Ethical Accounting Report: Case Studies on Financial Ethics

VerifiedAdded on 2020/04/01

|10

|2008

|51

Report

AI Summary

This report delves into the realm of ethical accounting, examining a case study involving a manager's pressure on an accountant to manipulate revenue recognition for tax and bonus benefits. The report analyzes the ethical dilemmas that arise, focusing on the stakeholders involved, the motivations behind the unethical requests, and the potential consequences of such actions. It explores the accountant's ethical obligations and the impact of distorting financial statements. The report also includes general ledger entries, trial balances, and an analysis of breaches of ethical standards by professional organizations, referencing specific examples of disciplinary actions taken against members for non-compliance with ethical guidelines. The examples are analyzed in the context of the APES 110 standards and the appropriateness of the penalties imposed.

Running head: ETHICAL ACCOUNTING

Ethical Accounting

Student’s Name:

University Name:

Author Note:

Ethical Accounting

Student’s Name:

University Name:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ETHICAL ACCOUNTING

Table of Contents

Question 1..................................................................................................................................2

Answer to Part A:...................................................................................................................2

Answer to Part B:...................................................................................................................2

Answer to Part C:...................................................................................................................2

Answer to Part D:...................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Answer to Part 1:....................................................................................................................6

Answer to Part 2:....................................................................................................................7

Answer to Part 3:....................................................................................................................7

Referencing................................................................................................................................8

Table of Contents

Question 1..................................................................................................................................2

Answer to Part A:...................................................................................................................2

Answer to Part B:...................................................................................................................2

Answer to Part C:...................................................................................................................2

Answer to Part D:...................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Answer to Part 1:....................................................................................................................6

Answer to Part 2:....................................................................................................................7

Answer to Part 3:....................................................................................................................7

Referencing................................................................................................................................8

2ETHICAL ACCOUNTING

Question 1

Answer to Part A:

The stakeholders in this situation are, the manager of Vroom Ltd, Freda Chuse and the

accountant herself, Lucia and all the acting and present shareholders of the company.

Answer to Part B:

Freda asked Lucia to find ways of deferring recognition of as much revenue as

possible for the next financial year because Freda anticipated the fact that the total earned

revenue for the financial year ending 30 June, 2016 being $3.5 million would definitely be a

hindrance. This is because too much revenue if earned by the company then the government

would refrain from paying Vroom Ltd the grant for training apprentice mechanics and the

company would lose upon $100000 tax-free cash inflow (Zadek, Evans and Pruzan 2013).

The other reason for Freda to ask Lucia to do this is, as stated in the question, Freda’s bonus

will be maximized when the firm earns $3 million therefore she will not receive any kind of

benefit for revenue earned of $3.5 million. However according to the estimations of Freda the

next financial year will not observe such higher amounts of profit so it is in her best interests

to forward the excess of $3 million to the next financial year. This will not only maximize her

bonus earned but also help in maintaining the goodwill of the company by removing the

negativities that a poor financial statement may have (Tweedie et al., 2013).

Answer to Part C:

The ethical issues that may arise in this situation is that Lucia due to the unjustified

pressure from her manager succumbs to the pressure and commits the unethical task as

demanded by her manager, Freda. Another reason for Lucia to commit such a task is that she

does not want to risk her own opportunities for promotion by upsetting her manager. The

Question 1

Answer to Part A:

The stakeholders in this situation are, the manager of Vroom Ltd, Freda Chuse and the

accountant herself, Lucia and all the acting and present shareholders of the company.

Answer to Part B:

Freda asked Lucia to find ways of deferring recognition of as much revenue as

possible for the next financial year because Freda anticipated the fact that the total earned

revenue for the financial year ending 30 June, 2016 being $3.5 million would definitely be a

hindrance. This is because too much revenue if earned by the company then the government

would refrain from paying Vroom Ltd the grant for training apprentice mechanics and the

company would lose upon $100000 tax-free cash inflow (Zadek, Evans and Pruzan 2013).

The other reason for Freda to ask Lucia to do this is, as stated in the question, Freda’s bonus

will be maximized when the firm earns $3 million therefore she will not receive any kind of

benefit for revenue earned of $3.5 million. However according to the estimations of Freda the

next financial year will not observe such higher amounts of profit so it is in her best interests

to forward the excess of $3 million to the next financial year. This will not only maximize her

bonus earned but also help in maintaining the goodwill of the company by removing the

negativities that a poor financial statement may have (Tweedie et al., 2013).

Answer to Part C:

The ethical issues that may arise in this situation is that Lucia due to the unjustified

pressure from her manager succumbs to the pressure and commits the unethical task as

demanded by her manager, Freda. Another reason for Lucia to commit such a task is that she

does not want to risk her own opportunities for promotion by upsetting her manager. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ETHICAL ACCOUNTING

right way to react to the situation would be that if Lucia would have ensured all assets and

liabilities and other major components of an accounting statement are recorded in the

financial statements of the correct accounting period (Tweedie et al., 2013). It becomes

highly unreasonable and unethical, if Lucia in reality does realize other assets and liabilities

and other components of business that do not present a true and fair view of the financial

statements of that particular year that is it does not righteously reflect the organizational

performance and the position in terms of finance in the current period. Not to mention there

are a huge number of techniques which can be utilized by Lucia in order to manipulate the

amount of revenue earned, for instance, change in the procedure of calculating depreciation

or manipulation in the number of remaining utilizable life of assets. These activities of

manipulation in techniques may be generally accepted by all the accounting standards and

might even fall under legal provisions but the practice is not at all ethical. It also becomes

unacceptable on the part of the manager that she puts excess pressure on Lucia to execute

entries in the books of accounts against the wishes of Lucia as she recognizes the task to be

unethical (Liu, Yao and Hu, 2012).

Answer to Part D:

Lucia can defer all kinds of revenues and accrue as many expenses as possible by

adjusting journal entries but this may lead to distortion in the financial statements which may

in turn lead to improper reflection of the liquidity or financial position and financial

performance of the company. This is not only a legal offence but it also displays a wrong or

misleading image to the investors and shareholders. Lucia, if under pressure agrees to defer

revenue and accrue expenses to show the total revenue earned for a particular financial year

as less then it must be done on a short scale because passing adjusting entries in order to

cover up revenue if done on a large scale will lead to serious issues like presentation of

right way to react to the situation would be that if Lucia would have ensured all assets and

liabilities and other major components of an accounting statement are recorded in the

financial statements of the correct accounting period (Tweedie et al., 2013). It becomes

highly unreasonable and unethical, if Lucia in reality does realize other assets and liabilities

and other components of business that do not present a true and fair view of the financial

statements of that particular year that is it does not righteously reflect the organizational

performance and the position in terms of finance in the current period. Not to mention there

are a huge number of techniques which can be utilized by Lucia in order to manipulate the

amount of revenue earned, for instance, change in the procedure of calculating depreciation

or manipulation in the number of remaining utilizable life of assets. These activities of

manipulation in techniques may be generally accepted by all the accounting standards and

might even fall under legal provisions but the practice is not at all ethical. It also becomes

unacceptable on the part of the manager that she puts excess pressure on Lucia to execute

entries in the books of accounts against the wishes of Lucia as she recognizes the task to be

unethical (Liu, Yao and Hu, 2012).

Answer to Part D:

Lucia can defer all kinds of revenues and accrue as many expenses as possible by

adjusting journal entries but this may lead to distortion in the financial statements which may

in turn lead to improper reflection of the liquidity or financial position and financial

performance of the company. This is not only a legal offence but it also displays a wrong or

misleading image to the investors and shareholders. Lucia, if under pressure agrees to defer

revenue and accrue expenses to show the total revenue earned for a particular financial year

as less then it must be done on a short scale because passing adjusting entries in order to

cover up revenue if done on a large scale will lead to serious issues like presentation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ETHICAL ACCOUNTING

misstatements. Lastly adjustments done on a short scale or a large scale is obviously an

ethical issue and must not be done (Apostolou, Dull and Schleifer, 2013).

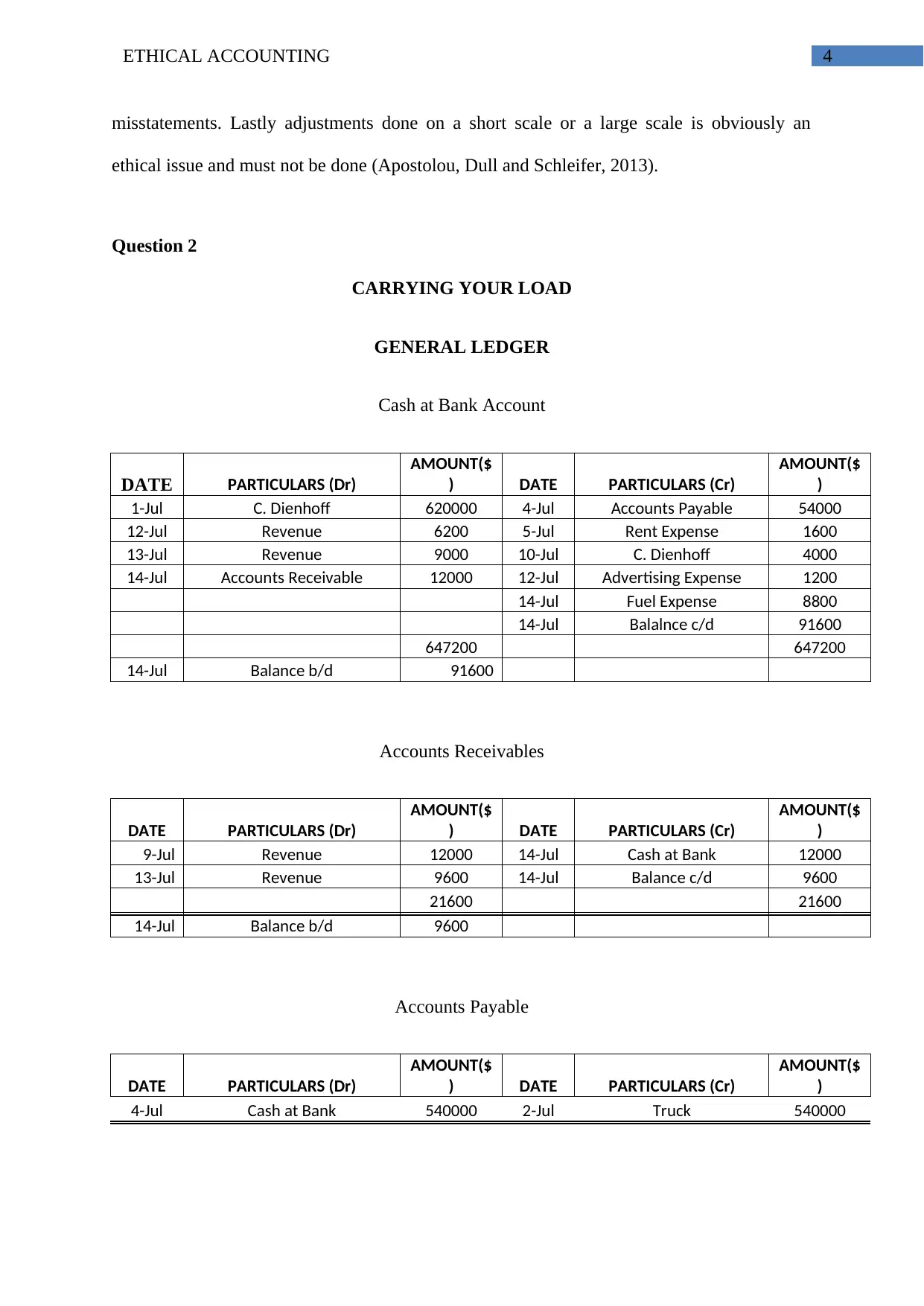

Question 2

CARRYING YOUR LOAD

GENERAL LEDGER

Cash at Bank Account

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

1-Jul C. Dienhoff 620000 4-Jul Accounts Payable 54000

12-Jul Revenue 6200 5-Jul Rent Expense 1600

13-Jul Revenue 9000 10-Jul C. Dienhoff 4000

14-Jul Accounts Receivable 12000 12-Jul Advertising Expense 1200

14-Jul Fuel Expense 8800

14-Jul Balalnce c/d 91600

647200 647200

14-Jul Balance b/d 91600

Accounts Receivables

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

9-Jul Revenue 12000 14-Jul Cash at Bank 12000

13-Jul Revenue 9600 14-Jul Balance c/d 9600

21600 21600

14-Jul Balance b/d 9600

Accounts Payable

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

4-Jul Cash at Bank 540000 2-Jul Truck 540000

misstatements. Lastly adjustments done on a short scale or a large scale is obviously an

ethical issue and must not be done (Apostolou, Dull and Schleifer, 2013).

Question 2

CARRYING YOUR LOAD

GENERAL LEDGER

Cash at Bank Account

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

1-Jul C. Dienhoff 620000 4-Jul Accounts Payable 54000

12-Jul Revenue 6200 5-Jul Rent Expense 1600

13-Jul Revenue 9000 10-Jul C. Dienhoff 4000

14-Jul Accounts Receivable 12000 12-Jul Advertising Expense 1200

14-Jul Fuel Expense 8800

14-Jul Balalnce c/d 91600

647200 647200

14-Jul Balance b/d 91600

Accounts Receivables

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

9-Jul Revenue 12000 14-Jul Cash at Bank 12000

13-Jul Revenue 9600 14-Jul Balance c/d 9600

21600 21600

14-Jul Balance b/d 9600

Accounts Payable

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

4-Jul Cash at Bank 540000 2-Jul Truck 540000

5ETHICAL ACCOUNTING

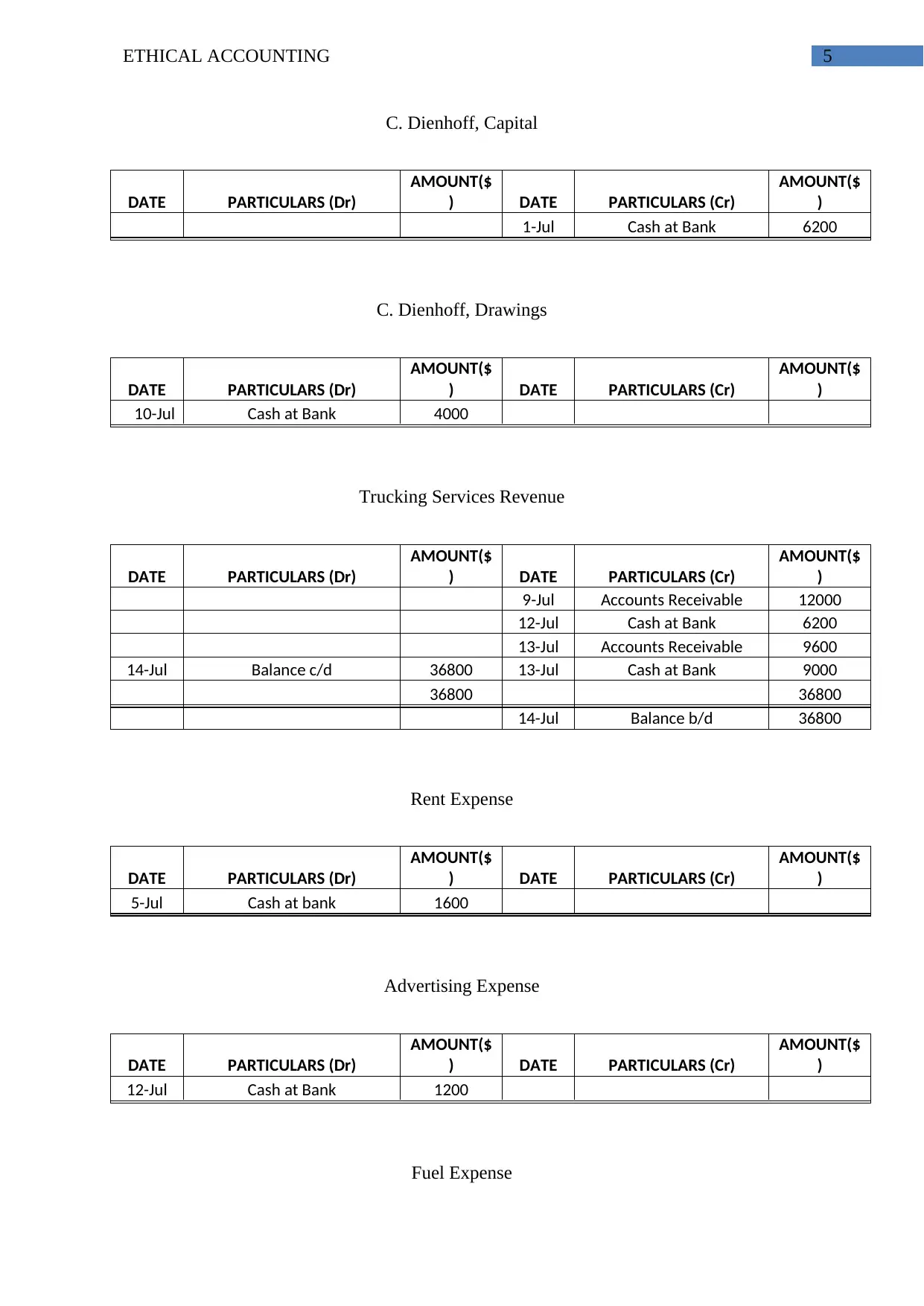

C. Dienhoff, Capital

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

1-Jul Cash at Bank 6200

C. Dienhoff, Drawings

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

10-Jul Cash at Bank 4000

Trucking Services Revenue

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

9-Jul Accounts Receivable 12000

12-Jul Cash at Bank 6200

13-Jul Accounts Receivable 9600

14-Jul Balance c/d 36800 13-Jul Cash at Bank 9000

36800 36800

14-Jul Balance b/d 36800

Rent Expense

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

5-Jul Cash at bank 1600

Advertising Expense

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

12-Jul Cash at Bank 1200

Fuel Expense

C. Dienhoff, Capital

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

1-Jul Cash at Bank 6200

C. Dienhoff, Drawings

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

10-Jul Cash at Bank 4000

Trucking Services Revenue

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

9-Jul Accounts Receivable 12000

12-Jul Cash at Bank 6200

13-Jul Accounts Receivable 9600

14-Jul Balance c/d 36800 13-Jul Cash at Bank 9000

36800 36800

14-Jul Balance b/d 36800

Rent Expense

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

5-Jul Cash at bank 1600

Advertising Expense

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

12-Jul Cash at Bank 1200

Fuel Expense

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ETHICAL ACCOUNTING

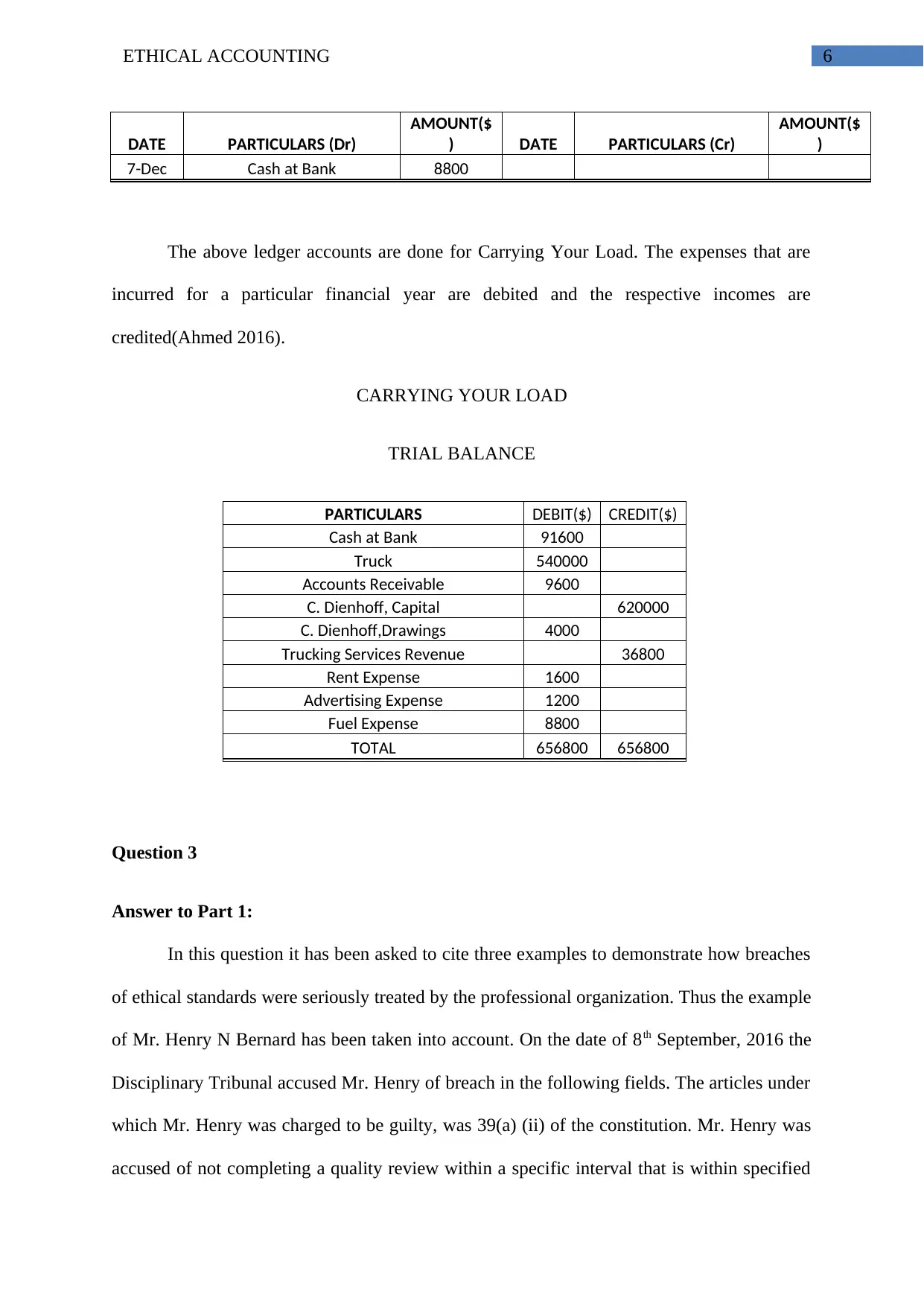

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

7-Dec Cash at Bank 8800

The above ledger accounts are done for Carrying Your Load. The expenses that are

incurred for a particular financial year are debited and the respective incomes are

credited(Ahmed 2016).

CARRYING YOUR LOAD

TRIAL BALANCE

PARTICULARS DEBIT($) CREDIT($)

Cash at Bank 91600

Truck 540000

Accounts Receivable 9600

C. Dienhoff, Capital 620000

C. Dienhoff,Drawings 4000

Trucking Services Revenue 36800

Rent Expense 1600

Advertising Expense 1200

Fuel Expense 8800

TOTAL 656800 656800

Question 3

Answer to Part 1:

In this question it has been asked to cite three examples to demonstrate how breaches

of ethical standards were seriously treated by the professional organization. Thus the example

of Mr. Henry N Bernard has been taken into account. On the date of 8th September, 2016 the

Disciplinary Tribunal accused Mr. Henry of breach in the following fields. The articles under

which Mr. Henry was charged to be guilty, was 39(a) (ii) of the constitution. Mr. Henry was

accused of not completing a quality review within a specific interval that is within specified

DATE PARTICULARS (Dr)

AMOUNT($

) DATE PARTICULARS (Cr)

AMOUNT($

)

7-Dec Cash at Bank 8800

The above ledger accounts are done for Carrying Your Load. The expenses that are

incurred for a particular financial year are debited and the respective incomes are

credited(Ahmed 2016).

CARRYING YOUR LOAD

TRIAL BALANCE

PARTICULARS DEBIT($) CREDIT($)

Cash at Bank 91600

Truck 540000

Accounts Receivable 9600

C. Dienhoff, Capital 620000

C. Dienhoff,Drawings 4000

Trucking Services Revenue 36800

Rent Expense 1600

Advertising Expense 1200

Fuel Expense 8800

TOTAL 656800 656800

Question 3

Answer to Part 1:

In this question it has been asked to cite three examples to demonstrate how breaches

of ethical standards were seriously treated by the professional organization. Thus the example

of Mr. Henry N Bernard has been taken into account. On the date of 8th September, 2016 the

Disciplinary Tribunal accused Mr. Henry of breach in the following fields. The articles under

which Mr. Henry was charged to be guilty, was 39(a) (ii) of the constitution. Mr. Henry was

accused of not completing a quality review within a specific interval that is within specified

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ETHICAL ACCOUNTING

quality time frames. Mr. Henry was also accused of the breach of not implementing a risk

management framework for his firm. Thus the penalties were imposed.

The next example is of Ms Tracey Redman-Slater who was found to breach under

Article 39(a)(ii)A of the Constitution on the date of 9th August, 2016. The breach committed

by Ms Tracey was that she had failed to provide requested information to the professional

code of conduct in reaction to a complaint lodged, within the span of ten days. She was also

charged guilty of depreciative attitude towards CPA Australia which was conducted in no

best interest of the institution.In clearer terms she had failed to keep her promise to complete

a client’s work within a period of eighteen months, hence the penalties were imposed

(Hansen, V.J. and White, 2012).

The third example is of Harvey Goodman who was accused of breach on the date of

5th April, 2016. The breach that Harvey Goodman was accused of was that he did fail to

finish a check up on review of quality despite the fact of being selected on August 2013. He

was also found guilty of depreciating or demeaning attitude towards CPA Australia which

was in no best interest of the institution. After repeated warnings and a fixed up date for the

review of quality on November 2014, Harvey Goodman failed to keep his promise, thus was

charged guilty. He was also not able to provide a written explanation to the professional code

of conduct body for the reasons of his failure. Thus the penalties were imposed (Hansen, V.J.

and White, 2012).

Answer to Part 2:

All the three examples cited in the above study fall under the sub section of 100.21 of

the APES 110 standards because it is clearly mentioned in this section that if a member is

unable to perform his or her responsibility then it falls under this section (Carey, Monroe and

Shailer, 2014).

quality time frames. Mr. Henry was also accused of the breach of not implementing a risk

management framework for his firm. Thus the penalties were imposed.

The next example is of Ms Tracey Redman-Slater who was found to breach under

Article 39(a)(ii)A of the Constitution on the date of 9th August, 2016. The breach committed

by Ms Tracey was that she had failed to provide requested information to the professional

code of conduct in reaction to a complaint lodged, within the span of ten days. She was also

charged guilty of depreciative attitude towards CPA Australia which was conducted in no

best interest of the institution.In clearer terms she had failed to keep her promise to complete

a client’s work within a period of eighteen months, hence the penalties were imposed

(Hansen, V.J. and White, 2012).

The third example is of Harvey Goodman who was accused of breach on the date of

5th April, 2016. The breach that Harvey Goodman was accused of was that he did fail to

finish a check up on review of quality despite the fact of being selected on August 2013. He

was also found guilty of depreciating or demeaning attitude towards CPA Australia which

was in no best interest of the institution. After repeated warnings and a fixed up date for the

review of quality on November 2014, Harvey Goodman failed to keep his promise, thus was

charged guilty. He was also not able to provide a written explanation to the professional code

of conduct body for the reasons of his failure. Thus the penalties were imposed (Hansen, V.J.

and White, 2012).

Answer to Part 2:

All the three examples cited in the above study fall under the sub section of 100.21 of

the APES 110 standards because it is clearly mentioned in this section that if a member is

unable to perform his or her responsibility then it falls under this section (Carey, Monroe and

Shailer, 2014).

8ETHICAL ACCOUNTING

Answer to Part 3:

The penalties imposed and the fines levied on the individuals for the breach

committed by them is perfectly fine and apt. The decision taken by the disciplinary tribunal is

completely just and requires no other alterations or adjustments. Therefore in both the three

cases the penalties imposed by the accounting bodies are sufficient and need not be changed.

Answer to Part 3:

The penalties imposed and the fines levied on the individuals for the breach

committed by them is perfectly fine and apt. The decision taken by the disciplinary tribunal is

completely just and requires no other alterations or adjustments. Therefore in both the three

cases the penalties imposed by the accounting bodies are sufficient and need not be changed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ETHICAL ACCOUNTING

Referencing

Ahmed, R., 2016. Trial Balance Report. In Cloud Computing Using Oracle Application

Express (pp. 171-181). Apress.

Apostolou, B., Dull, R.B. and Schleifer, L.L., 2013. A framework for the pedagogy of

accounting ethics. Accounting Education, 22(1), pp.1-17.

Carey, P.J., Monroe, G.S. and Shailer, G., 2014. Review of Post‐CLERP 9 Australian

Auditor Independence Research. Australian Accounting Review, 24(4), pp.370-380.

Hansen, V.J. and White, R.A., 2012. An investigation of the impact of preparer penalty

provisions on tax preparer aggressiveness. Journal of the American Taxation Association,

34(1), pp.137-165.

Liu, C., Yao, L.J. and Hu, N., 2012. Improving ethics education in accounting: Lessons from

medicine and law. Issues in Accounting Education, 27(3), pp.671-690.

Tweedie, D., Dyball, M.C., Hazelton, J. and Wright, S., 2013. Teaching global ethical

standards: a case and strategy for broadening the accounting ethics curriculum. Journal of

Business ethics, 115(1), pp.1-15.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging

practice in social and ethical accounting and auditing. Routledge.

Referencing

Ahmed, R., 2016. Trial Balance Report. In Cloud Computing Using Oracle Application

Express (pp. 171-181). Apress.

Apostolou, B., Dull, R.B. and Schleifer, L.L., 2013. A framework for the pedagogy of

accounting ethics. Accounting Education, 22(1), pp.1-17.

Carey, P.J., Monroe, G.S. and Shailer, G., 2014. Review of Post‐CLERP 9 Australian

Auditor Independence Research. Australian Accounting Review, 24(4), pp.370-380.

Hansen, V.J. and White, R.A., 2012. An investigation of the impact of preparer penalty

provisions on tax preparer aggressiveness. Journal of the American Taxation Association,

34(1), pp.137-165.

Liu, C., Yao, L.J. and Hu, N., 2012. Improving ethics education in accounting: Lessons from

medicine and law. Issues in Accounting Education, 27(3), pp.671-690.

Tweedie, D., Dyball, M.C., Hazelton, J. and Wright, S., 2013. Teaching global ethical

standards: a case and strategy for broadening the accounting ethics curriculum. Journal of

Business ethics, 115(1), pp.1-15.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging

practice in social and ethical accounting and auditing. Routledge.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.