Ernst & Young Global Limited: Accounting's Role and Budgeting Impact

VerifiedAdded on 2023/07/13

|42

|9411

|406

Report

AI Summary

This report delves into the critical role of accounting within Ernst & Young Global Limited (EY) in the United Kingdom, examining its purpose and scope in complex operating environments. It highlights the accounting function's significance in informing decision-making, meeting stakeholder expectations, and addressing ethical, legal, and compliance issues. The report covers the main branches of accounting, required job skillsets, and the integration of technology in modern accounting systems. Furthermore, it includes a memorandum detailing cash budgeting exercises, analyzing changes in the master budget under various scenarios, and discussing the benefits and limitations of budgetary planning and control. The analysis provides insights into how budgets facilitate effective resource planning and control within an organization like EY.

TABLE OF CONTENTS

INTRODUCTION................................................................................................................3

About Ernst & Young Global Limited (EY) in United Kingdom.........................................3

1. The role of accounting in an organization........................................................................4

1.1. The purpose accounting in complex operating environments....................................4

1.2. The scope of accounting in complex operating environments...................................5

1.2.1. Individual............................................................................................................5

1.2.2. Business organizations........................................................................................5

1.2.3. Non-profit organizations.....................................................................................6

1.2.4. Government organizations..................................................................................6

1.2.5. Non-profit organizations.....................................................................................6

1.3. The accounting function in informing decision-making and meeting stakeholder and

societal needs and expectations........................................................................................6

1.3.1.An evaluation of the environment and objectives of an organization's accounting

function.........................................................................................................................7

1.4. The main branches of accounting and job skillsets and competencies.......................8

1.5. Accounting systems and the role of technology in modern-day accounting............11

1.6. The organization's ethical, legal, and compliance issues.........................................12

2. Memorandum.................................................................................................................15

2.1. Cash budgeting........................................................................................................15

2.1.1. Preparing a cash budget for the company..........................................................15

2.2. Analyzing the change in the master budget.........................................................20

2.2.1. Scenario 1.........................................................................................................20

2.2.2. Scenario 2.........................................................................................................23

2.2.3. Scenario 3.........................................................................................................26

2.2.4. Scenario 4.........................................................................................................29

1

INTRODUCTION................................................................................................................3

About Ernst & Young Global Limited (EY) in United Kingdom.........................................3

1. The role of accounting in an organization........................................................................4

1.1. The purpose accounting in complex operating environments....................................4

1.2. The scope of accounting in complex operating environments...................................5

1.2.1. Individual............................................................................................................5

1.2.2. Business organizations........................................................................................5

1.2.3. Non-profit organizations.....................................................................................6

1.2.4. Government organizations..................................................................................6

1.2.5. Non-profit organizations.....................................................................................6

1.3. The accounting function in informing decision-making and meeting stakeholder and

societal needs and expectations........................................................................................6

1.3.1.An evaluation of the environment and objectives of an organization's accounting

function.........................................................................................................................7

1.4. The main branches of accounting and job skillsets and competencies.......................8

1.5. Accounting systems and the role of technology in modern-day accounting............11

1.6. The organization's ethical, legal, and compliance issues.........................................12

2. Memorandum.................................................................................................................15

2.1. Cash budgeting........................................................................................................15

2.1.1. Preparing a cash budget for the company..........................................................15

2.2. Analyzing the change in the master budget.........................................................20

2.2.1. Scenario 1.........................................................................................................20

2.2.2. Scenario 2.........................................................................................................23

2.2.3. Scenario 3.........................................................................................................26

2.2.4. Scenario 4.........................................................................................................29

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3. The role that budgets play in the effective planning and control of resources in an

organization....................................................................................................................32

2.3.1. The benefits of budgets, budgetary planning, and control for an organization.. 32

2.3.2. The limitation of budgets, budgetary planning, and control for an organization.

.................................................................................................................................... 32

2.4. An outline of a range of budgetary control solutions...............................................33

CONCLUSION.................................................................................................................. 35

REFERENCES...............................................................................................................36

2

organization....................................................................................................................32

2.3.1. The benefits of budgets, budgetary planning, and control for an organization.. 32

2.3.2. The limitation of budgets, budgetary planning, and control for an organization.

.................................................................................................................................... 32

2.4. An outline of a range of budgetary control solutions...............................................33

CONCLUSION.................................................................................................................. 35

REFERENCES...............................................................................................................36

2

LIST OF TABLES AND FIGURES

Figure 1. The main branches of accounting.....................................................................................10

Table 1. Schedule of expected cash collection................................................................................16

Table 2. Schedule of expected merchandise purchases...................................................................17

Table 3. Schedule of expected cash disbursements for merchandise purchases..............................18

Table 4. Schedule of expected cash disbursement for selling and administrative expenses...........19

Table 5. Schedule of expected cash budget.....................................................................................21

Table 6. Schedule of cash collection of Scenario 1.........................................................................22

Table 7. Variance of Scenario 1.......................................................................................................23

Table 8. Schedule of cash budget of Scenario 1..............................................................................24

Table 9. Schedule of cash disbursements for merchandise purchases of Scenario 2.......................25

Table 10. Schedule of cash collection of Scenario 2.......................................................................26

Table 11. Schedule of cash disburse for selling and administrative expenses of Scenario 2..........27

Table 12. Schedule of cash disbursements for merchandise purchases of Scenario 3.....................29

Table 13. Schedule of expected cash disburse for selling and administrative expenses.................30

Table 14. Schedule of expected cash disbursements for merchandise purchases of Scenario 4.....31

Table 15. Schedule of expected cash disburse for selling and administrative.................................33

3

Figure 1. The main branches of accounting.....................................................................................10

Table 1. Schedule of expected cash collection................................................................................16

Table 2. Schedule of expected merchandise purchases...................................................................17

Table 3. Schedule of expected cash disbursements for merchandise purchases..............................18

Table 4. Schedule of expected cash disbursement for selling and administrative expenses...........19

Table 5. Schedule of expected cash budget.....................................................................................21

Table 6. Schedule of cash collection of Scenario 1.........................................................................22

Table 7. Variance of Scenario 1.......................................................................................................23

Table 8. Schedule of cash budget of Scenario 1..............................................................................24

Table 9. Schedule of cash disbursements for merchandise purchases of Scenario 2.......................25

Table 10. Schedule of cash collection of Scenario 2.......................................................................26

Table 11. Schedule of cash disburse for selling and administrative expenses of Scenario 2..........27

Table 12. Schedule of cash disbursements for merchandise purchases of Scenario 3.....................29

Table 13. Schedule of expected cash disburse for selling and administrative expenses.................30

Table 14. Schedule of expected cash disbursements for merchandise purchases of Scenario 4.....31

Table 15. Schedule of expected cash disburse for selling and administrative.................................33

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

About Ernst & Young Global Limited (EY) in United Kingdom

A worldwide professional services firm called Ernst & Young Global Limited (EY) has

certainly done considerable business consulting for its clients. They have a main office in

central London and regional offices in Birmingham and Southampton in the UK. The

group's revenue for the year was clear: it was £200 million, with 25% of that coming from

markets outside the UK, mainly in Southeast Asia. In Singapore, they have a small

regional office. The business also has a policy of accepting smaller customers when they

feel there is potential for rapid growth. Ernst & Young Global Limited's goal is to create a

better working environment. The skilled workers and top services they provide contribute

to the growth of confidence and confidence in financial markets and economic

fundamentals worldwide.

I recently started working for the company as a Graduate Trainee in their UK SME

(Small and Medium Enterprises) Unit, which provides accounting and financial services to

companies that typically have a turnover between £0.5 million and £15 million. I have

been invited to participate in some exercises as part of continuous training.

4

About Ernst & Young Global Limited (EY) in United Kingdom

A worldwide professional services firm called Ernst & Young Global Limited (EY) has

certainly done considerable business consulting for its clients. They have a main office in

central London and regional offices in Birmingham and Southampton in the UK. The

group's revenue for the year was clear: it was £200 million, with 25% of that coming from

markets outside the UK, mainly in Southeast Asia. In Singapore, they have a small

regional office. The business also has a policy of accepting smaller customers when they

feel there is potential for rapid growth. Ernst & Young Global Limited's goal is to create a

better working environment. The skilled workers and top services they provide contribute

to the growth of confidence and confidence in financial markets and economic

fundamentals worldwide.

I recently started working for the company as a Graduate Trainee in their UK SME

(Small and Medium Enterprises) Unit, which provides accounting and financial services to

companies that typically have a turnover between £0.5 million and £15 million. I have

been invited to participate in some exercises as part of continuous training.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. The role of accounting in an organization

The aim of this online blog is to promote and market EY accounting services to new and

existing clients. “The role of accounting in the organization” focuses mainly on the

following objective:

the purpose and scope of accounting in complex operating environments

the accounting function in informing decision-making and meeting stakeholder and

societal needs and expectations

the main branches of accounting and job skillsets and competencies

accounting systems and the role of technology in modern-day accounting

issues of ethics, regulation, and compliance and the extent to which they are

constraints or threats to the organization.

Earlier than we dive into the significance of accounting in business, let’s cowl the basics

– what's accounting? "Accounting is a service provided for those who need information on

an entity's financial performance and its financial position", defined by Dyson and

Franklin (2020). From this definition of accounting, we could understand that accounting a

service activity, is the process of identifying, measuring, and communicating economic

information to permit informed judgment and decision by users of the information.

1.1. The purpose accounting in complex operating environments

First, like any other created service, accounting serves its purpose, which is to provide

quantitative information about economic institutions that are essentially financial and

designed to be useful in making economic decisions. The preparation of financial

statements that provide information about the company is the primary goal of financial

accounting. Within the laws and regulations of a given country, financial accounting is

performed according to generally accepted accounting principles (GAAP) in the United

States and International Accounting Standards Board(IASB)/ International Financial

Reporting Standards(IFRS) in all other countries. Accounting is a tool to support

5

The aim of this online blog is to promote and market EY accounting services to new and

existing clients. “The role of accounting in the organization” focuses mainly on the

following objective:

the purpose and scope of accounting in complex operating environments

the accounting function in informing decision-making and meeting stakeholder and

societal needs and expectations

the main branches of accounting and job skillsets and competencies

accounting systems and the role of technology in modern-day accounting

issues of ethics, regulation, and compliance and the extent to which they are

constraints or threats to the organization.

Earlier than we dive into the significance of accounting in business, let’s cowl the basics

– what's accounting? "Accounting is a service provided for those who need information on

an entity's financial performance and its financial position", defined by Dyson and

Franklin (2020). From this definition of accounting, we could understand that accounting a

service activity, is the process of identifying, measuring, and communicating economic

information to permit informed judgment and decision by users of the information.

1.1. The purpose accounting in complex operating environments

First, like any other created service, accounting serves its purpose, which is to provide

quantitative information about economic institutions that are essentially financial and

designed to be useful in making economic decisions. The preparation of financial

statements that provide information about the company is the primary goal of financial

accounting. Within the laws and regulations of a given country, financial accounting is

performed according to generally accepted accounting principles (GAAP) in the United

States and International Accounting Standards Board(IASB)/ International Financial

Reporting Standards(IFRS) in all other countries. Accounting is a tool to support

5

management. It is a system that records financial transactions and checks them to generate

reports on the financial and operating status of an economic entity.

The information regulator receives the data it needs to make decisions through the

accounting process. Interested parties, both internal and external to the organization,

request this information. In addition, the main scope of accounting is very wide due to

social needs and economic and monetary developments; it includes both for-profit and

non-profit organizations as well as governments and individuals. Accounting is widely

used in the field of business it is called the phrase "The language of business". Every

company takes profit as the top goal. To determine the operating results and financial

position of a business, financial transactions are recorded in the accounting books.

Also, a common misconception is that the field of accounting is primarily concerned

with the financial activities of commercial enterprises. But practically every type of

business, including individuals and families, needs an accountant. In addition, they

perform some kind of accounting to collect financial data and make financial decisions on

their own. The scope of accounting also exists in governments. These companies use

accounting systems for a number of functions, including income and expense calculations

as well as efficient administrative management.

1.2 The scope of accounting in complex operating environments

1.2.1. Individual

Accounting is the process of collecting, recording, and analyzing financial transactions.

You can use your accounting skills to apply them to your personal or daily life. For

individuals, accountants help in calculating tax payable, income, bills, etc. In addition,

they engage in some financial activities to generate income. In order for them to make

judgments, accountants provide them with access to personal financial data.

1.2.2. Business organizations

The scope of accounting in business organization is a very broad field and their

financial accountants produce some important company documents and have profit and

loss statements. Financial accounting in a business also creates a balance sheet that

6

reports on the financial and operating status of an economic entity.

The information regulator receives the data it needs to make decisions through the

accounting process. Interested parties, both internal and external to the organization,

request this information. In addition, the main scope of accounting is very wide due to

social needs and economic and monetary developments; it includes both for-profit and

non-profit organizations as well as governments and individuals. Accounting is widely

used in the field of business it is called the phrase "The language of business". Every

company takes profit as the top goal. To determine the operating results and financial

position of a business, financial transactions are recorded in the accounting books.

Also, a common misconception is that the field of accounting is primarily concerned

with the financial activities of commercial enterprises. But practically every type of

business, including individuals and families, needs an accountant. In addition, they

perform some kind of accounting to collect financial data and make financial decisions on

their own. The scope of accounting also exists in governments. These companies use

accounting systems for a number of functions, including income and expense calculations

as well as efficient administrative management.

1.2 The scope of accounting in complex operating environments

1.2.1. Individual

Accounting is the process of collecting, recording, and analyzing financial transactions.

You can use your accounting skills to apply them to your personal or daily life. For

individuals, accountants help in calculating tax payable, income, bills, etc. In addition,

they engage in some financial activities to generate income. In order for them to make

judgments, accountants provide them with access to personal financial data.

1.2.2. Business organizations

The scope of accounting in business organization is a very broad field and their

financial accountants produce some important company documents and have profit and

loss statements. Financial accounting in a business also creates a balance sheet that

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provides valuable information to the business about its assets, liabilities, and equity at a

particular point in time. Without these financial accounting documents, it would be very

difficult to run the business organization. Therefore, the field of accounting in business

organizations is very important.

1.2.3. Non-profit organizations

Non-governmental organizations are included in the scope of accounting. The object of

accounting in nonprofit organizations is to do good for members through reasonable clarity

about the cost of their money. These organizations keep track of all their financial

transactions, including membership fees, gifts, and other spending. The audience of the

organizations are clubs, schools, hospitals, mosques and other non-profit organizations all

associated with accounting. To achieve this, reports including balance sheet, income and

expense accounts, income and expenditure accounts are prepared according to accounting

regulations.

1.2.4. Government organizations

Government agencies always need accounting to achieve accountability goals, financial

information must be relevant and reliable for the reasonable users of the information.

Government agencies always need accounting information to help with planning,

budgeting, and apportionment of government funds. Organizations must execute a national

plan, devise a financial strategy, assess a nation's growth or decline, and conduct a variety

of other tasks.

1.2.5. Non-profit organizations

An important role of accountants in a business is to ensure the quality of financial

statements. Therefore, the scope of accounting in the specialty is very large and wide.

Sometimes professionals like doctors, engineers have to pay taxes on their income. In

addition, they want financial data to understand their financial statements and invest or

save money. For this reason, they must take their income into account. Therefore, their

account holding system is different from business institutions.

7

particular point in time. Without these financial accounting documents, it would be very

difficult to run the business organization. Therefore, the field of accounting in business

organizations is very important.

1.2.3. Non-profit organizations

Non-governmental organizations are included in the scope of accounting. The object of

accounting in nonprofit organizations is to do good for members through reasonable clarity

about the cost of their money. These organizations keep track of all their financial

transactions, including membership fees, gifts, and other spending. The audience of the

organizations are clubs, schools, hospitals, mosques and other non-profit organizations all

associated with accounting. To achieve this, reports including balance sheet, income and

expense accounts, income and expenditure accounts are prepared according to accounting

regulations.

1.2.4. Government organizations

Government agencies always need accounting to achieve accountability goals, financial

information must be relevant and reliable for the reasonable users of the information.

Government agencies always need accounting information to help with planning,

budgeting, and apportionment of government funds. Organizations must execute a national

plan, devise a financial strategy, assess a nation's growth or decline, and conduct a variety

of other tasks.

1.2.5. Non-profit organizations

An important role of accountants in a business is to ensure the quality of financial

statements. Therefore, the scope of accounting in the specialty is very large and wide.

Sometimes professionals like doctors, engineers have to pay taxes on their income. In

addition, they want financial data to understand their financial statements and invest or

save money. For this reason, they must take their income into account. Therefore, their

account holding system is different from business institutions.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 The accounting function in informing decision-making and meeting stakeholder and

societal needs and expectations.

We need to understand first that the ultimate aim of accounting is to provide financial

statements to organizations (Dyson & Ellie, 2010). To assist users in decision making,

financial statements will provide both internal and external users with a summary of

financial performance and financial position such as providing investors, regulators

creditors and creditors. While the management accounting system is aimed at internal

decision-makers such as managers, to critically appreciate the role of accounting in

providing information to the decision-making process to meet the needs and organization's

expectations. To perform that function, the accounting function may need to work with

other parts of the organization, such as the purchasing function, the production function,

the marketing function, the sales function, and the sales function, sales ability, supply

capacity, and service level (Kosinski, 2021).

1.3.1.An evaluation of the environment and objectives of an organization's accounting

function.

Management accountants will be tasked with gathering information and providing data

for these options. They will highlight additional factors that need to be taken into account

before making a final decision, even though the information they provide is primarily

financial in nature (Dyson & Ellie, 2010). In other words, owners and managers rely on

accounting information to analyze and check the performance and position of

organizations. In a for-profit organization, the accounting function also interacts with other

business functions. In the purchasing function, accountants take into account finding credit

terms, setting prices to be paid for goods and services, making payments, gathering data,

and inventory details. Firstly, in the manufacturing function, the accounting department

will consult with the purchasing department to help with sourcing at economical prices and

optimal quality. Second, the production department determines the relationship between

factors and the quantity of inputs for production and the number of goods it produces most

efficiently. Another functional area that accountants will have to work with is the

marketing department. Third, the accounting department assists the marketing department

8

societal needs and expectations.

We need to understand first that the ultimate aim of accounting is to provide financial

statements to organizations (Dyson & Ellie, 2010). To assist users in decision making,

financial statements will provide both internal and external users with a summary of

financial performance and financial position such as providing investors, regulators

creditors and creditors. While the management accounting system is aimed at internal

decision-makers such as managers, to critically appreciate the role of accounting in

providing information to the decision-making process to meet the needs and organization's

expectations. To perform that function, the accounting function may need to work with

other parts of the organization, such as the purchasing function, the production function,

the marketing function, the sales function, and the sales function, sales ability, supply

capacity, and service level (Kosinski, 2021).

1.3.1.An evaluation of the environment and objectives of an organization's accounting

function.

Management accountants will be tasked with gathering information and providing data

for these options. They will highlight additional factors that need to be taken into account

before making a final decision, even though the information they provide is primarily

financial in nature (Dyson & Ellie, 2010). In other words, owners and managers rely on

accounting information to analyze and check the performance and position of

organizations. In a for-profit organization, the accounting function also interacts with other

business functions. In the purchasing function, accountants take into account finding credit

terms, setting prices to be paid for goods and services, making payments, gathering data,

and inventory details. Firstly, in the manufacturing function, the accounting department

will consult with the purchasing department to help with sourcing at economical prices and

optimal quality. Second, the production department determines the relationship between

factors and the quantity of inputs for production and the number of goods it produces most

efficiently. Another functional area that accountants will have to work with is the

marketing department. Third, the accounting department assists the marketing department

8

in setting the budget and determining if it is cost-effective. It answers questions about

marginal productivity, the level of production, and the cheapest mode of production of

goods. Finally, there are a number of issues where the accounting department needs to

cooperate in providing a service, such as establishing a service charge rate, providing an

estimate of the costs incurred in providing the service, and estimating the cost of the

service. additional benefits for customers.

1.3.2. A critical of the accounting function's role in guiding decision-making and

satisfying stakeholders' and society's requirements and expectations.

The accounting process provides direct managers with a thorough view of the financial

statements, the evolution of the financial position, the performance of the organization, its

capabilities and risks. Financial accounting is important in helping organizations keep

track of all their financial activities. It is the process by which companies collect and report

financial data in and out of their organizations, helping both company management as well

as outside investors and analysts understand the health of the company. company and

make informed decisions (Vu Thi Hoai Anh, 2021).

According to The Investopedia Team (2021), fundamental analysis relies heavily on

accounting data recorded on a company's financial records, such as balance sheets, income

statements, and cash flow statements. bad. It is regulated by the Financial Accounting

Standards Board (FASB) and it is registered with the Securities and Exchange

Commission (SEC). Jawahar (2009) has found that published financial statements are

almost certainly more helpful in forecasting future performance, which is of course the

primary concern of investing. It contains statistics on human capital. Therefore, according

to Kren (1992) accounting data is usually separated into two categories: data that support

decision-making, which is mainly used for internal cooperation of the company, and data

that affects decision-making and is primarily used by corporate management. It is clear

from the comments made in the aforementioned studies that financial accounting and

financial information should always be used before, during and after the decision-making

process. Although the above opinions are slightly different, everyone agrees that

accounting information is important to an organization's decision making because it

provides authentic information based on the activities and company reviews.

9

marginal productivity, the level of production, and the cheapest mode of production of

goods. Finally, there are a number of issues where the accounting department needs to

cooperate in providing a service, such as establishing a service charge rate, providing an

estimate of the costs incurred in providing the service, and estimating the cost of the

service. additional benefits for customers.

1.3.2. A critical of the accounting function's role in guiding decision-making and

satisfying stakeholders' and society's requirements and expectations.

The accounting process provides direct managers with a thorough view of the financial

statements, the evolution of the financial position, the performance of the organization, its

capabilities and risks. Financial accounting is important in helping organizations keep

track of all their financial activities. It is the process by which companies collect and report

financial data in and out of their organizations, helping both company management as well

as outside investors and analysts understand the health of the company. company and

make informed decisions (Vu Thi Hoai Anh, 2021).

According to The Investopedia Team (2021), fundamental analysis relies heavily on

accounting data recorded on a company's financial records, such as balance sheets, income

statements, and cash flow statements. bad. It is regulated by the Financial Accounting

Standards Board (FASB) and it is registered with the Securities and Exchange

Commission (SEC). Jawahar (2009) has found that published financial statements are

almost certainly more helpful in forecasting future performance, which is of course the

primary concern of investing. It contains statistics on human capital. Therefore, according

to Kren (1992) accounting data is usually separated into two categories: data that support

decision-making, which is mainly used for internal cooperation of the company, and data

that affects decision-making and is primarily used by corporate management. It is clear

from the comments made in the aforementioned studies that financial accounting and

financial information should always be used before, during and after the decision-making

process. Although the above opinions are slightly different, everyone agrees that

accounting information is important to an organization's decision making because it

provides authentic information based on the activities and company reviews.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In summary, Patrick (2020) recognizes that the success of organizations depends on the

data collected. The information collected will serve as the basis for any business decisions

made by your senior management. To ensure proper and efficient implementation of your

new platform, it is important to follow the procedures outlined above. In short, having a

well-developed and maintained accounting information system will provide you with

efficient and accurate data, which is a key component of a successful business.

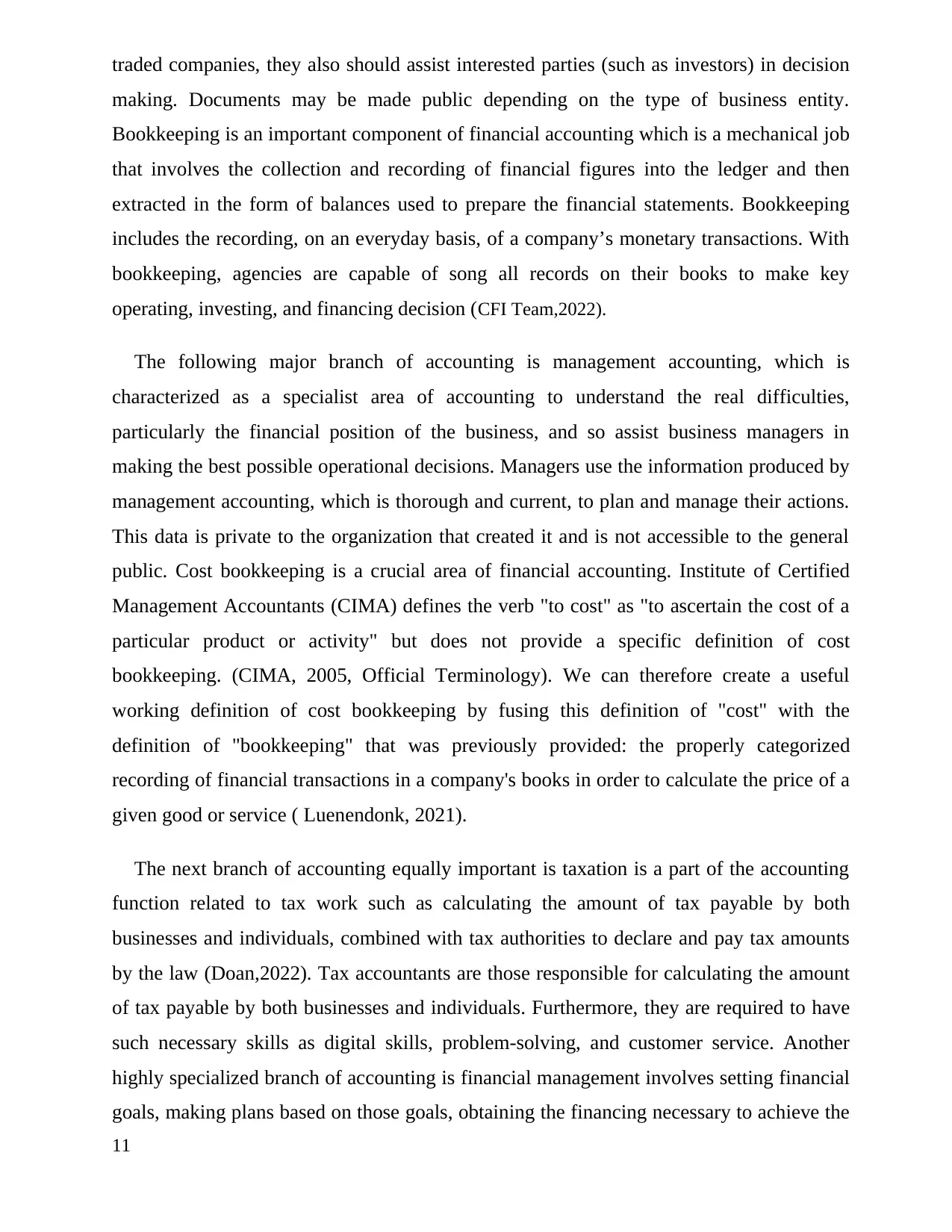

1.4. The main branches of accounting and job skillsets and competencies.

The main branches of accounting are financial accounting and reporting, management

accounting, auditing, tax accounting, financial management, and bankruptcy and

liquidation or insolvency or forensic accounting.

Figure 1. The main branches of accounting

To begin with, a financial accountant is a process of recording, analyzing, summarizing,

and reporting financial data (Doan,2022). This specific job requires such important skills

as digital skills, strong accounting ethics, and teamwork to incorporate functions within the

entity. Managers prepare income statements and summary balance sheets as formal

statement of the management of the resources entrusted to them, but in the case of publicly

10

data collected. The information collected will serve as the basis for any business decisions

made by your senior management. To ensure proper and efficient implementation of your

new platform, it is important to follow the procedures outlined above. In short, having a

well-developed and maintained accounting information system will provide you with

efficient and accurate data, which is a key component of a successful business.

1.4. The main branches of accounting and job skillsets and competencies.

The main branches of accounting are financial accounting and reporting, management

accounting, auditing, tax accounting, financial management, and bankruptcy and

liquidation or insolvency or forensic accounting.

Figure 1. The main branches of accounting

To begin with, a financial accountant is a process of recording, analyzing, summarizing,

and reporting financial data (Doan,2022). This specific job requires such important skills

as digital skills, strong accounting ethics, and teamwork to incorporate functions within the

entity. Managers prepare income statements and summary balance sheets as formal

statement of the management of the resources entrusted to them, but in the case of publicly

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

traded companies, they also should assist interested parties (such as investors) in decision

making. Documents may be made public depending on the type of business entity.

Bookkeeping is an important component of financial accounting which is a mechanical job

that involves the collection and recording of financial figures into the ledger and then

extracted in the form of balances used to prepare the financial statements. Bookkeeping

includes the recording, on an everyday basis, of a company’s monetary transactions. With

bookkeeping, agencies are capable of song all records on their books to make key

operating, investing, and financing decision (CFI Team,2022).

The following major branch of accounting is management accounting, which is

characterized as a specialist area of accounting to understand the real difficulties,

particularly the financial position of the business, and so assist business managers in

making the best possible operational decisions. Managers use the information produced by

management accounting, which is thorough and current, to plan and manage their actions.

This data is private to the organization that created it and is not accessible to the general

public. Cost bookkeeping is a crucial area of financial accounting. Institute of Certified

Management Accountants (CIMA) defines the verb "to cost" as "to ascertain the cost of a

particular product or activity" but does not provide a specific definition of cost

bookkeeping. (CIMA, 2005, Official Terminology). We can therefore create a useful

working definition of cost bookkeeping by fusing this definition of "cost" with the

definition of "bookkeeping" that was previously provided: the properly categorized

recording of financial transactions in a company's books in order to calculate the price of a

given good or service ( Luenendonk, 2021).

The next branch of accounting equally important is taxation is a part of the accounting

function related to tax work such as calculating the amount of tax payable by both

businesses and individuals, combined with tax authorities to declare and pay tax amounts

by the law (Doan,2022). Tax accountants are those responsible for calculating the amount

of tax payable by both businesses and individuals. Furthermore, they are required to have

such necessary skills as digital skills, problem-solving, and customer service. Another

highly specialized branch of accounting is financial management involves setting financial

goals, making plans based on those goals, obtaining the financing necessary to achieve the

11

making. Documents may be made public depending on the type of business entity.

Bookkeeping is an important component of financial accounting which is a mechanical job

that involves the collection and recording of financial figures into the ledger and then

extracted in the form of balances used to prepare the financial statements. Bookkeeping

includes the recording, on an everyday basis, of a company’s monetary transactions. With

bookkeeping, agencies are capable of song all records on their books to make key

operating, investing, and financing decision (CFI Team,2022).

The following major branch of accounting is management accounting, which is

characterized as a specialist area of accounting to understand the real difficulties,

particularly the financial position of the business, and so assist business managers in

making the best possible operational decisions. Managers use the information produced by

management accounting, which is thorough and current, to plan and manage their actions.

This data is private to the organization that created it and is not accessible to the general

public. Cost bookkeeping is a crucial area of financial accounting. Institute of Certified

Management Accountants (CIMA) defines the verb "to cost" as "to ascertain the cost of a

particular product or activity" but does not provide a specific definition of cost

bookkeeping. (CIMA, 2005, Official Terminology). We can therefore create a useful

working definition of cost bookkeeping by fusing this definition of "cost" with the

definition of "bookkeeping" that was previously provided: the properly categorized

recording of financial transactions in a company's books in order to calculate the price of a

given good or service ( Luenendonk, 2021).

The next branch of accounting equally important is taxation is a part of the accounting

function related to tax work such as calculating the amount of tax payable by both

businesses and individuals, combined with tax authorities to declare and pay tax amounts

by the law (Doan,2022). Tax accountants are those responsible for calculating the amount

of tax payable by both businesses and individuals. Furthermore, they are required to have

such necessary skills as digital skills, problem-solving, and customer service. Another

highly specialized branch of accounting is financial management involves setting financial

goals, making plans based on those goals, obtaining the financing necessary to achieve the

11

plans, and generally preserving all of the entity's financial resources (Doan,2022). Career

opportunities for this specific branch are chief financial officers (CFO) and financial

support staff who also have accounting qualifications. However, their job requires more

areas of knowledge, than other accounting disciplines, such as economics, statistics, and

mathematics. They often use more non-financial and qualitative data for financial goal

setting, planning, digital skills, problem-solving, and negotiation, where the high demand

is negotiation to find the source financing needed to achieve business objectives (

Luenendonk, 2021).

The next area of accounting is financial management, which is a highly specialized area

of accounting. It involves setting financial goals, creating strategies based on those goals,

obtaining the capital needed to execute the plans, and generally protecting all of your

financial resources. organization. Alternatively, it can mean planning, arranging, directing

and regulating financial activities such as the acquisition and use of corporate funds. It

requires the application of general management ideas to the financial resources of the

enterprise.Financial managers like chief financial officers (CFO), and financial supporting

staff are also qualified accountants but work needs a much wider range of knowledge

fields than other branches of accounting, such as economics, statistics, and mathematics.

They often use more non-financial and more qualitative data to set up financial objectives

and make plans. Besides, managing finances requires skills numerical skills, problem-

solving, and negotiation which negotiation is highly required to seek finance needed to

achieve the business objectives (Vu Thi Hoai Anh, 2021).

Accounting also has another significant branch of auditing. Auditing has traditionally

been the primary service offered by most public accounting practitioners. Auditing is the

examination and verification of the truthfulness of financial statements, thereby providing

the most accurate information about the financial position of an enterprise or organization.

There are two main types of auditors: external auditors and internal auditors. Auditing

skills are key skills required are integrity, customer service especially needed for external

auditors, and digital and problem-solving skills (Vu Thi Hoai Anh, 2021).

12

opportunities for this specific branch are chief financial officers (CFO) and financial

support staff who also have accounting qualifications. However, their job requires more

areas of knowledge, than other accounting disciplines, such as economics, statistics, and

mathematics. They often use more non-financial and qualitative data for financial goal

setting, planning, digital skills, problem-solving, and negotiation, where the high demand

is negotiation to find the source financing needed to achieve business objectives (

Luenendonk, 2021).

The next area of accounting is financial management, which is a highly specialized area

of accounting. It involves setting financial goals, creating strategies based on those goals,

obtaining the capital needed to execute the plans, and generally protecting all of your

financial resources. organization. Alternatively, it can mean planning, arranging, directing

and regulating financial activities such as the acquisition and use of corporate funds. It

requires the application of general management ideas to the financial resources of the

enterprise.Financial managers like chief financial officers (CFO), and financial supporting

staff are also qualified accountants but work needs a much wider range of knowledge

fields than other branches of accounting, such as economics, statistics, and mathematics.

They often use more non-financial and more qualitative data to set up financial objectives

and make plans. Besides, managing finances requires skills numerical skills, problem-

solving, and negotiation which negotiation is highly required to seek finance needed to

achieve the business objectives (Vu Thi Hoai Anh, 2021).

Accounting also has another significant branch of auditing. Auditing has traditionally

been the primary service offered by most public accounting practitioners. Auditing is the

examination and verification of the truthfulness of financial statements, thereby providing

the most accurate information about the financial position of an enterprise or organization.

There are two main types of auditors: external auditors and internal auditors. Auditing

skills are key skills required are integrity, customer service especially needed for external

auditors, and digital and problem-solving skills (Vu Thi Hoai Anh, 2021).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 42

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.