Corporate Accounting and Financial Statement Analysis of Estia Health

VerifiedAdded on 2020/05/16

|19

|2949

|52

Report

AI Summary

This report provides a detailed financial analysis of Estia Health Ltd., focusing on its corporate accounting practices. The executive summary highlights the assessment of equity, tax expenses, and the treatment of income tax. The analysis includes an examination of the company's equity structure, including issued capital, shared-based payment reserves, and accumulated losses. The report also delves into the company's tax expenses, comparing current and deferred income tax expenses and analyzing the company's tax rate. Furthermore, it explores the deferred tax assets and liabilities, the current tax expense, and compares the income tax expense as per the income statement and cash flow statement. The report includes tables and figures illustrating key financial data and provides insights into the company's financial disclosure practices and compliance with tax laws.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial statement analysis can be specified as a procedure for assessing and reviewing

financial information of business comprised in Balance Sheet, Statement of Income, Statement of

change in equity and Cash flow statement. The present report provides a descriptive evaluation

of the financial statements of Estia Health Ltd. Core emphasis has been made on the accounting

treatment of equity and income tax expense during the current year. The present study shows that

treatment of income tax is a complex and detail procedure. Thus, appropriate income tax liability

can be ascertained only after assessing the overall provision of accounting relating to income tax.

Financial statement analysis can be specified as a procedure for assessing and reviewing

financial information of business comprised in Balance Sheet, Statement of Income, Statement of

change in equity and Cash flow statement. The present report provides a descriptive evaluation

of the financial statements of Estia Health Ltd. Core emphasis has been made on the accounting

treatment of equity and income tax expense during the current year. The present study shows that

treatment of income tax is a complex and detail procedure. Thus, appropriate income tax liability

can be ascertained only after assessing the overall provision of accounting relating to income tax.

TABLE OF CONTENTS

Introduction......................................................................................................................................5

Assessment of Equity......................................................................................................................5

Tax Expenses of the Organization...................................................................................................8

Company Tax Rate Times of Firm Accounting Income.................................................................9

Deferred Tax Asset or Liability.......................................................................................................9

Current Tax Expense.....................................................................................................................10

Income Tax Expense as Per Income Statement and As Per Cash Flow Statement.......................10

Analysis of Treatment of Tax Expense and New Insights Learned From Above Study...............12

Appendices....................................................................................................................................13

Income Statement......................................................................................................................13

Balance Sheet.............................................................................................................................14

Statement of Change in Equity..................................................................................................15

Consolidated statements of Cash Flows....................................................................................16

Introduction......................................................................................................................................5

Assessment of Equity......................................................................................................................5

Tax Expenses of the Organization...................................................................................................8

Company Tax Rate Times of Firm Accounting Income.................................................................9

Deferred Tax Asset or Liability.......................................................................................................9

Current Tax Expense.....................................................................................................................10

Income Tax Expense as Per Income Statement and As Per Cash Flow Statement.......................10

Analysis of Treatment of Tax Expense and New Insights Learned From Above Study...............12

Appendices....................................................................................................................................13

Income Statement......................................................................................................................13

Balance Sheet.............................................................................................................................14

Statement of Change in Equity..................................................................................................15

Consolidated statements of Cash Flows....................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LIST OF FIGURES

Figure 1: The shared Based payment reserve for the year 2017 and 2016......................................7

Figure 1: The shared Based payment reserve for the year 2017 and 2016......................................7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIST OF TABLES

Table 1: profit attributable to Equity shareholders..........................................................................7

Table 2: The equity structure of the Company in the current and the past year..............................7

Table 3: Tax expenses of Estia Health Limited...............................................................................9

Table 4: Income tax payable for two consecutive years................................................................11

Table 5: Statement of P&L............................................................................................................12

Table 6: Cash Flow Statement.......................................................................................................13

Table 1: profit attributable to Equity shareholders..........................................................................7

Table 2: The equity structure of the Company in the current and the past year..............................7

Table 3: Tax expenses of Estia Health Limited...............................................................................9

Table 4: Income tax payable for two consecutive years................................................................11

Table 5: Statement of P&L............................................................................................................12

Table 6: Cash Flow Statement.......................................................................................................13

Introduction

The present study is based on the financial analysis of Estia Health Limited. The report analysis

the taxation practices of the Company along with the statement of the equity of the Company.

Estia health is one of the leading providers of aged care services in Australia in the private

sector. The Company is committed to improving their operational performance expanding their

refurbishment plans for which continues to be a major source of earnings growth (Estia Health,

2017). The report highlights the composition of equity, deferred tax assets and liabilities; a

comparison has also been derived with the past figures. The study also depicts the taxation

practices with regards to the income tax payable, the taxation expenses and its compliance with

the Tax laws of the country. The income tax payables as per cash flow statement and as per the

income statement are compared for any variations and the underlying reason behind the same. A

conclusion is made regarding the financial disclosure of the company.

Assessment of Equity

After looking at the capital and funding structure of the Company that majorly comprises of

RADs, borrowings by equity, we can conclude that the Company is in a strong position

(Dagwell, Wines and Lambert, 2015). The capital management of the Group includes issued

capital and all other reserves of equity that is attributable to the parent company’s equity holders.

The primary objective of any company’s capital management is to maximise the shareholder

value. The total quoted equity securities of the Company as on year ending 2017 were

$260,150,443 (Estia Health, 2017). The total equity of the Company includes deferred payments

to senior executives which are given in the form of shares. The equity also delivers LTIP which

includes the interests of the executive which have led to increasing in shareholder’s wealth in the

long-term. The profit attributable to the equity shareholders for the year 2016 and 2017 are as

follows-

Table 1: profit attributable to Equity shareholders

(Source: Annual Report of Estia Health. 2017)

2017 2016

The present study is based on the financial analysis of Estia Health Limited. The report analysis

the taxation practices of the Company along with the statement of the equity of the Company.

Estia health is one of the leading providers of aged care services in Australia in the private

sector. The Company is committed to improving their operational performance expanding their

refurbishment plans for which continues to be a major source of earnings growth (Estia Health,

2017). The report highlights the composition of equity, deferred tax assets and liabilities; a

comparison has also been derived with the past figures. The study also depicts the taxation

practices with regards to the income tax payable, the taxation expenses and its compliance with

the Tax laws of the country. The income tax payables as per cash flow statement and as per the

income statement are compared for any variations and the underlying reason behind the same. A

conclusion is made regarding the financial disclosure of the company.

Assessment of Equity

After looking at the capital and funding structure of the Company that majorly comprises of

RADs, borrowings by equity, we can conclude that the Company is in a strong position

(Dagwell, Wines and Lambert, 2015). The capital management of the Group includes issued

capital and all other reserves of equity that is attributable to the parent company’s equity holders.

The primary objective of any company’s capital management is to maximise the shareholder

value. The total quoted equity securities of the Company as on year ending 2017 were

$260,150,443 (Estia Health, 2017). The total equity of the Company includes deferred payments

to senior executives which are given in the form of shares. The equity also delivers LTIP which

includes the interests of the executive which have led to increasing in shareholder’s wealth in the

long-term. The profit attributable to the equity shareholders for the year 2016 and 2017 are as

follows-

Table 1: profit attributable to Equity shareholders

(Source: Annual Report of Estia Health. 2017)

2017 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

$m $m

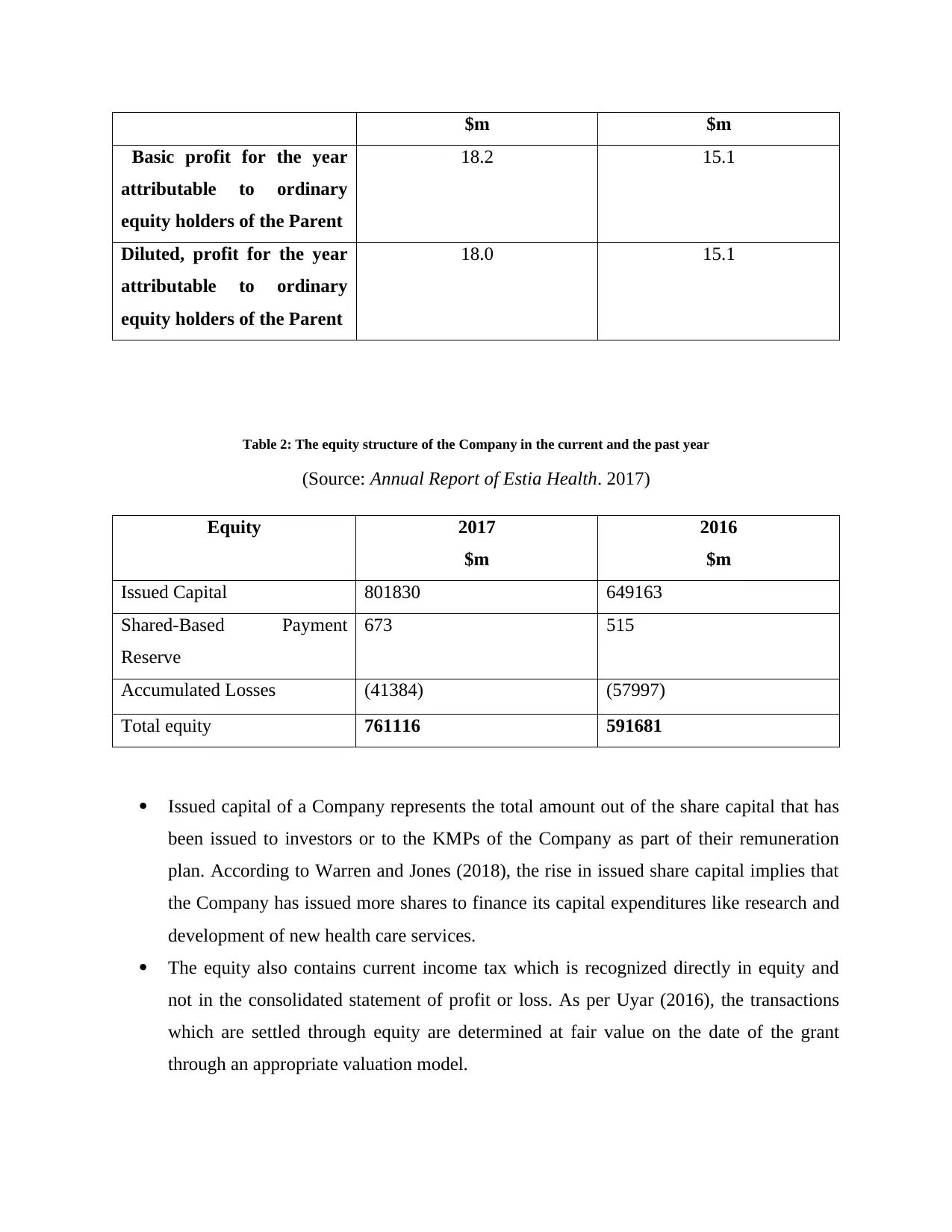

Basic profit for the year

attributable to ordinary

equity holders of the Parent

18.2 15.1

Diluted, profit for the year

attributable to ordinary

equity holders of the Parent

18.0 15.1

Table 2: The equity structure of the Company in the current and the past year

(Source: Annual Report of Estia Health. 2017)

Equity 2017

$m

2016

$m

Issued Capital 801830 649163

Shared-Based Payment

Reserve

673 515

Accumulated Losses (41384) (57997)

Total equity 761116 591681

Issued capital of a Company represents the total amount out of the share capital that has

been issued to investors or to the KMPs of the Company as part of their remuneration

plan. According to Warren and Jones (2018), the rise in issued share capital implies that

the Company has issued more shares to finance its capital expenditures like research and

development of new health care services.

The equity also contains current income tax which is recognized directly in equity and

not in the consolidated statement of profit or loss. As per Uyar (2016), the transactions

which are settled through equity are determined at fair value on the date of the grant

through an appropriate valuation model.

Basic profit for the year

attributable to ordinary

equity holders of the Parent

18.2 15.1

Diluted, profit for the year

attributable to ordinary

equity holders of the Parent

18.0 15.1

Table 2: The equity structure of the Company in the current and the past year

(Source: Annual Report of Estia Health. 2017)

Equity 2017

$m

2016

$m

Issued Capital 801830 649163

Shared-Based Payment

Reserve

673 515

Accumulated Losses (41384) (57997)

Total equity 761116 591681

Issued capital of a Company represents the total amount out of the share capital that has

been issued to investors or to the KMPs of the Company as part of their remuneration

plan. According to Warren and Jones (2018), the rise in issued share capital implies that

the Company has issued more shares to finance its capital expenditures like research and

development of new health care services.

The equity also contains current income tax which is recognized directly in equity and

not in the consolidated statement of profit or loss. As per Uyar (2016), the transactions

which are settled through equity are determined at fair value on the date of the grant

through an appropriate valuation model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to the words of Gitman, Juchau and Flanagan (2015), the cost of equity is

driven from the anticipated return which the investors of the Group expect from their

investment in the equity of the Company.

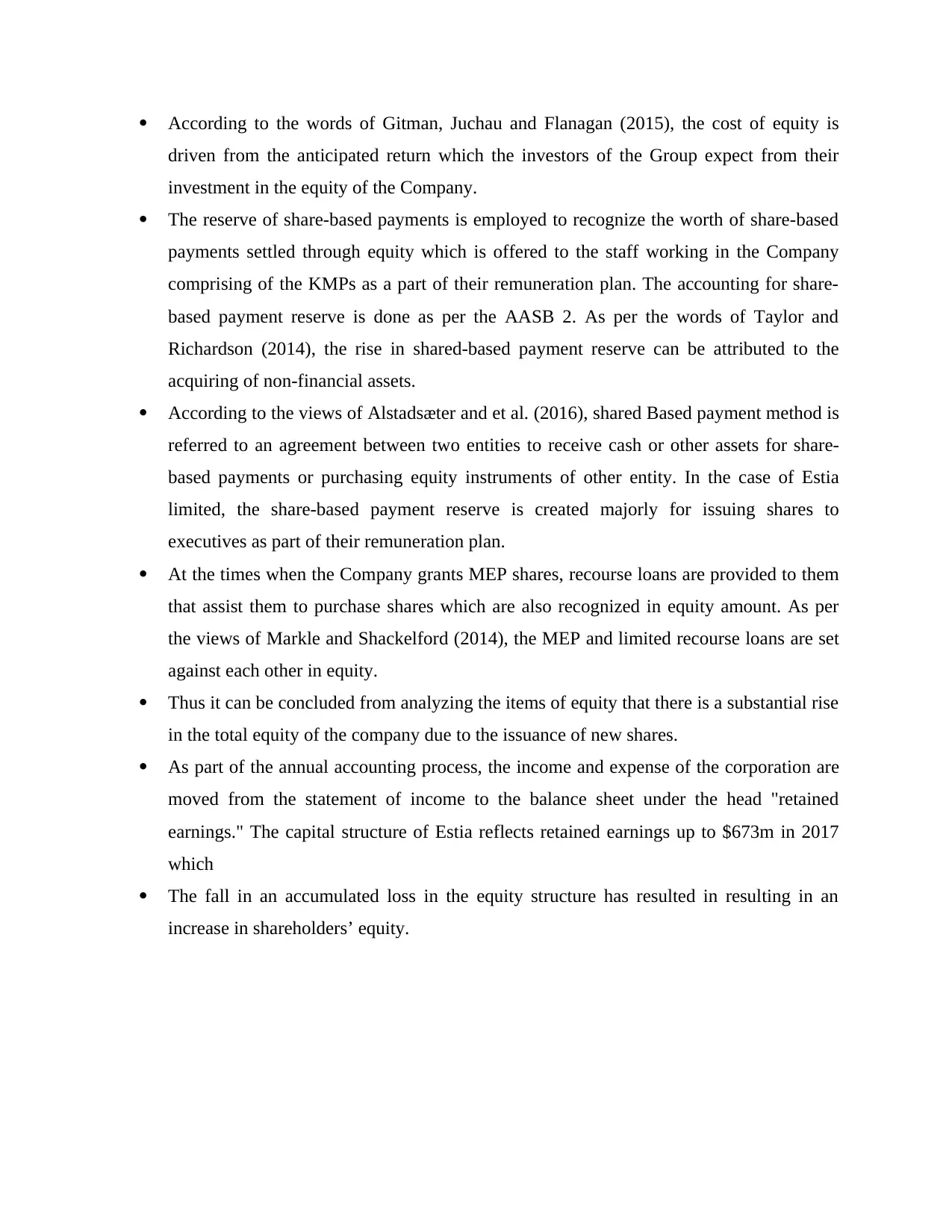

The reserve of share-based payments is employed to recognize the worth of share-based

payments settled through equity which is offered to the staff working in the Company

comprising of the KMPs as a part of their remuneration plan. The accounting for share-

based payment reserve is done as per the AASB 2. As per the words of Taylor and

Richardson (2014), the rise in shared-based payment reserve can be attributed to the

acquiring of non-financial assets.

According to the views of Alstadsæter and et al. (2016), shared Based payment method is

referred to an agreement between two entities to receive cash or other assets for share-

based payments or purchasing equity instruments of other entity. In the case of Estia

limited, the share-based payment reserve is created majorly for issuing shares to

executives as part of their remuneration plan.

At the times when the Company grants MEP shares, recourse loans are provided to them

that assist them to purchase shares which are also recognized in equity amount. As per

the views of Markle and Shackelford (2014), the MEP and limited recourse loans are set

against each other in equity.

Thus it can be concluded from analyzing the items of equity that there is a substantial rise

in the total equity of the company due to the issuance of new shares.

As part of the annual accounting process, the income and expense of the corporation are

moved from the statement of income to the balance sheet under the head "retained

earnings." The capital structure of Estia reflects retained earnings up to $673m in 2017

which

The fall in an accumulated loss in the equity structure has resulted in resulting in an

increase in shareholders’ equity.

driven from the anticipated return which the investors of the Group expect from their

investment in the equity of the Company.

The reserve of share-based payments is employed to recognize the worth of share-based

payments settled through equity which is offered to the staff working in the Company

comprising of the KMPs as a part of their remuneration plan. The accounting for share-

based payment reserve is done as per the AASB 2. As per the words of Taylor and

Richardson (2014), the rise in shared-based payment reserve can be attributed to the

acquiring of non-financial assets.

According to the views of Alstadsæter and et al. (2016), shared Based payment method is

referred to an agreement between two entities to receive cash or other assets for share-

based payments or purchasing equity instruments of other entity. In the case of Estia

limited, the share-based payment reserve is created majorly for issuing shares to

executives as part of their remuneration plan.

At the times when the Company grants MEP shares, recourse loans are provided to them

that assist them to purchase shares which are also recognized in equity amount. As per

the views of Markle and Shackelford (2014), the MEP and limited recourse loans are set

against each other in equity.

Thus it can be concluded from analyzing the items of equity that there is a substantial rise

in the total equity of the company due to the issuance of new shares.

As part of the annual accounting process, the income and expense of the corporation are

moved from the statement of income to the balance sheet under the head "retained

earnings." The capital structure of Estia reflects retained earnings up to $673m in 2017

which

The fall in an accumulated loss in the equity structure has resulted in resulting in an

increase in shareholders’ equity.

Figure 1: The shared Based payment reserve for the year 2017 and 2016.

(Source: Annual Report of Estia Health. 2017)

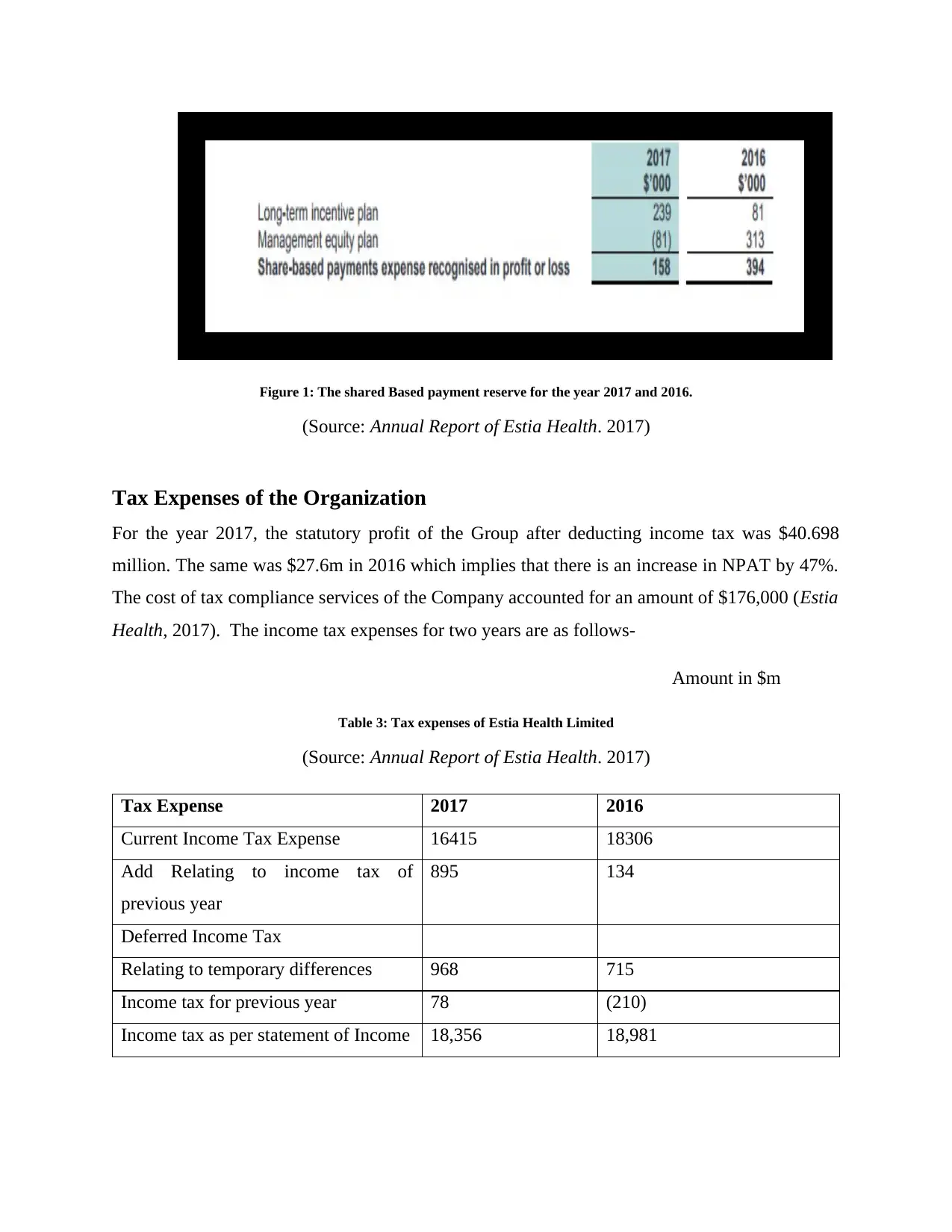

Tax Expenses of the Organization

For the year 2017, the statutory profit of the Group after deducting income tax was $40.698

million. The same was $27.6m in 2016 which implies that there is an increase in NPAT by 47%.

The cost of tax compliance services of the Company accounted for an amount of $176,000 (Estia

Health, 2017). The income tax expenses for two years are as follows-

Amount in $m

Table 3: Tax expenses of Estia Health Limited

(Source: Annual Report of Estia Health. 2017)

Tax Expense 2017 2016

Current Income Tax Expense 16415 18306

Add Relating to income tax of

previous year

895 134

Deferred Income Tax

Relating to temporary differences 968 715

Income tax for previous year 78 (210)

Income tax as per statement of Income 18,356 18,981

(Source: Annual Report of Estia Health. 2017)

Tax Expenses of the Organization

For the year 2017, the statutory profit of the Group after deducting income tax was $40.698

million. The same was $27.6m in 2016 which implies that there is an increase in NPAT by 47%.

The cost of tax compliance services of the Company accounted for an amount of $176,000 (Estia

Health, 2017). The income tax expenses for two years are as follows-

Amount in $m

Table 3: Tax expenses of Estia Health Limited

(Source: Annual Report of Estia Health. 2017)

Tax Expense 2017 2016

Current Income Tax Expense 16415 18306

Add Relating to income tax of

previous year

895 134

Deferred Income Tax

Relating to temporary differences 968 715

Income tax for previous year 78 (210)

Income tax as per statement of Income 18,356 18,981

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There has been fall in the tax expenses of the Company from past year. The company adjust

current tax asset against current tax liabilities only if same are legally enforceable. In case of

deferred tax asset or liability; the same is adjusted if the income tax is levied by one tax authority

in both the cases. In present year the company has made a retrospective change in accordance

with AASB 108 accounting policies relating to the accounting treatment of intangible assets, i.e.

treating them as having an indefinite useful life for the purpose of evaluation of deferred tax

(Estia Health, 2017). Prior to this company followed the policy of for calculating deferred tax on

temporary difference raised due to an indefinite life of intangible assets based on tax which

would result in future same. However, now the company evaluates deferred tax on the basis of

the fact that tax which will arise due to the consequence of the use of the intangible asset.

Company Tax Rate Times of Firm Accounting Income

The tax expense of Estia Health Ltd. is same as the company rate tax applicable to accounting

income. The reason behind same is that the total accountable income is taxable in the hands of

company only; that is income relating to present as well as the previous year. According to the

opinion of Larrimore, Burkhauser, and Armour (2015), the difference in rate occurs only if

taxation on the part of income is paid by other person or entity. However, in case of Estia Health

Ltd, the tax liability of total income is to be paid by itself only. The company has appropriately

applied provisions of AASB 112 Income Taxes in an appropriate manner. The tax rates and laws

that are used for calculating the amount are the ones that are enacted by the provisions of the

reporting date.

Deferred Tax Asset or Liability

The deferred tax liability of the Company for the year 2017 was $ 64,482, and the same was

$30,538 in 2016 (Estia Health, 2017). The Company provides the deferred tax by employing the

liability method which is based on the variation between the tax rates of assets and liabilities and

their carrying amount. As per the opinion of Dagwell Wines and Lambert, (2015), the liabilities

for deferred income tax are recognized on the basis of these differences except the following

cases-

current tax asset against current tax liabilities only if same are legally enforceable. In case of

deferred tax asset or liability; the same is adjusted if the income tax is levied by one tax authority

in both the cases. In present year the company has made a retrospective change in accordance

with AASB 108 accounting policies relating to the accounting treatment of intangible assets, i.e.

treating them as having an indefinite useful life for the purpose of evaluation of deferred tax

(Estia Health, 2017). Prior to this company followed the policy of for calculating deferred tax on

temporary difference raised due to an indefinite life of intangible assets based on tax which

would result in future same. However, now the company evaluates deferred tax on the basis of

the fact that tax which will arise due to the consequence of the use of the intangible asset.

Company Tax Rate Times of Firm Accounting Income

The tax expense of Estia Health Ltd. is same as the company rate tax applicable to accounting

income. The reason behind same is that the total accountable income is taxable in the hands of

company only; that is income relating to present as well as the previous year. According to the

opinion of Larrimore, Burkhauser, and Armour (2015), the difference in rate occurs only if

taxation on the part of income is paid by other person or entity. However, in case of Estia Health

Ltd, the tax liability of total income is to be paid by itself only. The company has appropriately

applied provisions of AASB 112 Income Taxes in an appropriate manner. The tax rates and laws

that are used for calculating the amount are the ones that are enacted by the provisions of the

reporting date.

Deferred Tax Asset or Liability

The deferred tax liability of the Company for the year 2017 was $ 64,482, and the same was

$30,538 in 2016 (Estia Health, 2017). The Company provides the deferred tax by employing the

liability method which is based on the variation between the tax rates of assets and liabilities and

their carrying amount. As per the opinion of Dagwell Wines and Lambert, (2015), the liabilities

for deferred income tax are recognized on the basis of these differences except the following

cases-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Asset or liability that does not account for any profit or loss at the time of the transaction

and is not a part of the business combination.

In cases of investment in the joint venture and subsidiaries and associates.

In cases where the reversal of temporary difference is controllable, and the Company is

certain that the reversal will not occur in new future.

In accordance with Warren and Jones (2018), the current assets related to deferring taxes are also

recognized at temporary differences and the unused tax credits are carrying forwarded along with

any losses in the same. The Deferred tax assets are recognized to the limit where it is possible

that the taxable profit will will be sufficient to set off against the temporary difference. The

deferred tax assets’ carrying amount is reviewed every year, and changes are reflected if

required. The deferred tax assets are measured at tax rates prevailing in the year in which the

asset or liability is settled.

Current Tax Expense

Table 4: Income tax payable for two consecutive years

(Source: Annual Report of Estia Health. 2017)

Amount in $m 2017 2016

28595 6662

The substantial rise in income tax of the Company can be traced to the changes in accounting

policy as per AASB 112 (Income Taxes). In the past years, the Group measured their deferred

taxes on the basis of temporary differences that arise from intangible assets’ indefinite life that is

based upon the tax resulting from the future sale. Thus an accounting policy has been adopted by

the Group that measures deferred taxes on the basis of temporary differences in the indefinite

useful life of intangible assets based upon the consequences of tax payable that arises through

their use. In accordance with the words of Uyar (2016), the assets and liabilities related to current

assets are valued at an amount which is expected to be recovered from the taxation authorities.

The current income tax is recognized directly in the equity and not in the P&L account. The

and is not a part of the business combination.

In cases of investment in the joint venture and subsidiaries and associates.

In cases where the reversal of temporary difference is controllable, and the Company is

certain that the reversal will not occur in new future.

In accordance with Warren and Jones (2018), the current assets related to deferring taxes are also

recognized at temporary differences and the unused tax credits are carrying forwarded along with

any losses in the same. The Deferred tax assets are recognized to the limit where it is possible

that the taxable profit will will be sufficient to set off against the temporary difference. The

deferred tax assets’ carrying amount is reviewed every year, and changes are reflected if

required. The deferred tax assets are measured at tax rates prevailing in the year in which the

asset or liability is settled.

Current Tax Expense

Table 4: Income tax payable for two consecutive years

(Source: Annual Report of Estia Health. 2017)

Amount in $m 2017 2016

28595 6662

The substantial rise in income tax of the Company can be traced to the changes in accounting

policy as per AASB 112 (Income Taxes). In the past years, the Group measured their deferred

taxes on the basis of temporary differences that arise from intangible assets’ indefinite life that is

based upon the tax resulting from the future sale. Thus an accounting policy has been adopted by

the Group that measures deferred taxes on the basis of temporary differences in the indefinite

useful life of intangible assets based upon the consequences of tax payable that arises through

their use. In accordance with the words of Uyar (2016), the assets and liabilities related to current

assets are valued at an amount which is expected to be recovered from the taxation authorities.

The current income tax is recognized directly in the equity and not in the P&L account. The

management regularly reviews the applicable tax regulations to ensure that the accounting is

done as per the norms.

Income Tax Expense as Per Income Statement and As Per Cash Flow

Statement

Income tax expense for the year 2017 as per statement of comprehensive statement is

$18356000, and as per cash flow statement, it is $28595000 (Estia Health, 2017). Thus, it can

be accessed that the amount in both the statement is different. In income statement the amount of

income tax payable for the current year is accounted; however, income tax paid for the current

year is accounted in cash flow statement. In accordance with the views of Gitman, Juchau and

Flanagan (2015), the liability of income tax is ascertained after giving the effect of current tax as

well as deferred tax asset or liability and amount which has been still unpaid and will be paid in

next year. The amount which is shown in cash flow statement represents the amount paid in

present year; whether it is related to present year or any other year.

Table 5: Statement of P&L

(Source: Annual Report of Estia Health. 2017)

done as per the norms.

Income Tax Expense as Per Income Statement and As Per Cash Flow

Statement

Income tax expense for the year 2017 as per statement of comprehensive statement is

$18356000, and as per cash flow statement, it is $28595000 (Estia Health, 2017). Thus, it can

be accessed that the amount in both the statement is different. In income statement the amount of

income tax payable for the current year is accounted; however, income tax paid for the current

year is accounted in cash flow statement. In accordance with the views of Gitman, Juchau and

Flanagan (2015), the liability of income tax is ascertained after giving the effect of current tax as

well as deferred tax asset or liability and amount which has been still unpaid and will be paid in

next year. The amount which is shown in cash flow statement represents the amount paid in

present year; whether it is related to present year or any other year.

Table 5: Statement of P&L

(Source: Annual Report of Estia Health. 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.