National Business Institute Trust Relations Assignment BSBCNV506A

VerifiedAdded on 2023/06/10

|15

|4619

|74

Homework Assignment

AI Summary

This assignment addresses key aspects of trust relations and account management, covering topics such as required documents, compliance procedures, and the roles of professional third parties. It explores the types of accounting systems used, compliance requirements for trust accounts, and the identification, storage, and retrieval of source documents. The assignment delves into error reporting and correction processes, including relevant sections of the Act. Furthermore, it defines trusts, their origins, and advantages, while outlining the powers and duties of a trustee, including potential reasons for declining the role. The assignment also differentiates between various types of trusts, explaining their characteristics and features of a fiduciary relationship, including the obligations of those in a fiduciary role, and the meaning of "inter vivos" trusts. The assignment is based on the requirements of the BSBCNV506A unit from the National Business Institute of Australia.

Trust Relations 1

Assignment

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trust relations 2

Question 1: What documents are required with ‘trust records’?

Answer 1: Trust records are known as those records which are related to the structure of the

trust, and it also include those records which are related to the transactions and business activities

occurred in the trust. There are number of documents which are required to be kept in the form

of trust records and these documents are:

Financial records such as trust accounts, trust transaction records, bank deposit book,

current and used cheque books, bank records, invoice and payment authorizations, etc.

Records related to the assets and any other property of the trust.

Records related to the trust execution such as deed of execution, and document in which

declaration is made by the owner that he or she holds the land on behalf of another

person.

Records related to the controlled money.

Records related to the title of the trust assets.

Question 2: What policy and procedures (p+p) are in place at your organisation to ensure trust

requirements are met, and meet, compliance requirements?

Answer 2: Following is the policy and procedure which is established in the organization for

ensuring compliance requirement:

Management of an organization must maintain the sound system of internal control for

the purpose of ensuring the compliance requirements.

Review must be conducted by the management of the internal control system, and this

review covers different topics such as financial, operational and compliance controls and

risk management.

Internal control system in the organization must consider certain situations of the

business into account.

Management must review on the continuous basis in context of implementation of the

internal control system and meeting its reporting obligations.

Question 1: What documents are required with ‘trust records’?

Answer 1: Trust records are known as those records which are related to the structure of the

trust, and it also include those records which are related to the transactions and business activities

occurred in the trust. There are number of documents which are required to be kept in the form

of trust records and these documents are:

Financial records such as trust accounts, trust transaction records, bank deposit book,

current and used cheque books, bank records, invoice and payment authorizations, etc.

Records related to the assets and any other property of the trust.

Records related to the trust execution such as deed of execution, and document in which

declaration is made by the owner that he or she holds the land on behalf of another

person.

Records related to the controlled money.

Records related to the title of the trust assets.

Question 2: What policy and procedures (p+p) are in place at your organisation to ensure trust

requirements are met, and meet, compliance requirements?

Answer 2: Following is the policy and procedure which is established in the organization for

ensuring compliance requirement:

Management of an organization must maintain the sound system of internal control for

the purpose of ensuring the compliance requirements.

Review must be conducted by the management of the internal control system, and this

review covers different topics such as financial, operational and compliance controls and

risk management.

Internal control system in the organization must consider certain situations of the

business into account.

Management must review on the continuous basis in context of implementation of the

internal control system and meeting its reporting obligations.

Trust relations 3

Risk based approach must be adopted by the organization for the purpose of establishing

the sound system of the internal control.

Internal control system must facilitates the effectiveness and efficiency of the operations

for the purpose of ensuring the internal and external reporting, and also taking help in the

compliance with all the laws and requirements.

Question 3: It is acceptable that you can’t be a qualified accountant, lawyer, conveyancer

financial planner etc. So what professional third parties do you use and refer to at your

organization? What is the process to action their recommendations and how is it

disbursed/communicated to the employees?

Answer 3: For the purpose of getting recommendations and relevant advice, trust can also

choose professional third parties and these third parties involve adviser or banker. It must be

noted that these third parties also own fiduciary duties towards the beneficiaries of the

organization. These third parties help the trust in conducting number of transactions and also

provide relevant recommendations in context of any issue faced by the trust in different areas.

However, law also creates remedies in case these third parties breach their duties towards the

beneficiaries.

Following is the process for implementing the recommendation given by third parties and the

manner in which this information is communicated to the employees:

Advice given by the third parties must be reviewed and management must check the

suitability of this advice in context of the availability of the resources.

Once review is completed, management develops the plan in context of this advice and

communicated the plan with the advice to the employees through E-mail, personal

meetings, letters, etc.

Question 4: What type of accounting system does the organization use and why was it chosen?

And what are the compliance requirements for trust accounts?

Answer 4: Organization can choose electronic accounting system, as this is the application

related to the online and internet technologies in context of the business accounting function.

Risk based approach must be adopted by the organization for the purpose of establishing

the sound system of the internal control.

Internal control system must facilitates the effectiveness and efficiency of the operations

for the purpose of ensuring the internal and external reporting, and also taking help in the

compliance with all the laws and requirements.

Question 3: It is acceptable that you can’t be a qualified accountant, lawyer, conveyancer

financial planner etc. So what professional third parties do you use and refer to at your

organization? What is the process to action their recommendations and how is it

disbursed/communicated to the employees?

Answer 3: For the purpose of getting recommendations and relevant advice, trust can also

choose professional third parties and these third parties involve adviser or banker. It must be

noted that these third parties also own fiduciary duties towards the beneficiaries of the

organization. These third parties help the trust in conducting number of transactions and also

provide relevant recommendations in context of any issue faced by the trust in different areas.

However, law also creates remedies in case these third parties breach their duties towards the

beneficiaries.

Following is the process for implementing the recommendation given by third parties and the

manner in which this information is communicated to the employees:

Advice given by the third parties must be reviewed and management must check the

suitability of this advice in context of the availability of the resources.

Once review is completed, management develops the plan in context of this advice and

communicated the plan with the advice to the employees through E-mail, personal

meetings, letters, etc.

Question 4: What type of accounting system does the organization use and why was it chosen?

And what are the compliance requirements for trust accounts?

Answer 4: Organization can choose electronic accounting system, as this is the application

related to the online and internet technologies in context of the business accounting function.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trust relations 4

Online accounting is considered as the electronic version of the lawful traditional accounting and

also the traceable accounting process.

This accounting system is chosen because of the comfort level of the employees with the

technology and also because of the large size of the organization. Following is the compliance

requirements of the trust accounts:

Documents related to the trust records must be produced for the purpose of giving

accurate record of practice in context of clients.

Transactions are considered as completed transaction only when proper authorization and

documentation is completed.

All the transaction and entries are recorded in proper manner in context of the trust

accounts.

Question 5: What are source documents and how are they identified, stored and retrieved?

Answer 5: This answer defines the meaning of the source document, and also defines the

manner in which these documents are identified, stored and retrieved. Source document is

considered as the document which is created and received by the business organization in day-to-

day business operations. Source documents are considered as the proof of the transaction. In

other words, it is the original record which includes the details to substantiate the transaction

entered in the accounting system. Following are some of the Source documents:

Bank statement,

Cheque books

Cash receipts

Bill sent or received

Deposit Books

Purchase Invoices

Employee Pay slips

Trial Balances

Cash receipt & payment books

Proof of sale

Proof of disposal of assets

Online accounting is considered as the electronic version of the lawful traditional accounting and

also the traceable accounting process.

This accounting system is chosen because of the comfort level of the employees with the

technology and also because of the large size of the organization. Following is the compliance

requirements of the trust accounts:

Documents related to the trust records must be produced for the purpose of giving

accurate record of practice in context of clients.

Transactions are considered as completed transaction only when proper authorization and

documentation is completed.

All the transaction and entries are recorded in proper manner in context of the trust

accounts.

Question 5: What are source documents and how are they identified, stored and retrieved?

Answer 5: This answer defines the meaning of the source document, and also defines the

manner in which these documents are identified, stored and retrieved. Source document is

considered as the document which is created and received by the business organization in day-to-

day business operations. Source documents are considered as the proof of the transaction. In

other words, it is the original record which includes the details to substantiate the transaction

entered in the accounting system. Following are some of the Source documents:

Bank statement,

Cheque books

Cash receipts

Bill sent or received

Deposit Books

Purchase Invoices

Employee Pay slips

Trial Balances

Cash receipt & payment books

Proof of sale

Proof of disposal of assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trust relations 5

All these source documents must be identified and recorded on clear basis in context with the

legislative requirements, policies, and procedures. These documents contain the basic elements

in context of the transaction occurred such as date, aim, amount, etc.

This document can be created either through the paper or electronic format, and it is the primary

article in the process of accounts.

Question 6: If there is an error at your organization, how is it reported and how is it corrected?

Who would you seek out if you needed help with a problem?

What are the two sections of the Act that provide for a trust account deficiency and irregularity,

and explain what is required when a deficiency occurs?

Answer 6: Organization can set the framework under its internal control system through which

errors in the organization can be reported, as this framework sets the communication system and

also the effective cross check of the transactions.

Section 78 of the Act provides the provisions related to the trust accounts deficiency and section

79 of the Act defines the provisions related to the trust account irregularities. In case any

deficiency occurred then:

Licensee whenever get aware about the deficiency in context of the trust accounts or trust

ledger accounts, then licensee is under obligation to provide written information of the

same to the director of the organization.

After receiving the information director is under obligation to take appropriate steps.

To,

Registered Government Auditor

Subject: conduct audit for the organization.

Sir,

All these source documents must be identified and recorded on clear basis in context with the

legislative requirements, policies, and procedures. These documents contain the basic elements

in context of the transaction occurred such as date, aim, amount, etc.

This document can be created either through the paper or electronic format, and it is the primary

article in the process of accounts.

Question 6: If there is an error at your organization, how is it reported and how is it corrected?

Who would you seek out if you needed help with a problem?

What are the two sections of the Act that provide for a trust account deficiency and irregularity,

and explain what is required when a deficiency occurs?

Answer 6: Organization can set the framework under its internal control system through which

errors in the organization can be reported, as this framework sets the communication system and

also the effective cross check of the transactions.

Section 78 of the Act provides the provisions related to the trust accounts deficiency and section

79 of the Act defines the provisions related to the trust account irregularities. In case any

deficiency occurred then:

Licensee whenever get aware about the deficiency in context of the trust accounts or trust

ledger accounts, then licensee is under obligation to provide written information of the

same to the director of the organization.

After receiving the information director is under obligation to take appropriate steps.

To,

Registered Government Auditor

Subject: conduct audit for the organization.

Sir,

Trust relations 6

This letter is writing for the purpose of making the proposal to Registered Government Auditor

for the purpose of conducting auditing of financial statements for the fiscal year ending **** in

our organization, and also for auditing the financial statement of some fiscal years. Please

provide your conformation within the period of 14 days from the date of letter.

I hope you accept this proposal and deliver your confirmation within stipulated period.

Thanking you

ABC

File Note:

Particulars date Matter To Confirmation

period

Auditing 13th

June

2018

Letter to

conduct

auditing

Registered

Governmen

t Auditor

14 days

Question 7: What is a trust, and why or when would I prefer to use one. How did they come

about and why?

Answer 7: Trust is considered as the fiduciary association between the parties in which one

party who is known as trustee holds the title related to the property for the advantage of the other

person who is known as beneficiary. Structure related to the trust is of such nature as it

distinguishes the legal ownership from the beneficial one.

It can be said that trust maintains the structure of formal nature in which beneficiaries hold the

responsibility of their property and assets in the hands of the trustee for the purpose of managing

such property such manner as it creates benefit for the beneficiaries.

Trust allows the asset to be handover to the trustee and such trustee also get the legal control of

the property. Trustee is under obligation to manage the assets for the benefit of any other person,

and this duty of the trustee is known as the fiduciary duty.

The main purpose of creating the trust is to provide protection to the assets of the trust, and to

manage them for creating advantage. This can be understood through example that is wills in

which assets are kept in trust till the time beneficiaries of the assets attain the majority.

This letter is writing for the purpose of making the proposal to Registered Government Auditor

for the purpose of conducting auditing of financial statements for the fiscal year ending **** in

our organization, and also for auditing the financial statement of some fiscal years. Please

provide your conformation within the period of 14 days from the date of letter.

I hope you accept this proposal and deliver your confirmation within stipulated period.

Thanking you

ABC

File Note:

Particulars date Matter To Confirmation

period

Auditing 13th

June

2018

Letter to

conduct

auditing

Registered

Governmen

t Auditor

14 days

Question 7: What is a trust, and why or when would I prefer to use one. How did they come

about and why?

Answer 7: Trust is considered as the fiduciary association between the parties in which one

party who is known as trustee holds the title related to the property for the advantage of the other

person who is known as beneficiary. Structure related to the trust is of such nature as it

distinguishes the legal ownership from the beneficial one.

It can be said that trust maintains the structure of formal nature in which beneficiaries hold the

responsibility of their property and assets in the hands of the trustee for the purpose of managing

such property such manner as it creates benefit for the beneficiaries.

Trust allows the asset to be handover to the trustee and such trustee also get the legal control of

the property. Trustee is under obligation to manage the assets for the benefit of any other person,

and this duty of the trustee is known as the fiduciary duty.

The main purpose of creating the trust is to provide protection to the assets of the trust, and to

manage them for creating advantage. This can be understood through example that is wills in

which assets are kept in trust till the time beneficiaries of the assets attain the majority.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trust relations 7

Question 8: What are the powers and duties of a trustee? Are there any reasons why wouldn’t

you agree to become a trustee?

Answer 8: Following are the duties of the trustee:

Trustee is under obligation to act in the best interest of the trust.

Trustee must not take any personal benefit from the property of the trust.

In case trustee breach his fiduciary duty then he or she is under obligation to ensure that

trust must be put in the same position as it is before in case no trust is created.

The biggest reason because of which, I would not like to become the trustee is the immense

liabilities of the trustee towards the beneficiaries.

Following are the powers of the trustee:

Trustee has power to reimburse those trust expenses which are incurred in the proper

exercise of the trust’s powers.

Power to invest- most but not jurisdictions limit trustees to "authorized trustee

investments"

Power of sale.

Power to mortgage

Power to Lease.

Power to issue receipts for payment made to the trust estate

Power to deposit trust documents for safe custody.

Power to call for an audit.

Power to employ the agents.

Question 9: List the types of trusts with a brief clarification of how they differ?

Answer 9: Trust is the commercial organization which is managed through the appointment of

trustee for the purpose of creating the benefits for the trustee. There are different types of trusts

and all trusts are stated below:

Question 8: What are the powers and duties of a trustee? Are there any reasons why wouldn’t

you agree to become a trustee?

Answer 8: Following are the duties of the trustee:

Trustee is under obligation to act in the best interest of the trust.

Trustee must not take any personal benefit from the property of the trust.

In case trustee breach his fiduciary duty then he or she is under obligation to ensure that

trust must be put in the same position as it is before in case no trust is created.

The biggest reason because of which, I would not like to become the trustee is the immense

liabilities of the trustee towards the beneficiaries.

Following are the powers of the trustee:

Trustee has power to reimburse those trust expenses which are incurred in the proper

exercise of the trust’s powers.

Power to invest- most but not jurisdictions limit trustees to "authorized trustee

investments"

Power of sale.

Power to mortgage

Power to Lease.

Power to issue receipts for payment made to the trust estate

Power to deposit trust documents for safe custody.

Power to call for an audit.

Power to employ the agents.

Question 9: List the types of trusts with a brief clarification of how they differ?

Answer 9: Trust is the commercial organization which is managed through the appointment of

trustee for the purpose of creating the benefits for the trustee. There are different types of trusts

and all trusts are stated below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trust relations 8

Express trust- in this document is executed by the owner in which owner made the declaration

that they hold the land on trust. In other words, it is the trust which created in the express terms,

and generally in writing. This type of trust is different from the one which is incidental by the

law from the conduct or dealings of the parties.

Implied trust- in this property is not transferred or conveyance, but in this two people enter into

relationship with each other impliedly. It is the trust which is inferred by the operation of the

law, and imposed by law by considering the intentions of the parties. There are two types of

implied trust that are constructive trust and resulting trust:

Resulting trust- This trust is creating by the operation of equity where land is conveyed

and transferred to the person in context of the equitable interest held by another.

Constructive trust-this trust arise when equity impose the trust without considering the

intentions of the parties for preventing the injustice.

Question 10: What is, and what are, the features of a fiduciary relationship? Who has a fiduciary

obligation?

Answer 10: Following are the three features of the fiduciary relationship:

The most important feature is that fiduciary accepts the obligation to act on behalf or in

the interest of another person in legal context.

There must be relationship of reliance.

Any relationship of disadvantage, vulnerability and unequal bargaining power in context

of one person cause dependency on another person.

Trustee, employees, professionals, and third party professionals own duty towards the

beneficiaries.

Question 11: Trusts are inter vivos. What does this mean? Include express and discretionary

trusts in your answer?

Answer 11: Trust created at the time when individual is alive is known as the inter vivos trust,

and those trusts which established after the individual death is known as the testamentary trusts.

Express trust- in this document is executed by the owner in which owner made the declaration

that they hold the land on trust. In other words, it is the trust which created in the express terms,

and generally in writing. This type of trust is different from the one which is incidental by the

law from the conduct or dealings of the parties.

Implied trust- in this property is not transferred or conveyance, but in this two people enter into

relationship with each other impliedly. It is the trust which is inferred by the operation of the

law, and imposed by law by considering the intentions of the parties. There are two types of

implied trust that are constructive trust and resulting trust:

Resulting trust- This trust is creating by the operation of equity where land is conveyed

and transferred to the person in context of the equitable interest held by another.

Constructive trust-this trust arise when equity impose the trust without considering the

intentions of the parties for preventing the injustice.

Question 10: What is, and what are, the features of a fiduciary relationship? Who has a fiduciary

obligation?

Answer 10: Following are the three features of the fiduciary relationship:

The most important feature is that fiduciary accepts the obligation to act on behalf or in

the interest of another person in legal context.

There must be relationship of reliance.

Any relationship of disadvantage, vulnerability and unequal bargaining power in context

of one person cause dependency on another person.

Trustee, employees, professionals, and third party professionals own duty towards the

beneficiaries.

Question 11: Trusts are inter vivos. What does this mean? Include express and discretionary

trusts in your answer?

Answer 11: Trust created at the time when individual is alive is known as the inter vivos trust,

and those trusts which established after the individual death is known as the testamentary trusts.

Trust relations 9

In context of the express trust, settlor is considered as the creator of the trust. In context of the

inter vivos gifting (occurred between the living people), settlor is considered as the donor of the

trust.

In case of discretionary trust, goodwill and assets of the trust are transferred to the trustee by the

will of the individual.

Question 12: Describe the winding up process of a trust?

Answer 12: Following are the three options through which trust can be wind up:

Trust assets can be distributed to the beneficiaries in kind or by distributing the cash if

authorized either in express manner or as per the terms of the instrument.

Obligations of the trust can be changed or release either through the trustee or the

beneficiaries, or by the Courts.

By making sale or disposing the property of the trust to any other entity.

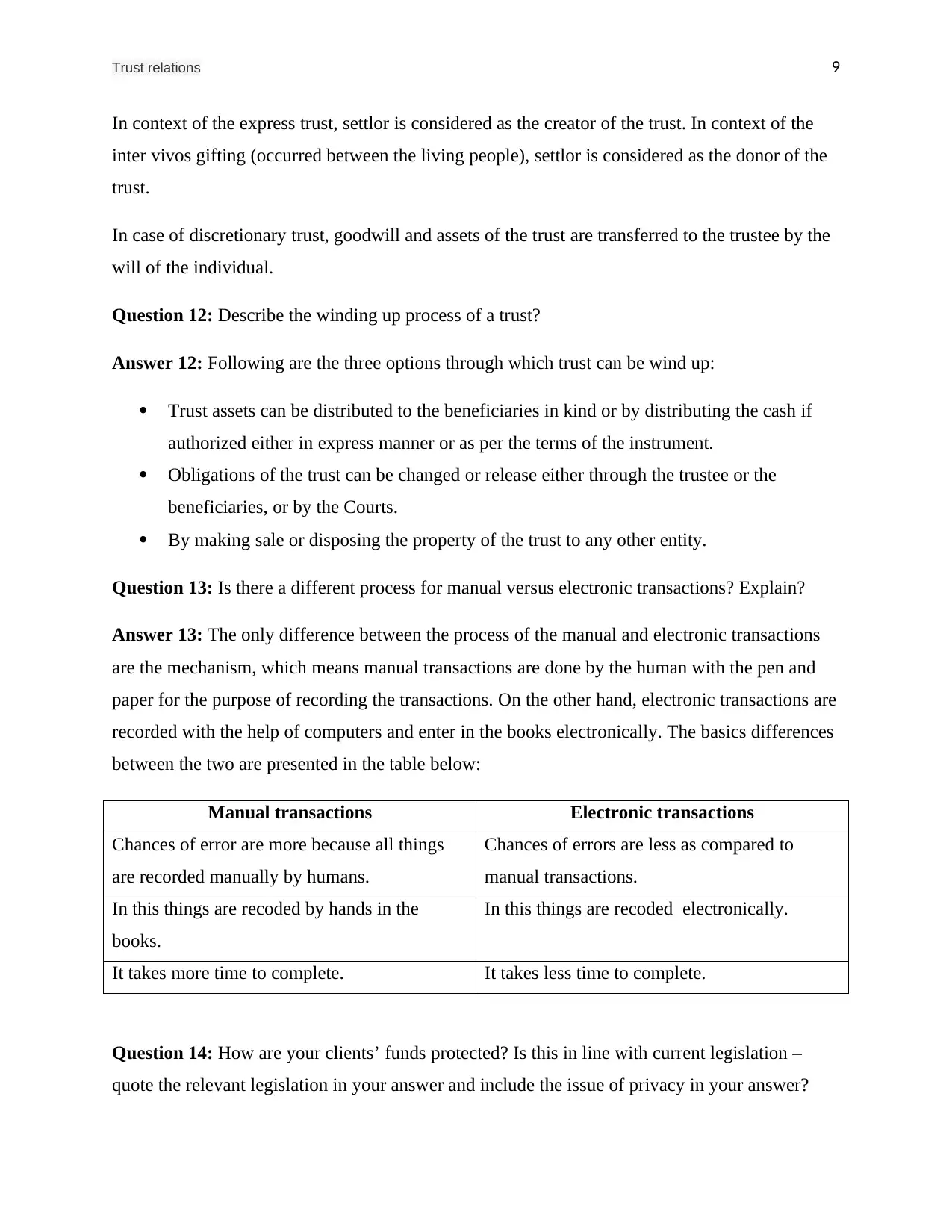

Question 13: Is there a different process for manual versus electronic transactions? Explain?

Answer 13: The only difference between the process of the manual and electronic transactions

are the mechanism, which means manual transactions are done by the human with the pen and

paper for the purpose of recording the transactions. On the other hand, electronic transactions are

recorded with the help of computers and enter in the books electronically. The basics differences

between the two are presented in the table below:

Manual transactions Electronic transactions

Chances of error are more because all things

are recorded manually by humans.

Chances of errors are less as compared to

manual transactions.

In this things are recoded by hands in the

books.

In this things are recoded electronically.

It takes more time to complete. It takes less time to complete.

Question 14: How are your clients’ funds protected? Is this in line with current legislation –

quote the relevant legislation in your answer and include the issue of privacy in your answer?

In context of the express trust, settlor is considered as the creator of the trust. In context of the

inter vivos gifting (occurred between the living people), settlor is considered as the donor of the

trust.

In case of discretionary trust, goodwill and assets of the trust are transferred to the trustee by the

will of the individual.

Question 12: Describe the winding up process of a trust?

Answer 12: Following are the three options through which trust can be wind up:

Trust assets can be distributed to the beneficiaries in kind or by distributing the cash if

authorized either in express manner or as per the terms of the instrument.

Obligations of the trust can be changed or release either through the trustee or the

beneficiaries, or by the Courts.

By making sale or disposing the property of the trust to any other entity.

Question 13: Is there a different process for manual versus electronic transactions? Explain?

Answer 13: The only difference between the process of the manual and electronic transactions

are the mechanism, which means manual transactions are done by the human with the pen and

paper for the purpose of recording the transactions. On the other hand, electronic transactions are

recorded with the help of computers and enter in the books electronically. The basics differences

between the two are presented in the table below:

Manual transactions Electronic transactions

Chances of error are more because all things

are recorded manually by humans.

Chances of errors are less as compared to

manual transactions.

In this things are recoded by hands in the

books.

In this things are recoded electronically.

It takes more time to complete. It takes less time to complete.

Question 14: How are your clients’ funds protected? Is this in line with current legislation –

quote the relevant legislation in your answer and include the issue of privacy in your answer?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trust relations 10

Answer 14: Section 308 of the Act impose statutory duty on the auditor for the purpose of

providing protection of the funds of the Client is considered as the statutory duty of the auditor,

and there are number of ways through which protections of these funds can be ensured:

Accurate audit and security arrangements must be ensured by the auditor for the purpose

of providing adequate protection to the client confidentiality and client funds held by the

trust.

Financial reports are must be prepared on the periodic basis and these reports must be

discussed with the clients for ensuring the accuracy.

Records in this context must be maintained and review of these records must be done on

continuous basis.

Question 15: How are funds disbursed and how are those disbursements authorized, checked for

accuracy and to prevent fraud? Refer to the relevant legislation in your answer?

Answer 15: Trustee has power to disburse the funds of the trust in manner they think

appropriate, but such disbursement must be fall in the authorized power of the trustee. All these

disbursements must be recorded in the books and receipts for the disbursements must be given

by the trustee, and in case trustee fail to provide proper receipt for the funds allocated or fails to

record the disbursed funds in the books then such disbursement is not considered as accurate

disbursement. All these steps are necessary for the purpose of preventing the fraud in the trust.

Question 16: Who reviews, and how is your p+p system reviewed for compliance and currency?

Answer 16: Board of the organization has different responsibilities in context of the P+P system

of the organization:

Process is defined by the organization for review conducted by the board.

Board is under obligation to receive and review the ongoing reports related to the internal

control of the system.

Particular exercise is carried out by the board on the annual basis for making the

statement in the annual report.

Answer 14: Section 308 of the Act impose statutory duty on the auditor for the purpose of

providing protection of the funds of the Client is considered as the statutory duty of the auditor,

and there are number of ways through which protections of these funds can be ensured:

Accurate audit and security arrangements must be ensured by the auditor for the purpose

of providing adequate protection to the client confidentiality and client funds held by the

trust.

Financial reports are must be prepared on the periodic basis and these reports must be

discussed with the clients for ensuring the accuracy.

Records in this context must be maintained and review of these records must be done on

continuous basis.

Question 15: How are funds disbursed and how are those disbursements authorized, checked for

accuracy and to prevent fraud? Refer to the relevant legislation in your answer?

Answer 15: Trustee has power to disburse the funds of the trust in manner they think

appropriate, but such disbursement must be fall in the authorized power of the trustee. All these

disbursements must be recorded in the books and receipts for the disbursements must be given

by the trustee, and in case trustee fail to provide proper receipt for the funds allocated or fails to

record the disbursed funds in the books then such disbursement is not considered as accurate

disbursement. All these steps are necessary for the purpose of preventing the fraud in the trust.

Question 16: Who reviews, and how is your p+p system reviewed for compliance and currency?

Answer 16: Board of the organization has different responsibilities in context of the P+P system

of the organization:

Process is defined by the organization for review conducted by the board.

Board is under obligation to receive and review the ongoing reports related to the internal

control of the system.

Particular exercise is carried out by the board on the annual basis for making the

statement in the annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trust relations 11

It must be noted that, organization’s internal control system and the corporate application of its

structure is mainly based on the corporate culture of the business. It must be noted that, internal

control system is not the checker for the system but it is the system itself.

Question 17: What is the auditing and financial reporting system in your organization? In your

answer explain the difference between internal and external auditing?

Answer 17: Auditing and financial reporting system is defined as the examination of the

organizations financial statements and this is also accompanied by the disclosures made by the

independent auditor, and reports are also prepared by the auditors in context of these

examinations. These reports are attested by the auditors in context fairness of presentation. The

main aim of this auditing is to add credibility to the reported financial position and performance.

The main difference between the external and internal audit is stated below:

Internal audit External audit

Internal auditors are the employees of the

company.

External auditors work outside for an audit

firm.

In this auditors are appointed by the

organization

In this auditors are appointed on the basis of

the shareholders vote.

Internal auditors does not have any CPA In case of external auditors, CPA is the main

driver of their activities.

In these auditors own duty towards the

management of the organization.

In this auditors won duty towards the

shareholders of the organization.

Less accurate reports. More accurate reporting.

Question 18: What CPD requirements are available for the staff, and in what areas of expertise

would you like them to be available for you?

Answer 18: It is necessary to incorporate the process of CPD in the organization for the purpose

of maintaining the ongoing training for all the members of the staff in context of different areas

such as trust accounts, financial and IT systems and implementation of plans. These

It must be noted that, organization’s internal control system and the corporate application of its

structure is mainly based on the corporate culture of the business. It must be noted that, internal

control system is not the checker for the system but it is the system itself.

Question 17: What is the auditing and financial reporting system in your organization? In your

answer explain the difference between internal and external auditing?

Answer 17: Auditing and financial reporting system is defined as the examination of the

organizations financial statements and this is also accompanied by the disclosures made by the

independent auditor, and reports are also prepared by the auditors in context of these

examinations. These reports are attested by the auditors in context fairness of presentation. The

main aim of this auditing is to add credibility to the reported financial position and performance.

The main difference between the external and internal audit is stated below:

Internal audit External audit

Internal auditors are the employees of the

company.

External auditors work outside for an audit

firm.

In this auditors are appointed by the

organization

In this auditors are appointed on the basis of

the shareholders vote.

Internal auditors does not have any CPA In case of external auditors, CPA is the main

driver of their activities.

In these auditors own duty towards the

management of the organization.

In this auditors won duty towards the

shareholders of the organization.

Less accurate reports. More accurate reporting.

Question 18: What CPD requirements are available for the staff, and in what areas of expertise

would you like them to be available for you?

Answer 18: It is necessary to incorporate the process of CPD in the organization for the purpose

of maintaining the ongoing training for all the members of the staff in context of different areas

such as trust accounts, financial and IT systems and implementation of plans. These

Trust relations 12

requirements can be in the form of formal or in the combination, and organization can choose

those form which provide best results to both employee and organization. Proper CPD help the

organization in ensuring the compliance of records and maintain all the records in context of

monitoring the trust accounts and transactions.

Question 19: Explain the five major elements, which make up a trust?

Answer 19: Following are the five major elements of the trust are:

Settlor is the person who in context of the express trust results in the emergence of the

trust relationship.

Trustee is another person in whom property of the trust is vested for the benefit of

another person.

Beneficiary is considered as that person who gets the benefit of the trust under the

fiduciary relationship.

It is necessary that particular trust property exist, or there is any interest in the particular

property.

Obligation of individual in context of trustee referred to the duty owned by the trustee

towards the beneficiary.

Question 20: After receiving trust money, what must you do?

Answer 20: If trustee receives the trust money, then trustee is under obligation to maintain the

general trust account in which such money is deposited, and any licensee who is under obligation

to maintain such trust account must maintain, and trustee must established this account as per the

law.

Transactions related to this account must be recorded by the trustee in the fair and proper

manner, and these transactions include receipt of cash, payments of cash, expenses occurred

from the trust account, etc. These transactions must be recorded in the fair manner for the

purpose of maintaining the fiduciary trust between the parties.

Later, trustee must notify about the account to the director within 14 days after creating the trust

account. Licensee also informs the director about the number of the account and the name and

address of the branch in which account is maintained by the trustee.

requirements can be in the form of formal or in the combination, and organization can choose

those form which provide best results to both employee and organization. Proper CPD help the

organization in ensuring the compliance of records and maintain all the records in context of

monitoring the trust accounts and transactions.

Question 19: Explain the five major elements, which make up a trust?

Answer 19: Following are the five major elements of the trust are:

Settlor is the person who in context of the express trust results in the emergence of the

trust relationship.

Trustee is another person in whom property of the trust is vested for the benefit of

another person.

Beneficiary is considered as that person who gets the benefit of the trust under the

fiduciary relationship.

It is necessary that particular trust property exist, or there is any interest in the particular

property.

Obligation of individual in context of trustee referred to the duty owned by the trustee

towards the beneficiary.

Question 20: After receiving trust money, what must you do?

Answer 20: If trustee receives the trust money, then trustee is under obligation to maintain the

general trust account in which such money is deposited, and any licensee who is under obligation

to maintain such trust account must maintain, and trustee must established this account as per the

law.

Transactions related to this account must be recorded by the trustee in the fair and proper

manner, and these transactions include receipt of cash, payments of cash, expenses occurred

from the trust account, etc. These transactions must be recorded in the fair manner for the

purpose of maintaining the fiduciary trust between the parties.

Later, trustee must notify about the account to the director within 14 days after creating the trust

account. Licensee also informs the director about the number of the account and the name and

address of the branch in which account is maintained by the trustee.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.