Ethical Principles: A PowerPoint Presentation for ACC30010 Auditors

VerifiedAdded on 2023/06/08

|9

|487

|89

Presentation

AI Summary

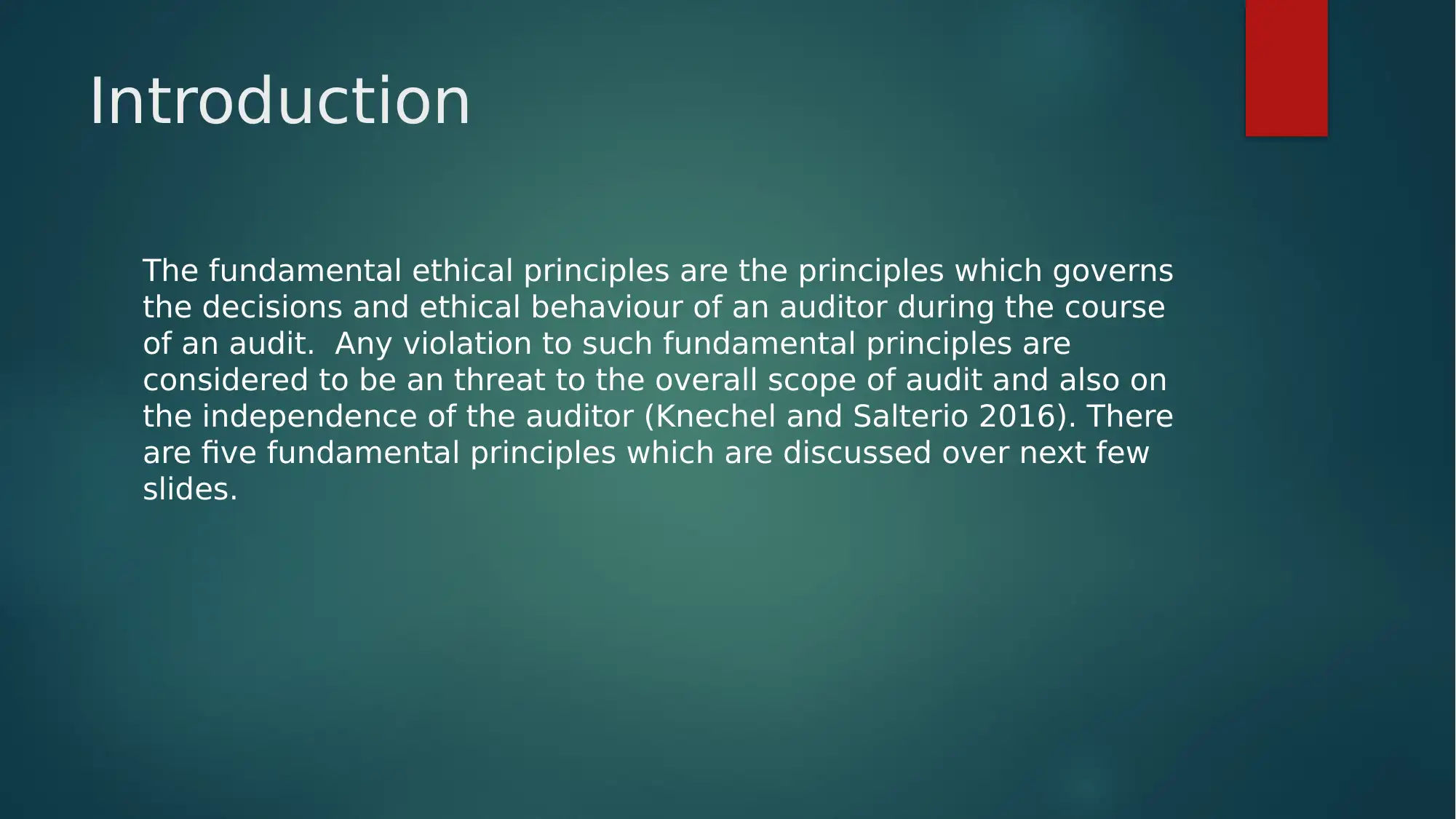

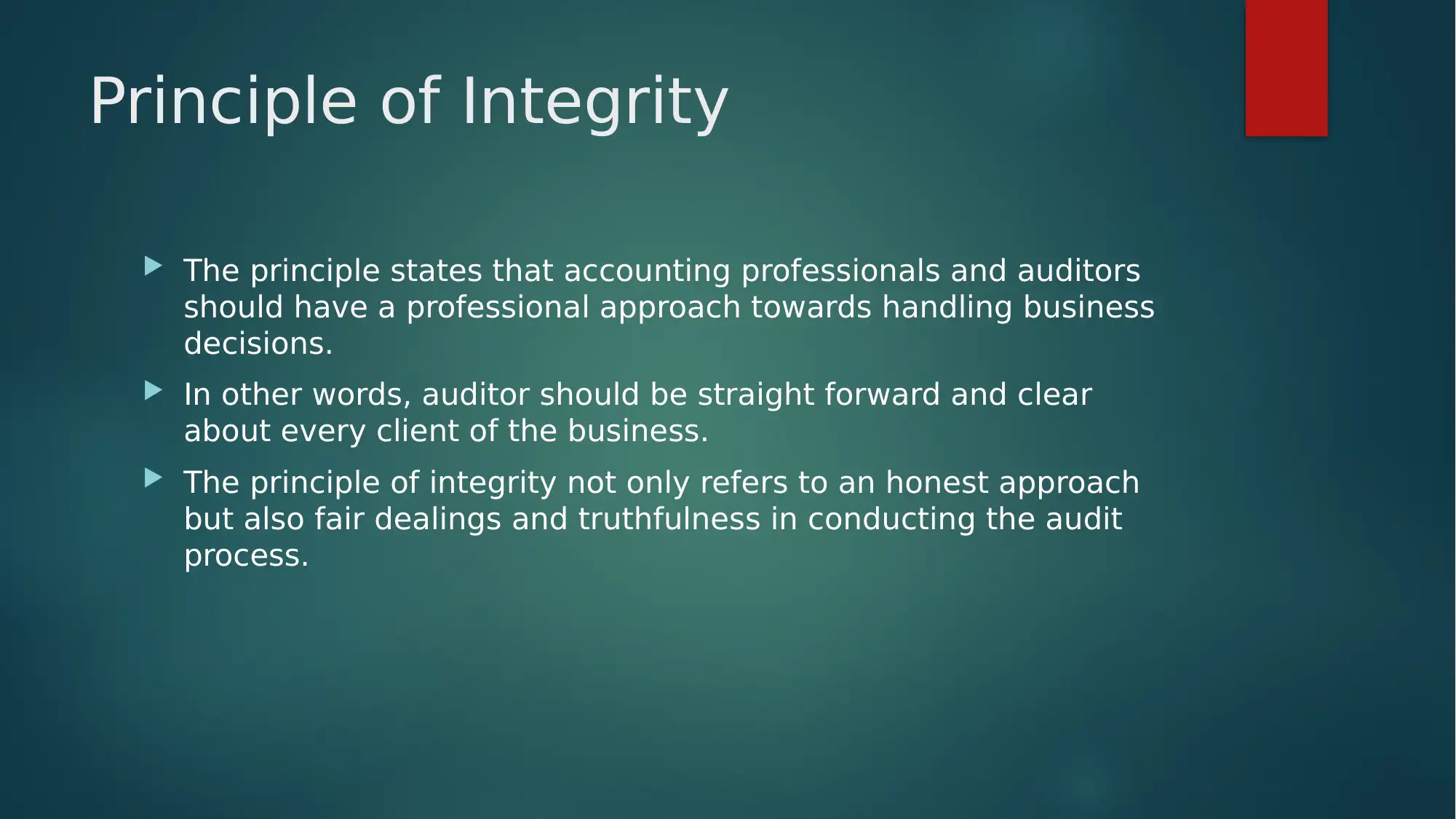

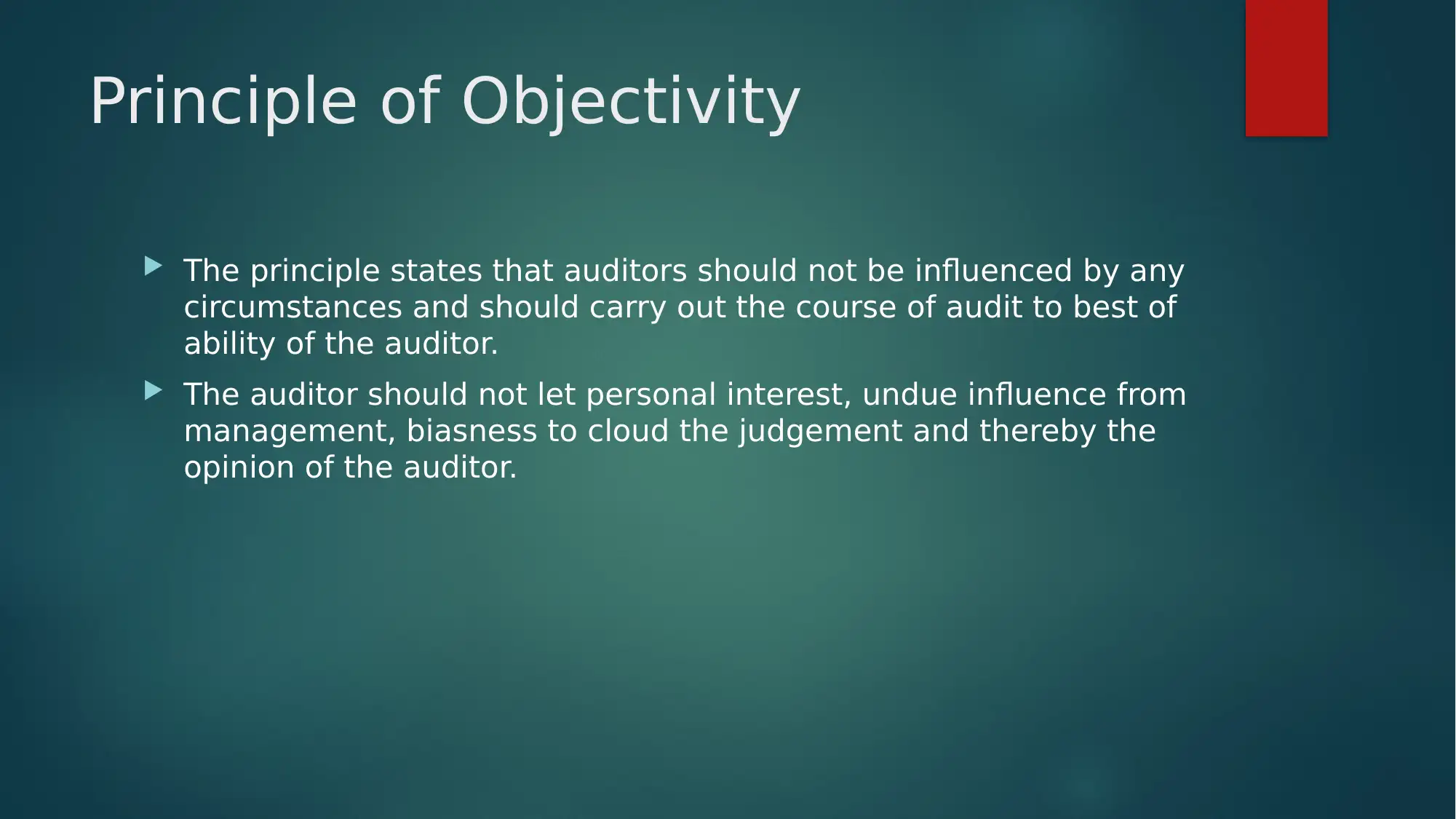

This PowerPoint presentation, created for ACC30010 Auditing, explores the fundamental ethical principles that govern the conduct of auditors. It delves into five key principles: integrity, objectivity, professional competence and due care, confidentiality, and professional behavior. The presentation defines each principle and explains its importance in maintaining the credibility and independence of the auditing process. The principle of integrity emphasizes honesty and fairness, while objectivity requires auditors to avoid bias. Professional competence highlights the need for qualified auditors with up-to-date knowledge. Confidentiality protects client information, and professional behavior ensures adherence to regulations and ethical standards. The presentation includes references to academic sources that support the discussion of these principles.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.