Equity Securities/Tax and Estate Planning: A Financial Analysis

VerifiedAdded on 2020/03/23

|10

|2212

|74

Homework Assignment

AI Summary

This assignment solution delves into the realm of equity securities and tax and estate planning, covering various financial instruments such as bonds, common stock, and preferred stock, and their associated risks and potential recurring incomes. It includes calculations of Free Cash Flow to the Firm (FCFF) and Free Cash Flow to Equity (FCFE), analyzing the impact of dividend policies and interest rate changes on these metrics. A case study examines property tax calculations for an individual, including income tax and property tax liabilities. The document provides detailed computations and relevant references, offering a comprehensive understanding of the financial concepts discussed.

Running head: EQUITY SECURITIES/TAX AND ESTATE PLANNING

Equity securities/tax and estate planning

Name of the student

Name of the university

Author note

Equity securities/tax and estate planning

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1EQUITY SECURITIES/TAX AND ESTATE PLANNING

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................4

Question 3..................................................................................................................................5

Question 4..................................................................................................................................7

Reference....................................................................................................................................9

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................4

Question 3..................................................................................................................................5

Question 4..................................................................................................................................7

Reference....................................................................................................................................9

2EQUITY SECURITIES/TAX AND ESTATE PLANNING

Question 1

Bond

Bond is also known as the security for fixed income and it is a debt instrument that is

created for raising the capital. The bonds are generally regarded as the loan agreement among

the investor and the issuer of bond where the issuer is obliged to pay certain specific amount

at a specific date in future. When the investor purchases the bond he is loaning the amount to

the issuer who generally raises the amount for any project.

Most common risk associated with the bond is the risk of interest rate that is the risk

that the prices of the bond will fall with the rise in the rates of interest. Through purchase of

the bond, the bondholder commits to receive the fixed rate of return for the fixed term period.

Various other risks associated with the bonds are the default risk, call risk, re-investment risk

and inflation risk. Further, the coupon rate is affected if the interest rate in the market

changed.

Possible recurring incomes from bonds are from 2 ways – interest payment that is

known as the coupon over the lifetime of bond and from price fluctuation that depends on

factors like interest rate (Bodie, 2013).

Common stock

Common stock is the securities that are represented by the equity ownership in any

company, firm or organization. Common stock provides voting rights and enables the holder

to get a share in the profit of the company through capital appreciation and dividend.

However, in case of liquidation the common stock holder gets their right on the asset only

after the preferred stockholders, debt holders and various other debt holders.

Question 1

Bond

Bond is also known as the security for fixed income and it is a debt instrument that is

created for raising the capital. The bonds are generally regarded as the loan agreement among

the investor and the issuer of bond where the issuer is obliged to pay certain specific amount

at a specific date in future. When the investor purchases the bond he is loaning the amount to

the issuer who generally raises the amount for any project.

Most common risk associated with the bond is the risk of interest rate that is the risk

that the prices of the bond will fall with the rise in the rates of interest. Through purchase of

the bond, the bondholder commits to receive the fixed rate of return for the fixed term period.

Various other risks associated with the bonds are the default risk, call risk, re-investment risk

and inflation risk. Further, the coupon rate is affected if the interest rate in the market

changed.

Possible recurring incomes from bonds are from 2 ways – interest payment that is

known as the coupon over the lifetime of bond and from price fluctuation that depends on

factors like interest rate (Bodie, 2013).

Common stock

Common stock is the securities that are represented by the equity ownership in any

company, firm or organization. Common stock provides voting rights and enables the holder

to get a share in the profit of the company through capital appreciation and dividend.

However, in case of liquidation the common stock holder gets their right on the asset only

after the preferred stockholders, debt holders and various other debt holders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3EQUITY SECURITIES/TAX AND ESTATE PLANNING

Various risks associated with common stocks are the investment risk that is the prices

are fluctuating and volatile. Further, there is lack of control as the success of the investor is

dependent on the success of the company. Moreover, there is the risk regarding payment as in

case of liquidation the preferred stock will not get paid till the higher rank of preferred debts

are paid off. The dividend on common stocks is not guaranteed as the company at any time

can eliminate or reduce the payment of dividend (Smith, 2015).

Possible recurring incomes from bonds are from 2 ways – capital gains through

selling the stock of the company and dividend that is paid to the stock holder by the company.

Preferred stock

Like the common stock, the preferred stocks are represented by the equity ownership

in any company, firm or organization. To be more specific, preferred stocks are rights on

earnings and assets. as the name suggests, the preferred stocks carries few advantages like it

gets the priority on getting the payment in case of bankruptcy and dividend. However, as like

the common stock, preferred stock can also be sold and bought through the broker.

Primary risks associated with the preferred stocks are that it is sensitive to the interest

rates similar to the bonds as they pay fixed rate dividend. It is also exposed to industry sector

risk as well as the credit risks. Further, it is associated with the call risk as most of the

preferred shares are allowed to be redeemed on demand even before the date of actual

redemption. Moreover, the dividend will not be pain if the company is not able to earn

enough money to pay as dividend.

Preference stock holder mainly gets recurring incomes through regular dividend

Various risks associated with common stocks are the investment risk that is the prices

are fluctuating and volatile. Further, there is lack of control as the success of the investor is

dependent on the success of the company. Moreover, there is the risk regarding payment as in

case of liquidation the preferred stock will not get paid till the higher rank of preferred debts

are paid off. The dividend on common stocks is not guaranteed as the company at any time

can eliminate or reduce the payment of dividend (Smith, 2015).

Possible recurring incomes from bonds are from 2 ways – capital gains through

selling the stock of the company and dividend that is paid to the stock holder by the company.

Preferred stock

Like the common stock, the preferred stocks are represented by the equity ownership

in any company, firm or organization. To be more specific, preferred stocks are rights on

earnings and assets. as the name suggests, the preferred stocks carries few advantages like it

gets the priority on getting the payment in case of bankruptcy and dividend. However, as like

the common stock, preferred stock can also be sold and bought through the broker.

Primary risks associated with the preferred stocks are that it is sensitive to the interest

rates similar to the bonds as they pay fixed rate dividend. It is also exposed to industry sector

risk as well as the credit risks. Further, it is associated with the call risk as most of the

preferred shares are allowed to be redeemed on demand even before the date of actual

redemption. Moreover, the dividend will not be pain if the company is not able to earn

enough money to pay as dividend.

Preference stock holder mainly gets recurring incomes through regular dividend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4EQUITY SECURITIES/TAX AND ESTATE PLANNING

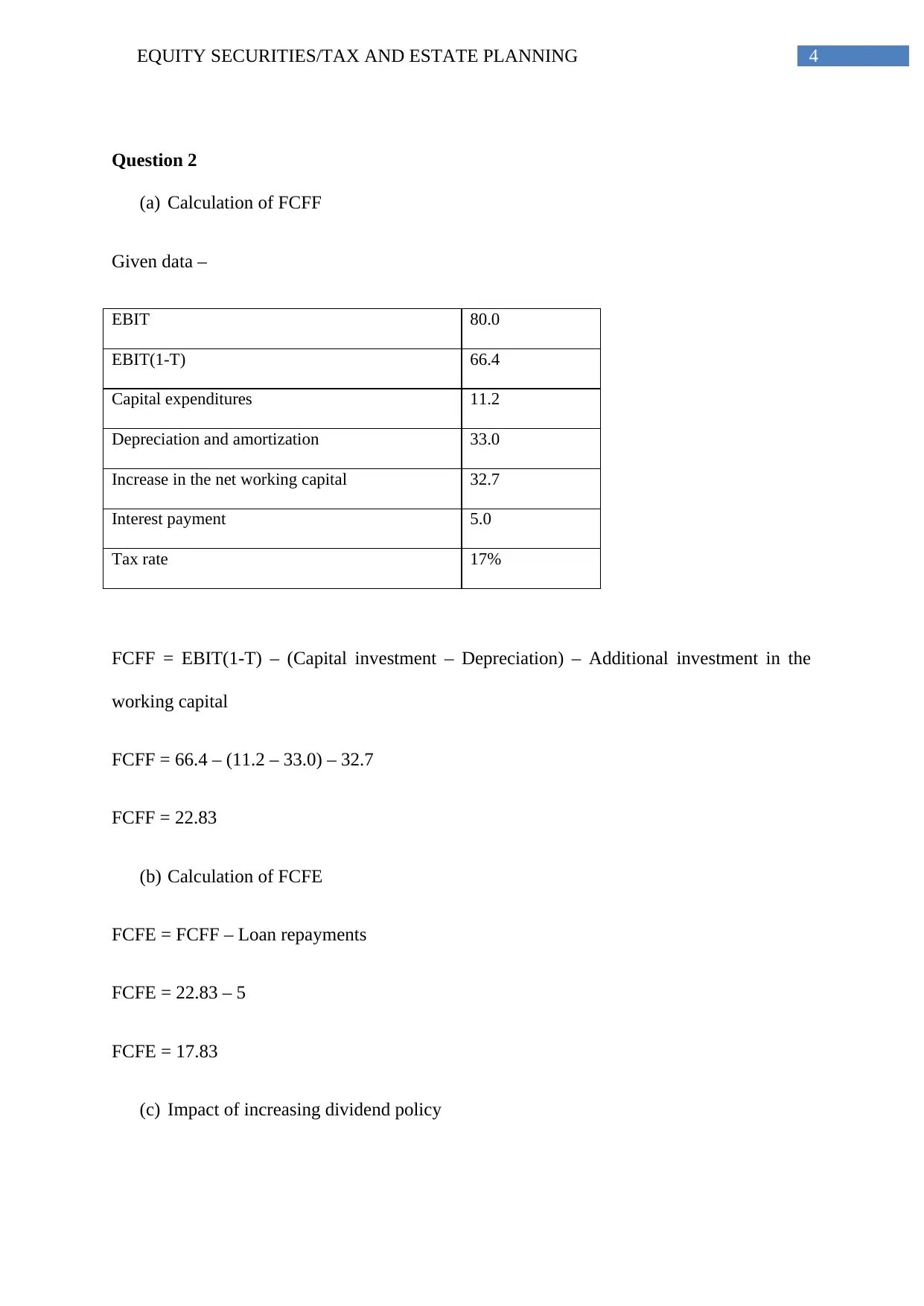

Question 2

(a) Calculation of FCFF

Given data –

EBIT 80.0

EBIT(1-T) 66.4

Capital expenditures 11.2

Depreciation and amortization 33.0

Increase in the net working capital 32.7

Interest payment 5.0

Tax rate 17%

FCFF = EBIT(1-T) – (Capital investment – Depreciation) – Additional investment in the

working capital

FCFF = 66.4 – (11.2 – 33.0) – 32.7

FCFF = 22.83

(b) Calculation of FCFE

FCFE = FCFF – Loan repayments

FCFE = 22.83 – 5

FCFE = 17.83

(c) Impact of increasing dividend policy

Question 2

(a) Calculation of FCFF

Given data –

EBIT 80.0

EBIT(1-T) 66.4

Capital expenditures 11.2

Depreciation and amortization 33.0

Increase in the net working capital 32.7

Interest payment 5.0

Tax rate 17%

FCFF = EBIT(1-T) – (Capital investment – Depreciation) – Additional investment in the

working capital

FCFF = 66.4 – (11.2 – 33.0) – 32.7

FCFF = 22.83

(b) Calculation of FCFE

FCFE = FCFF – Loan repayments

FCFE = 22.83 – 5

FCFE = 17.83

(c) Impact of increasing dividend policy

5EQUITY SECURITIES/TAX AND ESTATE PLANNING

On FCFF – The FCFF is free cash flow to the organization. Therefore, it involves all the free

cash flows to the bond holders and the equity owners. However, if the company increases the

payments of dividend, the equity owners will have more flow of cash from the dividends

whereas they will be able to get less flow of cash from other sources. Bond holders will not

be affected as the net dividends or incomes are not attributable to the bond holders (Pinto et

al., 2013). Further, the entire cash flow to the bond holders as well as the equity owners will

not change.

On FCFE – it is the free cash flow that is attributable to the equity. Therefore, it is quite

obvious that it includes all the free cash flows to the equity owners containing the payments

for dividends (Pinto et al., 2015). However, if the company increases the payment for

dividends, the cash flow from other sources may reduce. Further, the total flow for free cash

to the equity owners will not be affected.

Question 3

Impact on FCFF and FCFE due to interest rate change

FCFF that is the free cash flow of any firm is the measure for the financial

performance that states the total amount of cash generated for a company after taxes,

expenses and the changes in investment and net working capital are deducted. On the other

hand, the FCFE that is the free cash flow to the equity is the measure to analyse the amount

of cash that can be distributed to equity shareholders of any company in form of stock

buybacks or dividend after meeting all the expenses, debt repayments and reinvestment. The

FCFE is also known as the levered free cash flow (Kumar, 2015).

The FCFF can be calculated using the cash flow from the operations (CFO) or the net

income. The computation of FCFF through CFO is same as the computation of FCF as the

On FCFF – The FCFF is free cash flow to the organization. Therefore, it involves all the free

cash flows to the bond holders and the equity owners. However, if the company increases the

payments of dividend, the equity owners will have more flow of cash from the dividends

whereas they will be able to get less flow of cash from other sources. Bond holders will not

be affected as the net dividends or incomes are not attributable to the bond holders (Pinto et

al., 2013). Further, the entire cash flow to the bond holders as well as the equity owners will

not change.

On FCFE – it is the free cash flow that is attributable to the equity. Therefore, it is quite

obvious that it includes all the free cash flows to the equity owners containing the payments

for dividends (Pinto et al., 2015). However, if the company increases the payment for

dividends, the cash flow from other sources may reduce. Further, the total flow for free cash

to the equity owners will not be affected.

Question 3

Impact on FCFF and FCFE due to interest rate change

FCFF that is the free cash flow of any firm is the measure for the financial

performance that states the total amount of cash generated for a company after taxes,

expenses and the changes in investment and net working capital are deducted. On the other

hand, the FCFE that is the free cash flow to the equity is the measure to analyse the amount

of cash that can be distributed to equity shareholders of any company in form of stock

buybacks or dividend after meeting all the expenses, debt repayments and reinvestment. The

FCFE is also known as the levered free cash flow (Kumar, 2015).

The FCFF can be calculated using the cash flow from the operations (CFO) or the net

income. The computation of FCFF through CFO is same as the computation of FCF as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6EQUITY SECURITIES/TAX AND ESTATE PLANNING

FCFF is that cash flow which is distributed to the investors containing the debt holders and

interest expenses is the cash that is the cash available to the debt holders shall be added back.

While valuing any firm, the FCF is to be calculated over number of years. Therefore,

it is likely that the firma can change their financing policies during these long periods. Owing

to this, the impact on the cash flow of required to be considered in the even t of changes in

the financial policy. The analysts generally takes into consideration the factor that operation

cost of the firm is likely to be changed. They take into account the factors like increase in the

material cost, increase in the wages and the inflation (Kaviani, 2013).

Impact on FCFF – the total borrowing whether increased or paid back does not have any

impact on the FCFF as the FCFF measures the cash flow created in the business and

borrowing is not created in the business and therefore, the net effect of borrowing is zero

(Rubio, 2015).

Impact on FCFE – the borrowing has an impact on FCFE as it is the cash that can be

distributed to the shareholder if the management wishes so. However, unlike the company,

that has to pay off the borrowing, equities do not have to pay off the borrowings and it is

generally paid by from the operational cash flow (Alberro, 2015). Therefore, as the firm

borrows money it becomes available to the equity which in turn increases the FCFE

(Mielcarz & Mlinarič, 2014). More the borrowings more the burden of interest and where no

new borrowings are there, the firm has to pay the interest only. However, when the borrowing

is paid back it will reduce the FCFE.

FCFF is that cash flow which is distributed to the investors containing the debt holders and

interest expenses is the cash that is the cash available to the debt holders shall be added back.

While valuing any firm, the FCF is to be calculated over number of years. Therefore,

it is likely that the firma can change their financing policies during these long periods. Owing

to this, the impact on the cash flow of required to be considered in the even t of changes in

the financial policy. The analysts generally takes into consideration the factor that operation

cost of the firm is likely to be changed. They take into account the factors like increase in the

material cost, increase in the wages and the inflation (Kaviani, 2013).

Impact on FCFF – the total borrowing whether increased or paid back does not have any

impact on the FCFF as the FCFF measures the cash flow created in the business and

borrowing is not created in the business and therefore, the net effect of borrowing is zero

(Rubio, 2015).

Impact on FCFE – the borrowing has an impact on FCFE as it is the cash that can be

distributed to the shareholder if the management wishes so. However, unlike the company,

that has to pay off the borrowing, equities do not have to pay off the borrowings and it is

generally paid by from the operational cash flow (Alberro, 2015). Therefore, as the firm

borrows money it becomes available to the equity which in turn increases the FCFE

(Mielcarz & Mlinarič, 2014). More the borrowings more the burden of interest and where no

new borrowings are there, the firm has to pay the interest only. However, when the borrowing

is paid back it will reduce the FCFE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7EQUITY SECURITIES/TAX AND ESTATE PLANNING

Question 4

Case study on Mr and Mrs Anthony Chan Soon Thoong

Property tax is the tax on the property ownership. Further, it is not the tax on income

that applies tax on the income from rent received by the property owner. Property tax

becomes payable by all the owners of the property on property they own, irrespective of the

fact that the property is occupied by the owner, let or or left vacant by the owner. However, if

the property is leased, the tax on income is collected on rental income apart from the charges

of property tax at the rate of 10% on the annual value. Further, if the property is occupied by

the owner, the concessionary rate of tax can be claimed. At present the rate of tax on property

is 10% of the annual value of property with the concessionary rate ranged from 0 to 6% for

the homes occupied by the owner (Surico & Trezzi, 2015). During 2013, the rebate with

regard to HDB property tax was $ 40. Further, from 1st Jan 2014, the rate of tax on property

shifted to the progressive system that is the Residential Property Tax Annual Value and it

was effective from 1st Jan 2014.

Computation of net tax payable by Anthony

Computation of income from employment and trade

Particulars Amount

Income

Bonus for 5 months $ 35,000.00

Relevant course study $ 8,000.00

Exempt as incurred to enhance income $ (8,000.00)

income from selling the books $ 12,500.00

Dividend received on stock portfolio $ 4,300.00

Total income of Anthony $ 51,800.00

Tax applicable

1st 20,000 $ -

Next 10,000 @ 2% $ 200.00

Next 10,000 @ 3.5% $ 350.00

On balance amount $ 7% $ 826.00

Question 4

Case study on Mr and Mrs Anthony Chan Soon Thoong

Property tax is the tax on the property ownership. Further, it is not the tax on income

that applies tax on the income from rent received by the property owner. Property tax

becomes payable by all the owners of the property on property they own, irrespective of the

fact that the property is occupied by the owner, let or or left vacant by the owner. However, if

the property is leased, the tax on income is collected on rental income apart from the charges

of property tax at the rate of 10% on the annual value. Further, if the property is occupied by

the owner, the concessionary rate of tax can be claimed. At present the rate of tax on property

is 10% of the annual value of property with the concessionary rate ranged from 0 to 6% for

the homes occupied by the owner (Surico & Trezzi, 2015). During 2013, the rebate with

regard to HDB property tax was $ 40. Further, from 1st Jan 2014, the rate of tax on property

shifted to the progressive system that is the Residential Property Tax Annual Value and it

was effective from 1st Jan 2014.

Computation of net tax payable by Anthony

Computation of income from employment and trade

Particulars Amount

Income

Bonus for 5 months $ 35,000.00

Relevant course study $ 8,000.00

Exempt as incurred to enhance income $ (8,000.00)

income from selling the books $ 12,500.00

Dividend received on stock portfolio $ 4,300.00

Total income of Anthony $ 51,800.00

Tax applicable

1st 20,000 $ -

Next 10,000 @ 2% $ 200.00

Next 10,000 @ 3.5% $ 350.00

On balance amount $ 7% $ 826.00

8EQUITY SECURITIES/TAX AND ESTATE PLANNING

Total income tax payable $ 1,376.00

Computation of property tax

Particulars Amount

Value of property $ 1,100,000.00

Tax applicable

1st 8,000 @ 0% $ -

next 47,0000 @ 4% $ 1,880.00

next 15,000 @ 6% $ 900.00

next 15,000 @ 8% $ 1,200.00

Next 15,000 @ 10% $ 1,500.00

Next 15000 @ 12% $ 1,800.00

Next 15000 @ 14% $ 2,100.00

Balance amount @ 16% $ 155,200.00

Total property tax payable $ 164,580.00

Total tax payable by Anthony $ 165,956.00

Note – Childcare relief is assumed to be availed by Mr. Anthony’s wife Janet as she is also

working and can file his return separately.

In case of mortgage, Anthony will be liable to pay the stamp duty on the mortgage

value.

In case of sale of the property, the conveyancing lawyer will notify the new owner

and the tax will be shared equally by Anthony and new owner. Therefore, Anthony will be

liable to pay = 1,376 +(164,580*50%) = $ 83,666

Total income tax payable $ 1,376.00

Computation of property tax

Particulars Amount

Value of property $ 1,100,000.00

Tax applicable

1st 8,000 @ 0% $ -

next 47,0000 @ 4% $ 1,880.00

next 15,000 @ 6% $ 900.00

next 15,000 @ 8% $ 1,200.00

Next 15,000 @ 10% $ 1,500.00

Next 15000 @ 12% $ 1,800.00

Next 15000 @ 14% $ 2,100.00

Balance amount @ 16% $ 155,200.00

Total property tax payable $ 164,580.00

Total tax payable by Anthony $ 165,956.00

Note – Childcare relief is assumed to be availed by Mr. Anthony’s wife Janet as she is also

working and can file his return separately.

In case of mortgage, Anthony will be liable to pay the stamp duty on the mortgage

value.

In case of sale of the property, the conveyancing lawyer will notify the new owner

and the tax will be shared equally by Anthony and new owner. Therefore, Anthony will be

liable to pay = 1,376 +(164,580*50%) = $ 83,666

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9EQUITY SECURITIES/TAX AND ESTATE PLANNING

Reference

Alberro, J. (2015). Estimating Damages Using DCF: From Free Cash Flow to the Firm to

Free Cash Flow to Equity (and Back). ICSID Review-Foreign Investment Law

Journal, 30(3), 689-698.

Bodie, Z. (2013). Investments. McGraw-Hill.

Kaviani, M. (2013). Study of information content economic value added in explain new

models based on free cash flow (CVFCFF and CVFCFE). International Journal of

Accounting and Financial Reporting, 3(1), 277.

Kumar, R. (2015). Valuation: Theories and concepts. Academic Press.

Mielcarz, P., & Mlinarič, F. (2014). The superiority of FCFF over EVA and FCFE in capital

budgeting. Economic Research-Ekonomska Istraživanja, 27(1), 559-572.

Pinto, J. E., Henry, E., Robinson, T. R., & Stowe, J. D. (2015). Equity asset valuation. John

Wiley & Sons.

Pinto, J., Robinson, T. R., Rath, R. D., & ASA, C. (2013). Equity Valuation.

Rubio, A. (2015). How to Consider Excess Cash in Firm Valuation. Browser Download This

Paper.

Smith, E. L. (2015). Common stocks as long term investments. Pickle Partners Publishing.

Surico, P., & Trezzi, R. (2015). Consumer Spending and Property Taxes.

Reference

Alberro, J. (2015). Estimating Damages Using DCF: From Free Cash Flow to the Firm to

Free Cash Flow to Equity (and Back). ICSID Review-Foreign Investment Law

Journal, 30(3), 689-698.

Bodie, Z. (2013). Investments. McGraw-Hill.

Kaviani, M. (2013). Study of information content economic value added in explain new

models based on free cash flow (CVFCFF and CVFCFE). International Journal of

Accounting and Financial Reporting, 3(1), 277.

Kumar, R. (2015). Valuation: Theories and concepts. Academic Press.

Mielcarz, P., & Mlinarič, F. (2014). The superiority of FCFF over EVA and FCFE in capital

budgeting. Economic Research-Ekonomska Istraživanja, 27(1), 559-572.

Pinto, J. E., Henry, E., Robinson, T. R., & Stowe, J. D. (2015). Equity asset valuation. John

Wiley & Sons.

Pinto, J., Robinson, T. R., Rath, R. D., & ASA, C. (2013). Equity Valuation.

Rubio, A. (2015). How to Consider Excess Cash in Firm Valuation. Browser Download This

Paper.

Smith, E. L. (2015). Common stocks as long term investments. Pickle Partners Publishing.

Surico, P., & Trezzi, R. (2015). Consumer Spending and Property Taxes.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.