a sustainable growth of the companies

and also in the development of the socio-economic condition of any country.

The environment disclosure and sustainability in financial reporting is also defined as

the science to law. Environment disclosure and sustainability reporting is the scientific

method that provide legal remedy against the forgeries or negligence’s that may results in the

occurrence of any environmental issues. The author of this article defines the environment

disclosure and sustainability in financial reporting as the method of accounting which is

appropriate for legal review and the greatest level of assurance and ensure that the modern

days complex fraudulent activities can be detected in a scientific way and that prevent the

organizations to involve in the emanating hazardous industrial wastages that leads to the

happening of serious environmental incidents in the future. According to the author the

environment disclosure and sustainability in financial reporting method is so scientific that it

is very difficult to hide any manipulative process from the investigation done under this

system. They further claim that the sustainability and environment disclosure reporting

system is sufficiently complete so that an organisation through proper judgement can detect a

probable reason for the occurrence of any environmental issue and take a legal action against

such matter. It is further be opined that in order to get detailed evidence about the

improvement of the environment the environment and sustainability reporting system shows

a guideline based on which it might be possible for any organisation should have in depth

knowledge about the nature of the environment pollution and that will help the investigator to

easily find out the area from which the pollution of the environment has evolved and the

responsible persons who have committed such activities. The environment disclosure and

sustainability in financial reporting thus possesses legal concepts in order to give aa legal

review of all the transactions that are made by the company. The environment disclosure and

sustainability in financial reporting system thus contain a legal aspect which helps it to

provide remedy from the negative affect of accounting mis statements (Adler et al 2017).

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

Environment pollution causes a major harm in the economic development of any

country and this is required to be prevented. The environment disclosure and sustainability in

financial reporting system provides the guidelines to the organisations to protect the economy

from the effect of environment pollution and maintain a sustainable growth of the companies

and also in the development of the socio-economic condition of any country.

The environment disclosure and sustainability in financial reporting is also defined as

the science to law. Environment disclosure and sustainability reporting is the scientific

method that provide legal remedy against the forgeries or negligence’s that may results in the

occurrence of any environmental issues. The author of this article defines the environment

disclosure and sustainability in financial reporting as the method of accounting which is

appropriate for legal review and the greatest level of assurance and ensure that the modern

days complex fraudulent activities can be detected in a scientific way and that prevent the

organizations to involve in the emanating hazardous industrial wastages that leads to the

happening of serious environmental incidents in the future. According to the author the

environment disclosure and sustainability in financial reporting method is so scientific that it

is very difficult to hide any manipulative process from the investigation done under this

system. They further claim that the sustainability and environment disclosure reporting

system is sufficiently complete so that an organisation through proper judgement can detect a

probable reason for the occurrence of any environmental issue and take a legal action against

such matter. It is further be opined that in order to get detailed evidence about the

improvement of the environment the environment and sustainability reporting system shows

a guideline based on which it might be possible for any organisation should have in depth

knowledge about the nature of the environment pollution and that will help the investigator to

easily find out the area from which the pollution of the environment has evolved and the

responsible persons who have committed such activities. The environment disclosure and

sustainability in financial reporting thus possesses legal concepts in order to give aa legal

review of all the transactions that are made by the company. The environment disclosure and

sustainability in financial reporting system thus contain a legal aspect which helps it to

provide remedy from the negative affect of accounting mis statements (Adler et al 2017).

11

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

According to this literature review it can be claimed that in the modern days the

organisation should set a sustainable growth model in which priority is to be given in both

profits earning and also in the development of the society and the protection of the

environment. As business can not exist without taking the help of the society so it is a big

responsibility of the organisations to pay back to the society what they have earned from it.

The environment disclosure reporting makes it mandatory for the organisations to disclose all

the actions that it has taken for the improvement of the environment and to ensure that these

actions are properly implemented by the organisation. the company also have to disclose the

fund that they allocated for various social responsibility programs and should spend more for

the protection of the environment.

On the other hand, the author of this article define that the environmental and

sustainable financial reporting should have the potential to demonstrate special technique in

rules of evidence and the law. The author explained that the sustainable reporting required

analytical skills rather than the practical knowledge as that will help the organisation to find

out the strategies that are essential to achieve long term growth. According to the author of

this article, it is observed that the sustainability reporting enables the company to take

necessary actions to prevent the pollution in the environment and increase the corporate

social responsibility initiatives of the organisation. He states that without having strong

analytical and investigative knowledge it will never be possible to predict the complex nature

of the fraudulent activities in the modern business world. In order to detect frauds, it will be

required to face more practical issues that will help the investigator to solve the cases more

quickly and more efficiently. Knowledge is required but it is more essential to apply the

knowledge accurately without having practical knowledge it will never be possible to prepare

an environmental disclosure report and the sustainable strategies that will assist the

organisation to achieve its objective (Cojoianu and Ascui 2017).

Accounting theories

The environment disclosure and sustainability reporting are based on several

accounting theories some of these are stated below

Agency theory

ENVIRONMENT DISCLOSURE AND SUSTAINABILITY IN FINANCIAL

REPORTING

According to this literature review it can be claimed that in the modern days the

organisation should set a sustainable growth model in which priority is to be given in both

profits earning and also in the development of the society and the protection of the

environment. As business can not exist without taking the help of the society so it is a big

responsibility of the organisations to pay back to the society what they have earned from it.

The environment disclosure reporting makes it mandatory for the organisations to disclose all

the actions that it has taken for the improvement of the environment and to ensure that these

actions are properly implemented by the organisation. the company also have to disclose the

fund that they allocated for various social responsibility programs and should spend more for

the protection of the environment.

On the other hand, the author of this article define that the environmental and

sustainable financial reporting should have the potential to demonstrate special technique in

rules of evidence and the law. The author explained that the sustainable reporting required

analytical skills rather than the practical knowledge as that will help the organisation to find

out the strategies that are essential to achieve long term growth. According to the author of

this article, it is observed that the sustainability reporting enables the company to take

necessary actions to prevent the pollution in the environment and increase the corporate

social responsibility initiatives of the organisation. He states that without having strong

analytical and investigative knowledge it will never be possible to predict the complex nature

of the fraudulent activities in the modern business world. In order to detect frauds, it will be

required to face more practical issues that will help the investigator to solve the cases more

quickly and more efficiently. Knowledge is required but it is more essential to apply the

knowledge accurately without having practical knowledge it will never be possible to prepare

an environmental disclosure report and the sustainable strategies that will assist the

organisation to achieve its objective (Cojoianu and Ascui 2017).

Accounting theories

The environment disclosure and sustainability reporting are based on several

accounting theories some of these are stated below

Agency theory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.