Minimizing Tax Liability: Estate Share Transfer Strategy for Client

VerifiedAdded on 2023/06/11

|3

|885

|167

Report

AI Summary

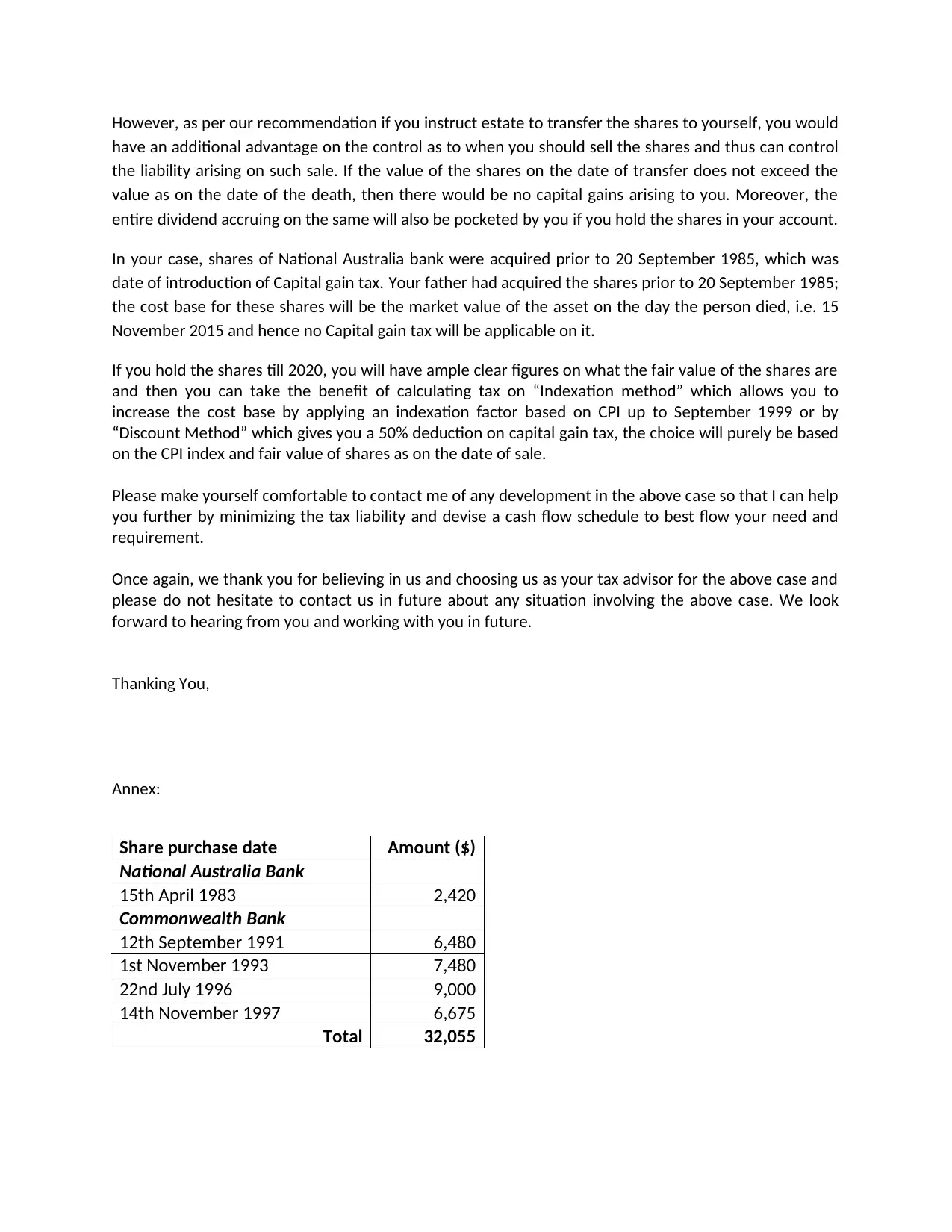

This management letter provides advice to George Spencer, the sole executor and beneficiary of the estate of Alexander Spencer, regarding the tax implications of handling the estate's shares. It recommends transferring the shares to George personally before selling them to potentially minimize tax liability. The letter details how the date of acquisition for tax purposes would be the date of Alexander's death, and how waiting until the estate is settled in 2020 could allow for a fairer assessment of market value and potential benefits from indexation or discount methods for capital gains tax. It also addresses the treatment of shares acquired before September 1985 and encourages George to seek further assistance for cash flow planning and tax minimization. The report includes an annex with details of share purchases.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.