Financial Management Assessment Report: Equity & Investment Appraisal

VerifiedAdded on 2023/01/13

|14

|3682

|52

Report

AI Summary

This report delves into key aspects of financial management, focusing on equity finance and investment appraisal techniques. It begins by examining right issues, calculating the number of shares issued and the ex-right price, and critically evaluating the advantages of scrip dividends for both shareholders and corporations. The main body of the report then explores investment appraisal techniques, including payback period, accounting rate of return (ARR), and net present value (NPV), providing detailed calculations and a critical evaluation of their advantages and disadvantages. The report uses Love-well Limited as a case study for applying these techniques. The analysis includes specific calculations for each method, such as determining the payback period, calculating ARR, and computing the NPV to assess the viability of an investment in new machinery. The conclusion summarizes the findings and recommendations based on the analysis.

Financial

Management

Assessment

Management

Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question 2. Long term finance: Equity finance...............................................................................3

Number of the shares issued and ex-right price:.........................................................................3

Critically evaluating and discussion on advantages of scrip dividends in context of

shareholders and corporation:.....................................................................................................5

MAIN BODY...................................................................................................................................7

Question 3. Investment Appraisal Techniques................................................................................7

(a). Calculate by using following investment appraisal techniques............................................8

(b). Critically evaluate the advantages or disadvantages of different investment appraisal

techniques..................................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question 2. Long term finance: Equity finance...............................................................................3

Number of the shares issued and ex-right price:.........................................................................3

Critically evaluating and discussion on advantages of scrip dividends in context of

shareholders and corporation:.....................................................................................................5

MAIN BODY...................................................................................................................................7

Question 3. Investment Appraisal Techniques................................................................................7

(a). Calculate by using following investment appraisal techniques............................................8

(b). Critically evaluate the advantages or disadvantages of different investment appraisal

techniques..................................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management implies to systematic and effective process relates to plan,

direction, regulate and manage fiscal functions such as collection, generation and utilisation of

multiple sources funds within enterprise. In simple terms this is structured usage of policies and

principles farmed by managing officials to to manage organisation's financial resources (Arianti,

2018). This study-report focuses on different characteristics and elements of financial

management which enable to find-out most efficacious right-issue for corporation and equity

option. It also discuss about advantages of option of scrip dividends with respect to corporation

as well as shareholders. This study-report highlighting calculations of no. of shares to be issued

by corporation Lexbel and EPS for showing most suited options concerned with right issues.

While later part of report evaluates benefits and drawbacks of multiple investment-appraisal

techniques.

TASK

Question 2. Long term finance: Equity finance

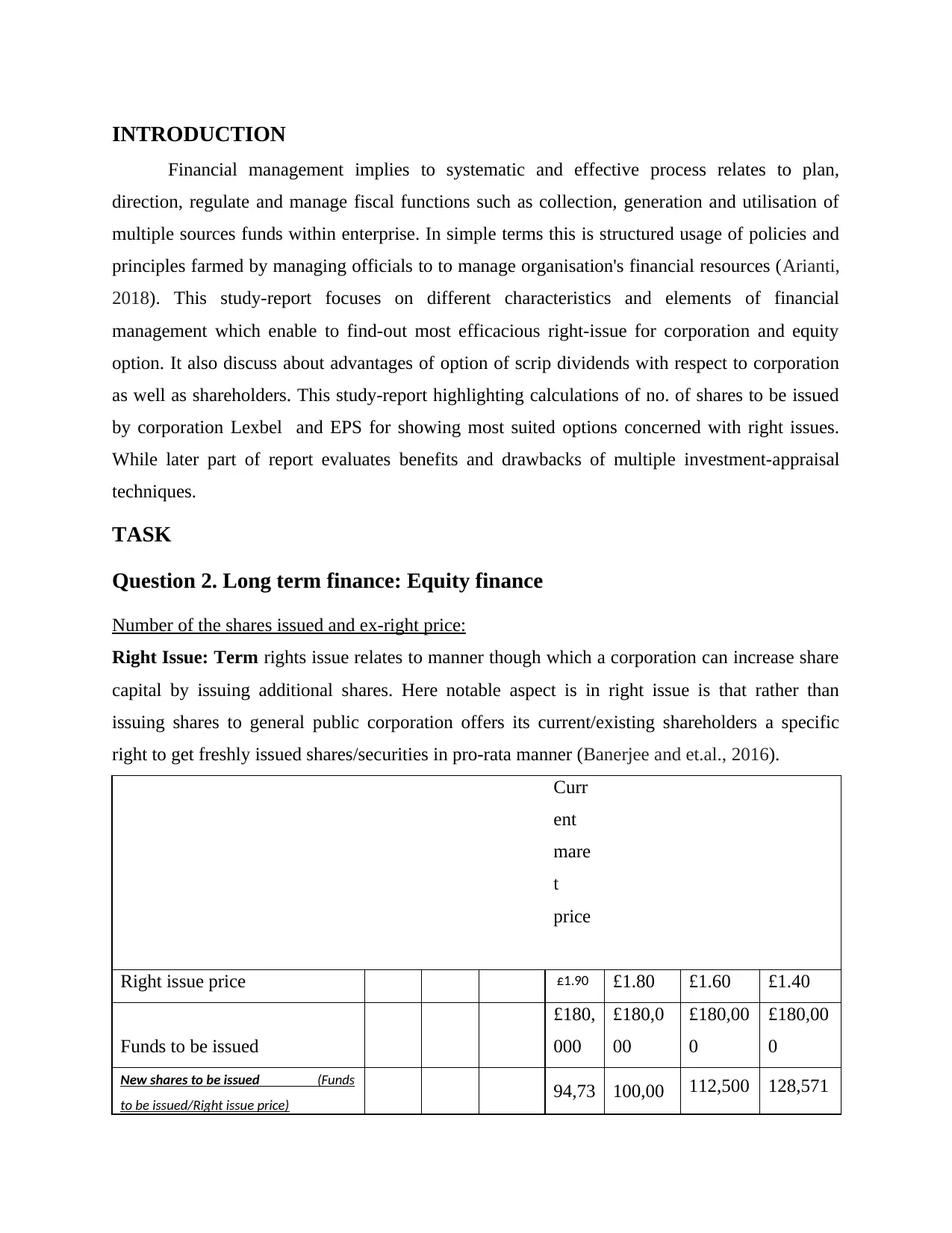

Number of the shares issued and ex-right price:

Right Issue: Term rights issue relates to manner though which a corporation can increase share

capital by issuing additional shares. Here notable aspect is in right issue is that rather than

issuing shares to general public corporation offers its current/existing shareholders a specific

right to get freshly issued shares/securities in pro-rata manner (Banerjee and et.al., 2016).

Curr

ent

mare

t

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued

£180,

000

£180,0

00

£180,00

0

£180,00

0

New shares to be issued (Funds

to be issued/Right issue price) 94,73 100,00 112,500 128,571

Financial management implies to systematic and effective process relates to plan,

direction, regulate and manage fiscal functions such as collection, generation and utilisation of

multiple sources funds within enterprise. In simple terms this is structured usage of policies and

principles farmed by managing officials to to manage organisation's financial resources (Arianti,

2018). This study-report focuses on different characteristics and elements of financial

management which enable to find-out most efficacious right-issue for corporation and equity

option. It also discuss about advantages of option of scrip dividends with respect to corporation

as well as shareholders. This study-report highlighting calculations of no. of shares to be issued

by corporation Lexbel and EPS for showing most suited options concerned with right issues.

While later part of report evaluates benefits and drawbacks of multiple investment-appraisal

techniques.

TASK

Question 2. Long term finance: Equity finance

Number of the shares issued and ex-right price:

Right Issue: Term rights issue relates to manner though which a corporation can increase share

capital by issuing additional shares. Here notable aspect is in right issue is that rather than

issuing shares to general public corporation offers its current/existing shareholders a specific

right to get freshly issued shares/securities in pro-rata manner (Banerjee and et.al., 2016).

Curr

ent

mare

t

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued

£180,

000

£180,0

00

£180,00

0

£180,00

0

New shares to be issued (Funds

to be issued/Right issue price) 94,73 100,00 112,500 128,571

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 0

Book value of ordinary shares

of £0.50

£300

,000

Numbers of shares

(Ordinary shares/price)

600,0

00

Current market value of the shares

(Number of shares*Current market

price)

£1,14

0,000

Funds raised through right

issus

£180,

000

Final value market

(Current market + Funds to be issued)

£

1,320,

000

Total new shares after right issue

( New shares issued+Number of shares)

694,7

37

700,00

0 712,500 728,571

Reserves shares

£

400,

000

Total value of the company

(Book value of shares+rezerved)

£

700,

000

Profit after tax (PAT)

(Value of the company*20%)

£

140,

000

Earning from new funds (20%)

(Funds to be issue*20%)

£

36,0

00

Total earnings after right issue

£

176,

000

Book value of ordinary shares

of £0.50

£300

,000

Numbers of shares

(Ordinary shares/price)

600,0

00

Current market value of the shares

(Number of shares*Current market

price)

£1,14

0,000

Funds raised through right

issus

£180,

000

Final value market

(Current market + Funds to be issued)

£

1,320,

000

Total new shares after right issue

( New shares issued+Number of shares)

694,7

37

700,00

0 712,500 728,571

Reserves shares

£

400,

000

Total value of the company

(Book value of shares+rezerved)

£

700,

000

Profit after tax (PAT)

(Value of the company*20%)

£

140,

000

Earning from new funds (20%)

(Funds to be issue*20%)

£

36,0

00

Total earnings after right issue

£

176,

000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

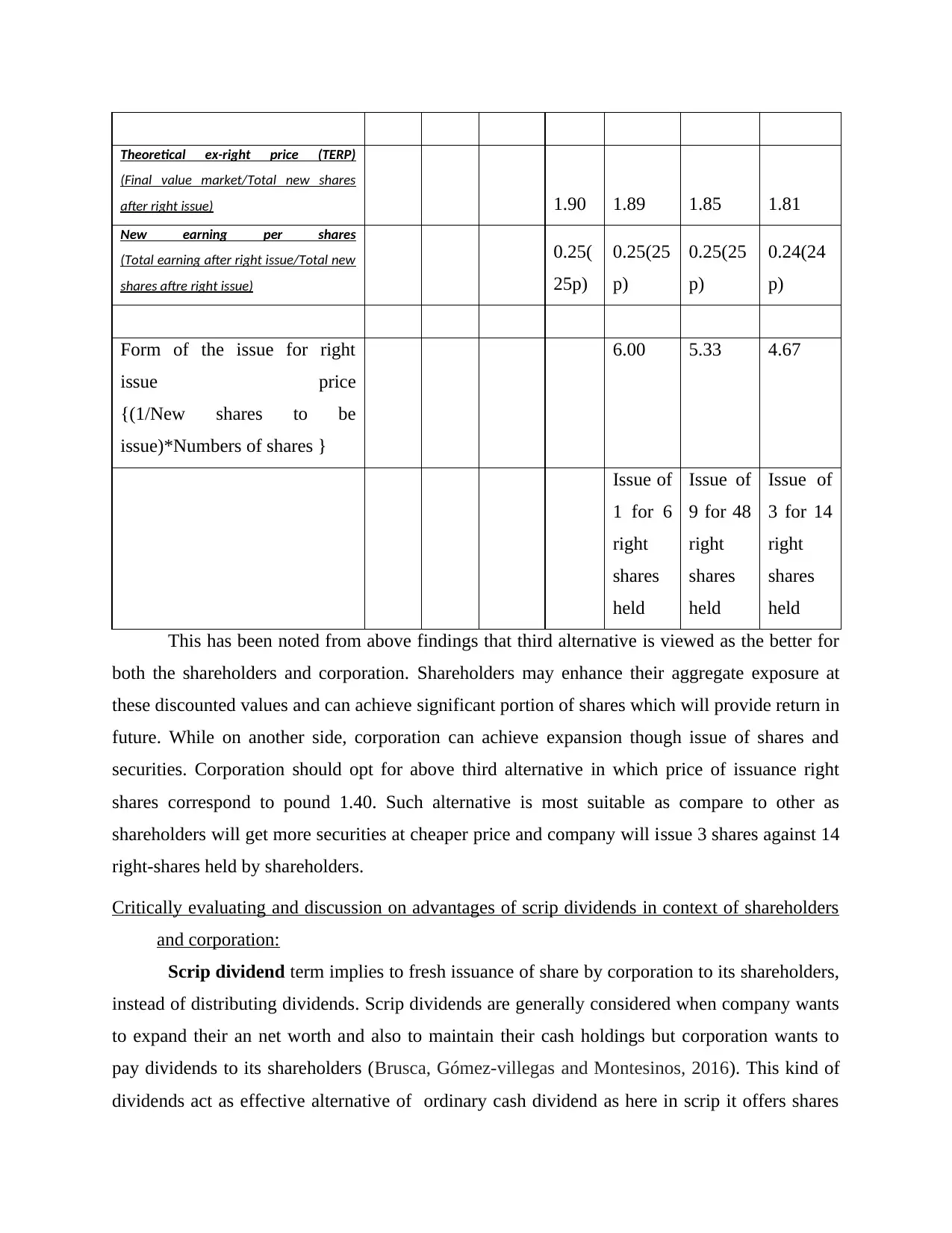

Theoretical ex-right price (TERP)

(Final value market/Total new shares

after right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total new

shares aftre right issue)

0.25(

25p)

0.25(25

p)

0.25(25

p)

0.24(24

p)

Form of the issue for right

issue price

{(1/New shares to be

issue)*Numbers of shares }

6.00 5.33 4.67

Issue of

1 for 6

right

shares

held

Issue of

9 for 48

right

shares

held

Issue of

3 for 14

right

shares

held

This has been noted from above findings that third alternative is viewed as the better for

both the shareholders and corporation. Shareholders may enhance their aggregate exposure at

these discounted values and can achieve significant portion of shares which will provide return in

future. While on another side, corporation can achieve expansion though issue of shares and

securities. Corporation should opt for above third alternative in which price of issuance right

shares correspond to pound 1.40. Such alternative is most suitable as compare to other as

shareholders will get more securities at cheaper price and company will issue 3 shares against 14

right-shares held by shareholders.

Critically evaluating and discussion on advantages of scrip dividends in context of shareholders

and corporation:

Scrip dividend term implies to fresh issuance of share by corporation to its shareholders,

instead of distributing dividends. Scrip dividends are generally considered when company wants

to expand their an net worth and also to maintain their cash holdings but corporation wants to

pay dividends to its shareholders (Brusca, Gómez‐villegas and Montesinos, 2016). This kind of

dividends act as effective alternative of ordinary cash dividend as here in scrip it offers shares

(Final value market/Total new shares

after right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total new

shares aftre right issue)

0.25(

25p)

0.25(25

p)

0.25(25

p)

0.24(24

p)

Form of the issue for right

issue price

{(1/New shares to be

issue)*Numbers of shares }

6.00 5.33 4.67

Issue of

1 for 6

right

shares

held

Issue of

9 for 48

right

shares

held

Issue of

3 for 14

right

shares

held

This has been noted from above findings that third alternative is viewed as the better for

both the shareholders and corporation. Shareholders may enhance their aggregate exposure at

these discounted values and can achieve significant portion of shares which will provide return in

future. While on another side, corporation can achieve expansion though issue of shares and

securities. Corporation should opt for above third alternative in which price of issuance right

shares correspond to pound 1.40. Such alternative is most suitable as compare to other as

shareholders will get more securities at cheaper price and company will issue 3 shares against 14

right-shares held by shareholders.

Critically evaluating and discussion on advantages of scrip dividends in context of shareholders

and corporation:

Scrip dividend term implies to fresh issuance of share by corporation to its shareholders,

instead of distributing dividends. Scrip dividends are generally considered when company wants

to expand their an net worth and also to maintain their cash holdings but corporation wants to

pay dividends to its shareholders (Brusca, Gómez‐villegas and Montesinos, 2016). This kind of

dividends act as effective alternative of ordinary cash dividend as here in scrip it offers shares

option along with cash dividend. Scrip dividends also defined as efficient process of enabling

shareholders with alternative of getting cash dividends or sum of dividend at any future-period.

Scrip dividend, often recognized as liability dividend, being provided by the Corporation to

shareholders in the forms of a certificates rather than an ordinary cash dividend and offers its

shareholders with the option of collecting dividends at later point time or may receive shares

rather than dividends. Industries give such dividends if they don't have enough money to pay-out

as dividends. Scrip Dividends are normally paid by the enterprise in a circumstances in which the

it wishes to issue dividends but the organisation doesn't have adequate cash/monies or liquid

funds to pay-out dividends or it wants to invest available cash-funds towards company's growth,

capital spending/costs or any other specific purposes. However at same point that provides the

bad signal about stock to the investors because shareholder doesn't want to buy stock as they

don't receive cash dividend since they believe their wealth gets diverted and financial condition

of the firm is not really nice and it has cash crunches (Engel and et.al., 2016).

Benefits:

For shareholders-

This kind of dividend offers strength in shareholders and securities holders in corporation

with holding position as well as their voting rights.

Option of shareholding under scrip dividend enables shareholders to enhance their

shareholding with any additional costs.

Selecting of share option at any future date can lead to more yield and profits as compare

to ordinary dividend option on shares.

It advantageous in terms of tax saving because opting for shares option can lead to tax

advantages.

By selling shares obtained in scrip dividend can result in greater profits in comparison to

benefits value of ordinary cash-dividend (Ferguson and Morton-Huddleston, 2016).

For company-

The very first and foremost benefit of scrip dividend is that corporation can save and

maintain cash funds which are available.

Excessive and instant cash out flow due to distribution of dividends can lead to negative

or adverse liquidity position within entity so avoid such adverse circumstance scrip

dividend is most beneficial option.

shareholders with alternative of getting cash dividends or sum of dividend at any future-period.

Scrip dividend, often recognized as liability dividend, being provided by the Corporation to

shareholders in the forms of a certificates rather than an ordinary cash dividend and offers its

shareholders with the option of collecting dividends at later point time or may receive shares

rather than dividends. Industries give such dividends if they don't have enough money to pay-out

as dividends. Scrip Dividends are normally paid by the enterprise in a circumstances in which the

it wishes to issue dividends but the organisation doesn't have adequate cash/monies or liquid

funds to pay-out dividends or it wants to invest available cash-funds towards company's growth,

capital spending/costs or any other specific purposes. However at same point that provides the

bad signal about stock to the investors because shareholder doesn't want to buy stock as they

don't receive cash dividend since they believe their wealth gets diverted and financial condition

of the firm is not really nice and it has cash crunches (Engel and et.al., 2016).

Benefits:

For shareholders-

This kind of dividend offers strength in shareholders and securities holders in corporation

with holding position as well as their voting rights.

Option of shareholding under scrip dividend enables shareholders to enhance their

shareholding with any additional costs.

Selecting of share option at any future date can lead to more yield and profits as compare

to ordinary dividend option on shares.

It advantageous in terms of tax saving because opting for shares option can lead to tax

advantages.

By selling shares obtained in scrip dividend can result in greater profits in comparison to

benefits value of ordinary cash-dividend (Ferguson and Morton-Huddleston, 2016).

For company-

The very first and foremost benefit of scrip dividend is that corporation can save and

maintain cash funds which are available.

Excessive and instant cash out flow due to distribution of dividends can lead to negative

or adverse liquidity position within entity so avoid such adverse circumstance scrip

dividend is most beneficial option.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporation can save significant amount of dividend distribution taxes and expenses, also

shares options under it not lead to heavy share-issue expenses.

Also a company can enhance their capital and net-worth by retaining same cash level and

in quickly manner (Mitchell and Calabrese, 2019).

Drawbacks:

For shareholders-

Major and considerable drawback of a scrip-divided is that shares option herein

dependent upon corporation's future performance which is unpredictable for normal

shareholders. Thus shares price there might be risk of drop in shares price of entity.

Some times proportion of share issue under scrip-divided is not as per expectations of

shareholders.

For shareholders who have selected option of cash-dividend there may be additional tax

liabilities.

In case majority of shareholders/securities holders opting for cash dividend then share

option generally not provide so much benefits due to lower dividend (Muneer, Ahmad

and Ali, 2017).

For company-

Major drawback here for a company is that issuance of shares can lead to distribution of

ownership and business-control.

In normal cases, a company only issues scrip dividend when it is facing and struggling

with cash issues, negative cash-flows or other liquidity issues, so this can lead to negative

image of entity in industry.

Another considerable disadvantage of it is that most of the shareholders after opting

shares option sold out all or significant amount of shares which can often lead to decline

in overall net-worth of corporation (Munge, Kimani and Ngugi, 2016).

So as per above discussion, this has clear that corporation should consider all discussed

advantages and drawbacks carefully before selecting scrip dividend. Further, shareholders should

also determine the viability of scrip dividend options based on above explained benefits and

disadvantages.

shares options under it not lead to heavy share-issue expenses.

Also a company can enhance their capital and net-worth by retaining same cash level and

in quickly manner (Mitchell and Calabrese, 2019).

Drawbacks:

For shareholders-

Major and considerable drawback of a scrip-divided is that shares option herein

dependent upon corporation's future performance which is unpredictable for normal

shareholders. Thus shares price there might be risk of drop in shares price of entity.

Some times proportion of share issue under scrip-divided is not as per expectations of

shareholders.

For shareholders who have selected option of cash-dividend there may be additional tax

liabilities.

In case majority of shareholders/securities holders opting for cash dividend then share

option generally not provide so much benefits due to lower dividend (Muneer, Ahmad

and Ali, 2017).

For company-

Major drawback here for a company is that issuance of shares can lead to distribution of

ownership and business-control.

In normal cases, a company only issues scrip dividend when it is facing and struggling

with cash issues, negative cash-flows or other liquidity issues, so this can lead to negative

image of entity in industry.

Another considerable disadvantage of it is that most of the shareholders after opting

shares option sold out all or significant amount of shares which can often lead to decline

in overall net-worth of corporation (Munge, Kimani and Ngugi, 2016).

So as per above discussion, this has clear that corporation should consider all discussed

advantages and drawbacks carefully before selecting scrip dividend. Further, shareholders should

also determine the viability of scrip dividend options based on above explained benefits and

disadvantages.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MAIN BODY

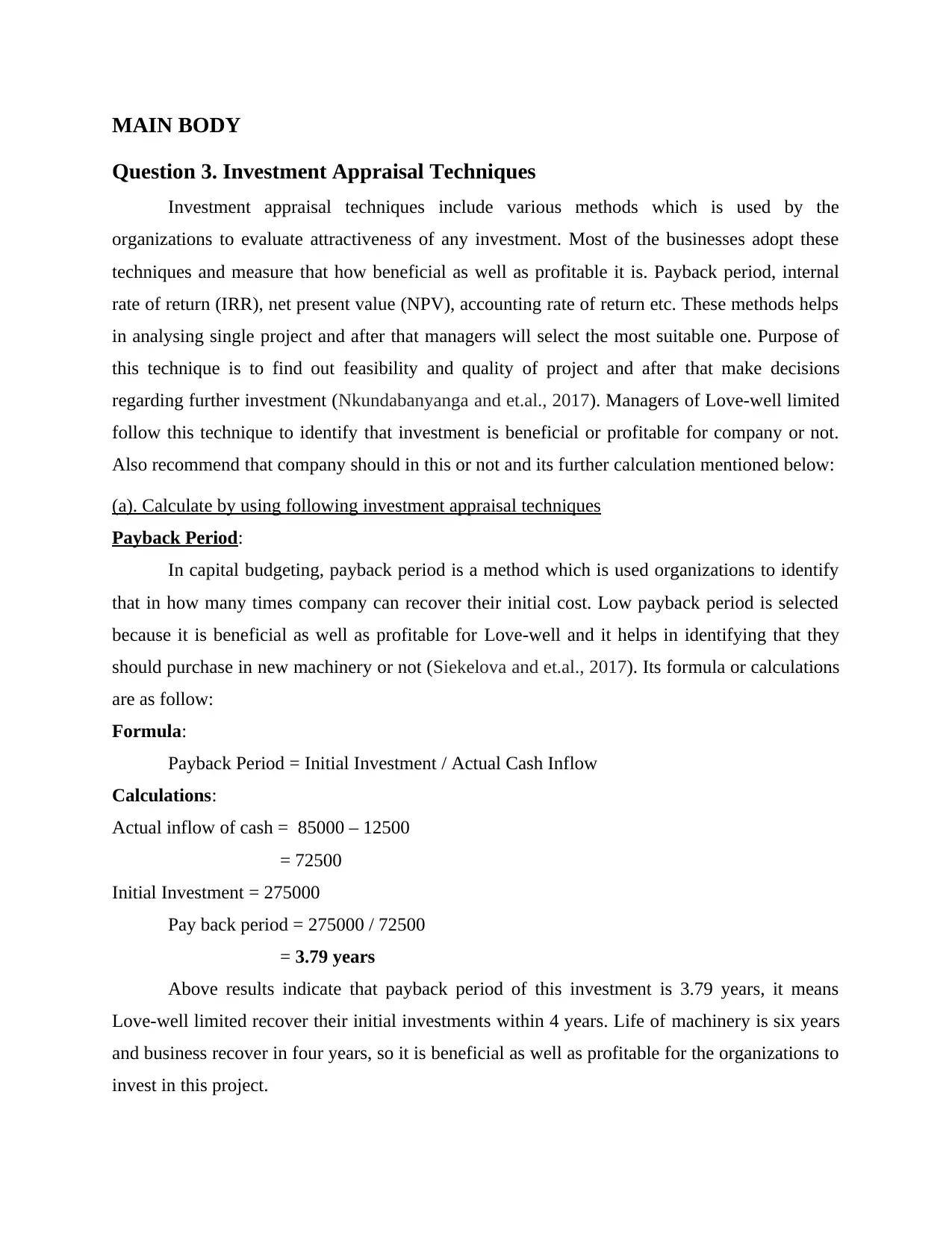

Question 3. Investment Appraisal Techniques

Investment appraisal techniques include various methods which is used by the

organizations to evaluate attractiveness of any investment. Most of the businesses adopt these

techniques and measure that how beneficial as well as profitable it is. Payback period, internal

rate of return (IRR), net present value (NPV), accounting rate of return etc. These methods helps

in analysing single project and after that managers will select the most suitable one. Purpose of

this technique is to find out feasibility and quality of project and after that make decisions

regarding further investment (Nkundabanyanga and et.al., 2017). Managers of Love-well limited

follow this technique to identify that investment is beneficial or profitable for company or not.

Also recommend that company should in this or not and its further calculation mentioned below:

(a). Calculate by using following investment appraisal techniques

Payback Period:

In capital budgeting, payback period is a method which is used organizations to identify

that in how many times company can recover their initial cost. Low payback period is selected

because it is beneficial as well as profitable for Love-well and it helps in identifying that they

should purchase in new machinery or not (Siekelova and et.al., 2017). Its formula or calculations

are as follow:

Formula:

Payback Period = Initial Investment / Actual Cash Inflow

Calculations:

Actual inflow of cash = 85000 – 12500

= 72500

Initial Investment = 275000

Pay back period = 275000 / 72500

= 3.79 years

Above results indicate that payback period of this investment is 3.79 years, it means

Love-well limited recover their initial investments within 4 years. Life of machinery is six years

and business recover in four years, so it is beneficial as well as profitable for the organizations to

invest in this project.

Question 3. Investment Appraisal Techniques

Investment appraisal techniques include various methods which is used by the

organizations to evaluate attractiveness of any investment. Most of the businesses adopt these

techniques and measure that how beneficial as well as profitable it is. Payback period, internal

rate of return (IRR), net present value (NPV), accounting rate of return etc. These methods helps

in analysing single project and after that managers will select the most suitable one. Purpose of

this technique is to find out feasibility and quality of project and after that make decisions

regarding further investment (Nkundabanyanga and et.al., 2017). Managers of Love-well limited

follow this technique to identify that investment is beneficial or profitable for company or not.

Also recommend that company should in this or not and its further calculation mentioned below:

(a). Calculate by using following investment appraisal techniques

Payback Period:

In capital budgeting, payback period is a method which is used organizations to identify

that in how many times company can recover their initial cost. Low payback period is selected

because it is beneficial as well as profitable for Love-well and it helps in identifying that they

should purchase in new machinery or not (Siekelova and et.al., 2017). Its formula or calculations

are as follow:

Formula:

Payback Period = Initial Investment / Actual Cash Inflow

Calculations:

Actual inflow of cash = 85000 – 12500

= 72500

Initial Investment = 275000

Pay back period = 275000 / 72500

= 3.79 years

Above results indicate that payback period of this investment is 3.79 years, it means

Love-well limited recover their initial investments within 4 years. Life of machinery is six years

and business recover in four years, so it is beneficial as well as profitable for the organizations to

invest in this project.

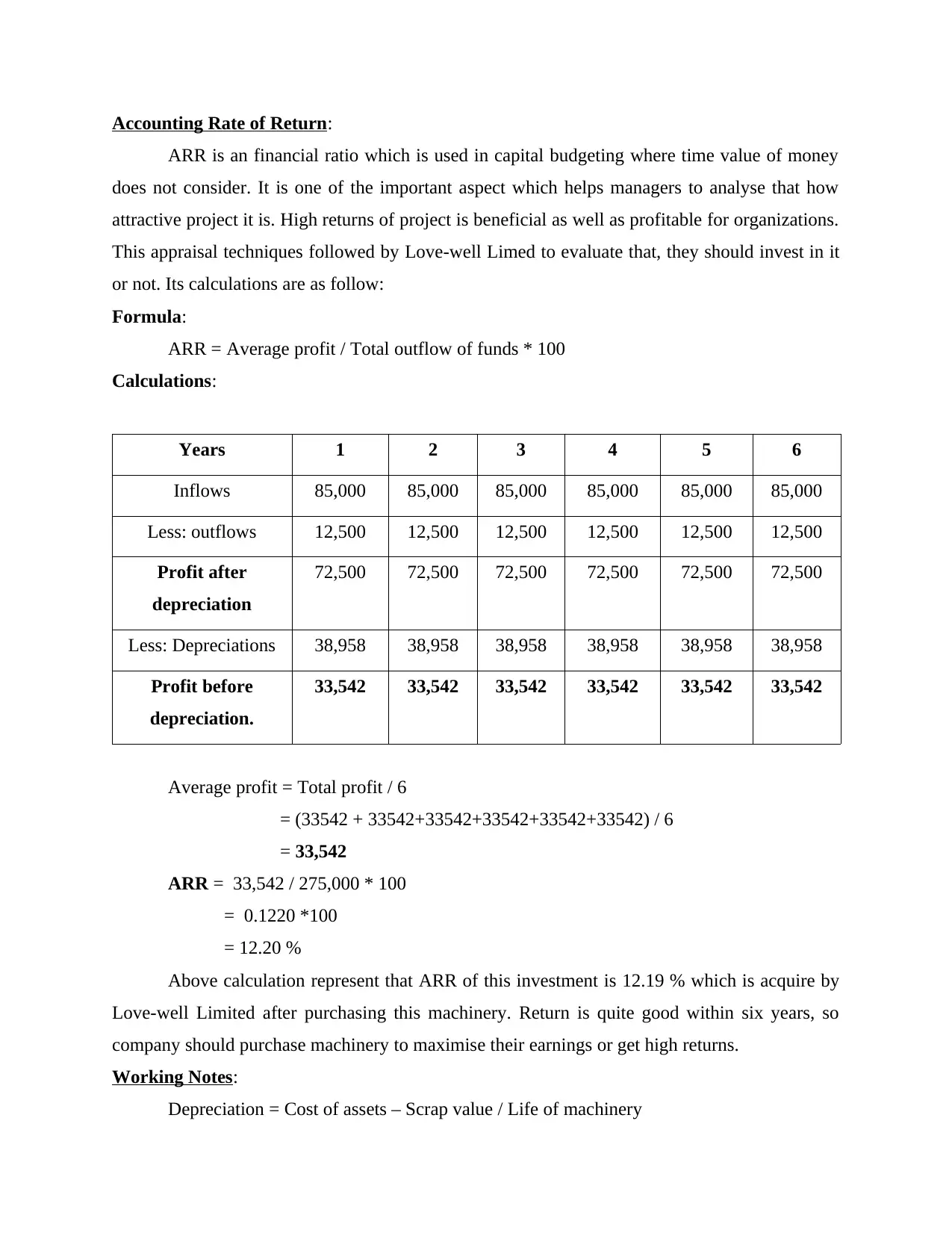

Accounting Rate of Return:

ARR is an financial ratio which is used in capital budgeting where time value of money

does not consider. It is one of the important aspect which helps managers to analyse that how

attractive project it is. High returns of project is beneficial as well as profitable for organizations.

This appraisal techniques followed by Love-well Limed to evaluate that, they should invest in it

or not. Its calculations are as follow:

Formula:

ARR = Average profit / Total outflow of funds * 100

Calculations:

Years 1 2 3 4 5 6

Inflows 85,000 85,000 85,000 85,000 85,000 85,000

Less: outflows 12,500 12,500 12,500 12,500 12,500 12,500

Profit after

depreciation

72,500 72,500 72,500 72,500 72,500 72,500

Less: Depreciations 38,958 38,958 38,958 38,958 38,958 38,958

Profit before

depreciation.

33,542 33,542 33,542 33,542 33,542 33,542

Average profit = Total profit / 6

= (33542 + 33542+33542+33542+33542+33542) / 6

= 33,542

ARR = 33,542 / 275,000 * 100

= 0.1220 *100

= 12.20 %

Above calculation represent that ARR of this investment is 12.19 % which is acquire by

Love-well Limited after purchasing this machinery. Return is quite good within six years, so

company should purchase machinery to maximise their earnings or get high returns.

Working Notes:

Depreciation = Cost of assets – Scrap value / Life of machinery

ARR is an financial ratio which is used in capital budgeting where time value of money

does not consider. It is one of the important aspect which helps managers to analyse that how

attractive project it is. High returns of project is beneficial as well as profitable for organizations.

This appraisal techniques followed by Love-well Limed to evaluate that, they should invest in it

or not. Its calculations are as follow:

Formula:

ARR = Average profit / Total outflow of funds * 100

Calculations:

Years 1 2 3 4 5 6

Inflows 85,000 85,000 85,000 85,000 85,000 85,000

Less: outflows 12,500 12,500 12,500 12,500 12,500 12,500

Profit after

depreciation

72,500 72,500 72,500 72,500 72,500 72,500

Less: Depreciations 38,958 38,958 38,958 38,958 38,958 38,958

Profit before

depreciation.

33,542 33,542 33,542 33,542 33,542 33,542

Average profit = Total profit / 6

= (33542 + 33542+33542+33542+33542+33542) / 6

= 33,542

ARR = 33,542 / 275,000 * 100

= 0.1220 *100

= 12.20 %

Above calculation represent that ARR of this investment is 12.19 % which is acquire by

Love-well Limited after purchasing this machinery. Return is quite good within six years, so

company should purchase machinery to maximise their earnings or get high returns.

Working Notes:

Depreciation = Cost of assets – Scrap value / Life of machinery

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

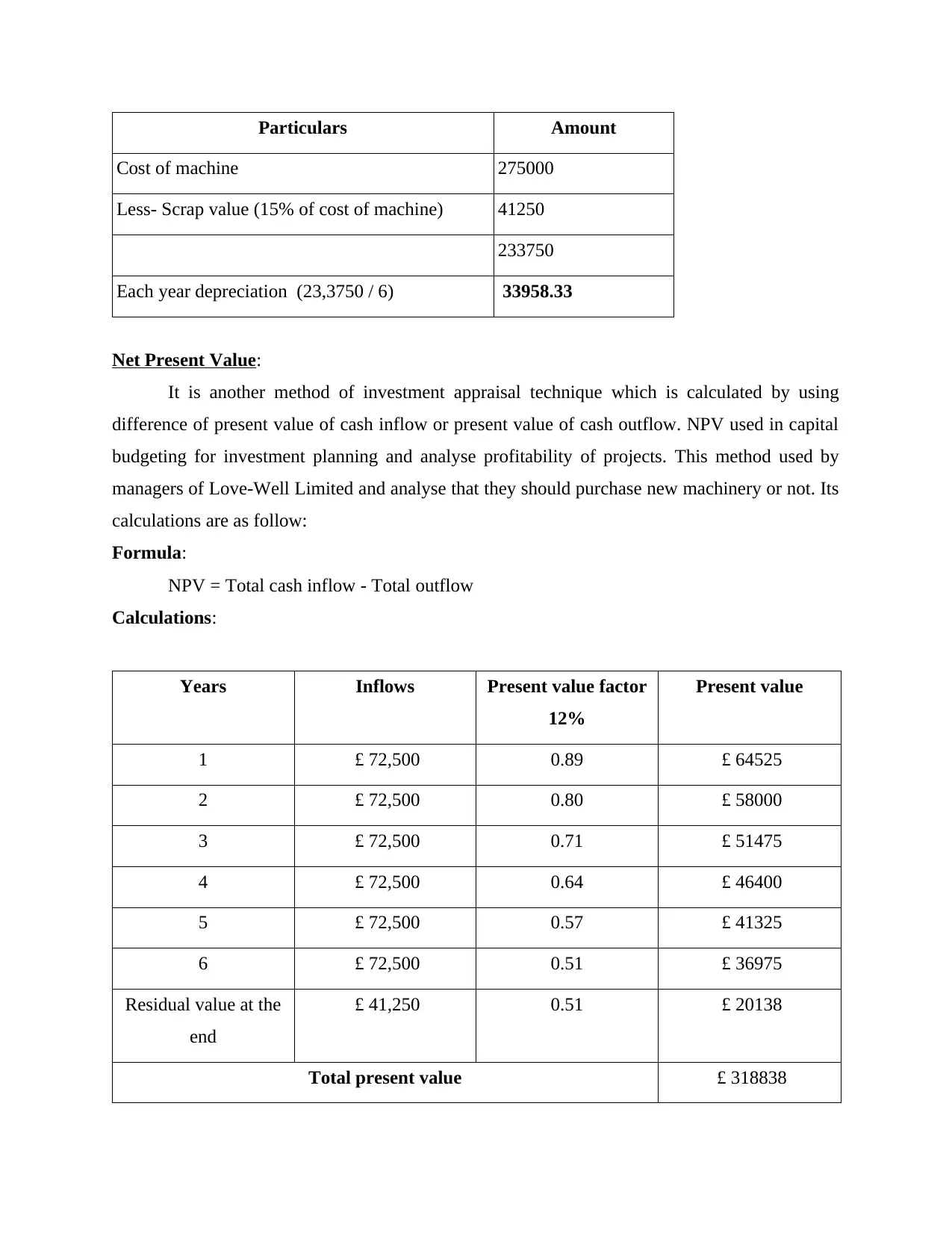

Particulars Amount

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

233750

Each year depreciation (23,3750 / 6) 33958.33

Net Present Value:

It is another method of investment appraisal technique which is calculated by using

difference of present value of cash inflow or present value of cash outflow. NPV used in capital

budgeting for investment planning and analyse profitability of projects. This method used by

managers of Love-Well Limited and analyse that they should purchase new machinery or not. Its

calculations are as follow:

Formula:

NPV = Total cash inflow - Total outflow

Calculations:

Years Inflows Present value factor

12%

Present value

1 £ 72,500 0.89 £ 64525

2 £ 72,500 0.80 £ 58000

3 £ 72,500 0.71 £ 51475

4 £ 72,500 0.64 £ 46400

5 £ 72,500 0.57 £ 41325

6 £ 72,500 0.51 £ 36975

Residual value at the

end

£ 41,250 0.51 £ 20138

Total present value £ 318838

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

233750

Each year depreciation (23,3750 / 6) 33958.33

Net Present Value:

It is another method of investment appraisal technique which is calculated by using

difference of present value of cash inflow or present value of cash outflow. NPV used in capital

budgeting for investment planning and analyse profitability of projects. This method used by

managers of Love-Well Limited and analyse that they should purchase new machinery or not. Its

calculations are as follow:

Formula:

NPV = Total cash inflow - Total outflow

Calculations:

Years Inflows Present value factor

12%

Present value

1 £ 72,500 0.89 £ 64525

2 £ 72,500 0.80 £ 58000

3 £ 72,500 0.71 £ 51475

4 £ 72,500 0.64 £ 46400

5 £ 72,500 0.57 £ 41325

6 £ 72,500 0.51 £ 36975

Residual value at the

end

£ 41,250 0.51 £ 20138

Total present value £ 318838

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

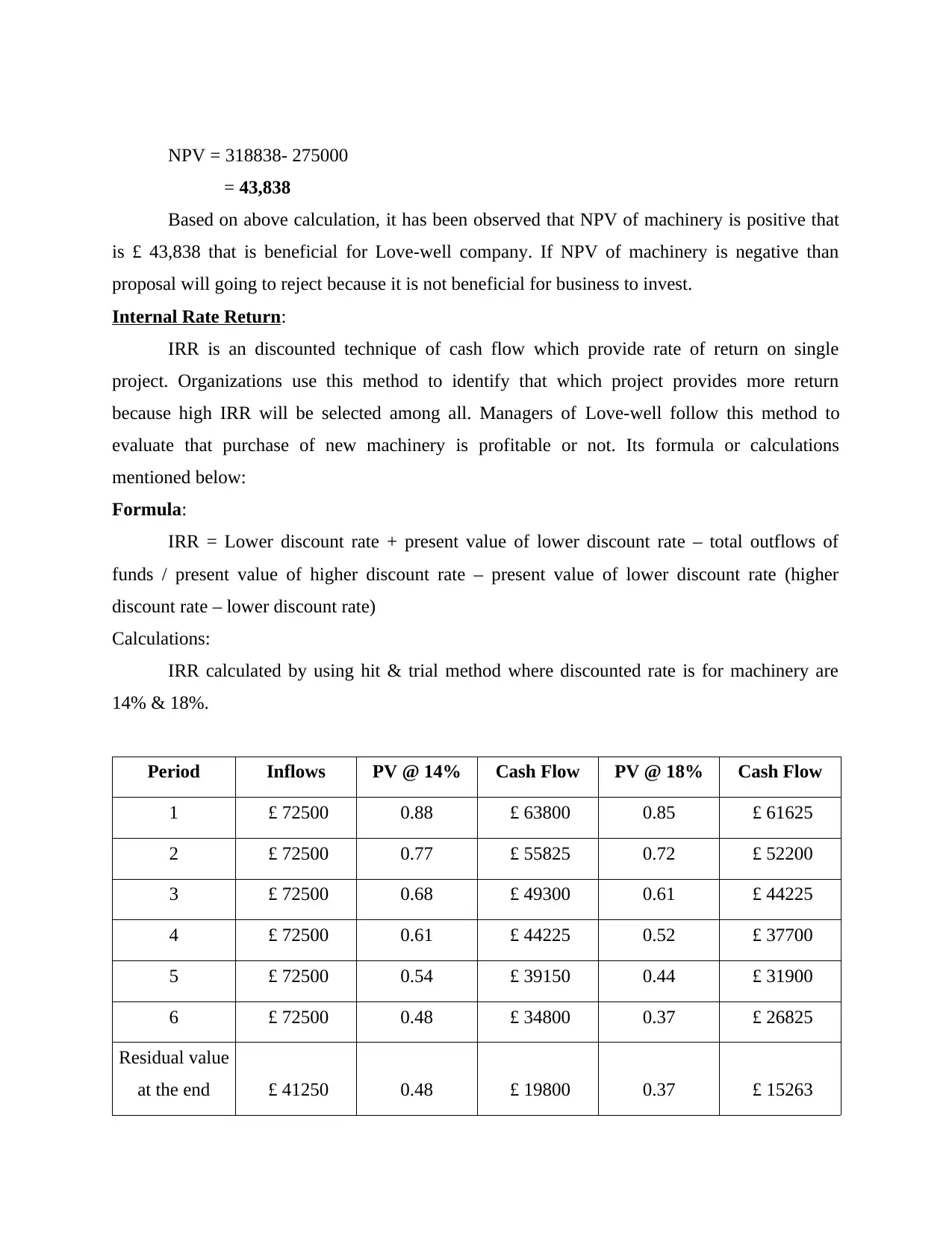

NPV = 318838- 275000

= 43,838

Based on above calculation, it has been observed that NPV of machinery is positive that

is £ 43,838 that is beneficial for Love-well company. If NPV of machinery is negative than

proposal will going to reject because it is not beneficial for business to invest.

Internal Rate Return:

IRR is an discounted technique of cash flow which provide rate of return on single

project. Organizations use this method to identify that which project provides more return

because high IRR will be selected among all. Managers of Love-well follow this method to

evaluate that purchase of new machinery is profitable or not. Its formula or calculations

mentioned below:

Formula:

IRR = Lower discount rate + present value of lower discount rate – total outflows of

funds / present value of higher discount rate – present value of lower discount rate (higher

discount rate – lower discount rate)

Calculations:

IRR calculated by using hit & trial method where discounted rate is for machinery are

14% & 18%.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

1 £ 72500 0.88 £ 63800 0.85 £ 61625

2 £ 72500 0.77 £ 55825 0.72 £ 52200

3 £ 72500 0.68 £ 49300 0.61 £ 44225

4 £ 72500 0.61 £ 44225 0.52 £ 37700

5 £ 72500 0.54 £ 39150 0.44 £ 31900

6 £ 72500 0.48 £ 34800 0.37 £ 26825

Residual value

at the end £ 41250 0.48 £ 19800 0.37 £ 15263

= 43,838

Based on above calculation, it has been observed that NPV of machinery is positive that

is £ 43,838 that is beneficial for Love-well company. If NPV of machinery is negative than

proposal will going to reject because it is not beneficial for business to invest.

Internal Rate Return:

IRR is an discounted technique of cash flow which provide rate of return on single

project. Organizations use this method to identify that which project provides more return

because high IRR will be selected among all. Managers of Love-well follow this method to

evaluate that purchase of new machinery is profitable or not. Its formula or calculations

mentioned below:

Formula:

IRR = Lower discount rate + present value of lower discount rate – total outflows of

funds / present value of higher discount rate – present value of lower discount rate (higher

discount rate – lower discount rate)

Calculations:

IRR calculated by using hit & trial method where discounted rate is for machinery are

14% & 18%.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

1 £ 72500 0.88 £ 63800 0.85 £ 61625

2 £ 72500 0.77 £ 55825 0.72 £ 52200

3 £ 72500 0.68 £ 49300 0.61 £ 44225

4 £ 72500 0.61 £ 44225 0.52 £ 37700

5 £ 72500 0.54 £ 39150 0.44 £ 31900

6 £ 72500 0.48 £ 34800 0.37 £ 26825

Residual value

at the end £ 41250 0.48 £ 19800 0.37 £ 15263

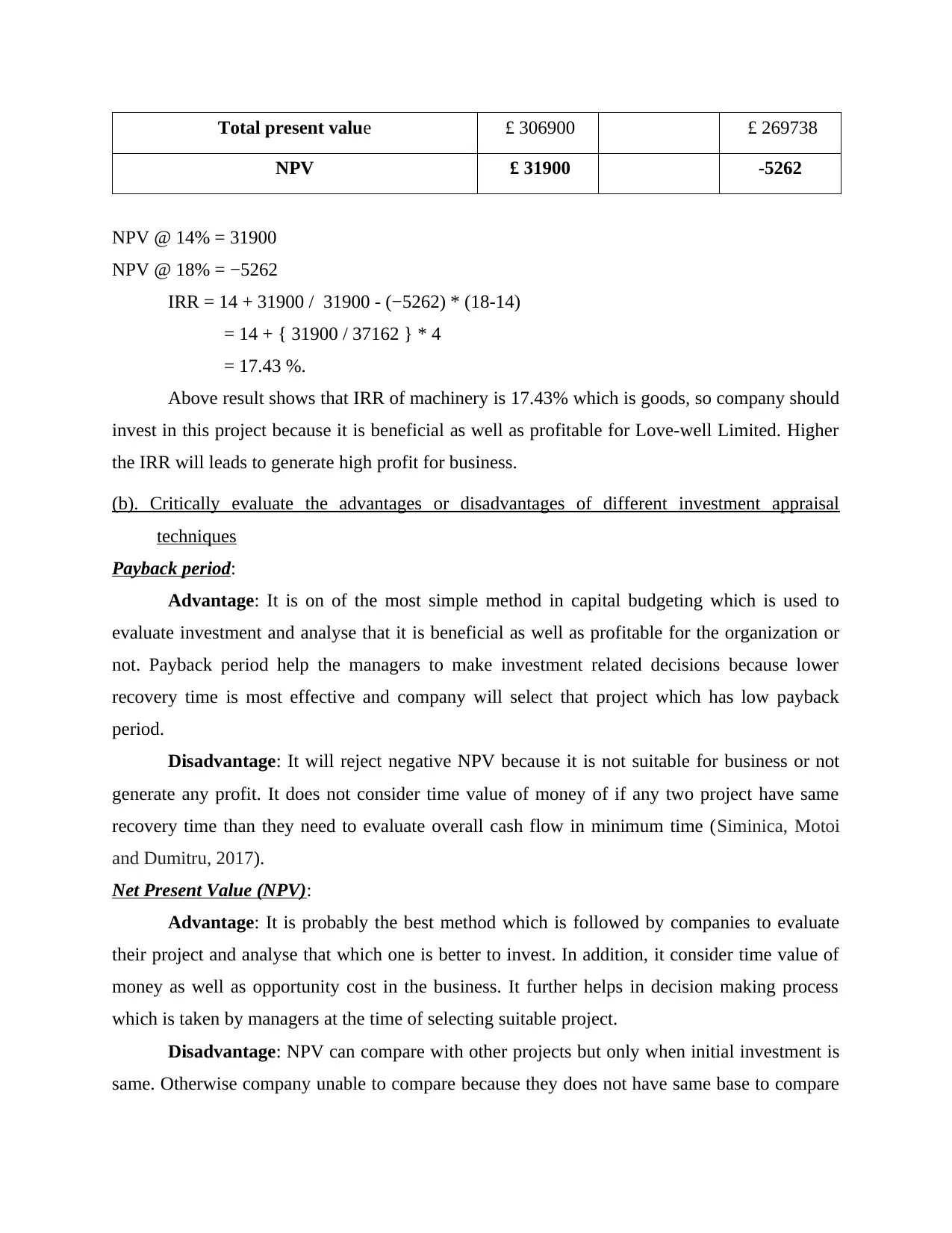

Total present value £ 306900 £ 269738

NPV £ 31900 -5262

NPV @ 14% = 31900

NPV @ 18% = −5262

IRR = 14 + 31900 / 31900 - (−5262) * (18-14)

= 14 + { 31900 / 37162 } * 4

= 17.43 %.

Above result shows that IRR of machinery is 17.43% which is goods, so company should

invest in this project because it is beneficial as well as profitable for Love-well Limited. Higher

the IRR will leads to generate high profit for business.

(b). Critically evaluate the advantages or disadvantages of different investment appraisal

techniques

Payback period:

Advantage: It is on of the most simple method in capital budgeting which is used to

evaluate investment and analyse that it is beneficial as well as profitable for the organization or

not. Payback period help the managers to make investment related decisions because lower

recovery time is most effective and company will select that project which has low payback

period.

Disadvantage: It will reject negative NPV because it is not suitable for business or not

generate any profit. It does not consider time value of money of if any two project have same

recovery time than they need to evaluate overall cash flow in minimum time (Siminica, Motoi

and Dumitru, 2017).

Net Present Value (NPV):

Advantage: It is probably the best method which is followed by companies to evaluate

their project and analyse that which one is better to invest. In addition, it consider time value of

money as well as opportunity cost in the business. It further helps in decision making process

which is taken by managers at the time of selecting suitable project.

Disadvantage: NPV can compare with other projects but only when initial investment is

same. Otherwise company unable to compare because they does not have same base to compare

NPV £ 31900 -5262

NPV @ 14% = 31900

NPV @ 18% = −5262

IRR = 14 + 31900 / 31900 - (−5262) * (18-14)

= 14 + { 31900 / 37162 } * 4

= 17.43 %.

Above result shows that IRR of machinery is 17.43% which is goods, so company should

invest in this project because it is beneficial as well as profitable for Love-well Limited. Higher

the IRR will leads to generate high profit for business.

(b). Critically evaluate the advantages or disadvantages of different investment appraisal

techniques

Payback period:

Advantage: It is on of the most simple method in capital budgeting which is used to

evaluate investment and analyse that it is beneficial as well as profitable for the organization or

not. Payback period help the managers to make investment related decisions because lower

recovery time is most effective and company will select that project which has low payback

period.

Disadvantage: It will reject negative NPV because it is not suitable for business or not

generate any profit. It does not consider time value of money of if any two project have same

recovery time than they need to evaluate overall cash flow in minimum time (Siminica, Motoi

and Dumitru, 2017).

Net Present Value (NPV):

Advantage: It is probably the best method which is followed by companies to evaluate

their project and analyse that which one is better to invest. In addition, it consider time value of

money as well as opportunity cost in the business. It further helps in decision making process

which is taken by managers at the time of selecting suitable project.

Disadvantage: NPV can compare with other projects but only when initial investment is

same. Otherwise company unable to compare because they does not have same base to compare

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.